Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

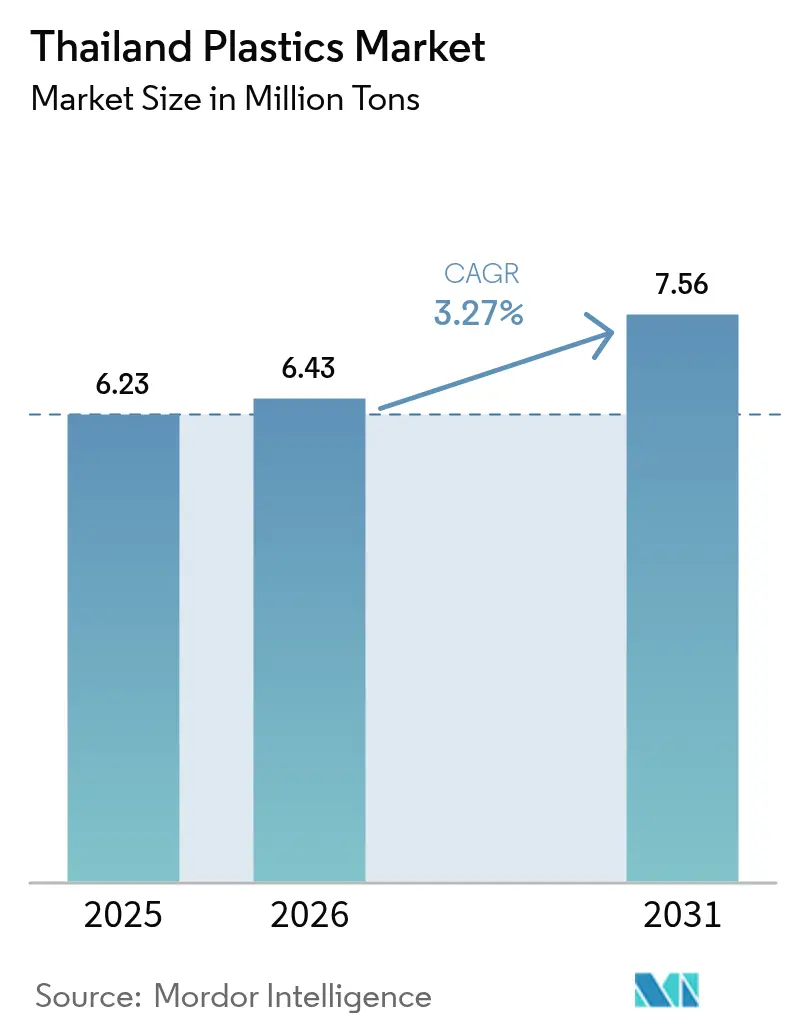

| Base Year Market Size (2025) | 6.23 Million tons |

| Market Volume (2026) | 6.43 Million tons |

| Market Volume (2031) | 7.56 Million tons |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

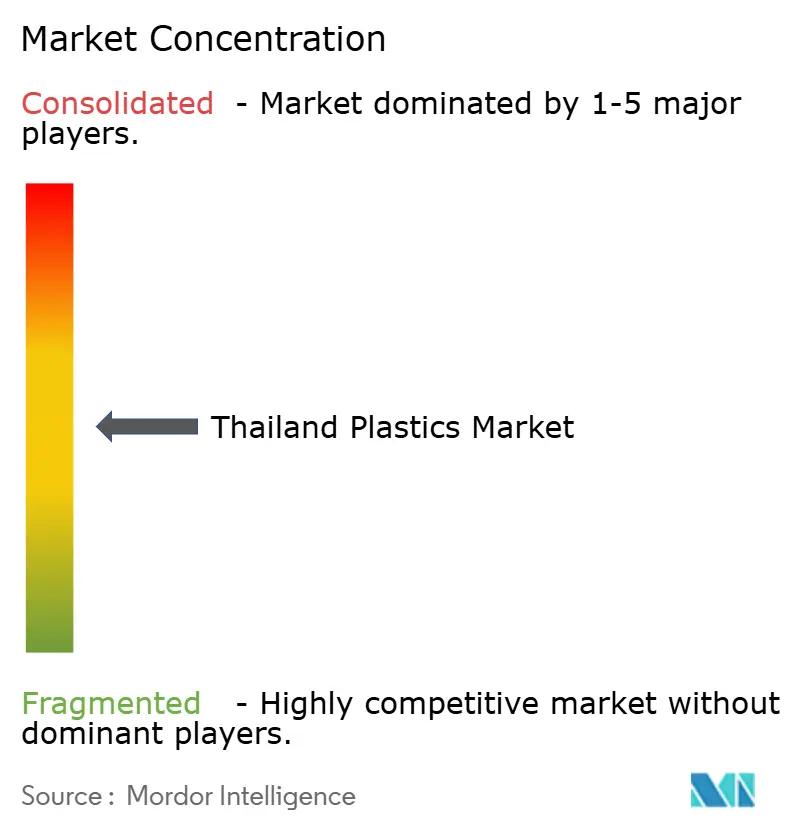

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Plastics Market Analysis by Mordor Intelligence

Thailand Plastics Market size in 2026 is estimated at 6.43 million tons, growing from 2025 value of 6.23 million tons with 2031 projections showing 7.56 million tons, growing at 3.27% CAGR over 2026-2031. This moderate headline growth conceals a decisive shift toward low-carbon feedstocks, circular economy practices, and specialty applications that lift margins even as commodity spreads tighten. Traditional resins dominate volumes, yet a rapid pivot to biopolymers is underway because joint ventures are unlocking bio-ethylene and PLA capacity at scale. Demand momentum remains strongest in food, beverage, and e-commerce packaging, but the emergence of an electric-vehicle supply chain and large-scale infrastructure projects creates fresh pull for engineering resins and high-performance compounds. Intensifying Chinese oversupply, volatile naphtha costs, and stricter waste regulations pressure margins; firms that diversify feedstocks and invest in recycling infrastructure are best placed to protect returns in the Thailand plastics market.

Key Report Takeaways

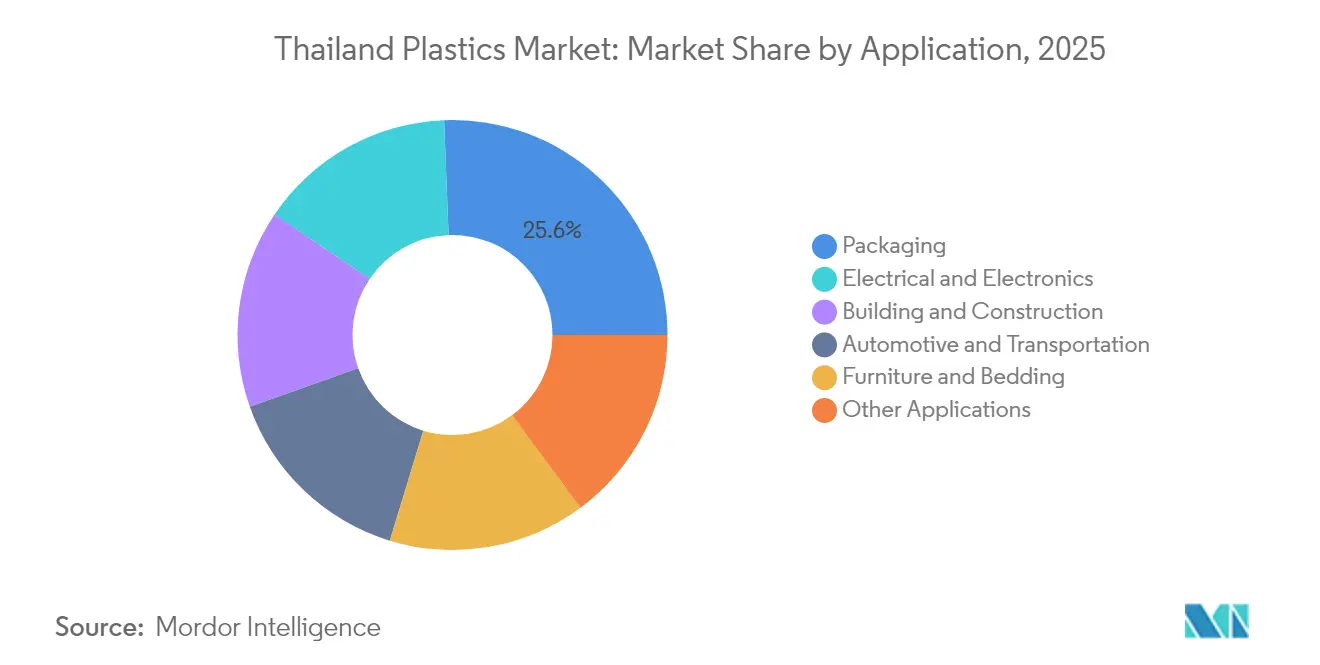

- By type, traditional plastics led with 70.55% of Thailand plastics market share in 2025; bioplastics is projected to expand at a 5.53% CAGR through 2031.

- By application, packaging captured 25.62% of the Thailand plastics market size in 2025 while automotive and transportation is advancing at a 3.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Plastics Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from food and beverage packaging | +1.2% | National, with concentration in Bangkok and Eastern Economic Corridor | Medium term (2-4 years) |

| Increasing plastics use in building and construction | +0.8% | National, driven by infrastructure megaprojects | Long term (≥ 4 years) |

| Lightweighting needs in automotive and EV components | +0.9% | Eastern Economic Corridor, Rayong province | Medium term (2-4 years) |

| Rapid e-commerce growth boosting protective packaging | +0.6% | Urban centers, Bangkok metropolitan area | Short term (≤ 2 years) |

| Bio-based polymer joint ventures | +0.4% | Map Ta Phut industrial complex, Rayong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Food and Beverage Packaging

Domestic beverage consumption continues to expand, locking in steady packaging tonnage. New food-contact standards effective March 2025 encourage converters to adopt recyclable and heat-resistant formulations that command premium pricing. Beverage exports to neighboring Cambodia and Vietnam add incremental volumes, and food-delivery growth has more than doubled since the pandemic, generating multiple plastic items per order. Rising temperatures, rapid urbanization, and a tourism rebound sustain packaging intensity in the Thailand plastics market. Demand for rigid containers grows in parallel with the personal-care segment, where mid-single-digit sales growth of cosmetics and health products boosts specialized packaging uptake.

Increasing Plastics Use in Building and Construction

Government spending across over 150 infrastructure projects underwrites long-run demand for PVC pipes, insulation, and roofing sheets. The Plastic Roads initiative, which incorporates up to five tons of recycled material per kilometer, signals a policy pivot toward circular construction practices that enlarge the addressable market for recycled resin. More than 800 mid- and large-size manufacturers now integrate digital ordering tools and low-carbon processes to satisfy green-building specifications. An expected 1 million new jobs linked to megaprojects will spur residential and commercial builds, reinforcing demand for plastic building products even as energy inflation and cheap Chinese imports squeeze margins.

Lightweighting Needs in Automotive and EV Components

Thailand’s 30@30 policy targets 30% electric-vehicle production by 2030. EV sales climbed from 84,500 units in 2022 to 206,000 units in 2024, creating outsized demand for lightweight battery casings, interior trims, and structural composites. Projects such as BYD’s USD 900 million Rayong plant and BMW’s forthcoming local assembly lines will rely on engineering resins that provide heat resistance and electrical insulation. Localization mandates that set domestic-content thresholds through 2035 further anchor those supply chains inside the Thailand plastics market. As automakers press suppliers to cut vehicle mass and extend range, polypropylene and advanced polyamides gain share in dashboards, under-hood applications, and EV charging components.

Bio-Based Polymer Joint Ventures

The USD 1.54 billion Braskem-SCGC bio-ethylene venture will deliver 200,000 tons a year of renewable polyethylene derived from sugarcane ethanol, cutting cradle-to-gate emissions by as much as 70% versus fossil resin[1]SCG Chemicals, “Discover the trends and initiatives set to revolutionize plastic recycling in 2025 with SCGC,” scgchemicals.com . NatureWorks is adding 75,000 tons of PLA at its Nakhon Sawan complex, backed by USD 350 million in domestic financing[2]NatureWorks LLC, “NatureWorks’ Ingeo PLA Manufacturing Expansion Attracts Record Financing,” natureworksllc.com. These projects position Thailand as a regional leader in sustainable resins, expand feedstock optionality for converters, and open export windows into premium consumer-goods markets that mandate lower-carbon packaging. The initiatives align with the national Bio-Circular-Green economic model, deepen farmer participation in the plastics value chain, and support the upward revision of renewable-material targets within the Thailand plastics market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter single-use-plastic bans and taxes | -0.7% | National, with enforcement focus on urban areas | Short term (≤ 2 years) |

| Crude-oil/naphtha price volatility | -0.9% | National, affecting all petrochemical producers | Medium term (2-4 years) |

| PP and PE oversupply and low-cost imports from China | -1.1% | National, with particular impact on commodity plastics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Single-Use-Plastic Bans and Taxes

Thailand’s plastic-waste roadmap phases out imports from January 2025 and tightens quality rules for food-contact articles. Urban centers such as Bangkok generate 1,800 metric tons of single-use waste daily, prompting authorities to fast-track levies and labeling mandates that raise compliance costs for converters. Additional legislation under the Draft Industrial Waste Management Act introduces a dedicated fund to remediate environmental impacts and imposes stricter disposal rules on hazardous scrap. Producers in the Thailand plastics market must invest in certified recyclable or compostable alternatives and enhance traceability systems or face penalties. These rules initially restrict disposable items but ultimately catalyze demand for higher-value sustainable resins.

Polypropylene and Polyethylene Oversupply and Low-Cost Imports from China

China is bringing nearly 5 million tons of additional polyethylene capacity online each year, pushing surplus volumes into Southeast Asia at discounted prices. Spot HDPE film assessments have slipped to multi-year lows, and regional crackers periodically cut rates below economic thresholds. Domestic production indices for packaging and finished goods deteriorated in early 2025, and converters postponed offtake amid margin squeeze. Although Thai exports to the United States temporarily rose because of tariff-driven stock-building, overall throughput in the Thailand plastics market faces cyclical contraction when import pressure peaks. Integrated producers are accelerating recycle and specialty upgrades to defend utilization and value capture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Adaptation of Legacy Resins Alongside Renewable Momentum

Traditional resins retained 70.55% of Thailand's plastics market share in 2025 thanks to entrenched infrastructure, scale economics, and diversified end-use exposure. Among them, polyethylene and polypropylene anchor packaging, automotive, and construction demand, while PET has grown beyond bottles into technical yarns and tire fabrics. HMC Polymers surpassed THB 25 billion in sales in 2023, illustrating the continuing commercial relevance of commodity grades. Engineering resins such as polyamides and polycarbonates post mid-single-digit demand gains tied to electronics assembly and EV power-train applications.

Biopolymers are the fastest-expanding category, progressing at a 5.53% CAGR and lifted by the 200,000-ton bio-ethylene venture and the 75,000-ton PLA expansion. Mainstream producers now trial chemical-recycling routes and circular naphtha streams to future-proof their asset bases and preserve relevance under new food-contact rules. The competitive gap narrows as conventional suppliers license bio-based processes, while newcomers differentiate through carbon-footprint declarations and compostability certifications.

By Application: Packaging Scale Leads as Mobility Drives Incremental Value

Packaging commanded 25.62% of the Thailand plastics market size in 2025 and is still expanding in line with rising food, beverage, personal-care, and e-commerce volumes. SCGP grew recycling revenue 80% in 2023 as brand owners demanded closed-loop solutions. Converters adopt microwave-safe PP and mono-material laminates to meet new food-contact rules, and smart-label innovations bring additional resin demand for near-field-communication tags embedded in caps and pouches.

Automotive and transportation applications exhibit the highest growth trajectory at 3.56% CAGR through 2031. The country’s pivot to EV assembly amplifies demand for engineering plastics that reduce weight and meet stringent thermal requirements. BYD, BMW, and more than a dozen other automakers have announced localized plants, giving compounders visibility on long-run volumes and justifying investments in advanced mixing lines. Downstream, charging-infrastructure rollouts require weatherable PC housings and flame-retardant PA connectors, further deepening the opportunity pool for the Thailand plastics market.

Geography Analysis

Roughly 80% of upstream and intermediate output feeds domestic conversion, reinforcing a self-sufficient ecosystem that underpins the Thailand plastics market. Bangkok’s metropolitan region is the biggest consumption hub; online retail, tourism, and foodservice platforms collectively generate elevated per-capita plastic use.

The Eastern Economic Corridor clusters assets in Rayong, Chonburi, and Chachoengsao, including mega-investments in bio-ethylene, EV assembly, and gas-to-olefins projects. Co-location reduces logistics costs and anchors high-value downstream processing, enabling rapid commercialization of new resins. Map Ta Phut hosts both fossil and renewable feedstock complexes, giving converters immediate access to diverse polymer grades and recycled pellets.

Regional exports remain a strategic outlet. Thailand leverages ASEAN trade frameworks to supply packaging resin to Cambodia and Vietnam, while tariff arbitrage under the US-China trade dispute unlocked a 61.7% jump in shipments to the United States early in 2025. Yet oversupply from China and shifting polypropylene trade balances require proactive portfolio management and customer diversification to safeguard utilization.

Competitive Landscape

The market demonstrates moderate fragmentation. PTT Global Chemical, SCG Chemicals, and Indorama Ventures anchor capacity through integrated refinery-to-polymer chains and maintain multi-continent customer bases. Competitive advantage increasingly derives from carbon-footprint transparency, closed-loop partnerships, and the ability to co-innovate with brand owners on design-for-recycling. Companies capable of scaling bio-based ventures, integrating mechanical-plus-chemical recycling, and switching feedstocks rapidly are projected to outpace peers within the Thailand plastics market.

Thailand Plastics Industry Leaders

HMC Polymers Thailand

Indorama Ventures Public Company Limited

IRPC Public Company Limited

PTT Global Chemical Public Company Limited

SCG Chemicals Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: NatureWorks secured USD 350 million in financing from Krungthai Bank to build a 75,000-ton PLA facility that will source local sugarcane.

- May 2024: Dow and SCG Chemicals signed an agreement to transform 200,000 tons of plastic waste in the Asia-Pacific region into circular products by 2030.

Thailand Plastics Market Report Scope

Plastics are semi-synthetic or synthetic materials, with polymer as the vital ingredient. It is also defined as polymers having long carbon chains. Plastic has the capability of being molded or shaped generally by the application of pressure and heat. The raw materials used to produce plastics include cellulose, coal, natural gas, salt, crude oil, etc. The Thailand plastics market is segmented by type and application. By type, the market is segmented into traditional plastics, engineering plastics, and bioplastics. By application, the market is segmented into packaging, electrical and electronics, building and construction, automotive and transportation, furniture and bedding, and other applications. The report offers the market sizes and forecasts for each segment on the basis of value (USD million).

By Type

| Traditional Plastics | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) | |

| Engineering Plastics | Polyethylene Terephthalate (PET) |

| Polyamides (PA) | |

| Polycarbonates (PC) | |

| Styrene Copolymers (ABS and SAN) | |

| Polybutylene Terephthalate (PBT) | |

| Polymethyl Methacrylate (PMMA) | |

| Other Engineering Plastics | |

| Bioplastics |

By Application

| Packaging |

| Electrical and Electronics |

| Building and Construction |

| Automotive and Transportation |

| Furniture and Bedding |

| Other Applications |

| By Type | Traditional Plastics | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polyvinyl Chloride (PVC) | ||

| Polystyrene (PS) | ||

| Engineering Plastics | Polyethylene Terephthalate (PET) | |

| Polyamides (PA) | ||

| Polycarbonates (PC) | ||

| Styrene Copolymers (ABS and SAN) | ||

| Polybutylene Terephthalate (PBT) | ||

| Polymethyl Methacrylate (PMMA) | ||

| Other Engineering Plastics | ||

| Bioplastics | ||

| By Application | Packaging | |

| Electrical and Electronics | ||

| Building and Construction | ||

| Automotive and Transportation | ||

| Furniture and Bedding | ||

| Other Applications | ||

Key Questions Answered in the Report

What is the current production volume of the Thailand plastics market?

Production reached 6.43 million tons in 2026 and is projected to expand to 7.56 million tons by 2031.

How large is packaging within the Thailand plastics market?

Packaging accounted for 25.62% of total volume in 2025 and continues to grow on the back of food, beverage, and e-commerce demand.

What role do electric vehicles play in Thai plastics demand?

EV production targets under the 30@30 policy have lifted demand for lightweight engineering resins, pushing automotive plastics toward a 3.56% CAGR.

How are Thai producers responding to stricter waste regulations?

Leading companies invest in mechanical and chemical recycling, adopt bio-based feedstocks, and collaborate on circular-economy projects to stay compliant and competitive.

Page last updated on: