Asia-Pacific AI In HR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

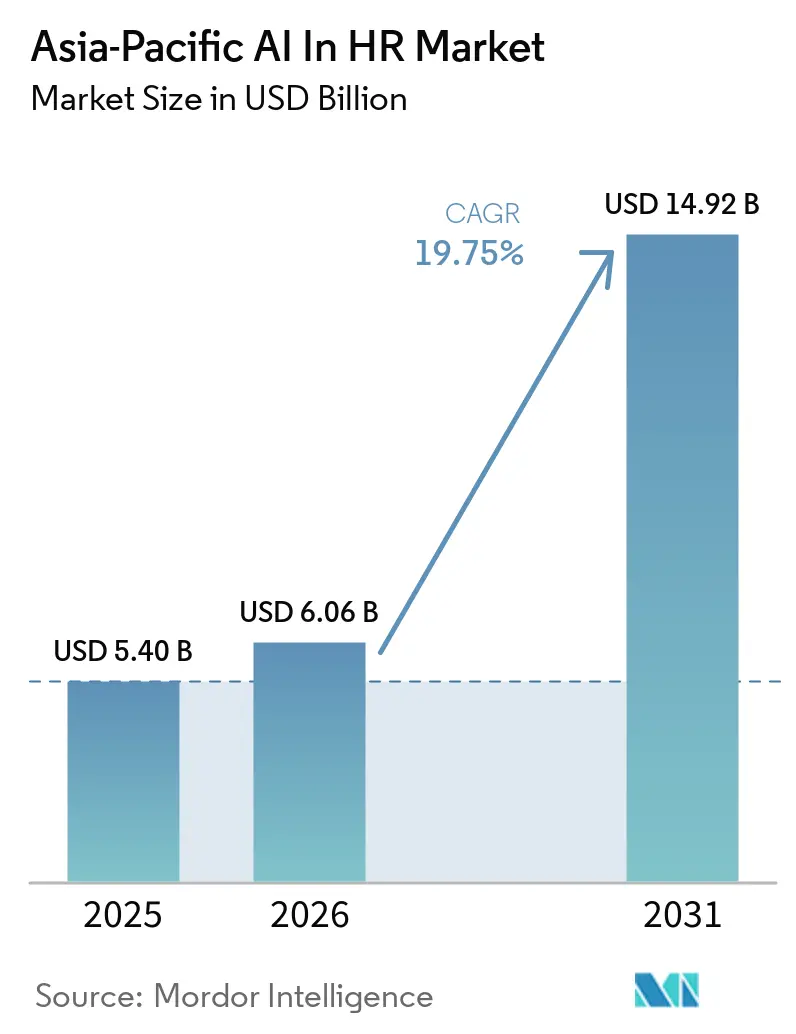

| Base Year Market Size (2025) | USD 5.40 Billion |

| Market Size (2026) | USD 6.06 Billion |

| Market Size (2031) | USD 14.92 Billion |

| Growth Rate (2026 - 2031) | 19.75% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific AI In HR Market Analysis by Mordor Intelligence

The Asia-Pacific AI in HR market size is expected to grow from USD 5.40 billion in 2025 to USD 6.06 billion in 2026 and is forecast to reach USD 14.92 billion by 2031 at 19.75% CAGR over 2026-2031. This expansion reflects a broader shift across regional enterprises as HR systems move beyond workflow automation into data-linked decision support across hiring, development, service delivery, and workforce planning. Spending is also holding up because organizations continue to expand their workforces while investing in AI, keeping human capital software budgets active even as cost control remains important. Cloud-led delivery still shapes the current structure of the Asia-Pacific AI in HR market, while hybrid models are gaining ground where data residency rules limit full adoption of public cloud. Recruitment remains the largest application area because employers continue to compete for scarce digital talent, while learning and development is rising faster as employers respond to retraining needs across a changing labor base. The competitive field remains broad, with global enterprise platforms and APAC-native vendors both expanding through product depth, regional compliance capabilities, and service-led delivery models.

Key Report Takeaways

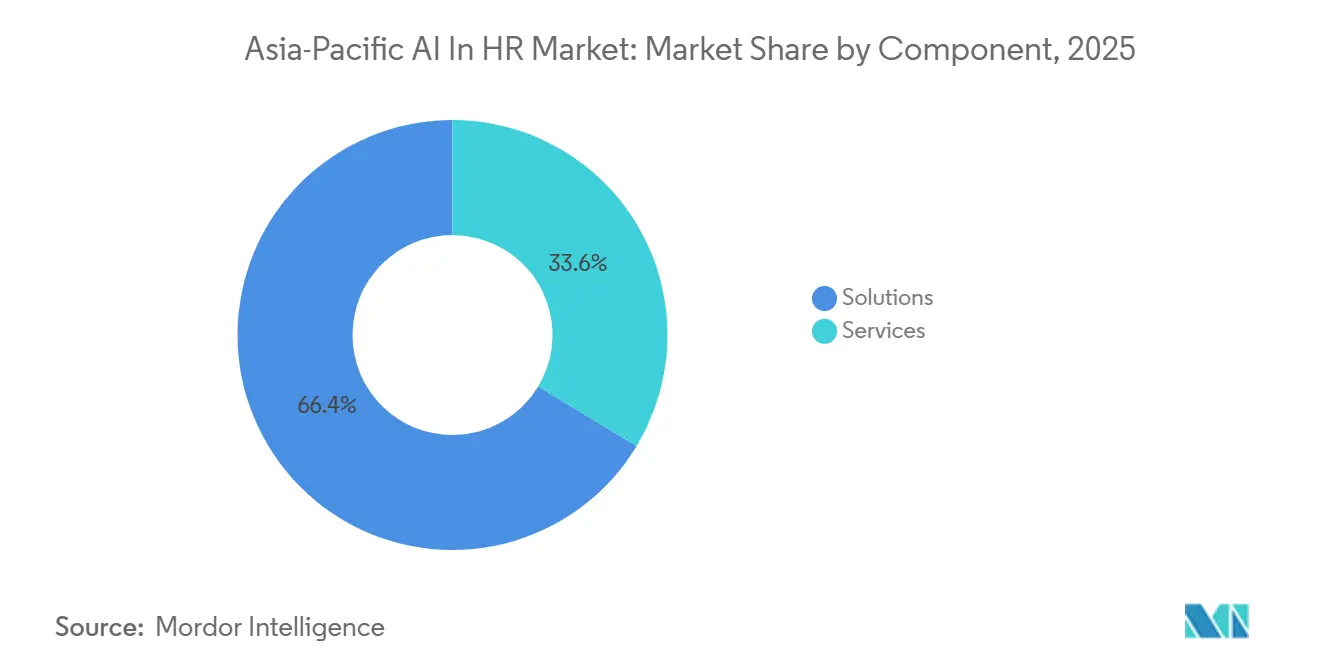

- By component, solutions held a 66.37% share of the Asia-Pacific AI in HR market in 2025, while services are projected to expand at a 21.34% CAGR through 2031.

- By deployment mode, cloud-based deployment held 72.41% of the Asia-Pacific AI in HR market share in 2025, while hybrid deployment is projected to grow at a 22.47% CAGR through 2031.

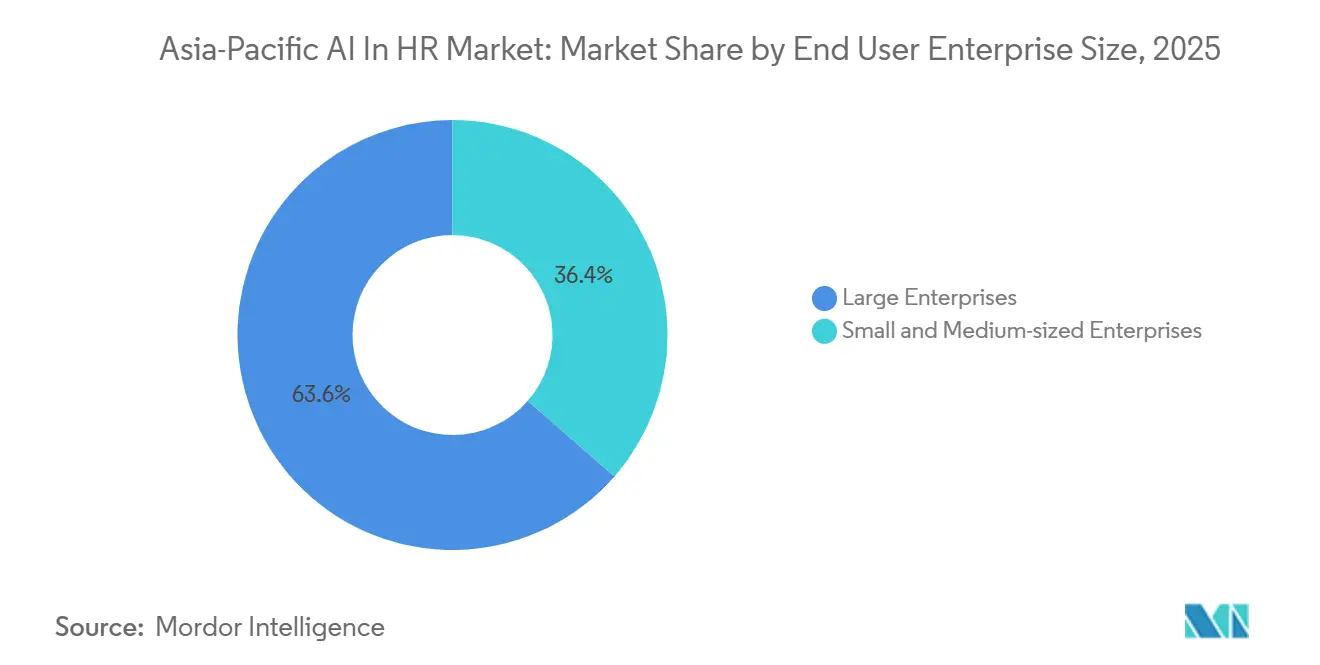

- By end-user enterprise size, large enterprises accounted for 63.57% of the APAC AI in HR market in 2025, while SMEs are projected to expand at a 23.68% CAGR through 2031.

- By application, recruitment and talent acquisition accounted for a 22.73% share of the Asia-Pacific AI in HR market size in 2025, while learning and development is projected to grow at a 20.82% CAGR through 2031.

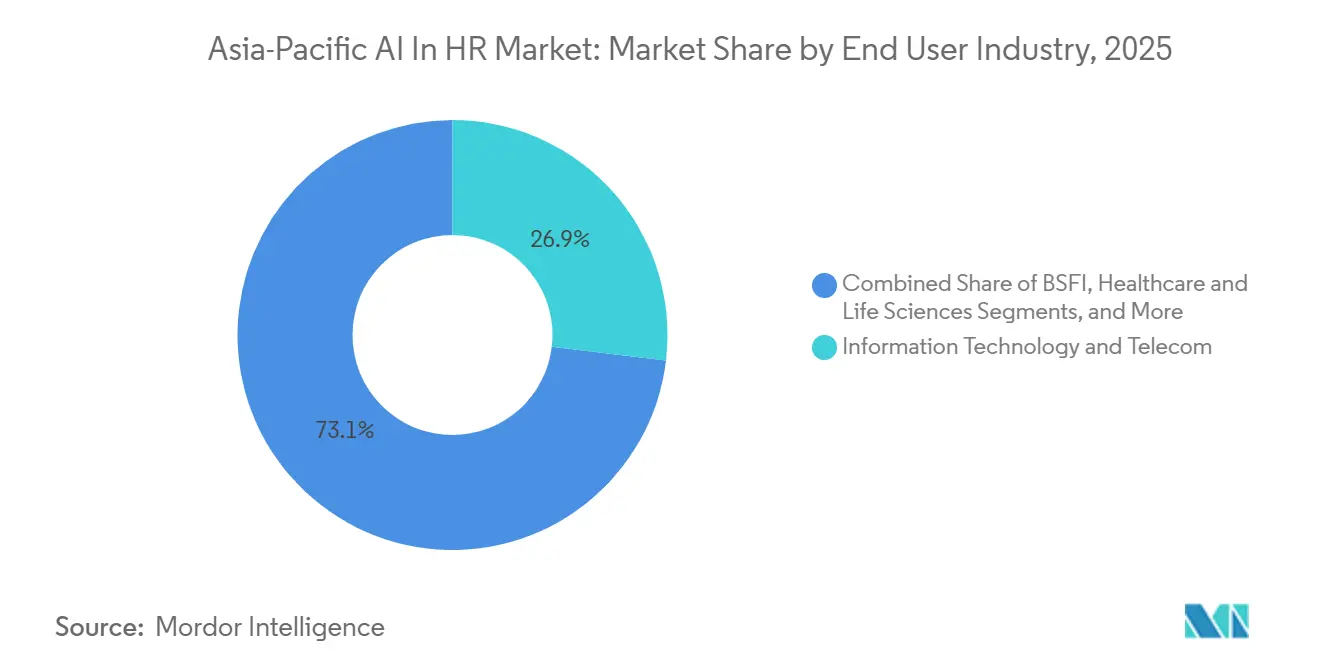

- By end user industry, IT and Telecom held a 26.89% share of the APAC AI in HR market in 2025, while healthcare and life sciences are projected to expand at a 19.93% CAGR through 2031.

- By geography, China led with a 24.47% share of the APAC AI in HR market in 2025, while India is projected to record the fastest CAGR of 24.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific AI In HR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Cloud-Native Human Resources Platforms | +5.2% | Global, with concentration in India, Southeast Asia, and China | Short term (= 2 years) |

| Intensifying Competition For Digital And AI Talent | +4.1% | APAC core, India, China, South Korea, and Australia | Medium term (2-4 years) |

| Demand For Data-Driven Recruitment And Workforce Analytics | +3.8% | Global, with early gains in Singapore, Australia, and India's GCC clusters | Medium term (2-4 years) |

| Expansion Of AI-Enabled Employee Self-Service And Human Resources Automation | +3.2% | Global, spill-over to ASEAN and Japan | Short term (= 2 years) |

| Multilingual Generative AI Agents For Frontline And Distributed Workforces | +2.4% | APAC core, India, Southeast Asia, and China | Medium term (2-4 years) |

| Skills-Graph Adoption In Regional Conglomerates And Global Capability Centers | +1.8% | India and Southeast Asia, with early gains in South Korea | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption Of Cloud-Native Human Resources Platforms

Cloud-native deployment has moved from a preferred setup to a practical operating model across the Asia-Pacific AI in HR market. Vendors now package model updates, language support, and compliance features directly into software-as-a-service environments, which reduces the ongoing maintenance burden for enterprise IT teams. In late 2025, enterprises in labor-constrained markets such as Australia and Japan were expanding their use of cloud HCM beyond core HR into AI-enabled talent and financial planning functions, indicating that buyers increasingly want connected operating data rather than isolated HR records. This demand pattern also explains why the Asia-Pacific AI in HR market continues to favor platforms that can be updated centrally across multiple countries. The same shift is not producing a single architecture outcome across markets because many organizations still want sensitive employee data to be partly stored on domestic infrastructure. A survey across 12 Asia-Pacific markets found that 65% of organizations in the region and 66% of Japanese companies preferred on-premises or hybrid infrastructure for AI workloads, supporting the strong rise of hybrid models alongside the broader cloud base.[1]Lenovo Japan, “2025年における日本のAI支出額は5倍以上の増加、一方で組織全体でAIを導入した企業はわずか2%,” Lenovo Japan via PR TIMES, prtimes.jp

Intensifying Competition For Digital And AI Talent

The contest for digital and AI talent is driving demand across the Asia-Pacific AI in HR market, as companies need better hiring, retention, and skills tools simultaneously. In 2026, firms in the region planned an average AI investment of USD 245 million over the next 12 months, while 56% were also hiring for new AI-specific roles, indicating that automation is not reducing pressure on workforce planning. In 2025, 90% of APAC employers prioritized skills initiatives in workforce decision-making, yet fewer than 40% had programs ready to build capabilities for future roles, leaving a clear gap between intent and execution. That gap pushes employers toward platforms that can infer skills, identify internal mobility options, and shorten hiring cycles without adding large HR teams. One Southeast Asia financial services deployment processed more than 35,000 resumes and reduced time-to-hire by 48%, demonstrating that adoption is justified by direct hiring outcomes rather than experimentation alone. As a result, the Asia-Pacific AI in HR market is seeing demand from both fast-scaling enterprises and employers seeking to retain scarce technical talent within existing teams.

Demand For Data-Driven Recruitment And Workforce Analytics

Recruitment and workforce analytics are moving from support functions into decision tools for senior management across the Asia-Pacific AI in HR market. A recent study found that 65% of organizations viewed analytics-driven decision-making as the most valuable outcome of AI in HR, ahead of efficiency gains and bias reduction. The same study noted that 49% of organizations expected workforce analytics investment to nearly double within 12 months, from a current 29% adoption base, pointing to a strong budget shift toward insight-led HR operating models. This helps explain why the Asia-Pacific AI in HR market is rewarding platforms that connect applicant, employee, performance, and productivity data within a single environment. When HR leaders can query turnover, skill availability, and workforce cost changes in real time, AI tools become part of planning rather than an isolated reporting layer. Over time, stronger internal analytics may also reduce dependence on third-party external talent datasets, which could shift value toward integrated HCM and analytics vendors rather than stand-alone applicant tracking products.

Expansion Of AI-Enabled Employee Self-Service And Human Resources Automation

Employee self-service is expanding beyond chatbot support into workflow execution in the Asia-Pacific AI in HR market. In 2025, one vendor announced an AI Assistant that allows employees to ask questions about policies, leave entitlements, and procedures via natural-language chat, using the Azure OpenAI Service and Azure AI Document Intelligence.[2]SmartHR, “SmartHR、人事・労務に関する問い合わせにAIが回答する「AIアシスタント」機能を7月下旬に提供開始,” SmartHR, smarthr.co.jp Another platform highlighted its Super Agent and earlier Model Context Protocol server, which enabled third-party AI agents to securely access and act on HR data, demonstrating how vendors are trying to turn HR systems into orchestration layers rather than simple record systems. This matters because shared service teams are under pressure to handle a larger number of employee requests without expanding headcount at the same pace. In South Korea, a large employer was reported to be operating more than 85 robotic process automation tasks alongside named agentic AI systems for payroll, welfare notifications, and education guidance, signaling that enterprises are assigning AI a direct operational role in HR processes. The Asia-Pacific AI in HR market is therefore expanding not only through new software seats, but also through broader use of AI inside routine service delivery and process management.[3]Yonhap News, “[AI픽] AI 직원이 출근했다…SK하이닉스 'HR 혁명',” Yonhap News, yna.co.kr

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy And Cybersecurity Concerns | -3.2% | Global, most acute in China, India, Japan, and Vietnam | Short term (= 2 years) |

| Integration Complexity With Legacy Human Resources And Payroll Systems | -2.5% | APAC core, Japan, China, and India legacy payroll stacks | Medium term (2-4 years) |

| Fragmented Data Localization And Labor-Law Requirements Across Asia-Pacific | -1.8% | APAC core, spill-over to Southeast Asia | Medium term (2-4 years) to Long term (= 4 years) |

| Shortage Of AI Governance Skills Within Human Resources Teams | -1.2% | Global, concentrated in SME and mid-market segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy And Cybersecurity Concerns

Data governance remains one of the clearest brakes on the Asia-Pacific AI in HR market because employee information is sensitive, fragmented, and often subject to country-level handling restrictions. Organizations need systems that can manage consent, review pathways, and cross-border transfer rules without exposing payroll, performance, or hiring records to unauthorized use. China's Personal Information Protection Law and India's Digital Personal Data Protection Act are important constraints, and those legal frameworks continue to slow rollout decisions where employee data crosses borders or feeds automated screening models. The same concern is growing at the application level because employers are also dealing with rising volumes of AI-generated candidate content. By mid-2025, AI-generated resumes across Asia had increased by 91%, with Malaysia recording a 109% rise, which adds new verification and audit pressure for recruitment systems. These issues do not stop adoption, but they do favor vendors in the Asia-Pacific AI in HR market that offer local hosting, auditable workflows, and controls designed for high-sensitivity employment data.[4]SEEK, “How the Company Is Using AI to Transform Recruitment Across Asia,” Tech Edition, techedt.com

Integration Complexity With Legacy Human Resources And Payroll Systems

Integration remains a major constraint because many APAC enterprises still operate country-specific payroll, attendance, and compliance systems that were never designed for AI-enabled workflows. This friction is especially visible in large organizations that manage several local systems across Japan, China, India, and Southeast Asia. A recent Southeast Asia survey found that 62% of organizations cited system integration issues as the main barrier to AI-HR return on investment, ahead of cost, data security concerns, and skills gaps. That finding shows why implementation depth matters as much as product quality in the Asia-Pacific AI in HR market. Buyers increasingly screen vendors on the availability of local compliance connectors and deployment support before they evaluate advanced AI features. This dynamic benefits established platforms that can integrate with statutory systems and local payroll frameworks without requiring a full replacement of the installed HR stack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Redefining Platform Deployment Economics

Solutions held a 66.37% share in 2025, indicating that software licenses, SaaS subscriptions, and application layers still anchor the current revenue mix of the Asia-Pacific AI in HR market. Enterprises generally started their spending with platform adoption, recruitment tools, core HR systems, and workforce analytics products before expanding into larger implementation programs. Within the solutions category, demand has been moving toward pre-integrated HR applications rather than broad model-building environments, as buyers want faster deployment and clearer business ownership. That shift supports vendors that package recruitment, performance, planning, and service-delivery tools into a single environment rather than offering AI capabilities as a technical toolkit. It also explains why function-specific applications are gaining relative weight inside the Asia-Pacific AI in HR industry, as enterprises prefer configured outcomes over bespoke development.

Services are projected to grow at a 21.34% CAGR through 2031, making them the faster-growing component even though solutions remain larger. The rise of services reflects the fact that deployment in the Asia-Pacific AI in HR market often requires regional configuration, systems integration, workflow redesign, and long-term model maintenance. In March 2026, one vendor signaled this direction by acquiring SUNITED Corporation to build an AI BPaaS model that combines SaaS, AI technology, and IT operations expertise. As more buyers ask vendors to deliver outcomes rather than software alone, implementation and managed support become part of the core commercial offer. This pattern is reshaping platform economics because vendors can capture a larger share of wallet per customer, even while service-heavy delivery may pressure gross margins over time.

By Deployment Mode: Hybrid Adoption Signals Unresolved Data Sovereignty Tensions

Cloud-based deployment accounted for 72.41% of revenue in 2025, making it the largest share of the Asia-Pacific AI in HR market. Buyers across the region favored continuously updated architectures because they support faster rollouts, lower infrastructure burden, and easier delivery of new AI features across multiple business units. Cloud environments also align with the broader move toward centralized HCM platforms that connect talent, payroll-adjacent processes, analytics, and service delivery in a single stack. For many organizations, this model has become the default path for new AI-led HR investment rather than a later-stage modernization step. The Asia-Pacific AI in HR market share held by cloud-based deployment in 2025 reflects that practical preference for scale, speed, and lower internal maintenance demands.

Hybrid deployment is projected to grow at a 22.47% CAGR through 2031, which makes it the fastest-growing deployment mode. Growth is being shaped by data localization rules, governance concerns, and the fact that many large employers cannot move all payroll and employee data into public cloud environments in a single cycle. One vendor addressed this issue with its Model Context Protocol server, which was designed to let compatible AI agents securely access and act on HR data across on-premises, hybrid, and cloud environments. Japan remains an important example of this demand pattern because many companies still want internal infrastructure involvement for AI workloads. A regional survey found that only 34% of Japanese organizations planned to buy AI-as-a-service from specialized providers without involving internal infrastructure, which supports a durable role for hybrid deployment in the Asia-Pacific AI in HR market.

By End User Enterprise Size: SME Uptake Reshaping The Competitive Funnel

Large enterprises held a 63.57% revenue share in 2025, which kept them at the center of current demand in the Asia-Pacific AI in HR market. These buyers usually manage large, diverse workforces across several countries, so they commit to multi-module deployments with higher contract values and longer implementation cycles. They also have stronger internal requirements for integration, governance, reporting, and data controls, which support spending on full-suite platforms rather than stand-alone tools. This has allowed major vendors to build their initial scale around complex enterprise accounts before pushing deeper into smaller customer groups. The current structure of the APAC AI in HR market, therefore, still rests on the spending depth of large employers.

SMEs are projected to expand at a 23.68% CAGR through 2031, making them the fastest-growing segment of enterprises. That trajectory points to a broader customer base in which per-seat pricing, faster onboarding, and bundled functionality matter more than large, consulting-led deployments. Cloud-native commercial models reduce the total cost of ownership for smaller buyers, which is a key reason adoption is spreading beyond the large-enterprise core. At the same time, vendors still need to meet local compliance, language, and mobile usability expectations if they want to scale in this part of the Asia Pacific AI in HR industry. This creates a strong opening for platforms that combine payroll, attendance, hiring, and talent features inside a single tenant. Over time, SME growth will likely widen the competitive funnel, as regional and local vendors can target volume-based adoption even if they do not match global incumbents in enterprise breadth.

By Application: Recruitment Leads, But Learning And Development Holds Structural Upside

Recruitment and talent acquisition led applications, with a 22.73% share in 2025, indicating where the APAC AI in HR market is most concentrated today. Employers across the region have been using AI to source candidates, screen resumes, rank applications, and improve matching accuracy in tighter labor markets. This large share reflects direct business pressure, as hiring delays can affect revenue, delivery capacity, and digital transformation programs much more quickly than slower-moving HR functions. Survey evidence also showed that AI and machine learning were already widely deployed in HR and talent management across ASEAN, supporting the strength of recruitment-led spending. Other applications, such as core HR, service delivery, performance management, employee engagement, and workforce planning, remain important, but they are expanding from a smaller installed base.

Learning and development is projected to grow at a 20.82% CAGR through 2031, making it the fastest-growing application in the Asia-Pacific AI in HR market. The main reason is the scale of retraining needed across Southeast Asia and other regional labor pools, as job requirements shift faster than traditional learning models can accommodate. In 2025, it was reported that 62 out of every 100 workers in Southeast Asia would require formal retraining by 2030, while 96% of employers said they needed to invest in improving or adapting existing workers. That scale of need supports AI-led learning pathways, personalized training, and skills-based workforce planning rather than one-time course delivery. The Asia-Pacific AI in HR market is therefore seeing learning move closer to workforce strategy, especially where companies cannot hire all the required digital skills from outside. Workforce planning and analytics should also benefit from this shift, as learning decisions increasingly depend on skill data, attrition risk, and future role demand within the same platform environment.

By End User Industry: IT And Telecom Anchors, Healthcare Accelerates

IT and Telecom accounted for 26.89% of the APAC AI in HR market in 2025, making it the largest vertical. This sector has high-volume recruitment needs, strong digital capability, and a long record of early enterprise SaaS adoption, so it has moved faster than most other industries in deploying AI across hiring, planning, and talent operations. Large employer groups, especially in technology-led service environments, use AI for attrition prediction, internal mobility, and workforce planning at a depth that often sets the benchmark for other sectors. The result is a vertical with both current scale and ongoing product influence because vendor roadmaps are often shaped by what IT and Telecom buyers adopt first. This leadership also reflects the speed at which digital talent shortages translate into measurable business risk for these employers.

The healthcare and life sciences industry is projected to grow at a 19.93% CAGR through 2031, making it the fastest-growing industry segment. Growth is being driven by shortages in clinical and support roles, credential-matching complexity, and aging-population pressures that affect labor supply across several APAC countries. By 2050, more than a quarter of the region's population will be aged 60 and above, and 61% of Japanese executives already see aging workforces affecting recruitment and retention decisions. In April 2026, South Korea’s Ministry of Employment and Labor expanded its national AI job-matching service for mid-career and elderly workers, showing how public systems are also pushing AI-led labor allocation in healthcare and welfare-related employment channels. This mix of labor scarcity, regulatory screening needs, and public employment support is creating a strong growth path for healthcare use cases inside the Asia-Pacific AI in HR market.

Geography Analysis

China held a 24.47% share in 2025, giving it the largest country position in the Asia-Pacific AI in HR market. Its lead reflects a more mature domestic platform base, broader enterprise cloud migration, and the scale advantages that come from a large employer universe across technology, manufacturing, BFSI, and public administration. The country's regulatory structure also increases the localization burden for foreign vendors, as HR data-handling rules make cross-border processing more difficult. Japan remains one of the region's largest markets in absolute terms, but adoption still looks uneven across functions. AI use in Japanese HR was broad at the surface level, while deeper use in high-sensitivity areas, such as compensation, remained limited, suggesting caution in governance and more complex data preparation needs.

India is projected to post the fastest CAGR at 24.27% through 2031, making it the clearest growth engine within the APAC AI in HR market. The country benefits from rapid GCC expansion, a dense, homegrown HR technology ecosystem, and a growing base of AI-native vendors scaling across both white-collar and frontline workforce use cases. This growth is also linked to changing statutory and payroll requirements, which increase demand for automated compliance and workforce administration tools. Southeast Asia is also becoming a major demand pocket, as many organizations increased AI-HR budgets in 2026, although maturity still varies sharply by country. In this sub-region, multilingual support is often as important as functional depth, as employers expect systems to work across local languages and diverse workforce profiles.

Australia and New Zealand are among the region's more analytically mature environments, though deployment depth still varies across organizations. In late 2025, 81% of Australian recruitment agencies were using AI, and 86% of Australian HR professionals expected AI to significantly affect operations, indicating a strong readiness for further adoption. South Korea is also advancing quickly, supported by larger enterprise AI budgets and early use of agentic systems in HR operations. The rest of Asia Pacific remains earlier in adoption, but it offers opportunities for cloud-based HR and payroll automation vendors that can meet local compliance requirements. Across the full Asia-Pacific AI in HR market, geography remains decisive because regulatory design, language requirements, data residency rules, and enterprise digital maturity differ sharply from one country group to another.

Competitive Landscape

The APAC AI in HR market remains fragmented, as no single vendor controls a dominant share of regional revenue. The top 5 to 7 global and regional platforms together account for less than half of total revenue, while a long tail of specialist vendors competes in assessment, skills inference, conversational AI, and people analytics. This structure keeps competitive pressure high and prevents the market from consolidating around a single product architecture. Global enterprise software vendors still hold strong positions because they offer broad suites, deep integration, and established enterprise relationships. At the same time, APAC-native vendors continue to close the gap through regional compliance support, mobile-first design, and faster adaptation to local language requirements.

Workday strengthened its position in October 2025 by completing the acquisition of Paradox, adding conversational AI capabilities for high-volume frontline hiring to its existing talent stack. Workday had also announced in June 2025 its AI Agent Partner Network and Agent Gateway, which framed AI governance around an Agent System of Record and showed how large incumbents are building operating infrastructure for both human and digital workers. Darwinbox responded on the regional level by launching the first Model Context Protocol server in the HCM category, positioning itself as an orchestration layer that enables secure agent access to HR data across enterprise systems. SmartHR also expanded beyond core HR software through acquisitions, including SUNITED in March 2026 and Crossbit in May 2026, which showed a clear move toward broader labor management and service-linked delivery. These actions show that the Asia-Pacific AI in HR market is being shaped by both platform consolidation and broader workflow ownership.

There is still clear room for new entrants in areas such as blue-collar workforce management, AI governance, explainability tools, and skills-graph infrastructure for multi-country employers. Eightfold AI added to this competitive picture by opening a 22,000 sq. ft. Bangalore office in November 2025, expanding its engineering footprint in India and supporting its AI-native talent platform strategy. Competitive success in the APAC AI in HR market increasingly depends on whether vendors can combine product depth with local compliance delivery and real workflow outcomes. Buyers are rewarding platforms that can support hiring, employee service, analytics, and skills programs inside a connected environment rather than through isolated modules. That is why differentiation now rests less on generic AI claims and more on deployment fit, governance design, and regional execution strength.

Asia-Pacific AI In HR Industry Leaders

Darwinbox Digital Solutions Private Limited

PeopleStrong Technologies Private Limited

SmartHR, Inc.

Beijing Beisen Cloud Computing Co., Ltd.

Eightfold AI Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SmartHR acquired Crossbit Inc. (Rakushifu) to integrate attendance, shift optimization, and employee data, aiming to become a full HCM infrastructure provider.

- March 2026: SmartHR acquired SUNITED Corporation to launch “AI BPaaS,” combining SaaS, AI, and human IT operations for enterprise HR digitization.

- November 2025: General Atlantic invested JPY 14.6 billion (USD 96 million) in SmartHR, supporting product development, M&A, and go-to-market expansion in Japan’s cloud HR market.

- October 2025: Workday acquired Paradox, integrating its conversational AI with HiredScore and Workday Recruiting to build an end-to-end AI talent acquisition suite.

Asia-Pacific AI In HR Market Report Scope

The Asia-Pacific AI in HR market refers to technology platforms and services that apply artificial intelligence to transform human resource management across enterprises in the region. These solutions include AI software, platforms, and AI-enabled HR applications, supported by professional services, and deployed via cloud, on-premises, or hybrid models. They serve both large enterprises and SMEs, enabling applications such as core HR administration, recruitment and talent acquisition, HR service delivery via virtual assistants, performance management, learning and development, employee engagement, and workforce analytics. Adopted across industries including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others, the market’s primary purpose is to help organizations in Asia-Pacific optimize workforce productivity, enhance employee experience, and align HR strategies with business outcomes through AI-driven insights and automation.

The Asia-Pacific AI in HR market is segmented by Component (Solutions [AI Software and Platforms, AI-enabled HR Applications], and Services), Deployment Mode (Cloud-based, On-premise, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), Application (Core Human Resources and Administration, Recruitment and Talent Acquisition, HR Service Delivery and Virtual Assistants, Performance Management, Learning and Development, Employee Engagement and Experience, and Workforce Planning and Analytics), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (China, India, Japan, South Korea, Australia and New Zealand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | AI Software and Platforms |

| AI-enabled HR Applications | |

| Services |

| Cloud-based |

| On-premise |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Core Human Resources and Administration |

| Recruitment and Talent Acquisition |

| Human Resources Service Delivery and Virtual Assistants |

| Performance Management |

| Learning and Development |

| Employee Engagement and Experience |

| Workforce Planning and Analytics |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Component | Solutions | AI Software and Platforms |

| AI-enabled HR Applications | ||

| Services | ||

| By Deployment Mode | Cloud-based | |

| On-premise | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Application | Core Human Resources and Administration | |

| Recruitment and Talent Acquisition | ||

| Human Resources Service Delivery and Virtual Assistants | ||

| Performance Management | ||

| Learning and Development | ||

| Employee Engagement and Experience | ||

| Workforce Planning and Analytics | ||

| By End User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current and forecast value of the Asia-Pacific AI in HR market?

The Asia-Pacific AI in HR market was valued at USD 5.40 billion in 2025, is projected at USD 6.06 billion in 2026, and is forecast to reach USD 14.92 billion by 2031 at a 19.75% CAGR.

Which deployment model leads adoption in Asia-Pacific AI in HR?

Cloud-based deployment led with a 72.41% share in 2025, while hybrid is growing faster because many employers still need local control over sensitive employee data.

Which application area generates the highest revenue in this space?

Recruitment and talent acquisition led with a 22.73% share in 2025 because employers across the region are still competing for scarce digital and AI talent.

Which country is growing fastest across Asia Pacific?

India is projected to record the fastest CAGR at 24.27% through 2031, supported by GCC growth, startup activity, and demand for payroll and compliance automation.

Which end-user industry shows the strongest momentum?

IT and Telecom held the largest share at 26.89% in 2025, while healthcare and life sciences is projected to grow fastest at a 19.93% CAGR through 2031.

Why are services gaining importance alongside software platforms?

Services are projected to grow at a 21.34% CAGR because enterprises need integration, regional configuration, and ongoing operational support to make AI-HR systems work across fragmented local environments.

Page last updated on: