AI Bias Audit And Algorithmic Fairness In HR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 468.58 Million |

| Market Size (2031) | USD 992.69 Million |

| Growth Rate (2026 - 2031) | 16.20% CAGR |

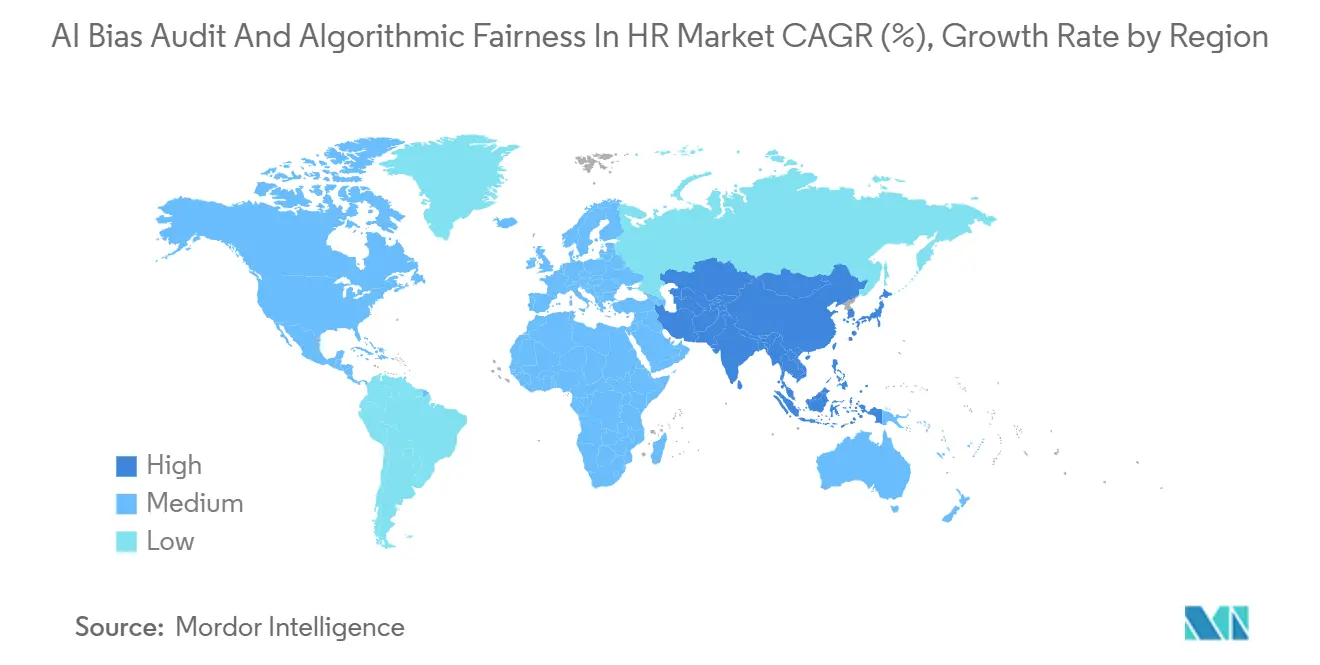

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Bias Audit And Algorithmic Fairness In HR Market Analysis by Mordor Intelligence

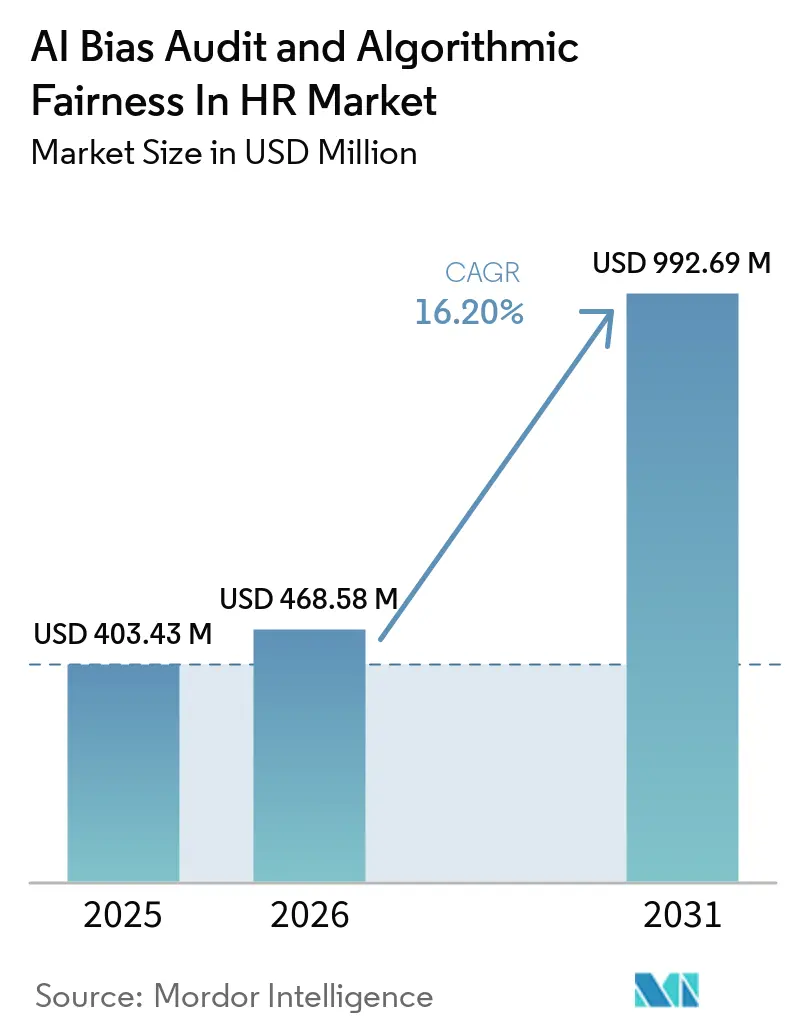

The AI bias audit and algorithmic fairness in HR market size was valued at USD 403.43 million in 2025 and is forecast to reach USD 992.69 million by 2031, advancing at a CAGR of 16.20% during 2026-2031. The current phase of the AI bias audit and algorithmic fairness in HR market is being shaped less by voluntary ethics programs and more by enforcement risk, daily penalty exposure, and the need to defend hiring decisions under closer legal scrutiny. Buyers are moving faster because the cost of waiting has become more visible, especially when automated employment decision tools are already embedded in recruitment and workforce management systems. The AI bias audit and algorithmic fairness in HR market is also widening from one-time checks into broader governance programs that cover model drift, documentation, audit readiness, and remediation support across several workflows. Competitive positioning remains fluid because no single vendor covers every buyer's need, and enterprises are increasingly combining specialist auditors, governance platforms, and embedded talent tools in the same stack. This leaves room for growth across software, services, and continuous monitoring solutions, even as fragmented rules across jurisdictions raise procurement complexity and favor vendors that can support repeatable compliance operations.

Key Report Takeaways

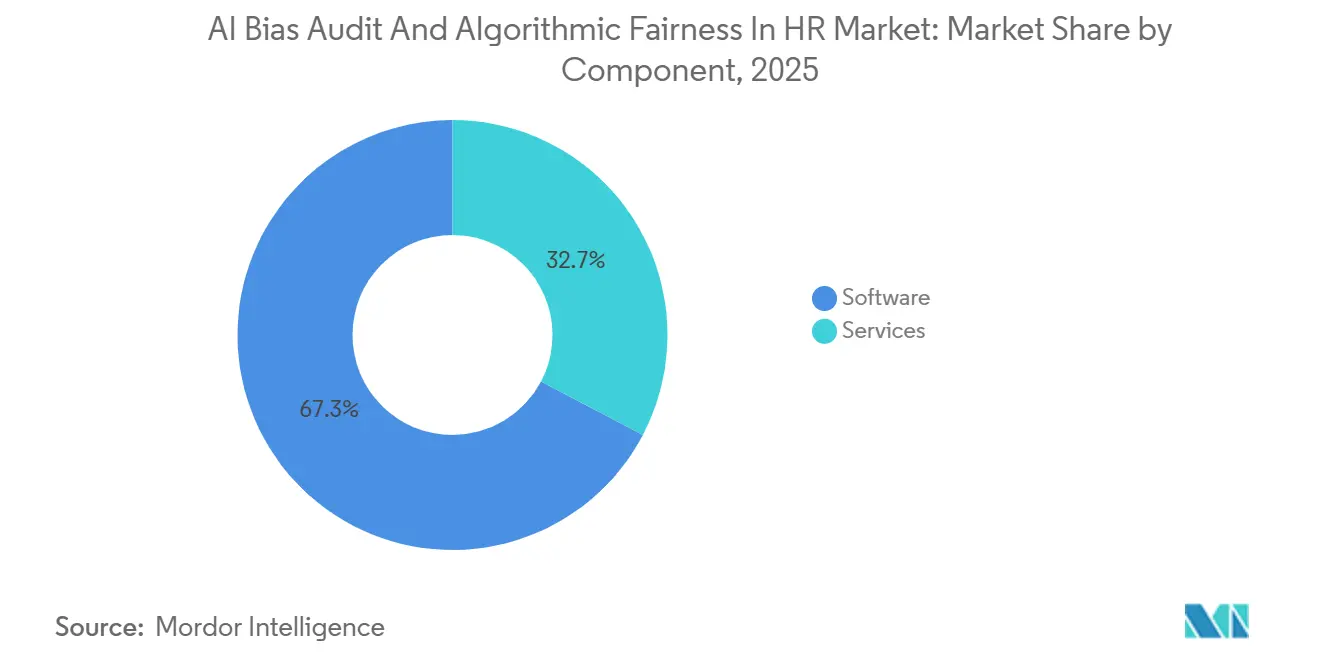

- By component, software held 67.31% of the AI bias audit and algorithmic fairness in HR market share in 2025, while services are projected to expand at a 19.84% CAGR through 2031.

- By HR workflow, candidate screening and ranking accounted for 36.49% of revenue in 2025, while HR governance, monitoring, and reporting are projected to grow at an 18.23% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 65.16% of revenue in 2025, while hybrid deployment is projected to grow at a 19.22% CAGR through 2031.

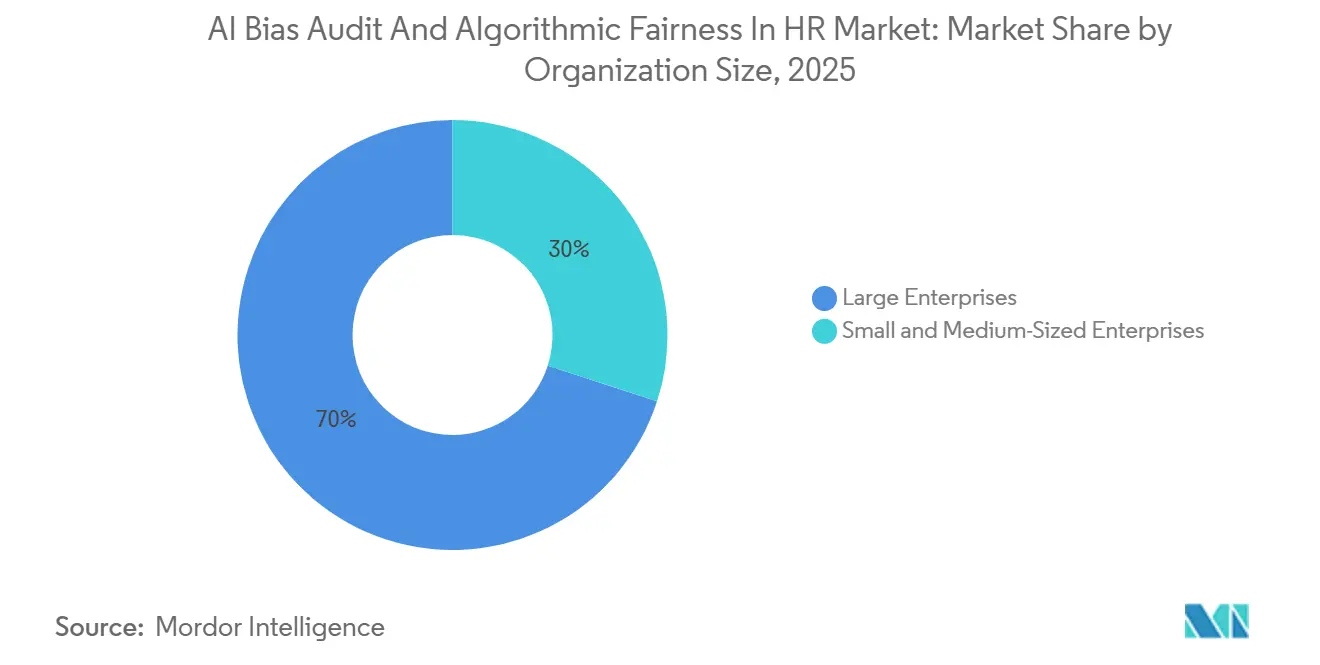

- By organization size, large enterprises represented 70.02% of revenue in 2025, while small and medium-sized enterprises are projected to expand at a 19.51% CAGR through 2031.

- By end-user industry, information technology and telecommunications held 29.61% of revenue in 2025, while healthcare and life sciences are projected to grow at a 17.68% CAGR through 2031.

- By geography, North America held 38.21% of the AI bias audit and algorithmic fairness in HR market share in 2025, while Asia-Pacific is projected to expand at an 18.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Bias Audit And Algorithmic Fairness In HR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enforcement-Led Expansion of Bias Audits for Automated Employment Decision Tools | +3.5% | North America primary, EU and Asia-Pacific as replication broadens | Short term (≤ 2 years) |

| EU AI Act Classification of Employment AI as High-Risk | +2.8% | EU core markets, with spillover to global multinationals | Medium term (2-4 years) |

| Enterprise Shift to Explainable, Bias-Audited Talent Intelligence Platforms | +2.4% | Global, with strongest momentum in North America and Asia-Pacific | Medium term (2-4 years) |

| Cloud-Based Continuous Monitoring and Governance Tooling Adoption | +2.1% | Global, especially cloud-first enterprise markets | Short term (≤ 2 years) |

| Synthetic Resume and Counterfactual Testing Unlocking Audits Where Demographic Data Is Sparse | +1.6% | Global, with higher relevance in GDPR-constrained European markets | Medium term (2-4 years) |

| Procurement Shift From Vendor Trust to Pre-Purchase Algorithm Assurance and Public Audit Dashboards | +1.3% | North America and EU, with early adoption among large enterprises globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enforcement-Led Expansion of Bias Audits for Automated Employment Decision Tools

The AI bias audit and algorithmic fairness in HR market moved into a stricter compliance phase after New York City required independent bias audits for automated employment decision tools. The rule requires covered employers to obtain an audit within 12 months of deployment, publish a summary, and notify candidates before the tool is used in evaluation. The same framework also introduced penalties of USD 500 to USD 1,500 per violation per day, which changed audit spending from a discretionary budget item into a legal risk-control measure. Illinois extended this compliance pressure when Public Act 103-0804 amended the Illinois Human Rights Act and made discriminatory effects from AI use in employment a direct employer concern from January 1, 2026. That shift matters because employers can no longer rely on vendor claims alone when AI tools affect hiring, screening, or related decisions. As more jurisdictions follow this pattern, the AI bias audit and algorithmic fairness in HR market is being pulled forward by legal deadlines rather than long-cycle internal governance programs.

EU AI Act Classification of Employment AI as High-Risk

The AI bias audit and algorithmic fairness in HR market is also being supported by the EU AI Act because employment systems used in recruitment, selection, promotion, task allocation, and performance monitoring fall within the high-risk category. Regulation EU 2024/1689 requires technical documentation, data governance, human oversight, post-market monitoring, and formal compliance controls for high-risk AI systems. Article 4 also brought AI literacy obligations into force for organizations whose staff interact with these systems, meaning compliance activity is already underway before later enforcement milestones fully arrive. Article 99 imposes significant financial pressure, as non-compliance can lead to fines of up to EUR 15 million (USD 16.2 million) or 3% of global turnover. For multinational employers, this creates a parallel workstream that sits alongside U.S. bias audit rules rather than replacing them. As a result, the AI bias audit and algorithmic fairness in HR market is benefiting from demand for conformity preparation, documentation support, and workflow-level controls across global HR operations.

Enterprise Shift to Explainable, Bias-Audited Talent Intelligence Platforms

Enterprise demand is shifting toward platforms that can explain candidate outcomes and demonstrate fairness at the time of procurement. Warden AI reported that 50% of HR buyers now run formal pre-purchase evaluations of AI systems, while only 17% rely mainly on vendor reputation, suggesting a sharper focus on documented assurance.[1]Warden AI, “AI Bias in Hiring, What 150+ Bias Audits Reveal, 2025 State of AI Bias in Talent Acquisition,” Warden AI, warden-ai.com The same report drew on more than 150 bias audits and over 1 million test samples, which gives this change in buyer behavior practical weight inside the AI bias audit and algorithmic fairness in HR market. Platform vendors are also using standards as a market signal, and Eightfold AI stated that its AI Interviewer is backed by ISO 27001 and ISO 42001 certifications. Independent academic work is reinforcing this direction, as counterfactual explainability methods deliver strong explainability-performance trade-offs, including E-P scores of 0.95 in person-job recommendation analyses. This makes the AI bias audit and algorithmic fairness in HR market more favorable for tools built around transparent scoring logic instead of opaque ranking systems.

Cloud-Based Continuous Monitoring and Governance Tooling Adoption

The AI bias audit and algorithmic fairness in HR market is moving beyond annual audit events because fairness issues can surface after deployment as data patterns and models change over time. Holistic AI reflected this product shift through its release of Programmable Controls for Continuous AI Governance in May 2026 and Shadow AI Discovery in April 2026. These capabilities align with the EU AI Act's requirements for logging and lifecycle controls, which push buyers toward systems that can document ongoing oversight rather than isolated reviews. The Cambridge Center for Alternative Finance found that nearly two-thirds of financial services respondents were not monitoring for bias or arbitrary discrimination, indicating that adoption remains early even in regulated sectors. That gap leaves room for cloud-based platforms that automate logging, drift review, and fairness checks across multiple hiring workflows. It also means the AI bias audit and algorithmic fairness in HR market is starting to reward vendors that can support continuous governance at enterprise scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardized Fairness Benchmarks Across Tools and Jurisdictions | -1.8% | Global, most acute for multinationals across U.S., EU, and Asia-Pacific | Long term (≥ 4 years) |

| Privacy, Black-Box Complexity, and Data Access Barriers Slow Independent Audits | -1.4% | EU and Asia-Pacific first, with secondary drag in North America | Medium term (2-4 years) |

| Deployer-Led Compliance Slows Procurement Cycles | -1.0% | North America and EU, concentrated in mid-market enterprise segments | Short term (≤ 2 years) |

| Audit Scope Gaps Create Residual Exposure for Intersectional and Disability Risk | -0.8% | Global, especially where intersectional analysis is legally important | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Fairness Benchmarks Across Tools and Jurisdictions

The AI bias audit and algorithmic fairness in HR market still lacks a single fairness standard that works across every legal and operational setting. Warden AI found that fairness scores can vary by up to 40% across nominally similar systems and that 15% of audited tools fail at least one demographic threshold while passing others. That creates a problem for employers because the audit result can depend heavily on the choice of metrics, test design, and the legal framework applied during the review. Academic research in AI and Ethics reached a similar conclusion, arguing that AI-HR systems cannot reliably satisfy fairness requirements across different legal settings without stronger and more plural oversight structures. For vendors, this increases the cost of serving multinational buyers because a single audit approach cannot be cleanly reused across regions. For buyers, it slows procurement because comparing competing vendors becomes harder when each supplier frames fairness through a different testing logic.

Privacy, Black-Box Complexity, and Data Access Barriers Slow Independent Audits

Data access remains a practical barrier in the AI bias audit and algorithmic fairness in HR market because protected attribute data is often limited, sensitive, or restricted. The problem becomes sharper when systems rely on demographic proxies rather than declared attributes, since the audit result becomes less precise and harder to defend. Large model architectures add another layer of difficulty because auditors cannot always trace how candidate features are weighted inside complex scoring pipelines. Nature Scientific Reports showed that detecting hidden intersectional bias in AI recruitment systems can require multi-task adversarial learning rather than standard single-dimension fairness checks. That raises audit effort, computing needs, and the skill threshold required for independent review. These conditions extend review timelines and reduce willingness to pay for a broad audit scope, especially when buyers need fast deployment, and regulators expect strong evidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground on Software-Led Foundations

Software held 67.31% of AI bias audit and algorithmic fairness in HR market share in 2025, which reflected enterprise preference for scalable governance tooling over one-off project delivery. In the first wave of spending, buyers favored platforms that could centralize audit dashboards, testing environments, workflow controls, and documentation. That logic remains strong because large employers often manage multiple hiring workflows simultaneously and need repeatable oversight across them. The AI bias audit and algorithmic fairness in HR market has therefore treated software as the operational base layer for policy enforcement, evidence capture, and cross-jurisdiction reporting. This part of the AI bias audit and algorithmic fairness in HR industry is supported by the need to maintain logs, document model behavior, and coordinate compliance activity across teams rather than around one isolated audit event.

The AI bias audit and algorithmic fairness in HR market size for services is projected to expand at a 19.84% CAGR through 2031, which shows how quickly buyers are discovering the limits of tool-only adoption. Enterprises that started with software are finding that independent reviews, remediation plans, policy design, and technical advisory work still require specialist input. Audit and monitoring services are also benefiting from regulatory structures that separate developer claims from third-party validation, especially when public disclosures or candidate notifications are involved. As a result, the AI bias audit and algorithmic fairness in HR market is seeing more blended contracts where software subscriptions sit beside managed audits and compliance support. That overlap creates margin pressure for stand-alone advisers, but it also expands recurring service demand as organizations revisit governance controls after deployment.

By HR Workflow: Screening Leads While Governance Expands

Candidate screening and ranking accounted for 36.49% of the market in 2025, making it the largest workflow in the AI bias audit and algorithmic fairness in HR market. This position reflects where regulation and litigation risk have been most visible, since automated screening is often the first hiring step that directly affects candidate access. Stanford HAI reported in May 2026 that its study of 4 million applications across 150 employers found that 26% of Black applicants and 15% of Asian applicants applied to positions where an AI tool produced outcomes triggering federal discrimination scrutiny. That evidence explains why screening audits have drawn the largest early budgets, especially among employers that process large candidate pools. In the AI bias audit and algorithmic fairness in HR market, screening remains the most exposed workflow because ranking models, shortlisting tools, and automated recommendations directly shape who moves forward.

HR governance, monitoring, and reporting is projected to expand at a 18.23% CAGR through 2031, indicating that buyers are widening the scope of review beyond the screening stage. Employers are realizing that a compliant screening tool does not eliminate risk if sourcing, promotion, performance monitoring, or retention models create bias elsewhere. The EU AI Act reinforces this broader view, as employment-related AI is not limited to recruitment and extends to promotion, task allocation, and performance oversight.[2]European Commission, “Regulation EU 2024/1689 (EU AI Act),” European Commission, digital-strategy.ec.europa.eu That is shifting the AI bias audit and algorithmic fairness in HR market toward workflow-spanning controls that support continuous reporting, exception handling, and audit readiness. The AI bias audit and algorithmic fairness in HR market also gains from emerging use cases in onboarding, learning-path assignment, and compensation calibration, where adoption can move faster than formal oversight and create future review needs.

By Deployment Mode: Cloud Leads While Hybrid Supports Control

Cloud-based deployment held 65.16% of the market in 2025, giving it the leading position in the AI bias audit and algorithmic fairness in HR market. Buyers favored cloud tools because they enable faster rollouts, centralized dashboards, ongoing model checks, and easier coordination across dispersed HR teams. Continuous monitoring also aligns well with cloud delivery because drift review, adverse impact flagging, and audit log management are easier to automate in a shared platform environment. In the AI bias audit and algorithmic fairness in HR market, cloud adoption has therefore been linked to speed, visibility, and the need to maintain governance activity after implementation. This model also suits enterprises that want to update controls frequently as regulations, internal policies, and model inputs change.

Hybrid deployment is projected to grow at a 19.22% CAGR through 2031, driven by demand from regulated buyers seeking data control without sacrificing centralized oversight. These buyers often need sensitive records to remain in controlled environments while fairness dashboards and governance reporting stay accessible to corporate teams. The AI bias audit and algorithmic fairness in HR market is seeing this pattern in industries where data residency, privacy expectations, or internal security rules remain strict. On-premises deployment still matters for public sector and sovereign infrastructure requirements, but its growth is slower because dedicated environments are harder to maintain and update. As a result, the AI bias audit and algorithmic fairness in HR market is likely to keep favoring cloud first for flexibility and hybrid for control-heavy use cases.

By Organization Size: SMEs Enter the Category More Quickly

Large enterprises accounted for 70.02% of the market in 2025, keeping them at the center of AI bias audits and algorithmic fairness in HR market demand. Their position was supported by large candidate volumes, broader geographic exposure, and a greater need to coordinate compliance across multiple legal settings simultaneously. Large organizations are also more likely to use multiple AI hiring tools from different vendors, which increases the need for independent review and for integrating governance. In the AI bias audit and algorithmic fairness in HR industry, this makes large buyers the earliest adopters of formal audit platforms, remediation programs, and vendor assurance processes. It also explains why many suppliers first built offerings around enterprise reporting needs, audit documentation, and cross-functional compliance teams.

The AI bias audit and algorithmic fairness in HR market size for small and medium-sized enterprises is projected to grow at a 19.51% CAGR through 2031, which signals a faster expansion from a smaller base. Illinois made this shift more visible because the law applies to employers with even 1 Illinois-based employee, which lowers the threshold for compliance attention. The EU AI Act also places deployer responsibilities on organizations that use high-risk systems, which keeps size from becoming a shield against governance duties. SHRM reported that 63% of organizations had moved beyond the proof-of-concept stage in HR AI, suggesting that adoption is spreading even where formal control structures remain light. That creates a favorable opening in the AI bias audit and algorithmic fairness in HR market for simpler SaaS tools and lighter compliance support designed for smaller HR teams.

By End-User Industry: Technology Leads While Healthcare Accelerates

Information technology and telecommunications accounted for 29.61% of revenue in 2025, making it the largest end-user segment in the AI bias audit and algorithmic fairness in HR market. Technology companies were early adopters because they run large hiring programs, face close public scrutiny, and often understand the technical limits of internal validation better than many other sectors. The size of their applicant pools also increases the visibility of disparate outcomes, thereby raising both legal and reputational risks when AI tools are used in screening and ranking. In the AI bias audit and algorithmic fairness in HR industry, this has kept technology buyers near the front of demand for governance platforms, independent audits, and documented explainability. It also helps explain why many public examples of bias review, standards alignment, and product assurance have emerged first from talent technology and enterprise software providers.

The AI bias audit and algorithmic fairness in HR market size for healthcare and life sciences is projected to grow at a 17.68% CAGR through 2031. This segment is expanding as workforce AI decisions in staffing, allocation, and broader operational planning are held to higher governance standards. Banking, financial services, and insurance also remain material, as the Cambridge Center for Alternative Finance found that 43% of AI vendors in financial services identified algorithmic bias and fairness as among the top risks in the sector. Manufacturing, retail, and e-commerce are adding demand as they apply AI to staffing and operations workflows that can carry repeated fairness exposure across large worker populations. Government and public sector use is smaller in revenue terms, but procurement requirements in these settings often influence later private sector buying behavior inside the AI bias audit and algorithmic fairness in HR market.

Geography Analysis

North America held 38.21% of AI bias audit and algorithmic fairness in HR market share in 2025, which kept the region in the lead. The region is defined by the strongest enforcement backdrop, with New York City requiring independent audits and candidate notice for covered automated employment decision tools.[3]New York City Department of Consumer and Worker Protection, “Automated Employment Decision Tools Frequently Asked Questions,” New York City Department of Consumer and Worker Protection, nyc.gov Illinois added further weight from January 1, 2026, by amending the Illinois Human Rights Act to address discriminatory effects arising from AI use in employment. These actions have pushed employers to treat audit readiness as a live operating requirement rather than a future planning task. North America also benefits from the concentration of major HR technology buyers and vendors, which means compliance spending in the region can quickly influence product design and commercial priorities elsewhere in the AI bias audit and algorithmic fairness in HR market.

Europe remains a major demand center because the EU AI Act classifies recruitment, promotion, task allocation, and performance monitoring systems as high-risk in employment contexts. Article 4 AI literacy obligations are already in effect, meaning organizations are not waiting for later milestones before building governance processes. GDPR-related limits on sensitive data use continue to raise the need for counterfactual testing and other methods that can support fairness reviews where direct demographic data is limited. Germany, France, and the Netherlands remain important because they host many multinational employers that must align local labor practices with broader AI compliance duties.

The AI bias audit and algorithmic fairness in HR market size in Asia-Pacific is projected to expand at an 18.79% CAGR through 2031, making it the fastest-growing regional segment. Growth is being supported by a faster move from general AI adoption toward more formal workplace governance expectations across key economies. SHRM reported that HR AI adoption is already high across Asia-Pacific, which increases the need for control layers before use becomes more deeply embedded in employment decisions. South America, the Middle East, and Africa remain smaller in terms of current revenue, but they are beginning to build demand as large enterprises and multinational employers apply privacy, anti-discrimination, and AI governance principles to hiring practices. These regions still contribute a limited share today, yet their regulatory maturation and cross-border compliance needs support above-average expansion through 2031 relative to the global baseline of the AI bias audit and algorithmic fairness in HR market.

Competitive Landscape

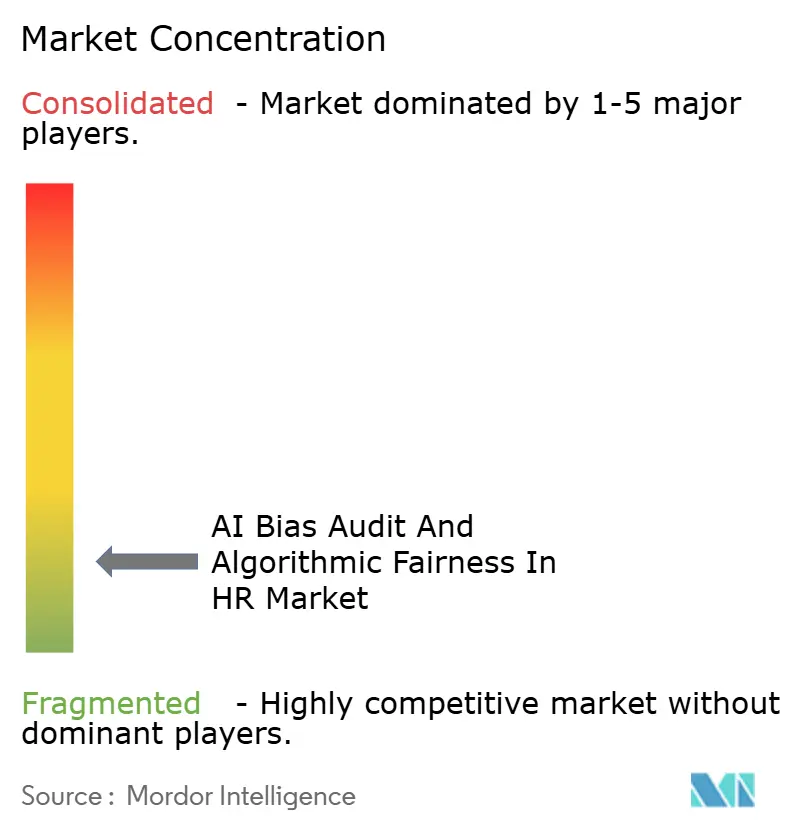

The AI bias audit and algorithmic fairness in HR market remains fragmented, with specialist audit firms, enterprise governance platforms, and fairness-enabled talent suites all competing for overlapping budgets. No single vendor has established a structural moat across all buyer types, and enterprise customers increasingly combine multiple tools rather than standardize on one provider. That pattern narrows the gap between leaders and followers because product breadth, audit independence, and workflow integration matter in different proportions for different buyers. In practice, some suppliers win on technical audit depth, while others win on governance automation or embedded hiring functionality. This keeps the AI bias audit and algorithmic fairness in HR market open to both specialist firms and broader platform vendors.

Strategic moves in 2026 show how quickly vendors are extending their positions. Eightfold AI expanded its interview capabilities in 2026 and stated that its AI Interviewer is supported by ISO 27001 and ISO 42001 certifications, which align with its product positioning.[4]Eightfold AI, “2026 AI Bias Audit Results,” Eightfold AI, eightfold.ai The company also published the 2026 audit results for its matching model, under a Local Law 144-compliant review conducted by BABL AI, providing buyers with a public compliance reference point. Holistic AI, by contrast, moved further into continuous governance with Programmable Controls and Shadow AI Discovery, which broadens its value beyond one-time audit preparation. HireVue expanded its position through product and ecosystem moves, including Assessment Builder, the Hireguide technology acquisition, and integration with the Workday AI Agent Partner Network.

White space remains visible in intersectional and disability fairness testing, SME-accessible assurance infrastructure, and continuous monitoring for generative or agentic hiring workflows. Nature Scientific Reports highlighted the technical challenge here by showing that hidden intersectional bias can require more advanced testing methods than standard fairness checks. The AI bias audit and algorithmic fairness in HR market is therefore likely to reward vendors that can combine audit defensibility with lower implementation burden for smaller buyers. It is also likely to favor providers that can fit into multi-vendor governance stacks without forcing enterprises to replace existing hiring systems.

AI Bias Audit And Algorithmic Fairness In HR Industry Leaders

HireVue, Inc.

Eightfold AI Inc.

Beamery Inc.

Holistic AI Limited

Warden AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Stanford University, Chapman University, and Northeastern University published "Algorithmic Monocultures in Hiring," a study of 4 million applications across 150 employers finding that 26% of Black applicants and 15% of Asian applicants applied to positions where an AI tool produced outcomes triggering federal discrimination scrutiny; the study was presented at the ACM Conference on Fairness, Accountability, and Transparency, and directly increased enforcement urgency for enterprises relying on single-vendor AI screening ecosystems.

- May 2026: The European Commission published draft guidance on high-risk AI classification on May 19, 2026, confirming that AI systems that score, rank, shortlist, or generate targeted job advertisements materially influence hiring outcomes and fall under EU AI Act Annex III; the guidance followed a Digital Omnibus political agreement deferring stand-alone high-risk enforcement to December 2, 2027.

- May 2026: Holistic AI released Programmable Controls for Continuous AI Governance, enabling enterprises to define and automate policy enforcement rules across their AI portfolios, with applications to HR bias monitoring; this followed its launch of Shadow AI Discovery for risk scoring and reconciliation of undisclosed AI deployments.

- April 2026: Credo AI joined the Coalition for Health AI (CHAI) Partner Program, extending its AI governance platform to healthcare workforce AI use cases, with plans to collaborate on standardized vendor AI assessments and agentic AI governance workflows for clinical decision support environments.

Global AI Bias Audit And Algorithmic Fairness In HR Market Report Scope

The AI Bias Audit and Algorithmic Fairness in the HR Market encompasses platforms and services that assess, monitor, and reduce bias in AI-driven HR decisions across recruitment, promotions, and compensation. These solutions leverage statistical tests, explainability models, and fairness metrics to achieve fair outcomes across diverse employee demographics. They seamlessly integrate into HR tech ecosystems, promoting responsible AI use. The market's expansion is fueled by heightened regulatory oversight, Diversity, Equity, and Inclusion (DEI) initiatives, and the growing adoption of AI in workforce decisions.

The AI Bias Audit and Algorithmic Fairness in HR Market Report is Segmented by Component (Software, and Services [Audit and Monitoring Services, and Advisory and Compliance Services]), HR Workflow (Candidate Screening and Ranking, Talent Sourcing and Matching, Internal Mobility and Promotion Analytics, Workforce Performance and Retention Analytics, HR Governance, Monitoring and Reporting, and Other HR Workflows), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services and Insurance, Healthcare and Life Sciences, Information Technology and Telecommunications, Manufacturing, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Audit and Monitoring Services |

| Advisory and Compliance Services |

| Candidate Screening and Ranking |

| Talent Sourcing and Matching |

| Internal Mobility and Promotion Analytics |

| Workforce Performance and Retention Analytics |

| HR Governance, Monitoring and Reporting |

| Other HR Workflows |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| Information Technology and Telecommunications |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | Audit and Monitoring Services | |

| Advisory and Compliance Services | ||

| By HR Workflow | Candidate Screening and Ranking | |

| Talent Sourcing and Matching | ||

| Internal Mobility and Promotion Analytics | ||

| Workforce Performance and Retention Analytics | ||

| HR Governance, Monitoring and Reporting | ||

| Other HR Workflows | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecommunications | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the AI bias audit and algorithmic fairness in HR market?

The market was valued at USD 403.43 million in 2025 and is forecast to reach USD 992.69 million by 2031, advancing at a 16.20% CAGR during 2026-2031.

What is driving spending on AI bias audits in HR?

Enforcement pressure is a core factor, especially where employers face audit, disclosure, and candidate notice rules tied to automated employment decision tools.

Which component leads revenue and which one is growing fastest?

Software led with a 67.31% share in 2025, while services is projected to record the fastest growth at a 19.84% CAGR through 2031.

Which HR workflow is attracting the most demand?

Candidate screening and ranking held the largest share at 36.49% in 2025, while HR governance, monitoring and reporting is projected to grow fastest at 18.23% through 2031.

Which region is leading and which one is expanding the quickest?

North America led with a 38.21% share in 2025, while Asia-Pacific is projected to post the fastest regional growth at an 18.79% CAGR through 2031.

Why are enterprises adopting continuous monitoring tools instead of one-time audits?

Annual reviews are often not enough once models drift or workflows change, so buyers are moving toward cloud and hybrid systems that support ongoing logging, monitoring, and governance.

Page last updated on: