AI Copilot For HR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 15.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

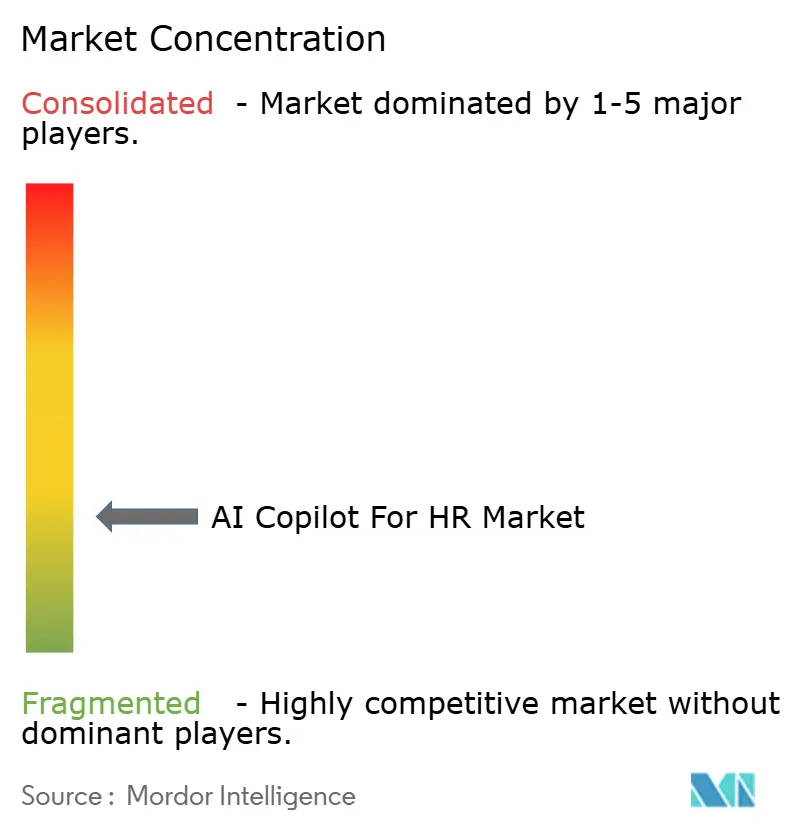

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Copilot For HR Market Analysis by Mordor Intelligence

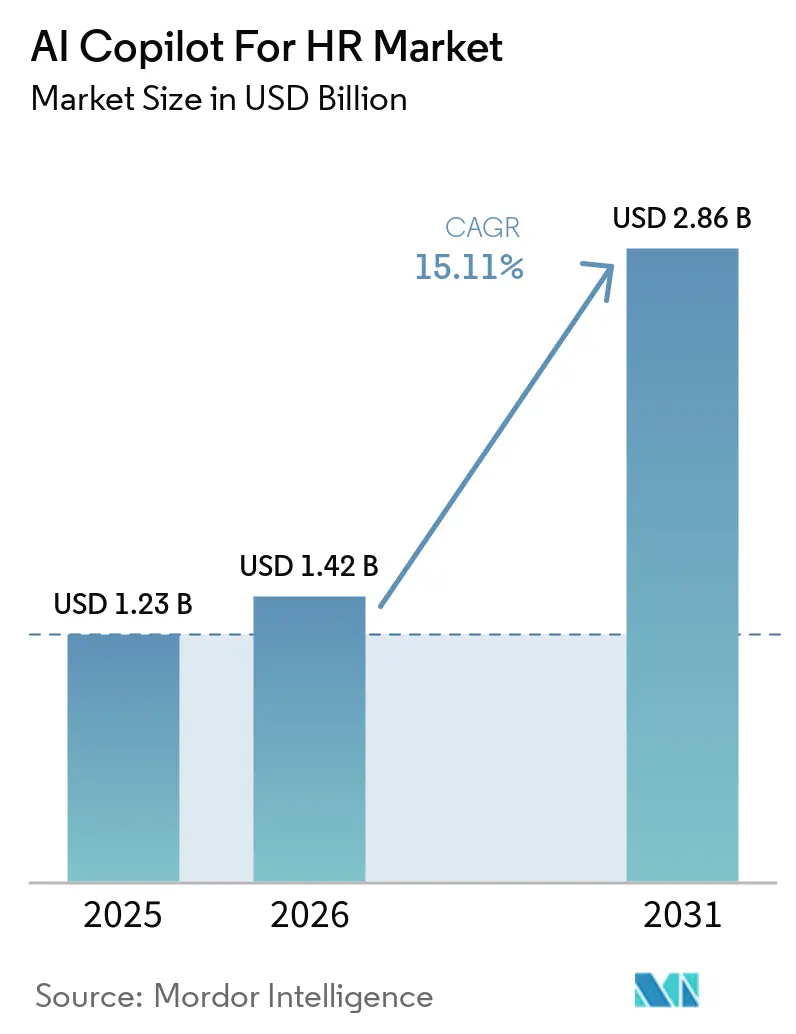

The AI copilot for HR market size is expected to grow from USD 1.23 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 2.86 billion by 2031 at 15.11% CAGR over 2026-2031. Growth in the AI copilot for HR market is being shaped by a broad shift from manual HR administration to software-led decision support across recruiting, service delivery, workforce planning, and employee support. Employers are facing heavier workloads, tighter hiring conditions, and stronger pressure to improve efficiency without expanding HR teams at the same pace. Buying patterns are also changing because organizations now want connected systems that can screen candidates, answer employee questions, support managers, and work inside existing HCM environments rather than stand-alone tools. Compliance, auditability, and data handling are becoming part of the core purchase decision, especially in regulated industries and cross-border deployments. Competition in the AI copilot for HR market is therefore moving beyond feature depth alone and toward platform fit, deployment flexibility, service capability, and proof of measurable operating value.

Key Report Takeaways

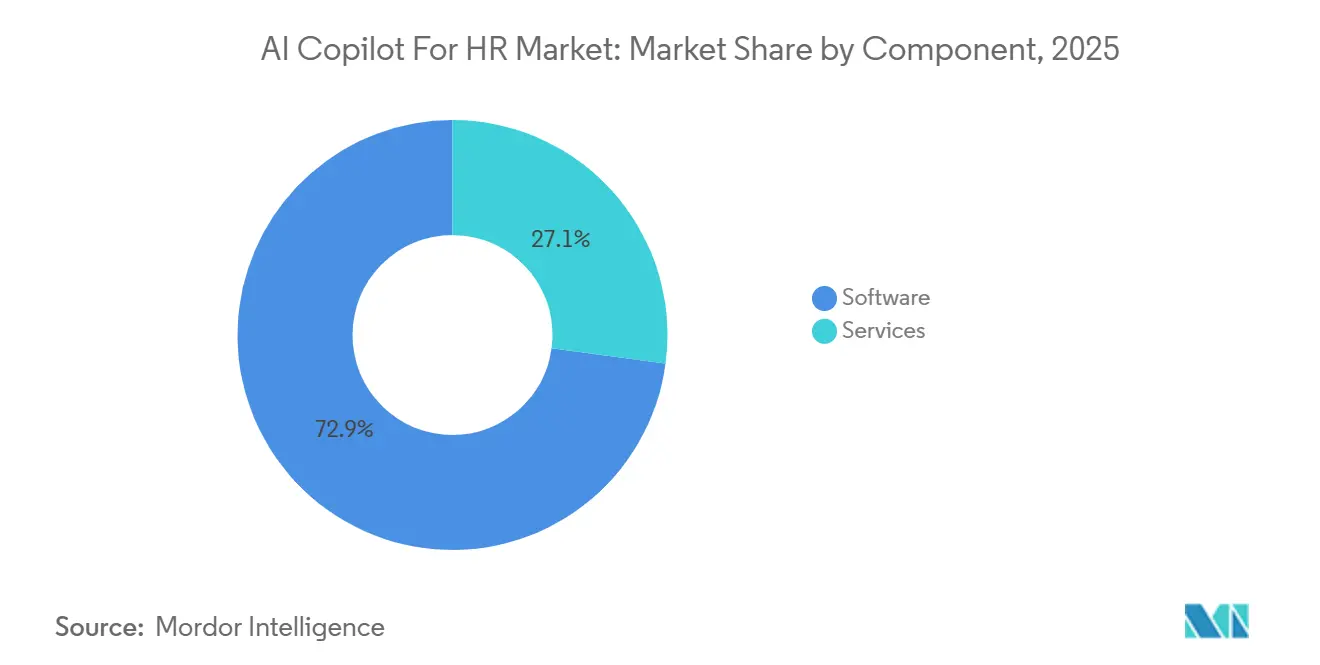

- By component, software accounted for 72.89% of the AI copilot for HR market in 2025, while services are projected to expand at a 17.04% CAGR through 2031.

- By application, recruitment and talent acquisition accounted for 31.28% share in 2025, while performance management is projected to grow at 15.99% CAGR through 2031.

- By deployment mode, cloud-based delivery held 67.21% share in 2025, while hybrid deployment is projected to expand at 16.78% CAGR through 2031.

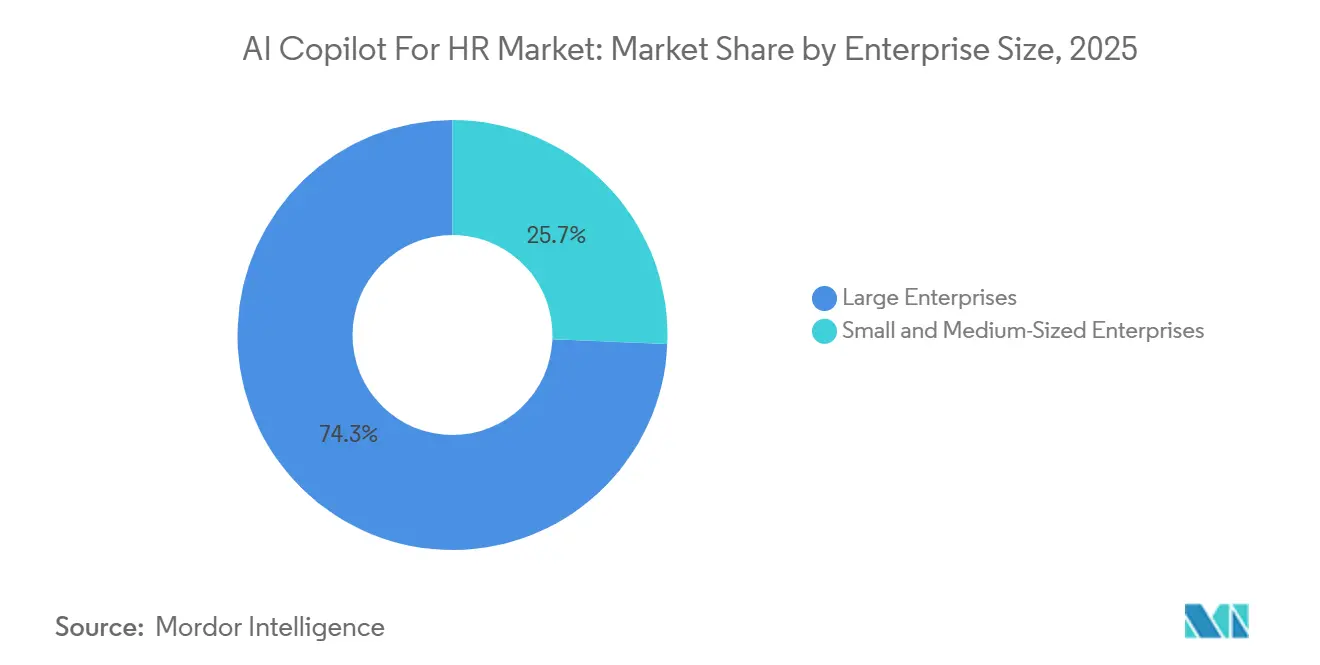

- By enterprise size, large enterprises held 74.33% share in 2025, while SMEs are projected to grow at 17.39% CAGR through 2031.

- By end-user industry, IT and telecommunications held 29.41% share in 2025, while BFSI is projected to expand at 15.65% CAGR through 2031.

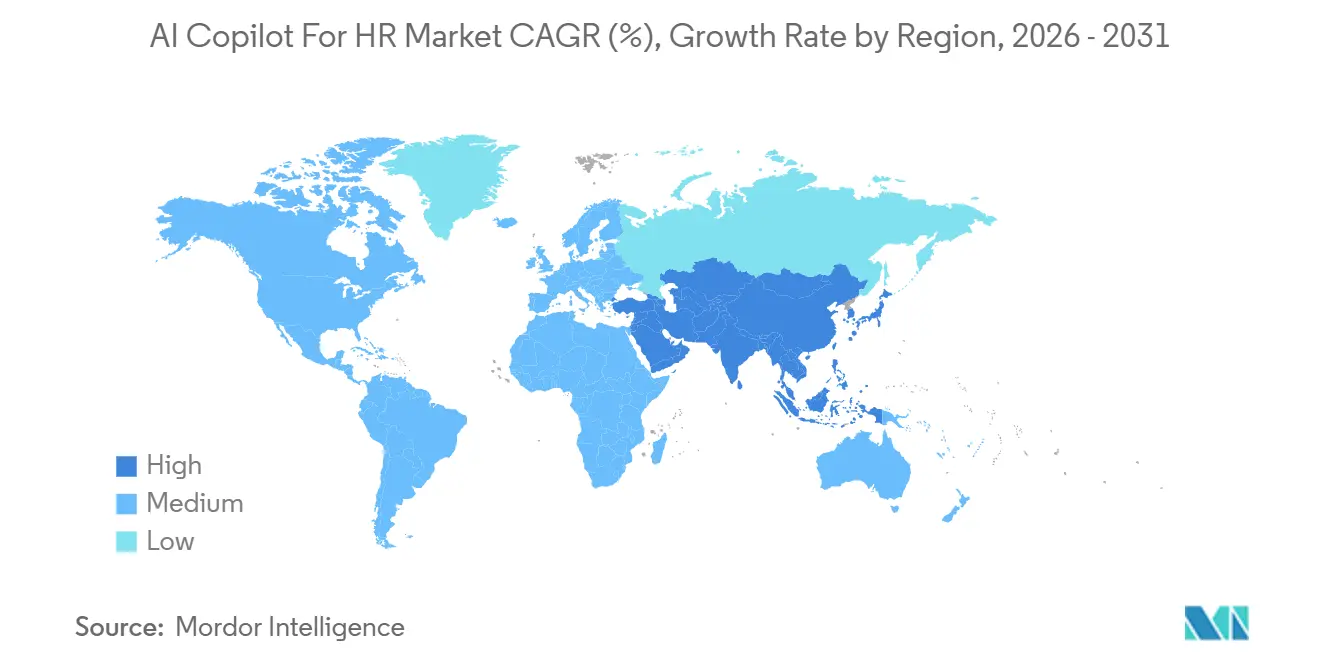

- By geography, North America held 36.55% of the AI copilot for HR market in 2025, while Asia-Pacific is projected to grow at 16.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Copilot For HR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recruitment-Volume Automation and Time-To-Hire Compression | +4.2% | Global, with peak impact in North America and APAC core markets | Short term (≤ 2 years) |

| Shift from HR Helpdesks to Employee Self-Service Copilots | +3.1% | Global, strongest uptake in North America and Europe | Short term (≤ 2 years) |

| Skills Intelligence, and Internal Mobility Orchestration | +2.5% | Global, with spill-over to Middle East, Africa, and Southeast Asia | Medium term (2-4 years) |

| Need for Multilingual Frontline Hiring and Support at Scale | +1.8% | APAC core, with spill-over to Middle East, Africa, and South America | Medium term (2-4 years) |

| Compliance-By-Design Demand as AI Employment Rules Tighten | +1.4% | North America and EU, with early gains in Australia and Singapore | Short term (≤ 2 years) |

| Workforce Data Layer Modernization Unlocking Embedded Copilots | +1.0% | Global, with early gains in the United States, the United Kingdom, and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recruitment-Volume Automation and Time-To-Hire Compression

Recruitment workflows are becoming harder to manage manually as generative tools enable candidates to produce and submit more applications in less time. Greenhouse said applications per recruiter had risen 412% since 2023, which shows how sharply screening pressure has increased for hiring teams. This pressure is pushing the AI copilot for HR market toward automated shortlisting, voice-led screening, interview scheduling, and candidate communication that can run with less recruiter intervention. The strongest demand is coming from roles where speed matters and recruiter bandwidth is limited, especially in frontline and hourly hiring. Employers are also looking for tools that can compress time-to-hire without weakening audit trails, structured evaluation, or candidate experience. Vendors that can connect screening, validation, and workflow orchestration inside existing recruiting systems are therefore gaining a clearer advantage.

Shift from HR Helpdesks to Employee Self-Service Copilots

The move from ticket-based HR support to conversational employee assistance is changing how organizations handle routine questions on payroll, policies, leave, and benefits. In October 2025, Interact Software and Leena AI introduced an agentic employee experience offering that enabled employees to access knowledge and complete actions across HRIS, ITSM, ERP, and CRM systems through a single interface. That model fits a broader pattern in the AI copilot for HR market, where buyers increasingly prefer front-end assistants that reduce service queues instead of adding more HR service headcount. These copilots also generate a steady stream of employee interaction data, helping employers spot recurring policy gaps, manager friction points, and service bottlenecks earlier. The value is not limited to cost control because response speed and consistency matter to employee trust as well. As a result, vendors are building self-service tools with stronger workflow depth, broader system reach, and clearer escalation paths to human review.

Skills Intelligence, and Internal Mobility Orchestration

Skills-led workforce management is becoming more important as employers try to redeploy talent before opening new requisitions. Gloat introduced its Agentic HR platform in March 2026, featuring a workforce context engine designed to match employees to internal opportunities, identify retention risk, and support redeployment within large enterprises. This is expanding the AI copilot for HR market beyond hiring and into the ongoing management of internal labor supply. Employers want these tools to do more than map skills because they also need help with succession, career movement, reskilling, and workforce visibility across business units. That creates demand for systems that can combine employee profiles, role requirements, learning pathways, and talent-marketplace logic within a single operating layer. Vendors that can turn workforce data into practical internal mobility actions are likely to strengthen their position over the forecast period.

Need for Multilingual Frontline Hiring and Support at Scale

Multilingual capability is becoming a core requirement in high-volume sectors such as retail, hospitality, logistics, manufacturing, and healthcare. Eightfold AI launched its AI Interviewer in October 2025, supporting 22+ languages, demonstrating that language coverage is becoming part of mainstream product design rather than a niche feature.[1]Eightfold AI, “Eightfold AI Launches AI Interviewer to Deliver Faster and More Equitable Hiring,” Eightfold AI, eightfold.ai Removing unnecessary qualification filters can expand candidate pools by 11.4x in India and 9.5x in Indonesia, which makes language-ready screening more valuable at scale. In the AI copilot for HR market, this pushes vendors to build interview, screening, and support tools that work across local languages and varied literacy levels. The need is strongest in countries where employers recruit across regional languages and labor pools outside large urban centers. Language coverage is therefore becoming a practical market differentiator tied to conversion, reach, and operational throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bias, Explainability, and Audit Exposure in Employment Decisions | -2.1% | Global, with the highest compliance burden in North America and the EU | Short term (≤ 2 years) |

| Sensitive HR Data Privacy and Cross-Border Governance Burdens | -1.8% | EU, APAC, and North America | Medium term (2-4 years) |

| Fragmented HR Data and Legacy HCM Integration Bottlenecks | -1.3% | Global, pronounced in Japan, China, South Korea, and large enterprises with multi-platform HCM stacks | Long term (≥ 4 years) |

| Entry-Level Hiring Distortion From AI-Generated Applications and Screening Noise | -0.8% | Global, concentrated in professional services, technology, and financial services verticals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Bias, Explainability, and Audit Exposure in Employment Decisions

Bias risk remains one of the main brakes on wider deployment because employment decisions carry direct legal, reputational, and governance consequences. Colorado’s SB 26-189 added post-decision transparency requirements in May 2026, indicating that regulatory expectations are moving closer to the actual points of hiring and promotion decisions. This means buyers in the AI copilot for HR market are asking harder questions about audit logs, model documentation, review controls, and candidate-level explanation. Vendors are responding by making responsible AI credentials more visible, including through formal governance programs and support for external standards. Eightfold AI positioned its interview process to comply with NYC Local Law 144, Illinois BIPA, and ISO/IEC 42001, demonstrating how product trust is becoming part of commercial competition. The result is a market where explainability is no longer a legal footnote but a direct factor in procurement and rollout speed.

Sensitive HR Data Privacy and Cross-Border Governance Burdens

HR data brings together personal, financial, behavioral, and employment records, which makes it one of the hardest enterprise data domains to move across borders. Eversheds Sutherland noted that the EU AI Act classifies HR decision-support systems as high-risk under Annex III from August 2, 2026, which adds another governance layer on top of existing privacy requirements. APAC is not moving under one single rulebook, with stronger compliance expectations in markets such as China, Japan, South Korea, Singapore, and Australia shaping how vendors design local deployments. In the AI copilot for HR market, this makes regional hosting, data residency options, and configurable governance controls more important than standard cloud convenience alone. Enterprises with multinational workforces often need different approval, storage, and review models across the same deployment. These burdens do not stop adoption, but they do lengthen buying cycles and give vendors with mature compliance infrastructure a greater advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Narrows Software's Lead

Software accounted for 72.89% share of the AI copilot for HR market size in 2025, which shows how strongly buyers still prefer platform-led deployments over stand-alone advisory models. The largest revenue pool remains tied to core copilot platforms, talent intelligence engines, and conversational agents that sit inside recruiting and HCM workflows. This part of the market benefits from enterprise demand for repeatable automation, centralized administration, and easier user adoption inside familiar systems. Product vendors are also strengthening their position through tighter workflow integration, such as Eightfold AI’s connection with Oracle Fusion Cloud Recruiting, which keeps autonomous interviewing inside established recruiting environments.

Services are projected to expand at 17.04% CAGR through 2031, making them the fastest-growing component in the AI copilot for HR market. The rise comes from the practical difficulty of connecting copilots to legacy ATS, payroll, HR service, and workforce data systems without ongoing technical and change support. Enterprises also need help with use-case design, prompt governance, rollout planning, employee training, and post-launch optimization to keep service demand active after the initial implementation. Gloat’s 2026 platform launch showed how wide the integration surface has become, with connections across Microsoft 365 Copilot, Teams, Slack, Google Chat, Workday, SAP SuccessFactors, and Oracle, and that complexity supports a larger services role across the AI copilot for HR industry.

By Application: Performance Management Gains on Talent Acquisition's Structural Lead

Recruitment and talent acquisition accounted for 31.28% of the AI copilot for HR market size in 2025, reflecting that hiring remains the clearest entry point for automation and measurable returns. Employers can see the value quickly when tools improve screening speed, reduce manual scheduling, and widen recruiter coverage across large applicant pools. Greenhouse linked its Ezra AI Labs acquisition to a 412% increase in applications per recruiter since 2023, which shows why the recruiting stack remains the largest application area. This keeps recruitment at the center of the AI copilot for HR market because buying decisions are often easiest to justify when time-to-fill and recruiter productivity can be tracked directly.

Performance management is projected to advance at 15.99% CAGR through 2031, making it the fastest-growing application in the AI copilot for HR market. Growth here is tied to demand for continuous feedback, calibration support, manager guidance, and more consistent evaluation processes across distributed teams. This use case is moving forward because enterprises want better visibility into goals, capability gaps, and development actions without depending only on periodic review cycles. Learning and development, onboarding, workforce planning, and HR administration continue to hold the rest of the application mix, and many deployments now connect these functions so hiring, performance, and development data can inform one another. Over time, this broader workflow connection should make application expansion a major source of revenue depth across the AI copilot for HR industry.

By Deployment Mode: Hybrid Architectures Emerge From Regulated Sector Pressure

Cloud-based deployment held a 67.21% share in 2025, confirming that most buyers still favor faster rollouts, centralized updates, and easier integration over locally managed infrastructure. Cloud delivery also aligns with the release cycle of AI copilots, as model updates, workflow changes, and security patches can be managed more consistently across distributed user bases. For many organizations, cloud deployment shortens implementation time and lowers the burden on internal IT teams that already support multiple HR systems. This pattern keeps cloud as the default path in the AI copilot for HR market, especially for recruiting, employee support, and broader HCM augmentation.

Hybrid deployment is projected to grow at 16.78% CAGR through 2031, making it the fastest-growing architecture in the AI copilot for HR market. The main reason is that regulated employers increasingly want to keep sensitive employee records in private or on-premises environments while still using cloud-based inference, orchestration, or analytics. The EU AI Act’s treatment of employment AI as high-risk supports this shift because governance expectations are rising even where cloud tools remain operationally attractive. On-premises deployments therefore continue to hold a role in government, defense, and tightly controlled financial environments, while hybrid models give the AI copilot for HR industry a more practical route to balance speed with data control.

By Enterprise Size: SME Velocity Challenges Large Enterprise Incumbency

Large enterprises held a 74.33% share in 2025, reflecting their budget capacity, larger workforce footprints, and greater need to standardize HR operations across functions and geographies. These organizations usually have sufficient scale to justify multi-workflow rollouts that cover recruiting, employee services, mobility, and manager support in a single program. Microsoft WorkLab demonstrated this scale at BNY Mellon, where AI deployment has extended across tens of thousands of employees and is supported by a large technology investment base.[2]Microsoft WorkLab, “The Making of a Frontier Firm, How AI Is Redesigning Work at BNY,” Microsoft, microsoft.com In the AI copilot for HR market, large organizations still set the pace for early adoption because they can more easily absorb integration, governance, and change-management costs.

SMEs are projected to expand at 17.39% CAGR through 2031, making them the fastest-growing enterprise segment in the AI copilot for HR market. Growth is being supported by lower entry barriers, easier cloud access, modular purchasing, and pricing structures that reduce the need for large upfront commitments. Smaller employers are also more willing to adopt single-workflow copilots first, especially in screening, scheduling, onboarding, and employee support, then add features once outcomes are visible. This gives the AI copilot for HR industry a second growth lane beyond large enterprise transformation programs, with SMEs adopting faster where implementation risk and budget exposure stay controlled.

By End-User Industry: BFSI's Skills Crisis Accelerates Copilot Investment

IT and telecommunications held 29.41% share in 2025, giving the sector the largest position within the AI copilot for HR market. The sector’s lead comes from frequent hiring, distributed technical teams, high demand for scarce skills, and a greater comfort level with API-led software integration. These employers are often early adopters because they both buy HR AI tools and compete for the same digital talent that other sectors need. That dual pressure makes recruiting, internal mobility, and workforce visibility especially important in IT and telecommunications.

BFSI is projected to expand at 15.65% CAGR through 2031, making it the fastest-growing vertical in the AI copilot for HR market. The investment case is strong because financial institutions need better support for compliance-heavy roles, internal movement, skills validation, and employee service across complex operating structures. BFSI buyers also tend to insist on governance, documentation, and workflow control before scaling new systems, which supports higher-value deployments rather than narrow pilot activity. As a result, BFSI is becoming a key growth engine for the AI copilot for HR industry, while healthcare, retail, manufacturing, government, and other sectors continue to widen the market base with role-specific use cases.

Geography Analysis

North America accounted for 36.55% share in 2025, giving it the largest regional position in the AI copilot for HR market. The region benefits from a deep HR technology ecosystem, strong enterprise software spending, and persistent hiring pressure in the United States. The Bureau of Labor Statistics reported 6.9 million open positions against 5.6 million monthly hires in early 2026, which kept recruiting efficiency high on the corporate agenda.[3]Bureau of Labor Statistics, “Job Openings and Labor Turnover Survey (JOLTS),” Bureau of Labor Statistics, bls.govThe United States remains the main demand center, while Canada and Mexico are also seeing stronger interest, with bilingual and frontline hiring needs rising. State-level rules are adding another layer of buyer scrutiny, with requirements in places such as Colorado increasing attention on transparency and review practices.

Europe remains an important region for the AI copilot for HR market, but adoption is moving alongside tighter governance and stronger employee protection frameworks. The EU AI Act classifies employment decision-support tools as high risk from August 2, 2026, underscoring the importance of documentation, conformity processes, and human oversight. This makes Europe a market where explainability, regional hosting, and deployment controls can matter as much as workflow automation itself. Germany, the United Kingdom, and France continue to shape regional demand, but buyers across the region are moving more carefully when employee monitoring, decision support, or cross-border data use is involved.

Asia-Pacific is projected to grow at 16.41% CAGR through 2031, making it the fastest-growing regional slice of the AI copilot for HR market size. India is the fastest-growing country market, supported by the expansion of global capability centers and a 12.2% projected CAGR through 2031. The same source noted that removing unnecessary qualification filters can expand candidate pools by 11.4x in India and 9.5x in Indonesia, which strengthens the case for AI-led screening and multilingual hiring tools. China remains important because candidate data governance and audit readiness are becoming more central to deployment design, while Japan and South Korea continue to face labor scarcity that supports automation. South America, the Middle East, and Africa remain smaller in current revenue terms, but adoption is expanding as mobile-first HR platforms, national AI programs, and local-language capabilities improve deployment feasibility.

Competitive Landscape

The AI copilot for HR market is moderately fragmented, with pure-play specialists competing against embedded AI capabilities from major HCM suite vendors. Large enterprise buyers often compare point solutions from companies such as Phenom, Eightfold AI, HireVue, Beamery, Gloat, and Visier with broader platforms from Workday, SAP SuccessFactors, and Oracle. This creates a market where incumbents benefit from existing procurement relationships, while specialists compete on speed, workflow depth, and product focus. SAP reinforced its broader AI position in May 2026 by announcing the acquisition of Prior Labs and a EUR 1 billion (USD 1.13 billion) 4-year plan to build a frontier AI lab in Europe. Oracle’s ecosystem has also become a more active battleground, with Eightfold AI integrating agentic interviewing into Oracle Fusion Cloud Recruiting in May 2026.

Pure-play vendors are responding with acquisitions, platform expansion, and distribution partnerships. Phenom completed 3 acquisitions in a short span across Included AI, Be Applied, and Plum, which extended its coverage from people analytics to structured hiring and psychometric assessment. Gloat took a different path by bringing its agentic HR capabilities into the Microsoft Agent Store and Microsoft Teams, which gave it access to a distribution channel already embedded in enterprise work patterns. Greenhouse also moved to strengthen voice-led hiring automation through its acquisition of Ezra AI Labs in May 2026. These moves show that the AI copilot for HR market is no longer defined only by feature launches and is now being shaped by portfolio breadth, workflow control, and access to enterprise channels.

The next competitive gap is forming around governance-grade explainability, regional compliance support, and tools built for deskless and frontline workers. Eightfold’s TalentForge launch in May 2026 showed how vendors are positioning themselves as infrastructure layers on which enterprises can build their own HR applications, rather than buying fixed-use-case solutions. Beamery’s 2025 integration with LinkedIn CRM Connect pointed to another competitive route, where connected skills and candidate data ecosystems improve workflow value without requiring a full suite replacement. Because buyers still have many credible options across suites and specialists, the AI copilot for HR market remains active and contested rather than concentrated around a small group of dominant vendors.

AI Copilot For HR Industry Leaders

Phenom People, Inc.

Eightfold AI Inc.

Beamery, Inc.

Avature Limited

Paradox, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge, a platform enabling enterprises to build proprietary HR applications on Eightfold's Talent Intelligence layer, and simultaneously introduced Workforce Readiness, a tool providing CHROs with real-time AI adoption and productivity analytics across the enterprise with personalized development plans via a coaching agent.

- May 2026: SAP announced a definitive agreement to acquire Prior Labs, a pioneer in Tabular Foundation Models, and committed to investing over EUR 1 billion (USD 1.13 billion) over 4 years to establish a frontier AI lab in Europe. The acquisition targets integration into the agentic layer of Joule, SAP's AI copilot, with direct implications for SAP SuccessFactors HR workflows.

- May 2026: Eightfold AI announced the integration of its agentic AI interviewer with Oracle Fusion Cloud Recruiting, enabling Oracle's enterprise recruiting customers to access autonomous, skills-based interviewing capabilities within existing workflows using Oracle Universal Cloud Credits.

- May 2026: Greenhouse entered a definitive agreement to acquire Ezra AI Labs, a voice AI interviewing platform, to address the 412% surge in applications per recruiter since 2023. The acquisition integrates voice AI with structured hiring workflows and Greenhouse's monthly independent bias auditing via Warden AI under its ISO 42001 certification.

Global AI Copilot For HR Market Report Scope

The AI Copilot for HR Market encompasses AI-powered assistant platforms that are reshaping HR operations by automating tasks and offering insights. These copilots engage with HR users, employees, and managers, streamlining processes like recruitment support and employee queries. Harnessing the power of natural language processing and machine learning, this market signifies a shift in HR systems towards conversational, task-oriented AI. The goal is to boost productivity, refine decision-making, and elevate the overall employee experience through intelligent automation.

The AI Copilot for HR Market Report is Segmented by Component (Software [Core AI Copilot Platforms, Talent Intelligence and Matching Engines, Conversational Agents and Workflow Orchestration, and Analytics and Insights Modules], and Services [Implementation and Integration Services, Training and Change Management Services, and Managed and Optimization Services]), Application (Recruitment and Talent Acquisition, Employee Onboarding and Engagement, Performance Management, Learning and Development, Workforce Planning and Analytics, Payroll, Benefits and HR Administration, and Other Applications), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Retail and E-commerce, Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | Core AI Copilot Platforms |

| Talent Intelligence and Matching Engines | |

| Conversational Agents and Workflow Orchestration | |

| Analytics and Insights Modules | |

| Services | Implementation and Integration Services |

| Training and Change Management Services | |

| Managed and Optimization Services |

| Recruitment and Talent Acquisition |

| Employee Onboarding and Engagement |

| Performance Management |

| Learning and Development |

| Workforce Planning and Analytics |

| Payroll, Benefits and HR Administration |

| Other Applications |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| IT and Telecommunications |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | Core AI Copilot Platforms |

| Talent Intelligence and Matching Engines | ||

| Conversational Agents and Workflow Orchestration | ||

| Analytics and Insights Modules | ||

| Services | Implementation and Integration Services | |

| Training and Change Management Services | ||

| Managed and Optimization Services | ||

| By Application | Recruitment and Talent Acquisition | |

| Employee Onboarding and Engagement | ||

| Performance Management | ||

| Learning and Development | ||

| Workforce Planning and Analytics | ||

| Payroll, Benefits and HR Administration | ||

| Other Applications | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-user Industry | IT and Telecommunications | |

| Banking, Financial Services, and Insurance | ||

| Healthcare and Life Sciences | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the AI copilot for HR market?

The AI copilot for HR market was worth USD 1.23 billion in 2025, reached USD 1.42 billion in 2026, and is forecast to hit USD 2.86 billion by 2031 at a 15.11% CAGR.

Which application leads current demand?

Recruitment and talent acquisition led with 31.28% share in 2025 because employers can measure gains in screening speed, recruiter productivity, and hiring workflow efficiency more quickly than in most other use cases.

Which deployment model is growing the fastest?

Hybrid deployment is projected to grow at 16.78% CAGR through 2031 as employers try to balance cloud flexibility with tighter control over sensitive HR records and local compliance demands.

Why are SMEs becoming more active buyers?

SMEs are projected to grow at 17.39% CAGR because cloud delivery, modular purchases, and lower entry costs make adoption easier without large upfront transformation programs.

Which region offers the strongest growth outlook?

Asia-Pacific is the fastest-growing region at 16.41% CAGR, supported by expanding candidate pools, multilingual hiring needs, and strong adoption momentum in markets such as India, China, Japan, and South Korea.

What is the biggest challenge holding wider adoption back?

Bias risk, explainability, and data governance remain the main barriers because employers need clearer audit trails, transparency controls, and regional compliance coverage before scaling AI-led HR decisions.

Page last updated on: