AI In Agriculture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 8.39 Billion |

| Growth Rate (2026 - 2031) | 21.96% CAGR |

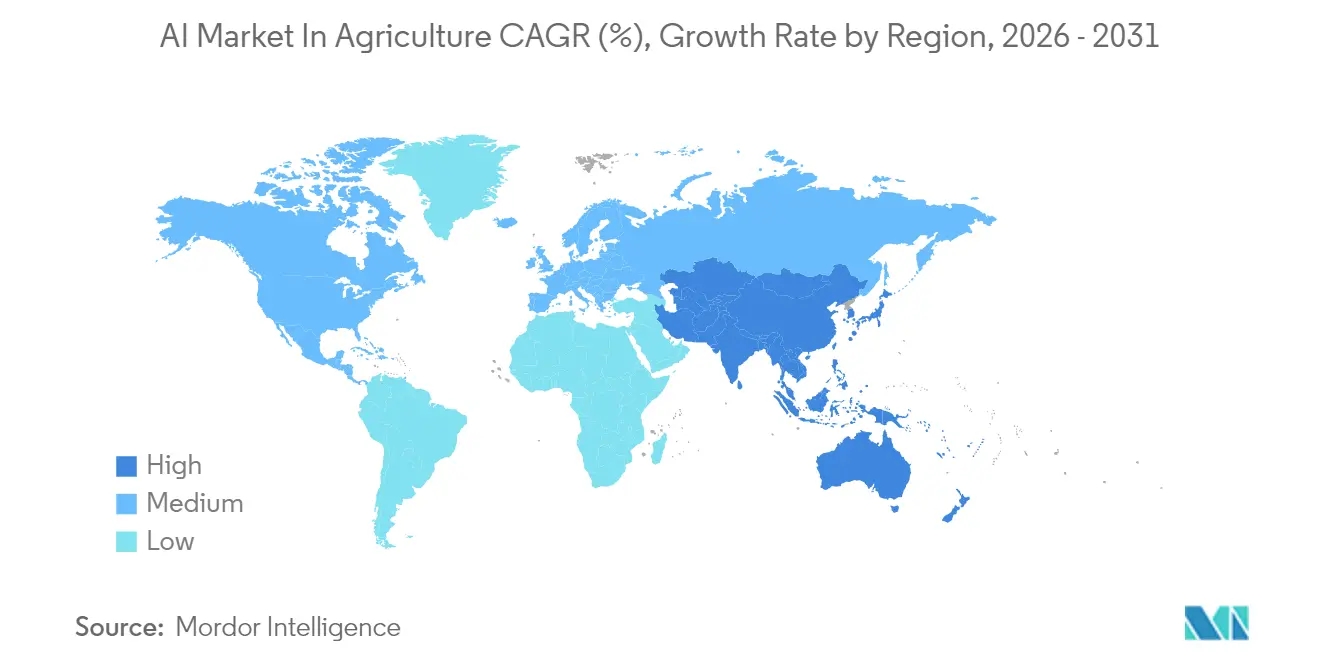

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

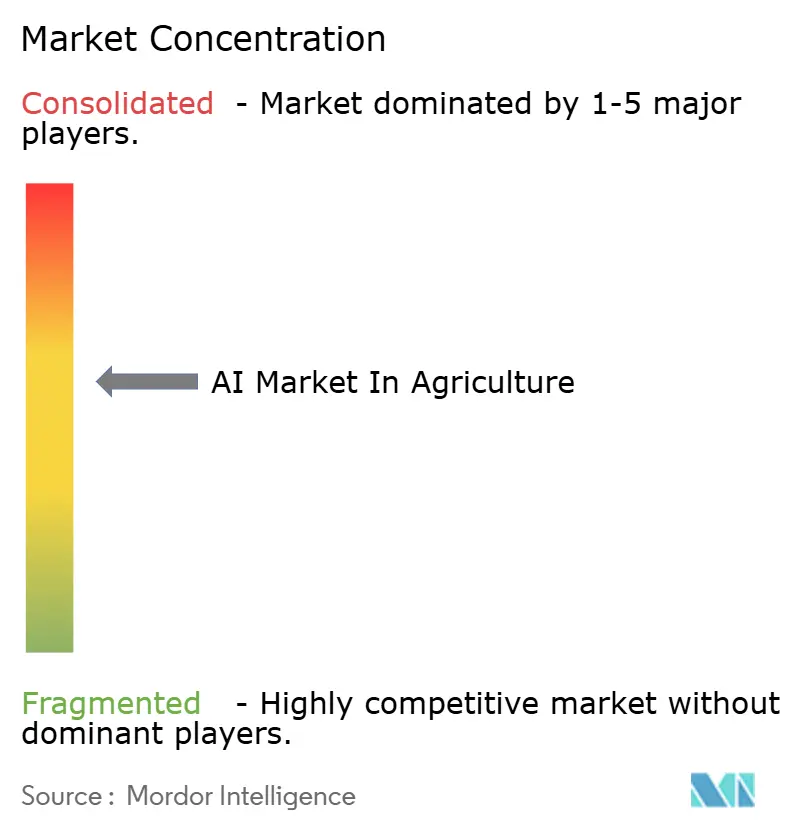

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Agriculture Market Analysis by Mordor Intelligence

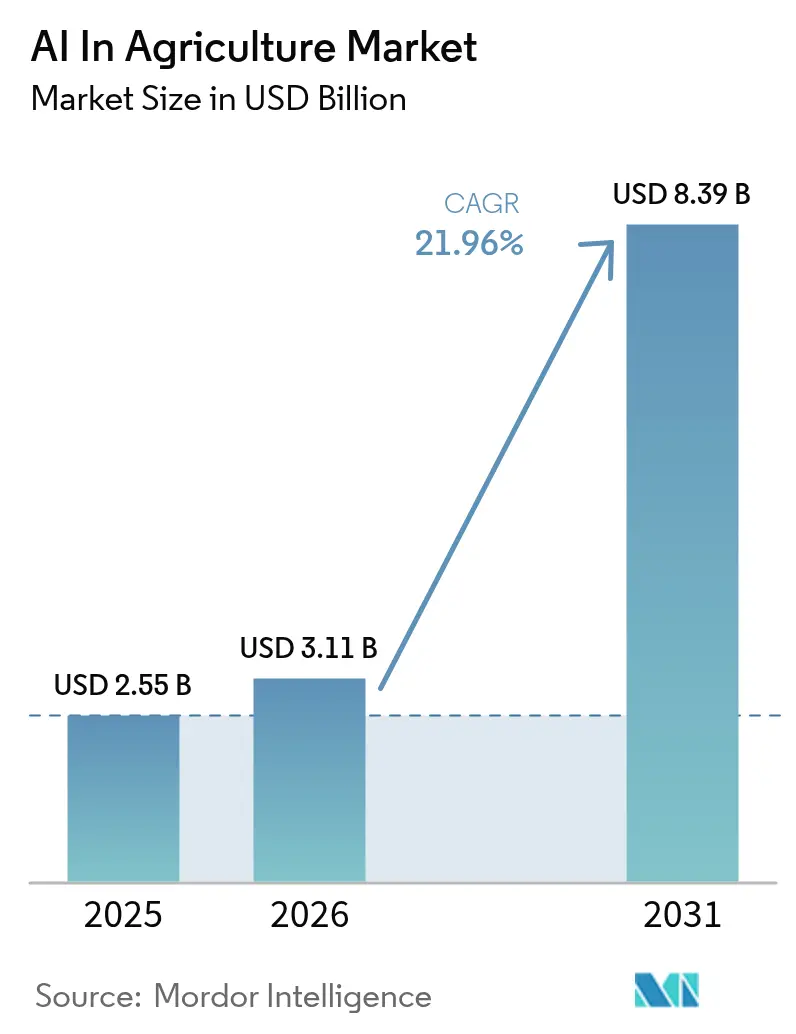

The AI in agriculture market size is expected to grow from USD 2.43 billion in 2025 to USD 3.11 billion in 2026 and is forecast to reach USD 8.39 billion by 2031 at a 21.96% CAGR over 2026-2031. Robust cloud connectivity, falling edge-AI hardware costs, and stringent sustainability mandates are converting algorithmic decision-making from an optional pilot into a routine line item for row-crop, horticulture, and livestock operations. Growers increasingly monetize data streams by feeding sensor, drone, and satellite observations into machine-learning pipelines that prescribe variable-rate inputs, trimming fertilizer waste by double digits while raising yields. Affordable AI-as-a-Service pricing is removing capital barriers for cooperatives in Latin America and Africa, while 5G open-RAN backhaul is giving autonomous sprayers and weeding robots sub-meter positional accuracy without additional base-station hardware. Supply-side fragmentation persists, yet this very diversity of sensors, software, and service providers is widening the solution catalogue available to specialty-crop and controlled-environment operators.

Key Report Takeaways

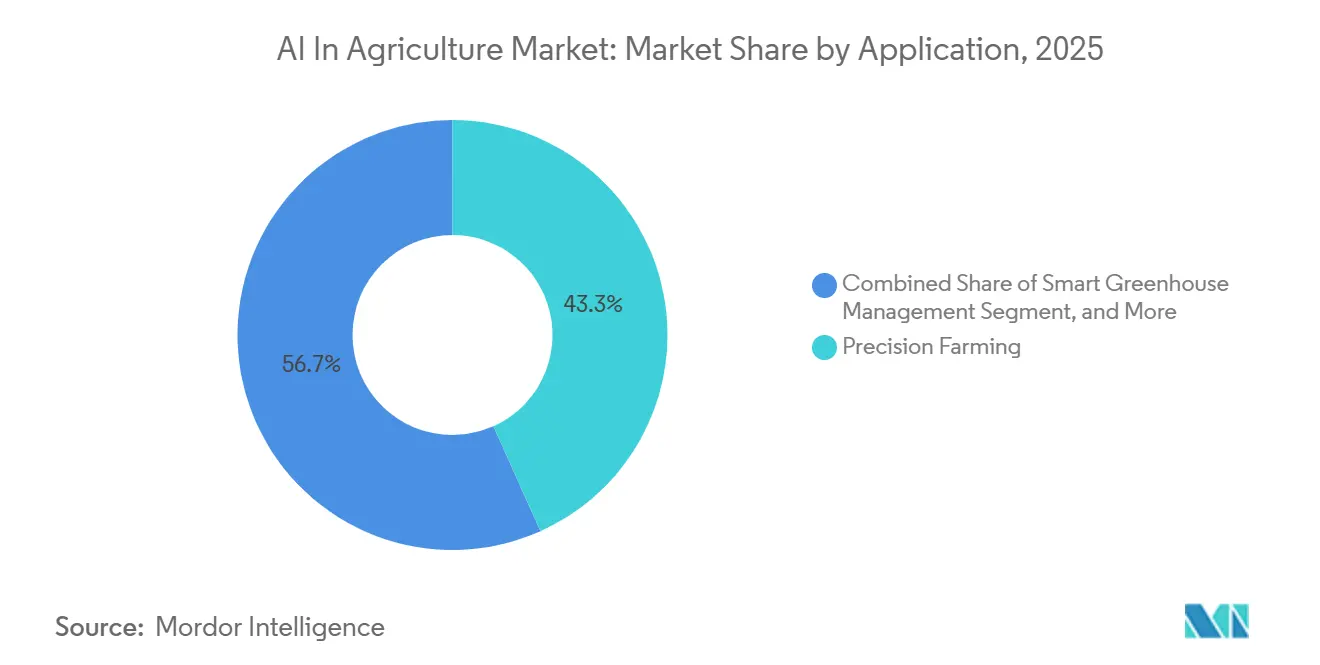

- By application, precision farming led with 43.29% revenue share in 2025; smart greenhouse management is projected to expand at a 22.47% CAGR through 2031.

- By technology, machine learning held 48.19% of 2025 spending, whereas computer vision is forecast to advance at a 22.68% CAGR between 2026-2031.

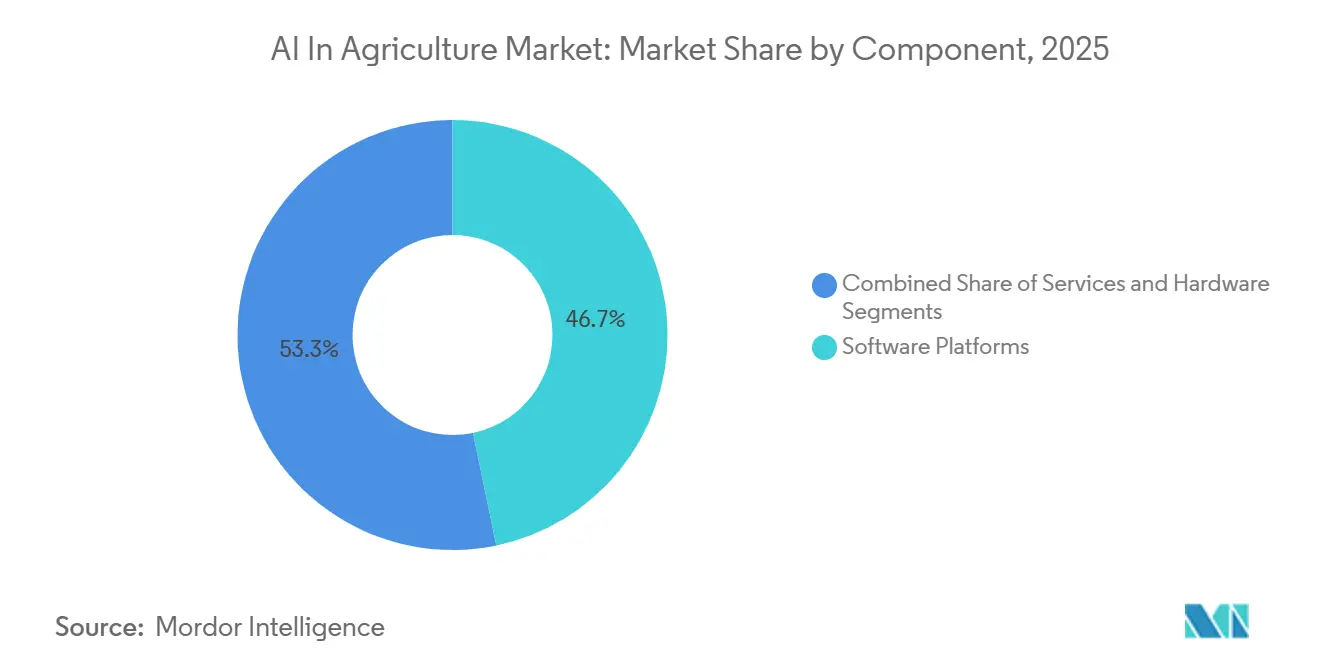

- By component, software platforms accounted for 46.73% revenue share in 2025; services are poised for the fastest growth, rising at a 22.91% CAGR to 2031.

- By deployment mode, cloud deployments captured 59.68% share in 2025, while hybrid architectures are expected to grow at a 22.96% CAGR over 2026-2031.

- By geography, North America represented 38.91% of 2025 sales, but Asia-Pacific is projected to record the highest regional CAGR at 22.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Precision Agriculture Platforms | +4.20% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of High-Resolution Drone and Satellite Imagery Services | +3.80% | Global, accelerating in Asia-Pacific and South America | Medium term (2-4 years) |

| Government Digital-Farming Subsidies and Mandates | +3.50% | North America, Europe, China, India | Short term (≤ 2 years) |

| Affordable Cloud-Based AI-as-a-Service Offerings | +3.10% | Global, with highest uptake in Asia-Pacific and Africa | Short term (≤ 2 years) |

| On-Farm GenAI Copilots Reducing Agronomist Field Visits | +2.90% | North America, Europe, Australia | Medium term (2-4 years) |

| 5G Open-RAN Sub-Meter Positioning for Autonomous Robots | +2.70% | North America, Europe, China, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Precision Agriculture Platforms

Deere and Company embedded machine-learning algorithms into its Operations Center in 2025, allowing the platform to ingest multi-year yield maps and soil conductivity readings, then automatically generate seeding prescriptions that trimmed seed outlays by 8-12% for early adopters.[1]John Deere, “Operations Center Overview,” DEERE.COM Trimble followed in early 2026 by layering generative-AI report-writing tools onto its Ag Software suite, letting farm managers brief financiers without manually compiling dashboards.[2]Trimble Inc., “Ag Software Suite Enhancements,” AGRICULTURE.TRIMBLE.COM Carbon-accounting modules are now standard add-ons because protocols such as Verra VM0042 require plot-level quantification of sequestration before issuing credits.[3]Verra, “VM0042 Methodology for Improved Agricultural Land Management,” VERRA.ORG As growers trade verified carbon credits, they reinvest proceeds into additional sensors, reinforcing data network effects. The result is a flywheel in which platform usage deepens each season, making switching increasingly costly.

Expansion of High-Resolution Drone and Satellite Imagery Services

PrecisionHawk launched a 2025 service tier that fuses drone imagery with Sentinel-1 synthetic-aperture radar, providing all-weather soil-moisture and biomass maps.[4]PrecisionHawk, “Multi-Sensor Crop Intelligence,” PRECISIONHAWK.COM Aerobotics deployed computer-vision models in 2026 to count individual citrus fruit, enabling packers to lock forward contracts six weeks earlier than before. Planet Labs’ SuperDove constellation now revisits every field daily at 3-meter resolution, giving agronomists near-real-time feedback for double-cropping systems. Such temporal density compresses decision cycles and minimizes yield penalties caused by timing errors.

Government Digital-Farming Subsidies and Mandates

The United States Department of Agriculture disbursed USD 3.1 billion under the Climate-Smart Commodities initiative in 2025, directing 40% of funds toward AI-enabled nutrient management for underserved producers. Europe’s Common Agricultural Policy requires that at least 35% of rural-development budgets finance precision-farming investments, accelerating sensor uptake across France and Germany. China’s Ministry of Agriculture committed to 200 smart-farming zones by 2027, each outfitted with IoT sensors and edge-AI gateways. India’s Kisan Suvidha app delivers AI-generated pest and irrigation advisories to 50 million growers, dramatically widening the advisory footprint. In effect, compliance is converting AI from a discretionary spend into a ticket-to-play.

Affordable Cloud-Based AI-as-a-Service Offerings

Microsoft Azure Data Manager for Agriculture prices pre-trained yield-prediction models at under USD 0.10 per hectare per season, a level workable for smallholder cooperatives. IBM integrated large-language models into its Watson Decision Platform in 2025, translating research papers into plain-language, plot-specific guidance. AWS SageMaker Geospatial bundles satellite-imagery preprocessing with model-training pipelines, cutting time-to-insight from weeks to hours for agribusinesses. Consumption-based billing eliminates the need for capex on GPU clusters, a decisive advantage in regions where annual farm income is below USD 5,000.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Agronomic Data Standards | -2.10% | Global, most acute in Asia-Pacific and Africa | Medium term (2-4 years) |

| High Upfront Cost of Sensors and Robotics for Smallholders | -1.90% | Asia-Pacific, Africa, South America | Short term (≤ 2 years) |

| Limited AI-Ready Agronomic Datasets and Privacy Hurdles | -1.60% | Global, with regulatory complexity highest in Europe | Medium term (2-4 years) |

| Slow Soil-Carbon Credit Verification Cycles | -1.30% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Agronomic Data Standards

Only 30% of farm-management software vendors had adopted AgGateway’s ADAPT data-exchange framework by 2025, forcing growers to reconcile incompatible file formats when switching suppliers. Soil taxonomies diverge; the USDA recognizes 12 soil orders, while the World Reference Base lists 32, confounding model portability. Weather-station protocols and pest nomenclatures vary, degrading forecast accuracy when datasets are pooled internationally. Vendors must build and maintain regional models, inflating development costs and delaying feature launches.

High Upfront Cost of Sensors and Robotics for Smallholders

A basic sensor suite costs USD 800-1,200 per field, and an autonomous weeding robot exceeds USD 30,000, figures many two-hectare farms in India and Sub-Saharan Africa cannot finance. Commercial banks view AI hardware as high-risk collateral, and micro-finance institutions rarely underwrite technology leases. CropX offers a sensor-as-a-service contract at USD 18-25 per hectare per season, yet adoption among smallholders was below 5% in 2025. The resulting digital divide slows the data-network effects needed to refine localized models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Smart Greenhouses Outpace Row-Crop Fields

Precision farming held the largest AI in agriculture market share at 43.29% in 2025, reflecting widespread variable-rate equipment on corn and soybean acres. Smart greenhouse management, however, is projected to lead application growth, expanding at 22.47% through 2031. Intelligent Growth Solutions’ generative-AI copilot fine-tunes CO₂ levels and LED spectra every few minutes, enabling vertical farms to cut energy use by 18% without yield loss. Livestock monitoring is gaining velocity as computer-vision systems flag lameness and calving risks days in advance, reducing vet costs and mortality. Drone analytics maintains a mid-teens position but can rise once regulators enable beyond-visual-line-of-sight flights.

Dense greenhouse datasets sensor readings every five minutes across dozens of variables accelerate model iteration, whereas open-field crops produce sparser data, slowing algorithm refinement. Certifications such as GlobalGAP are beginning to require AI-enabled traceability, nudging post-harvest optimization platforms into mainstream budgets. As a result, the AI in agriculture market size for controlled-environment applications is on track to close part of the gap with mainstream row crops by 2031.

By Technology: Camera-Centric Growth Surges

Machine learning commanded 48.19% of 2025 spending, anchoring the broader AI in agriculture market. Computer vision, though smaller, is forecast to expand at 22.68% over 2026-2031, outpacing other technologies as drone fleets and edge processors proliferate. Deere’s See and Spray system uses convolutional networks to differentiate crops from weeds at 20 frames per second, cutting herbicide use by up to 90%. Taranis captures sub-millimeter imagery to spot early fungal lesions, enabling fungicide precision that lowers chemical bills by 30-40%.

Edge-inference chips such as NVIDIA Jetson Orin and Google Coral now retail below USD 200, allowing real-time processing on sprayers without cloud latency. European AI-Act proposals that rate some agricultural systems as “limited risk” could tilt demand toward interpretable algorithms, adding a regional flavour to global technology splits. In numerical terms, the computer-vision segment’s share of AI in agriculture market size is projected to climb steadily, even as machine learning retains core workload dominance.

By Component: Services Bridge the Skills Gap

Software platforms captured the highest AI in agriculture market share among components at 46.73% in 2025, led by subscription bundles from Bayer Climate FieldView and Trimble. Services consulting, integration, and support are projected to grow fastest, registering a 22.91% CAGR to 2031, as growers struggle to harmonize legacy SCADA assets with cloud-native stacks. CNH Industrial’s precision team reported that professional-services revenue rose 35% year-over-year in 2025 as customers demanded custom API bridges between Slingshot and weather-data feeds.

Hardware growth remains steady but constrained by long replacement cycles for tractors and combines. Vendors are embedding intelligence at the edge to reduce integration pain; Topcon’s 2026 tractor guidance fuses GPS and computer vision on board, sustaining sub-2-centimeter accuracy without cellular links. Over time, turnkey hardware may slow services revenue, yet for now, integrators capture value as farms balance agronomy and data engineering skill sets.

By Deployment Mode: Hybrid Architectures Gain Favor

Cloud deployments dominated with 59.68% share in 2025, reflecting hyperscale’s’ cost advantage. Hybrid modes are forecast to grow at 22.96% through 2031 because growers want real-time latency without forfeiting data sovereignty. Prospera runs pest-detection models on edge gateways and uploads only anomalies, slashing bandwidth by 80%. Gamaya processes hyperspectral data in situ on drones, sending compressed insights to dashboards, ensuring growers keep raw imagery in-house.

Rural 5G pilots in Germany and Japan demonstrated sub-10 millisecond round-trip times, adequate for autonomous path planning. This connectivity enables robots to offload heavy computation to nearby edge servers rather than distant clouds. Consequently, the AI in the agriculture market size attributed to hybrid deployments is primed for double-digit expansion, while pure on-premises installations remain niche.

Geography Analysis

North America commanded 38.91% of 2025 spending thanks to high penetration of GPS-guided machinery, broadband coverage in rural counties, and climate-smart subsidies. USDA’s Conservation Stewardship revisions reimburse up to 75% of AI sensor and software costs when nutrient plans are machine-verified. Canada’s Agricultural Clean Technology Program disbursed CAD 50 million (USD 37 million) in 2025 for precision-farming gear. Mexico’s avocado exporters now integrate AI traceability to meet United States import rules. Labor limits still slow fully autonomous robots pending regulatory clearance.

Asia-Pacific is projected to grow fastest at a 22.98% CAGR through 2031. China’s 200 smart-farm zones mandate local AI stack deployment, anchoring domestic cloud partnerships. India’s Kisan Suvidha serves 50 million users with satellite-based advisories. Japan targets 100,000 hectares under autonomous tractors by 2027 to offset rural aging. Australia leverages AI evapotranspiration models to ration Murray-Darling water. Regulatory divergence from China’s data-localization rules to India’s consent-based regime forces vendors to regionalize data flows, yet demand outstrips these frictions.

Europe, South America, the Middle East, and Africa each held single-digit to low-teens slices in 2025. The EU earmarks over one-third of rural-development funds for digital farming, spurring sensor rollouts across Germany and Poland. Brazil’s Agro 4.0 tax incentives catalyse AI uptake on soybean estates. Saudi Arabia’s National Center for Agriculture Technology backs AI-optimized vertical farms to cut import dependency. South Africa’s citrus packers deploy computer-vision grading to meet EU standards, while Nigeria pilots satellite crop monitoring for rice in the Niger Delta. Collectively, these initiatives expand the global AI in agriculture market, even where infrastructure gaps persist.

Competitive Landscape

The AI in agriculture market remains moderately fragmented: the top five vendors Deere and Company, Trimble, Bayer Crop Science, Microsoft, and IBM hold under 30% combined share. Equipment makers leverage installed bases to upsell software; Deere connected 500,000 machines to its Operations Center by 2025, creating a proprietary data moat. Trimble integrates over 200 third-party devices, positioning itself as a neutral platform. Cloud hyperscale’s focus on horizontal infrastructure, teaming with agronomic specialists for vertical depth.

Startups such as Prospera, Taranis, and CropX undercut incumbents by 30-50% and specialize in crop-specific analytics, appealing to growers wary of equipment lock-in. Syngenta’s 2024 acquisition of Cropio illustrates vertical bundling of seeds, chemicals, and data services. Patent activity surged, with over 800 United States agricultural-AI patents issued in 2024-2025, many in weed-detection and yield-prediction fields. Edge-AI chipmakers Hailo and Blaize enable battery-powered sensors to run computer vision locally, opening underserved geographies where broadband is scarce.

Standard-setting is now a competitive lever; vendors active in AgGateway’s ADAPT group influence interoperability norms. As value-chain roles blur, the AI in agriculture market offers white-space in livestock biometrics, post-harvest quality prediction, and regenerative-agriculture verification, none yet dominated by a single vendor.

AI In Agriculture Industry Leaders

Microsoft Corporation

IBM Corporation

Granular Inc.

aWhere Inc.

Prospera Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Deere and Company partnered with NVIDIA to embed Jetson Orin edge-AI modules in next-gen autonomous tractors, targeting commercial rollouts across 50,000 hectares in the U.S. Midwest by late 2027.

- December 2025: Trimble acquired Bilberry, adding real-time weed-detection algorithms to its spot-spraying portfolio for European customers.

- November 2025: Bayer Crop Science released Climate FieldView Pro, bundling generative-AI agronomic reports and carbon-credit quantification at USD 15 per hectare per season across North America, Brazil, and Germany.

- October 2025: Microsoft Azure Data Manager for Agriculture added 12 crop-specific yield-prediction models and hyperspectral satellite support from Planet Labs.

Global AI In Agriculture Market Report Scope

The AI in Agriculture Market Report is Segmented by Application (Precision Farming, Livestock Monitoring, Drone Analytics, Smart Greenhouse Management, Supply-Chain and Post-Harvest Optimization), Technology (Machine Learning, Computer Vision, Predictive Analytics, Natural-Language Processing), Component (Hardware, Software Platforms, Services), Deployment Mode (Cloud, On-Premise, Hybrid), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Precision Farming |

| Livestock Monitoring |

| Drone Analytics |

| Smart Greenhouse Management |

| Supply-Chain and Post-Harvest Optimization |

| Machine Learning |

| Computer Vision |

| Predictive Analytics |

| Natural-Language Processing (NLP) |

| Hardware (Sensors, Drones, Robots) |

| Software Platforms |

| Services (Consulting, Integration, Support) |

| Cloud |

| On-Premise |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Application | Precision Farming | |

| Livestock Monitoring | ||

| Drone Analytics | ||

| Smart Greenhouse Management | ||

| Supply-Chain and Post-Harvest Optimization | ||

| By Technology | Machine Learning | |

| Computer Vision | ||

| Predictive Analytics | ||

| Natural-Language Processing (NLP) | ||

| By Component | Hardware (Sensors, Drones, Robots) | |

| Software Platforms | ||

| Services (Consulting, Integration, Support) | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is spending on AI tools expected to grow in farming between 2026 and 2031?

Overall expenditure is projected to rise at a 21.96% CAGR, lifting the AI in agriculture market from USD 3.11 billion in 2026 to USD 8.39 billion by 2031.

Which application is gaining ground quickest?

Smart greenhouse management shows the fastest trajectory, advancing at a 22.47% CAGR as operators automate climate, lighting, and nutrient regimes.

What region offers the strongest future growth prospects?

Asia-Pacific is forecast to register the highest regional CAGR at 22.98% through 2031, powered by large-scale programs in China and India.

Why are services revenue growing faster than software sales?

Farms need integrators to mesh legacy tractors, sensor networks, and cloud platforms, so consulting and support revenue is slated to expand at 22.91% annually.

How concentrated is vendor power today?

The five largest suppliers hold less than 30% of global sales, leaving the competitive landscape moderately fragmented and open to innovators.

Are hybrid deployments overtaking cloud-only models?

Hybrid architectures that mix edge processing with cloud training are set to grow at 22.96% annually, gradually eroding the dominance of pure-cloud setups.

Page last updated on: