Embedded AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.74 Billion |

| Market Size (2031) | USD 26.24 Billion |

| Growth Rate (2026 - 2031) | 13.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded AI Market Analysis by Mordor Intelligence

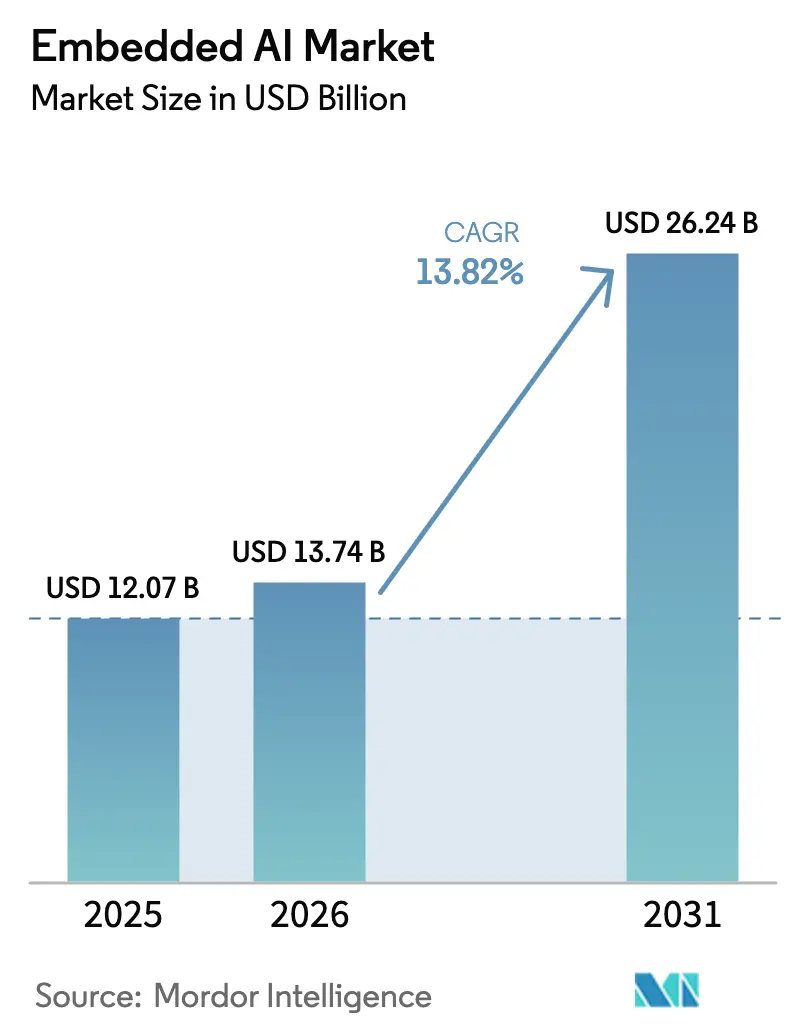

The Embedded AI Market size was valued at USD 12.07 billion in 2025 and estimated to grow from USD 13.74 billion in 2026 to reach USD 26.24 billion by 2031, at a CAGR of 13.82% during the forecast period (2026-2031). Growth stems from three interconnected shifts: 1) advanced semiconductor designs that embed neural-network accelerators directly on chips, 2) ultra-low-latency 5G networks that let devices collaborate without cloud dependence, and 3) enterprises’ urgency to process data on-device for privacy and real-time control. Hardware continues to anchor the Embedded AI market, yet software tools that compress, quantize, and orchestrate models across heterogeneous silicon are scaling faster than any other layer, pulling new service revenues into view. Demand for edge-first deployments is reinforced by regulatory scrutiny of data residency and the high cost of shuttling unfiltered sensor streams to centralized clusters. These tailwinds collectively ensure the Embedded AI market will keep outpacing overall semiconductor spending through the decade.

Key Report Takeaways

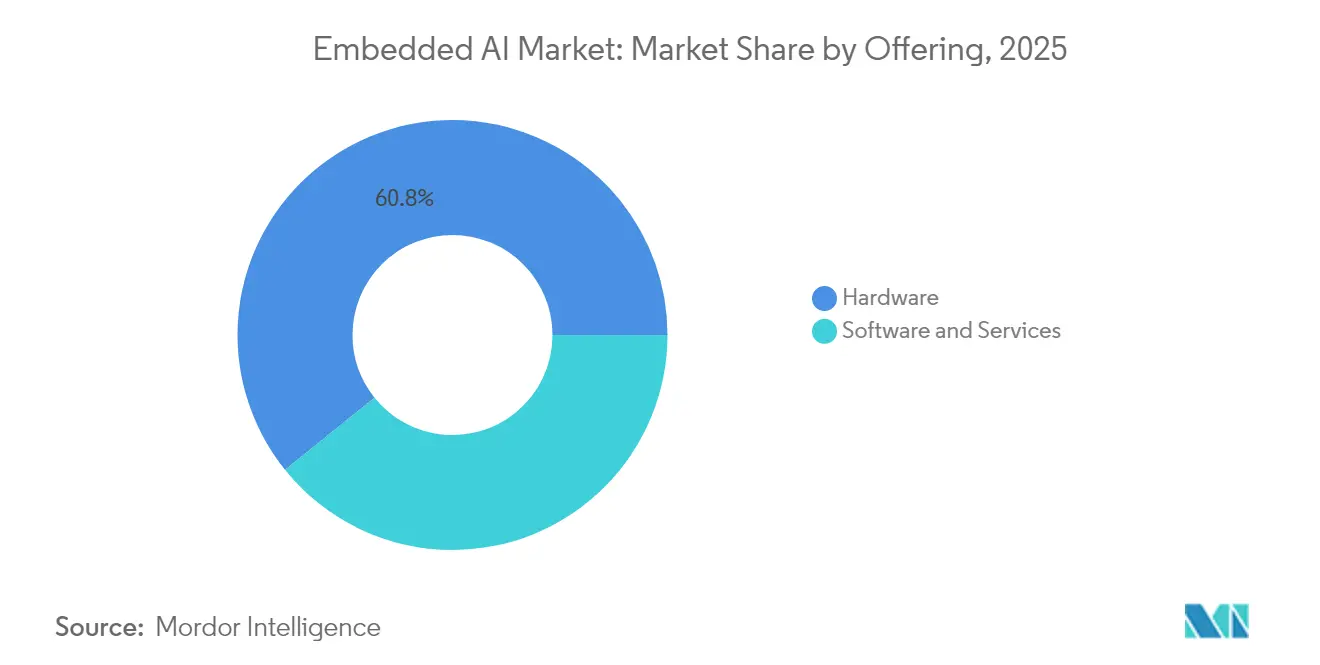

- By offering, hardware held 60.78% of the Embedded AI market share in 2025, while software and services are on track for a 16.55% CAGR to 2031.

- By hardware type, CPUs led with 33.82% revenue share in 2025; neuromorphic chips are poised for the fastest 16.02% CAGR.

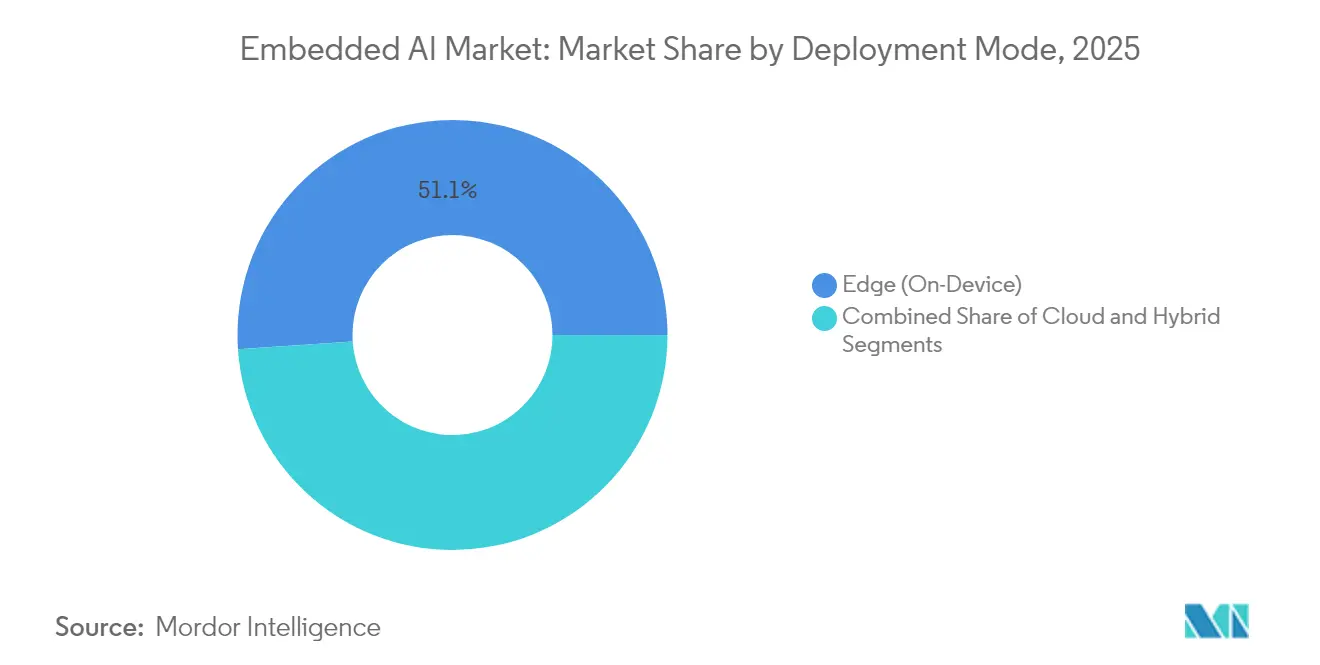

- By deployment mode, edge implementations accounted for 51.05% of the Embedded AI market in 2025; hybrid strategies show the highest projected 16.44% CAGR.

- By data type, image and video workloads captured 40.12% of revenue in 2025; text and audio workloads are advancing at a 16.21% CAGR.

- By end-user vertical, IT and telecommunication led with a 28.19% share in 2025, while automotive is expanding quickest at a 16.11% CAGR.

- By geography, North America commanded 39.62% revenue in 2025; Asia-Pacific is projected to grow at 16.19% CAGR through 2031.

- NVIDIA, Intel, and Qualcomm together controlled under one-quarter of the total 2024 revenue, underscoring a fragmented playing field where innovators such as BrainChip and Hailo continue to carve white-space niches.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Embedded AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in edge computing deployments | +2.5% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Rapid advances in AI accelerator hardware | +1.8% | North America and EU core, spill-over to APAC | Short term (≤ 2 years) |

| Proliferation of connected IoT devices | +1.9% | Global, led by APAC manufacturing hubs | Long term (≥ 4 years) |

| Expansion of 5G and ultra-low-latency networks | +1.7% | APAC core, North America and EU following | Medium term (2-4 years) |

| Emergence of on-sensor AI event-based vision | +1.6% | Global, early adoption in automotive and industrial | Long term (≥ 4 years) |

| Open-source RISC-V ISA driving custom chips | +1.5% | Global, with strong momentum in China and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Edge Computing Deployments

Organizations are redesigning data pipelines so that inference executes within milliseconds on the device rather than in distant clouds. Industrial automation illustrates this shift: Bosch cut unplanned downtime by 25% after installing predictive-maintenance nodes that analyze vibration signals locally, eliminating bandwidth costs tied to raw-data backhaul. [1]Embedded Staff, “BrainChip’s Akida NPU: Redefining AI Processing with Event-Based Architecture,” Embedded, embedded.com The same logic now applies to healthcare wearables, traffic cameras, and logistics scanners, each requiring decisions without a round-trip to a data center. Hardware vendors, therefore, prioritise cache hierarchies, on-chip memory, and domain-specific DSP blocks optimised for edge workloads. As these deployments scale, the Embedded AI market gains a durable demand floor across both mature and emerging economies.

Rapid Advances in AI Accelerator Hardware

Special-purpose chips increasingly outperform general-purpose GPUs on power, throughput, and cost metrics that matter at the edge. Intel’s 1.15 billion-neuron neuromorphic system shows how brain-inspired spikes deliver orders-of-magnitude gains in energy efficiency. Start-ups are following with transformer-specific ASICs; Etched’s Sohu prototype targets 10× GPU inference performance while slashing watt-hours consumed. Vendors that bundle tuned software stacks with silicon shorten time-to-production for customers, accelerating unit shipments and lifting the Embedded AI market trajectory through 2027.

Proliferation of Connected IoT Devices

Global IoT endpoints exceeded 15 billion in 2024 and continue to climb, saturating networks with telemetry that no longer fits classic sensor-to-cloud models. Embedded inferencing lets smart meters compress energy-usage histograms, city cameras transmit only anomaly clips, and factory sensors trigger alarms locally. Such selective communication reduces recurring connectivity fees and shields sensitive operational data from external exposure. Edge-ready operating systems and machine-learning toolchains that auto-generate binaries for microcontrollers expand the developer base, accelerating adoption within small and mid-sized enterprises worldwide.

Expansion of 5G and Ultra-Low-Latency Networks

5G achieves sub-10-millisecond round-trips, enabling distributed intelligence where edge nodes handle safety-critical tasks and tap nearby MEC servers for heavier analytics. Autonomous vehicles exemplify the concept: on-board vision stacks maintain lane-keeping locally, while 5G links coordinate platooning maneuvers when coverage exists. Similar hybrids appear in telesurgery robots and AR headsets. This architecture aligns with the Embedded AI market because device makers must still integrate inference accelerators to survive network dropouts, reinforcing silicon demand even as bandwidth improves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and integration costs | -1.2% | Global, particularly affecting SMEs in developing markets | Short term (≤ 2 years) |

| Data privacy and cyber-security concerns | -0.8% | EU and North America regulatory focus, global implications | Medium term (2-4 years) |

| Scarcity of AI-optimized embedded-software talent | -0.6% | Global, acute in specialized domains | Long term (≥ 4 years) |

| Thermal/power limits for continuous edge inference | -0.4% | Global, critical in mobile and battery-powered applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Costs

Total cost of ownership often surpasses initial hardware quotes by 40–60%, once custom software, compliance testing, and staff training are included. Healthcare device makers, for instance, face USD 2–5 million per product line to certify AI-enabled features under medical regulations. Similar hurdles arise in aviation, energy, and defense. These overheads delay projects, especially for small manufacturers with narrow margins, and moderate Embedded AI market adoption in price-sensitive geographies until turnkey reference designs mature.

Data Privacy and Cyber-Security Concerns

Edge-deployed models store proprietary weights that attackers can reverse-engineer. Adversarial firmware injections can also alter inference outcomes, jeopardising safety-critical operations. GDPR and forthcoming EU AI rules oblige enterprises to secure each node, perform continual risk assessments, and provide explainability logs. [2]Dina Genkina, “Brain-Like Computers Tackle the Extreme Edge,” IEEE Spectrum, spectrum.ieee.org Compliance drives demand for encrypted memory enclaves and federated-learning frameworks, adding engineering complexity that tempers the Embedded AI industry’s near-term pace, albeit stimulating niches for security-centric silicon variants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Acceleration Drives Market Evolution

Hardware retained 60.78% revenue in 2025, yet software and services are expanding at a 16.55% CAGR as toolchains become decisive in workload portability and lifecycle management. Vendors bundle pruning, quantization, and compiler toolsets to squeeze larger models onto shrinking die areas, making software a critical growth flywheel for the Embedded AI market. The segment’s rise reflects enterprise demands for quick model iterations and over-the-air updates that preserve device uptime. Service providers now monetise model-as-a-service contracts that keep inference pipelines evergreen. Meanwhile, hardware roadmaps increasingly align with open-source runtimes, blurring traditional silos and embedding software capability as a purchasing criterion. The interplay between optimized stacks and specialised silicon elevates overall Embedded AI market efficiency, reinforcing platform stickiness for chip vendors that integrate both layers.

While hardware dominance persists, product lifecycles are shortening. Chipmakers introduce yearly revisions that double TOPS-per-watt, forcing OEMs to refactor firmware to exploit new instructions. This dynamic ensures continuous pull for associated tool licenses and consultancy engagements, further amplifying software’s topline growth. In parallel, emerging SaaS platforms orchestrate swarm learning across fleets, letting edge devices share aggregated gradients without centralising raw data. Such license-based models enhance recurring revenue visibility across the Embedded AI market, supporting broader ecosystem capitalization.

By Hardware Type: Neuromorphic Revolution Challenges Traditional Architectures

CPUs captured 33.82% revenue in 2025 by virtue of ubiquity and backward compatibility; however, neuromorphic chips lead the growth curve at 16.02% CAGR thanks to spike-driven computation that emulates synaptic efficiency. These event-based processors demonstrate energy draws measured in microwatts, enabling months-long battery life for noise-suppression earbuds or predictive-maintenance stickers. The switch from frame-based to temporal encoding reduces memory movement, a primary energy drain in conventional designs. GPUs remain essential for convolution-heavy imaging workloads, while FPGAs attract industrial buyers seeking field-upgradable logic to accommodate changing standards. ASICs dominate high-volume endpoints such as smart speakers, where per-unit cost dictates silicon selection.

NPUs and TPUs now ship inside mainstream smartphones, accelerating voice assistants and generative imaging on-device. Their inclusion reshapes bill-of-materials allocations, reallocating cost from baseband radios toward AI co-processors. Complementary accelerators like vision-processing units handle HDR demosaicing and object detection in parallel, easing CPU load. Collectively, this diversification expands the Embedded AI market size for edge silicon platforms, ensuring multiple architecture types can flourish without cannibalization during the forecast period.

By Deployment Mode: Hybrid Strategies Emerge as Optimal Architecture

Edge deployments represented 51.05% revenue in 2025, cementing on-device inference as the default for latency-critical tasks. Real-time demands in robotics, drones, and AR glasses mean compute must remain operational during network outages. Nevertheless, hybrid models exhibit the steepest growth at 16.44% CAGR, balancing deterministic edge processing with cloud-based retraining and fleet analytics. Retail chains, for instance, stream aggregate foot-traffic summaries to regional data lakes while preserving shopper privacy by discarding facial frames locally. This duality optimises bandwidth and regulatory compliance simultaneously.

Pure-cloud remains relevant for bursty workloads and global model rollouts, yet rising egress fees and sovereignty laws encourage partial repatriation of compute. MEC nodes positioned in carrier facilities further blur distinctions, enabling sub-5-millisecond hops between device and micro-data-center. Such architectures boost service availability without inflating device thermal envelopes. As OEMs refine task-placement heuristics, the Embedded AI market size for orchestration middleware grows in lockstep, stimulating partnership opportunities across telecom operators, hyperscalers, and silicon vendors.

By Data Type: Vision Applications Drive Market Expansion

Image and video streams generated 40.12% of 2025 revenue as surveillance, automotive perception, and factory inspection depend on high-fidelity scene understanding. Convolutional backbones ingest frames at 30–120 fps, pushing TOPS requirements that justify dedicated accelerators and thus underpin the Embedded AI market. Vision pipelines increasingly incorporate transformer heads for long-range context, intensifying memory-bandwidth demands. Text and audio pipelines, although smaller today, are scaling fastest at 16.21% CAGR; voice pick-and-pack instructions in warehouses and LLM-powered customer kiosks highlight their commercial relevance.

Sensor fusion adds layers of complexity. Gyroscopes, LiDAR, and radar feed numeric and categorical arrays into late-stage model ensembles, enhancing robustness against visual occlusion. Chips capable of heterogeneous scheduling across vision DSPs, MAC arrays, and classical control cores become critical. Consequently, vendors that disclose deterministic latency bounds win preference in safety-critical procurement. The diversification of modalities elevates the total Embedded AI market share for flexible architecture suppliers able to switch context without expensive silicon duplication.

By End-user Vertical: Automotive Transformation Accelerates Adoption

IT and telecommunication maintained 28.19% revenue in 2025, applying embedded intelligence to optimise radio scheduling, anomaly detection, and customer-premise equipment. Automotive, however, advances at 16.11% CAGR through fleet electrification and autonomous-drive programs. Embedded inferencing steers lane-keeping, monitors driver fatigue, and manages battery thermal envelopes in real time, creating a sustained silicon refresh cycle within OEM platforms. Manufacturing follows closely, equipping machine-vision stations that flag defects within milliseconds, thereby reducing scrap rates.

Healthcare adopts prudently due to stringent validation, yet portable diagnostics and smart prosthetics illustrate the sector’s long-run potential. Energy utilities install grid-edge phasor units that predict transformer stress, minimising outages. Smart-city operators embed AI across lighting, waste, and emergency-response networks, each forming new revenue pools for service integrators. Collectively, cross-industry penetration cements the Embedded AI industry’s resilience against sector-specific cycles, widening addressable opportunities for suppliers that tailor reference designs to each regulatory and environmental requirement.

Geography Analysis

North America retained 39.62% revenue in 2025, fortified by domestic fabs, multibillion-dollar venture inflows, and early enterprise experimentation that accelerates pilot-to-production cycles. Federal incentives channel capital into advanced packaging lines, reducing exposure to overseas wafer capacity and assuring supply continuity for defense-grade edge devices. Universities and start-ups alike benefit from this ecosystem density, funneling patents into silicon tape-outs at a record pace.

Asia-Pacific delivers the steepest trajectory at 16.19% CAGR, leveraging large-scale manufacturing, state-sponsored AI strategies, and explosive IoT rollouts. China’s industrial-scale non-binary processor program exemplifies sovereign ambition to localize critical compute while raising energy-efficiency bars. Japan and South Korea emphasize automotive sensors and collaborative robotics, whereas India’s telecom giants pilot rural-edge diagnostics that leapfrog fixed-line constraints.

Europe maintains regulatory influence, mandating privacy-by-design and explainability, which favors embedded over cloud-centric inference. Germany’s Industrie 4.0 guidelines push neuromorphic trials in machine tools; France funds sovereign edge AI stacks compatible with Gaia-X data-spaces. Latin America and the Middle East and Africa still trail on revenue but unlock greenfield deployments in agriculture, yield-monitoring, and grid balancing, foreshadowing a second-wave adoption cycle once connectivity expands. This mosaic of regional priorities ensures diversified revenue streams across the Embedded AI market, insulating suppliers from isolated macro shocks.

Competitive Landscape

The Embedded AI market features moderate fragmentation: no single supplier holds even a 15% revenue slice, and the combined top five remain below 35%. NVIDIA leverages CUDA ecosystems to dominate general-purpose inference, Intel advances neuromorphic R&D, while Qualcomm integrates NPU blocks into cellular SoCs targeting handset volumes. Parallel to these giants, BrainChip’s event-based Akida, Hailo’s Hailo-8, and Innatera’s Pulsar focus on microwatt-class efficiency, carving moats where power budgets trump TOPS bragging rights.

Strategic activity centers on vertical integration. NXP’s Kinara acquisition embeds vision DSPs into its automotive controllers, compressing supply chains and capturing software margins. Qualcomm’s purchase of Edge Impulse aligns developer tooling with Snapdragon silicon, lowering friction for appliance OEMs. Start-ups pursue compute-in-memory and wafer-level stacking to crash cost curves; Rain AI’s RISC-V partnership claims 50× matrix-multiply efficiency gains, hinting at future disruption potential. [4]Andrei Santalo, “Rain and Andes Partnership RISC-V,” Rain AI, rain.ai

Suppliers increasingly license hardened IP blocks so customers can spin custom ASICs under tight confidentiality, helping regional fabs meet sovereign-compute mandates. Meanwhile, open-source frameworks extend vendor-neutral APIs, enabling cross-generation model portability and reducing customer lock-in. These dynamics collectively steer the Embedded AI market toward a coopetitive equilibrium where ecosystem depth, not just transistor counts, dictates sustainable advantage.

Embedded AI Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Qualcomm Incorporated

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: China commenced mass production of the first industrial-scale non-binary AI chip developed at Beihang University.

- May 2025: Innatera unveiled Pulsar, the inaugural mass-market neuromorphic microcontroller for sensor-edge use cases.

- March 2025: Qualcomm closed its acquisition of Edge Impulse, expanding its embedded-AI software reach.

- February 2025: NXP Semiconductors purchased Kinara for USD 307 million, bolstering its automotive AI portfolio.

- January 2025: Groq partnered with GlobalFoundries to scale production of its Language Processing Units.

- December 2024: Syntiant completed the USD 150 million acquisition of Knowles’ Consumer MEMS Microphones business.

Global Embedded AI Market Report Scope

Embedded AI integrates artificial intelligence directly into hardware or software systems. This allows devices to perform intelligent tasks locally without depending on external cloud computing. By merging machine learning, neural networks, and other AI technologies with embedded systems such as microcontrollers, sensors, or edge devices, embedded AI facilitates real-time data processing, decision-making, and automation, even in resource-constrained environments. Its applications span smart appliances, autonomous vehicles, IoT devices, and industrial automation.

The embedded AI market is segmented by offering (hardware and software & services), by data type (sensor data, image, and video data, numeric data, categorial data, and others), by end-user vertical (BFSI, IT & telecommunication, retail & ecommerce, manufacturing, energy & utilities, transportation & logistics, healthcare & life sciences, and other end-user verticals), and by geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and Middle East & Africa).

The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Hardware |

| Software and Services |

| CPUs |

| GPUs |

| ASICs |

| FPGAs |

| NPUs/TPUs |

| Neuromorphic Chips |

| Other Accelerators |

| Edge (On-Device) |

| Cloud |

| Hybrid |

| Sensor Data |

| Image and Video Data |

| Numeric Data |

| Categorical Data |

| Text and Audio Data |

| Others |

| BFSI |

| IT and Telecommunication |

| Automotive |

| Retail and E-Commerce |

| Manufacturing |

| Energy and Utilities |

| Transportation and Logistics |

| Healthcare and Life Sciences |

| Government and Defense |

| Smart Cities |

| Other End-user Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Hardware | ||

| Software and Services | |||

| By Hardware Type | CPUs | ||

| GPUs | |||

| ASICs | |||

| FPGAs | |||

| NPUs/TPUs | |||

| Neuromorphic Chips | |||

| Other Accelerators | |||

| By Deployment Mode | Edge (On-Device) | ||

| Cloud | |||

| Hybrid | |||

| By Data Type | Sensor Data | ||

| Image and Video Data | |||

| Numeric Data | |||

| Categorical Data | |||

| Text and Audio Data | |||

| Others | |||

| By End-user Vertical | BFSI | ||

| IT and Telecommunication | |||

| Automotive | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Transportation and Logistics | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Smart Cities | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Embedded AI market?

The market stands at USD 13.74 billion in 2026 and is projected to more than double by 2031.

Which segment of the Embedded AI market is growing fastest?

Software and services exhibit the highest growth at a 16.55% CAGR as enterprises prioritise toolchains that optimise on-device models.

Why are neuromorphic chips gaining traction?

They emulate brain-style spikes, achieving microwatt-class power draw that extends battery life for sensor-edge devices.

How does 5G influence Embedded AI adoption?

5G’s ultra-low latency lets edge devices cooperate with nearby servers for heavier analytics without compromising real-time safety functions.

Which region will lead Embedded AI growth through 2031?

Asia-Pacific is forecast to grow at 16.19% CAGR, propelled by large-scale manufacturing and aggressive state-sponsored AI programs.

What is the biggest barrier for small enterprises adopting Embedded AI?

High integration costs—including compliance, software customization, and workforce training—remain the foremost hurdle for resource-constrained firms.

Page last updated on: