Articaine Hydrochloride Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

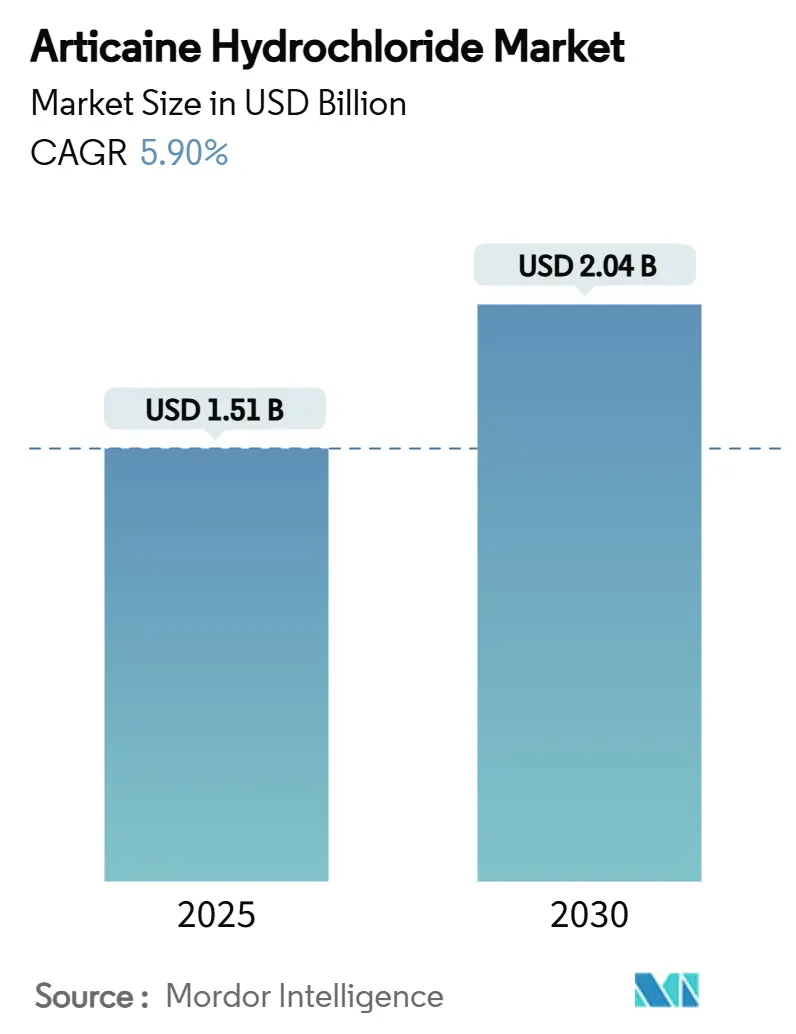

| Market Size (2025) | USD 1.51 Billion |

| Market Size (2030) | USD 2.04 Billion |

| Growth Rate (2025 - 2030) | 5.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Articaine Hydrochloride Market Analysis by Mordor Intelligence

The articaine hydrochloride market size stood at USD 1.51 billion in 2025 and is forecast to reach USD 2.04 billion by 2030, advancing at a 5.9% CAGR over the period. This expansion reflects a decisive swing away from lidocaine as clinicians gravitate to articaine’s faster onset, deeper diffusion and lower reinjection rates. Wider regulatory clearances, growth in complex dental interventions, and manufacturer investment in buffered and pediatric formulations reinforce steady demand. Supply-side discipline has improved product integrity through tighter sterility protocols, but it also raises production costs that favor incumbents with scale. At the same time, intermittent shortages of pharmaceutical-grade epinephrine underline the need for diversified sourcing and alternative vasoconstrictor options, keeping risk management high on board agendas. Competition now pivots on incremental formulation advances, cartridge convenience and digital delivery aids rather than basic molecule differentiation, signalling a value-added phase for the articaine hydrochloride market.

Key Report Takeaways

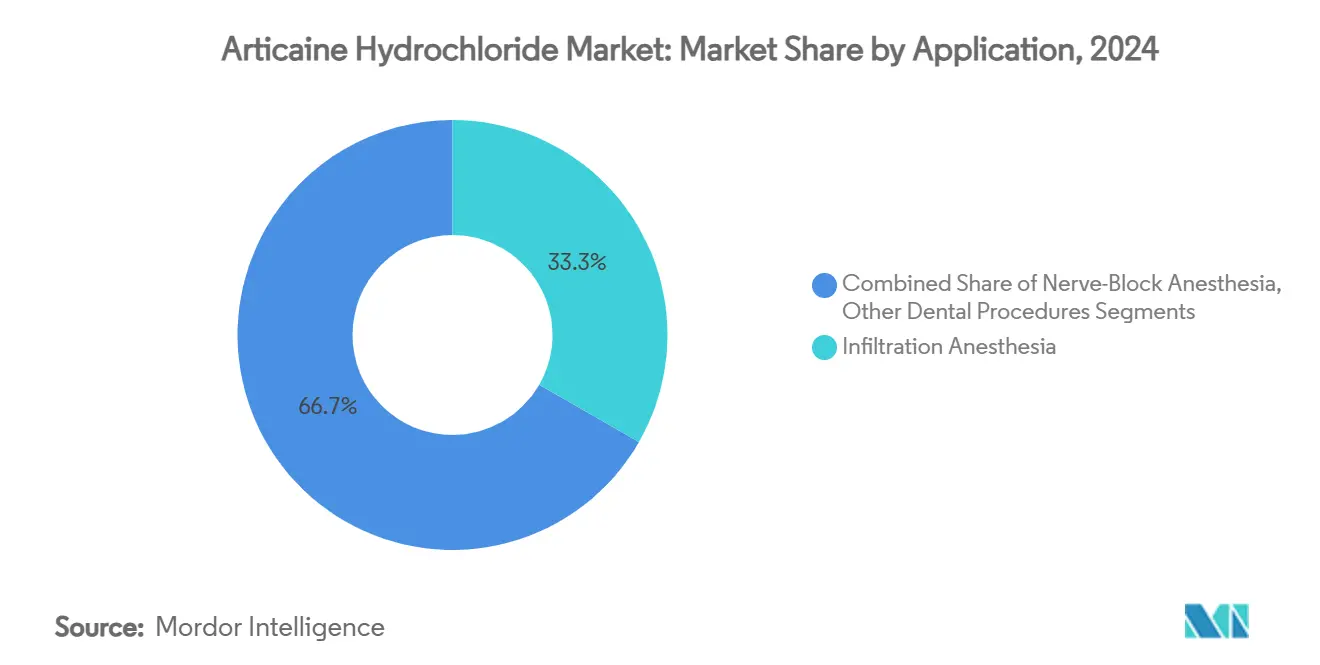

- By application, infiltration anesthesia commanded 33.3% of articaine hydrochloride market share in 2024 while nerve-block procedures are on track to expand at a 9.3% CAGR through 2030.

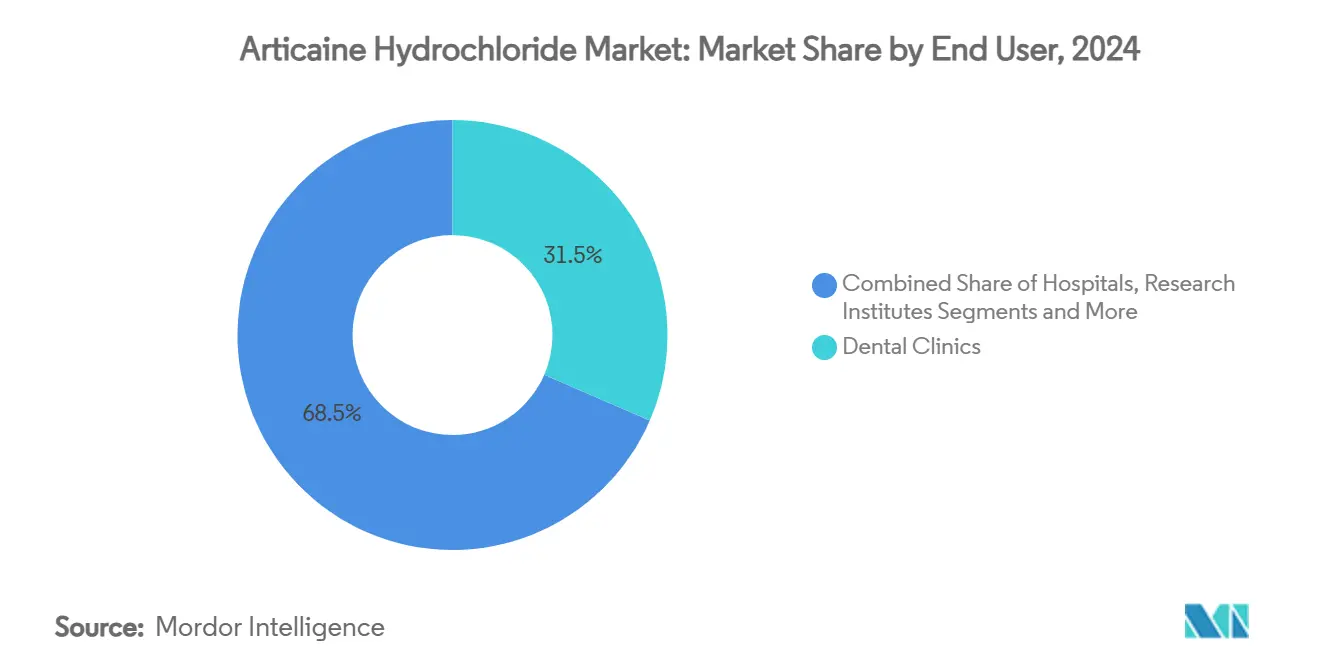

- By end-user, dental clinics held 31.5% share of the articaine hydrochloride market size in 2024, whereas ambulatory surgical centers are projected to post the fastest 9.7% CAGR to 2030.

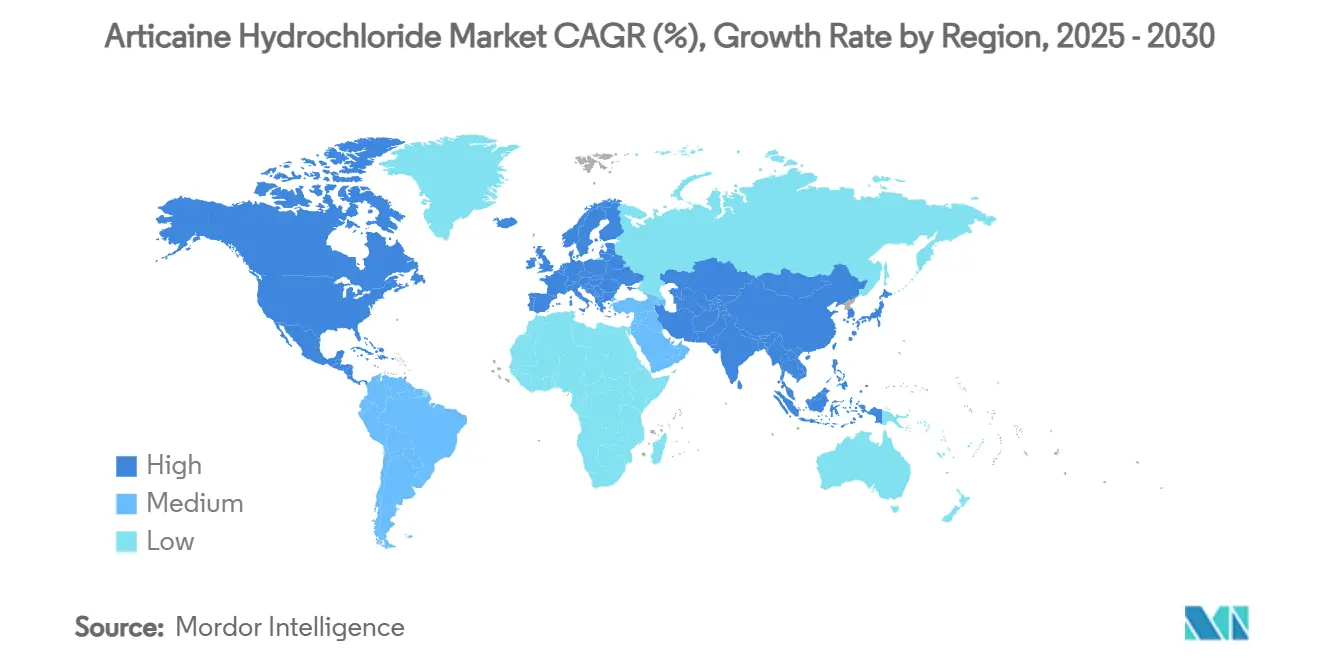

- By geography, Europe led with 38.9% share of the articaine hydrochloride market size in 2024 and Asia-Pacific is forecast to register the quickest 8.8% CAGR during the outlook period.

Global Articaine Hydrochloride Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume Of Complex Dental Procedures Worldwide | +1.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing Adoption Of Articaine Over Lidocaine For Infiltration Due To Higher Diffusion Efficiency | +0.80% | Global, particularly Europe & Asia-Pacific | Short term (≤ 2 years) |

| Favorable Safety Profile Driving Regulatory Approvals Of Pediatric Formulations | +0.60% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Gradual Shift Toward Single-Cartridge Delivery Systems In Emerging Markets | +0.40% | APAC core, spill-over to Latin America | Medium term (2-4 years) |

| Investments In Buffered Anesthetic Innovations For Faster Onset | +0.50% | Global, led by North America | Short term (≤ 2 years) |

| Growth In Teledentistry Driving Demand For On-Site Anesthesia Kits For Mobile Clinics | +0.30% | Global, with early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Complex Dental Procedures Worldwide

The steady increase in multi-stage implant therapies, endodontic retreatments, and full-arch rehabilitations is raising baseline anesthetic consumption. Articaine’s 95.9% success rate in challenging pulpal anesthesia versus 77.6% for lidocaine provides clinicians with measurable chair-time savings and fewer reinjections, aligning directly with productivity goals.[1]Yilei Che, Minhua Wang, Xiaozhen Wu, and Xueling Wang, “The Efficacy of Articaine in Pain Management During Endodontic Procedures in Pediatric Patients,” Perioperative Medicine, biomedcentral.com Ageing populations in Europe and North America add to procedure complexity, lengthening average case duration and amplifying the requirement for longer-acting agents. These dynamics translate into consistent unit growth for 4% articaine with epinephrine formulations, positioning the articaine hydrochloride market as a structural beneficiary of global oral-health demand. Manufacturers that bundle length-of-action data with digital dosing guidance further raise switching costs for rival molecules, deepening articaine’s entrenchment.

Increasing Adoption of Articaine Over Lidocaine for Infiltration

Germany’s near-universal 98% penetration illustrates how quickly preferences can flip once articaine protocols become mainstream in undergraduate training.[2]Viktorija Bojic et al., “Local Anesthetic Usage Among Dentists: German and International Data,” ResearchGate, researchgate.net Comparative trials show a 76% pulpal anesthesia success rate for articaine against 58% for lidocaine in irreversible pulpitis, an outcome that motivates formulary committees to re-evaluate procurement policies.[3]U.S. Food and Drug Administration, “21 CFR 610.12 – Sterility,” Electronic Code of Federal Regulations, ecfr.govAs dental schools revise curricula, new graduates enter practice already fluent in articaine diffusion mechanics, accelerating adoption in Asia-Pacific and Latin America. The trend also carries pricing power; hospitals report willingness to pay a 15-20% premium for predictable onset and shorter chair time. This migration remains the single largest share-gainer for the articaine hydrochloride market through mid-decade.

Favorable Safety Profile Driving Regulatory Approvals of Pediatric Formulations

Regulators are approving lower-concentration, smaller-volume cartridges after evidence confirmed a 35% reduction in post-operative complications compared with adult formulations. United States guidance now recognises articaine as suitable for children aged four and above when dosed appropriately, opening a sizeable pediatric revenue pool. The European Medicines Agency has adopted parallel positions, giving multi-market players immediate leverage. Firms with pediatric pharmacovigilance infrastructure enjoy an early-mover moat because the clinical dossier required for approval is extensive and costly. Over the long term, specialized pediatric SKUs are expected to lift average selling prices and deepen brand differentiation inside the articaine hydrochloride industry.

Gradual Shift Toward Single-Cartridge Delivery Systems in Emerging Markets

Clinics in Southeast Asia, the Middle East and parts of Latin America are replacing multi-dose vials with pre-filled single cartridges to cut wastage and minimise cross-contamination. Government procurement frameworks increasingly mandate single-use formats to align with international infection-control standards, positioning articaine producers that offer value-tier cartridges for volume contracts at an advantage. The change dovetails with fast-growing mobile dentistry programs, where lightweight, sterile packaging simplifies supply logistics. While the margin per unit remains thin, scale volumes elevate absolute profit, underpinning a 0.4% incremental lift to the articaine hydrochloride market CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Batch-Wise Sterility & Pyrogen Testing Requirements | -0.70% | Global, particularly stringent in North America & EU | Short term (≤ 2 years) |

| Intermittent Shortages Of Pharmaceutical-Grade Epinephrine | -0.90% | Global, acute in North America | Short term (≤ 2 years) |

| Competition From Needle-Free Anesthesia Techniques | -0.50% | North America & EU, expanding globally | Medium term (2-4 years) |

| Rising Public Scrutiny On Anesthetic Overuse In Pediatric Dentistry | -0.40% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Batch-Wise Sterility & Pyrogen Testing Requirements

Revisions to United States Code of Federal Regulations 21 CFR 610.12 now oblige every articaine batch to undergo full sterility and endotoxin validation, extending release cycles by up to three weeks and lifting per-unit costs around 12%. Smaller regional manufacturers struggle to absorb these costs, encouraging consolidation that could limit price competition. European authorities are aligning with similar GMP amendments, so the pressure is global. While heightened quality bolsters clinician confidence, the near-term effect is slower capacity additions and lengthier backorders, trimming 0.7% from the articaine hydrochloride market CAGR until automation alleviates bottlenecks.

Intermittent Shortages Of Pharmaceutical-Grade Epinephrine

ASHP has reported periodic backorders for 1:100,000 epinephrine vials, a critical co-ingredient in most articaine cartridges. The shortage compels dentists to rely on plain articaine or switch temporarily to mepivacaine, both scenarios cutting into articaine-epinephrine sales. Although global suppliers are adding redundant manufacturing lines, geopolitical disruptions and limited raw-based production capacity mean interruptions will persist over the next two years. The lost revenue opportunity equates to a 0.9% CAGR drag on the articaine hydrochloride market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Infiltration Leadership Leverages Diffusion Advantages

Infiltration techniques accounted for 33.3% of the articaine hydrochloride market share in 2024 as clinicians capitalized on the molecule’s superior cortical bone penetration to secure rapid, profound anesthesia. Average procedure duration fell by 12 minutes when 4% articaine replaced lidocaine, a time-saving that translates straight to clinic throughput. Over the forecast window, the infiltration segment is projected to maintain steady growth as buffered products lessen injection discomfort and broaden acceptance among needle-averse patients. Nerve-block procedures, meanwhile, are forecast to rise at a 9.3% CAGR, reflecting wider adoption in mandibular third-molar extractions where diffusion depth is critical.

Market momentum also stems from innovation in delivery hardware. Computer-assisted injection systems calibrated specifically for articaine doses mitigate the risk of intravascular placement and improve onset predictability, especially for inferior alveolar and Gow-Gates blocks. Manufacturers packaging instructional QR codes with each cartridge reinforces clinician proficiency and encourages brand loyalty. Collectively, these developments safeguard infiltration’s leadership while supporting above-market gains for advanced nerve-block indications, keeping the articaine hydrochloride market firmly oriented toward high-complexity dental procedures.

By End-User: Clinics Sustain Volume While Ambulatory Surgical Centers Accelerate

Dental clinics generated 31.5% of 2024 revenue for the articaine hydrochloride market size, drawing on repeat restorative work and hygiene-driven anesthesia during periodontal maintenance. Their demand profile is stable but sensitive to disposable income cycles. Ambulatory surgical centers, in contrast, logged the fastest 9.7% CAGR as insurers incentivized outpatient extraction and implant bundles to reduce inpatient costs. ASC protocols favor longer-acting agents; thus, articaine cartridges with 1:100,000 epinephrine see higher per-case volumes compared with standard practice settings.

Hospitals remain essential for trauma and multi-quadrant reconstruction, yet their share is set to plateau as payors steer suitable cases off the ward. Academic and research institutes, though small in absolute volume, wield disproportionate influence by publishing comparative efficacies that shape clinical guidelines. As each setting deepens articaine usage, manufacturers customize pack sizes and educational materials—multi-packs for high-volume clinics, premium buffered variants for ASCs—expanding total addressable opportunity across the articaine hydrochloride industry.

Geography Analysis

Europe retained leadership with 38.9% of the articaine hydrochloride market size in 2024, a position rooted in decades of practitioner experience and an educational ecosystem that standardized articaine curricula. Germany’s 98% penetration underscores entrenched preference, while France and Italy follow closely. EU Pharmaceutical Directive harmonization further simplifies multi-country launches, giving global suppliers predictable approval timelines. Parallel trade within the bloc helps rebalance local shortages, keeping end-user prices relatively stable despite tighter GMP rules. The region’s incremental growth is propelled by an older demographic demanding implant-supported prostheses, an intervention class ideally suited to articaine’s long-acting profile.

Asia-Pacific is positioned as the growth engine, expected to clock an 8.8% CAGR through 2030. China’s dental-clinic density rose 14% between 2024 and 2025, expanding access to premium anesthesia despite price sensitivity. Government insurance pilots in tier-two cities now reimburse articaine for complex endodontic work, widening the adoption funnel. India shows similar momentum as corporate chains roll out franchise models equipped with digital imaging and computer-assisted injections that pair naturally with articaine cartridges. Southeast Asian health ministries, meanwhile, procure single-cartridge packs for public-health mobile units, making the molecule visible in rural outreach campaigns. As these dynamics converge, regional penetration is set to eclipse North American levels by the end of the decade, materially enlarging the global articaine hydrochloride market.

North America presents a mature yet dynamic setting where regulatory intensity shapes product mix more than volume. The United States Food and Drug Administration’s push for pediatric-specific labeling has motivated formulators to submit low-volume, low-concentration SKUs, which now account for 12% of domestic cartridge sales. Concurrently, some states require quarterly emergency-response drills and paediatric life-support certification for deep sedation permits that utilize articaine, raising operational costs but underscoring safety. Although lidocaine still maintains a presence in certain general-practice circles, continuing-education trends and insurance criteria now lean toward articaine for high-value restorative procedures. Canada mirrors these shifts, though bilingual labeling adds a compliance layer that slightly lengthens launch timelines. Combined, these elements sustain steady value growth for the articaine hydrochloride market even in otherwise saturated North American territories.

Competitive Landscape

Global supply is moderately concentrated, with the top five manufacturers accounting for an estimated 62% of cartridge volume, placing the market in a classic oligopolistic band. Septodont leads through vertically integrated production across France, Canada, and Brazil, allowing price buffering and swift redeployment of capacity when regional epinephrine shortages arise. The company’s USD 10+ million investment in Balanced Pharma to co-develop multi-day articaine formulations illustrates a strategy of moving beyond commodity anesthesia toward differentiated pain-management platforms. 3M-ESPE and Dentsply Sirona fortify their share through bundled chairside equipment that relies on proprietary cartridge designs, effectively locking in downstream consumables.

Innovation pipelines now prioritize delivery-system refinements. Computer-controlled flow-rate pens calibrated for articaine parameters reduce intravascular risk and are being trialed in teaching hospitals. Thin-wall stainless needles with proprietary bevel cuts claim to lower insertion force, enhancing patient comfort without altering dosage. Meanwhile, smaller firms in Asia focus on competitive single-cartridge pricing to penetrate public tenders, a tactic that grows volume but offers limited margin headroom. Mergers and acquisitions are likely as sterility compliance costs escalate, making volume scale essential for long-run viability in the articaine hydrochloride market.

Threats originate from emerging needle-free platforms and non-amide molecular classes. A photothermal device that achieved regulatory clearance for intraoral soft-tissue analgesia could encroach on articaine’s low-pain positioning if future iterations attain pulpal depth. However, established companies are hedging by acquiring minority stakes in start-ups developing such modalities, ensuring upside participation. Barriers to entry remain high given the extensive clinical data, pharmacovigilance infrastructure and cold-chain stewardship demanded by regulators. Consequently, competitive behaviour is expected to revolve around line-extensions, value-added kits and co-marketing with digital-dentistry platforms rather than price wars, sustaining healthy margins for leading participants in the articaine hydrochloride market.

Articaine Hydrochloride Industry Leaders

Septodont

Dentsply Sirona

3M

Pierrel S.p.A.

Novocol Pharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Septodont invested in Balanced Pharma and appointed a senior executive to the partner’s board to accelerate work on extended-duration articaine formulations targeting post-procedure pain control.

- October 2024: Septodont and Premier Dental entered an exclusive distribution pact for BufferPro, a chairside buffering system that reduces injection discomfort when used with 4% articaine.

- July 2024: Researchers at Sichuan University synthesised more than 400 articaine analogs with enhanced anti-inflammatory properties using the DeepSA generative framework.

- March 2024: Ohio State Dental Board enforced updated anesthesia rules requiring Providers of Advanced Life Support certification for deep sedation of patients under eight years old when administering articaine.

Global Articaine Hydrochloride Market Report Scope

| Infiltration Anesthesia |

| Nerve-Block Anesthesia |

| Other Dental Procedures |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Infiltration Anesthesia | |

| Nerve-Block Anesthesia | ||

| Other Dental Procedures | ||

| By End-user | Dental Clinics | |

| Hospitals | ||

| Academic & Research Institutes | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the articaine hydrochloride market?

The articaine hydrochloride market size was USD 1.51 billion in 2025 and is projected to hit USD 2.04 billion by 2030.

How fast is demand growing for articaine infiltration anesthesia?

Infiltration holds 33.3% share and continues to expand as clinics adopt buffered formulations that shorten onset time.

Which region shows the fastest uptake of articaine hydrochloride?

Asia-Pacific is forecast to post an 8.8% CAGR through 2030, overtaking other regions in growth momentum.

Why are ambulatory surgical centers important for suppliers?

ASCs consume higher volumes per case and are expected to grow at 9.7% CAGR, favouring premium long-acting articaine cartridges.

How are sterility rules affecting manufacturers?

New batch-wise sterility and pyrogen tests add roughly 12% to unit costs, pushing smaller players toward consolidation.

What innovations could challenge traditional injections?

Needle-free photothermal devices and reactive-oxygen-activated prodrugs are in clinical trials and could shift demand dynamics by 2030.

Page last updated on: