Oxytocin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

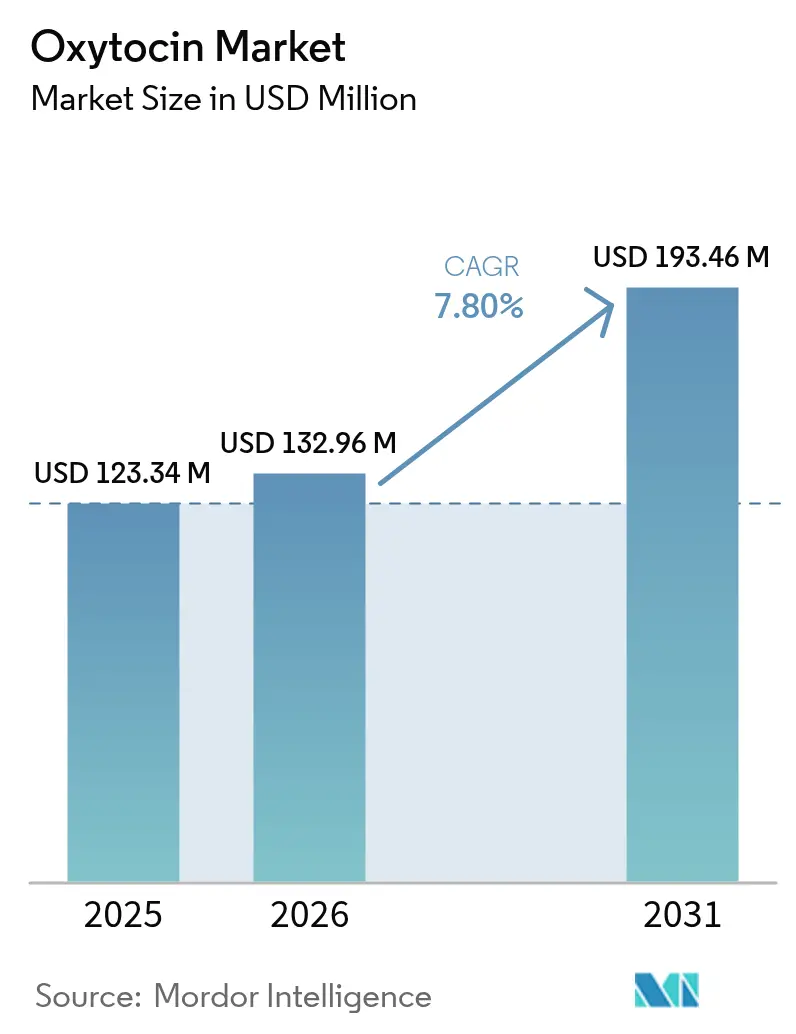

| Market Size (2026) | USD 132.96 Million |

| Market Size (2031) | USD 193.46 Million |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Oxytocin Market Analysis by Mordor Intelligence

The oxytocin market size was valued at USD 123.34 million in 2025 and estimated to grow from USD 132.96 million in 2026 to reach USD 193.46 million by 2031, at a CAGR of 7.80% during the forecast period (2026-2031). Rising postpartum hemorrhage (PPH) cases, expanding institutional deliveries in emerging economies, and technological advances in thermostable and needle-free formulations underpin this steady expansion. Global demographic trends amplify demand: live-births remain elevated in Asia-Pacific while advanced maternal age in OECD markets raises obstetric complexity. Regulatory moves—especially the 2024 WHO/FIGO protocol update mandating active third-stage management—further increase utilization rates. At the same time, supply chain fragility, exemplified by the 2024 United States injectable drug shortage, forces health systems to diversify sourcing and adopt conservation protocols. Innovation centered on intranasal and oromucosal delivery widens application horizons beyond routine obstetrics, positioning the oxytocin market for durable growth despite cold-chain cost pressure.

Key Report Takeaways

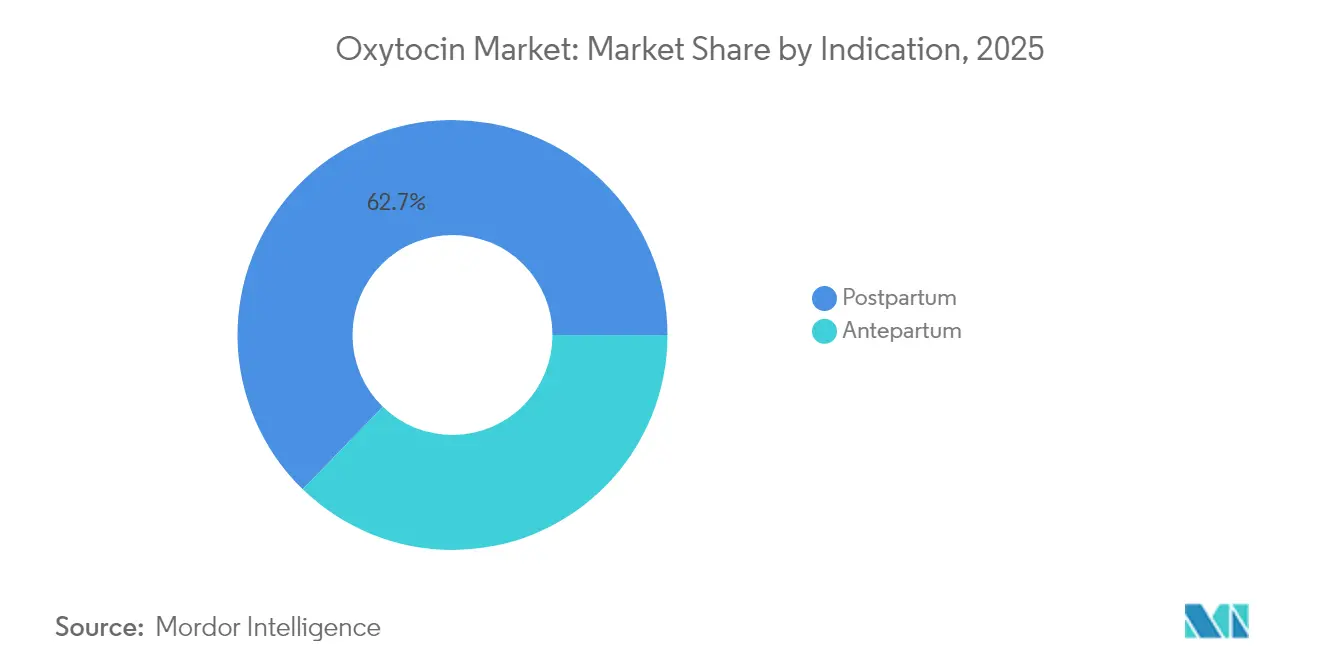

- By indication, postpartum applications commanded 62.74% of the oxytocin market share in 2025, while the antepartum segment is projected to grow at an 8.28% CAGR through 2031.

- By route of administration, parenteral products held 78.25% revenue share in 2025; oromucosal formats are poised for the fastest 8.33% CAGR to 2031.

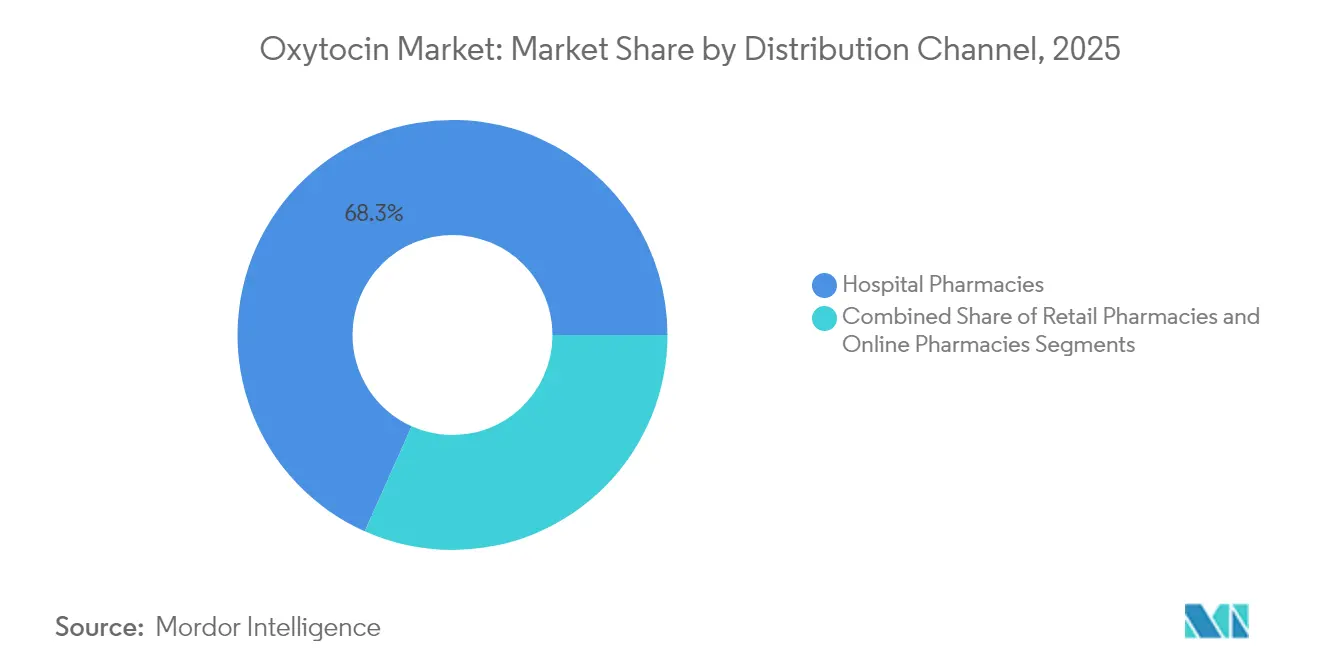

- By distribution channel, hospital pharmacies captured 68.31% share of the oxytocin market size in 2025; retail pharmacies are expanding at an 8.37% CAGR.

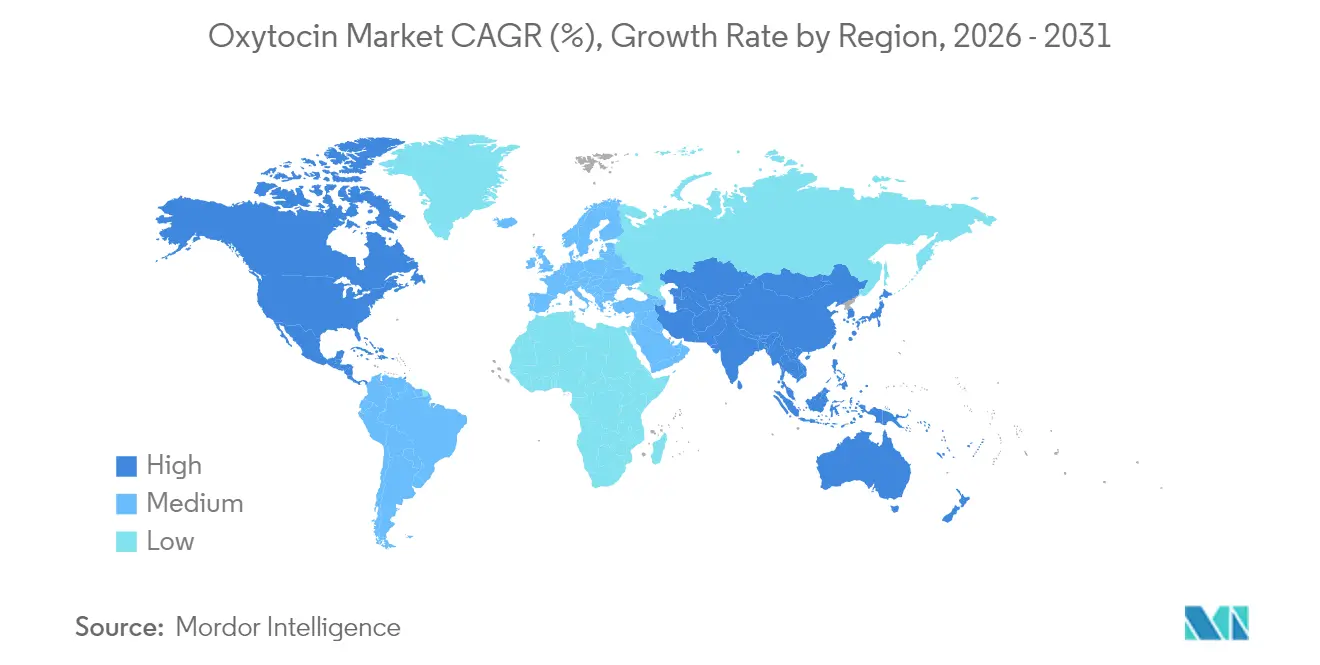

- By geography, North America led with 42.68% revenue share in 2025; Asia-Pacific is set to record the highest 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oxytocin Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obstetric complications | +1.2% | Global (higher in LMIC) | Medium term (2-4 years) |

| Increasing live-births in emerging economies | +1.8% | Asia-Pacific, Sub-Saharan Africa | Long term (≥ 4 years) |

| Updated WHO/FIGO labour-management guidelines | +0.9% | Global | Short term (≤ 2 years) |

| Wider intranasal OT pipeline | +1.1% | North America, Europe | Medium term (2-4 years) |

| Low cost of production | +0.7% | Global | Short term (≤ 2 years) |

| Thermostable OT formulations | +1.4% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Obstetric Complications

Advanced maternal age now accounts for more than 20% of births in developed markets, creating 2.5-fold higher risks of dystocia and uterine atony [1]American College of Obstetricians and Gynecologists, “Clinical Guidance for Labor Induction,” acog.org . Cesarean delivery prevalence reached 32% worldwide in 2024, and parturients with prior cesareans require infusion rates of 27.7 IU/h versus 14.6 IU/h for standard cases. Asia-Pacific mirrors this demographic pattern but faces workforce shortages, leaving hospitals reliant on high-potency oxytocin formulations. These factors elevate the drug from a routine uterotonic to a critical, dose-sensitive intervention in complex deliveries.

Increasing Live-Births in Emerging Economies

Institutional birth rates in India jumped from 39% to 79% between 2005 and 2015 as incentive programs and cultural shifts encouraged hospital deliveries. Up to 23% of these births now need oxytocin compared with historical levels below 15%. Similar demographic dividends in Indonesia, Nigeria, and Pakistan reinforce sustained volume growth. Manufacturers are responding by investing in localized fill-finish plants and last-mile logistics networks to meet the structural shift in demand.

Updated WHO/FIGO Labour-Management Guidelines

The 2024 WHO/FIGO update standardized active third-stage care protocols, anchoring oxytocin as the primary prophylactic agent. North American and European facilities already report 80% compliance, but uptake lags at 45% in many low- and middle-income countries (LMIC) [2]Alyssa R. Hersh, "Third stage of labor: evidence-based practice for prevention of adverse maternal and neonatal outcomes," American Journal of Obstetrics and Gynecology, sciencedirect.com. Implementation drives procurement of pre-filled syringes and auto-injectors that simplify nurse training, spurring incremental unit growth even where birth volumes are static.

Wider Intranasal OT Pipeline

Tonix Pharmaceuticals secured FDA orphan drug designation for TNX-2900 in June 2024, validating intranasal delivery for Prader-Willi syndrome. Clinical trials show 12% bioavailability—adequate for both central-nervous-system and uterotonic effects—while eliminating needles and cold-chain dependence. Similar candidates targeting pain, autism spectrum disorders, and metabolic dysfunction diversify revenue beyond cyclical obstetric demand.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Rx controls & GMP cold-chain costs | -0.8% | Global, acute in tropics | Short term (≤ 2 years) |

| Adverse-event scrutiny | -0.6% | North America, Europe | Medium term (2-4 years) |

| Homebirth/minimal-intervention trends | -0.4% | North America, Europe, Australia | Long term (≥ 4 years) |

| Recurring API shortages | -1.1% | Global, severe in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Rx Controls & GMP Cold-Chain Costs

Mandatory refrigeration during transit raises logistics expenses by 15-25% in high-temperature regions. Studies reveal shipment excursions from -9.9 °C to +30.1 °C, compromising potency and triggering batch recalls. Regulatory inconsistencies—some labels permit ≤25 °C storage without demonstrable stability gain—force multinationals to navigate divergent rules, escalating compliance costs [3]World Health Organization (WHO), "Appropriate Storage and Management of Oxytocin – a Key Commodity for Maternal Health", who.int.

Recurring API Shortages from Supply-Chain Consolidation

Only a handful of peptide manufacturers dominate global output; Fresenius Kabi’s 2024 production halt precipitated a nationwide shortage in the United States. Hospitals rationed oxytocin, adopted reduced-dose regimens, and reported scheduling delays for elective inductions. China’s shortage registry lists 980 drugs, 92.65% of them injectables, underscoring systemic fragility when sterile injectables cluster in a few plants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Postpartum Dominance Drives Market Stability

The postpartum indication represented 62.74% of oxytocin market share in 2025, anchored by WHO first-line guidelines for PPH prevention. Consequently, it forms the revenue base that steadies topline growth across developed and emerging regions. The antepartum segment, although smaller, is forecast to expand at an 8.28% CAGR through 2031, propelled by older maternal age and updated ACOG protocols recommending both low- and high-dose augmentations to curb operative deliveries. Rising infusion rates in elderly parturients reinforce volume gains. Manufacturers therefore align R&D pipelines with divergent needs: fast-acting injectables for postpartum emergencies and controlled-release systems that moderate uterine response during inductions.

Meanwhile, academic centers are testing algorithm-based dosing that tailors antepartum oxytocin infusions to patient BMI and parity. Such precision approaches could moderate total unit volumes but upgrade demand for smart-pump compatible formulations. This balancing act signals sustained mid-single-digit growth for postpartum products and upper-single-digit gains for antepartum therapies throughout the forecast horizon.

By Route of Administration: Parenteral Leadership Faces Innovation Pressure

Injectables dominated with 78.25% of 2025 revenue, reflecting clinician familiarity and low unit cost. Nonetheless, oromucosal formats are tracking an 8.33% CAGR, led by medicated lollipops and thin-film strips suitable for community midwives. Intranasal sprays, though presently niche, ride on FDA orphan-designation momentum and could cannibalize a fraction of inpatient volumes once head-to-head trials confirm equivalence.

Parenteral suppliers defend their base through ready-to-use syringes that cut preparation time by 30% and reduce dosing errors. Oromucosal innovators, by contrast, tout ambient-temperature stability and user comfort. In LMIC settings without reliable power grids, heat-stable oromucosal or intranasal formats could displace injectables entirely, posing a medium-term risk to entrenched parenteral players.

By Distribution Channel: Hospital Dominance Challenged by Retail Expansion

Hospital pharmacies controlled 68.31% of the oxytocin market size in 2025, driven by inpatient delivery volumes and immediate access requirements during obstetric emergencies. Retail outlets, however, are scaling at an 8.37% CAGR as outpatient induction protocols and home-use intranasal products progress through late-stage trials. Tele-consult–driven prescription fulfillment further accelerates over-the-counter pick-up for follow-on doses after discharge.

Cold-chain complexity still tilts the field toward hospitals, but thermostable sublingual tablets under Phase II evaluation may unlock wider retail reach. Supply-chain planners now segment stock-keeping units: chilled injectable packs for institutional buyers and shelf-stable oral sprays for pharmacies. This dual-track model increases manufacturer margin diversification but demands granular demand forecasting to avoid expiries.

Geography Analysis

North America generated 42.68% of 2025 revenue, supported by high PPH intervention rates and generous insurer reimbursement. Yet supply disruptions exposed dependence on offshore active pharmaceutical ingredient (API) plants, prompting policy debates on reshoring critical drug manufacturing. Asia-Pacific, meanwhile, is projected to deliver an 8.62% CAGR to 2031 as India, China, and Indonesia upgrade maternity wards and scale midwife training. Government tender volumes already surpass those of many OECD peers.

Asia-Pacific’s ascendance reshapes global supply-demand balance. India’s Janani Suraksha Yojana program finances facility births and free uterotonics, driving 10-year oxytocin unit growth that outpaces population expansion. China’s 2025 pharmaceutical modernization plan accelerates domestic peptide approvals, encouraging local fill-finish investments. Together, these markets will likely eclipse North American volume by 2027. Infrastructure disparities persist, but bilateral aid initiatives fund cold-chain upgrades in rural clinics, narrowing the access gap. Europe maintains low-single-digit growth as universal insurance ensures steady procurement, while Latin America and Africa exhibit upside tempered by infrastructure gaps. For multinational suppliers, success hinges on portfolio localization—heat-stable strips for equatorial Africa, auto-injectors for European ambulances, and cost-efficient multidose vials for US hospital groups.

Regulatory Landscape

Oxytocin remains anchored as a core maternal-health commodity through essential-medicine and obstetric-care standards, which supports broad reimbursement and tender eligibility. The 24th WHO Model List of Essential Medicines (published September 2025) continues to include oxytocin (10 IU per mL) under uterotonics, reinforcing its role in postpartum hemorrhage prevention and treatment across public procurement systems.

Regulatory execution varies by region and shapes supply strategy. In the United States, oxytocin injections are governed through FDA pathways, including NDA-based labeling for branded products, and labeling maintenance continues to be actively managed, including a Pitocin (oxytocin injection, USP) label update effective May 6, 2026. In Europe, oxytocin is generally handled through national authorizations rather than an EMA centralized route, creating a fragmented approval and pharmacovigilance environment and increasing the need for country-by-country quality and supply compliance under EU medicinal-product and GMP frameworks.

Competitive Landscape

The oxytocin industry comprises a mix of global incumbents and region-specific specialists. Pfizer’s monopoly on branded Pitocin in the United States grants hospital formulary loyalty, while Fresenius Kabi and Hikma dominate generic injectables across Europe and the Middle East. Mid-tier players such as CordenPharma scale peptide APIs for third parties, underpinning contractual manufacturing growth. Market entrants—including Tonix Pharmaceuticals and Insud Pharma—concentrate on delivery innovation: intranasal sprays and thermostable sublingual tablets target unmet needs in both high-income outpatient care and LMIC outreach.

Strategic responses to recent shortages include dual-sourcing APIs, vertical integration, and regional redundancy. CordenPharma’s EUR 900 million peptide platform expansion adds European capacity that mitigates dependence on Asian intermediates. Partnerships like Kinoxis Therapeutics-Boehringer Ingelheim explore neuropsychiatric indications, mitigating obstetric cyclicality.

Patent activity intensifies around formulation stability, with microneedle patches and heat-sensitive color indicators leading the pipeline. The competitive environment thus rewards scale, quality compliance, and delivery science, leaving formulary share fluid for innovators able to pair regulatory agility with credible supply assurances.

Oxytocin Industry Leaders

-

Pfizer Inc.

-

Weefsel Pharma

-

EVER Pharma

-

AdvaCare Pharma

-

Fresenius Kabi AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Cold-chain constraints and injectable supply fragility continue to create whitespace for quality-assured API diversification, and for delivery formats that reduce refrigeration dependence. WHO prequalification signals are increasingly used in maternal-health procurement to de-risk quality and continuity, and WHO-prequalified oxytocin API status (for example, Hemmo Pharmaceuticals Pvt Ltd) provides a clear pathway for finished-dose manufacturers serving donor-funded and public-sector channels.

Formulation innovation is also broadening oxytocin beyond conventional parenteral obstetrics. China adding domestic API capacity through new regulatory clearances, including the NMPA approval reported in June 2026 for an oxytocin API from Chengdu Shengnuo Biopharm, supports additional supply options for regional fill-finish and tender participation. On the technology side, heat-stable delivery work is moving into clinical evaluation, including an April 2026 Phase 1 study of a heat-stable inhaled oxytocin system benchmarked against a 10 IU intramuscular dose. Together with ongoing intranasal programs, including Tonix Pharmaceuticals earlier FDA orphan drug designation momentum, these efforts align with demand for needle-free administration and improved access in settings where refrigeration and trained injection staff remain limiting factors.

Recent Industry Developments

- July 2026: Delhi authorities reported the seizure of 31,000 oxytocin injection vials linked to improper storage at room temperature. The enforcement action highlighted how closely cold-chain compliance is policed in high-volume markets, where it directly affects product usability and tender participation.

- September 2025: The World Health Organization published the 24th WHO Model List of Essential Medicines, continuing to include oxytocin under uterotonics. This maintained a key policy anchor for national formularies and donor-funded procurement, keeping volume demand tied to guideline adherence in maternal care.

- November 2024: Insud Pharma received USD 2.7 million in funding from the Bill & Melinda Gates Foundation to advance Phase II work on a thermostable sublingual oxytocin program for postpartum hemorrhage prevention. The grant supported a development path aimed at reducing reliance on refrigerated injectables in low-resource care settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the oxytocin market covers revenues generated from oxytocin products used in clinical care, mainly linked to labor management and postpartum bleeding prevention, across hospital and outpatient dispensing settings. Values are captured at the product sales level in USD for the covered geographies.

Scope exclusions: This sizing excludes unrelated uterotonic drugs, device-only postpartum hemorrhage solutions, and broad maternal care services that do not represent oxytocin product revenues.

Segmentation Overview

-

By Indication

- Antepartum

- Postpartum

-

By Route of Administration

- Parenteral

- Intranasal

- Oromucosal

-

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping demand signals and treatment practices that affect oxytocin usage, then aligning them with supply availability and policy guidance. Public sources used for this include World Health Organization guidance on essential medicines and maternal care protocols, UNICEF supply and procurement references, and national health statistics agencies that publish birth and maternal outcome indicators.

We also review publications and datasets from the United Nations system, the World Bank for health system indicators, and peer reviewed clinical literature that clarifies dosing norms and route-of-administration patterns. This is complemented with company filings, investor presentations, regulatory press releases, and reputable news coverage to track launches, shortages, and formulation shifts. In a limited way, paid subscriptions for company financials and patent databases help validate manufacturer activity and timelines. These desk sources are illustrative, and many additional public references were checked to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions around where oxytocin is actually used, how procurement is structured, and how pricing moves by channel and formulation. We speak with a mix of manufacturers, distributors, hospital pharmacy stakeholders, and clinical experts across APAC, EMEA, and the Americas to reconcile regional birth volumes with on-the-ground availability and adoption patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 41% |

| Mid tier: 57% | Functional/Unit leaders: 39% | EMEA: 33% |

| Smaller Players: 14% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

The sizing starts with a top-down demand pool build using live births, institutional delivery share, and postpartum hemorrhage prevention practices, then converts those into estimated oxytocin use volumes using typical dosing and the route mix. Once implied volume is built, pricing is applied using a blended average selling price that reflects the channel split (hospital pharmacy, retail, and online), and differences in formulation handling such as cold-chain sensitivity.

To keep the totals grounded, we corroborate results with selective bottom-up approximations where available, using supply-side signals, sampled price points, and channel checks rolled up to see if the implied revenues look realistic for the covered countries. Inputs that typically matter here include annual live-birth trends, shifts in institutional deliveries, guideline changes that influence active management of the third stage of labor, tender-driven procurement intensity, and the rate of stock-outs or supply disruptions discussed by interviewees.

For forecasting, scenario analysis is used around a core path because demand is closely tied to demographic volumes, while pricing and access can move due to procurement cycles and formulation transitions. When gaps show up in country-level data, nearby-country analogs and clearly stated penetration assumptions are applied, and then corrected after expert review so the model stays reproducible and not overly granular.

Data Validation & Update Cycle

Outputs are checked against independent signals such as births-related health indicators, procurement and availability narratives, and the expected channel mix for oxytocin dispensing. When values look out of pattern, the inputs are rechecked for unit conversions, currency treatment, and the timing of price updates, then reviewed again before internal sign-off.

The report is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major guideline revisions, notable shortages, or policy changes affecting institutional deliveries. Before publication, a final validation pass is completed so clients receive the most current view that can be traced back to clear inputs and review steps.

Mordor Intelligence's Oxytocin Market Estimate Compared With Other Published Estimates

Published oxytocin market values often differ even when the topic name looks the same, because the year of pricing, the treatment of channel markups, and the included geographies are not always aligned. Differences also show up when one estimate leans more on demographic demand signals while another leans more on supply visibility.

A refresh-led gap is common in this market because currency timing and tender-linked pricing can shift reported revenues without a large change in patient volumes, and small base-year changes carry through the forecast. By updating average selling prices with recent channel checks and revalidating exchange-rate timing during the refresh cycle, Mordor Intelligence reduces drift that can come from older price points and one-time conversion assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 123.34 M (2025) | |

| Market Research Publisher A | USD 94.97 M (2024) | Uses an earlier base year and can understate value if channel pricing and recent procurement-driven price resets are not carried into the base, especially when currency conversion timing is not updated consistently. |

| Market Research Publisher B | USD 96.10 M (2024) | Reports in USD billions and may apply broader blended pricing with fewer country-level validation checks, which can compress differences between institutional procurement and retail pricing in the current year. |

Across the three figures, the spread is explained more by timing and pricing treatment than by a disagreement on the core demand pool. When scope, currency timing, and the ASP build are stated clearly and then rechecked with field feedback, the resulting market value becomes easier to replicate and more stable for planning.

Key Questions Answered in the Report

What is the current oxytocin market size and projected growth?

What is the current oxytocin market size and projected growth?

Which indication generates the highest revenue?

Postpartum hemorrhage prevention and treatment dominate, contributing 62.74% of 2025 revenue.

Which region will grow the fastest through 2031?

Asia-Pacific is poised for the highest CAGR at 8.62%, driven by expanding institutional deliveries and demographic momentum.

What delivery innovations are reshaping the market?

Intranasal sprays, oromucosal strips, and thermostable sublingual tablets are gaining traction, offering needle-free administration and reduced cold-chain reliance.

How are supply shortages being addressed?

Manufacturers are investing in redundant API sources, domestic fill-finish capacity, and strategic stockpiles to mitigate recurring injectable shortages.

Who are the leading players in the oxytocin industry?

Pfizer, Fresenius Kabi, and Hikma lead injectable supply, while Tonix Pharmaceuticals and Insud Pharma drive alternative delivery innovations.

Page last updated on: