Chile Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

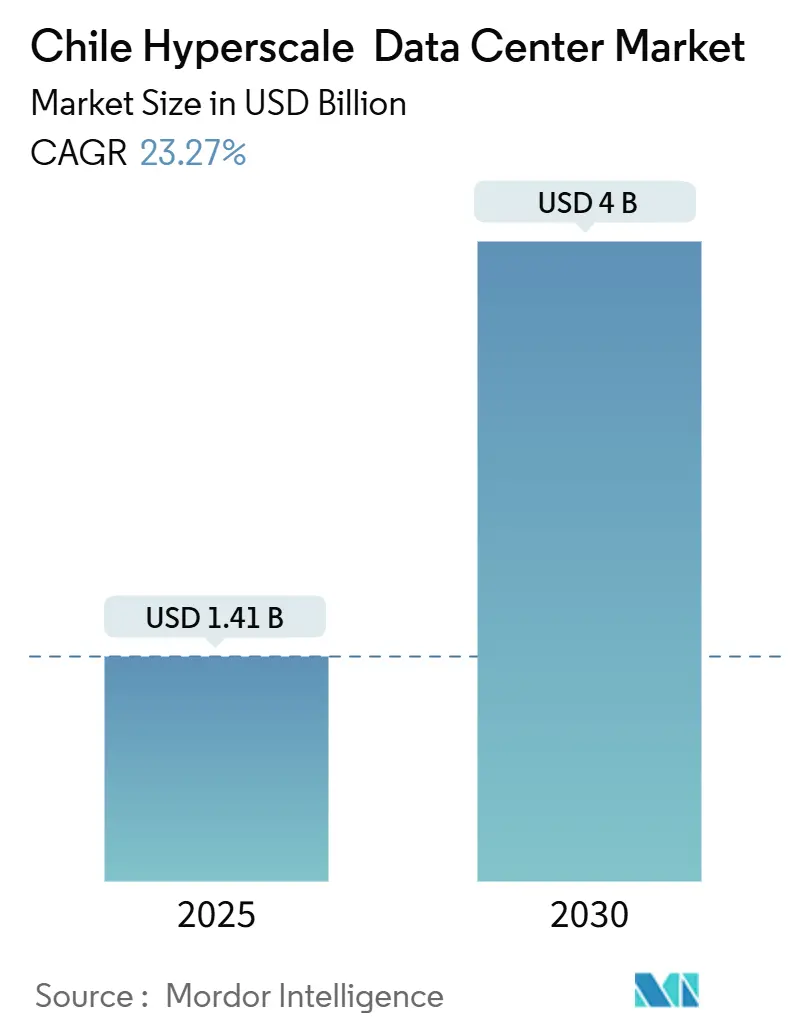

| Market Size (2025) | USD 1.41 Billion |

| Market Size (2030) | USD 4 Billion |

| Growth Rate (2025 - 2030) | 23.27% CAGR |

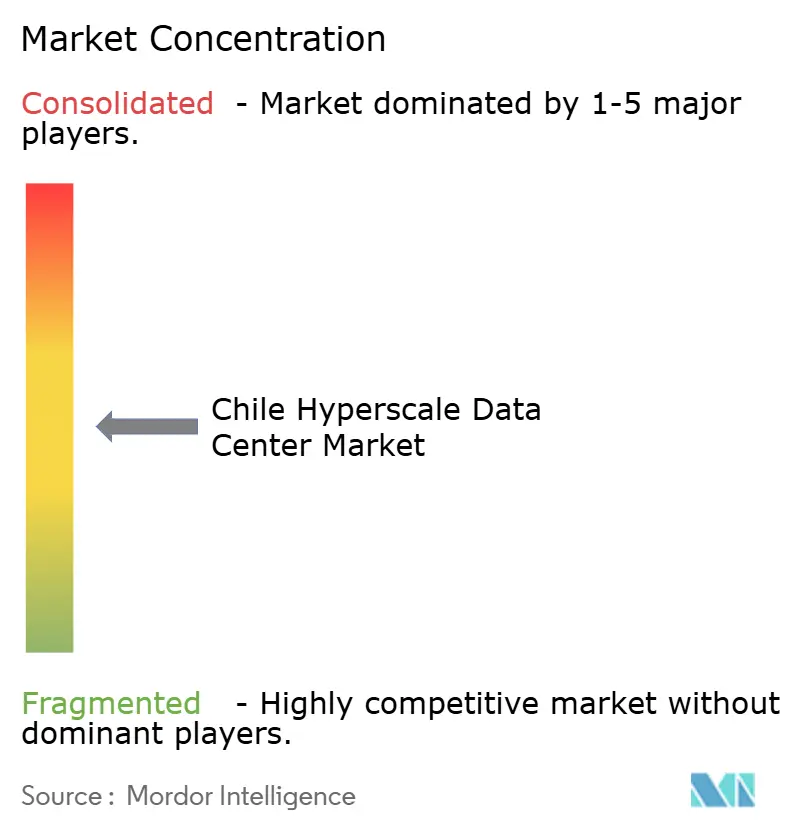

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Hyperscale Data Center Market Analysis by Mordor Intelligence

Chile hyperscale data center market spending is valued at USD 1.41 billion in 2025 and is forecast to reach USD 4.00 billion by 2030, representing a 23.27% CAGR during the period. Operators are scaling capacity in Santiago from 300 MW of live IT power to an additional 50 MW now under construction, supported by predictable renewable-energy supply and strong submarine-cable connectivity. Government incentives introduced under the National Data Centers Plan in December 2024 target USD 2.5 billion of inward investment and shorten permitting cycles, which has intensified development pipelines across both colocation and self-build footprints [2]United Nations Conference on Trade and Development, “Chile National Data Centres Plan,” investmentpolicyhub.unctad.org. E-commerce platforms, banks and media-streaming providers are accelerating cloud adoption, lifting demand for high-density racks that can host GPU clusters for AI model training. Tight but improving grid capacity in northern Chile and innovative cooling designs addressing drought risk are shaping competitive positioning among global hyperscalers and Latin American specialists.

Key Report Takeaways

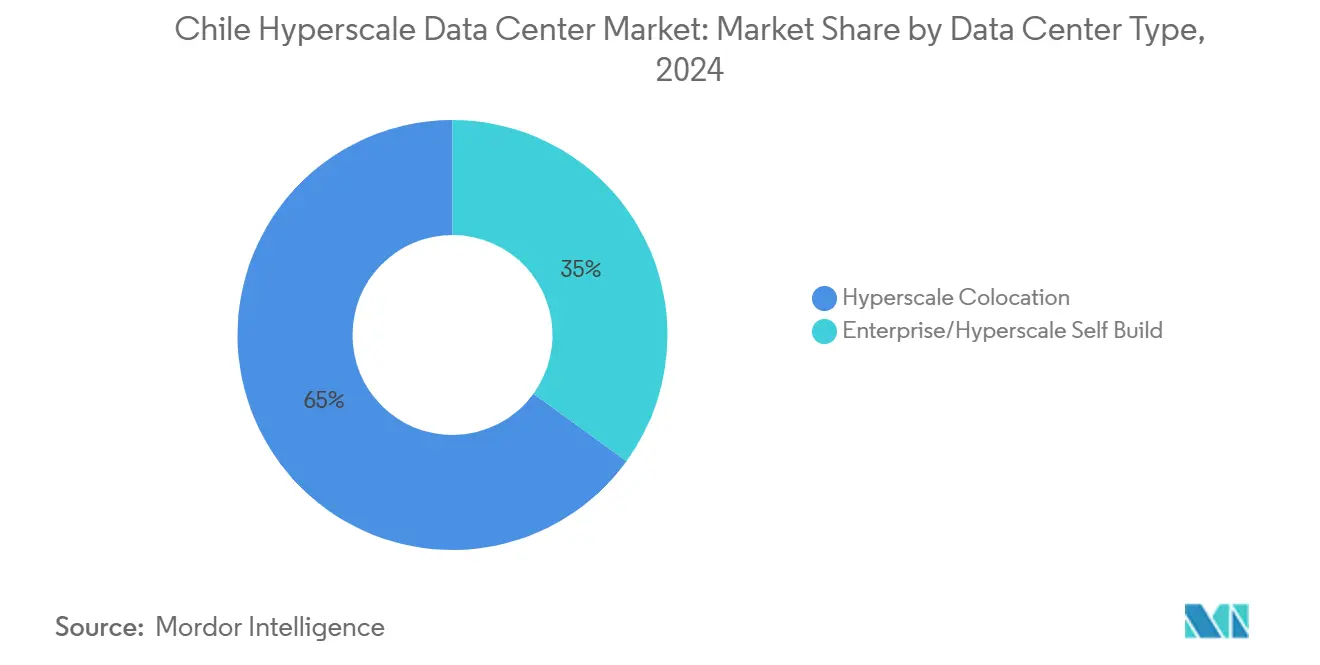

- By data-center type, hyperscale colocation led with 65% of Chile hyperscale data center market share in 2024; the enterprise/self-build segment is projected to expand at an 20% CAGR between 2025-2030.

- By service type, Infrastructure-as-a-Service accounted for 55% share of the Chile hyperscale data center market size in 2024, while Platform-as-a-Service is growing at a 15% CAGR through 2030.

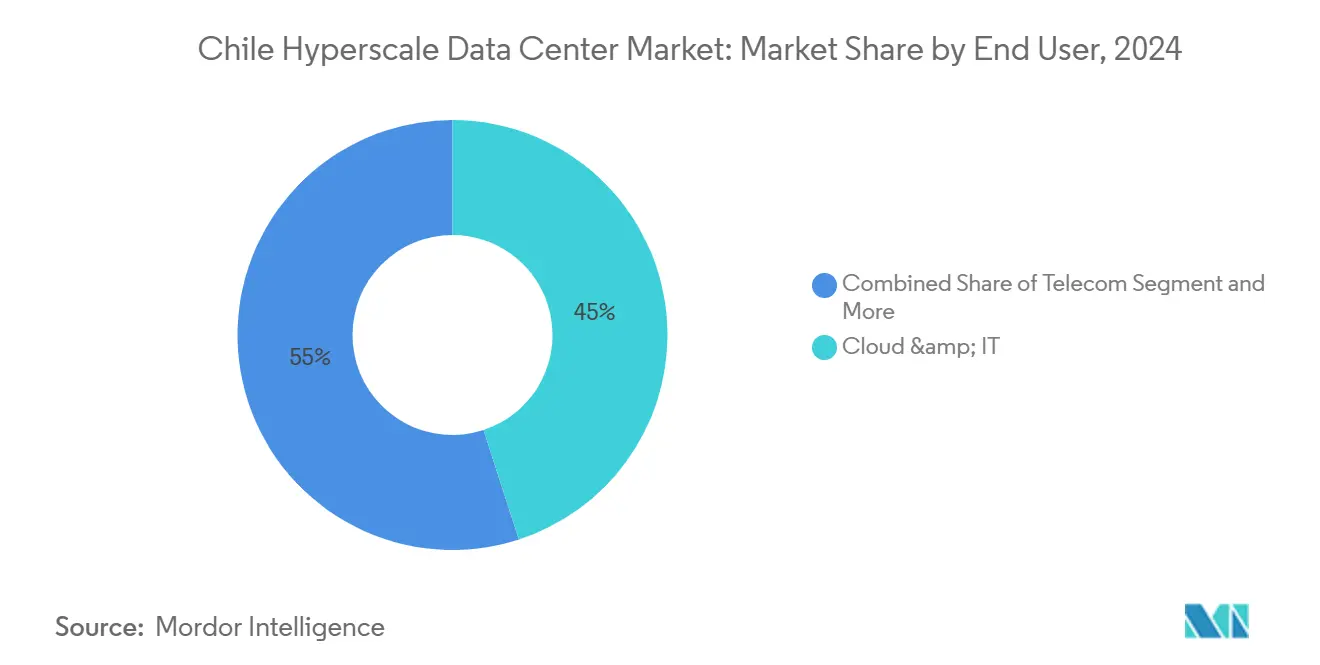

- By end user, Cloud and IT providers held 45% share of the Chile hyperscale data center market size in 2024; e-commerce is advancing at a 25% CAGR to 2030.

- By geography, Santiago captured 250 MW of installed IT power—roughly 65% of total capacity—while northern Chile is the fastest-growing cluster with a 22% CAGR driven by solar-powered campuses.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile represents one dimension of a structure that spans multiple countries, continents and economic zones. Our global hyperscale data center market report covers details on that full structure.

Chile Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI and big-data workloads | +7.2% | Nationwide; concentrated in Santiago | Medium term (2-4 years) |

| Abundant renewable power and green incentives | +5.8% | Northern solar belts; national transmission grid | Long term (≥ 4 years) |

| Humboldt cable cuts trans-Pacific latency | +4.5% | Coastal landing stations | Medium term (2-4 years) |

| Digital-Transformation Law | +3.1% | Nationwide | Short term (≤ 2 years) |

| Santiago rising as Latin American edge hub | +2.3% | Santiago metropolitan area | Medium term (2-4 years) |

| Tax credits in designated investment zones | +1.8% | Santiago and selected northern municipalities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in AI and big-data workloads

Chile hyperscale data center market operators are re-architecting campuses for 50 kW-plus racks that host H100 and forthcoming B200 GPU cards. AWS committed to expanding H100 inventory in its Chile Availability Zones during 2025 to meet generative-AI demand. International Energy Agency simulations indicate that a single AI-focused hall can consume electricity equivalent to 100,000 households, pressuring utilities to prioritize renewable additions [1]International Energy Agency, “Data Centres and Energy Consumption,” iea.org. Liquid-immersion and rear-door heat-exchange systems have moved from pilot to standard specification, and vendors reporting largest Chile orders in 2025 include Vertiv and Schneider Electric for warm-water cooling skids. Facilities offering AI-ready white space are commanding pricing premiums of 15-20% per kW, improving project return profiles despite higher capital intensity.

Abundant renewable power and green-energy incentives

Chile draws 31% of national generation from solar and wind, enabling data-center operators to lock PPAs at predictable tariffs. Microsoft signed a multi-year agreement with AES Andes to achieve 100% solar-plus-wind coverage for its Chile region by 2025. ODATA partnered with Atlas Renewable Energy on a similar structure that pairs a 112 MW solar farm with firming hydro capacity, lowering the colocation provider's weighted energy cost by 12%. Senate amendments in March 2025 made on-site battery storage eligible for accelerated depreciation, cutting effective tax rates on advanced UPS deployments. Operators are now co-developing utility-scale renewables, a shift that deepens energy security and enhances ESG scoring for hyperscale tenants.

Sub-sea Humboldt cable enhancing latency

The USD 400 million Humboldt system will shorten round-trip latency between Santiago and Sydney below 120 ms, positioning Chile as a landing point for Asia-Pacific workloads. Google and the Ministry of Transport and Telecommunications confirmed cable manufacturing completion in April 2025, with marine lay scheduled for Q3 2025 and commercial service by early 2026. Comparable to the economic uplift created by the Curie cable in 2020, the project is modeled to inject USD 19 billion into GDP and support 67,000 jobs by 2027. New edge facilities are breaking ground near Valparaíso and La Serena to interconnect with the Humboldt cable landing stations.

Chilean Digital-Transformation Law

The law effective July 2025—exempts inbound server hardware from VAT, slices corporate income tax to 10% for certified digital-infrastructure companies, and mandates government cloud adoption. Public-service digitization targets 95% completion by 2025, instantly creating workloads for identity, payments and healthcare datasets. SERNAC released preliminary AI governance guidelines in February 2025, giving operators legal clarity to host consumer-data training models. Early adopters report a 9-month reduction in procurement lead times for government cloud projects under the fast-track scheme.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seismic construction cost premium | −1.9% | Nationwide; highest in central valley fault zones | Long term (≥ 4 years) |

| Skilled-labor shortage in advanced cooling | −1.4% | National | Medium term (2-4 years) |

| Water scarcity for liquid cooling | −1.2% | Northern altiplano and Santiago outskirts | Long term (≥ 4 years) |

| Grid congestion in northern transmission | −0.8% | Antofagasta and Atacama solar corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Seismic construction cost premium

Chilean building codes require base-isolation and steel bracing capable of withstanding magnitude-9 events. Equinix disclosed in its 2024 Form 10-K that local greenfield projects carry a 15-25% capex premium relative to comparable Brazilian builds. Engineering firms Turner and Townsend and Fluor report lead times on seismically rated chillers extending to 42 weeks amid global supply constraints. Developers are experimenting with modular steel pods pre-certified for shake-table compliance, trimming site schedules by 12% but adding material costs. Despite the premium, steady revenue visibility through 20-year hyperscale leases offsets structural-risk surcharges in lender models.

Water scarcity for liquid cooling

Chile endured its 15th consecutive drought year in 2024, prompting regulators to screen data-center water use alongside mining and agriculture. Google’s site permit in Cerrillos was partially revoked in August 2024 after community appeals over aquifer depletion. Moody’s labeled data centers “emerging water-stress assets” in its January 2025 ESG heatmap. Operators are pivoting to closed-loop cooling and thermal-siphon heat reuse. TECfusions’ Puente Alto campus will implement a zero-water-use design that circulates dielectric fluid directly across cold plates, setting a template for future Chile hyperscale data center market entrants.[4]Victoria Advocate, “TECfusions Zero-Water Data Center Plans,” victoriaadvocate.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Type: Self-build momentum accelerates

Hyperscale colocation owns 65% Chile hyperscale data center market share in 2024, supported by operators such as Ascenty, ODATA and Scala Data Centers. At 250 MW installed, Santiago’s colocation footprint offers cloud-on-ramp, peering and interconnection services aligned with carrier hotels. This dominance of third-party space reflects enterprise preference for rapid deployment and opex funding models. However, the Chile hyperscale data center market size for enterprise/self-build footprints is projected to compound at 20% through 2030 as hyperscalers pursue dedicated halls optimized for liquid cooling and AI hardware.

The enterprise/self-build cohort is anchored by Amazon’s USD 4 billion Chile region, featuring three Availability Zones planned for service launch in 2026. Similar self-build blueprints from Google and Microsoft focus on 100-acre campuses outside quake-fault buffers and near renewable-energy substations. These projects grant operators greater PUE control, allow direct investment in on-site solar plus battery farms, and deliver proprietary network fabrics that outperform multi-tenant facilities. The hybrid strategy core self-build plus edge colocation will characterize hyperscaler real estate portfolios across Chile over the forecast horizon.

By Service Type: PaaS growth outpaces market

IaaS retains 55% share of Chile hyperscale data center market size in 2024, underpinning cloud foundations for compute, storage and networking. The segment’s scale is visible in Santiago’s six on-ramps to AWS Direct Connect, Google Cloud Interconnect and Oracle FastConnect. National demand is robust from fintech sandboxes, health-record digitization projects and content-distribution stacks. Platform-as-a-Service, while smaller, is pacing at a 15% CAGR to 2030 as local DevOps teams embrace container orchestration, serverless functions and AI toolchains. AWS’s January 2025 roll-out of Bedrock in Spanish and Portuguese catalyzed adoption among digital agencies building generative-AI chatbots.

SaaS solutions continue to diversify, but price-sensitive Chilean corporates often combine open-source components with managed PostgreSQL and Kafka services. Public-sector frameworks under the Digital-Transformation Law stipulate sovereign-cloud instances for sensitive workloads, amplifying demand for infrastructure that can host both multi-tenant PaaS and isolated workloads within the same availability zone. The resulting service-mix flexibility strengthens the Chile hyperscale data center market by drawing a fuller spectrum of cloud buyers into domestic facilities rather than distant U.S. west-coast regions.

By End User: E-commerce drives digital-infrastructure demand

Cloud and IT tenants captured 45% of Chile hyperscale data center market size in 2024 as global providers extend region availability to reduce latency and comply with data-sovereignty rules. AWS leads with an edge node in Quinta Normal, Microsoft with a forthcoming region in San Bernardo, Google with its long-standing Quilicura site, and Oracle operating twin clouds in Santiago. These deployments create gravitational pull for analytics, cybersecurity and backup workloads that migrate from on-premise server rooms.

E-commerce tops growth at a 25% CAGR to 2030. Retailers Falabella and Mercado Libre doubled click-through conversions after migrating catalog search and recommendations onto GPU-accelerated clusters housed in Santiago data halls. Cross-border logistics platforms leverage the Humboldt cable to deliver sub-250 ms checkout performance for Asian shoppers buying Chilean wine or lithium battery packs. BFSI workloads follow closely as banks implement ISO 20022 real-time-payments clearing, requiring ultra-low-latency interconnects and high-availability zones within metropolitan fault lines. Secondary verticals—media streaming, gaming, manufacturing and telecom—are adopting hybrid clouds but remain smaller contributors to occupied megawatts.

Geography Analysis

Santiago anchors the Chile hyperscale data center market with 250 MW of live IT load and 50 MW in active builds, equivalent to roughly 83% of national capacity. Three-phase power redundancy, eight fiber rings and proximity to 40% of the nation’s GDP make the capital the default landing point for new entrants. However, escalating land premiums averaging USD 3 million per acre within tech corridors along with longer municipal approval cycles are prompting operators to scout peripheral communes such as Lampa and Paine. Even with these pressures, Santiago’s colocation facilities maintain 85% average occupancy rates and continue to absorb AI-GPU deployments that demand dense fiber cross-connects.

Northern Chile is emerging as a renewable-first cluster. The Atacama Desert offers world-class solar irradiance, enabling 24 / 7 net-zero PPAs at competitive tariffs. Atlas Renewable Energy has reserved 112 MWAC from its Sol del Desierto farm to back ODATA’s upcoming Calama campus. Grid-congestion risk along the Antofagasta-Santiago 500 kV lines has delayed some projects, yet the Ministry of Energy’s March 2025 auction of dynamic-line-rating upgrades promises 14 GW of incremental north-to-center transfer capacity by 2027. Northern projects must also contend with water stress; thus, most designs rely on closed-loop evaporative-free cooling to sidestep groundwater permitting.

Mordor Intelligence tracks the hyperscale data center market across other major regions such as North America, Middle East, and Africa, with additional country-level coverage spanning Canada, Mexico, Israel, South Africa, Thailand, and Philippines, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Chile hyperscale data center market is moderately concentrated. The four largest operators AWS, Microsoft, Google and Oracle when combined with the three main colocation specialists Ascenty, ODATA and Scala control around 78% of commissioned megawatts. AWS is executing a USD 4 billion self-build region expected online by late 2026, featuring heat-reuse into district-heating networks for nearby residential. Microsoft’s San Bernardo region will run entirely on wind and solar delivered under a 20-year PPA with AES Andes. Google partnered with the Ministry of Science to study geothermal cooling options at its Quilicura campus as part of its 24/7 Carbon-Free Energy commitment.

Colocation specialists are honing differentiation on scale-out blocks, connectivity fabrics and sustainability. Ascenty filed environmental approvals in March 2025 for a 36-MW hall adjacent to its existing SCL2 site, promising water-free cooling and solar-powered rooftop UPS. Scala Data Centers, backed by DigitalBridge, announced an 80-MW campus in Curauma focused on AI clusters that require 50 kW per rack. Equinix, having acquired Entel’s four data centers in 2022 for USD 638 million, is upgrading them to its “xScale” specification to win dedicated hyperscaler pods.[3]U.S Securities and Exchange Commission, “Equinix Form 10-K 2024,” sec.gov

Chile Hyperscale Data Center Industry Leaders

Amazon Web Services Inc.

Google LLC

Microsoft Corporation

Huawei Technologies Co., Ltd.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amazon confirmed more than USD 4 billion for a new AWS infrastructure region with three Availability Zones scheduled for late 2026.

- May 2025: Pátria Investments launched Omnia, a USD 1 billion AI-ready hyperscale platform spanning Brazil, Mexico and Chile.

- January 2025: ODATA signed a PPA with Atlas Renewable Energy to power all Chile operations from solar and wind assets .

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Chile hyperscale data center market as all capital and operational spending tied to facilities that supply at least 4 MW of contiguous IT load to a single tenant or cloud region, together with the associated network backbones, on-site electrical and mechanical systems, and critical support services that keep those halls live. According to Mordor Intelligence, the scope captures both self-built campuses owned by global cloud providers and wholesale hyperscale suites leased from colocation landlords.

Scope Exclusions: edge micro sites below 1 MW, carrier hotels focused on interconnection only, and pure software IaaS revenues remain outside the baseline.

Segmentation Overview

- By Data Center Type

- Hyperscale Colocation

- Enterprise/Hyperscale Self Build

- By Service Type

- IaaS ( Infrastructure-as-a-Service)

- PaaS ( Platform-as-a-Service)

- SaaS( Software-as-a-Service)

- By End User

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility design engineers in Santiago, regional cloud infrastructure directors, electrical-equipment suppliers, and renewable-energy brokers across Chile and Brazil. These conversations clarified typical rack densities, landed PPA pricing, build timelines, and expected availability-zone footprints, giving us ground truth to validate secondary findings and fine-tune glide paths.

Desk Research

We started with public domain material such as InvestChile incentive filings, Comision Nacional de Energia power statistics, Subtel spectrum deployment updates, and customs import codes for server and switch assemblies. Trade associations like the Chilean Data Center Council and international groups such as the Uptime Institute supplied design and tier trends, while peer-reviewed pieces in IEEE Xplore outlined energy-efficiency benchmarks. Our team also tapped D&B Hoovers and Dow Jones Factiva to screen operator financials and news flow. The sources cited represent only a sample; many additional references informed variable selection, sanity checks, and narrative context.

Market-Sizing & Forecasting

A top-down reconstruction begins with national installed IT load and new-build pipelines, followed by capex-per-MW and opex-per-MW curves to translate capacity into dollar terms; selective bottom-up roll-ups of sampled campus contracts then test the totals. Key variables include cumulative permitted megawatts, average power usage effectiveness, long-term renewable PPA prices, Santiago fiber-pair landings, 5Gmobile data traffic, and corporate cloud adoption rates. Forecasts rely on multivariate regression supported by ARIMA overlays to capture cyclical power-price swings, with parameter ranges reviewed by our primary experts. Gap handling for missing campus costs uses analog builds from the Marklines and IMTMA paid datasets to impute material shares before the model locks.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, senior-analyst challenge sessions, and scheduled re-checks against quarterly build announcements. Reports refresh each year; yet material events such as a new 100 MW AWS zone approval trigger interim model patches so clients always receive the latest vetted view.

Credibility Anchor - Why Mordor's Chile Hyperscale Data Center Baseline Commands Reliability

Published estimates seldom align because firms pick different facility thresholds, measure investment instead of revenue, or freeze exchange rates too early.

Key gap drivers here include: some studies roll smaller wholesale halls into 'hyperscale,' others stop at capital outlays and ignore multi-year opex, and a few project growth from a 2023 base that predates the USD 4 billion AWS Las Cabras region. Mordor's framework, by matching >=4 MW tenant demand with real build and operating cost curves and by refreshing variables annually, minimizes these skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.41 B (2025) | Mordor Intelligence | - |

| USD 0.77 B (2024) | Regional Consultancy A | tracks only upfront investment, folds enterprise halls, excludes opex streams |

| USD 0.74 B (2023) | Trade Journal B | earlier base year, counts projects >5 MW only, static FX rate |

| USD 0.50 B (2023) | Global Consultancy A | measures total data-center revenue, not hyperscale-specific, omits self-built cloud campuses |

The comparison shows that once differing scopes, years, and cost inclusions are reconciled, Mordor's cadence-checked model offers the most balanced, transparent baseline for decision-makers in Chile's rapidly scaling hyperscale arena.

Key Questions Answered in the Report

How large is the Chile hyperscale data center market in 2025?

Spending on hyperscale data-center build-outs and services in Chile totals USD 1.41 billion in 2025, with installed IT power of about 250 MW concentrated in Santiago

What CAGR is expected for Chile’s hyperscale data center capacity up to 2030?

Aggregate market value is projected to expand at a 23.27% CAGR, driven by self-build expansions from global cloud providers and aggressive renewable-energy procurement.

Which data-center type is growing the fastest in Chile?

Enterprise or self-build hyperscale campuses are forecast to grow at 20% annually as operators pursue tailor-made halls optimized for GPU-dense AI workloads.

How will the Humboldt submarine cable affect Chile’s data center market?

The cable, operational in 2026, will cut trans-Pacific latency to below 120 ms and is modeled to add USD 19 billion to GDP by fostering new edge deployments along the coast.

Page last updated on: