Architectural Polyvinyl Butyral (PVB) Interlayers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

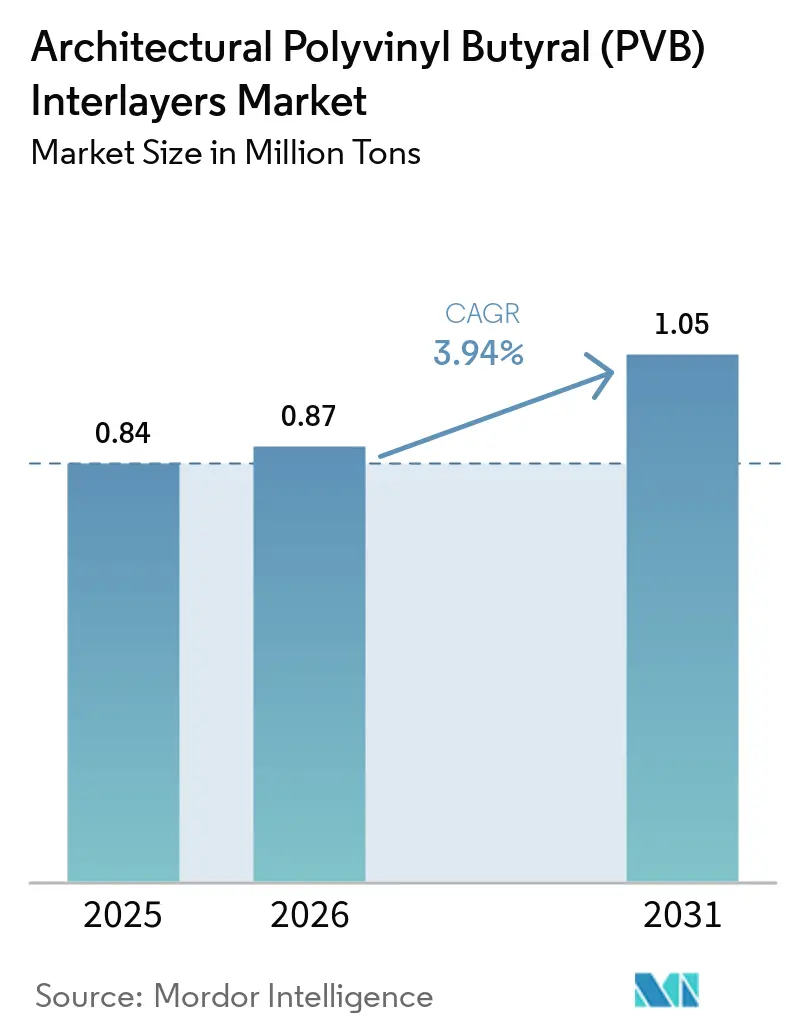

| Market Volume (2026) | 0.87 Million tons |

| Market Volume (2031) | 1.05 Million tons |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

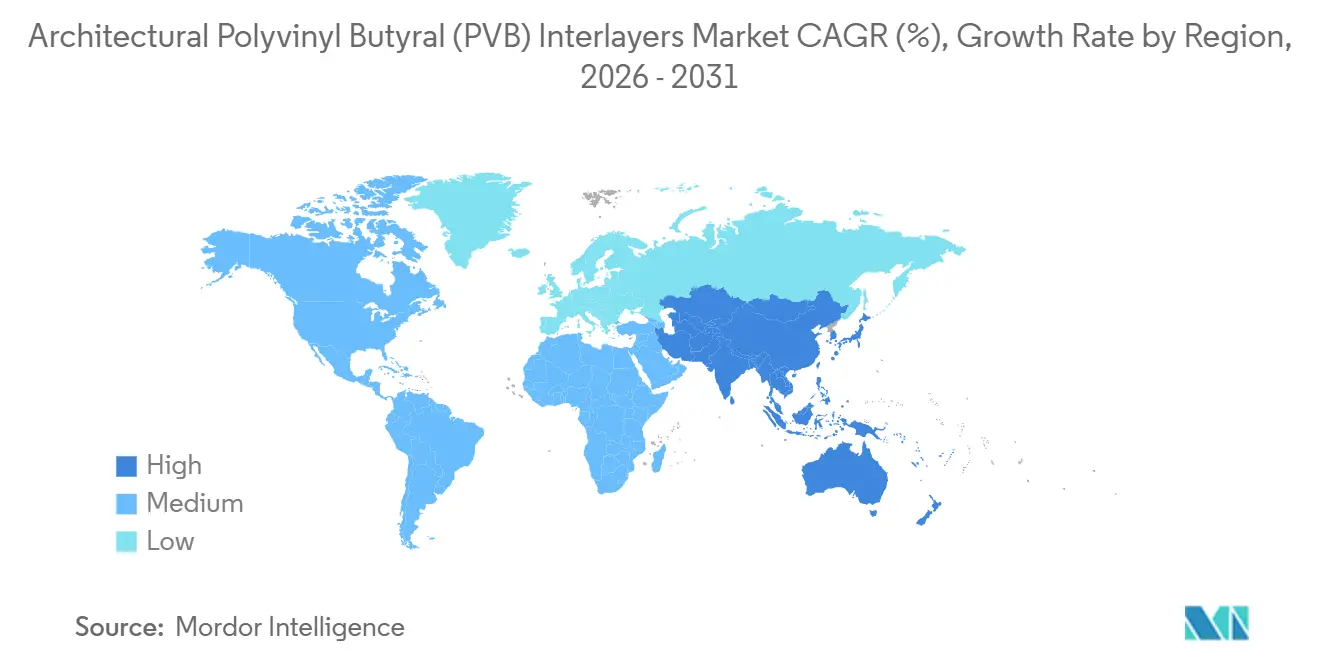

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Architectural Polyvinyl Butyral (PVB) Interlayers Market Analysis by Mordor Intelligence

The Architectural Polyvinyl Butyral Interlayers Market size is projected to be 0.84 million tons in 2025, 0.87 million tons in 2026, and reach 1.05 million tons by 2031, growing at a CAGR of 3.94% from 2026 to 2031. Specification upgrades, focusing on safety, acoustics, and energy performance, now drive volume growth more than new constructions do, particularly in the realm of laminated glass. The architectural polyvinyl butyral (PVB) interlayers market is experiencing growth due to innovations such as ionoplast and stiff-PVB. This growth is further supported by code-driven demands for thicker interlayers in balustrades and Asia-Pacific policy mandates advocating near-zero-energy envelopes. While transparent grades led in demand, ionomer films have made notable progress, benefiting from stricter post-breakage deflection limits. Asia-Pacific, already a major contributor to global tonnage, continues to grow at a faster pace. This momentum is largely attributed to China's ambitious dual-carbon targets, which aim to link building-envelope U-values to a stringent drop of 0.8 W/m² K in severe-cold zones. In the region's glazing output, prefabricated curtain-wall modules are now at the forefront, directing interlayer procurement towards suppliers recognized for their autoclave consistency and ISO-tracked quality.

Key Report Takeaways

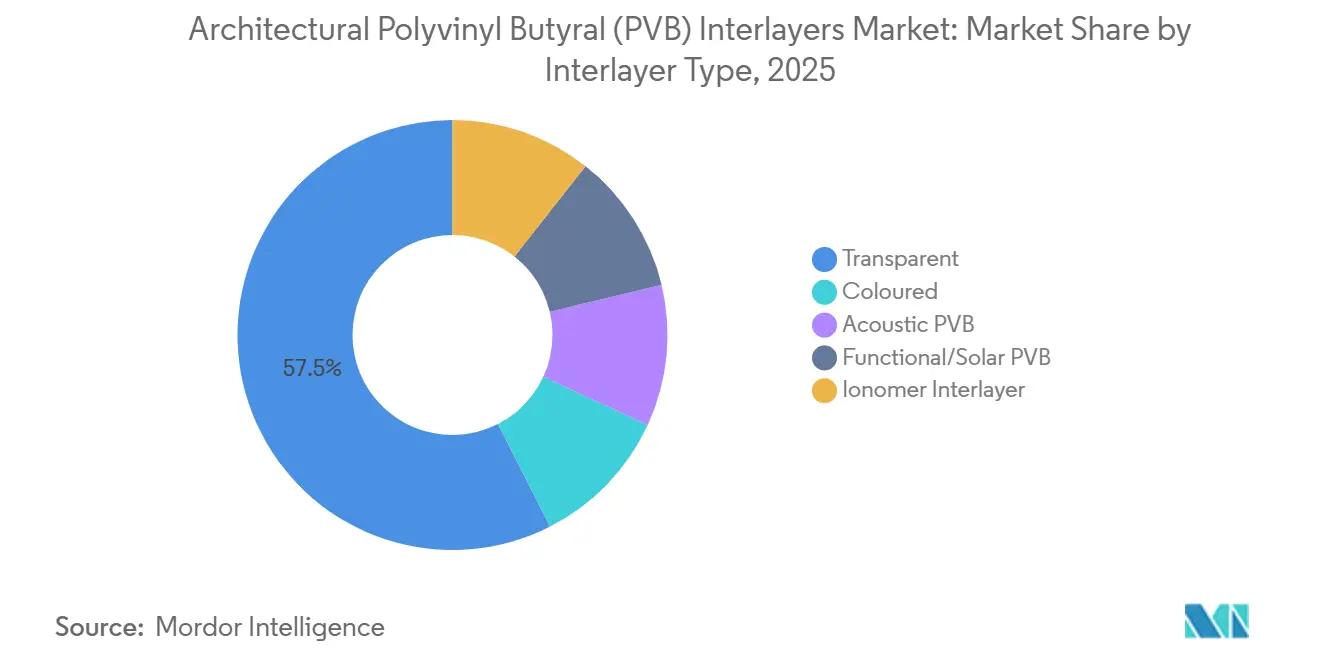

- By interlayer type, transparent PVB commanded 57.5% of the architectural polyvinyl butyral (PVB) interlayers market share in 2025, while ionomer films are projected to advance at a 5.19% CAGR between 2026 and 2031.

- By application, façades and curtain walls held 52.28% share in 2025 and are on track for a 4.18% CAGR between 2026 and 2031.

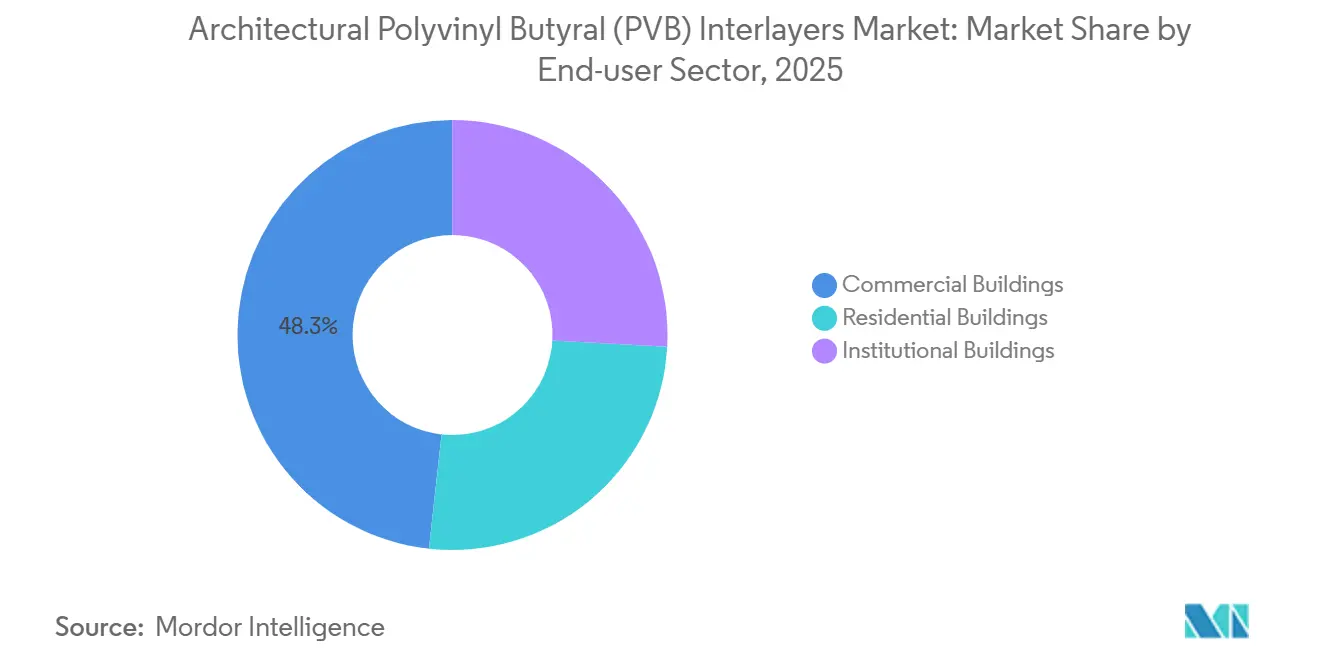

- By end-user sector, commercial buildings led with 48.26% share of the architectural polyvinyl butyral (PVB) interlayers market size in 2025, whereas residential retrofits are expected to post the strongest 4.01% CAGR outlook between 2026 and 2031.

- By geography, Asia-Pacific captured 45.43% of the 2025 architectural polyvinyl butyral (PVB) interlayers market share and is set to grow at 4.87% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Architectural Polyvinyl Butyral (PVB) Interlayers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for safety and security glazing in modern architecture | +1.2% | Global, with regulatory intensity highest in North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Expanding the APAC construction sector | +1.5% | APAC core (China, India, ASEAN), spill-over to the Middle-East | Short term (≤ 2 years) |

| Tightening energy-efficiency codes is driving laminated façade adoption | +0.8% | Europe, North America, China (near-zero energy building zones) | Long term (≥ 4 years) |

| Aesthetic differentiation via gradient and colored interlayers | +0.3% | Global, with premium adoption in commercial and institutional projects | Medium term (2-4 years) |

| Growing retrofit market for acoustic comfort in dense cities | +0.6% | Urban centers in APAC, Europe, and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Safety and Security Glazing in Modern Architecture

During 2024–2025, updated building codes mandate the use of laminated glass in handrails, guards, and sloped glazing, specifying a minimum interlayer thickness of 0.76 mm. The ASTM E2358-24 standard improves post-breakage deflection performance, subtly encouraging designers to adopt ionomer or stiff-PVB films, which ensure the glass remains intact after fracturing[1]ASTM International, “E2358-24 Standard Specification for Glazing in Permanent Railing Systems,” astm.org. Field tests conducted in 2025 reveal that triple-layer laminates with ionomer cores can handle significant line loads at high temperatures, whereas tempered monoliths with basic PVB fail. In Singapore, authorities establish a limit for total top-edge deflection in cases of complete glass loss. Standard PVB struggles to meet this benchmark without extensive multi-ply constructions. As inspectors increasingly require permanent markings and traceable test reports, documentation demands intensify, providing certified brands with a notable advantage.

Expanding APAC Construction Sector

China's dual-carbon policy has significantly increased the adoption of high-performance glass, resulting in higher laminated volumes without requiring additional raw floor space. In China, modular curtain-wall factories, which produce two-thirds of the nation's output, are now using consistent-tack PVB rolls designed for their automated production lines. Builders in India, Vietnam, and Indonesia are retrofitting high-rise towers for noise control and updating safety codes. Highlighting the tightness of the regional supply chains, domestic resin suppliers, such as Anhui Wanwei, have expanded their capacities, underscoring the dominance of the Asia-Pacific region in the upstream polyvinyl alcohol feedstock market.

Tightening Energy-Efficiency Codes Driving Laminated Façade Adoption

In cold regions, designers aim for composite U-values under 1.0 W/m² K to create near-zero-energy envelopes. They achieve thermal and fallout-prevention goals by using laminated units featuring PVB or ionoplast outer lites. Both LEED and BREEAM provide credits for features such as UV cut, glare control, and low SHGC. Laminated configurations offer these advantages while maintaining daylight. In the Northeast United States, triple-glazed IGUs with a laminated pane outperform double glazing in reducing heating loads. This efficiency compensates for the added weight, thanks to slimmer glass designs enabled by stiffer interlayers. As a result, the market for architectural polyvinyl butyral (PVB) interlayers flourishes, driven by policies that emphasize long-term energy savings over short-term material expenses.

Aesthetic Differentiation via Gradient and Colored Interlayers

Architects can now achieve an 80 cm transition from opaque to clear with a single 0.76 mm film, thanks to innovations like SEKISUI Cielora from Gradient products[2]SEKISUI Chemical, “Cielora Gradient PVB,” sekisuichemical.com. This advancement eliminates the traditional reliance on ceramic frit and stick-on privacy foils, streamlining the process with one laminated layer. Vanceva's color systems, offering thousands of tone combinations, not only elevate branding value but also command premium prices in green-certified developments. Beijing’s Rainbow Glass Cliff, located in the Asia-Pacific region and set to debut in 2026, exemplifies the allure of colored interlayers as a visual centerpiece, drawing in a significant annual visitor count. The architectural polyvinyl butyral (PVB) interlayers market sees a surge in potential, as aesthetic appeal rivals safety compliance in purchasing decisions during the forecast period of 2026–2031.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost and limited substitution flexibility | -0.9% | Global, with acute price sensitivity in cost-competitive residential and emerging-market projects | Medium term (2-4 years) |

| Moisture sensitivity and edge-stability issues in harsh climates | -0.5% | Coastal, tropical, and high-humidity regions (Southeast Asia, Middle-East coastal zones, tropical Americas) | Long term (≥ 4 years) |

| Volatility in PVB-resin feedstock supply | -0.3% | Global, with supply-chain concentration in China and limited alternative sourcing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Limited Substitution Flexibility

Ionomers command a premium price, yet they offer a shear modulus that is significantly greater than that of standard PVB. In May 2026, Kuraray, citing rising energy and additive costs, announced a global price increase for both PVB and ionomer products. Once a balustrade design is approved for ionoplast, reverting to PVB requires fresh testing under ASTM E2358, making such changes infrequent. Medium-sized laminators, lacking autoclave redundancy, face capital challenges, which delay their market entry and result in a moderate concentration in the architectural polyvinyl butyral (PVB) interlayers market.

Moisture Sensitivity and Edge-Stability Issues in Harsh Climates

PVB's hygroscopic nature makes it prone to edge milkiness during salt-spray cycles, unless cap rails or sealants effectively block ambient moisture. Kuraray's stiff-PVB B231 endured extensive ISO 9227 testing without delaminating. In contrast, ionoplast exhibits near immunity, maintaining clarity in frameless canopies at Gulf Coast resorts. In jurisdictions that permit exposed-edge balconies, the durability of ionomer often drives its preference, leading to a reduction in the volume of standard PVB grades in the architectural polyvinyl butyral (PVB) interlayers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Interlayer Type: Ionomer Outpaces Commodity Shift

By 2025, transparent grades captured 57.5% of the market volume. Their seamless welding with glass, neutral optical properties, and compatibility with existing autoclave cycles cemented their position as the preferred choice for mainstream façades. The market for architectural polyvinyl butyral (PVB) interlayers, particularly transparent films, has seen modest growth in alignment with the construction GDP.

Starting from a smaller base, ionomer films showcased the strongest growth, boasting a 5.19% CAGR during the forecast period of 2026–2031. This uptick was spurred by regulatory code clauses that curtailed deflection in broken balustrades. In 2025 field trials, laminates with 3.04 mm ionoplast cores, nestled between 8 mm heat-strengthened plies, withstood 1.5 kN/m loads, validating safety without top rails. Colored and gradient PVBs addressed twofold demands: branding and privacy, utilizing colorfast chemistries to block 99% of UV rays. Acoustic PVBs, featuring softer cores, boosted the Sound Transmission Class (STC) by 2–5 points. This enhancement has made them a top pick for residential retrofits, enabling landlords to charge premium rents for quieter spaces. Lastly, functional solar-control PVBs, equipped with infrared blockers, curbed peak cooling loads by 10–15 W/m², all while permitting 80% visible light transmission.

By Application: Façade Dominance Reflects Modular Prefabrication

In 2025, façades and curtain walls dominated the market, holding a 52.28% share and projected to grow at a CAGR of 4.18% during the forecast period of 2026–2031. In China and the Middle-East, automated workshops have refined roll-fed lamination lines for curtain walls, achieving consistent thickness throughout the day. This precision has streamlined procurement, relying heavily on a select group of ISO-certified suppliers. Although balcony and guard-rail glass accounts for a smaller tonnage, it sets the industry's performance benchmark. Frameless designs, utilizing ionomer or stiff-PVB, excel in dynamic-impact tests, thereby increasing their value per kilogram.

In hybrid workplaces, ultra-clear or gradient films are increasingly used in interior partitions, balancing privacy with natural light. Roof-lights and canopies now incorporate interlayers of 0.76 mm or thicker, eliminating the need for metal retention screens typically required in sloped-glazing. The rise of BIPV glass signals a nascent sector, emphasizing the importance of PVB's compatibility with transparent conductive oxides and junction lamination processes. This trend suggests a growing niche demand in the architectural polyvinyl butyral (PVB) interlayers market.

By End-User Sector: Residential Retrofit Accelerates

In 2025, commercial towers, from flagship corporate façades to airport terminals, drove 48.26% of shipments using laminated glass. This surge in the market coincided with Grade-A office refurbishments, hospitality upgrades, and data-center cladding, all emphasizing laminated glass to adhere to blast and forced-entry standards.

Residential demand, growing at a 4.01% CAGR in the forecast period of 2026 to 2031, was swift to pivot, spurred by safety glazing mandates in doors and stair panels and urban noise reduction needs. Urban tenants increasingly favored acoustic glass retrofits. Institutional entities, such as schools, hospitals, and museums, chose laminated units, emphasizing security and hygiene. Their heightened demand for environmental product declarations also favored manufacturers boasting cradle-to-gate carbon audits.

Geography Analysis

Asia-Pacific, projected to account for 45.43% of the global volume in 2025, is set to register a 4.87% CAGR during the forecast period of 2026–2031. In a bid to strengthen its green initiatives, China revised its energy code, capping U-values at 0.8 W/m²·K in its colder provinces. Additionally, the nation linked public project bids to green product certifications, increasing the prominence of laminated glass. In India, a 2025 safety amendment endorsed laminated glass for balcony rails in buildings exceeding 15 meters in height. The ASEAN region, responding to heightened acoustic specifications near new metro lines, saw a notable surge in demand. North America benefited from regulations on hurricane, seismic, and security glazing. Europe sustained its momentum through whole-life carbon reporting initiatives under Level(s) and compliance with national balustrade standards. Similarly, Latin America and the Middle-East experienced a demand spike from boutique high-rise clusters, which increasingly favored imported premium interlayers.

Competitive Landscape

The architectural polyvinyl butyral (PVB) interlayers market is moderately consolidated. Chinese players are capitalizing on captive PVA and benefiting from reduced power tariffs. However, they face challenges in obtaining international certifications and mastering color-gradient technology. The innovation spotlight is now on lower-carbon resins, recycled materials, and solutions for traceability. Kuraray's CertiPly blockchain tag exemplifies this trend, positioning Kuraray as a pivotal player for future orders from both government bodies and branded corporations.

Architectural Polyvinyl Butyral (PVB) Interlayers Industry Leaders

Eastman Chemical Company

Kuraray Co., Ltd.

SEKISUI Chemical Co., Ltd.

Chang Chun Group

Anhui Wanwei Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kuraray Co., Ltd. implemented a 10% global price increase for all Trosifol PVB and Mowital ionomer grades, effective May 1, 2026.

- November 2024: Eastman broke ground on an extrusion upgrade at its Ghent, Belgium, factory, slated for completion in 2026 and designed to lift Saflex interlayer capacity for both automotive and architectural clients.

Global Architectural Polyvinyl Butyral (PVB) Interlayers Market Report Scope

Architectural polyvinyl butyral (PVB) interlayer is a high-performance, tough, and elastic thermoplastic film, created by plasticizing polyvinyl alcohol (PVA) with butyraldehyde. It is used to bond two or more panels of architectural glass under heat and pressure, forming laminated safety glass. This interlayer provides superior optical clarity, safety through fragment retention, sound dampening, and ultraviolet (UV) shielding, making it a critical component in modern building structures.

The architectural polyvinyl butyral (PVB) interlayer market is segmented by interlayer type, application, end-user sector, and geography. By interlayer type, the market is segmented into transparent, colored, acoustic PVB, functional/solar PVB, and ionomer interlayer. By application, the market is segmented into façade/curtain wall, balcony and balustrade/guard-rail, interior partitions and privacy screens, and roof-lights/skylights/canopies. By end-user sector, the market is segmented into commercial buildings, residential buildings, and institutional buildings. The report also covers the market size and forecasts for the market in 18 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (Tons).

| Transparent | |

| Coloured | Opaque |

| Frosted/Matte | |

| Gradient and White Gradient (incl. Cielora and similar products) | |

| Acoustic PVB | |

| Functional/Solar PVB | |

| Ionomer Interlayer |

| Façade/Curtain Wall |

| Balcony and Balustrade/Guard-rail |

| Interior Partitions and Privacy Screens |

| Roof-lights/Skylights/Canopies |

| Commercial Buildings |

| Residential Buildings |

| Institutional Buildings |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Interlayer Type | Transparent | |

| Coloured | Opaque | |

| Frosted/Matte | ||

| Gradient and White Gradient (incl. Cielora and similar products) | ||

| Acoustic PVB | ||

| Functional/Solar PVB | ||

| Ionomer Interlayer | ||

| By Application | Façade/Curtain Wall | |

| Balcony and Balustrade/Guard-rail | ||

| Interior Partitions and Privacy Screens | ||

| Roof-lights/Skylights/Canopies | ||

| By End-user Sector | Commercial Buildings | |

| Residential Buildings | ||

| Institutional Buildings | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is expected for the architectural polyvinyl butyral (PVB) interlayers market between 2026 and 2031?

The market is forecast to expand at a 3.94% CAGR over 2026-2031, reaching 1.05 million tons by 2031 from 0.87 million tons.

Which interlayer type is growing the fastest?

Ionomer films lead the growth table with a projected 5.19% CAGR from 2026 to 2031 because of stricter post-breakage codes.

Why is Asia-Pacific the largest regional consumer?

Dual-carbon policy in China, rapid urbanization, and modular curtain-wall factories lift Asia-Pacific to 45.43% of 2025 volume with a 4.87% CAGR from 2026 to 2031.

How do acoustic PVB interlayers improve building comfort?

Specialized acoustic grades can cut exterior noise, lifting STC ratings to around 50 dB when paired with argon-filled cavities.

Page last updated on: