Polyether Polyol Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.67 Billion |

| Market Size (2031) | USD 22.89 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

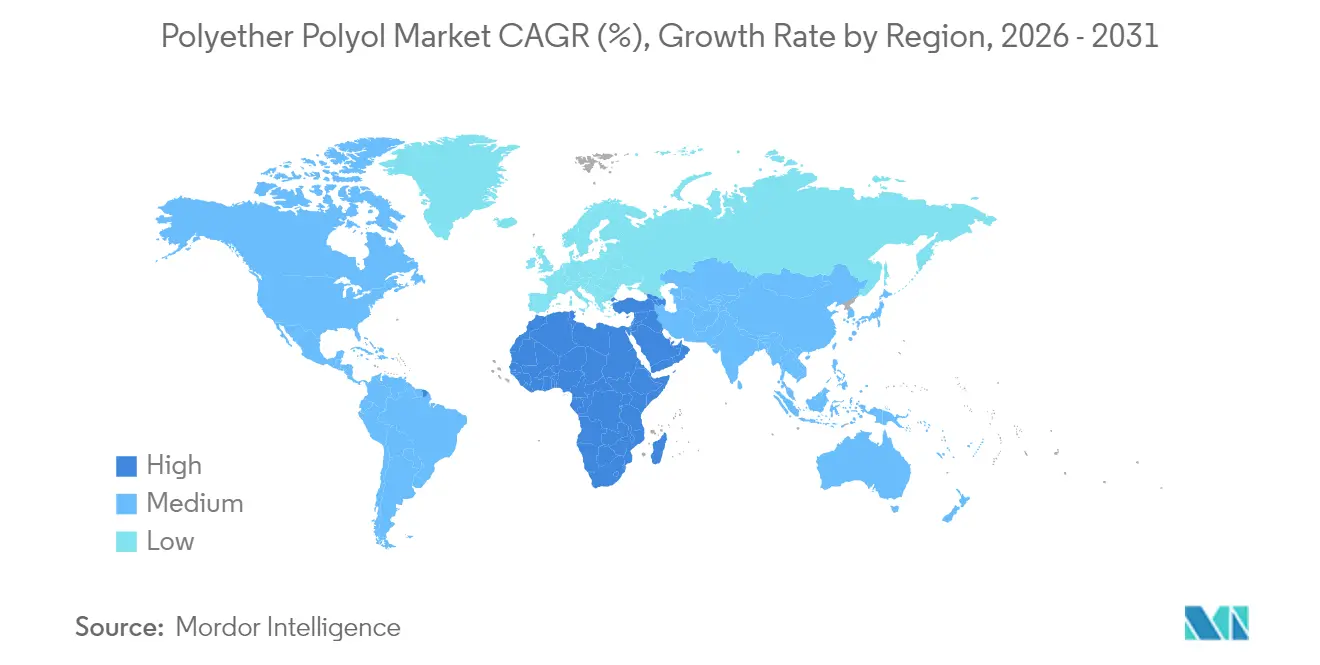

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

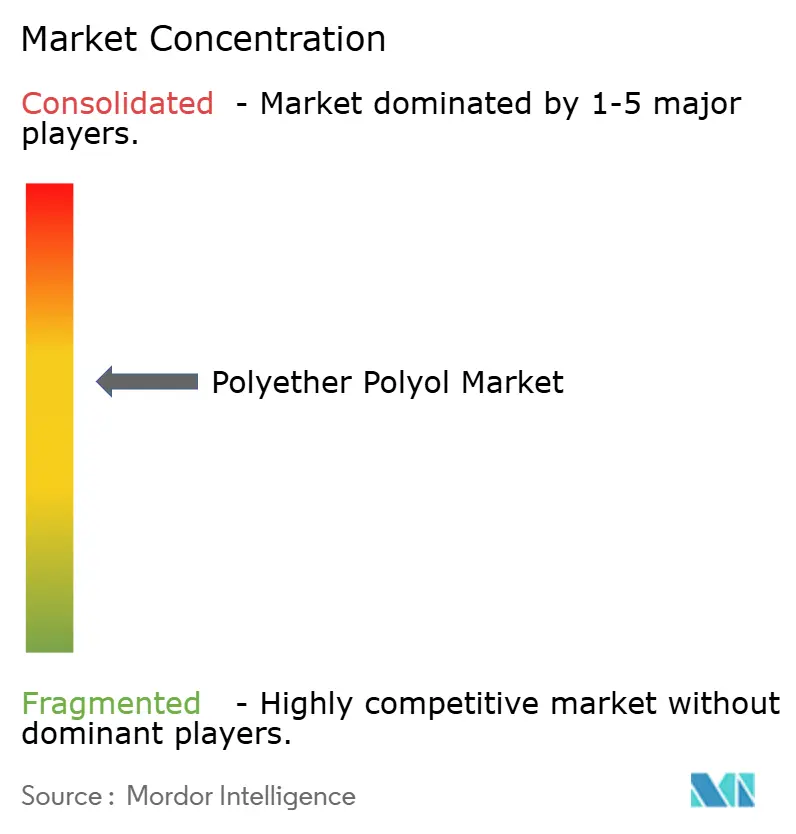

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyether Polyol Market Analysis by Mordor Intelligence

The Polyether Polyol Market size is expected to grow from USD 16.78 billion in 2025 to USD 17.67 billion in 2026 and is forecast to reach USD 22.89 billion by 2031 at 5.32% CAGR over 2026-2031. Strong insulation demand in new-build and retrofit construction, paired with lightweighting imperatives in electric vehicles, underpins steady volume gains despite raw-material cost volatility. Rigid polyether polyols retained pricing power through 2024 thanks to their superior thermal performance, while flexible grades captured premium margins in furniture, bedding, and automotive seating. Rapid technology adoption—especially CO₂-based synthesis routes—continues to lift the sustainability profile of polyurethane foams, and petrochemical integration strategies in the Middle East are reshaping global supply chains. Competitive intensity has increased as feedstock swings compress margins, prompting capacity rationalization, price announcements, and differentiated product development.

Key Report Takeaways

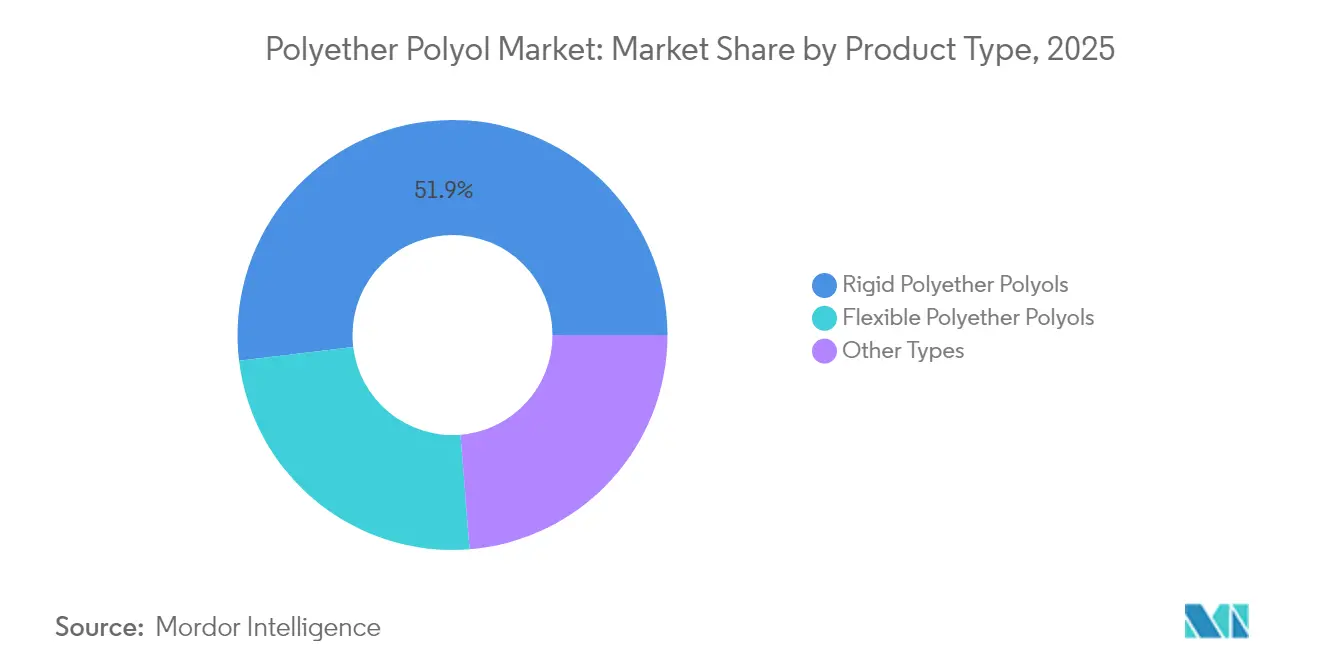

- By product type, rigid polyether polyols held 51.92% revenue share in 2025, whereas flexible polyether polyols are advancing at a 5.74% CAGR to 2031.

- By application, rigid PU foam commanded 45.62% share of the polyether polyol market size in 2025; the CASE (Coatings, Adhesives, Sealants, Elastomers) segment is growing the fastest at 5.98% CAGR through the forecast.

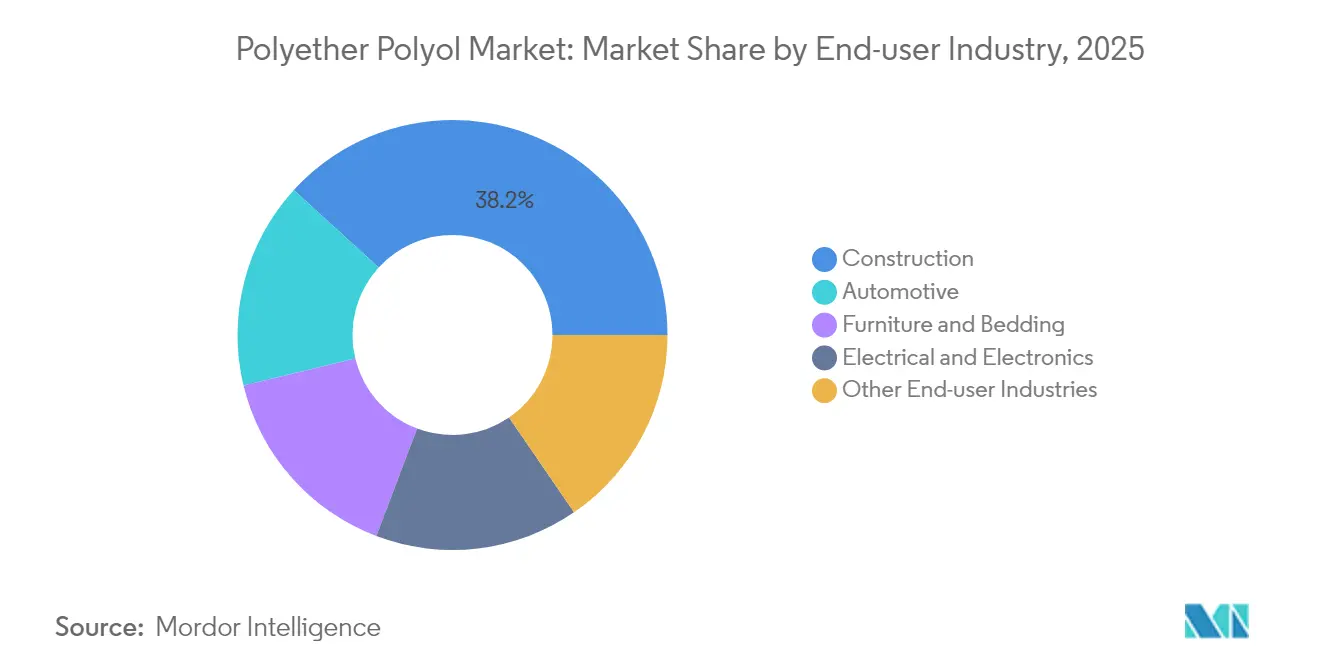

- By end-user industry, construction led with 38.21% share in 2025, while automotive is projected to post the highest CAGR at 6.08% through 2031.

- By geography, Asia-Pacific accounted for 44.05% of 2025 revenues, whereas the Middle-East and Africa is forecast to expand the quickest at 5.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyether Polyol Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low emission flexible foams | +0.8% | Global, led by EU and North America | Medium term (2-4 years) |

| CO₂-based polyol decarbonization | +0.7% | EU and North America, rising APAC | Long term (≥ 4 years) |

| Cold-chain build-out in emerging economies | +0.9% | Core APAC, spill-over MEA and South America | Short term (≤ 2 years) |

| Lightweighting in e-mobility interiors | +0.6% | Germany, China, U.S., Japan | Medium term (2-4 years) |

| Renewable-energy insulation demand | +0.5% | Global wind and solar hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Ultra-Low Emission Flexible Foams

Indoor-air-quality standards in Europe and North America are reshaping polyurethane formulations as regulators tighten VOC limits on construction materials. Producers have migrated from KOH to double-metal-cyanide catalysis to reduce unsaturated by-products, enabling flexible foams to meet stringent emission thresholds without sacrificing comfort or tensile properties. BASF markets several Lupranol grades engineered for these requirements, helping furniture and bedding manufacturers secure green-building certifications[1]BASF, “Polyols,” basf.com. California’s revised HFC restrictions on blowing agents add another compliance layer, strengthening demand for compatible polyether polyols that deliver low-VOC and low-GWP performance in rigid building insulation. Green-label programs such as LEED and WELL increasingly cite emission scores, turning low-emission polyols into a decisive procurement criterion for architectural projects.

Decarbonization Push Favoring CO₂-Based Polyols

Petrochemical incumbents are scaling carbon-utilization technologies that incorporate captured CO₂ into the polyol backbone, thereby lowering scope-3 emissions for downstream foam processors. Commercial polycarbonate polyols demonstrate superior hydrolytic resistance and tensile strength when blended at 10-25% with standard polyether grades, enabling customers to improve mechanical performance while claiming verified CO₂ savings[2]John Sinclair, “Polycarbonate Polyols,” polymerexpert.biz . Covestro has earmarked EUR 100 million for circular-chemistry research and development, including chemical recycling of post-consumer polyurethane foams, signaling intent to close the material loop and differentiate its product slate. Successful adoption could shift raw-material sourcing away from virgin propylene oxide, insulating margins from petrochemical volatility over the long term.

Rapid Cold-Chain Build-Out in Emerging Economies

Stricter food-safety and pharmaceutical-distribution standards are accelerating investments in temperature-controlled logistics across India, Southeast Asia, and the Gulf Cooperation Council. Cold-store builders specify rigid PU panels that require polyether polyols with tight molecular-weight distribution to achieve dimensional stability under extreme thermal cycling. Suppliers that can validate superior k-factor retention and compliance with global pharma guidelines capture premium prices, especially where local production shortens lead times and mitigates customs delays. Mexico’s emergence as a top-four polyurethane consumer illustrates how nearshoring and e-commerce are stimulating demand for high-performance insulation solutions.

Lightweighting Imperatives in E-Mobility Interiors

Battery-electric vehicle OEMs seek every kilogram of weight savings to extend driving range, thrusting high-performance flexible polyether polyols into seat cushioning, NVH dampening, and headliner foams. Formulators have achieved 15-20% density reductions compared with legacy automotive grades while preserving crash-test safety. This performance uplift supports the automotive segment’s projected 6.27% CAGR, with premium e-mobility platforms willing to pay higher polyol premiums in exchange for range gains that directly influence purchase decisions. Huntsman’s 2024-2025 segment earnings show resilience amid vehicle-production variability, underscoring durable demand for weight-optimized chemistry.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Propylene-oxide price volatility | −1.2% | Global, highest exposure in APAC | Short term (≤ 2 years) |

| Strict HAP caps under U.S. NESHAP 2026 | −0.4% | North America with global spillover | Medium term (2-4 years) |

| Emerging micro-plastics legislation | −0.3% | EU and Korea, expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Propylene-Oxide Feedstock Pricing

Quarterly propylene-oxide swings of 15-20% have become routine as energy prices fluctuate and unplanned shutdowns ripple through integrated production chains. Since this monomer represents nearly half of polyether polyol cash costs, margin compression forces producers to announce surcharges or idle high-cost assets. Dow’s decision to close its Argentina polyols unit in October 2024 illustrates how margin pressure accelerates footprint consolidation. Upstream methane-emission rules in the EU further inflate production costs, sharpening competitive gaps between regions with disparate environmental policies.

Strict HAP Emission Caps Under U.S. NESHAP Review 2026

The U.S. EPA is finalizing tighter hazardous-air-pollutant limits that could require multimillion-dollar upgrades to scrubbers, thermal oxidizers, and leak-detection systems at polyurethane facilities. Smaller independent producers face disproportionate compliance costs, nudging the polyether polyol industry toward further consolidation. Capital uncertainty is delaying expansions in the U.S. Gulf Coast while management teams await final rule language, pushing incremental volumes to jurisdictions with lighter regulatory frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Dominance Drives Infrastructure Growth

Rigid grades captured a 51.92% polyether polyol market share in 2025 and remain the backbone of building-envelope insulation, particularly in cold-chain warehouses and zero-energy commercial structures. This leadership is grounded in low thermal-conductivity values and compressive strength that meet evolving energy codes. The segment benefits from policy incentives such as U.S. tax credits for high-efficiency roofs and EU directives calling for deep-renovation targets, safeguarding demand through construction cycles. State-of-the-art rigid formulations integrate halogen-free flame retardants and DMC-initiated polyols to reduce VOCs, broadening their appeal in health-conscious architectural projects. With governments tightening carbon-emission caps, building owners increasingly quantify embodied carbon, which positions CO₂-based rigid polyols as attractive alternatives that embed captured carbon within insulation panels.

Flexible polyether grades, while holding a smaller revenue base, are on track for a 5.74% CAGR fueled by premium furniture, mattress-in-a-box e-commerce, and lightweight vehicle interiors. Advances in catalyst efficiency have lowered viscosity for easier processing without elevating aldehyde emissions, a key factor for bedding brands marketing low-odor products. Automotive tier suppliers are shifting to MDI-based flexible foams formulated with reactive polyether polyols, achieving density cuts that directly translate to range improvement in EVs.

By Application: Construction Insulation Leads Market Evolution

Rigid PU foam held 45.62% of 2025 demand and anchors steady volume for polyether polyol market size calculations. Building energy-codes mandating higher R-values and the ongoing push for net-zero carbon buildings guarantee a baseline of rigid-foam usage in roof and wall assemblies. Cold-chain facilities often specify higher-density rigid foams to ensure dimensional stability under thermal shock, raising per-square-meter polyol loading relative to residential insulation. Suppliers with on-site pentane pre-blends enjoy a revenue edge because they minimize flammable-liquid handling at customer sites, a logistics convenience prized by panel manufacturers in emerging markets.

The CASE segment (coatings, adhesives, sealants, elastomers) is growing fastest at 5.98% CAGR on the back of infrastructure-maintenance budgets, fleet-vehicle repainting, and bridge-deck joint-seal replacements. Polyether polyols formulated into high-solid polyurethane coatings offer rapid cure, high abrasion resistance, and low VOC profiles, aligning with stricter solvent-reduction mandates. Bridge-deck sealants blending hydrophobic polyether backbones resist freeze-thaw cycling in temperate climates, ensuring long-term adhesion even on weathered concrete.

By End-User Industry: Construction Sector Anchors Demand Stability

Construction held 38.21% of 2025 revenues, offering the polyether polyol market a dependable pillar that transcends economic cycles. Governments worldwide deploy green-stimulus packages targeting energy-efficient retrofits, which channel grant funding directly into spray-foam roofs and cavity-wall insulation. Rigid polyether systems with integrated fire retardants and low-VOC signatures remain the default solution for meeting new thermal-performance benchmarks. Over the next decade, skyscraper curtain-wall retrofits and district-cooling network upgrades in the Middle East are expected to secure sustained rigid-foam consumption.

Automotive accounts for a smaller volume base but leads growth at 6.08% CAGR, driven by battery-electric launches that integrate lightweight seat cushions, headliners, and acoustic foams. Polyether polyols optimized for thin-wall molding enable OEMs to shrink part thickness without compromising crash-worthiness, yielding both weight and cost savings. Furniture and bedding continue to source flexible grades focused on comfort and durability, while electrical and electronics demand flame-classified encapsulants and potting compounds.

Geography Analysis

Asia-Pacific dominated with 44.05% of 2025 revenue, buoyed by China’s massive construction pipeline and India’s aggressive cold-chain expansion under its National Logistics Policy. Regional producers benefit from scale economies, integrated propylene-oxide assets, and localized supply chains that shorten lead times for downstream foamers.

The Middle East and Africa is the fastest-growing bloc at 5.69% CAGR, reflecting petrochemical integration strategies and government-backed giga-projects such as Saudi Arabia’s NEOM and the UAE’s Masdar City. Abundant LPG feedstock and fiscal incentives attracting foreign direct investment underpin regional polyether capacity additions.

North America maintains steady volumes from residential reroofing, commercial retrofits, and joint-seal replacements on aging highways. U.S. Inflation Reduction Act tax credits for efficient building envelopes incentivize spray-foam adoption, while Canada’s climate-resilient building codes prioritize higher R-value assemblies. Europe’s market is defined by renovation needs across its aging building stock and strict VOC regulations that favor low-emission polyether grades.

South America presents a mixed outlook: Brazil’s automotive sector demands flexible polyols, yet construction volumes fluctuate with macroeconomic sentiment and fiscal policy shifts; nonetheless, regional capacity rationalization by multinationals is expected to tighten supply and lift utilization rates through 2028.

Competitive Landscape

The polyether polyol market exhibits moderate fragmentation: global leaders BASF, Covestro, and Dow leverage integrated propylene-oxide capacity and expansive distribution networks to hold a combined share well above midsized rivals. Sustainability-driven innovation is a focal point: Covestro’s EUR 100 million circular-chemistry program targets commercial CO₂-based polyols and solvent-free recycling routes. Chinese producers, historically positioned on cost, are venturing upstream to secure propylene-oxide via HPPO (hydrogen peroxide to propylene oxide) units, improving environmental footprints and lowering chlorinated coproduct formation.

Polyether Polyol Industry Leaders

Covestro AG

Dow

BASF

Huntsman International LLC

Wanhua

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Dow disclosed plans to close its 94 ktpa polyether polyols facility in Tertre, Belgium, by March 2026, citing sustained high European energy costs.

- October 2024: Dow permanently shut its Argentina polyols plant amid global oversupply, signaling ongoing capacity rationalization in South America.

Global Polyether Polyol Market Report Scope

Polyether polyol is a chemical structural component used in the production of polyurethanes. These are made by reacting organic oxides and glycols. This can be divided into rigid foam polyether, soft foam polyether, and elastomer with polyether according to the performance of polyether products. The polyether polyol market is segmented by type, end-user industry, and geography. By type, the market is segmented into flexible, rigid, and other types. By end-user industry, the market is segmented into furniture and bedding, construction, automotive, electrical and electronics, and other end-user industries. The report also covers the market size and forecasts for the polyether polyol market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (kilo tons).

| Flexible Polyether Polyols |

| Rigid Polyether Polyols |

| Other Types |

| Flexible PU Foam |

| Rigid PU Foam |

| CASE (Coatings, Adhesives, Sealants, Elastomers) |

| Thermoplastic Polyurethanes (TPU) |

| Others |

| Furniture and Bedding |

| Construction |

| Automotive |

| Electrical and Electronics |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Flexible Polyether Polyols | |

| Rigid Polyether Polyols | ||

| Other Types | ||

| By Application | Flexible PU Foam | |

| Rigid PU Foam | ||

| CASE (Coatings, Adhesives, Sealants, Elastomers) | ||

| Thermoplastic Polyurethanes (TPU) | ||

| Others | ||

| By End-user Industry | Furniture and Bedding | |

| Construction | ||

| Automotive | ||

| Electrical and Electronics | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the global polyether polyol sector today and how fast is it growing?

Global demand was valued at USD 17.67 billion in 2026 and is projected to reach USD 22.89 billion by 2031, reflecting a 5.32% CAGR during 2026-2031.

Which application currently uses the most polyether polyol volumes?

Rigid polyurethane foam for building-insulation applications accounts for 45.62% of 2025 global demand, ahead of flexible foams and CASE uses.

What end-user area is expanding the quickest?

Automotive applications are expected to rise at 6.08% CAGR to 2031 as electric-vehicle makers adopt lightweight flexible foams for seating, headliners, and acoustic parts.

Why are CO2-based polyether polyols gaining attention?

They embed captured carbon into the polymer backbone, cut dependence on virgin propylene oxide, and improve hydrolytic resistancedelivering measurable Scope-3 emission savings for converters.

Which region is forecast to see the fastest consumption growth?

The Middle East and Africa is on track for a 5.69% CAGR through 2031, driven by mega-construction projects and new integrated petrochemical capacity.

How are producers addressing propylene-oxide price volatility?

Leading suppliers are passing through surcharges, shutting high-cost assets, and investing in alternative feedstocks such as CO?-based synthesis to stabilize margins.

Page last updated on: