APAC Savoury Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

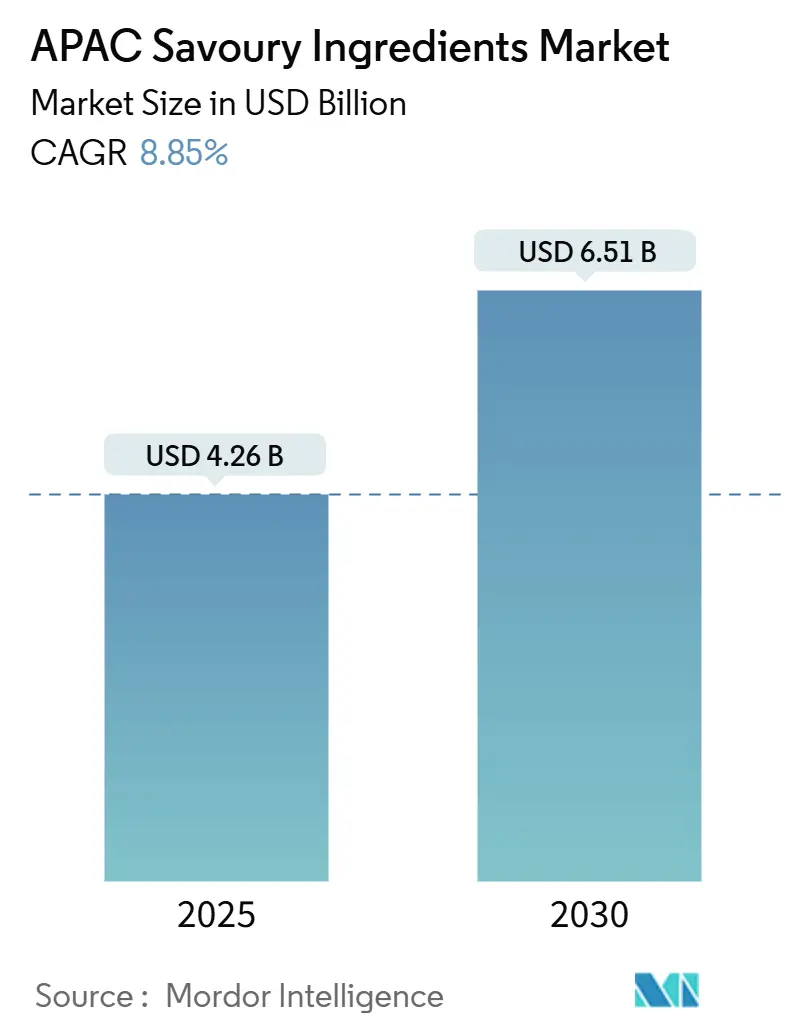

| Market Size (2025) | USD 4.26 Billion |

| Market Size (2030) | USD 6.51 Billion |

| Growth Rate (2025 - 2030) | 8.85% CAGR |

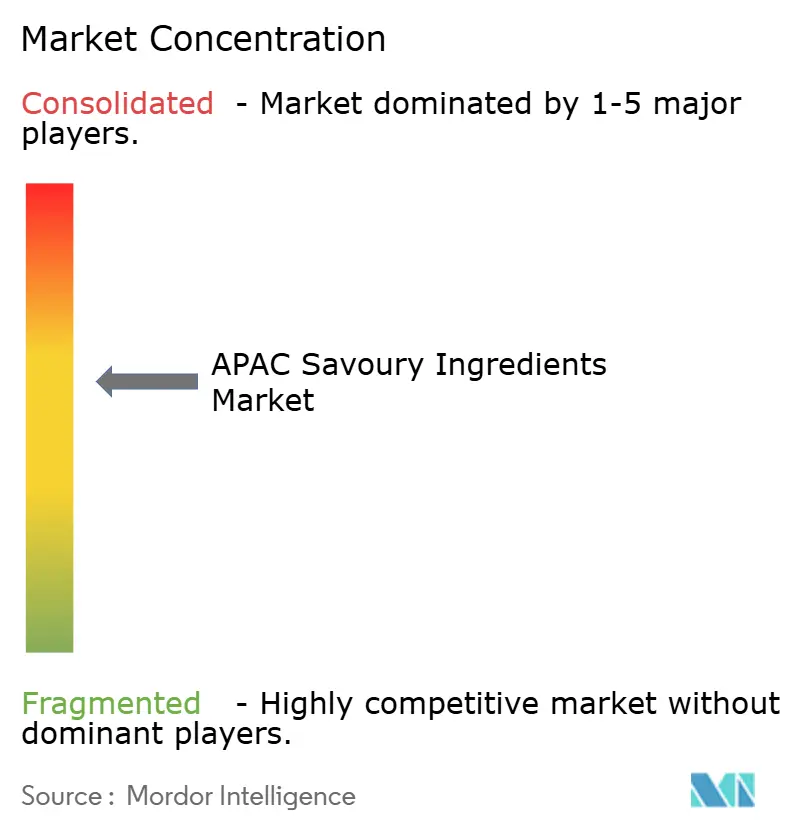

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

APAC Savoury Ingredients Market Analysis by Mordor Intelligence

The Asia-Pacific savory ingredients market size reached USD 4.26 billion in 2025 and is expected to grow to USD 6.51 billion by 2030, at a CAGR of 8.85%. Urbanization, rising disposable incomes, and diversification of processed food products are driving increased ingredient consumption across manufacturing facilities. Instant noodle manufacturers in China, Indonesia, and Thailand are incorporating fermented flavor enhancers to achieve product differentiation in the competitive market, while premium snack manufacturers in Japan and Australia are adopting clean-label ingredients to meet consumer demands. While ASEAN regulatory alignment reduces international compliance expenses across the region, stricter sodium reduction requirements in developed markets are increasing product reformulation costs significantly. The market demonstrates moderate competition as emerging biotechnology companies challenge traditional monosodium glutamate (MSG) manufacturers with innovative fermentation-based umami ingredients.

Key Report Takeaways

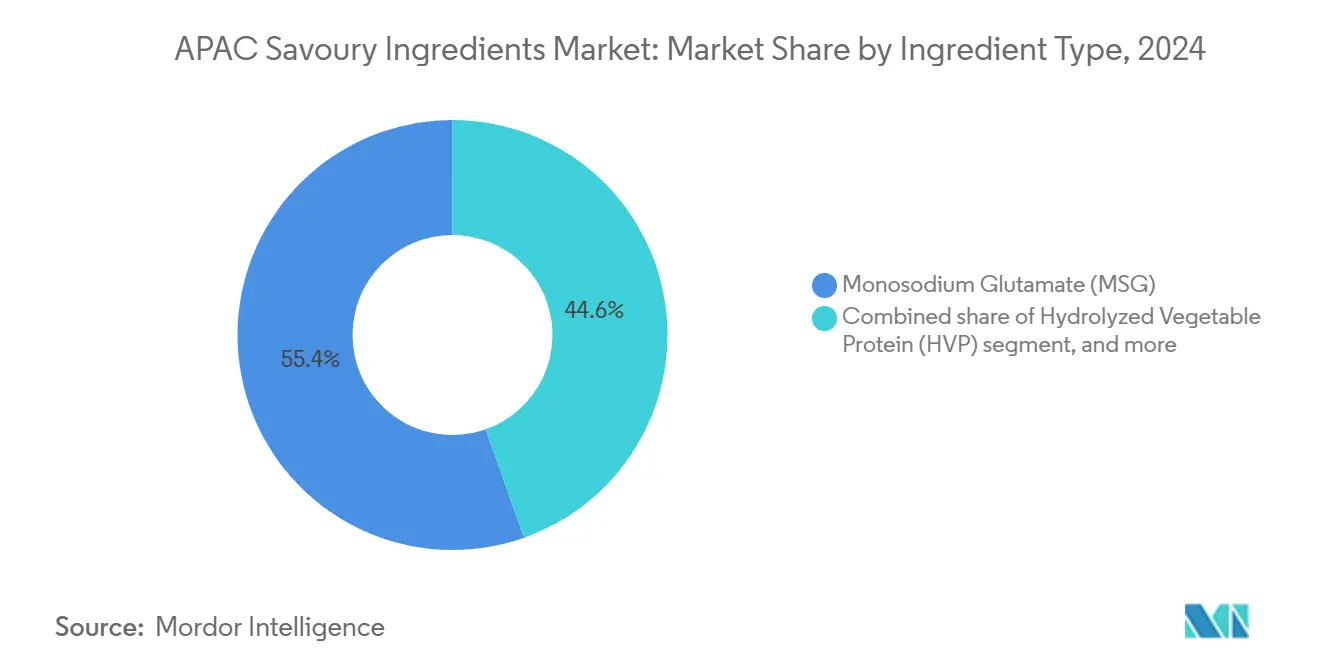

- By ingredient type, monosodium glutamate (MSG) commanded 55.41% of Asia-Pacific savoury ingredients market share in 2024, whereas hydrolyzed vegetable protein (HVP) is forecast to post the fastest 10.28% CAGR through 2030.

- By origin, natural ingredients held 63.25% share in 2024; synthetic counterparts are projected to expand at a 9.32% CAGR over 2025-2030.

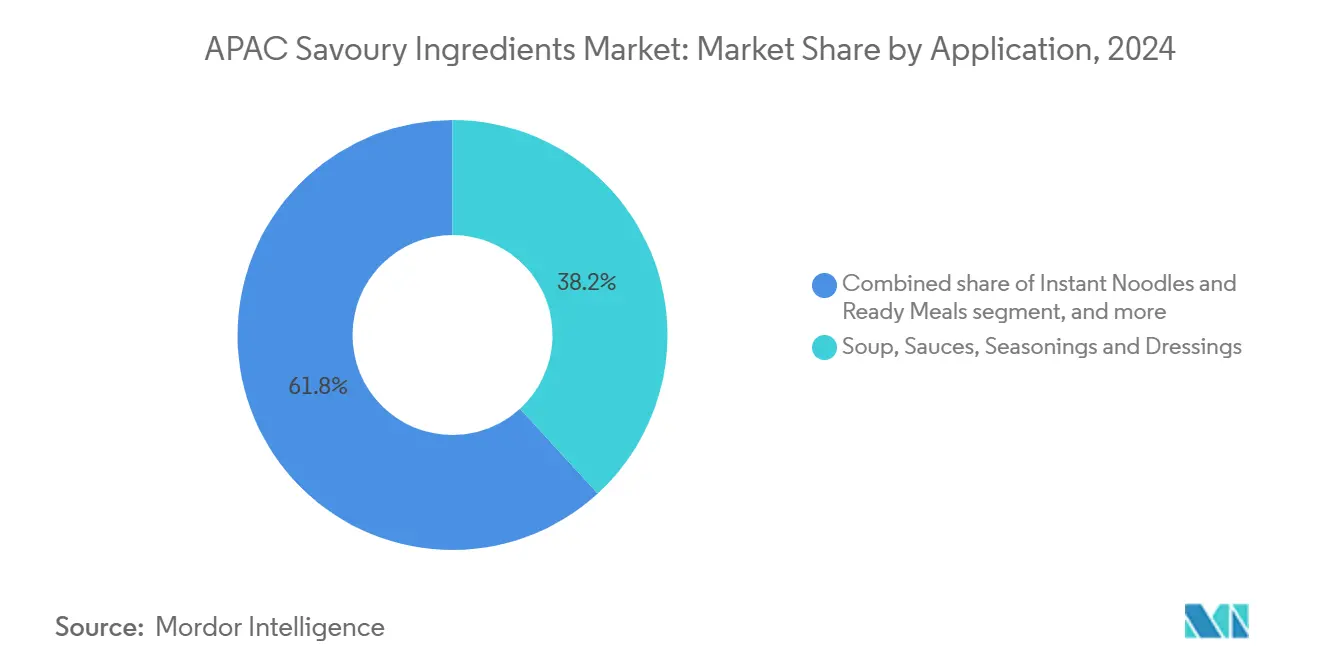

- By application, soup, sauces, seasonings and dressings accounted for 38.20% of the Asia-Pacific savoury ingredients market size in 2024, while instant noodles and ready meals are poised for the highest 11.23% CAGR.

- By geography, China led with a 35.18% share in 2024; India is set to grow at 9.98% CAGR between 2025-2030.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on savory ingredients market by Mordor Intelligence reflects how these regional layers combine into a single system.

APAC Savoury Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for processed food | +1.8% | China, India, Indonesia, Thailand | Medium term (2-4 years) |

| Growing shift toward clean-label and natural ingredients | +1.5% | Japan, Australia, South Korea, Singapore | Long term (≥ 4 years) |

| Expansion of instant noodles and ready-meal manufacturing hubs | +1.2% | China, Indonesia, Thailand, India | Short term (≤ 2 years) |

| Increased role of fermentation-based savoury enhancers | +0.9% | Global Asia-Pacific, with concentration in Japan, China | Medium term (2-4 years) |

| Technological advancements in precision fermentation and digital flavor design | +0.7% | Singapore, Japan, Australia, South Korea | Long term (≥ 4 years) |

| Industrial expansion of hydrolyzed vegetable protein (HVP) applications | +0.5% | China, India, Thailand, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Processed Food

Urbanization in Asia-Pacific is transforming food consumption patterns, with processed food demand growing faster than demographic trends suggest. The demand for convenience foods is increasing significantly in tier-2 and tier-3 cities, where working populations depend on packaged foods that need complex flavor profiles to match traditional cooking tastes. The rise in dual-income households and longer working hours has accelerated this shift, particularly among young urban professionals. Indonesia consumed 12-13 billion servings of instant noodles annually as of 2024, making it the second-largest market globally and increasing the demand for MSG, yeast extracts, and spice oleoresins in manufacturing[1]Source: AEGIC Organization, "The Indonesian noodle market," aegic.org. This demographic transition creates consistent volume growth for savory ingredient suppliers, especially those providing cost-effective solutions that preserve authentic tastes across different regional preferences. The market's evolution is further driven by consumers seeking familiar flavors in convenient formats, prompting manufacturers to develop innovative ingredient combinations that capture local taste preferences.

Growing Shift Toward Clean-Label and Natural Ingredients

Consumer preferences in premium markets are driving complex formulations as manufacturers balance clean-label requirements with functional performance. Australia's Therapeutic Goods Administration standards influence clean-label expectations across Southeast Asian markets, where export-focused manufacturers adopt similar formulation practices. This trend is expanding beyond premium segments, with mass-market brands using natural yeast extracts and fermented dairy concentrates instead of synthetic flavor enhancers. Singapore's regulatory approval of fermentation-derived proteins, such as Solein in Ajinomoto's protein ice cream products, shows how regulations can advance clean-label innovation in savory applications. This market evolution has prompted ingredient suppliers to invest in fermentation capabilities and natural extraction technologies, shifting competitive advantage toward companies with biotechnology expertise.

Expansion of Instant Noodles and Ready-Meal Manufacturing Hubs

The consolidation of instant noodle and ready meal manufacturing has created concentrated demand centers that influence ingredient procurement strategies and supply chain operations. Thailand has strengthened its position as a regional export hub for instant noodles, with manufacturers increasing production capacity to meet growing demand in ASEAN markets and other regions. Nissin Foods has expanded through joint ventures in Australia and New Zealand, establishing new demand centers for savory ingredients beyond traditional Asian markets. Korean manufacturers, including Nongshim and Samyang, have expanded into Latin American markets, showcasing the globalization of Asian instant noodle production and creating export opportunities for regional ingredient suppliers. The manufacturing hub model allows for economies of scale in ingredient procurement while requiring consistent quality and reliable supply across multiple production facilities. This concentration benefits large-scale ingredient producers but creates entry barriers for smaller suppliers who lack the capacity to serve industrial-scale customers with strict quality requirements.

Increased Role of Fermentation-Based Savoury Enhancers

Fermentation technology is advancing beyond traditional applications to provide precision-engineered solutions that address sensory and nutritional challenges in modern food formulations. Research from the University of Queensland on precision fermentation applications in Australia demonstrates the technology's ability to produce complex flavor compounds more sustainably than traditional extraction methods[2]Source: Tate & Lyle,"tate-lyle-launches-automated-lab-singapore-mouthfeel-solutions," tate-lyle.com. Fermented ingredients provide functional benefits beyond flavor enhancement, including improved shelf stability, lower sodium content, and enhanced nutrition through bioactive compounds. The technology enables local production of ingredients that typically rely on agricultural supply chains, reducing vulnerability to climate-related disruptions and price fluctuations. Companies that invest in fermentation capabilities gain advantages through ingredient customization and decreased reliance on commodity markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny on MSG and sodium content | -1.1% | Global Asia-Pacific, particularly Australia, Japan, South Korea | Short term (≤ 2 years) |

| Competition from traditional condiments and seasoning | -0.8% | China, India, Thailand, Indonesia | Medium term (2-4 years) |

| Supply volatility for oleoresins and spice extracts | -0.6% | India, China, Indonesia, Thailand | Short term (≤ 2 years) |

| Cost pressure of natural savoury systems | -0.4% | Japan, Australia, South Korea, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny on MSG and Sodium Content

Regulatory changes across developed Asia-Pacific markets are creating formulation challenges that require comprehensive product redesign rather than simple ingredient substitution. The U.S. Department of Commerce's preliminary determination on MSG circumvention from Malaysia in February 2025 has disrupted established supply chains, requiring manufacturers to diversify their sourcing[3]Source: Federal Register, "Monosodium Glutamate From the People's Republic of China: Preliminary Affirmative Determination of Circumvention," federalregister.gov. While Food Standards Australia New Zealand (FSANZ) confirms MSG's safety for general populations, negative consumer perceptions continue to drive manufacturers toward alternative umami solutions, often at higher costs. The World Health Organization's target of 30% global sodium reduction by 2025 adds pressure on savory ingredient formulations, particularly in processed foods where sodium-based enhancers serve essential functional purposes beyond flavor. This regulatory environment benefits ingredient suppliers with fermentation capabilities and natural umami enhancement technologies, while impacting companies relying on traditional MSG-based solutions.

Supply Volatility for Oleoresins and Spice Extracts

Supply chain disruptions caused by climate events are increasing volatility in spice and oleoresin markets, compelling companies to modify their sourcing and inventory strategies. The antidumping investigation by the U.S. Trade Representative regarding oleoresin paprika imports from India highlights how regulatory actions intensify existing supply chain difficulties and increase costs for manufacturers reliant on specific regions. Climate impacts are evident across multiple ingredients, as seen in Madagascar's vanilla production disruptions from cyclones and the 14% decline in West African cocoa production during 2023-2024. These supply constraints benefit ingredient suppliers with diverse sourcing networks and vertical integration while creating market opportunities for synthetic and fermentation-derived alternatives that provide supply stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: MSG Dominance Faces Clean-Label Disruption

Fermentation-derived alternatives are transforming the ingredient market dynamics, with hydrolyzed vegetable protein (HVP) projected to grow at 10.28% CAGR during 2025-2030, while MSG maintains a substantial 55.41% market share in 2024. Ajinomoto's introduction of Palate Perfect FL-TM fermented tomato flavor in July 2025 illustrates how traditional MSG manufacturers are expanding into clean-label alternatives to address supply chain risks while delivering comparable functional benefits. Yeast extracts continue to experience consistent demand in industrial applications, specifically in soup bases and seasoning blends, where their natural composition supports clean-label requirements without reducing umami intensity.

Nucleotides remain a niche segment primarily used in premium instant noodle formulations and restaurant-quality seasoning systems, where they work synergistically with MSG to enhance flavor profiles at reduced usage levels. The "Others" segment, including fermented dairy concentrates, mushroom concentrates, and kokumi extracts, demonstrates innovation in specialized applications where conventional ingredients fall short of functional requirements. Ingredient selection is increasingly influenced by regulatory requirements under FSANZ guidelines and emerging ASEAN harmonization initiatives, particularly for manufacturers operating across multiple regions with diverse approval standards.

By Origin: Natural Premiumization Drives Synthetic Innovation

Natural ingredients hold a 63.25% market share in 2024, as consumers demonstrate willingness to pay premium prices for products they perceive as authentic. Meanwhile, synthetic alternatives achieve a 9.32% CAGR through improved technology and optimized production costs. The natural segment leverages fermentation-based production methods, which integrate elements of both natural and synthetic processes. This enables ingredients such as yeast extracts and fermented proteins to maintain natural positioning while achieving industrial-scale efficiency.

Synthetic ingredients maintain their position in applications that require consistent performance and extended shelf stability, particularly in export products exposed to varying temperatures during distribution. Supply chain disruptions and climate-related challenges in natural ingredient sourcing create opportunities for synthetic alternatives that provide stable pricing and reliable supply. The increasing adoption of precision fermentation technologies indicates a potential shift from origin-based categorization toward functionality-based differentiation as consumers develop a better understanding of biotechnology applications.

By Application: Instant Noodles Drive Innovation Beyond Traditional Segments

Instant noodles and ready meals segment is projected to grow at a CAGR of 11.23% during 2025-2030. The Soup, sauces, seasonings, and dressings segment maintains market leadership with a 38.20% share in 2024. This growth pattern reflects increased urbanization impacts on consumption habits and expanded manufacturing capabilities across Southeast Asian markets. The savory snacks segment demonstrates strong performance through premium positioning, enabling manufacturers to manage ingredient costs effectively. This creates opportunities for specialized ingredients, including kokumi extracts and fermented dairy concentrates, which enhance product texture and flavor profiles.

Meat and poultry applications show increasing incorporation of plant-based protein extenders and hybrid formulations. This trend generates demand for ingredients that effectively combine traditional and alternative protein sensory characteristics. Additional applications include functional foods, sports nutrition, and pet food segments, where savory ingredients enhance palatability and provide nutritional benefits. Manufacturers are adopting multi-application ingredient platforms to optimize costs and simplify supply chains through cross-category ingredient utilization.

Geography Analysis

China holds a 35.18% market share in 2024, supported by its integrated production capabilities in MSG fermentation, HVP processing, and spice oleoresin extraction. These capabilities provide cost advantages in domestic and Southeast Asian export markets. The implementation of China's food security law in June 2024 strengthens domestic grain processing capacity and reduces food waste while enforcing stricter quality standards across the supply chain.

India's market demonstrates the fastest growth rate at 9.98% CAGR during 2025-2030. This growth results from FSSAI's regulatory modernization and expanded food processing infrastructure. The FSSAI's 2025 packaging and labeling requirement amendments benefit established ingredient suppliers with regulatory expertise but create entry barriers for smaller regional companies. The market faces challenges from FDA import refusals affecting food quality, creating opportunities for domestic suppliers and quality-focused importers. The 50% U.S. tariffs on Indian botanical exports, implemented in September 2025, affect traditional spice and extract supply chains while promoting domestic value-addition. The diverse consumer preferences across North, South, and Western India create opportunities for suppliers offering region-specific flavor profiles.

Other Asia-Pacific markets, including Japan, Australia, South Korea, Indonesia, Thailand, and Singapore, present varying market characteristics. Japan's MHLW maintains strict additive approval processes, which protect approved suppliers' market positions while restricting new ingredient entries. The FSANZ framework between Australia and New Zealand provides regulatory benefits for suppliers operating in both markets. Thailand's position as an instant noodle export center drives substantial industrial ingredient demand.

Competitive Landscape

The market demonstrates moderate consolidation levels, with multinational companies maintaining advantages through technology and scale, while regional players leverage local market knowledge and supply chain proximity. The competitive landscape shows a 6 out of 10 concentration score, indicating balanced competition between global ingredient suppliers and regional specialists.

Fermentation technology capabilities are becoming a key differentiator, as companies invest in biotechnology platforms for ingredient customization and supply chain stability. Companies are adopting vertical integration strategies to control key supply chain components and increase processing margins. The acquisition of DSM-Firmenich's yeast extract business by Lesaffre in October 2024 strengthens fermentation-based ingredient capabilities and expands presence in Asia-Pacific markets.

Partnerships between ingredient suppliers and biotechnology companies drive innovation in precision fermentation and digital flavor development, benefiting organizations that successfully combine traditional and modern production methods. Market opportunities exist in specialized segments such as plant-based protein enhancement, sodium reduction solutions, and clean-label alternatives to synthetic additives, where regulatory requirements and consumer acceptance create entry barriers that help maintain market positions.

APAC Savoury Ingredients Industry Leaders

-

Associated British Foods plc

-

Ajinomoto Co., Inc.

-

Angel Yeast Co., Ltd.

-

Lesaffre et Compagnie

-

Meihua Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lesaffre introduced a yeast extract product line in the Asia-Pacific region in July 2025. The product range focuses on enhancing flavor and nutritional content in savory foods, targeting food manufacturers and culinary applications, with an emphasis on natural ingredients and clean-label solutions.

- January 2025: Angel Yeast established a new production facility in January 2025 with an annual capacity of 11,000 metric tons of yeast proteins. The facility, designed for resource efficiency and reduced environmental impact, strengthens the company's position in alternative protein sources and fermentation-based food ingredients. The facility's products are suitable for protein bars, high-protein cereals, chips, cookies, and meat alternatives.

- October 2024: DSM-Firmenich completed the sale of its yeast extract business to Lesaffre, a global fermentation and microorganism specialist, in October 2024. While financial terms remained undisclosed, the divestment enabled DSM-Firmenich to focus on its core strategy while expanding Lesaffre's capabilities in yeast extract production and natural fermentation-based solutions.

APAC Savoury Ingredients Market Report Scope

| Monosodium Glutamate (MSG) |

| Yeast Extract |

| Hydrolyzed Vegetable Protein (HVP) |

| Nucleotides |

| Spice and Herb Oleoresins |

| Others (fermented dairy concentrates, mushroom concentrates, Kokumi extracts) |

| Natural |

| Synthetic |

| Savory Snacks |

| Soup, Sauces, Seasonings and Dressings |

| Meat and Poultry |

| Dairy and Cheese Analogues |

| Instant Noodles and Ready Meals |

| Other Applications |

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Indonesia |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| Ingredient Type | Monosodium Glutamate (MSG) |

| Yeast Extract | |

| Hydrolyzed Vegetable Protein (HVP) | |

| Nucleotides | |

| Spice and Herb Oleoresins | |

| Others (fermented dairy concentrates, mushroom concentrates, Kokumi extracts) | |

| By Origin | Natural |

| Synthetic | |

| Application | Savory Snacks |

| Soup, Sauces, Seasonings and Dressings | |

| Meat and Poultry | |

| Dairy and Cheese Analogues | |

| Instant Noodles and Ready Meals | |

| Other Applications | |

| Geography | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific savoury ingredients market in 2025?

The Asia Pacific savoury ingredients market size stands at USD 4.26 billion in 2025 with an 8.85% CAGR forecast to 2030.

Which ingredient type holds the biggest share?

MSG retains the largest 55.41% share in 2024 due to entrenched manufacturing scale in China.

What is the fastest-growing ingredient category?

Hydrolyzed Vegetable Protein is projected to record a 10.28% CAGR from 2025-2030, driven by clean-label demand.

Which application will expand most rapidly?

Instant Noodles and Ready Meals expect the highest 11.23% CAGR as urban consumers seek convenient meal formats.

Page last updated on: