Africa Fungicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 440 Billion |

| Market Size (2026) | USD 452.72 Billion |

| Market Size (2031) | USD 521.99 Billion |

| Growth Rate (2026 - 2031) | 2.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Fungicide Market Analysis by Mordor Intelligence

The Africa fungicide market size is expected to grow from USD 440 million in 2025 to USD 452.72 million in 2026 and is forecast to reach USD 521.99 million by 2031 at 2.89% CAGR over 2026-2031. Disease pressure driven by rising temperatures, expanding government food-security programs, and rapid growth in precision-spray technologies are the primary forces behind this steady advance. Climate variability is raising the incidence of foliar diseases across staple and high-value crops, prompting growers to increase both application frequency and spend. Governments in West and East Africa are bundling fungicides with input credits and grain-reserve schemes, which sustain demand even in smallholder systems. Export-oriented horticulture clusters in North and Southern Africa favor newer chemistries that comply with European residue limits, nudging overall product mix toward premium formulations. Meanwhile, drone-based and sensor-guided spraying services are emerging in Kenya, Nigeria, and South Africa, improving timing accuracy and reducing wastage, which reinforces grower confidence in formal crop-protection channels.

Key Report Takeaways

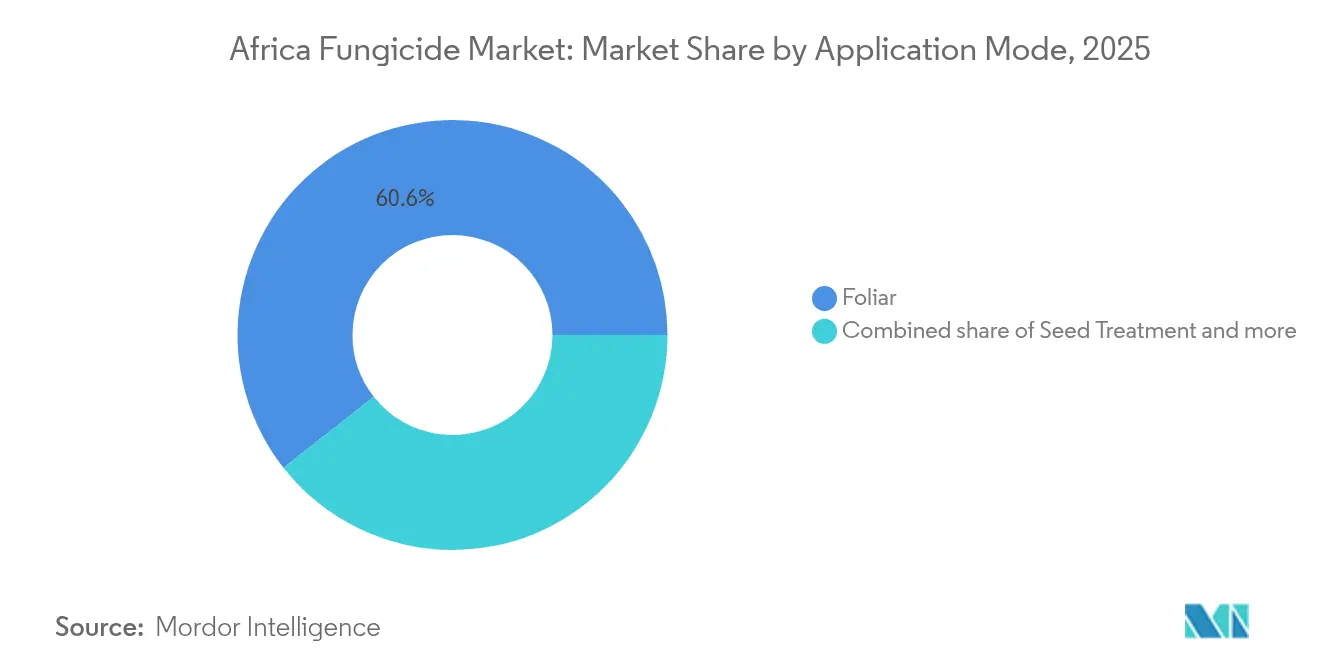

- By application mode, foliar led with 60.60% of the Africa fungicide market share in 2025, while foliar is rising at a 2.95% CAGR through 2031.

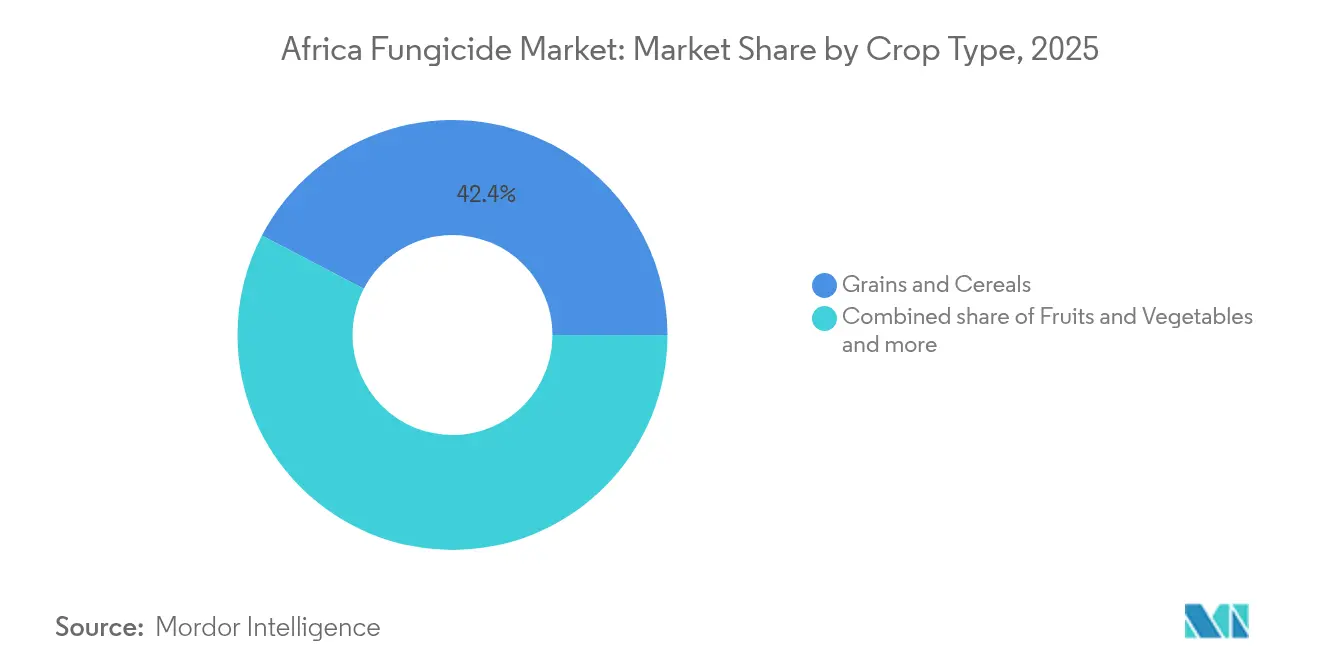

- By crop type, grains and cereals accounted for 42.35% of the Africa fungicide market size in 2025, while fruits and vegetables are rising at a 3.05% CAGR through 2031.

- By Geography, South Africa led with 11.75% of the Africa fungicide market size in 2025, while South Africa is rising at a 2.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Fungicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-change-driven surge in foliar diseases | +0.8% | West and Central Africa highest | Medium term (2-4 years) |

| Government food-security programs accelerating fungicide adoption | +0.6% | Sub-Saharan Africa | Short term (≤ 2 years) |

| Rapid shift toward high-value horticulture crops | +0.5% | North and Southern Africa | Medium term (2-4 years) |

| Expansion of controlled-environment farming across East Africa | +0.4% | East Africa core | Long term (≥ 4 years) |

| European residue-compliance pressure on export supply chains | +0.3% | Export corridors | Short term (≤ 2 years) |

| Rise of drone-based precision-spray service providers | +0.2% | South Africa, Kenya, Nigeria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Change-Driven Surge in Foliar Diseases

Rising temperatures and shifting precipitation patterns across Africa intensify fungal pathogen loads, creating sustained demand for foliar fungicides beyond traditional seasonal applications. Research indicates that temperature increases of 1-2°C expand the geographic range of major plant pathogens, with leaf rust, powdery mildew, and late blight showing enhanced virulence under elevated humidity conditions. West African cocoa regions experience particular pressure from black pod disease, while East African coffee zones face increased coffee leaf rust incidence, driving specialized fungicide demand in high-value export crops. The African Union's climate adaptation framework recognizes crop protection as essential infrastructure, supporting regulatory harmonization efforts that facilitate fungicide access across member states.

Government Food-Security Programs Accelerating Fungicide Adoption

Strategic grain reserve policies and input subsidy programs across sub-Saharan Africa directly stimulate fungicide uptake through reduced farmer costs and technical extension support. Nigeria's Anchor Borrowers Program and Kenya's National Cereals and Produce Board initiatives integrate crop protection into comprehensive agricultural financing packages, ensuring fungicide availability during critical application windows. Ethiopia's Agricultural Growth Program Phase II allocates substantial resources to wheat rust management, while Rwanda's Crop Intensification Program mandates integrated pest management practices that include prophylactic fungicide applications. These interventions prove particularly effective in smallholder systems where individual farmers lack resources for timely disease management, creating sustained demand that transcends market-driven adoption patterns.

Rapid Shift Toward High-Value Horticulture Crops

Export-oriented fruit and vegetable production expansion in North and Southern Africa generates premium fungicide demand characterized by strict residue tolerances and application timing requirements. Morocco's citrus export sector, valued at over USD 1.2 billion annually, drives adoption of pre-harvest interval-compliant fungicides that maintain Europe market access [1]Source: National Food Safety Office of Morocco, “Phytopharmacovigilance Actions,” onssa.gov.ma . South African table grape and stone fruit industries implement comprehensive spray programs using multiple modes of action to prevent resistance development, while Egyptian potato exports require specialized late blight management protocols. The shift toward protected cultivation in these regions further intensifies fungicide use, as greenhouse and tunnel systems concentrate disease pressure while enabling precise application timing that maximizes efficacy and minimizes residue risk.

Expansion of Controlled-Environment Farming Across East Africa

The adoption of greenhouses and shade nets in Kenya, Ethiopia, and Tanzania creates concentrated disease pressure environments that require specialized fungicide programs distinct from those used in open-field applications. Kenya's floriculture sector, generating export revenue, demonstrates the economic viability of intensive crop protection in controlled environments. Ethiopian greenhouse vegetable production for domestic and regional markets expands rapidly, supported by development finance institutions that recognize controlled-environment agriculture as climate adaptation infrastructure. These systems enable precise fungicide application timing and dosage control, often requiring higher-value active ingredients with specific modes of action that prevent the development of resistance in enclosed spaces where pathogen populations cycle rapidly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening regulatory phase-outs of legacy active ingredients | −0.4% | Export-oriented regions | Medium term (2-4 years) |

| Volatile China-origin technical prices and shipping costs | −0.3% | Import-dependent markets | Short term (≤ 2 years) |

| Proliferation of counterfeit / sub-standard products | −0.2% | West and Central Africa | Medium term (2-4 years) |

| Growing substitution by on-farm biological fungicides | −0.1% | East and Southern Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Regulatory Phase-Outs of Legacy Active Ingredients

Continental harmonization of pesticide regulations increasingly restricts access to established fungicide chemistries, forcing costly transitions to newer active ingredients with limited local efficacy data. The African Union's SPS Policy Framework mandates member state alignment with international standards, resulting in coordinated phase-outs of substances like chlorothalonil and mancozeb that historically anchored African crop protection programs[2]Source: African Union Commission, “SPS Policy Framework,” au.int . Morocco's ONSSA withdrew 15 active substances between 2018-2020, while Kenya's Pest Control Products Board implements increasingly stringent registration requirements that favor multinational companies over regional formulators. These regulatory shifts create supply disruptions and price volatility as farmers adapt to replacement chemistries, while smaller agricultural input dealers struggle with inventory obsolescence and reduced product availability.

Volatile China-Origin Technical Prices and Shipping Costs

Supply chain disruptions and raw material cost fluctuations in China, which supplies approximately 60% of global fungicide active ingredients, create unpredictable pricing pressures that discourage farmer adoption and destabilize distributor margins. Energy costs, environmental compliance expenses, and export restrictions in major Chinese production provinces generate price volatility that African importers cannot hedge effectively [3]Source: China Crop Protection Industry Association, “Market Analysis Report,” ccpia.org.cn . Container shipping rates between Asia and African ports experienced 300-400% increases during 2021-2022, with residual effects continuing through 2024-2025 as logistics networks normalize. Regional distributors with limited working capital cannot absorb these cost fluctuations, leading to delayed product availability and reduced farmer access during critical application windows when disease pressure peaks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar Applications Drive Market Expansion

Foliar application commands 60.60% market share in 2025, reflecting the predominance of leaf-targeting diseases across Africa's diverse cropping systems and climatic conditions. This segment exhibits the fastest growth at 2.95% CAGR through 2031, driven by climate-induced disease pressure and precision application technologies that improve efficacy while reducing environmental impact.

Foliar spraying allows precise control of diseases by directly applying fungicides onto the foliage, ensuring that the treatment reaches pest populations effectively while minimizing exposure to non-target organisms. The method has proven particularly successful in controlling various crop diseases, including Fusarium head blight in wheat crops and leaf spots in peanut cultivation across Africa. Farmers across the continent prefer foliar application due to its compatibility with other treatments and the ability to act before infections become established.

By Crop Type: Grains and Cereals Anchor Demand Structure

Grains and cereals dominate fungicide consumption with a 42.35% market share in 2025, reflecting government food security priorities and subsidy programs that ensure crop protection access for staple food production. Wheat rust management across East Africa and maize disease control in Southern Africa drive consistent demand, while rice production in West Africa increasingly adopts fungicide programs as intensification efforts expand yield potential. This significant market position is primarily driven by Africa's role as a major producer of cereals like sorghum, maize, pearl millet, finger millet, teff, and African rice. Maize, being a major food crop grown in diverse agricultural zones and farming systems of Sub-Saharan Africa, faces considerable challenges from fungal diseases like borde blanco, downy mildew, Phaeosphaeria leaf spot, and Botryodiplodia stalk rot.

Fruits and vegetables emerge as the fastest-growing segment at 3.05% CAGR, propelled by export market expansion and European residue compliance requirements that favor newer fungicide chemistries. This accelerated growth is attributed to the increasing focus on high-value horticultural crops and the rising awareness about crop protection measures among farmers. The segment's growth is particularly driven by the cultivation of important fruits such as bananas, pineapples, dates, figs, olives, and citrus, along with principal vegetables including tomatoes and onions.

Geography Analysis

South Africa has established itself as a dominant player in the African fungicide market, commanding approximately 11.75% of the total market value in 2025, with a CAGR of 2.67% through 2031. The country's market-oriented agricultural economy is characterized by its remarkable diversity, encompassing major grains, oilseeds, deciduous fruits, subtropical fruits, and vegetables. The fungicide market in South Africa is primarily driven by the grains and cereals segment, which represents a significant portion of agricultural production. The country's advanced agricultural practices and well-developed infrastructure facilitate the efficient distribution and application of fungicides.

West Africa exhibits significant growth potential, driven by government food security initiatives and expanding commercial agriculture in Nigeria, Ghana, and Côte d'Ivoire. Nigeria's agricultural transformation agenda emphasizes crop protection as essential infrastructure, while Ghana's cocoa sector implements comprehensive black pod disease management programs supported by international development partners. The sub-region faces significant challenges from counterfeit products and limited regulatory enforcement, creating opportunities for legitimate suppliers that invest in farmer education and quality assurance programs.

East Africa demonstrates balanced growth, supported by coffee and floriculture export sectors that demand specialized fungicide programs and controlled-environment agriculture expansion in Kenya and Ethiopia. Southern Africa, anchored by South Africa's advanced agricultural sector, maintains steady growth through established supply chains and regulatory frameworks that facilitate technology adoption. Central Africa remains the smallest regional market but shows emerging potential as infrastructure development and agricultural modernization programs gain momentum, particularly in Cameroon's cocoa and coffee production systems.

Competitive Landscape

The Africa fungicide market exhibits moderate concentration, with the top five players including Syngenta Group, BASF SE, Bayer AG, Corteva Agriscience, and UPL Limited. The competitive landscape is characterized by the strong presence of multinational agrochemical conglomerates that leverage their extensive research capabilities and global expertise to maintain market leadership. These companies operate through well-established subsidiaries and distribution networks across major African agricultural markets, particularly in South Africa, Kenya, and Nigeria. The market structure exhibits moderate consolidation, with the top players controlling a significant portion of the market share through their diverse product portfolios and strong brand recognition in the region.

The market has witnessed several strategic acquisitions and partnerships aimed at strengthening market positions and expanding product offerings. Local players, though present in the market, face challenges in competing with global giants due to limited R&D capabilities and resource constraints. They maintain relevance through their deep understanding of local farming practices and established relationships with regional distributors. The competitive dynamics are further shaped by increasing collaboration between global and local players to enhance market penetration and address region-specific challenges in crop protection.

For established players to maintain and expand their market share, focus needs to be placed on developing innovative fungicide solutions that address the specific challenges faced by African farmers, particularly in combating emerging crop diseases and adapting to changing climate conditions. Companies must invest in strengthening their local presence through enhanced distribution networks and technical support services while simultaneously developing sustainable and environmentally friendly products. Building strong relationships with key stakeholders, including government agricultural bodies and farming communities, will be crucial for long-term success in the market.

Africa Fungicide Industry Leaders

Syngenta Group

BASF SE

Bayer AG

Corteva Agriscience

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: BASF Launched Priaxor® EC fungicide, into the Ethiopian market. Priaxor® EC is suited for wheat and barley farmers as it disrupts fungal growth. It has a long-lasting protection window of up to 28 days, reducing the overall number of fungicide applications and enhancing cost saving.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

Africa Fungicide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type. South Africa are covered as segments by Country.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| South Africa |

| Rest of Africa |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| Geography | South Africa |

| Rest of Africa |

Market Definition

- Function - Fungicides are chemicals used to control or prevent fungi from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms