Rodenticides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

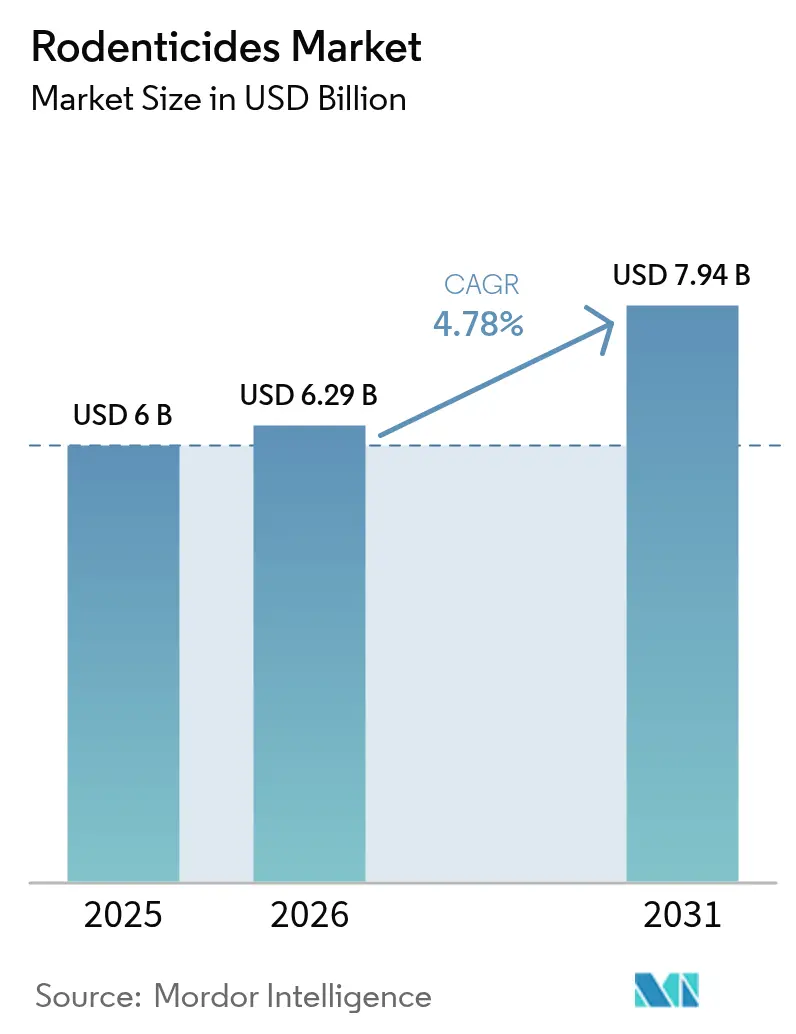

| Market Size (2026) | USD 6.29 Billion |

| Market Size (2031) | USD 7.94 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rodenticides Market Analysis by Mordor Intelligence

The rodenticides market size is expected to grow from USD 6.0 billion in 2025 to USD 6.29 billion in 2026 and is forecast to reach USD 7.94 billion by 2031 at 4.78% CAGR over 2026-2031. Rising climate-driven rodent populations, widening food-security gaps, and tightening public-health standards keep demand resilient across agricultural, commercial, and residential settings. Stringent sanitation rules in global food trade, combined with extended breeding seasons in warmer urban environments, amplify the need for reliable chemical and non-chemical solutions. Regulatory shifts restricting second-generation anticoagulant rodenticides (SGARs) in California and the United Kingdom accelerate innovation in low-toxicity flocoumafen and fertility-control products. Digital monitoring, including IoT-enabled bait stations, is lowering labor costs for pest-control operators while giving manufacturers new avenues to differentiate offerings.

Key Report Takeaways

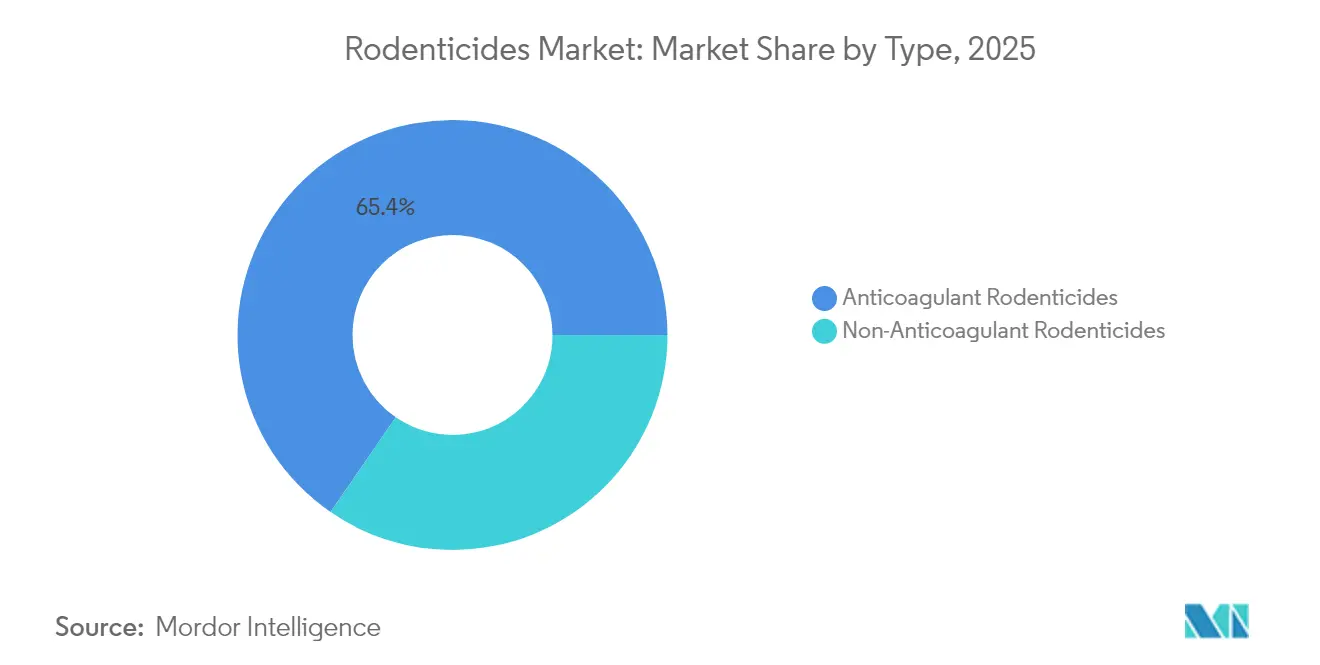

- By type, anticoagulants captured 65.40% of the 2025 rodenticide market size, and non-anticoagulants are projected to grow fastest at a 7.35% CAGR to 2031.

- By form, blocks led with 44.30% of the rodenticides market share in 2025, whereas liquid concentrates are set to expand at a 7.05% CAGR through 2031.

- By application, commercial and industrial premises held a 37.40% share of the rodenticides market size in 2025, while residential buildings are projected to rise at a 6.25% CAGR to 2031.

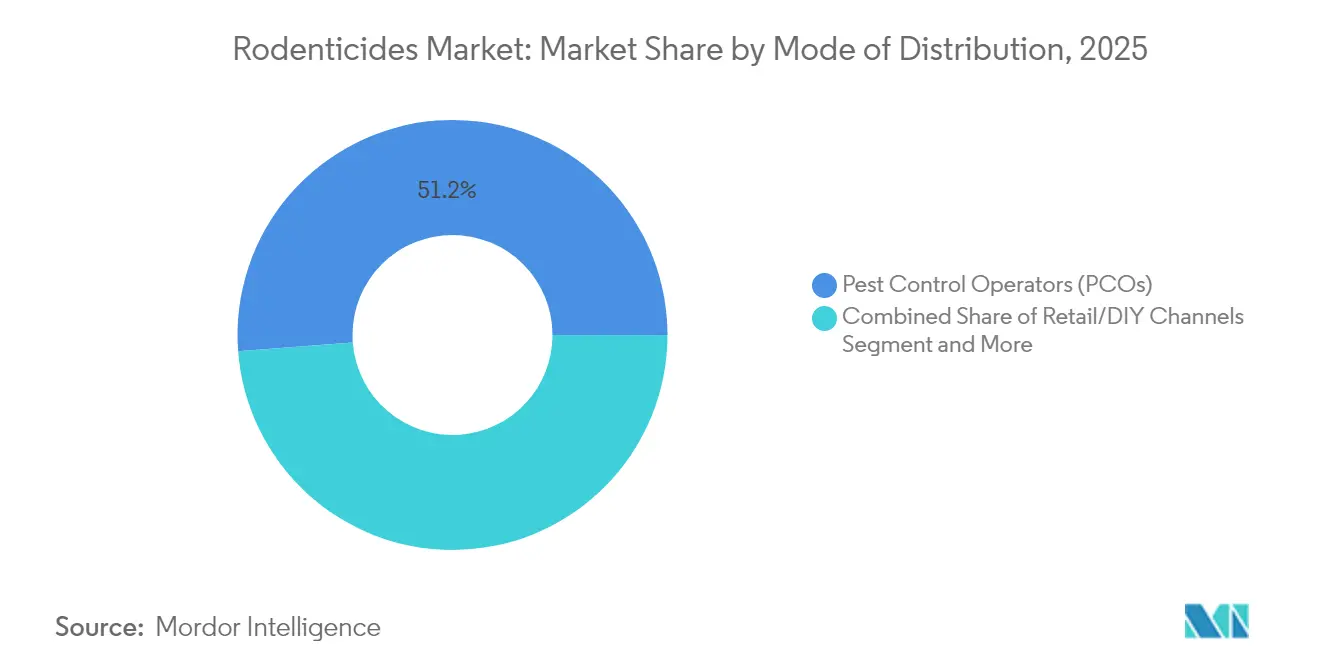

- By distribution, pest-control operators accounted for 51.20% of 2025 sales. Government vector-control programs are projected to show the highest CAGR at 7.02% through 2031.

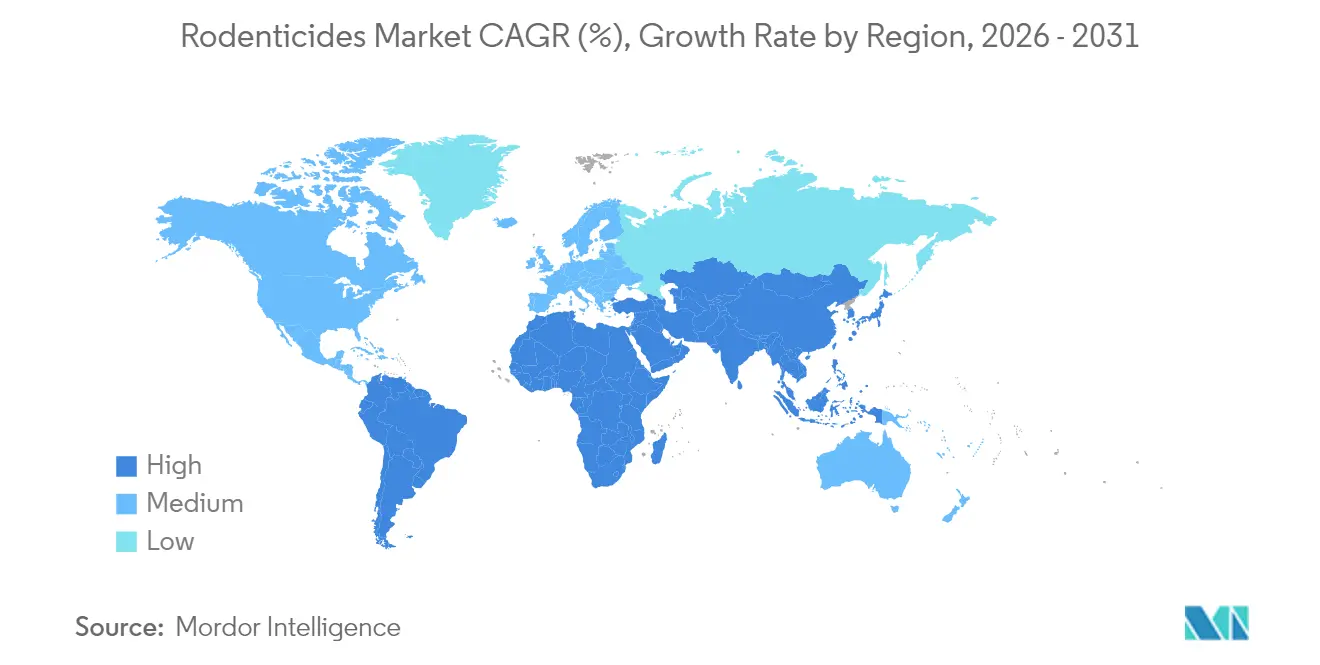

- By geography, North America led with 35.60% of the 2025 rodenticide market share, while the Asia-Pacific region recorded the fastest growth rate of 5.95% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rodenticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in bio-secure commodity trade standards | +0.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Increasing demand for food and agricultural productivity | +1.2% | Global, highest in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Proliferation of large-scale, vertically-integrated farming | +0.6% | Asia-Pacific core, spill-over to South America | Medium term (2-4 years) |

| Rapid urban rodent infestations linked to climate change | +0.9% | Global, concentrated in major metropolitan areas | Short term (≤ 2 years) |

| Adoption of single-dose, eco-labeled second-generation anticoagulants | +0.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Subsidized rodent-borne zoonosis prevention programs | +0.5% | Middle East, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Bio-secure Commodity Trade Standards

Trade agreements are increasingly requiring certified rodent-control protocols to prevent the transmission of pests across borders, compelling grain terminals, warehouses, and shipping lines to adopt professionally applied rodenticides and integrated pest-management (IPM) plans. Parallel mandates in the European Union and North America tie export eligibility to pest-free storage certificates, prompting exporters to deploy tamper-resistant bait boxes that comply with stewardship codes for second-generation anticoagulant rodenticides (SGAR). These measures shield multi-million-dollar consignments from quarantine holds, making professional-grade rodenticides a frontline tool in safeguarding trade continuity. The economic incentive widens as the Organisation for Economic Co-operation and Development and Food and Agriculture Organization (OECD-FAO) Agricultural Outlook anticipates 1.3% annual growth in consumption through 2032, intensifying pressure on already-stretched logistics networks [1]Source: Organisation for Economic Co-operation and Development, “OECD-FAO Agricultural Outlook 2023-2032,” oecd.org.

Increasing Demand for Food and Agricultural Productivity

Rising calorie needs and climate-induced yield volatility expose grain and horticulture systems to heavier post-harvest losses, which can reach 30-40% in emerging markets when rodent control is inadequate. Field studies across Asia-Pacific rice belts show ecologically based rodent management lifting yields 6-15% and farm incomes beyond 15%, a compelling return on rodenticide investments. In Africa, multimammate rats shave as much as 48% from maize harvests, pushing governments to subsidize broad-acre zinc-phosphide campaigns. The Food and Agriculture Organization confirms that combining structural silo upgrades with targeted chemical control sharply curtails storage losses[2]Source: Food and Agriculture Organization of the United Nations, “Integrated Rodent Management in Grain Storage,” fao.org . As climate shifts stretch breeding seasons, growers scale up from spot treatments to programmatic applications, reinforcing long-run volume growth in the rodenticides market.

Proliferation of Large-scale, Vertically Integrated Farming

Mega-farms standardize pest-management protocols across multiple sites, often outsourcing to certified pest-control operators to ensure compliance and consistent service quality. German pig-production research found that 70% of farms contract professionals, gaining both cost savings and higher efficacy. Bulk purchasing leverages pricing and secures the supply of advanced formulations like cholecalciferol blends, giving the rodenticides market a predictable baseline demand. Precision-agriculture platforms integrate rodent activity sensors, guiding bait placement and optimizing consumption, which amplifies the value proposition of digital-ready products.

Rapid Urban Rodent Infestations Linked to Climate Change

Heat-island effects and erratic precipitation favor longer breeding spells for commensal rodents, with Washington D.C. posting the world’s steepest surge in urban rat sightings during 2024. Similar spikes in Paris, Sydney, and Jakarta force municipalities to escalate baiting programs and citizen education. Cities now pair sanitation drives with real-time tracking of bait stations, compelling suppliers to deliver formulations that stay palatable despite outdoor temperature swings and moisture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in the number of resistant pests | -0.7% | Global, most severe in developed markets | Medium term (2-4 years) |

| Environmental and human-health hazards | -0.9% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Tightening restrictions on outdoor SGAR use | -0.6% | North America and Europe primarily | Short term (≤ 2 years) |

| Growing availability of fertility-control alternatives | -0.3% | North America and Europe, limited elsewhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in the Number of Resistant Pests

Genetic mutations, particularly in the Vkorc1 gene, undermine first- and second-generation anticoagulants, raising treatment costs and prolonging infestation timelines. Lebanese fieldwork confirmed resistance in house mice and rats despite limited oversight of rodenticide sales. New Zealand studies detected brodifacoum tolerance in isolated populations lacking prior exposure, hinting at spontaneous resistance via genetic drift[3]Source: Commonwealth Scientific and Industrial Research Organisation, “Brodifacoum Resistance Study,” csiro.au . California ground squirrels now survive diphacinone and chlorophacinone pulses, compelling rotation to zinc-phosphide or cholecalciferol mixtures. Resistance inflates service calls and drives investment in diagnostics, tempering volume growth for legacy chemistries.

Environmental and Human Health Hazards

North American raptor necropsies revealed anticoagulant residues in 951 carcasses spanning three decades[4]Source: Society of Environmental Toxicology and Chemistry, “Anticoagulant Rodenticide Residues in Raptors,” setac.org . In South Africa, 92% of tested caracals carried SGAR traces, with proximity to vineyards identified as a key factor. The United States Environmental Protection Agency suspended dimethyl tetrachloroterephthalate (DCTP) in 2024 due to concerns about its impact on thyroid [5]Source: Office of the Federal Register, “Emergency Suspension of DCPA Registrations,” federalregister.gov . Heightened media coverage fuels consumer pushback, increasing demand for fertility control or mechanical traps in residential segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Anticoagulants Dominate Despite Innovation Pressure

Anticoagulants secured 65.40% of 2025 revenue, underpinning the rodenticides market leadership story. Their single-dose lethality against resistant strains anchors usage in warehouses and food plants even as regulators trim permissible concentrations. Second-generation molecules, such as brodifacoum, remain favored among professionals, while non-anticoagulant classes are projected to grow at a 7.35% CAGR to 2031, drawing demand toward zinc phosphide and cholecalciferol hybrids. Studies show that zinc phosphide reduced field populations by 58.15%, surpassing traditional first-generation outcomes.

In parallel, bromethalin and strychnine hold niche utility for burrow systems where anticoagulant resistance soars. Regulatory developments against metal phosphides in low-income regions temper broader adoption, yet specialized needs sustain modest demand. Overall, portfolio diversification lets market leaders buffer exposure to any single regulatory clampdown, keeping the rodenticides market adaptable.

By Form: Blocks Lead While Liquid Concentrates Surge

Blocks retained a 44.30% share of the 2025 market size demand due to weather resistance and compatibility with tamper-proof stations mandated under Second-generation anticoagulant rodenticides (SGAR) stewardship. Professionals appreciate their longevity outdoors, limiting call-backs. Pellets followed, favored for mechanical broadcast across rice paddies and row crops. The rodenticides market size attributable to liquid concentrates is forecast to grow 7.05% CAGR, outpacing overall sector expansion as precision-spray rigs and bait baggers gain traction.

Fieldwork shows that paraffin blocks kept 100% active-ingredient recovery in open air, although 50% detached within five weeks, prompting innovation in anchor systems. Pastes and gels have a growing demand in high-visibility retail and hospitality settings, where discreet application is crucial. Powders are declining due to drift concerns, but retain relevance for fumigant burrow dusting in grain facilities. Ready-to-use sachets meet the demand among homeowners for convenience, but rising licensing barriers on Second-generation anticoagulant rodenticides (SGARs) are tilting the DIY aisle toward first-generation actives or fertility tablets. The move toward internet-connected bait boxes amplifies demand for formulations stable under sensor rigs that log consumption. Manufacturers of engineering denser blocks that resist fragmentation stand to capture incremental volume as service contracts specify reduced site visits.

By Mode of Distribution: PCO Channel Strength Amid Retail Expansion

Pest-control operators (PCOs) held 51.20% of the 2025 distribution, signifying that professional delivery remains central to modern pest management. PCOs utilize route density and telemetry-enabled bait stations to reduce revisit frequency by up to 40%, resulting in an attractive total cost of ownership for clients. Government vector-control programs are projected to chart a 7.02% CAGR to 2031, as public health departments intensify proactive campaigns against hantavirus and leptospirosis.

The mix of retail and DIY stores is shifting from SGARs toward first-generation actives or botanical repellents due to packaging and licensing regulations. Texas’s 16-pound minimum SGAR pack mandate effectively directs casual buyers to alternative options, nudging households toward service contracts. Online platforms emerge as a niche channel, yet most jurisdictions still limit direct-to-consumer sales of professional concentrations.

By Application: Commercial Dominance Amid Residential Growth

Commercial and industrial premises accounted for 37.40% of 2025 consumption, solidifying their position as the largest rodenticides market application segment. Food processors, pharmaceutical plants, and logistics hubs commit to year-round Integrated Pest Management (IPM) contracts that bundle surveillance tech, sanitation audits, and staged bait rotations. Agricultural fields followed at 36.4%, where seasonal surges in rodent pressure dictate campaign-style applications ahead of harvests.

Warehouses and cold-chain nodes are expanding bait programs as global e-commerce compresses delivery cycles, making infestation a zero-tolerance issue. Post-harvest losses of up to 40% in developing economies underscore the link between effective rodent control and food security outcomes. Residential buildings, although smaller today, are projected to post the fastest 6.25% CAGR through 2031. Urban densification and climate-driven rat booms increase call volume for municipal health departments, prompting city budgets to shift toward integrated rodent control that combines public education with strategic baiting.

Geography Analysis

North America maintained the largest regional market share at 35.60% in 2025, reflecting mature regulatory frameworks, high adoption of professional pest control services, and substantial commercial and industrial applications. The region’s leadership stems from stringent food-safety regulations in warehousing and processing facilities, extensive agricultural operations requiring systematic pest management, and urbanization patterns that create ideal conditions for rodent infestations. Growth is projected at 3.98% CAGR through 2031, constrained by environmental regulations yet supported by climate-driven urban rodent population rises and advances in application technology. The Environmental Protection Agency’s comprehensive rodenticide strategy, released in November 2024, delivers regulatory clarity while adding targeted mitigation measures for endangered-species protection.

Asia-Pacific represents the fastest-growing regional segment at a 5.95% CAGR to 2031, propelled by rapid urbanization, agricultural expansion, and heightened food security awareness in developing economies. China’s rodent programs rely heavily on diphacinone for commensal species and zinc phosphide for field pests, with provincial agencies coordinating large-scale campaigns across urban and rural zones. Ecologically-based rodent management has lifted cereal yields by 6-15% and farm income by more than 15% across multiple nations, reinforcing adoption momentum.

Europe is expected to advance at a 3.65% CAGR through 2031, as harmonized EU rules encourage standardized product labeling and spur the development of eco-friendly formulations. The United Kingdom’s ban on outdoor bromadiolone and difenacoum, effective July 2024, shifts product portfolios toward cholecalciferol and flocoumafen. Africa and the Middle East are projected to post CAGRs of 5.25% and 4.72%, respectively, driven by urban growth, expanding agriculture, and public health measures aimed at controlling rodent-borne diseases. South America is projected to advance at a 5.02% CAGR, with Brazil’s biosecurity-centered trade rules underpinning steady demand. A gradual shift toward ecologically based rodent management in Sub-Saharan Africa signals a strategic evolution, yet acute outbreaks still necessitate conventional rodenticides.

Note: Segment share of all individual segments available upon report purchase

Competitive Landscape

The top five suppliers account for a significant share of the 2024 rodenticide market size revenue, resulting in a highly concentrated market structure for rodenticides. BASF SE leads with the strength of the Selontra (cholecalciferol) and Storm (flocoumafen) brands, while Bayer AG leads through the Racumin (coumatetralyl) lines. Syngenta Group captures a significant share with the Talon and Weatherblok franchises, while Rentokil Initial plc secures a prominent share through service bundling. Liphatech rounds out the group with its advances products, including Rozol and FirstStrike.

BASF announced plans in 2023 to exit difenacoum and redirect research and development toward greener actives, signaling the industry's commitment to lower toxicity profiles. Bayer funnels pipeline capital into formulation technologies that enhance palatability at reduced active loads, doubling as stewardship and cost-of-goods strategies. Syngenta reports mixed sales as channel inventories linger, yet continues to trial data-logging bait stations to integrate chemistry with analytics.

Small entrants focus on niche segments, such as fertility control, with SenesTech’s ContraPest gaining municipal pilots but facing adoption hurdles tied to re-baiting frequency and cost. IoT start-ups supply hardware that lowers operator labor by automating route prioritization, partnering with chemistry majors eager to embed proprietary sensors in bait stations. Patent filings focus on calcium-based matrices and anti-crumble binders that resist fragmentation in high-humidity environments, highlighting formulation science as a durable competitive advantage.

Rodenticides Industry Leaders

BASF SE

Bayer AG

Rentokil Initial plc

Liphatech

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: The United States Environmental Protection Agency (EPA) released its final biological evaluation of 11 rodenticides, concluding that 88% of endangered species face no adverse impact under proposed mitigations.

- October 2024: BASF Group reported Q3 results showing higher contributions from its Agricultural Solutions division, which includes rodenticides, and highlighted continued investment in flocoumafen and cholecalciferol formulations.

- August 2024: EPA issued cancellation orders for multiple pesticide registrations, mandating stewardship steps for existing inventory disposal.

- March 2024: Bayer AG’s Capital Markets Day presentation emphasized its plan to launch ten blockbuster crop-protection products in the next decade, a pipeline that includes next-generation rodenticide technologies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global rodenticides market as all chemical or biologically derived formulations sold to kill or sterilize commensal rodents across farm fields, food warehouses, industrial facilities, commercial premises, and households. Covered actives span first- and second-generation anticoagulants, acute non-anticoagulants, and fertility-control baits supplied in blocks, pellets, powders, pastes, gels, and liquid concentrates.

Scope exclusion: For clarity, we exclude traps, electronic repellents, monitoring devices, and live-capture systems from valuation.

Segmentation Overview

- By Type

- Non-Anticoagulant Rodenticides

- Bromethalin

- Cholecalciferol

- Zinc Phosphide

- Strychnine

- Anticoagulant Rodenticides

- First-Generation

- Warfarin

- Chlorophacinone

- Diphacinone

- Coumatetralyl

- Second-Generation

- Difenacoum

- Brodifacoum

- Flocoumafen

- Bromadiolone

- First-Generation

- Non-Anticoagulant Rodenticides

- By Form

- Blocks

- Pellets

- Powders

- Pastes and Gels

- Liquid Concentrates

- By Application

- Agricultural Fields

- Warehouses and Storage Facilities

- Commercial and Industrial Premises

- Residential Buildings

- By Mode of Distribution

- Pest Control Operators (PCOs)

- Retail/DIY Channels

- Government Vector-Control Programs

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with agronomists, pest-control operators, municipal vector-control managers, and distributors across North America, Europe, Asia-Pacific, and Latin America. Interviews validated usage intensity, emerging ASP ranges, and expected regulatory changes that desk work could not fully capture.

Desk Research

We mined FAOSTAT, USDA NASS, Eurostat crop-loss files, UN Comtrade trade codes, and ECHA plus US EPA restricted-use product lists to size addressable demand and regulatory availability. Company 10-Ks, investor decks, and pest-control association surveys gave channel sales ratios, while patent alerts from Questel and news feeds in Dow Jones Factiva traced molecule pipelines and pricing shifts. These examples illustrate the breadth of sources. Numerous other public and paid datasets were reviewed.

Market-Sizing & Forecasting

We began with a top-down penetration model that linked rodent incident reports and crop or warehouse surface area to bait consumption by region. We then cross-checked it once through supplier roll-ups and sampled ASP × volume calculations. Inputs such as urbanization rate, grain storage capacity, climate-driven rodent population indices, pest-control service revenue, and regulatory phase-out timelines feed a multivariate regression used to project sales to 2030. Data gaps in supplier-level samples were bridged with nearest-neighbor benchmarks and reconfirmed via expert callbacks.

Data Validation & Update Cycle

Our outputs pass anomaly screening, peer review, and a single round of triangulation before release. Reports refresh annually, with interim updates triggered by major regulatory or disease-outbreak events.

Why Mordor's Rodenticides Baseline Commands Reliability

Published estimates diverge because firms pick different product mixes, channel coverage, years, and currency bases. We disclose scope and refresh cadence, so our baseline aligns closely with actual sales trends.

We observe external values often drop fertility-control baits, apply static ASPs, or pool retail DIY volumes with professional sales, inflating or deflating totals versus Mordor's calibrated split.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.0 billion (2025) | Mordor Intelligence | |

| USD 5.55 billion (2023) | Global Consultancy A | Stops at 2023 and omits fertility-control baits |

| USD 4.2 billion (2024) | Trade Journal B | Excludes commercial pest-control channel and uses conservative ASPs |

| USD 2.71 billion (2023) | Regional Consultancy C | Focuses only on farm use and fixed currency rates |

This comparison shows that Mordor Intelligence's disciplined variable selection and repeatable steps give decision-makers the most dependable starting point.

Key Questions Answered in the Report

What is the current size of the global rodenticides market?

The market is worth USD 6.29 billion in 2026 and is projected to reach USD 7.94 billion by 2031.

Which region holds the largest revenue share?

North America led in 2025 with a 35.60% share, supported by strict food‐safety regulations and widespread professional pest-control services.

Which region is growing the fastest?

Asia-Pacific posts the quickest expansion at a 5.95% CAGR through 2031, driven by rapid urbanization and rising food-security investments.

What product type dominates global sales?

Anticoagulant rodenticides accounted for 65.40% of 2025 revenue owing to their single-dose efficacy against resistant rodent species.

How are regulations shaping market dynamics?

Measures such as the United Kingdom’s 2024 outdoor SGAR ban tighten use conditions and push manufacturers toward eco-labeled flocoumafen and cholecalciferol formulations.

What technological trends are influencing the sector?

IoT-enabled bait stations that log consumption data are lowering service costs and helping pest-control operators optimize treatment routes.

Page last updated on: