China Fungicide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

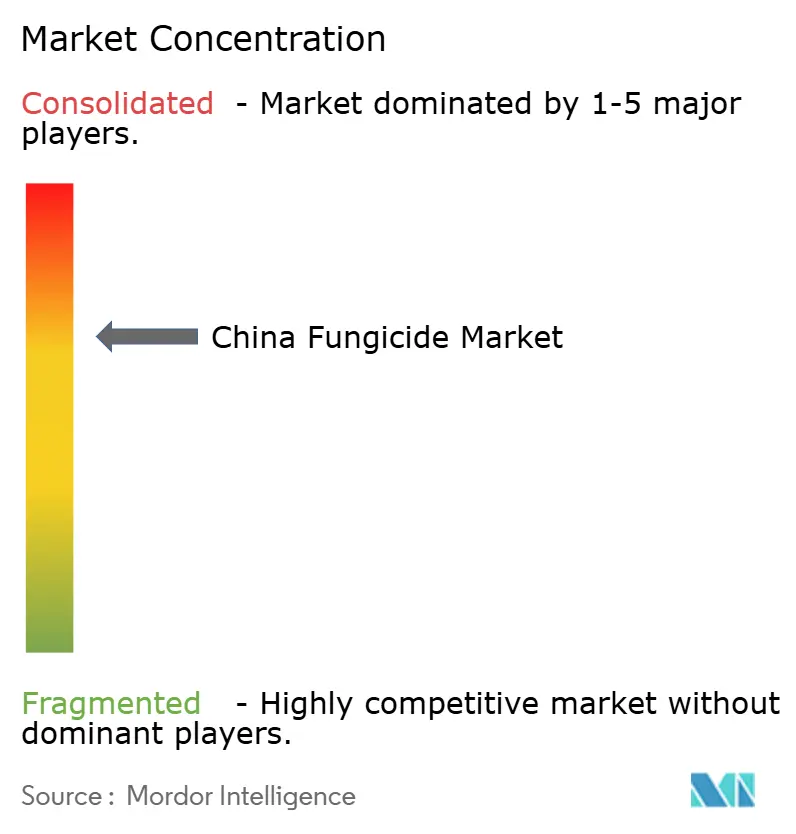

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Fungicide Market Analysis by Mordor Intelligence

The China fungicide market size is expected to grow from USD 1.35 billion in 2025 to USD 1.41 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at 4.15% CAGR over 2026-2031. Sustained enforcement of maximum residue limits (MRLs), rising biological registrations after the National Development and Reform Commission’s “Green Food” targets, and greenhouse acreage expansion in coastal provinces are collectively underpinning growth. Consolidation among distributors, broader e-commerce penetration, and smart-sprayer subsidies continue to enhance last-mile reach, while raw-material cost volatility and pathogen resistance to triazole and strobilurin molecules temper market momentum. Multinationals defend premium portfolios through rapid active ingredient launches, whereas domestic companies differentiate via localized biological solutions and price-sensitive offerings.

Key Report Takeaways

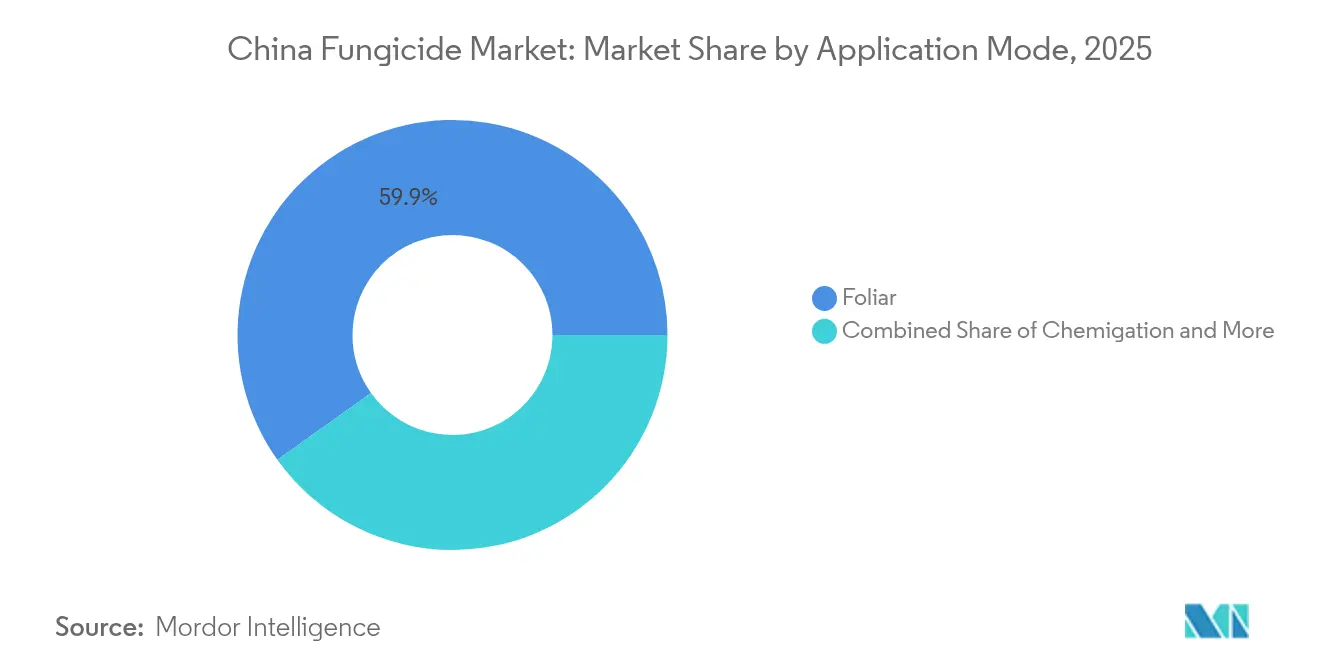

- By application mode, foliar application led with 59.85% of the China fungicide market share in 2025, and exhibits the fastest trajectory at a 4.23% CAGR through 2031.

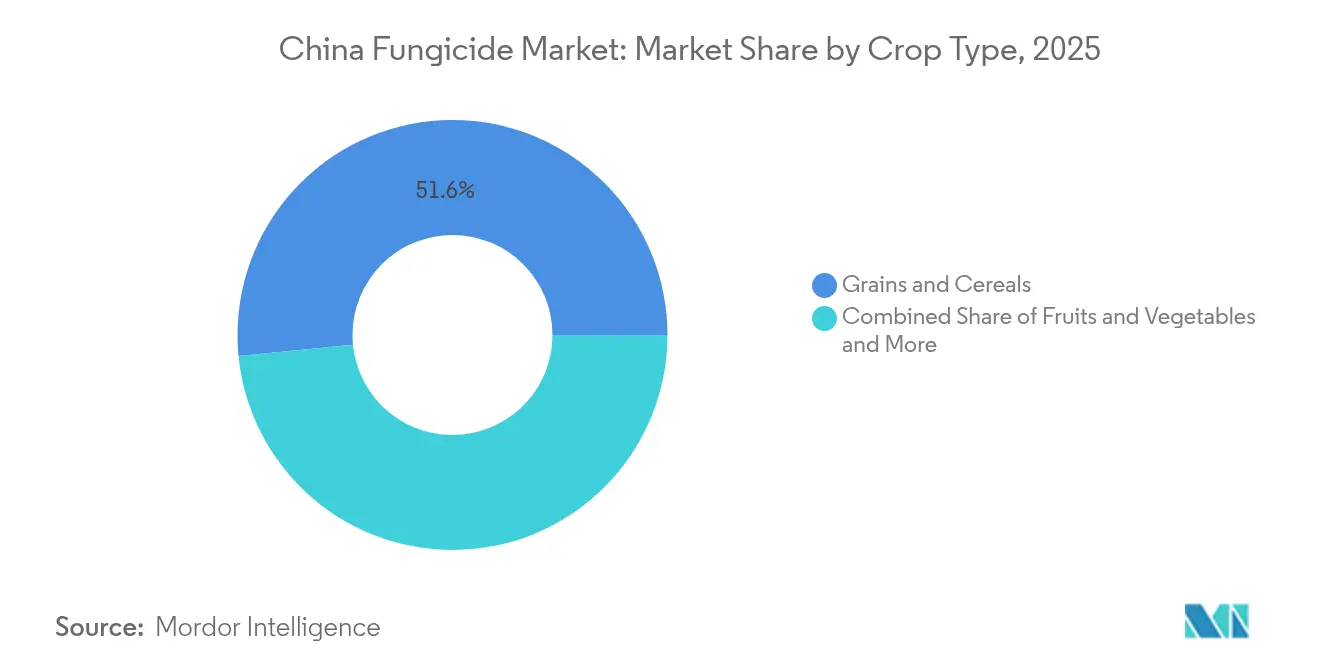

- By crop type, grains and cereals held 51.55% of the China fungicide market size in 2025, while fruits and vegetables are expanding at a 4.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Fungicide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent MRL enforcement boosting premium fungicide demand | +1.2% | East China, South China coastal provinces | Medium term (2-4 years) |

| Accelerated shift to biological actives after 2027 NDRC “Green Food” targets | +0.8% | National, with early adoption in Jiangsu, Shandong | Long term (≥ 4 years) |

| Expansion of high-value greenhouse acreage in coastal provinces | +0.6% | East China, South China | Medium term (2-4 years) |

| Government subsidies for smart-sprayer adoption in large farms | +0.5% | North China, Northeast China grain regions | Short term (≤ 2 years) |

| Rapid consolidation of distribution chains lowering last-mile costs | +0.4% | Central China, Southwest China rural areas | Medium term (2-4 years) |

| Investments by e-commerce platforms in ag-input marketplaces | +0.3% | National, concentrated in digital-first regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent MRL Enforcement Boosting Premium Fungicide Demand

China's enhanced maximum residue limit monitoring creates compelling economics for premium fungicide adoption across export-oriented agricultural regions. The Ministry of Agriculture and Rural Affairs implemented stricter testing protocols in 2024, with violation rates triggering immediate export bans that can cost individual producers USD 50,000 to USD 200,000 per incident [1]Source: Ministry of Agriculture and Rural Affairs, “Agricultural Chemical Registration and Management,” MOA.GOV.CN . This regulatory pressure particularly affects fruit and vegetable growers in coastal provinces, where export revenues justify premium product costs. The shift toward low-residue formulations accelerates biological fungicide adoption, with registration approvals increasing 40% in 2024 compared to conventional actives. Export-focused cooperatives now mandate certified low-residue products, creating predictable demand for manufacturers offering compliant solutions.

Accelerated Shift to Biological Actives After 2027 NDRC "Green Food" Targets

The National Development and Reform Commission's 2027 "Green Food" certification targets fundamentally reshaping fungicide development priorities by requiring a 30% reduction in synthetic active ingredient usage across certified operations. This policy creates a bifurcated market where biological products command premium pricing while conventional fungicides face volume pressure. Early adopters in Jiangsu and Shandong provinces report 15% to 25% yield improvements when combining biological fungicides with integrated pest management practices, validating the economic case for transition. The regulatory framework provides 5-year tax incentives for biological product manufacturers, spurring domestic R&D investment and accelerating time-to-market for new formulations.

Expansion of High-Value Greenhouse Acreage in Coastal Provinces

Coastal province greenhouse expansion drives specialized fungicide demand as controlled environment agriculture requires different disease management approaches than field crops. Greenhouse acreage in Shandong, Jiangsu, and Guangdong provinces increased 18% in 2024, with new facilities targeting high-value crops like tomatoes, peppers, and leafy greens that command premium prices. These operations use 3 to 5 times more fungicide per hectare than field crops but generate 8 to 12 times higher revenue per unit area, justifying premium product adoption. Greenhouse operators increasingly favor systemic fungicides and biological solutions that maintain consistent efficacy under controlled conditions while meeting food safety requirements for direct consumer sales.

Government Subsidies for Smart-Sprayer Adoption in Large Farms

Government subsidies covering 40% to 60% of precision application equipment costs accelerate smart sprayer adoption among large-scale grain producers, fundamentally changing fungicide application economics. The Ministry of Agriculture allocated CNY 2.8 billion (USD 390 million) in 2024 for precision agriculture equipment, with smart sprayers representing the largest category. These systems reduce fungicide usage by 25% to 35% while improving coverage uniformity, creating cost savings that offset premium product prices. Large farms in Heilongjiang and Inner Mongolia report 20% to 30% reduction in total crop protection costs after adopting variable-rate application technology, driving demand for concentrated formulations optimized for precision delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pathogen resistance to triazole and strobilurin molecules | -0.7% | National, concentrated in intensive cropping areas | Long term (≥ 4 years) |

| Ban on highly toxic active ingredients effective 2026 | -0.6% | National, affecting legacy product portfolios | Short term (≤ 2 years) |

| Volatile raw-material prices for key intermediates | -0.4% | National, impacting domestic manufacturers | Medium term (2-4 years) |

| Smallholder price sensitivity limiting premium uptake inland | -0.3% | Central China, Southwest China, Northwest China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Pathogen Resistance to Triazole and Strobilurin Molecules

Accelerating pathogen resistance to established fungicide classes forces costly product reformulation and limits treatment options for key diseases affecting China's major crops. Rice sheath blight resistance to triazole fungicides increased 25% across major production regions in 2024, requiring combination products or alternative chemistries that increase treatment costs by 40% to 60% [2]Source: Chinese Academy of Agricultural Sciences, “Plant Protection Research Annual Report 2024,” CAAS.CN . Wheat powdery mildew populations in North China show cross-resistance patterns that eliminate multiple product options simultaneously, forcing growers toward expensive biological alternatives or untested chemical combinations. This resistance pressure accelerates the need for new active ingredient development but creates market uncertainty as established products lose efficacy, potentially constraining overall market growth as farmers delay purchasing decisions pending new solution availability.

Ban on Highly Toxic Active Ingredients Effective 2026

The 2026 prohibition on highly toxic fungicide active ingredients eliminates approximately 15% of current product registrations, forcing market participants to reformulate existing products or exit specific crop segments. The Ministry of Agriculture's banned substance list includes several cost-effective actives used in grain production, creating supply gaps that alternative chemistries may not immediately fill. Manufacturers face USD 10 million to USD 50 million reformulation costs per major product line, with no guarantee that replacement products will achieve equivalent efficacy or cost structures. Small-scale domestic producers may exit the market rather than invest in reformulation, potentially reducing competitive pressure but also limiting product availability in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Precision Technology Drives Foliar Dominance

Foliar application commands 59.85% market share in 2025, reflecting China's rapid adoption of precision agriculture technologies and government subsidies for smart sprayer systems. The segment's 4.23% CAGR through 2031 outpaces other application methods as large-scale grain producers invest in variable-rate application equipment that optimizes fungicide placement and reduces waste . This dominance is driven by its effectiveness in targeting the plant's above-ground parts, where fungal pathogens commonly establish and thrive.

Foliar fungicide application provides rapid action against fungal pathogens through quick absorption and translocation properties within the plant, allowing fungicides to efficiently reach affected tissues and inhibit or kill fungi. The segment is experiencing robust growth supported by the increasing adoption of integrated pest management approaches that emphasize targeted and precise application methods. The segment's growth is further bolstered by technological advancements in spraying equipment and formulation technologies that enhance the efficiency of foliar applications while minimizing environmental impact.

By Crop Type: Grains Drive Volume While Fruits Command Premium

Grains and cereals dominate with 51.55% market share in 2025, underpinned by China's food security priorities and intensive rice-wheat cultivation systems that require consistent disease management. Fruits and vegetables emerge as the fastest-growing segment, benefiting from rising consumer incomes and export market development that justify premium fungicide investments. Major cereal-growing regions include Heilongjiang, Jilin, Liaoning provinces, Hebei, Henan, Shandong, and Anhui provinces. These regions face significant challenges from fungal diseases such as wheat stripe rust, wheat powdery mildew, rice blast, corn smut, barley leaf blight, and oat crown rust, which necessitate extensive fungicide usage to protect crop yields and ensure food security.

The fruits and vegetables segment is projected to exhibit the highest growth rate of approximately 4.33% during the forecast period 2031. This growth is driven by expanding cultivation areas, rising demand for fresh produce, and increased fungal disease pressure in the sector. The Northern China Plain, Yangtze River Delta, Pearl River Delta, Yunnan Province, Xinjiang Province, and Hainan Province are witnessing significant expansion in fruit and vegetable cultivation. These regions face challenges from various fungal diseases, including Citrus Huanglongbing (HLB), apple scab, grape downy mildew, tomato late blight, cucumber mosaic virus, fusarium wilt, and peach leaf curl, driving the increased adoption of plant fungicide for crop protection.

Geography Analysis

East China dominates the fungicide market through concentrated agricultural activity, advanced farming practices, and proximity to major chemical manufacturing centers that reduce distribution costs and improve product availability. The region's greenhouse expansion and export-oriented production drive premium fungicide adoption, with growers willing to invest in high-performance products that meet international residue standards and maximize crop quality. Jiangsu and Shandong provinces lead biological fungicide adoption, supported by government incentives and technical extension services that facilitate farmer education and product transition. The region's established distribution networks ensure rapid new product introduction and comprehensive technical support that accelerates innovation adoption across diverse crop segments.

North China and Northeast China grain production regions show steady demand growth supported by government subsidies for precision agriculture equipment and integrated pest management practices. Large-scale farming operations in Heilongjiang and Inner Mongolia increasingly adopt variable-rate application technologies that optimize fungicide placement and reduce waste, creating demand for concentrated formulations and biological alternatives. The region's harsh winter conditions limit disease pressure seasonality but create storage and handling challenges that favor stable liquid formulations over powder products. Crop rotation practices in these regions support diverse fungicide demand patterns as farmers manage different disease complexes across wheat, corn, and soybean production systems.

Central and South China regions benefit from crop diversification, year-round growing seasons, and rising consumer incomes that support premium product adoption. South China's tropical climate creates persistent disease pressure that requires consistent fungicide applications, particularly for biological products that maintain efficacy under high temperature and humidity conditions. Central China's rice-wheat rotation systems drive specialized product demand for diseases like rice sheath blight and wheat powdery mildew, while increasing vegetable production supports premium fungicide adoption. Southwest and Northwest China represent emerging markets where infrastructure development and crop intensification drive incremental demand growth, though smallholder price sensitivity limits premium product penetration in these regions.

Competitive Landscape

The China fungicide market exhibits a moderately consolidated structure with a mix of domestic and international players competing for market share. Nutrichem Co., Ltd., Syngenta AG Group, Bayer AG, UPL Limited, and BASF SE maintain a significant presence through their advanced technological capabilities and comprehensive product portfolios. The market has witnessed strategic consolidation through mergers and acquisitions, particularly among domestic players looking to strengthen their market position and expand their technological capabilities.

A balance between large-scale integrated agricultural solution providers and specialized fungicide manufacturers characterizes the competitive dynamics. Companies with integrated operations spanning research, manufacturing, and distribution have advantages in terms of cost efficiency and market reach. The market has seen increased collaboration between domestic and international players, combining local market knowledge with global technological expertise. This has led to the development of more sophisticated products and improved service delivery to farmers. The industry structure continues to evolve with companies focusing on vertical integration and expansion of their value chain presence.

For established players to maintain and expand their market share, focusing on sustainable product development and enhanced formulation technologies is crucial. Companies need to invest in developing biological fungicides and environmentally friendly solutions to align with increasing regulatory pressure and changing farmer preferences. Building strong relationships with agricultural communities through technical support and education programs helps create brand loyalty and market stability. Established players must also focus on digital integration and precision agriculture solutions to provide value-added services beyond traditional fungicide products. Investment in local manufacturing and R&D facilities helps companies adapt products to specific regional requirements and crop patterns.

China Fungicide Industry Leaders

Nutrichem Co., Ltd.

Syngenta AG Group

Bayer AG

UPL Limited

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: UPL Limited opened its new CNY 800 million (USD 111 million) formulation facility in Anhui Province, featuring automated production lines for liquid suspension concentrates and biological product manufacturing capabilities.

- February 2024: Syngenta Group announced a CNY 1.2 billion (USD 167 million) investment in biological fungicide manufacturing capacity at its Nantong facility, targeting 2027 production start for novel Bacillus-based products designed for rice and wheat applications.

China Fungicide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Market Definition

- Function - Fungicides are chemicals used to control or prevent fungi from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms