Copper Fungicides Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 435.60 Million |

| Market Size (2030) | USD 553.80 Million |

| Growth Rate (2025 - 2030) | 4.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

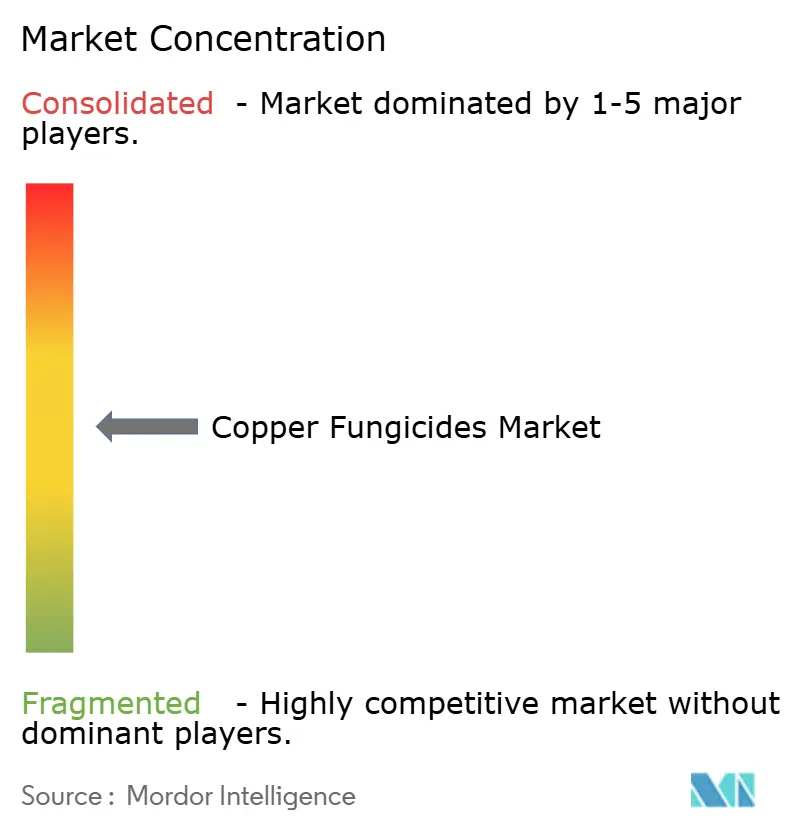

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Copper Fungicides Market Analysis by Mordor Intelligence

The copper fungicides market size stands at USD 435.6 million in 2025 and is forecast to advance at a 4.9% CAGR to USD 553.8 million by 2030, underscoring steady growth in an environment of stricter residue regulations and expanding specialty-crop acreage. The copper fungicides market continues to gain traction because these multi-site active ingredients remain integral to organic certification programs, offer dependable resistance-management value, and provide cost-effective disease control where synthetic options face curbs.[1]Agricultural Marketing Service, “Copper Sulfate,” ams.usda.gov Rising enforcement of maximum residue limits, progress in low-dust formulations, and government stimulus for orchard and vineyard revitalization sustain demand across high-value fruit, nut, and vegetable crops. Competition is moderate, leaving scope for regional specialists who commercialize products with lower metallic-copper loads. Asia-Pacific is poised for the fastest expansion on the back of orchard modernization policies and tropical disease pressure, while Europe retains leadership through entrenched organic practices despite tightening soil-load limits.

Key Report Takeaways

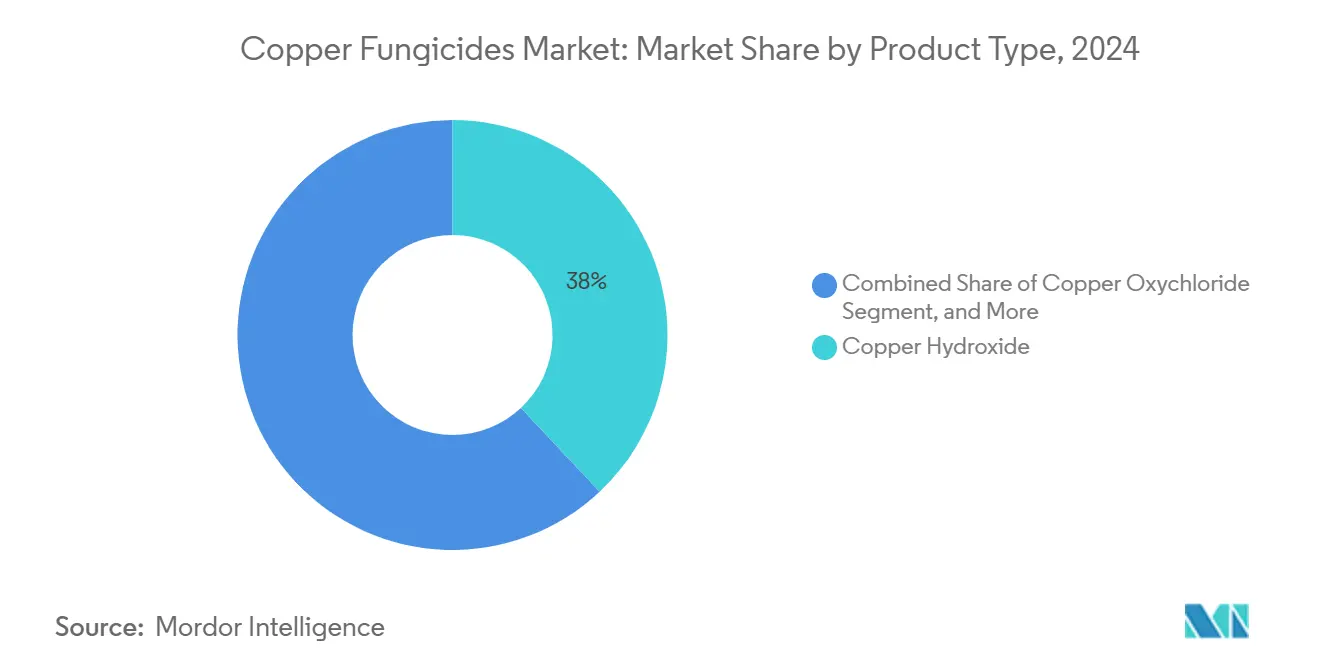

- By product type, copper hydroxide led with a 38% of the copper fungicides market share in 2024, whereas basic copper carbonate is projected to expand at a 6.9% CAGR through 2030.

- By formulation, wettable powder captured a 46% share of the copper fungicides market in 2024, and Suspension Concentrate (SC) formats are forecasted to rise at a 6.8% CAGR through 2030.

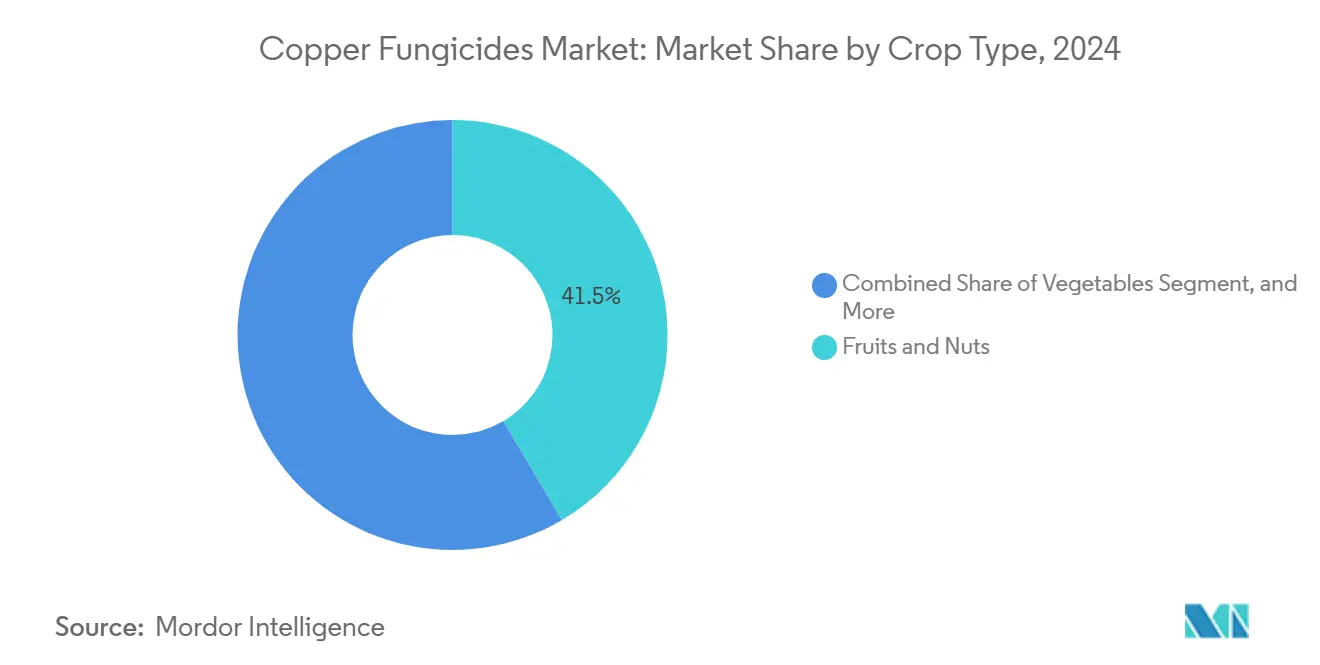

- By crop type, fruits and nuts accounted for a 41.5% share of the copper fungicides market size in 2024, while vegetables are projected to grow at a 6.8% CAGR between 2025 and 2030.

- By distribution channel, agro-retailers and cooperatives held a 65% share of the copper fungicides market in 2024, and online agricultural input platforms represent the fastest-growing route, advancing at an 8.2% CAGR.

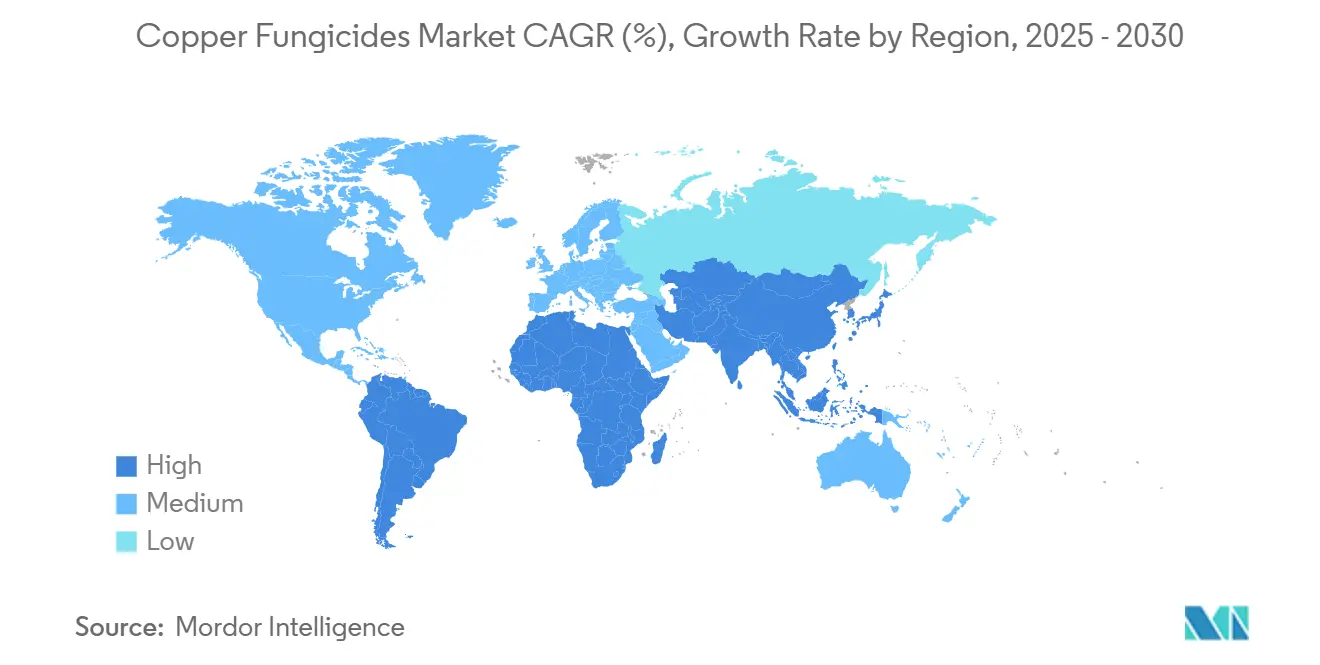

- By geography, Europe led with a 32% revenue share in 2024, and the Asia-Pacific region is projected to register the fastest growth at a 6.1% CAGR through 2030.

Global Copper Fungicides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Residue Level Enforcement in High-value Export Crops | +1.2% | Global, with emphasis on Europe, and North America | Medium term (2-4 years) |

| Expansion of Specialty Crop Acreage in Emerging Economies | +0.8% | Asia-Pacific core, spill-over to South America | Long term (≥ 4 years) |

| Cost-effectiveness Versus Synthetic Fungicides in Resistance-management Programs | +0.6% | Global | Short term (≤ 2 years) |

| Uptake of Micro-encapsulated and Low-dust WG Formulations for Worker-safety Compliance | +0.5% | North America and Europe | Medium term (2-4 years) |

| Growing Demand for Copper-based Inputs in Regenerative/Organic Certification Schemes | +0.7% | Global, with early gains in North America and Europe | Long term (≥ 4 years) |

| Government Stimulus for Orchard-replant and Vineyard-revitalization Projects | +0.4% | Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Residue-Level Enforcement in High-Value Export Crops

Regulatory requirements for lower residue limits are driving the adoption of advanced copper fungicides that remain effective at reduced application rates, enabling producers to comply with strict food safety standards. Specialty crop exporters targeting European Union and North American markets are moving away from traditional Bordeaux mixtures. Testing protocols, including in-season tissue analysis, influence buyers to choose products that comply with labeling requirements, supporting higher prices and market growth for copper fungicides. The Environmental Protection Agency's ongoing assessment indicates continued approval of copper-based active ingredients, provided manufacturers demonstrate reduced exposure risks.[2]EPA, “Pesticide Registration Review Notice,” federalregister.gov These regulatory frameworks support the development of durable, low-dose formulations that allow longer intervals between applications while staying within residue thresholds.

Expansion of Specialty-Crop Acreage in Emerging Economies

Governments in Asia-Pacific and South America are directing investments toward orchard establishment, greenhouse vegetables, and export-oriented floriculture, creating new demand for copper fungicides. The high humidity and bacterial pressures in tropical horticulture support the use of multi-site copper protectants, particularly in organic farming systems. Field trials in potato, banana, and mango cultivation demonstrate yield increases of 3 metric tons per hectare or more when copper-based programs are implemented during critical growth stages. As cultivation areas expand, distributors are increasing their warehouse capacity and combining copper fungicides with drip-fertigation services, strengthening the market position in long-cycle crops that need continuous disease control.

Cost-Effectiveness Versus Synthetic Fungicides in Resistance-Management Programs

Copper compounds play an important role in fungicide rotation programs due to increasing pathogen resistance to synthetic fungicides. As part of the FRAC group M01, copper fungicides provide multi-site activity with low resistance risk, offering growers a cost-effective option for disease management. Research trials on soybeans and grapes demonstrate that copper-based mixtures provide effective yield protection at lower costs compared to standalone triazole or succinate dehydrogenase inhibitor (SDHI) treatments. Copper fungicides are particularly valuable for organic producers, who cannot use synthetic alternatives, allowing them to maintain yields while accessing premium market prices.

Uptake of Micro-Encapsulated and Low-Dust WG Formulations for Worker-Safety Compliance

Worker safety regulations in North America and Europe are increasing the adoption of dust-free copper fungicides, which reduce inhalation exposure and minimize respirator requirements.[3]Occupational Safety and Health Administration, “Respiratory Protection Standard,” osha.gov These formulations feature encapsulated particles with enhanced rain-fastness, reducing re-application frequency by up to 33% compared to traditional wettable powders. Equipment manufacturers now incorporate closed-transfer systems compatible with water-dispersible granules to minimize handler exposure. Despite their higher prices, these safety-compliant formulations continue to gain market share, contributing to the growth of the copper fungicides market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Limits on Cumulative Copper Load in Soils | -0.9% | Global, with emphasis on Europe, and organic farming regions | Long term (≥ 4 years) |

| Volatility in Copper Raw-material Prices Impacting Formulation Costs | -0.6% | Global | Short term (≤ 2 years) |

| Proliferation of Biological Fungicide Substitutes with Zero Re-entry Interval | -0.7% | North America and Europe | Medium term (2-4 years) |

| Weather-driven Wash-off Losses Lowering Field-level Efficacy in Humid Tropics | -0.4% | Asia-Pacific and South America tropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Limits on Cumulative Copper Load in Soils

European regulations limit metallic-copper application to 6 kg per hectare annually, with proposed reductions to 4 kg. This requires farmers to implement precision spraying methods and regular soil testing, increasing operational costs. Research conducted in Poland demonstrates elevated copper accumulation in organic farming systems, leading to increased advocacy for stricter limits. These regulatory constraints affect the copper fungicides market by limiting application frequency, particularly in perennial crops that require multiple treatments for bacterial disease control.

Volatility in Copper Raw-Material Prices Impacting Formulation Costs

Copper price fluctuations, influenced by global electrification demands and mining industry consolidation, affect fungicide manufacturing costs. Supply chain disruptions further impact production expenses. Small-scale formulators, unable to hedge against price volatility, transfer increased costs to customers, reducing the price gap between copper and synthetic fungicides. Although improved copper-efficient delivery systems help offset cost increases, price volatility continues to impact the copper fungicides market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Copper Hydroxide Dominance Faces Carbonate Innovation

Copper hydroxide dominates the copper fungicides market size with a 38% share in 2024, primarily due to its high availability and extensive use in conventional agriculture. Its proven effectiveness in disease control and compatibility with crop protection programs maintains its market leadership. Basic copper carbonate is experiencing growth, particularly in organic horticulture, where its lower phytotoxicity is valued. The carbonate segment is projected to grow at a CAGR of 6.9%, supported by advancements in granular technologies that enhance handling, storage, and application efficiency.

Copper oxychloride and copper sulfate continue to serve specific market segments, particularly in citrus cultivation. Recent developments in copper salicylate suspensions indicate an evolution in formulation technology. These new concentrates provide effective disease control while using less metallic copper, addressing both sustainability requirements and regulatory standards. This development represents the industry's focus on increasing active ingredient efficiency while reducing environmental effects.

By Formulation: Suspension Concentrates Reshape Application Dynamics

Wettable Powders (WP) maintain a dominant 46% market share in agrochemical formulations due to their cost-effectiveness and wide application across agricultural practices. Their affordability and versatility make them the primary choice for small to medium-scale farmers, particularly in regions with budget limitations and conventional spraying methods. Suspension Concentrates (SC) are anticipated to grow at a compound annual growth rate (CAGR) of 6.8% through 2030. Suspension Concentrates have gained significant adoption among commercial farms and horticultural operations due to their enhanced handling characteristics and application precision.

SC formulations offer advantages through their ready-to-use liquid form and stable particle suspension, which ensures even distribution during application. These formulations are compatible with modern irrigation systems and closed-transfer mechanisms, enabling automated and safe agrochemical application. This compatibility reduces labor requirements and exposure risks while improving dosing precision, essential factors for large-scale agricultural operations meeting efficiency targets and regulatory requirements.

By Crop Type: Vegetables Segment Accelerates Through Organic Expansion

Fruits and nuts dominated the copper fungicides market size, accounting for 41.5% of total revenue. This dominance stems from established dormant-spray protocols that ensure consistent disease prevention across orchard crops. These practices have established copper use as a standard in perennial fruit production. The vegetables segment shows significant growth potential, with a projected compound annual growth rate (CAGR) of 6.8%. This growth is driven by the increasing adoption of organic farming, particularly in tomatoes, peppers, and leafy greens. Copper fungicides are essential in organic production, providing disease resistance while meeting organic certification requirements.

In cereal crops, copper-based seed treatments are integral to resistance management programs, providing alternative controls that complement broader-spectrum chemical applications. The ornamental and turf segments utilize specialized low-phytotoxic copper formulations for disease control. These formulations meet urban runoff regulations while providing effective treatment for landscaping and non-food crops.

By Distribution Channel: Digital Platforms Disrupt Traditional Agro-Retail Networks

Agro-retailers and cooperatives control 65% of the total copper fungicide market share through established grower relationships and specialized advisory services. Their local market knowledge and field support remain essential for farming operations, particularly those requiring specific product guidance and technical assistance. Digital platforms are transforming agricultural input procurement. These online channels are experiencing an 8.2% compound annual growth rate (CAGR), driven by increased smartphone adoption, improved internet connectivity, and farmer demand for price transparency. Agricultural operators increasingly use e-commerce platforms to access wider product selections, compare prices, and review products.

Traditional retail chains are adapting by implementing hybrid business models that combine physical locations with online platforms and digital engagement solutions. These retailers also focus on premium products, including specialized formulations that require technical expertise, strengthening their position with commercial growers. This transformation reflects the agricultural sector's modernization, as accessibility, convenience, and technical support reshape input distribution across farming segments.

Geography Analysis

Europe held 32% of the copper fungicides market size in 2024, maintaining its position as the largest regional market despite ongoing discussions about stricter soil regulations. German sales data in 2024 showed continued growers' dependence on copper fungicides, while Mediterranean vineyard operators maintain copper-based solutions for mildew control due to limited alternatives. Growers are implementing weather modeling systems and canopy sensors to optimize spray timing and maximize efficiency within permitted usage limits.

Asia-Pacific is the fastest-growing region in the global copper fungicides market, projected to achieve a robust CAGR of 6.1% through 2030. China continues to dominate regional demand, driven by persistent bacterial challenges in rice, citrus, and cucurbit cultivation. In the Philippines, successful banana farming in upland zones has accelerated the adoption of advanced copper formulations, catalyzing distribution network expansion across Mindanao and Luzon. India's copper fungicide market size is expanding due to increased usage in cereals, vegetables, and fruit crops. Enhanced disease management practices and emphasis on export-quality crop protection further support the country's market growth.

North America demonstrates stable market conditions, supported by the Environmental Protection Agency's 2024 registration review that confirmed copper's role in integrated pest management, driving improvements in low-dust granule formulations. Demand remains consistent through orchard-replant programs in the Pacific Northwest and vineyard revitalization initiatives in California. In South America, demand is driven by extensive soybean and corn cultivation, where copper serves as a resistance management tool, while local manufacturers secure raw materials through agreements with regional smelters. The Middle East and Africa represent smaller market segments but show growth in specific areas such as protected vegetable cultivation and export flower production. Israel specializes in drip-compatible copper chelates at premium prices, while Moroccan citrus producers are testing drone applications for copper distribution in challenging terrain, demonstrating technology-driven market development.

Competitive Landscape

The copper fungicides industry maintains a moderately fragmented structure. The major players include UPL Ltd., Bayer AG, BASF SE, Corteva Agriscience, and Nufarm Ltd., which influence pricing and technological advancement in the industry. These multinational companies utilize their global distribution networks and research capabilities to develop proprietary low-load formulations, including Kocide 50DF and Badge SC, maintaining product differentiation through enhanced efficacy and safety profiles.

Regional companies strengthen their market positions through strategic acquisitions. Sipcam Oxon's 2024 acquisition of Phyteurop assets enhanced its direct access to French agricultural cooperatives, expanding the distribution of copper hydroxide and oxychloride products. The industry also witnesses strategic collaborations between fungicide manufacturers. The 2025 fluindapyr agreement between FMC and Corteva demonstrates the emergence of co-marketing arrangements that combine broad-spectrum copper products with single-site SDHIs to provide comprehensive fungal control solutions for large-scale commodity farming operations.

Competition in the market centers on formulation patents, with companies developing nano-copper dispersions and copper-zinc hybrid products to improve rain resistance and extend treatment effectiveness. Companies enhance their market position by integrating decision-support platforms, offering subscription-based weather alert services that optimize copper spray timing for maximum effectiveness and minimal waste, thereby strengthening customer retention in the copper fungicides market.

Copper Fungicides Industry Leaders

UPL Ltd.

Bayer AG

BASF SE

Corteva Agriscience

Nufarm Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zhongda Agritech received official registration from China's Ministry of Agriculture and Rural Affairs for its new fungicide "Haoze" 40% Fluopyram · Oxine Copper SC (8% Fluopyram + 32% Oxine Copper). The product is designed for disease prevention, plant health maintenance, and sustained efficacy.

- September 2024: FMC Corporation established a distribution agreement with Ballagro Agro Tecnologia to expand its copper fungicide portfolio in Brazil. The agreement aims to provide Brazilian farmers with additional sustainable crop protection solutions.

- July 2024: FMC India introduced COSUIT, a copper fungicide containing Copper Hydroxychloride, designed to control fungal and bacterial diseases in grapes, paddy, tomato, chili, tea, fruits, vegetables, and ornamentals.

- June 2024: Sipcam Oxon acquired Phyteurop SA's distribution assets, expanding its presence in the European agricultural market, particularly in copper fungicides. The company established Sipcam France SA, a new subsidiary, and maintains a partnership with InVivo, Phyteurop's parent company, to ensure access to agricultural solutions.

Global Copper Fungicides Market Report Scope

Copper fungicides are agricultural chemicals containing copper compounds that prevent and control fungal and bacterial diseases in crops by inhibiting the growth of pathogens on plant surfaces.

The Copper Fungicides Market Report is egmented by product type (Copper Hydroxide, Copper Oxychloride, Copper Sulfate, Basic Copper Carbonate, and Other Product Types), by formulation (Wettable Powder (WP), Water-Dispersible Granules (WG), Suspension Concentrate (SC), and Other Formulations), by crop type (Fruits and Nuts, Vegetables, Cereals and Grains, Ornamental and Turf, and Other Crop Types), by distribution channel (Agro-Retailers and Cooperatives, and Online Agricultural Input Platforms), and by geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Copper Hydroxide |

| Copper Oxychloride |

| Copper Sulfate |

| Basic Copper Carbonate |

| Other Product Types |

| Wettable Powder (WP) |

| Water-Dispersible Granules (WG) |

| Suspension Concentrate (SC) |

| Other Formulations |

| Fruits and Nuts |

| Vegetables |

| Cereals and Grains |

| Ornamental and Turf |

| Other Crop Types |

| Agro-retailers and Cooperatives |

| Online Agricultural Input Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product Type | Copper Hydroxide | |

| Copper Oxychloride | ||

| Copper Sulfate | ||

| Basic Copper Carbonate | ||

| Other Product Types | ||

| By Formulation | Wettable Powder (WP) | |

| Water-Dispersible Granules (WG) | ||

| Suspension Concentrate (SC) | ||

| Other Formulations | ||

| By Crop Type | Fruits and Nuts | |

| Vegetables | ||

| Cereals and Grains | ||

| Ornamental and Turf | ||

| Other Crop Types | ||

| By Distribution Channel | Agro-retailers and Cooperatives | |

| Online Agricultural Input Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current copper fungicides market size?

The copper fungicides market size is USD 435.6 million in 2025 and is projected to reach USD 553.8 million by 2030 at a 4.9% CAGR.

Which region leads copper fungicide consumption?

Europe leads, holding 32% of 2024 revenue due to its extensive organic acreage and strict disease-management requirements.

Which crop segment is growing fastest for copper fungicides?

Vegetables segment is forecast to grow at a 6.8% CAGR through 2030, driven by organic production expansion and bacterial disease pressure.

How do soil-load regulations affect copper fungicides demand?

European proposals to cut annual copper limits from 6 kg to 4 kg per hectare may restrict application frequency, prompting growers to adopt low-load formulations or integrate biological alternatives.

What competitive strategies dominate the copper fungicides industry?

Companies focus on patented low-dust formulations, regional acquisitions, and digital advisory tools that bundle weather-based spray timing with product sales to cement customer loyalty.

Page last updated on: