Monoclonal Antibody Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 326.38 Billion |

| Market Size (2031) | USD 619.38 Billion |

| Growth Rate (2026 - 2031) | 13.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Monoclonal Antibody Therapeutics Market Analysis by Mordor Intelligence

The Monoclonal Antibody Therapeutics Market size is expected to increase from USD 287.13 billion in 2025 to USD 326.38 billion in 2026 and reach USD 619.38 billion by 2031, growing at a CAGR of 13.67% over 2026-2031.

Investment is shifting toward precision biologics that displace broad-spectrum small molecules, while multi-target constructs reach patients faster under accelerated review routes. Providers see clinical and economic value in home-administration formats that cut hospital days and lower readmission penalties. Sustained biosimilar pressure means innovators hedge with antibody-drug conjugates that defend premium price bands. Production footprints are also consolidating in Asia-Pacific, where new capacity trims per-gram cost to under USD 120, opening large addressable pools.

Key Report Takeaways

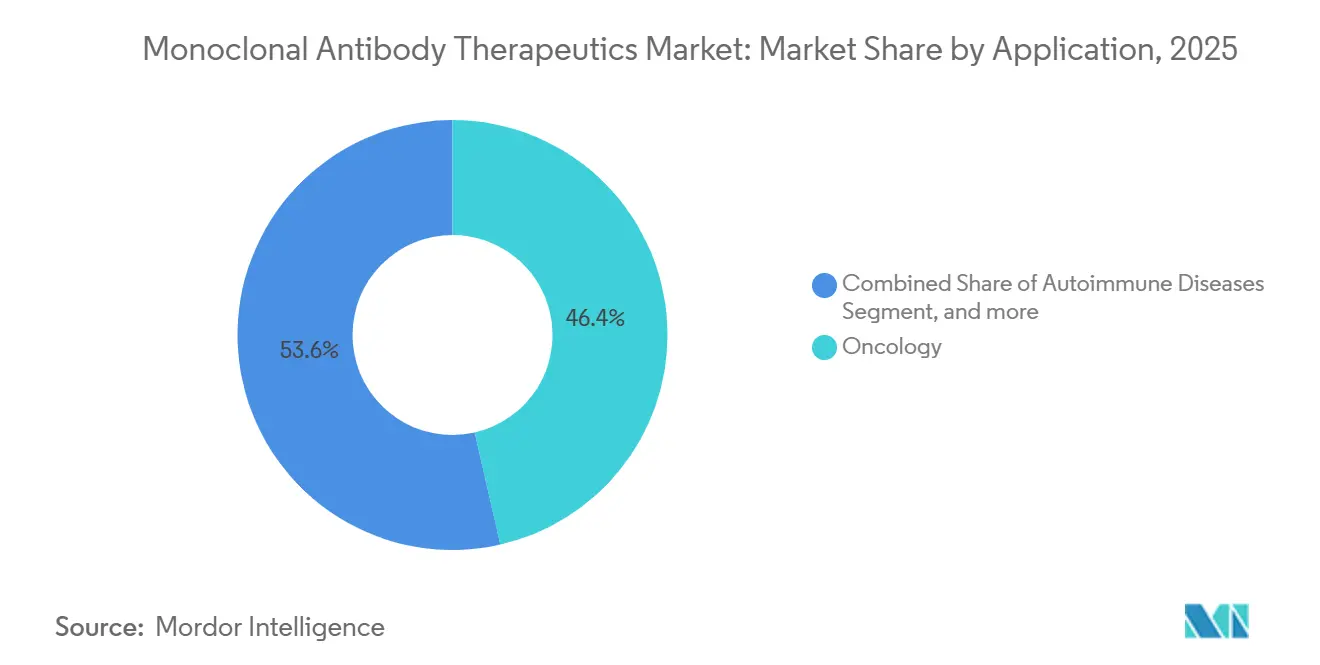

- By application, oncology led with 46.43% revenue in 2025, while infectious diseases are forecast to climb at 15.76% CAGR through 2031.

- By source, humanized antibodies held a 49.54% share in 2025, yet bispecific formats are set to advance at a 15.89% CAGR to 2031.

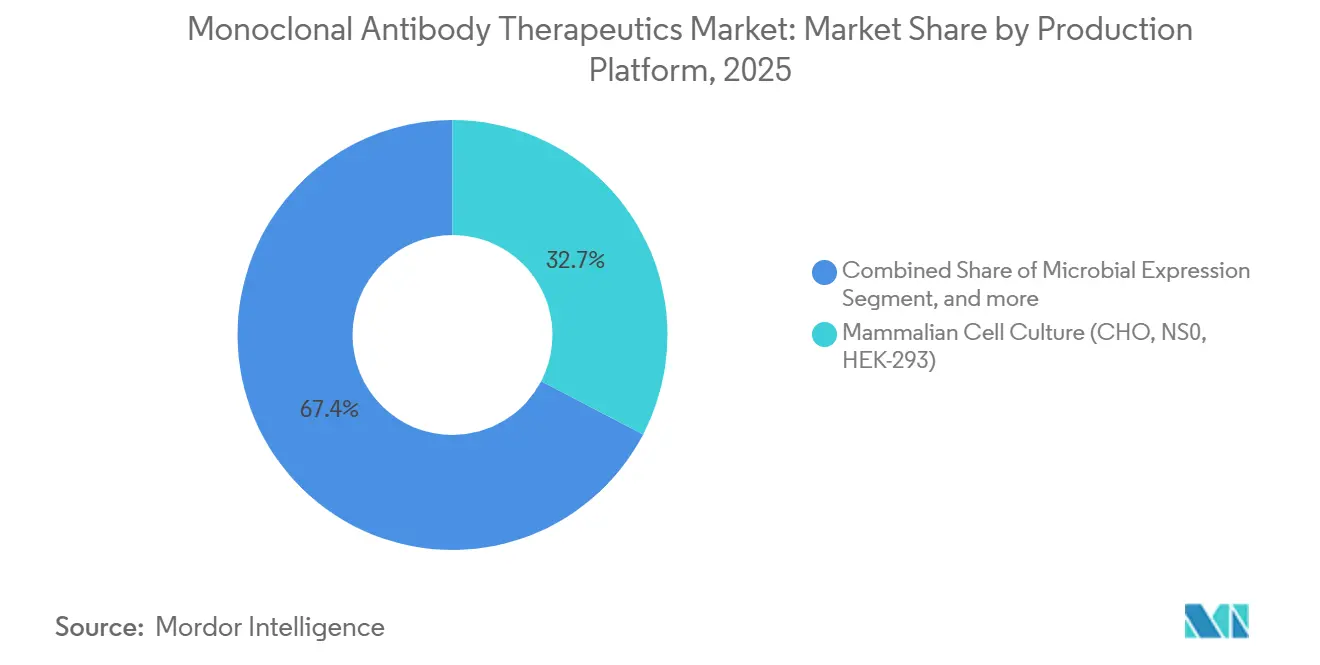

- By production platform, mammalian cell culture accounted for 32.65% of the 2025 base, whereas transgenic systems are projected to post a 15.32% CAGR over the outlook.

- By end user, hospitals accounted for 62.65% of 2025 spending, but home-care channels are growing at a 16.43% CAGR through 2031.

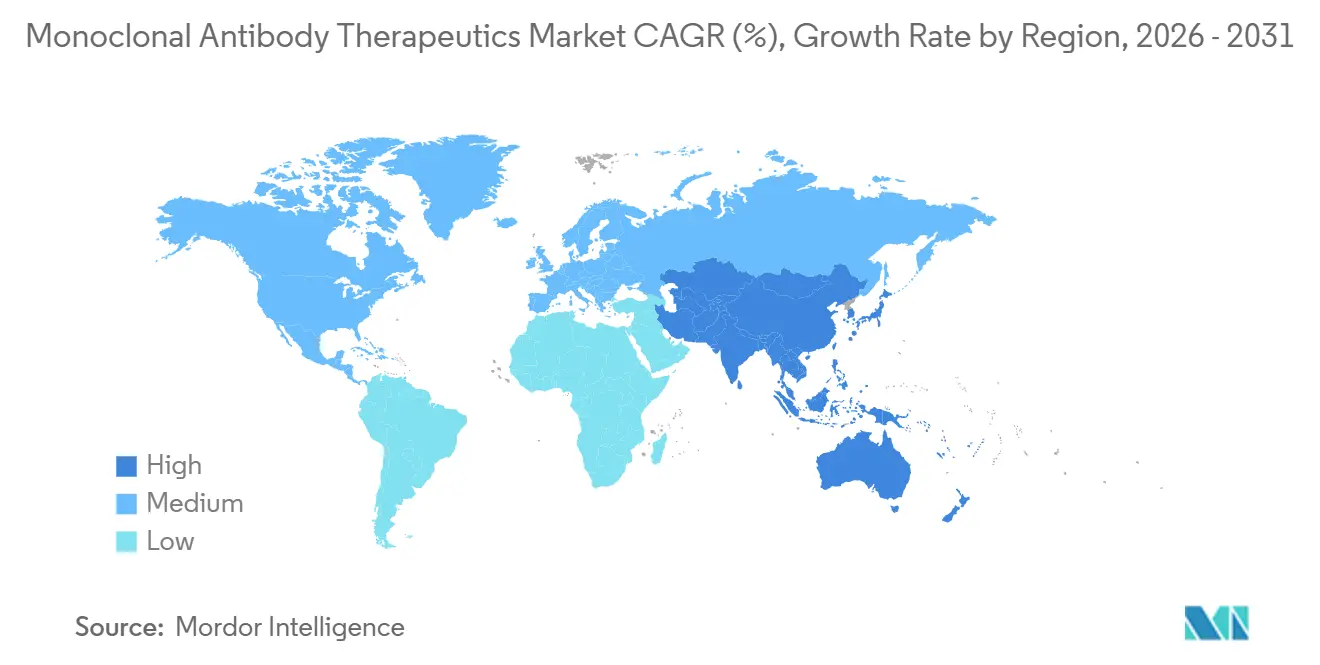

- By geography, North America captured the largest share at 42.76% in 2025, and Asia-Pacific is anticipated to deliver the fastest 14.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Monoclonal Antibody Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Disease Burden of Cancer and Autoimmune Disorders | +2.8% | Global, with peak incidence in North America and Europe | Long term (≥ 4 years) |

| Expanding Geriatric Population Base | +2.1% | Global, concentrated in Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Accelerated Regulatory Approval Pathways for Biologics | +2.3% | North America, Europe, APAC (China, Japan) | Medium term (2-4 years) |

| Increasing Preference for Targeted Therapies Over Small Molecules | +2.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Advancements in Antibody Engineering and Delivery Technologies | +2.0% | Global, R&D concentrated in North America, Europe, China | Medium term (2-4 years) |

| Growing Biologics Manufacturing Capacity in Emerging Markets | +1.8% | APAC core (China, India, South Korea), spill-over to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Disease Burden of Cancer and Autoimmune Disorders

Cancer incidence grew to 20 million new cases in 2024, and autoimmune diagnoses now top 80 million worldwide. Eight novel oncology antibodies cleared the U.S. market in 2025, cementing multi-step sequencing that extends survival but raises per-patient costs. Standard regimens now rely on PD-1, PD-L1, and TNF-alpha blockade that outranks historical chemotherapy in efficacy and tolerability. Autoimmune care follows a similar arc as IL-23 inhibitors, with eight-week dosing to lift adherence among chronic patients. Given this macro backdrop, the monoclonal antibody therapeutics market continues to scale through volume expansion, even before price effects are factored in.

Expanding Geriatric Population Base

Individuals aged 65 and above will represent 22% of global citizens by 2030[1]United Nations, “World Population Prospects 2025,” un.org. Older cohorts carry a higher prevalence of cancers, immune disorders, and age-related ophthalmic conditions that rely on biologic modulation. Medicare spending on infused antibodies reached USD 48 billion in 2025, despite emerging price controls, showing double-digit growth. Convenience remains paramount; subcutaneous versions of legacy infusions achieved 35% penetration among osteoporosis patients aged 70+ within 18 months. The demographic swell safeguards demand for the monoclonal antibody therapeutics market even if unit prices face negotiated reductions.

Accelerated Regulatory Approval Pathways for Biologics

Fourteen antibodies received U.S. breakthrough or accelerated tags in 2025, slashing the median review time to 6.5 months. Europe and China mirror the velocity, cutting queues to under 200 days for qualifying submissions. Sponsors gain an early-mover benefit that locks in a 60% share before rivals appear, and revenue accrues during confirmatory study windows. However, three agents lost approval when their survival data fell short, illustrating the calculated risk developers accept. Speed to shelf, therefore, remains a two-edged sword within the monoclonal antibody therapeutics market.

Increasing Preference for Targeted Therapies Over Small Molecules

A 2025 ASCO survey found that 68% of U.S. oncologists now select checkpoint inhibitors first-line for metastatic melanoma. Payers reinforce that tilt by slotting leading antibodies in preferred tiers while raising copays for older chemotherapies. Autoimmune prescribers adopt a similar hierarchy, with IL-17 and IL-23 agents displacing methotrexate in newly diagnosed patients. Once clinicians observe durable remission with biologics, therapeutic inertia favors continuation, even amid biosimilar entry that cuts prices by 40%. That clinical confidence anchors long-term volume for the monoclonal antibody therapeutics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs and Reimbursement Challenges | -1.9% | Global, acute in Europe and emerging markets with constrained budgets | Medium term (2-4 years) |

| Complex Manufacturing and Supply Chain Requirements | -1.2% | Global, bottlenecks in North America and Europe | Short term (≤ 2 years) |

| Safety Concerns and Adverse Event Profiles | -0.8% | Global, heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Intensifying Biosimilar Competition Post-Patent Expiries | -1.5% | North America, Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Reimbursement Challenges

Wholesale prices run from USD 80,000 to USD 250,000 per course, and Germany cut oncology antibody reference prices by 22% in 2025[2]Gemeinsamer Bundesausschuss, “Benefit Assessment Decisions Q4 2025,” g-ba.de. The U.S. Inflation Reduction Act placed three antibodies into negotiation for 2026 rebates that can slice 40% off list, trimming manufacturer yield. Emerging economies apply even harsher caps which dilute multinational revenue but boost local access. To safeguard gross margin, firms lean on value-based contracts that refund payers if endpoints falter. Successful real-world datasets become crucial evidence as stakeholders scrutinize budget impact.

Complex Manufacturing and Supply Chain Requirements

Campaigns last up to 21 days, and contamination at any step forces multi-month shutdowns, as seen with a Swiss facility outage in 2025. Three suppliers control most media inputs, allowing an 18% price rise that added USD 25,000 per kilogram to the cost of goods. Cold-chain mishaps spoiled USD 12 million of finished inventory after a mid-2025 logistics outage. Regulatory bodies issued 38% more citations in 2025, underscoring that cGMP compliance is not optional. These realities limit immediate scale and drive cost inflation in the monoclonal antibody therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Infectious Diseases Outpace Oncology Growth

Oncology accounted for 46.43% of 2025 revenue, yet infectious diseases are forecast to have the fastest 15.76% CAGR, driven by state stockpiles and pandemic insurance programs. The monoclonal antibody therapeutics market size for infectious applications is slated to swell as BARDA awards exceed USD 1.2 billion for pre-purchase of respiratory virus countermeasures. Government procurement secures volumes independent of insurer dynamics, giving newcomers a dependable launchpad.

Oncology still grows due to widening eligibility of checkpoint inhibition, but saturation in mature tumors tempers the pace. Autoimmune conditions add stable repeat dosing, while ophthalmology slows as extended-interval injectables limit vial turns. Neurology remains small today, yet gains mindshare with disease-modifying success in Alzheimer’s. Each subfield illustrates the broadening canvas that propels the monoclonal antibody therapeutics market.

By Source: Bispecific Formats Redefine Treatment Paradigms

Humanized antibodies delivered 49.54% of 2025 sales and stay prominent due to low immunogenicity and known processes. Still, bispecific constructs, though only 8% today, book a rapid 15.89% CAGR. Their dual-target action bypasses resistance, and early launches already seize share in refractory hematologic lines. The monoclonal antibody therapeutics market share for bispecifics is set to widen as 62% of Phase I entrants now carry multi-specific geometry.

Chimeric products lose steam under biosimilar assault, while fully human antibodies defend blockbuster franchises like pembrolizumab. Murine assets fall to niche imaging use where single-dose exposure sidesteps immune buildup. The shift forces manufacturing innovation, since only fifteen global sites can assemble heterodimers at scale, giving incumbents a supply advantage.

By Production Platform: Transgenic Systems Gain Traction

Mammalian cell culture remained the workhorse at 32.65% of 2025 output, prized for authentic glycosylation. Transgenic animals and plants will, however, post 15.32% CAGR because they cut capex and align with low-income disease targets. The monoclonal antibody therapeutics market size generated by these platforms increases as regulatory agencies approve plant-derived products that meet current quality guidance.

Microbial and cell-free systems cater to fragments lacking glycans and serve exploratory pipelines that need rapid milligram lots. Continuous bioprocess pilots show 70% footprint savings and hint at decentralized manufacturing near demand loci. Together, platform pluralism diversifies risk and expands supply flexibility for the monoclonal antibody therapeutics market.

By End User: Home-Care Channels Reshape Delivery Models

Hospitals still absorb 62.65% of 2025 spending because many agents need crash-cart support during the first infusions. Home self-injection channels, though currently at only 9%, will expand at a 16.43% CAGR. Payers reward migration away from inpatient care, and subcutaneous launches feature patient-friendly applicators vetted through human factors guidance. The monoclonal antibody therapeutics market size is driven by home care, as specialty pharmacies coordinate cold-chain drops directly to users.

Specialty clinics bridge the hospital and home through initial monitoring, while academic hubs consume investigational supply. Digital adherence tools track dose timing and feeding, and trigger value-based payment refunds for unmet outcomes. These dynamics align all stakeholders toward decentralized delivery.

Geography Analysis

North America commanded 42.76% of 2025 revenue, benefiting from Medicare co-insurance coverage and a dense trial network. Yet the Inflation Reduction Act introduces managed pricing from 2026, tightening net yields though not likely dampening volume. Canada negotiated 18% to 25% cuts that widened provincial access, and Mexico listed six oncology antibodies on its public formulary, albeit with lower per-capita utilization.

Asia-Pacific is the standout growth engine at 14.65% CAGR. China approved eleven novel antibodies in 2025 and pooled them into the national reimbursement list that covers 1.3 billion residents. India’s low-cost CDMO build-out combines with export-friendly regulation, letting local firms capture value from biosimilar orders across emerging regions. South Korea’s capacity surge rounds out a regional manufacturing corridor that underpins the monoclonal antibody therapeutics market.

Europe accounted for 28% of 2025 turnover. Health technology assessments in Germany, France, and the UK force manufacturers to meet strict cost-effectiveness thresholds, prompting 22% average price cuts on select oncology agents. Automatic substitution rules fast-track biosimilar share near 50% within a year of launch. Despite these headwinds, Western Europe remains central for early launches that cascade to global uptake once national payers conclude negotiations.

Competitive Landscape

Top players Roche, AbbVie, Merck, Bristol Myers Squibb, and Johnson & Johnson together held 52% of global revenue in 2025. Their lead stems from proven franchises, but it is narrowing as regional innovators capture domestic share at lower list prices. Incumbents invest heavily in bispecific T-cell engagers and antibody-drug conjugates that offer fresh exclusivity and defend brand equity even after core patents expire.

Strategy now blends vertical supply acquisition with digital discovery engines that compress design cycles. Roche committed USD 2.8 billion to new bioreactors in California to shore up captive capacity and trim external fees. Samsung Bioepis and other biosimilar specialists accelerate erosion of incumbents’ margins, yet the monoclonal antibody therapeutics market overall expands as biosimilars democratize access and grow the total treated population.

Regulatory quality remains a moat. Eleven FDA warning letters in 2025 illustrate how lapses can derail output for months. Companies with strong data-integrity cultures maintain customer trust and keep pharmacy shelves stocked reliably. Competitive footing, therefore, rests on both scientific novelty and unbroken compliance discipline.

Monoclonal Antibody Therapeutics Industry Leaders

Daiichi Sankyo Company Limited

Johnson & Johnson

Abbvie Inc

Amgen Inc

UCB S.A., Belgium (UCB Inc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: F. Hoffmann-La Roche Ltd announced that its phase III MAJESTY study showed positive results for Gazyva/Gazyvaro (obinutuzumab), a monoclonal antibody, in treating adults with primary membranous nephropathy. The study met its primary endpoint, demonstrating significant and meaningful clinical benefits.

- September 2025: KBI Biopharma, Inc. (KBI), a JSR Life Sciences company and cGMP contract development and manufacturing organization (CDMO), and Infinimmune, Inc., a biotechnology company pioneering human-first antibody discovery and design collaborated to advance manufacturing of Infinimmune’s lead human monoclonal antibody (“IFX-101”) program.

- August 2025: Eisai Co., Ltd. and Biogen, Inc. launched the anti-amyloid beta monoclonal antibody LEQEMBI in Austria and Germany, following EU approval in April 2025 for the treatment of early Alzheimer's disease. This marks the first therapy targeting the underlying cause of AD in the EU.

Global Monoclonal Antibody Therapeutics Market Report Scope

As per the scope of the report, monoclonal antibodies are antibodies that are made by identical immune cells that are all clones of a unique parent cell originating from various sources.

The Monoclonal Antibody Therapeutics Market is Segmented by Application (Oncology, Autoimmune Diseases, Hematological Diseases, Infectious Diseases, Ophthalmology, Neurology, and Other Applications), Source (Human, Humanized, Chimeric, Murine, and Bispecific/Multispecific), Production Platform (Mammalian Cell Culture, Microbial Expression, Transgenic Animals & Plants, and Cell-Free/Continuous Manufacturing), End-User (Hospitals, Specialty Clinics, Home-Care/Self-Administration, and Research & Academic Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Oncology |

| Autoimmune Diseases |

| Hematological Diseases |

| Infectious Diseases |

| Ophthalmology |

| Neurology |

| Other Applications |

| Human |

| Humanized |

| Chimeric |

| Murine |

| Bispecific / Multispecific |

| Mammalian Cell Culture (CHO, NS0, HEK-293) |

| Microbial Expression (E. Coli, Yeast) |

| Transgenic Animals & Plants |

| Cell-Free / Continuous Manufacturing |

| Hospitals |

| Specialty Clinics |

| Home-Care / Self-Administration |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Oncology | |

| Autoimmune Diseases | ||

| Hematological Diseases | ||

| Infectious Diseases | ||

| Ophthalmology | ||

| Neurology | ||

| Other Applications | ||

| By Source | Human | |

| Humanized | ||

| Chimeric | ||

| Murine | ||

| Bispecific / Multispecific | ||

| By Production Platform | Mammalian Cell Culture (CHO, NS0, HEK-293) | |

| Microbial Expression (E. Coli, Yeast) | ||

| Transgenic Animals & Plants | ||

| Cell-Free / Continuous Manufacturing | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Home-Care / Self-Administration | ||

| Research & Academic Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 revenue forecast for the monoclonal antibody therapeutics market?

The market is expected to reach USD 619.4 billion by 2031, reflecting a CAGR of 13.7% from 2026.

Which therapeutic area is expected to grow fastest within monoclonal antibodies?

Infectious diseases are projected to expand at a 15.76% CAGR-driven by government stockpiling and emerging pathogen threats.

How will home administration affect spending on monoclonal antibodies?

Subcutaneous and autoinjector formats that support home care are growing at 16.43% CAGR, shifting costs away from hospitals and expanding patient access.

Which region will deliver the highest growth rate through 2031?

Asia-Pacific is set to advance at 14.65% CAGR as China, India, and South Korea build capacity and widen reimbursement.

What competitive strategies are innovators using to offset biosimilar erosion?

Companies invest in antibody-drug conjugates, bispecific T-cell engagers, and vertical manufacturing integration to sustain pricing power and ensure reliable supply.

How concentrated is the supplier base for critical raw materials?

Three vendors control roughly 72% of cell-culture media, contributing to cost inflation and supply vulnerability for biologic manufacturers.

Page last updated on: