Alginate Dressing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.07 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

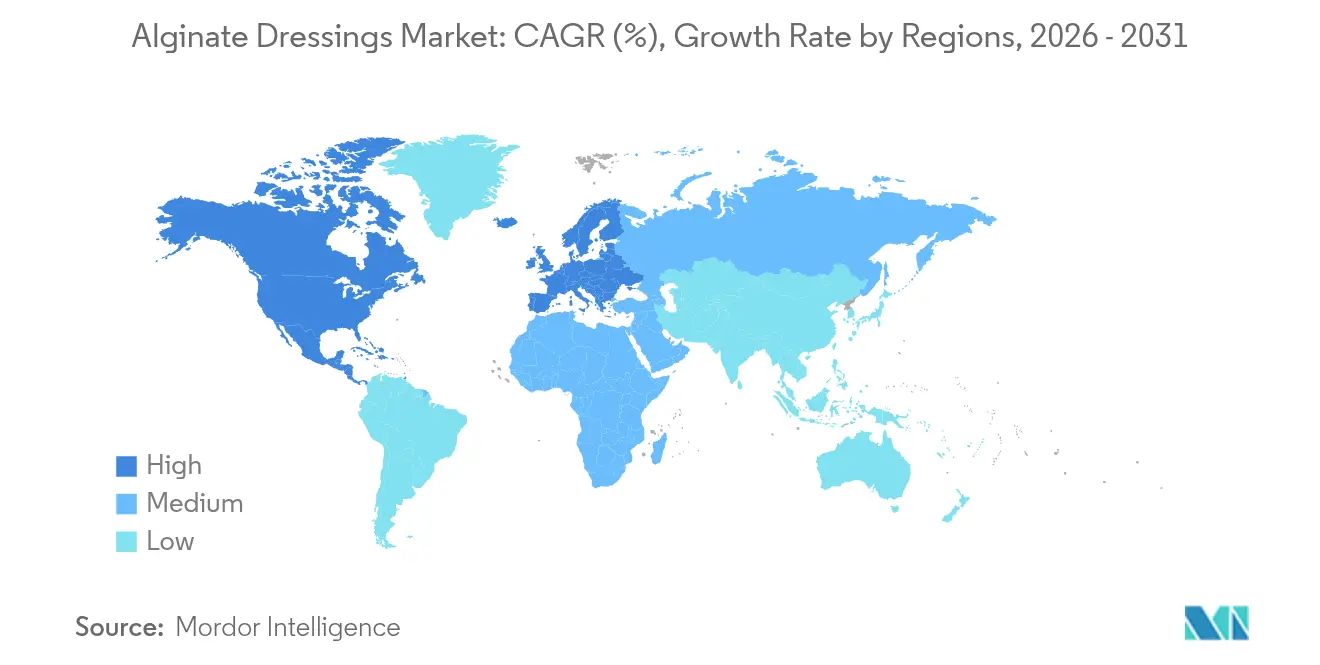

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

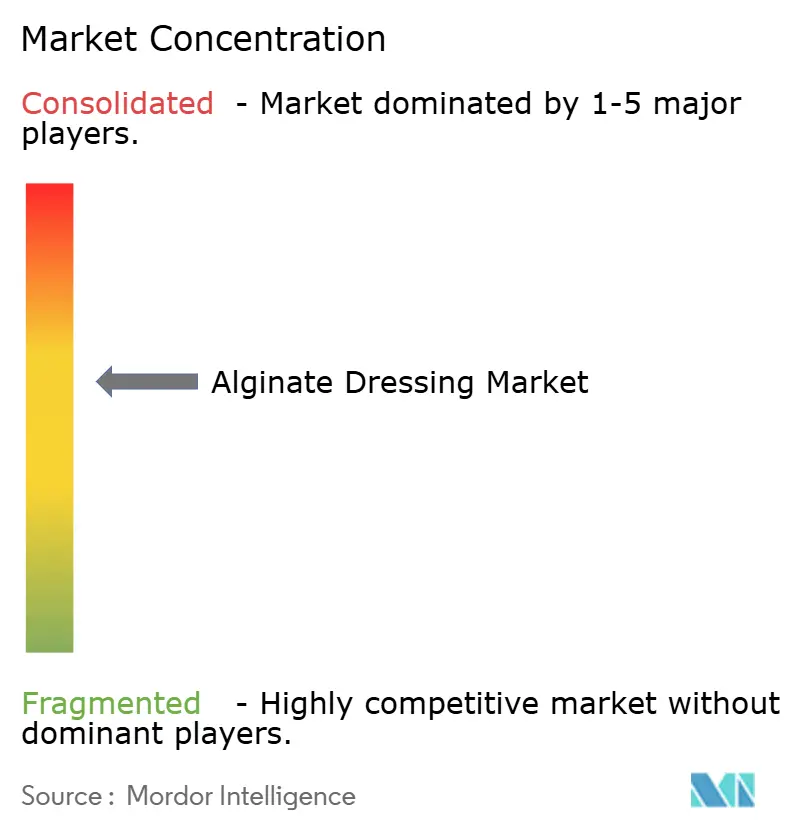

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alginate Dressing Market Analysis by Mordor Intelligence

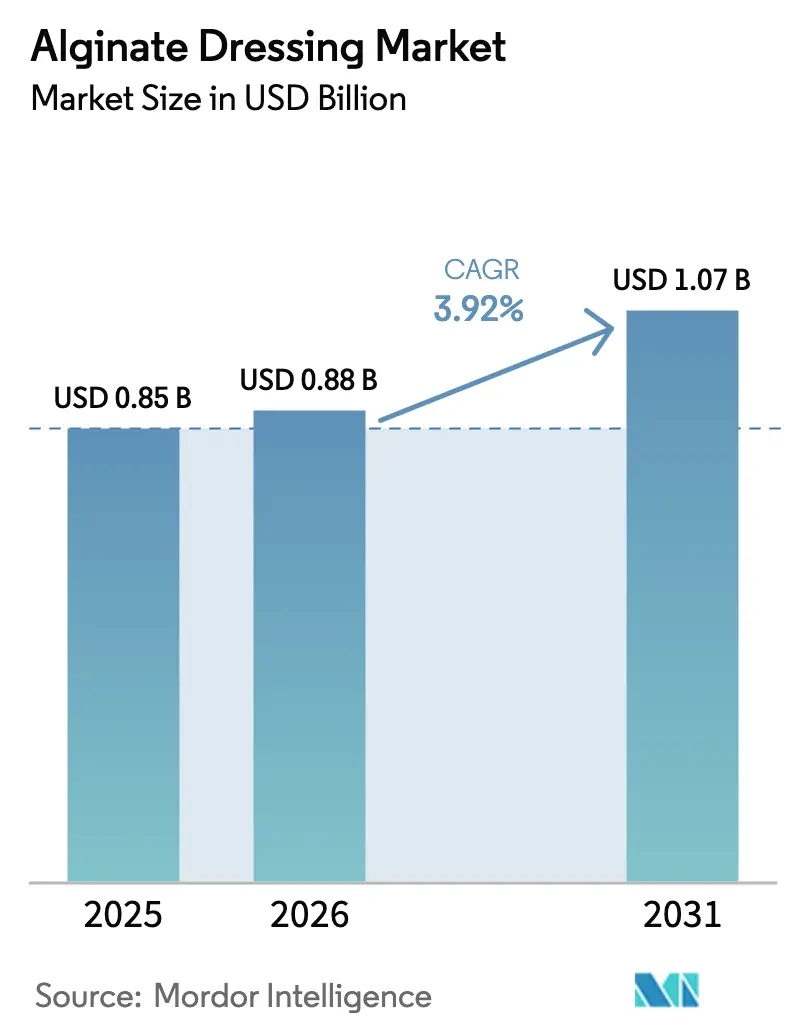

The alginate dressings market size in 2026 is estimated at USD 0.88 billion, growing from 2025 value of USD 0.85 billion with 2031 projections showing USD 1.07 billion, growing at 3.92% CAGR over 2026-2031. Consistent growth rests on three structural pillars: rising chronic-wound incidence, accelerating surgical volumes in outpatient settings, and a rapidly aging global population that requires long-term wound management. The alginate dressings market benefits from the material’s intrinsic capacity to absorb heavy exudate, minimize dressing-change frequency, and remove atraumatically, all of which lower total treatment costs and reduce infection risk. Demand also receives a lift from technological upgrades—such as nanoparticle integration and dual-stage growth-factor release—that convert a once-passive dressing into an active therapeutic platform. E-commerce broadens patient access, while government-backed seaweed aquaculture projects smooth raw-material supply, stabilizing prices and ensuring uninterrupted production.

Key Report Takeaways

- By geography, North America commanded 42.18% of global revenue in 2025, while Asia-Pacific is projected to register a 5.18% CAGR through 2031.

- By application, chronic wounds held 66.55% of the alginate dressings market share in 2025; acute wounds are expected to expand at a 4.74% CAGR to 2031.

- By distribution channel, retail and e-commerce secured 69.62% of revenue in 2025, whereas direct tenders are set to rise at a 4.49% CAGR through 2031.

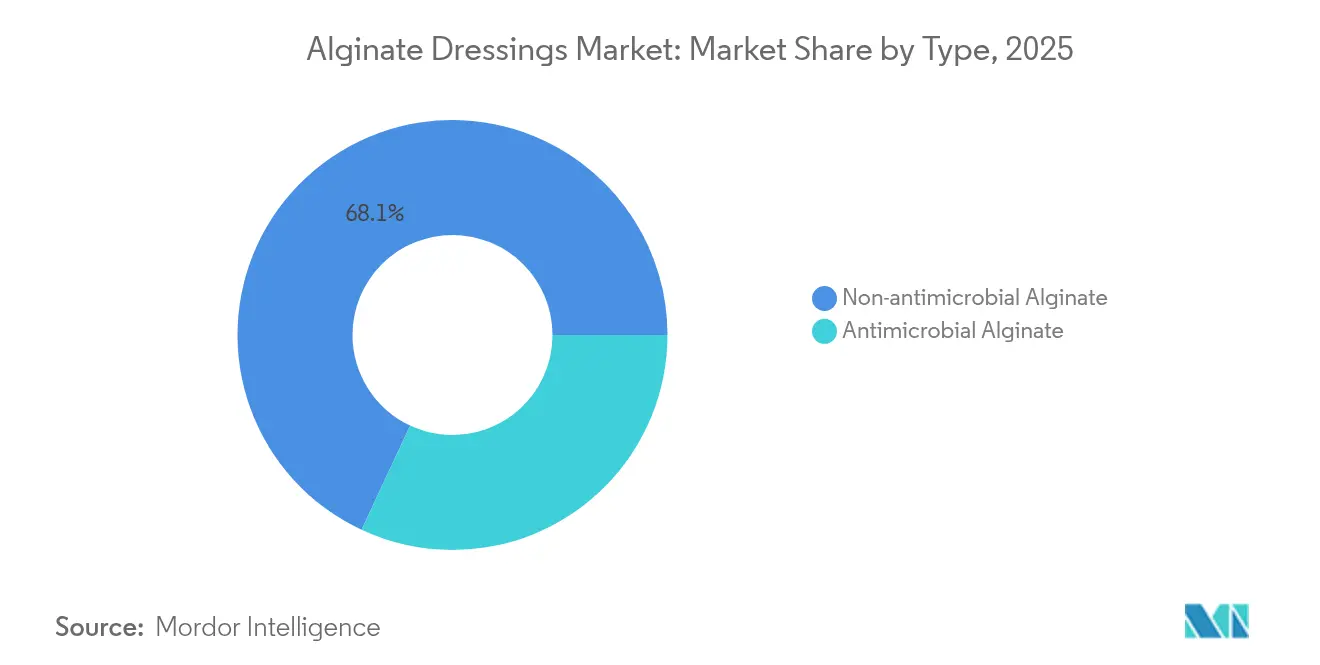

- By type, non-antimicrobial variants retained 68.05% share in 2025; antimicrobial formats are forecast to climb at a 5.01% CAGR to 2031.

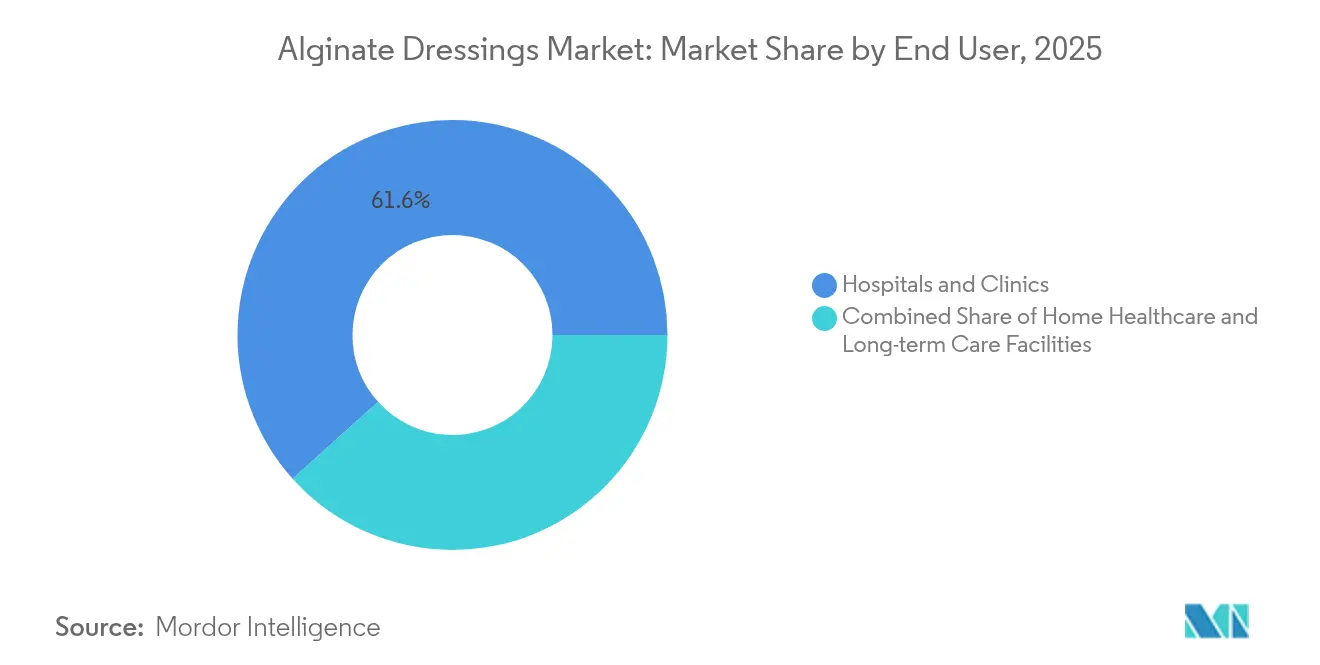

- By end-use, hospitals and clinics accounted for 61.65% of the alginate dressings market size in 2025, yet home healthcare is poised for a 4.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alginate Dressing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging prevalence of chronic wounds & diabetic ulcers | +1.2% | Global; concentrated in North America & Europe | Long term (≥ 4 years) |

| Rising surgical volumes in ambulatory settings | +0.8% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Rapidly expanding geriatric population | +1.0% | Global; acute in developed markets | Long term (≥ 4 years) |

| Breakthrough two-stage alginate dressings with growth factors & nanoparticles | +0.6% | North America & EU early adoption; APAC following | Medium term (2-4 years) |

| Government-backed seaweed aquaculture initiatives in coastal nations | +0.4% | APAC core; spill-over globally | Long term (≥ 4 years) |

| Heightened adoption of antimicrobial alginate variants | +0.7% | Global; led by North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Prevalence of Chronic Wounds & Diabetic Ulcers

Chronic wounds affect 6.7 million U.S. residents, generating USD 50 billion in annual care costs. Diabetic foot ulcers strike up to 25% of diabetic patients and drive 85% of diabetes-related amputations, with neuropathy implicated in 90% of cases. These wounds stagnate because macrophage-mediated inflammation disrupts normal healing. Clinical data show 88% of older adults present with multiple morbidities, amplifying wound complexity. Specialized centers therefore standardize high-absorbency alginate dressings that encourage autolytic debridement and reduce nursing visits. In southern Barcelona, chronic-wound care cost EUR 34.99 million (USD 39.55 million) over three years, implying EUR 1.76 billion (USD 1.99 billion) nationwide, a burden that intensifies pressure to adopt cost-effective advanced dressings.

Rising Surgical Volumes in Ambulatory Settings

Ambulatory surgery centers handled 3.3 million Medicare procedures in 2022, underlining a structural shift away from hospitals [1]Mark Mellott, “Medicare Beneficiaries in ASCs,” MedPAC, medpac.gov. CMS reimbursement schedules now reward outpatient migration, and orthopedic operations such as joint replacements increasingly leverage anesthesia protocols that support same-day discharge. Patients recuperate at home, so surgeons prefer alginate dressings for extended wear and easy self-application. Lower facility overheads and reduced readmission risks together reinforce the alginate dressings market trajectory.

Rapidly Expanding Geriatric Population

One fifth of U.S. citizens will be older than 65 by 2030. Long-term-care facilities now score 162.15 on standardized acuity scales, reflecting elevated nursing loads in physiological and safety domains. Atraumatic alginate dressings protect fragile skin, lessen pain, and lower staff workload, sustaining demand across institutional and home-care environments.

Breakthrough Two-Stage Alginate Dressings with Growth Factors & Nanoparticles

Two-stage matrices marry infection control with targeted regeneration. Silver nanoparticle–alginate composites achieved complete re-epithelialization in preclinical models within seven days, displaying minimal inflammation. Formulations containing fibroblast growth factor-2 or cefepime extend the concept, releasing bioactives sequentially for optimized healing. Zinc-oxide nanoparticle variants control Pseudomonas aeruginosa and Staphylococcus aureus without silver’s discoloration risk. Such innovations push the alginate dressings market toward premium, technology-led value propositions.

Government-Backed Seaweed Aquaculture Initiatives in Coastal Nations

India’s Pradhan Mantri Matsya Sampada Yojana and parallel programs in China support large-scale seaweed farming that secures brown-algae supply and boosts coastal employment. USDA research highlights environmental and revenue benefits of domestic kelp cultivation. Steadier raw-material pipelines reduce cost spikes that once limited expansion, fortifying profit margins and delivery reliability across the alginate dressings market.

Heightened Adoption of Antimicrobial Alginate Variants

Healthcare systems penalize hospital-acquired infections, prompting wider use of silver-embedded alginate pads that release ions for up to seven days. FDA draft guidance now specifies streamlined pathways for antimicrobial dressings, lowering regulatory risk. Early evidence shows antimicrobial formats cut surgical-site infection rates, justifying their higher unit price and accelerating market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement in emerging economies | -0.4% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| High product cost vs. traditional dressings | -0.3% | Global; acute in price-sensitive markets | Medium term (2-4 years) |

| Volatility in brown-seaweed raw-material pricing | -0.2% | Global; supply-chain-dependent regions | Short term (≤ 2 years) |

| Price pressure from synthetic super-absorbent polymer dressings | -0.3% | Global; cost-conscious segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement in Emerging Economies

Public insurers in low- and middle-income countries focus spending on communicable diseases and maternal health, frequently excluding advanced wound therapies. Fragmented hospital networks hinder chronic-wound program rollouts, as noted by World Bank assessments. Patients must self-fund alginate dressings, which can cost more than a month’s income in rural areas, curbing market access despite rising need.

High Product Cost vs. Traditional Dressings

Unit prices for alginate pads still exceed gauze and entry-level hydrocolloids—even if total-episode savings favor alginate—leading procurement teams to favor cheaper options in budget-constrained systems. Clinicians face limited economic-evaluation data, slowing formulary approvals and restraining the alginate dressings market in regions without value-based purchasing mandates.

Volatility in Brown-Seaweed Raw-Material Pricing

Climate-driven storm events and currency swings disrupt Indonesian and Philippine seaweed harvests, causing price spikes that squeeze manufacturers’ margins. Although aquaculture projects improve resilience, near-term variability still complicates production planning and end-user pricing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Antimicrobial Adoption Reshapes Portfolio Mix

Non-antimicrobial variants held 68.05% of revenue in 2025, reflecting broad clinical familiarity and lower unit cost. Antimicrobial formats, however, are set for a 5.01% CAGR, outpacing the alginate dressings market. Hospital quality programs now bundle silver alginate pads with orthopedic and cardiovascular kits to reduce readmission penalties. Regulatory clarity encourages R&D investment in zinc-oxide nanoparticle alternatives, widening product choice and fostering healthy competition.

Robust outcomes data support antimicrobial superiority against multidrug-resistant organisms, allowing suppliers to defend premium pricing. The alginate dressings market size for antimicrobial options is projected to account for a growing share of overall revenue, especially in tertiary hospitals and diabetic-foot specialty clinics.

By Application: Chronic Wounds Anchor Demand, Acute Wounds Accelerate

Chronic wounds represented 66.55% of the alginate dressings market share in 2025, thanks to their complexity and prolonged healing timelines. Diabetic foot ulcers dominate this pool, followed by pressure and venous leg ulcers. Alginate’s high absorption and easy removal remain decisive advantages. The alginate dressings market size allocated to chronic-wound care will stay large, yet growth moderates as protocols mature.

Acute wounds—including surgical incisions and trauma—are advancing at a 4.74% CAGR, helped by outpatient procedure growth. Alginate pads are valued for rapid hemostasis and moist-healing maintenance during early tissue formation. Burns provide a niche that leverages alginate’s analgesic and non-adherent properties, particularly in pediatrics.

By End-Use: Home Healthcare Fuels the Next Growth Wave

Hospitals and clinics secured 61.65% of revenue in 2025 through centralized purchasing and complex case management. Value-based reimbursement is, however, shifting chronic-wound care into homes, where alginate dressings cut nurse visits and improve quality of life. The home-healthcare segment, growing at a 4.89% CAGR, relies on online pharmacies and subscription kits that automate replenishment.

Long-term-care facilities remain steady consumers, driven by pressure-ulcer prevention mandates. Integration of sensor-enabled alginate pads that transmit exudate data to care teams promises to raise compliance and reduce litigation risk, further entrenching the alginate dressings market in elder-care settings.

By Distribution Channel: E-Commerce Democratizes Access

Retail and e-commerce dominated with 69.62% share in 2025 as patients embrace direct-purchase convenience. Detailed product pages, comparison tools, and recurring delivery services empower users to maintain continuity of care without hospital visits. The alginate dressings market benefits from this consumerization trend, which lowers barriers for niche brands and boosts overall unit volumes.

Direct-tender channels are projected to expand at a 4.49% CAGR, reflecting health-system consolidation. Group-purchasing organizations negotiate multi-year contracts that package alginate dressings with complementary wound-care supplies. Suppliers willing to provide data on healing outcomes win preferred-supplier status, securing predictable volume flows.

Geography Analysis

North America remains the largest regional contributor, holding 42.18% of 2025 revenue. Robust insurance coverage, well-established wound-care clinics, and strong clinical-evidence requirements sustain high utilization. U.S. registry data have shown infection-rate reductions when alginate pads are deployed early in diabetic-ulcer treatment, reinforcing formulary placement.

Europe records steady adoption, supported by centralized health technology assessments that favor cost-effective solutions with proven patient-reported outcomes. MDR implementation has elevated safety standards, benefiting manufacturers with rigorous quality systems. National procurement agencies in Germany and the United Kingdom increasingly include antimicrobial alginate dressings in framework agreements that standardize care pathways across acute and community settings.

Asia-Pacific is the fastest-growing region, projected at a 5.18% CAGR through 2031. Rising diabetes prevalence and rapid hospital construction create fertile ground for advanced dressings. Government marine-economy policies in China and India ensure raw-material security and nurture local manufacturers that export competitively priced alginate pads. Japan’s universal health-insurance system recently approved higher reimbursement ceilings for advanced wound dressings used in home care, an incentive that will widen consumer adoption.

Latin America and the Middle East & Africa experience slower uptake due to reimbursement gaps and fragmented supply chains. Pilot programs run by nongovernmental agencies demonstrate clinical gains but require sustainable funding models to scale. International aid projects that supply alginate dressings during disaster relief often seed awareness among local clinicians, laying groundwork for future commercial demand once economic conditions improve.

Competitive Landscape

The alginate dressings market shows moderate concentration. Smith+Nephew, 3M, ConvaTec, and Coloplast collectively hold about 60% of global revenue, bolstered by extensive distribution networks and long clinical track records. These companies prioritize continuous improvements—adding growth factors, antimicrobial agents, or sensor layers—to defend share without triggering race-to-the-bottom pricing.

Winner Medical, having secured FDA clearance for its silver alginate line in 2022, is expanding through U.S. retail pharmacies and e-commerce marketplaces [2]U.S. Food and Drug Administration, “510(k) Summary for Silver Alginate Dressing,” fda.gov. Axio Biosolutions focuses on hemostatic alginate sponges for battlefield and emergency medicine, carving a profitable niche. Regional firms in China leverage vertical integration from seaweed farming to finished dressings, giving them cost advantages that support aggressive export campaigns.

Technology convergence is reshaping the battlefield. FDA’s reclassification of devices that detect wound-fluid protease activity as Class II lowers entry barriers for diagnostic-dressing hybrids [3]Federal Register, “Special Controls for Wound-Protease Detectors,” federalregister.gov . Partnerships between dressing makers and telehealth platforms now bundle consumables with remote-monitoring apps, reinforcing brand loyalty and creating data streams that justify premium pricing and risk-sharing contracts with payers.

Alginate Dressing Industry Leaders

Cardinal Health

Smith and Nephew

3M

Coloplast Corp.

ConvaTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Smith+Nephew announced a pilot program with a U.S. telehealth provider to bundle its sensor-enabled alginate dressings with virtual wound-care visits.

- May 2024: Winner Medical Co. Ltd attracted strong interest for its Advanced Wound Dressing Experiment Interaction at EWMA 2024 in London.

- February 2022: Winner Medical’s silver alginate dressing received FDA 510(k) clearance, enabling direct entry into the United States market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the alginate dressing market as all sterile wound dressings manufactured from calcium or sodium alginate fibers that turn into a hydrophilic gel on contact with exudate, and that are supplied in pads, ropes, or ribbons for moderate-to-heavy drainage wounds.

Scope exclusion: We exclude non-alginate advanced dressings such as foams, films, hydrocolloids, and purely silver-impregnated textiles.

Segmentation Overview

- By Type

- Antimicrobial Alginate

- Non-antimicrobial Alginate

- By Application

- Acute Wounds

- Surgical & Traumatic Wounds

- Burns

- Chronic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Other Chronic Wounds

- Acute Wounds

- By End-use

- Hospitals and Clinics

- Home Healthcare

- Long-term Care Facilities

- By Distribution Channel

- Direct Tenders / Group Purchasing

- Retail & E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed wound-care nurses, diabetic-foot specialists, hospital purchasing heads, and regional distributors across North America, Europe, Asia-Pacific, and the Gulf. Discussions clarified average dressing change frequency, channel mark-ups, and the adoption pace of antimicrobial variants, enabling us to reconcile secondary indicators with frontline realities.

Desk Research

We began with open datasets that establish the size of the chronic-wound pool and surgical volumes, such as WHO Global Health Estimates, the International Diabetes Federation Atlas, Eurostat procedure statistics, and the U.S. Agency for Healthcare Research and Quality hospital discharge files. Trade and raw-material flows for seaweed-derived alginate were gathered from UN Comtrade and the China Seaweed Industry Association, while price movements were traced through company 10-Ks and U.S. FDA 510(k) filings that disclose product classes and pack-size ASPs.

Subscription databases used by Mordor analysts, including D&B Hoovers for manufacturer revenues and Dow Jones Factiva for real-time deal news, completed the desktop picture. These sources are illustrative, not exhaustive; many additional public and paid repositories informed supplementary checks.

Market-Sizing & Forecasting

A top-down prevalence-to-usage model was built. The chronic-wound and postsurgical patient pools were multiplied by average annual dressing consumption, then valued using region-specific ASPs. Results were stress-tested against selective bottom-up roll-ups of listed suppliers' alginate revenues and distributor audits, allowing adjustments where utilization or price assumptions diverged. Key variables driving the model included diabetes prevalence, lower-limb amputation rates, ambulatory surgery volumes, geriatric population growth, antimicrobial premium spreads, and seaweed-inflation pass-through. A multivariate regression fed with these six indicators generated the 2025-2030 forecast, after experts reviewed scenario bands for reimbursement shifts and raw-material supply shocks.

Data Validation & Update Cycle

We run multi-level variance checks, gap-flag rules, and peer review before sign-off. Reports refresh annually, and we trigger mid-cycle updates when material events, such as an FDA class-wide recall, alter baseline drivers.

Why Mordor's Alginate Dressing Baseline Commands Reliability

Published figures frequently diverge because firms differ on scope, ASP conventions, and refresh cadence.

We acknowledge these gaps upfront so decision-makers can judge suitability.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.85 B (2025) | Mordor Intelligence | - |

| USD 0.98 B (2024) | Global Consultancy A | Includes hydrogel-alginate hybrids and partial double counting |

| USD 1.20 B (2023) | Industry Research House B | Relies only on supplier revenue statements; limited channel mix |

| USD 1.05 B (2025) | Regional Consultancy C | Applies single global ASP and adds veterinary wound dressings |

These contrasts show that our disciplined scope, dual-track validation, and yearly refresh give stakeholders the most balanced and transparent baseline available, strengthening confidence in every Mordor Intelligence forecast.

Key Questions Answered in the Report

How big is the Alginate Dressing Market?

The Alginate Dressing Market size is expected to reach USD 0.88 billion in 2026 and grow at a CAGR of 3.92% to reach USD 1.07 billion by 2031.

Why are antimicrobial alginate dressings growing faster than standard variants?

Hospitals aim to prevent surgical-site infections, and silver- or zinc-enhanced pads offer proven antimicrobial efficacy, supporting a 5.01% CAGR for this segment.

Who are the key players in Alginate Dressing Market?

Cardinal Health, Smith and Nephew, 3M, Coloplast Corp. and ConvaTec are the major companies operating in the Alginate Dressing Market.

Which is the fastest growing region in Alginate Dressing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Alginate Dressing Market?

In 2026, the North America accounts for the largest market share in Alginate Dressing Market.

Page last updated on: