Alopecia Treatment (Hair Loss) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 5.05 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

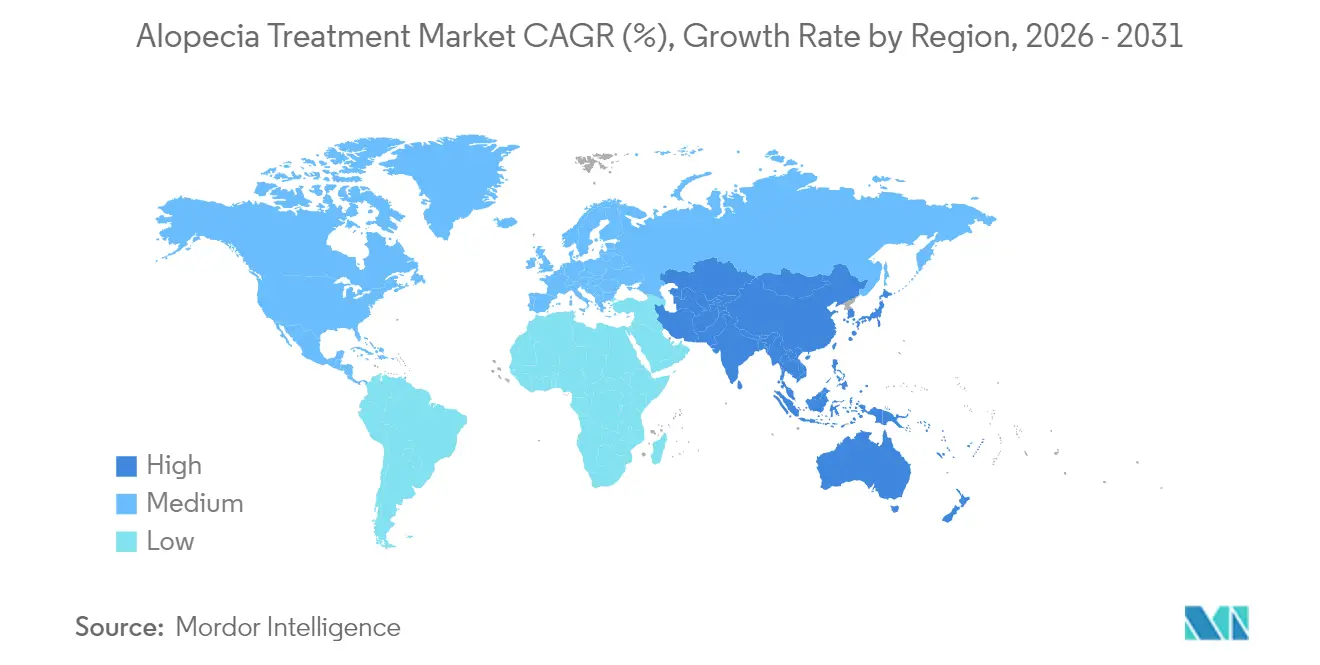

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

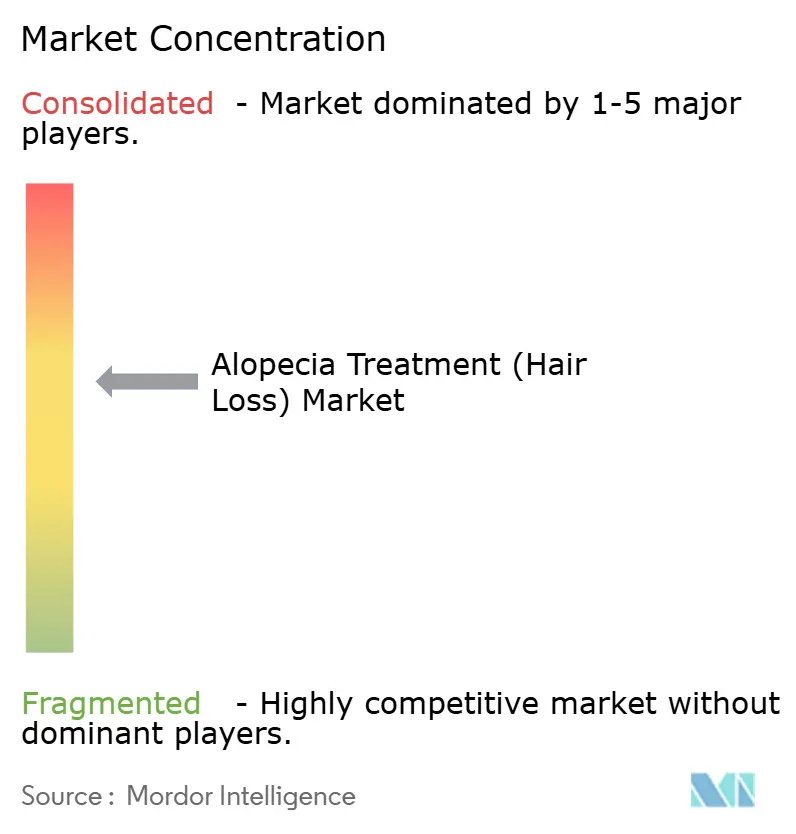

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alopecia Treatment (Hair Loss) Market Analysis by Mordor Intelligence

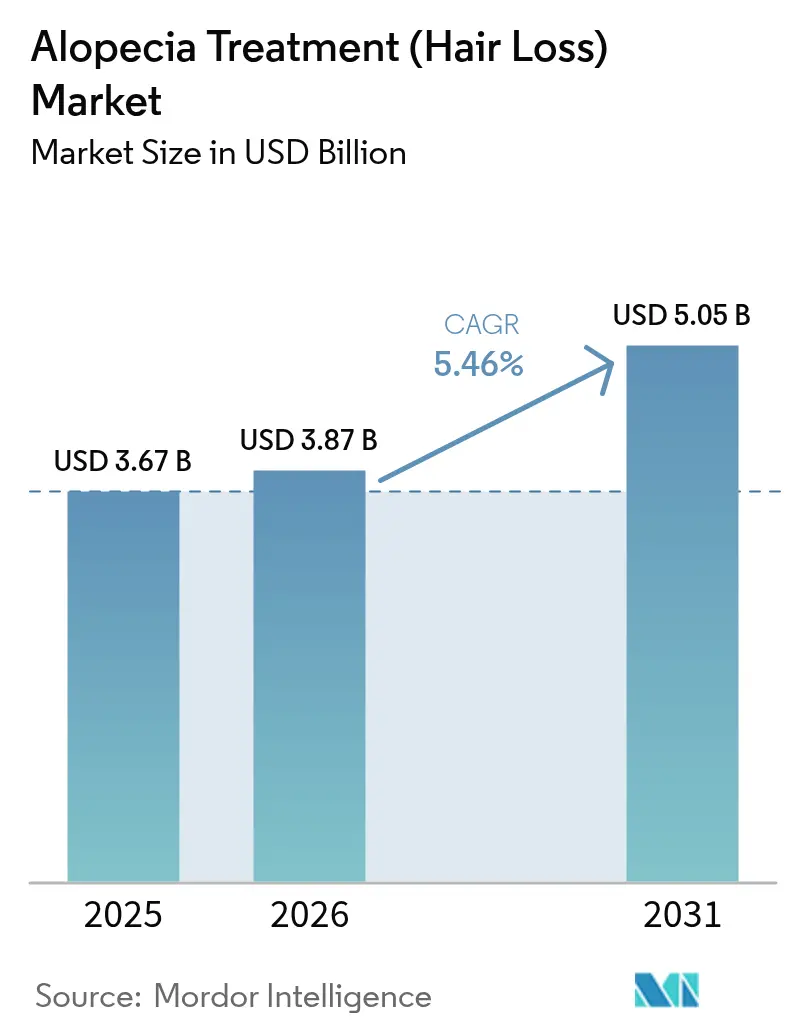

The alopecia treatment market size was valued at USD 3.67 billion in 2025 and estimated to grow from USD 3.87 billion in 2026 to reach USD 5.05 billion by 2031, at a CAGR of 5.46% during the forecast period (2026-2031). This expansion reflects growing clinical adoption of precision immunomodulation, regenerative medicine, and home-use devices that move care beyond the historic minoxidil-finasteride paradigm. Three oral JAK inhibitors now hold regulatory approval for severe alopecia areata, opening a therapeutic avenue for roughly 700,000 previously underserved U.S. patients[1]U.S. Food and Drug Administration, “FDA Approvals for Alopecia Areata Treatments,” fda.gov. Venture-backed start-ups have also introduced mitochondrial metabolism modulators and intradermal biologics that target follicular stem-cell pathways. Digital health ties these innovations together: AI-guided scalp imaging, tele-consultations, and e-pharmacy fulfillment shorten diagnostic cycles and improve adherence, particularly among younger consumers.

Key Report Takeaways

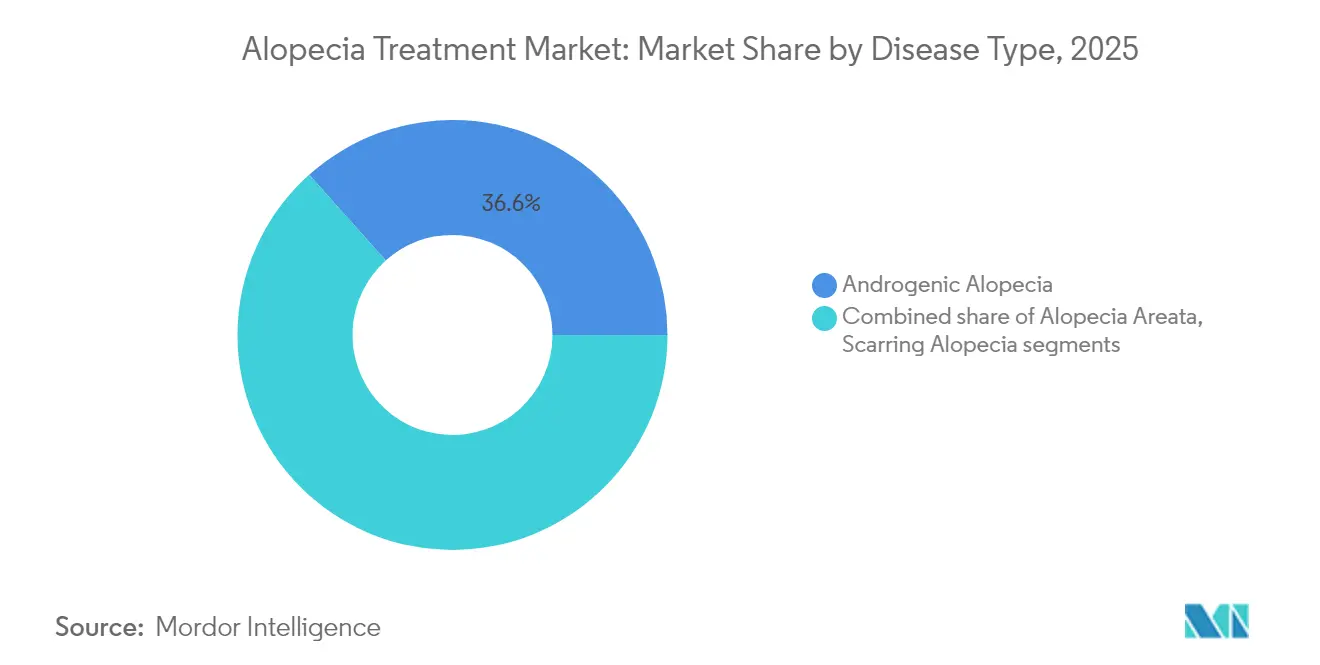

- By disease type, androgenic alopecia accounted for 36.62% of alopecia treatment market share in 2025, while alopecia totalis is projected to expand at a 7.12% CAGR through 2031.

- By gender, male patients represented 62.14% of the 2025 alopecia treatment market; the female segment is forecast to grow at 6.62% CAGR to 2031.

- By route of administration, topical products held 44.12% share of the alopecia treatment market size in 2025, whereas injectables are set to record the fastest 7.18% CAGR over the forecast horizon.

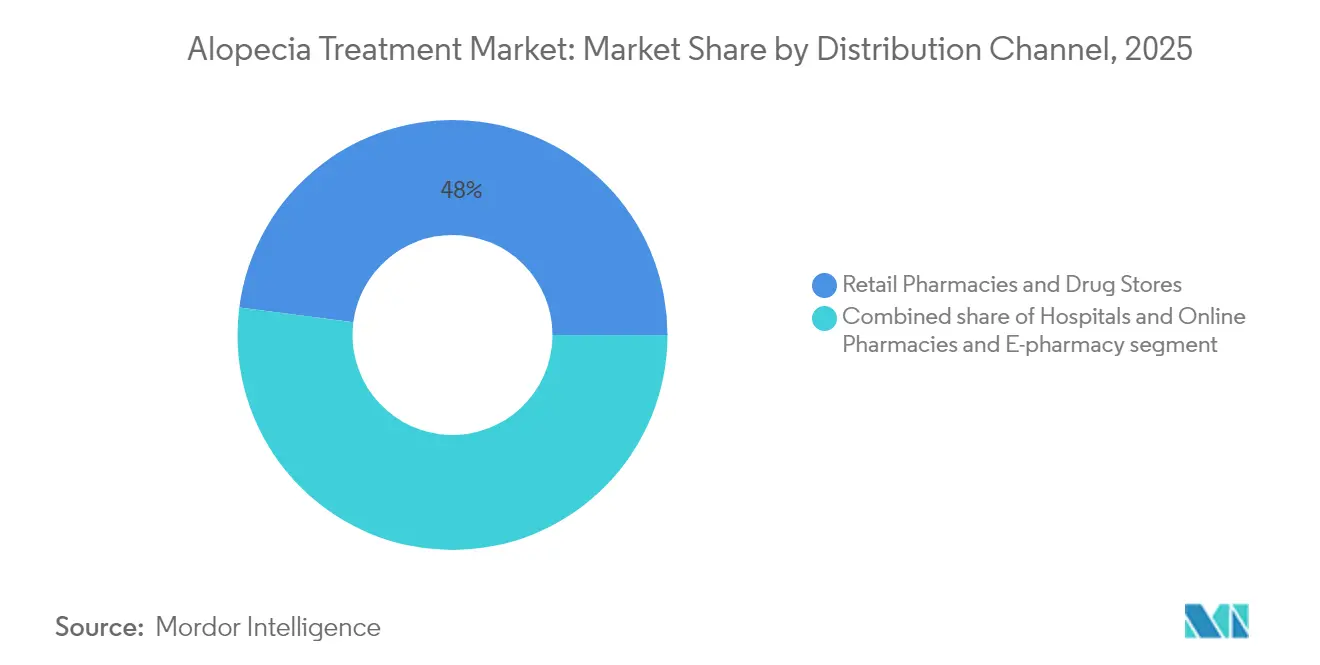

- By distribution channel, retail pharmacies led with 47.95% revenue share in 2025; online pharmacies are poised for an 7.76% CAGR to 2031.

- By end user, hospitals led with 41.21% revenue share in 2025; diagnostic laboratory are poised for an 8.05% CAGR to 2031.

- By geography, North America commanded 41.88% of 2025 revenue, but Asia-Pacific is advancing at a 6.32% CAGR on the back of China’s large patient pool and faster approvals.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alopecia Treatment (Hair Loss) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of alopecia | +1.0% | Global; highest patient growth in Asia-Pacific & North America | Long term (≥ 4 years) |

| Surge in Rx approvals of JAK-inhibitors & novel topicals | +1.2% | Global; early adoption in North America & EU | Medium term (2-4 years) |

| AI-driven personalised diagnostics & treatment planning | +0.8% | North America & Asia-Pacific core; spill-over to EU | Long term (≥ 4 years) |

| Rise of regenerative therapies (PRP, stem-cells, exosomes) | +0.7% | Global; premium uptake in developed markets | Medium term (2-4 years) |

| Rapid uptake of low-level-laser & at-home devices | +0.5% | North America & EU; expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing male grooming & tele-dermatology adoption | +0.4% | North America & Europe core; spreading to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge In Rx Approvals of JAK Inhibitors & Novel Topicals

Successive approvals of baricitinib, ritlecitinib, and deutuxolitinib have reset therapeutic expectations for autoimmune alopecia. Pivotal trials showed that 30% of adults achieved at least 80% scalp hair coverage within 24 weeks, a milestone unreachable with corticosteroids or topical immunotherapy. Patent coverage through 2034–2041 protects first movers and encourages additional indications such as cicatricial alopecia. Reimbursement frameworks in the United States, Canada, and major EU states now recognize severe alopecia areata as a medical—not cosmetic—condition, improving access and expanding the alopecia treatment market. Manufacturers project that oral JAK inhibitors could capture 15-20% of the severe alopecia segment within five years.

AI-Driven Personalised Diagnostics & Treatment Planning

AI-enabled scalp-image analysis replaces subjective grading with pixel-level quantification. In a 470,000-image training set, an FDA-listed platform produced 77.7% better hair-growth outcomes by matching patients to optimal regimens and tracking compliance[2]ClinicalTrials.gov, “AI-Guided Personalized Therapy for Hair Loss (NCT05874219),” clinicaltrials.gov. Clinics integrate these tools with genetic and hormonal panels, creating curated protocols that cut costly trial-and-error cycles. Venture investments exceeding USD 50 million highlight confidence that algorithmic decision support will become standard within three years, particularly in tele-dermatology networks that serve rural areas.

Rise of Regenerative Therapies (PRP, Stem-Cells, Exosomes)

Platelet-rich plasma (PRP) injections have gained momentum after randomized trials demonstrated superior follicular density compared with growth-factor mesotherapy. Autologous platelet fibrin further reduces inflammatory signaling, lowering relapse risk without systemic immunosuppression. Emerging exosome formulations and stem-cell-conditioned media offer higher growth-factor payloads, though regulatory agencies require stringent cell-handling controls. Session pricing of USD 500–1,500 positions PRP as a premium cash-pay option in developed economies, broadening the alopecia treatment market where drug therapy fails or is contraindicated.

Rapid Uptake of Low-Level-Laser and At-Home Devices

FDA-cleared laser caps and LED helmets deliver photobiomodulation that stimulates dermal papilla cells and microcirculation, yielding non-drug regrowth benefits. Unit prices between USD 500 and USD 3,000 are competitive with one year of branded oral therapy. Direct-to-consumer campaigns partner with tele-medicine providers that bundle prescriptions and devices, enhancing multi-modal adherence. Because light therapy has no systemic side-effect profile, dermatologists increasingly recommend it as a bridge or maintenance option, reinforcing growth of the alopecia treatment market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent cliff for minoxidil/finasteride brands | −0.5% | Global; revenue pressure in mature markets | Short term (≤ 2 years) |

| Adverse-event concerns (sexual, systemic, immune) | −0.9% | Global; heightened scrutiny in North America & EU | Short term (≤ 2 years) |

| High procedure cost & limited insurance coverage | −0.6% | Global; acute impact in emerging markets | Medium term (2-4 years) |

| Counterfeit & unregulated online products | −0.4% | Global; pronounced in emerging markets & unregulated e-commerce | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Concerns (Sexual, Systemic, Immune)

The FDA recorded 32 adverse-event reports tied to compounded topical finasteride, including persistent erectile dysfunction and mood disorders, prompting warning letters and heightened pharmacy oversight. Oral JAK inhibitors carry boxed warnings for infections and cardiovascular risks, leading some clinicians to favor topical or injectable alternatives in lower-risk populations. These safety profiles increase counseling time and may delay initiation, tempering growth in the alopecia treatment market.

High Procedure Cost & Limited Insurance Coverage

Annual out-of-pocket spending for alopecia areata can reach USD 2,685, while branded JAK inhibitors approach USD 50,000 before discounts, placing advanced care out of reach for many patients[3]Sun Pharmaceutical Industries Ltd., “Sun Pharma Completes Acquisition of Concert Pharmaceuticals,” sunpharma.com. Payers often classify androgenic alopecia as cosmetic, denying claims for regenerative treatments and devices. Emerging markets face sharper affordability gaps, which slow uptake despite high disease prevalence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Androgenic Alopecia Dominance Faces Autoimmune Innovation

Androgenic alopecia maintained 36.62% of alopecia treatment market share in 2025, anchored by lifelong prevalence and the availability of low-cost minoxidil and generic finasteride. The alopecia treatment market size for this segment is set to expand steadily as legacy products remain first-line therapy. Yet disruption is imminent. Pelage Pharmaceuticals’ PP405 increased non-vellus hair counts sixfold in early trials by targeting mitochondrial pyruvate carriers, attracting USD 14 million from strategic investors. Alopecia totalis, benefiting from the same JAK class that revolutionized alopecia areata care, is pacing a 7.12% CAGR and could narrow the revenue gap by 2031. Pipeline reviews list more than 100 candidates against androgenic alopecia alone, signifying a shift toward mechanism-specific interventions.

Second-order effects include greater segmentation of autoimmune subtypes. Clinicians now stratify patients by interferon signature and cytokine dominance rather than surface presentation, tailoring immunomodulators accordingly. Traction alopecia—once addressed only by counseling and topical steroids—gains new interest as device-based offloading and regenerative adjuncts show promise in trials. Collectively, these trends point to an alopecia treatment market that will be defined by precision phenotyping and multi-modal combinations.

By Gender: Male Market Leadership Challenged by Female Segment Acceleration

Male consumers accounted for 62.14% of 2025 revenue owing to higher clinical prevalence and established cultural acceptance of treatment. However, women represent the fastest-growing cohort at 6.62% CAGR. AI-guided pattern recognition reveals diffuse, vertex-sparing presentations typical of female pattern hair loss, driving earlier diagnosis. Clinical data from deutuxolitinib showed stronger response rates in women under 50, prompting gender-specific dosing studies [clinicaltrials.gov]. As safety profiles improve, topical micro-encapsulated formulas avoid systemic exposure, overcoming historical teratogenicity concerns.

Tele-dermatology also narrows access gaps: discreet e-commerce kits deliver prescriptions, supplements, and low-level-laser devices to the doorstep, reducing stigma that once deterred female patients. Influencer-led education campaigns elevate hair loss from cosmetic worry to treatable medical condition, pushing the alopecia treatment market toward gender parity.

By Route of Administration: Topical Dominance Challenged by Injectable Innovation

Topicals retained 44.12% of 2025 revenue because of convenience and OTC availability. Nonetheless, injectables are on track for a 7.18% CAGR, propelled by PRP, advanced platelet fibrin, and investigational biologics such as AMP-303. This subsegment benefited from deeper follicular penetration and longer dosing intervals, answering adherence problems found in daily topical routines. The alopecia treatment market size for injectables will rise as clinicians bundle in-office sessions with at-home maintenance, creating hybrid revenue streams.

Orals remain vital for systemic autoimmune cases, yet safety monitoring burdens and black-box warnings limit broader use. Device-assisted topical delivery methods like microneedle patches blur category lines, offering near-injectable bioavailability without needles. Regulators see these localized systems as risk-reducing, fostering expedited pathways that will further diversify the alopecia treatment market.

By Distribution Channel: Retail Pharmacy Strength Meets Online Disruption

Retail outlets captured 47.95% of 2025 sales through insurance integration and pharmacist counseling, but online channels will post an 7.76% CAGR as unified tele-medicine portals cover consult, script, and fulfillment in one visit. Patients value discreet packaging and subscription pricing that lowers monthly costs. Digital-first firms use AI chat-bots to monitor side effects and renew prescriptions, supporting adherence and data capture that feed real-world evidence dashboards.

Hospital pharmacies focus on severe alopecia areata cases needing specialist monitoring. They stock JAK inhibitors and compounded formulas under risk-evaluation protocols. Yet their share will erode as cloud-based monitoring technologies allow community providers to handle complex regimens remotely. The evolving ecosystem forces incumbents to enhance e-commerce capabilities or partner with digital start-ups, reshaping revenue allocation within the alopecia treatment market.

By End-User: Clinic Dominance Shifts Toward Homecare Empowerment

Dermatology and aesthetic clinics generated 39.68% of 2025 income thanks to advanced diagnostics and procedural offerings. High-margin regenerative injections, hair-transplant surgeries, and compounded therapies keep clinics central. However, homecare devices are expanding at 7.52% CAGR, led by FDA-cleared laser helmets that deliver medical-grade photobiomodulation without regular office visits. The alopecia treatment market size flowing through home settings grows each quarter as insurers pilot remote-monitoring reimbursements.

Clinics respond by offering blended packages: a six-month PRP series paired with loaned laser caps and AI progress apps. This hybrid care delivers outcome continuity while protecting professional revenue. As at-home platforms integrate trichoscopy via smartphone attachments, follow-up visits become virtual, broadening reach and reinforcing the alopecia treatment market as a continuum rather than a place.

Geography Analysis

North America held 41.88% of 2025 revenue because FDA breakthrough designations accelerated three oral JAK inhibitor approvals within two years. Coverage determinations now classify severe alopecia areata as a reimbursable inflammatory disorder, easing patient cost burdens. Robust venture funding, exemplified by Pelage Pharmaceuticals’ USD 14 million infusion, supports a vibrant pipeline. Cross-border care remains common: U.S. residents travel to Mexico for lower-cost transplant surgery, while Canadian patients purchase compounded topicals from U.S. tele-pharmacies, tightening regional integration inside the alopecia treatment market.

Asia-Pacific delivers the fastest 6.32% CAGR, anchored by China’s 250 million hair-loss population and rising middle-class healthcare spending. Kintor Pharmaceutical’s proxalutamide topical advanced into late-stage review, reflecting China’s push to localize innovation. Japan fast-tracked ritlecitinib in 2023 for intractable cases, while South Korea drives device leadership with domestic laser-cap manufacturing. Indian generics reduce systemic therapy costs, making once-premium treatments accessible to a broader cohort. As regulatory convergence improves, cross-licensing will help global brands enter local formularies.

Europe sustains moderate growth through centralized EMA reviews that balance safety with innovation [ema.europa.eu]. National health systems reimburse partial costs after rigorous cost-effectiveness appraisals, producing predictable but slower uptake. Germany and the United Kingdom host academic-industry clusters that pioneer stem-cell and exosome research. Southern European countries see stronger demand for cosmetic surgery tourism, although economic constraints limit adoption of high-priced biologics, keeping the alopecia treatment market stratified by income.

Competitive Landscape

The alopecia treatment market exhibits moderate fragmentation with acquisitive momentum. Sun Pharma captured deuruxolitinib by acquiring Concert Pharmaceuticals for USD 576.0 million in 2023, instantly challenging Pfizer and Eli Lilly in the JAK space [sunpharma.com]. Aclaris Therapeutics licensed dermatology rights while retaining systemic indications, illustrating collaborative risk sharing. Device makers like Capillus and HairMax bypass prescription pathways through direct-to-consumer marketing and subscription financing, appealing to price-sensitive segments.

Future competition hinges on data integration. Platforms that couple prescription products with AI diagnostics and longitudinal outcome tracking differentiate on evidence rather than molecule alone. Intellectual-property moats widen as innovative delivery systems—microneedle arrays, hydrogel patches, and exosome carriers—secure patents beyond core actives. Consolidation is expected among tele-health operators seeking scale economies in pharmacy fulfillment and specialist staffing. Companies that demonstrate durable efficacy while managing safety signals will secure formulary preference and insurance backing, reinforcing leadership within the alopecia treatment market.

Alopecia Treatment (Hair Loss) Industry Leaders

Johnson & Johnson

Cipla Inc.

Merck & Co. Inc.

Pfizer Inc.

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sun Pharma won a U.S. appellate ruling that removed an injunction and cleared the path for Leqselvi commercial launch in the United States.

- March 2025: SPARC began Phase 1 trials of SCD-153, an itaconic-acid derivative for alopecia areata therapy development.

- February 2025: Alys Pharmaceuticals received regulatory clearance to start clinical studies on a novel autoimmune alopecia candidate.

- January 2025: Eirion Therapeutics reported Phase 1 success for ET-02 topical, achieving a six-fold increase in non-vellus hair count within five weeks.

- December 2024: Veradermics raised USD 75 million in Series B financing to fund Phase 3 trials of a non-hormonal oral therapy.

- August 2024: Pelage Pharmaceuticals launched a Phase 2a study of PP405 after securing USD 14 million in Series A-1 funding.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the alopecia treatment market as prescription and over-the-counter pharmacotherapies, including minoxidil, finasteride, cyclosporine, emerging JAK inhibitors, and other systemic or topical drugs, used to halt or reverse medically diagnosed hair loss in scalp or body.

Scope exclusion: Surgical hair restoration procedures, cosmetic hair-care products, laser caps, and nutraceutical supplements are outside this study.

Segmentation Overview

- By Disease Type

- Androgenic Alopecia

- Alopecia Areata

- Scarring (Cicatricial) Alopecia

- Traction Alopecia

- Alopecia Totalis

- By Gender

- Male

- Female

- By Route of Administration

- Oral

- Topical

- Injectable

- By Distribution Channel

- Hospitals

- Retail Pharmacies & Drug Stores

- Online Pharmacies & E-pharmacy Platforms

- By End-User

- Dermatology & Aesthetic Clinics

- Homecare Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi-structured interviews with dermatologists, hospital pharmacists, and tele-trichology platform managers across North America, Europe, and Asia let us validate prevalence ranges, average prescription sizes, and discontinuation rates. Online surveys captured out-of-pocket spending habits of male and female patients. Insights helped us fine-tune uptake curves for fresh JAK inhibitor launches.

Desk Research

Our analysts first mapped worldwide prevalence and treatment-seeking patterns using open datasets such as WHO Global Health Observatory, CDC NHANES, Eurostat morbidity files, and peer-reviewed dermatology journals.

Regulatory archives (FDA, EMA), patent libraries via Questel, and import-export flows from Volza supplied launch timing, molecule lineage, and trade proxies.

Company 10-Ks, dermatologist association white papers, and news feeds on Dow Jones Factiva rounded out supply-side intelligence.

The sources listed illustrate but do not exhaust the reference universe we reviewed.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort model quantified the addressable patient pool, which we then valued through weighted average annual therapy costs.

Selected bottom-up checks, sample wholesaler invoice rolls and retail ASP x volume snapshots, were layered in to adjust regional totals.

Key variables include diagnosed alopecia incidence, dermatologist density, drug patent expiry timelines, median therapy price, and reimbursement coverage ratios.

Multivariate regression with scenario analysis projected 2025-2030 demand, and gaps in bottom-up data were bridged using regional price-elasticity factors vetted by experts.

Data Validation & Update Cycle

Outputs pass three-tier review: automated variance scans, senior analyst peer audit, and final lead analyst sign-off.

We refresh every twelve months, re-running critical indicators mid-cycle if material events, such as new FDA approvals, shift the base outlook.

Credibility Through Alopecia Treatment (Hair Loss) Baseline Selection

Published numbers diverge because firms mix pharmaceuticals with devices, cosmetic topicals, or even surgical services.

By centering exclusively on clinically prescribed and OTC drug therapies, our baseline remains lean yet decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.67 B (2025) | Mordor Intelligence | - |

| USD 9.48 B (2024) | Global Consultancy A | Bundles devices and surgical services; assumes uniform ASP uplift globally |

| USD 10.76 B (2025) | Industry Association B | Counts nutraceuticals and regenerative procedures; limited prevalence cross-checks |

These contrasts show that when scope balloons, so does value. By adhering to clearly defined therapy classes, applying transparent prevalence logic, and vetting each step with field clinicians, Mordor delivers a dependable, reproducible baseline that buyers can trace from raw statistic to final dollar figure.

Key Questions Answered in the Report

How big is the alopecia treatment market today?

The alopecia treatment market stood at USD 3.87 billion in 2026 and is forecast to reach USD 5.05 billion by 2031 at a 5.46% CAGR.

Which disease segment grows the fastest through 2031?

Alopecia totalis is the fastest-growing disease segment, registering a 7.12% CAGR over the forecast period.

Why are JAK inhibitors considered game changers?

Three FDA-approved JAK inhibitors can restore 80% or more scalp coverage in about one-third of severe alopecia areata patients, surpassing historical response rates from steroids.

What role does AI play in hair-loss management?

AI scalp-image analysis personalizes therapy selection and tracks progress, improving hair-growth outcomes by nearly 78% in controlled studies and expanding remote-care options.

Which region is expanding the quickest?

Asia-Pacific leads growth at a 6.32% CAGR, fueled by China’s large patient base, faster regulatory approvals, and local manufacturing that lowers therapy costs.

Are at-home laser devices effective?

FDA-cleared low-level-laser helmets improve cellular activity and microcirculation, offering a non-drug option that complements pharmacologic or regenerative treatments.

Page last updated on: