Cellulite Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

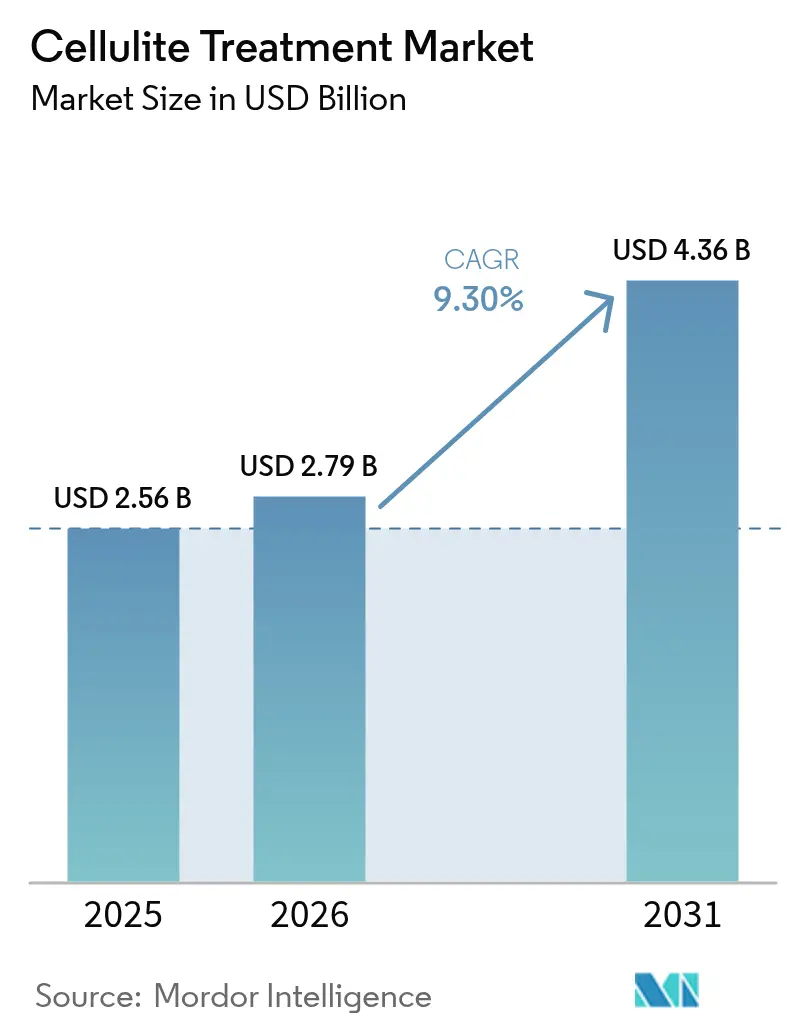

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 4.36 Billion |

| Growth Rate (2026 - 2031) | 9.30% CAGR |

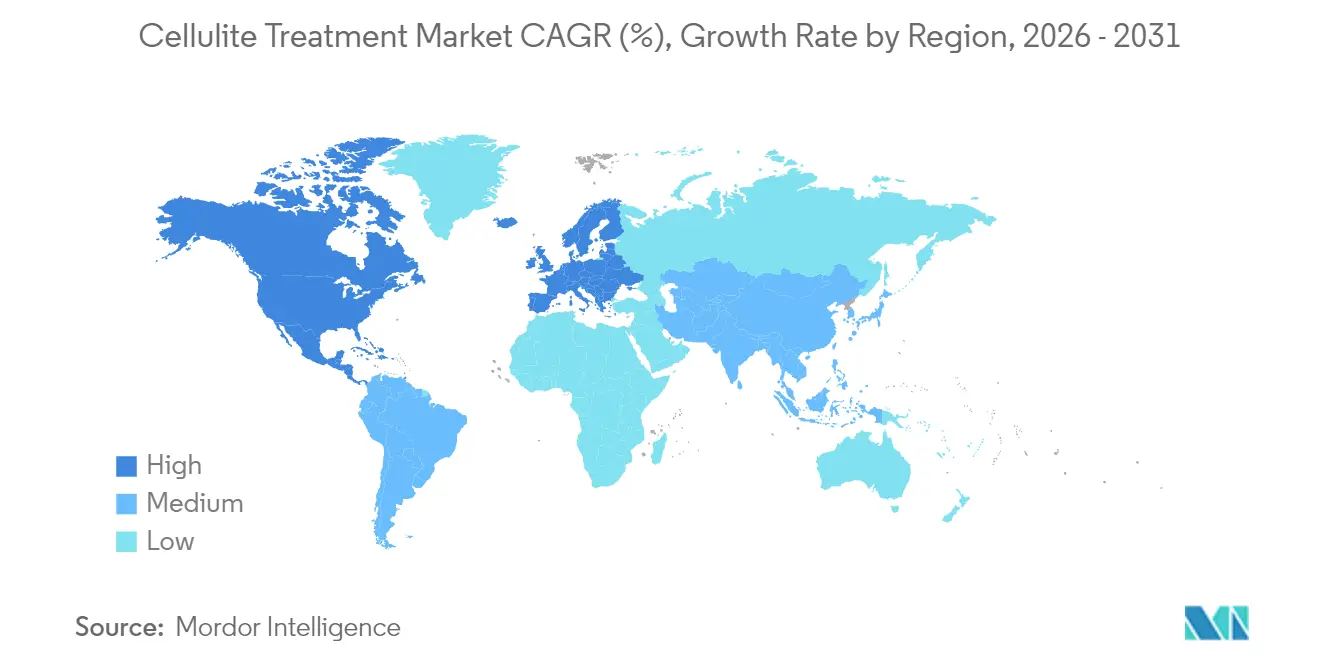

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

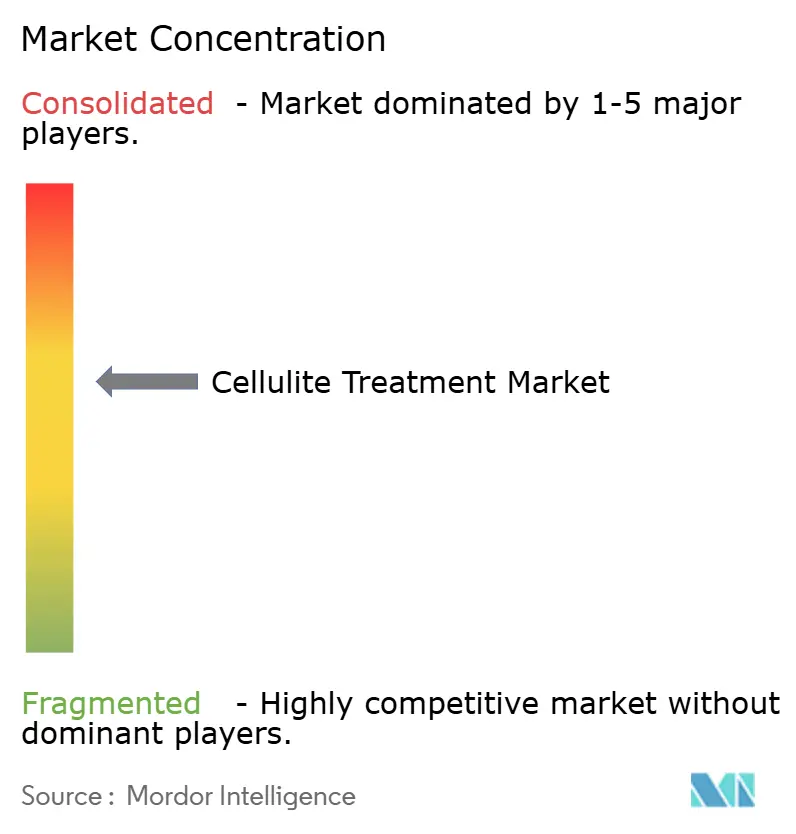

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cellulite Treatment Market Analysis by Mordor Intelligence

The cellulite treatment market size is expected to grow from USD 2.56 billion in 2025 to USD 2.79 billion in 2026 and is forecast to reach USD 4.36 billion by 2031 at 9.30% CAGR over 2026-2031. This expansion reflects steady patient demand driven by rising global obesity rates, accelerating adoption of AI-enabled energy-based devices, and a steady shift toward corporate wellness packages that reimburse aesthetic procedures. Non-invasive radiofrequency and ultrasound systems keep patient downtime to a minimum, while newly FDA-cleared minimally invasive platforms such as Avéli shorten recovery windows even further. Provider differentiation now hinges on data-guided personalization of treatment protocols, allowing clinics to combine multiple modalities in a single session and lift per-patient revenue. Rapid device innovation, broader practitioner training programs, and growing consumer willingness to finance appearance-oriented care positions the cellulite treatment market for multi-year expansion across developed and emerging economies alike.

Key Report Takeaways

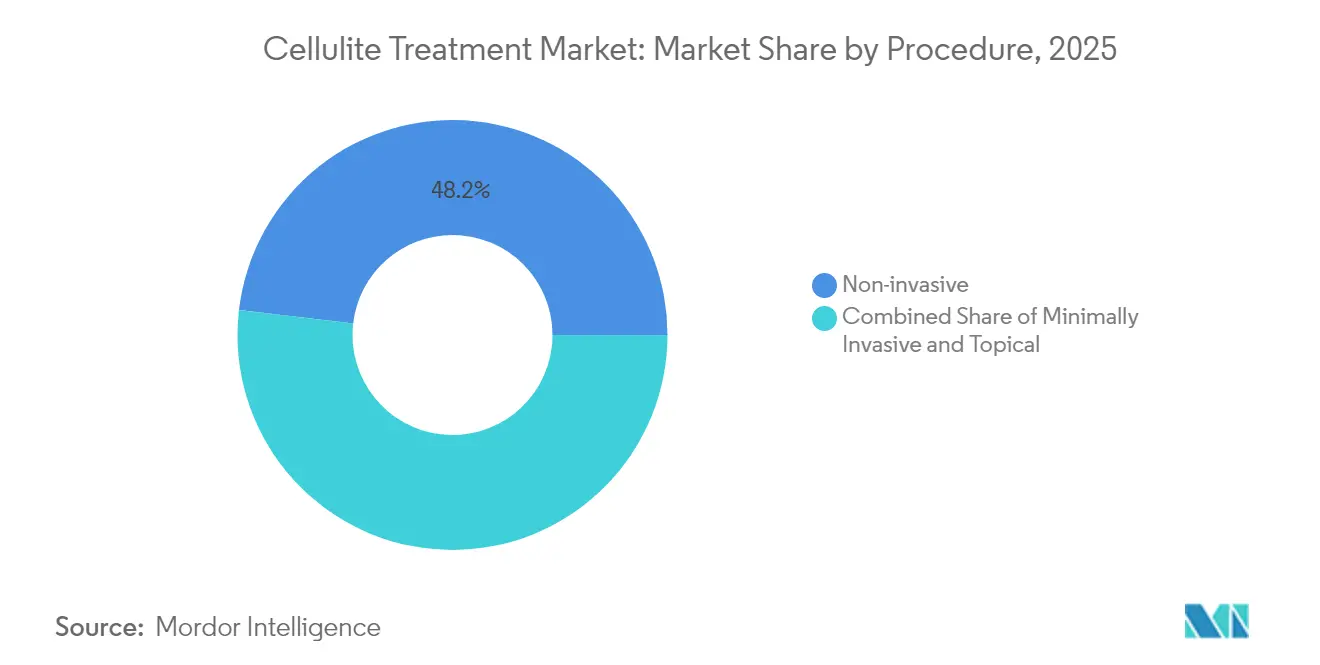

- By procedure, non-invasive options led with 48.15% revenue share in 2025; minimally invasive approaches are set to record the fastest 10.05% CAGR through 2031.

- By cellulite type, soft cellulite contributed 51.05% of the cellulite treatment market share in 2025, whereas hard cellulite is forecast to grow at a 10.21% CAGR to 2031.

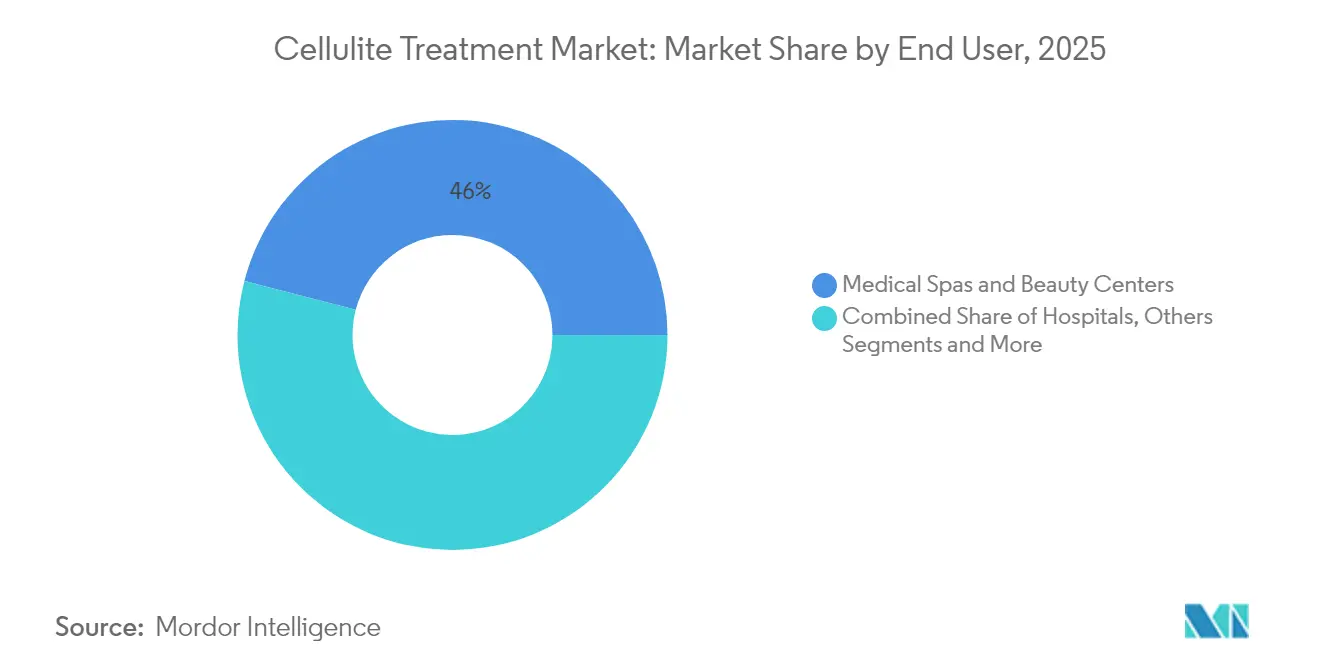

- By end user, medical spas and beauty centers captured 45.95% of the cellulite treatment market in 2025; specialized dermatology clinics are advancing at an 10.62% CAGR.

- By geography, North America held 41.95% of revenue in 2025, while Asia-Pacific is projected to expand at an 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cellulite Treatment Market*

| Driver | (`) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Obesity & Overweight Prevalence | +2.1% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Growing Preference For Non-Invasive Aesthetic Procedures | +1.8% | Global, led by developed markets | Medium term (2-4 years) |

| Technological Advances In Energy-Based Devices | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increasing Disposable Income & Aesthetic Consciousness | +1.3% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-Driven Personalised Treatment Protocols | +0.9% | North America, early adoption in EU | Short term (≤ 2 years) |

| Corporate Wellness Aesthetic Stipends | +0.6% | North America, selective EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Obesity & Overweight Prevalence

Higher body mass index intensifies dermal-adipose interactions that create visible dimpling, cementing obesity as a prime catalyst for the cellulite treatment market. A peer-reviewed evaluation of aesthetic clinics found 78% of cellulite patients present with elevated BMI, correlating directly with severity grades. Excess adiposity disrupts lymphatic flow and thins collagen septae, prompting practitioners to layer radiofrequency, ultrasound and injectable collagenase in one plan. Because such multimodal strategies command higher price points, average treatment revenue is rising alongside case volumes. The trend is particularly enduring in the United States and Western Europe, where processed-food consumption and sedentary lifestyles remain entrenched, providing a sustained clinical pipeline for providers.

Growing Preference for Non-Invasive Aesthetic Procedures

Social media advocacy and mainstream acceptance of lunchtime procedures have tilted demand sharply toward non-surgical care. Industry association data show non-invasive body contouring reached USD 17 billion in 2024, with cellulite therapies at the forefront [1]American Med Spa Association, “Medical Spa State of the Industry Report 2024,” americanmedspa.org. Younger demographics display markedly lower risk tolerance, favoring energy-based platforms that let them resume work the same day. Technical refinements in radiofrequency and high-intensity focused ultrasound now close much of the efficacy gap that once separated surgery and surface treatments. Clinics report that roughly 85% of consultations revolve exclusively around non-invasive options, a fundamental redesign of provider service mix that continues to widen the cellulite treatment market.

Technological Advances in Energy-Based Devices

Precision-guided platforms have redefined clinical outcomes. The FDA-cleared LipoAI system, for instance, combines 1444 nm laser output with machine-learning algorithms that adjust fluence according to real-time tissue feedback. Combination products such as EmTone or Venus Bliss MAX integrate synchronized RF and electromagnetic stimulation, shrinking adipocytes and stimulating collagen in a single pass. Clinical trials demonstrate 41% average reduction in adipose thickness when modalities are combined, versus 19% for single-technology protocols. As device makers roll out iterative upgrades every 12-18 months, practitioners gain new revenue streams and the cellulite treatment market benefits from technology-induced replacement cycles.

Increasing Disposable Income & Aesthetic Consciousness

Rising household earnings across Asia-Pacific are unlocking new patient segments. China’s aesthetic device outlays are projected to rise 6.20% annually to 2030, while India follows at 4.50%. Social platforms amplify aesthetic ideals and shorten decision cycles, creating a multiplier effect on procedure uptake. Medical tourism adds another layer: clinics in South Korea and Thailand market cellulite packages that cost 30–40% less than in Western cities yet use the same FDA-cleared systems, driving cross-border patient flows. These dynamics funnel additional volume into the cellulite treatment market and encourage providers to scale multilingual after-care services.

AI-Driven Personalised Treatment Protocols

Cloud-based assessment suites now grade cellulite severity, tissue density and skin laxity from high-resolution images, producing energy maps that guide device settings. North American dermatology groups report 22% shorter treatment plans and 15% higher patient satisfaction when AI analytics are used to configure session parameters. This data-rich workflow minimizes overtreatment risk, raises the success rate of first-time patients, and reduces consumable waste—collectively improving clinic margins. Early adopters therefore gain both clinical and commercial advantages, deepening the competitive moat inside the cellulite treatment market.

Restraints Impact Analysis of Cellulite Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness in emerging markets | -1.2% | APAC emerging, MEA, Latin America | Medium term (2-4 years) |

| High procedure cost & limited reimbursement | -0.8% | Global, heightened in price-sensitive zones | Long term (≥ 4 years) |

| Regulatory tightening on device safety | -0.7% | FDA & EU leadership | Short term (≤ 2 years) |

| Counterfeit home-use device proliferation | -0.5% | APAC e-commerce hubs, global online | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Awareness in Emerging Markets

Despite better spending power, fewer than 15% of prospective APAC or Latin American patients can name a cellulite therapy beyond topical creams, contrasting with 67% brand recall in North America. Lack of professional training programs and limited regional workshops slow practitioner adoption, capping territory expansion for device vendors. The resulting demand gap undercuts global revenue potential for the cellulite treatment market until sustained education campaigns gain traction.

High Procedure Cost & Limited Reimbursement

Out-of-pocket costs average USD 200–700 per session, and most protocols require 6–12 visits, keeping services out of reach for large middle-income cohorts. Cosmetic classification excludes cellulite treatments from public or private insurance, elevating affordability concerns. Subscription packages and clinic financing have emerged but have yet to prove meaningful in widening addressable demand. Persistent cost barriers therefore temper the otherwise strong growth trajectory of the cellulite treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cellulite Treatment Market Segment Analysis

By Procedure:

Technology Integration Drives Modality ConvergenceNon-invasive platforms commanded 48.15% of 2025 revenue, a testament to consumer preference for low-downtime solutions. Radiofrequency leads within this bracket thanks to deeper heat penetration and intelligent temperature controls that minimize epidermal risk. High-intensity ultrasound is closing ground as real-time thermal imaging supports precise energy deposition. Together, these improvements keep the cellulite treatment market size for non-invasive solutions on an uptrend.

Minimally invasive options accelerate at a 10.05% CAGR to 2031, buoyed by FDA greenlights for Avéli and next-generation subcision tools that use micro-blade designs to sever fibrous septae with fewer passes . Injectable collagenase, spearheaded by QWO, inaugurates a drug-device hybrid niche, offering clinicians chemical lysis alongside mechanical release. As efficacy data pile up, clinics diversify procedure menus, reinforcing the modality convergence that now characterizes the cellulite treatment market.

By Cellulite Type:

Diagnostic Precision Enables Targeted TherapiesSoft cellulite accounted for 51.05% of treated cases in 2025, primarily affecting thigh and buttock areas with visible but pliable dimples. Providers often pair radiofrequency bulk heating with manual lymphatic drainage to smooth surface irregularities. Diagnostic ultrasound pinpoints adipose pockets and guides handpiece positioning, enhancing single-session improvements and underpinning expansion of the cellulite treatment market.

Hard cellulite, more fibrotic and adherent, is advancing fastest at a 10.21% CAGR as imaging and AI-aided scoring refine case identification. Energy-assisted subcision paired with high-power RF delivers deeper thermal remodeling, while temperature feedback loops ensure safety in dense tissues. Edematous cellulite cases remain clinically demanding, requiring multi-visit regimes that combine intermittent pneumatic compression, ultrasound, and enzymatic injectables. This complex therapeutic mix underscores the importance of pathology-specific protocols inside the cellulite treatment industry.

By End User:

Specialization Drives Market DifferentiationMedical spas and beauty centers captured 45.95% of 2025 turnover, leveraging retail-like storefronts, loyalty programs and flexible hours. Average revenue per visit stands at USD 526, with cellulite regimens driving repeat footfall. Spa operators frequently bundle body contouring with facial treatments, broadening basket size and propelling the cellulite treatment market.

Dermatology clinics, while smaller in absolute volume, will post 10.62% CAGR through 2031. Their growth rests on board-certified expertise, insurance-grade electronic health records and in-house ultrasound diagnostics that bolster procedural credibility. Hospitals remain niche but handle complex cases for patients managing comorbidities such as diabetes or cardiovascular disease. This stratification illustrates how provider specialization boosts perceived value and supports premium pricing within the cellulite treatment market size.

Geography Analysis

North America Cellulite Treatment Market

North America retained 41.95% revenue leadership in 2025 thanks to affluent patient cohorts, broad device availability and a regulatorily transparent pathway for innovative platforms. The region added nearly 1,600 medical spas in 2023, increasing procedure access points. Corporate wellness stipends that reimburse aesthetic services extend demand beyond vanity-driven consumption, expanding the cellulite treatment market across diverse employee bases.

Europe Cellulite Treatment Market

Europe follows as a technology-mature arena, anchored by Germany, France and the United Kingdom. The European Medicines Agency’s stringent clinical-data requirements elevate capital hurdles, yet once cleared, devices benefit from physician confidence and sizeable private-pay markets. Multi-modality packages that marry cellulite therapy with skin-tightening and fat-reduction are commonplace, supporting cross-selling and deepening wallet share per patient. Intellectual property protections and robust clinical trial networks continue to draw U.S. and Asian manufacturers into European partnerships, enriching the cellulite treatment industry ecosystem.

APAC Cellulite Treatment Market

Asia-Pacific posts the highest 11.02% CAGR to 2031, riding middle-class expansion and social media-fueled aesthetic awareness. China’s tier-1 cities see double-digit annual growth in high-end cosmetic clinics, while India’s metro hubs invest in AI-guided RF systems to attract medical tourists. South Korea remains an innovation bellwether, exporting patent-backed handpieces and licensed algorithms worldwide. Meanwhile, price-competitive packages bundled with vacation itineraries funnel international patients into Thai and Malaysian hospitals, broadening the cellulite treatment market size in the region.

Regulatory Landscape

In the United States, cellulite treatment devices fall under FDA medical-device oversight, with cellulite reduction instruments regulated as Class II devices under 21 CFR 878.4790 and subject to special controls such as non-clinical testing, biocompatibility, and electrical-safety requirements. A key compliance anchor is the FDA Quality Management System Regulation (QMSR), which took effect in February 2026 and aligns quality-system expectations with ISO 13485:2016, placing greater weight on audit-ready design controls, supplier qualification, and post-market surveillance for energy-based and minimally invasive platforms.

In Europe, the EU Medical Device Regulation (MDR 2017/745) continues to raise evidence and technical documentation expectations for aesthetic and medical-aesthetic systems, while harmonized standards remain central to demonstrating conformity. EN IEC 60601-2-57:2026 entered into force in January 2026 for non-laser medical and aesthetic optical radiation devices, reinforcing safety and performance standards that support conformity routes under EU MDR. On the injectable side, product portfolios are expanding body indications; for example, Sculptra received EU MDR certification for new body indications, including improvement of cellulite appearance in selected areas, in December 2025, underscoring the role of notified bodies and updated labeling for aesthetic indications.

Value Chain Analysis

The value chain spans device and drug innovators through clinical delivery sites, with modality-specific pathways. Upstream, device OEMs develop energy-based (radiofrequency, laser, ultrasound) and acoustic-wave systems, often integrating suction or mechanical massage, while minimally invasive platforms add specialized handpieces and sterile accessories. In parallel, injectable options follow pharmaceutical manufacturing and quality pathways, with products such as collagenase requiring lyophilized drug production, cold-chain logistics, and clinic-level preparation steps before subcutaneous administration. Regulatory anchors such as EN IEC 60601-2-57:2026, which entered into force in January 2026, are shaping supplier qualification and post-market oversight across the chain.

Midstream commercialization typically runs through a mix of direct-to-clinic sales and authorized distributors, supported by practitioner training to standardize technique and limit outcome variability across medical spas, dermatology clinics, and hospital settings. Downstream, providers bundle cellulite treatment with broader body-contouring and skin-tightening menus, and revenue realization depends on consult workflow, imaging and assessment tools, consumables, and follow-up cadence. Key friction points include regulatory documentation burdens for new indications and device modifications, the need for verified supply channels to limit counterfeit home-use devices, and service-and-maintenance capacity that keeps installed systems utilized and compliant.

Competitive Landscape

The market is moderately fragmented, with scale advantages secondary to proprietary technology and clinical documentation. BTL Aesthetics leverages its high-intensity electromagnetic plus RF system to offer dual-action cellulite reduction and muscle toning in one 30-minute session, claiming a 7-pointimprovement on the Numeric Cellulite Severity Scale in multicenter trials. Venus Concept differentiates via subscription-based equipment leasing that lowers upfront costs and couples devices with continuous training, enabling independent clinics to update technology every 24 months without capital strain [3]Venus Concept, “Venus Bliss MAX Launch Announcement,” venusconcept.com. Merz Pharma capitalizes on its hybrid portfolio of injectables and devices, allowing cross-promotion between collagenase treatments and energy platforms, which elevates patient lifetime value.

Consolidation is reshaping competitive arithmetic. Hahn & Company’s merger of Cynosure and Lutronic pooled R&D pipelines and doubled direct-sales coverage, augmenting bargaining power with distributors and boosting R&D spend on AI-enabled interfaces. Start-ups such as Reshape Lifesciences pursue non-thermal acoustic wave systems that claim reduced pain and no skin-type limitations, while dermatology biotech firms explore topical RNA-interference compounds designed to modulate adipocyte metabolism. As device lifecycles compress and evidence thresholds climb, firms that supply structured clinical data, ongoing practitioner education and AI-driven treatment libraries are best positioned to gain incremental cellulite treatment market share.

White-space opportunity remains in regulated home-use devices. Although counterfeit handpieces circulate on e-commerce portals, legitimate offerings must pass rigorous safety testing; this delay creates runway for established manufacturers to enter with FDA-cleared consumer products. Firms that pair hardware with companion mobile apps that log treatment parameters and guide session cadence are expected to unlock new revenue layers, further enlarging the cellulite treatment market.

Cellulite Treatment Industry Leaders

Merz Pharma GmbH & Co KGa

Inceler Medikal Co Ltd

Candela Corporation

Hologic Inc

Cutera Inc

- *Disclaimer: Major Players sorted in no particular order

Cellulite Treatment Market Companies Covered in this Report

- Hologic

- Candela Medical

- Cutera

- Merz Pharma

- Allergan Aesthetics (AbbVie)

- Sisram Medical

- Venus Concept Inc.

- BTL

- Endo International plc (Qwo)

- Lumenis

- Sciton

- Fotona d.o.o.

- Lutronic

- Zimmer Aesthetics

- Cynosure LLC

- Inceler Medikal Co. Ltd.

- Beijing Nubway S&T Co. Ltd.

- Cymedics

- BeautyBio Inc.

- Tanceuticals

- Solta Medical

Market Opportunities and Future Outlook

A large opportunity area is protocol-driven combination care that addresses both fibrous septa and skin laxity in a single treatment plan, aligning with patient preference for lower downtime and fewer visits. Clinical direction is visible in combinations pairing targeted subcision platforms (such as Aveli) with energy-based skin remodeling modalities like helium plasma radiofrequency (Renuvion); Apyx Medical published combination-treatment clinical data in May 2026, reinforcing provider interest in multi-step workflows that can be operationalized within clinic throughput constraints. This creates whitespace for vendors packaging integrated treatment libraries, imaging guidance, and standardized training to help clinics deliver consistent outcomes across cellulite types.

A second opportunity sits in compliance-led differentiation for home-use and clinic-adjacent ecosystems, where legitimate manufacturers can pair cleared hardware with companion apps that log parameters and guide cadence, while meeting safety expectations that counterfeit products bypass. On the provider side, the market shows room for AI-enabled personalization of energy delivery and ultrasound-assisted assessment to reduce overtreatment risk and improve patient experience, which supports higher utilization of existing platforms. In regions with low awareness and limited reimbursement, omnichannel education and financing models remain under-penetrated, leaving room for manufacturers and large clinic groups to expand access through structured patient education, bundled packages, and corporate wellness programs that already reimburse aesthetic procedures in selective markets.

Recent Industry Developments in Cellulite Treatment Market

- January 2026: Candela Corporation announced the European launch of the Glace System at IMCAS World Congress 2026 in Paris. The platform combines hydrodermabrasion, dual-mode cupping massage, and LED technology in a non-invasive workflow. The launch broadens Candela's installed-base cross-sell potential for clinics that package multi-modality aesthetic sessions alongside established body contouring and cellulite procedures.

- March 2025: Candela Corporation announced the launch of the GLAC treatment at the American Academy of Dermatology (AAD) Annual Meeting. The rollout emphasized in-clinic add-on treatments that can be layered into existing aesthetic protocols with minimal downtime. This supports practice economics by expanding billable service menus around the same patient cohorts seeking body and skin appearance improvements.

- April 2024: Caliway Biopharmaceuticals announced Phase 2 results for CBL-514, an injectable being developed to treat raised cellulite areas. The update highlighted continued clinical development activity in injectable approaches beyond device-only solutions. Progress in this category expands the drug-device hybrid competitive space for providers that combine structural release and biologic or enzymatic remodeling in their cellulite offerings.

Cellulite Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues generated from solutions used to reduce the visible appearance of cellulite, including device-based procedures, minimally invasive procedures, and topical products delivered through clinical and consumer channels.

Scope exclusions: We do not count broader weight-loss, general skin tightening not intended for cellulite, or reconstructive surgeries where cellulite improvement is only a secondary outcome.

Segments Covered in This Report

- By Procedure

- Non-invasive

- Radiofrequency-based

- Laser-based

- Ultrasound-based

- Acoustic-wave

- Cryolipolysis

- Minimally Invasive

- Subcision

- Injectable collagenase

- Laser-assisted lipolysis

- Topical

- Retinol creams

- Caffeine creams

- Peptide-based formulations

- Non-invasive

- By Cellulite Type

- Soft Cellulite

- Hard Cellulite

- Edematous Cellulite

- By End User

- Hospitals

- Specialized Dermatology Clinics

- Medical Spas & Beauty Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the demand pool and to keep assumptions realistic across regions. We relied on non-paywalled sources such as CDC and NIH publications, FDA device and safety communications, OECD and World Bank health expenditure indicators, and peer-reviewed dermatology and aesthetic medicine journals to understand procedure outcomes and adoption.

For commercialization signals, we reviewed company annual reports, investor presentations, press releases, and reputable news coverage to map launches, price ranges, and clinic expansion. A paid subscription for company financials and news intelligence supported checks on revenue mix and geographic exposure, and a patent database helped track technology activity around energy-based devices and minimally invasive methods. The sources listed here are illustrative, and we also used other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually paid for cellulite reduction in clinics and medspas, and how usage differs by procedure type and setting. We spoke with a mix of providers, distributors, and industry advisors across Americas, EMEA, and APAC to test the treatment mix, typical price points, repeat sessions, and how demand shifts with consumer spending and new device introductions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | APAC: 43% |

| Mid tier: 42% | Functional/Unit leaders: 35% | EMEA: 32% |

| Smaller Players: 22% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Our core sizing uses a top-down build where procedure volumes and treated-population assumptions are reconstructed by region, then translated into value using typical price points and session intensity. The totals are cross-checked with selective bottom-up approximations, such as sampled clinic revenue per device or per treatment room, plus channel checks on topical product sell-through, and the model is adjusted where the two views do not reconcile.

Key inputs used in the model include the share of adult population seeking aesthetic body procedures, clinic and medspa density by major cities, average sessions per patient by modality, typical price per session or per course of treatment, and the split between provider-delivered procedures versus retail and e-commerce topical products. Because price can move faster than volumes, especially when new devices are launched, we stress-test ASP trends with primary feedback and observable consumer spending indicators.

For forecasting, scenario analysis is used around three drivers that interviewees consistently flagged: affordability and financing, provider capacity expansion, and adoption of newer non-invasive and minimally invasive techniques. When bottom-up checks are incomplete in smaller countries, gaps are handled through per-capita procedure intensity proxies and by anchoring to regional peer markets with similar income levels and clinic infrastructure.

Data Validation & Update Cycle

Validation is done through stepwise triangulation, where modeled revenues are compared against independent signals such as procedure utilization patterns, device install base commentary, and clinic capacity constraints. Outliers are reviewed for unit errors, price mix shifts, or one-time events, and then the assumptions are revisited before sign-off by a separate analyst.

The report is refreshed annually, and interim checks are triggered when material events occur, such as a major regulatory action, a meaningful technology shift, or sharp changes in consumer discretionary spending. Before delivery, we complete a final update pass to ensure the market numbers and assumptions reflect the latest available information.

Mordor Intelligence's Cellulite Treatment Market Size Compared Against Other Published Estimates

Published market values for cellulite treatment do not always match because the scope can shift between procedures and topical products, the base year can differ, and some models assume different session counts and pricing progression. Currency timing also matters since a meaningful share of demand sits in regions where exchange rates can move within a year.

A few gap drivers tend to dominate in this market, where one estimate may count only professional procedures while another blends in at-home creams and massage tools, and where aggressive forecasts can come from assuming fast uptake of new devices without checking clinic capacity. Our number stays closer to what providers can deliver because the model ties volumes to installed base and appointment throughput, and then only counts topical revenue when it is connected to cellulite positioning and not general skin care, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.79 B (2026) | |

| Global Consultancy A | USD 1.90 B (2023) | Uses an earlier base year and a broader global roll-up approach, and the revenue boundary between professional procedures and consumer topicals is not clearly separated, which can compress the starting value versus a later-year model. |

| Industry Publisher B | USD 0.61 B (2024) | Appears to focus on a narrower revenue pool with stronger weighting to consumer products and selected therapy types, which can undercount clinic and medspa procedure value and reduce the reported market size for the current year. |

Taken together, the spread mainly reflects what is counted as a cellulite-specific revenue stream and how quickly procedure pricing and session intensity are assumed to change. By keeping the inputs tied to observable treatment volumes, realistic provider capacity, and clearly stated inclusions, we keep the estimate easier to trace and repeat when new information comes in without reworking the whole model from scratch.

Key Questions Answered in the Report

How big is the Cellulite Treatment Market?

The Cellulite Treatment Market size is expected to reach USD 2.79 billion in 2026 and grow at a CAGR of 9.30% to reach USD 4.36 billion by 2031.

Which procedure segment leads today?

Non-invasive platforms hold 48.15% revenue share, driven by radiofrequency and ultrasound systems that minimize downtime.

Who are the key players in Cellulite Treatment Market?

Merz Pharma GmbH & Co KGa, Inceler Medikal Co Ltd, Candela Corporation, Hologic Inc and Cutera Inc are the major companies operating in the Cellulite Treatment Market.

Which is the fastest growing region in Cellulite Treatment Market?

Asia-Pacific is forecast to expand at an 11.02% CAGR to 2031, propelled by rising middle-class incomes and broader regulatory approvals.

What technology trends are shaping future growth?

AI-guided energy delivery, multi-modal combination platforms, and emerging injectable collagenase therapies are key innovation fronts.

Page last updated on: