Algeria Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

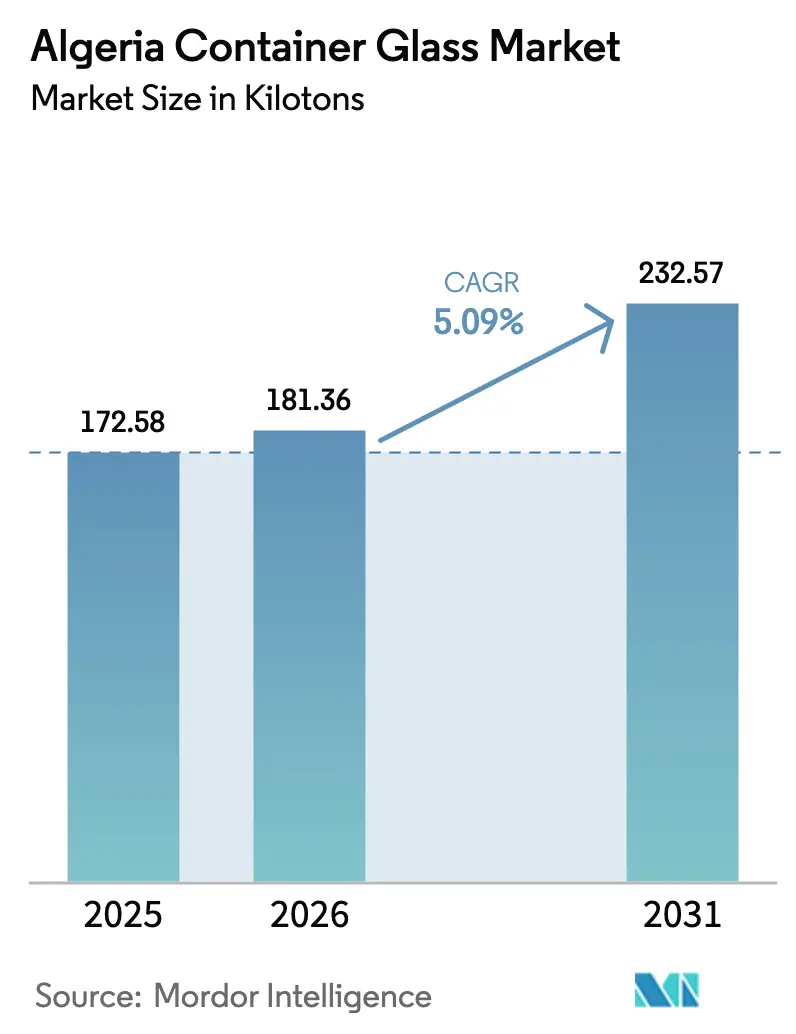

| Base Year Market Size (2025) | 172.58 kilotons |

| Market Volume (2026) | 181.36 kilotons |

| Market Volume (2031) | 232.57 kilotons |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Container Glass Market Analysis by Mordor Intelligence

The Algeria Container Glass Market size in 2026 is estimated at 181.36 kilotons, growing from 2025 value of 172.58 kilotons with 2031 projections showing 232.57 kilotons, growing at 5.09% CAGR over 2026-2031. This growth trajectory reflects Algeria's strategic pivot toward import-substitution manufacturing, supported by government incentives through the Agence Algérienne de Promotion de l'Investissement, which offers customs-duty exemptions and tax holidays for local production initiatives. The market's expansion coincides with French beverage group Castel’s acquisition of ALVER, Algeria’s largest glassworks, signaling renewed confidence in local glass-manufacturing capabilities and plans to reintroduce bottle-return systems for sustainable packaging.[1]Marie-Josée Cougard, “Le français Castel s’offre la plus grosse verrerie d’Algérie,” Les Echos, lesechos.fr

Key Report Takeaways

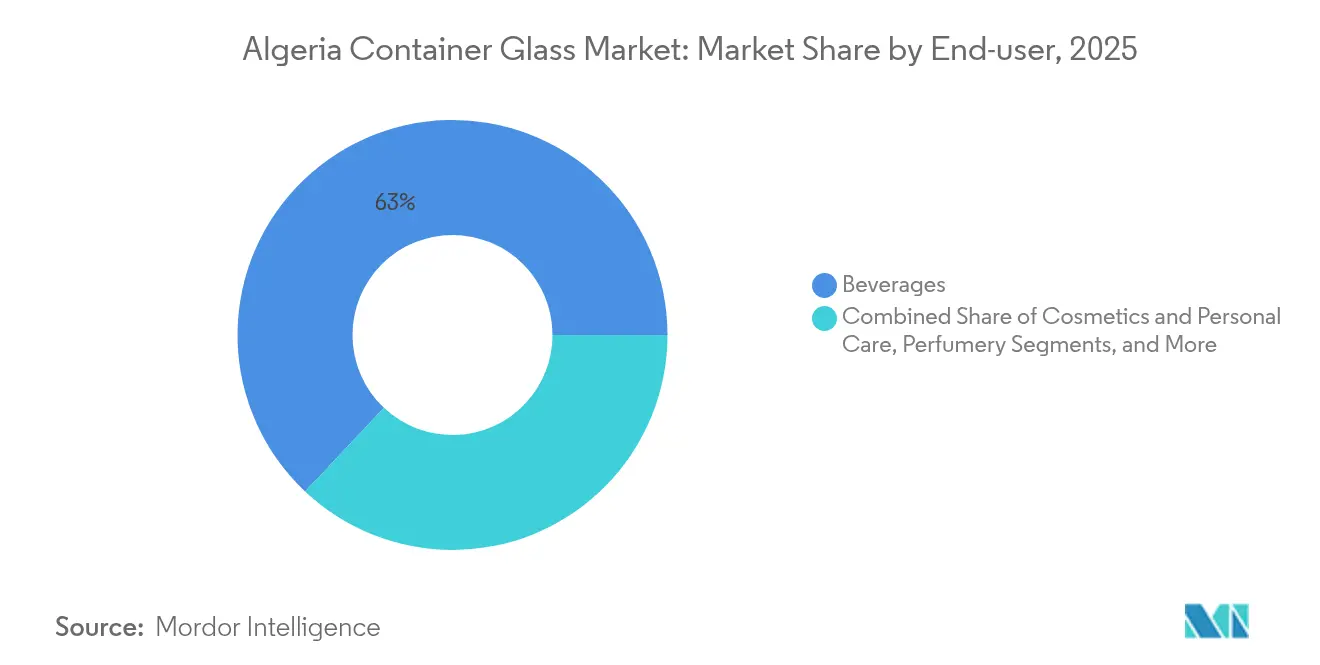

- By end-user, beverages captured 62.98% of the Algeria container glass market share in 2025.

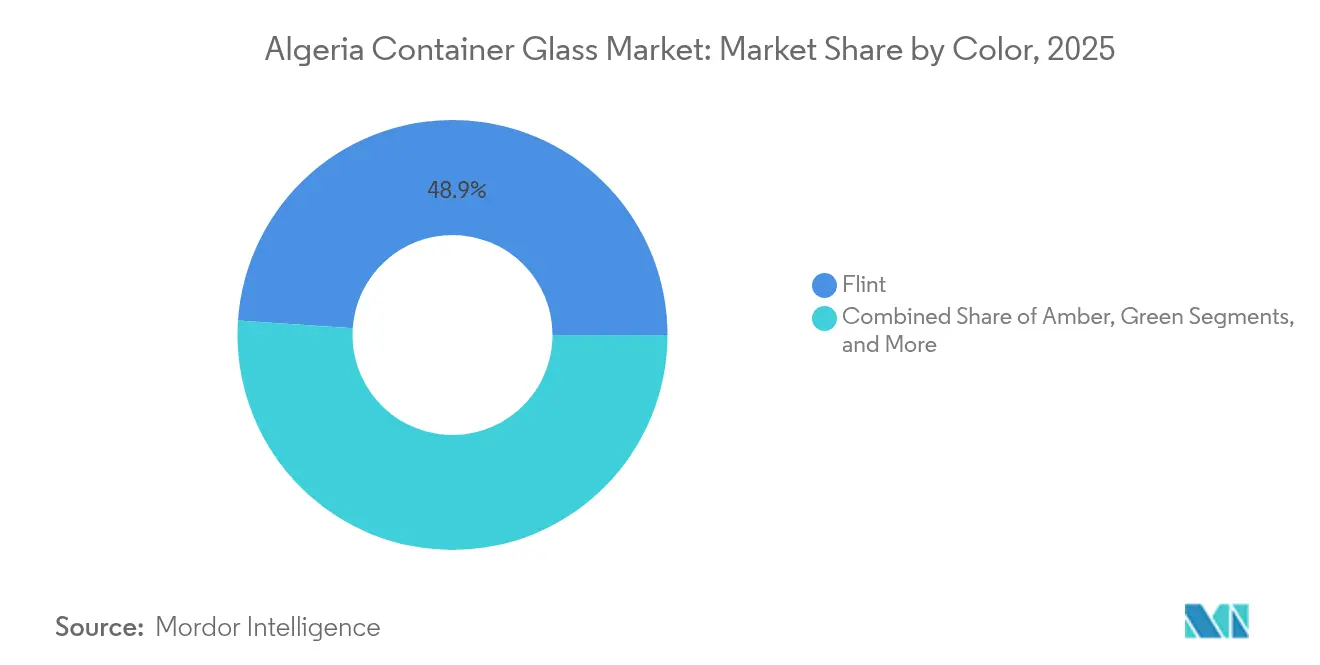

- By color, the Algeria container glass market for amber glass is projected to grow at a 7.28% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Algeria Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from beverage industry | +1.2% | National, concentrated in coastal urban centers | Medium term (2-4 years) |

| Government push for local container glass manufacturing | +0.8% | National, with priority zones in Chlef and Blida | Long term (≥ 4 years) |

| Strategic location boosts export potential | +0.6% | National, leveraging Mediterranean ports | Medium term (2-4 years) |

| Growing preference for sustainable and recyclable packaging | +0.9% | National, aligned with SNGID 2035 implementation | Long term (≥ 4 years) |

| Capacity expansion and modernization of furnaces | +0.7% | Regional, focused on existing production centers | Short term (≤ 2 years) |

| Halal-certified pharma packaging demand surge | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Beverage Industry

Algeria’s beverage sector drives container-glass demand through expanding mineral-water production and carbonated-beverage consumption, supported by urbanization rates reaching 74% and concentrated purchasing power in coastal cities such as Algiers, Oran, and Constantine. The sector benefits from Castel’s strategic repositioning, which reduces aluminum-can dependency for beer and plastic usage for fruit juices, by implementing bottle-return systems that align with circular economy principles. Recent automated bottling-line installations, including a 14,000-bottle-per-hour mineral water facility, demonstrate industry modernization trends favoring high-volume production capabilities. However, competition intensifies from PET packaging solutions, as evidenced by PRO-FORM Packaging’s expansion in eastern Algeria, targeting liquid-product applications with international-standard preform production. The beverage industry’s adoption of glass containers correlates with premium positioning strategies and sustainability messaging, creating differentiation opportunities against plastic alternatives in quality-conscious market segments.

Government Push for Local Container Glass Manufacturing

Algeria’s import-substitution strategy prioritizes local container-glass production through comprehensive investment incentives, including customs-duty exemptions for production equipment, VAT exemptions during project implementation, and corporate-tax holidays extending up to three years for qualifying manufacturers. The policy framework restricts foreign ownership in import-for-resale activities while encouraging 100% foreign ownership in manufacturing sectors, creating structural advantages for production-oriented glass-container enterprises over trading operations. AAPI’s one-stop investment-facilitation process streamlines permits and regulatory approvals, while state-land-concession mechanisms provide 33-year renewable terms for industrial projects, reducing capital requirements for greenfield glass-manufacturing facilities. The government’s preference for projects creating over 500 jobs and exceeding USD 63 million investment value aligns with large-scale glass-container production requirements, offering additional discretionary support for major industrial developments.

Strategic Location Boosting Export Potential

Algeria’s Mediterranean positioning provides direct access to European and North African markets, with established export channels demonstrated by USD 66.8 million in float-glass exports in 2022, ranking 25th globally. The country targets Spain (USD 32.9 million), Morocco (USD 16.1 million), and Tunisia (USD 10.0 million) as its primary destinations. The country’s port infrastructure comprises 45 commercial ports, with major facilities at Skikda, Béthioua, and the deep-water Djen Djen terminal. However, container throughput efficiency remains constrained by logistics performance indicators, ranking Algeria at 2.06 compared to regional peers, such as Tunisia, at 2.76. Export competitiveness benefits from subsidized energy costs, with natural gas priced at approximately USD 0.50 per MMBtu for domestic industrial use, significantly below international market rates, providing cost advantages for energy-intensive glass manufacturing. However, export growth faces headwinds from bureaucratic customs procedures, foreign-exchange controls that require one to six months for international transfers, and underdeveloped financial systems that limit access to trade-financing mechanisms.

Growing Preference for Sustainable and Recyclable Packaging

Algeria’s circular-economy transition, formalized through the National Integrated Waste Management Strategy (SNGID 2035), creates regulatory momentum favoring the infinite recyclability of glass containers over single-use plastic alternatives. The sustainability imperative gains urgency as domestic waste generation reaches 13 million tonnes annually, with 27.72% comprising plastic materials and 59% of plastic waste originating from packaging applications, highlighting the role of glass containers in waste-reduction strategies. Corporate environmental responsibility initiatives, prominently featured at the 2024 Plast and PrintPack Algeria conference, emphasize eco-design principles and sustainable packaging best practices, creating market pull for glass containers among environmentally conscious brands. Extended-Producer-Responsibility concepts, including the stalled Eco-Jem tax on containers introduced in 2004, signal potential future cost internalization for packaging-waste management, which favors the superior recyclability profile of glass containers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy costs and unstable supply impacting production | -0.9% | National, affecting all production centers | Medium term (2-4 years) |

| Heavy dependence on imported raw materials | -0.7% | National, concentrated at port entry points | Long term (≥ 4 years) |

| Transport and port infrastructure bottlenecks | -0.5% | Regional, affecting export-oriented facilities | Medium term (2-4 years) |

| Competition from low-cost plastic and metal packaging | -1.1% | National, intensifying in cost-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Costs and Unstable Supply Impacting Production

Algeria’s energy sector faces structural challenges, despite its abundant natural-gas reserves. Domestic gas consumption for electricity generation exceeds 40% of total production, and planned gas-fired capacity expansion is set to reach 36 GW by 2028, creating potential supply constraints for industrial users. The government’s energy-subsidy burden exceeds USD 8 billion annually (over 4% of GDP), with gas subsidies representing approximately 50% of this cost, creating fiscal pressures that may trigger subsidy reforms affecting industrial-energy pricing. The energy intensity of container-glass manufacturing, which requires continuous furnace operations at temperatures exceeding 1,500 °C, makes the sector particularly vulnerable to energy-price volatility and supply disruptions that could impact production scheduling and cost competitiveness. Export commitments to European markets, intensified following the Ukraine conflict, have led to Italy importing an additional 4 billion cubic meters in 2022, competing with domestic industrial allocation and potentially prioritizing export revenues over local manufacturing needs.[2]Pao-Yu Oei, “Fossil Gas Lock-in Risks: Analysis of Algeria’s Electricity Sector,” springer.com

Competition from Low-Cost Plastic and Metal Packaging

Algeria’s packaging sector is demonstrating accelerating investment in plastic alternatives, with EUR 127 million allocated to packaging technologies in 2022, positioning the country among Africa’s largest investors in packaging technology, alongside Nigeria, South Africa, and Egypt. Plastic-packaging infrastructure expansion includes domestic PET-preform production capabilities through companies such as PRO-FORM Packaging, reducing import dependence and improving cost competitiveness against glass containers in price-sensitive applications. The competitive pressure intensifies as plastic raw material imports grow from 304 kilotons in 2007 to over 1,000 kilotons in 2023, valued at more than USD 2 billion, indicating substantial scale economies in plastic packaging supply chains. Metal-packaging alternatives benefit from established aluminum supply chains through ArcelorMittal and Tosyalı operations, providing cost-effective solutions for beverage applications where glass containers face weight and transportation-cost disadvantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Market Leadership

The beverage segment commands 62.98% market share in 2025, reflecting Algeria’s expanding consumption of packaged drinks driven by urbanization and rising disposable income in coastal metropolitan areas. Within the beverage industry, alcoholic applications benefit from Castel’s strategic shift toward glass packaging, which reduces aluminum can dependency for beer production. Meanwhile, non-alcoholic segments capitalize on growing mineral water consumption and demand for carbonated soft drinks. The cosmetics and personal-care segment emerges as the fastest-growing application, with a 7.11% CAGR through 2031, driven by premiumization trends and a preference for glass packaging’s barrier properties in perfumery and high-value personal-care products.

Food applications, including jams, jellies, honey, condiments, and pickles, maintain steady demand, supported by domestic food-processing expansion and export-oriented packaging requirements for traditional Algerian products targeting diaspora markets in Europe. Pharmaceutical packaging represents a specialized niche served primarily by NOVER’s dedicated production lines, although growth remains constrained by regulatory requirements and competition from specialized pharmaceutical glass manufacturers. The perfumery segment benefits from Algeria’s position in the Mediterranean fragrance supply chain, with glass containers being preferred for their premium positioning and product protection requirements in international markets.

By Color: Flint Glass Dominance Faces Amber Acceleration

Flint glass maintains its market leadership with a 48.92% share in 2025, driven by its versatility across beverage, food, and cosmetic applications, where transparency and a neutral appearance support product visibility and brand presentation. The segment’s dominance reflects its broad applicability across end-user categories, particularly in mineral water, carbonated beverages, and clear spirit applications, where product clarity enhances consumer appeal. Amber glass exhibits the highest growth trajectory, with a 7.28% CAGR through 2031, benefiting from pharmaceutical applications that require UV protection and premium beer packaging, where light protection preserves product quality and extends shelf life.

Green glass applications focus primarily on wine and specialty-beverage packaging, maintaining stable demand despite limited growth potential in Algeria’s predominantly Muslim market context. The segment benefits from export opportunities targeting European wine markets and traditional glass-bottle applications in olive oil and specialty food products. Other colors, including cobalt blue and specialty tints, serve niche applications in cosmetics, perfumery, and premium packaging segments, although volume remains limited by specialized production requirements and higher manufacturing costs compared to standard-color formulations.

Geography Analysis

Algeria’s domestic container-glass market benefits from concentrated demand in northern coastal regions, where 74% urbanization rates and proximity to major ports create favorable logistics for both raw material imports and finished product distribution. The Blida-Algiers corridor emerges as the primary production hub, hosting Mediterranean Float Glass’s 30-hectare facility and benefiting from proximity to the capital’s consumer markets and Algiers port for export access.

The Chlef region gains prominence through NOVER’s pharmaceutical-glass specialization and recent furnace modernization by Falorni Tech, targeting a daily capacity of 50 tonnes for tableware and container applications. Regional development patterns favor locations with access to local silica-sand deposits, as demonstrated by NOVER’s site selection in Chlef’s industrial zone, approximately 70 kilometers from Ténès port and positioned along the RN4 Algiers-Oran highway for efficient logistics. Eastern regions, including Constantine and Souk Ahras, host smaller glass operations, such as Verrerie Silice International and Cedar Glass.

However, production focuses primarily on flat glass and specialty applications rather than container-glass manufacturing. The geographic distribution reflects infrastructure constraints and energy-access patterns, with coastal regions benefiting from natural-gas pipeline networks and port connectivity, which is essential for raw-material imports and access to export markets.

Competitive Landscape

Algeria’s container-glass market exhibits moderate fragmentation with a mix of state-owned enterprises, private domestic companies, and emerging foreign investment creating competitive dynamics across different market segments. Market concentration centers around established players such as ALVER (now under Castel ownership), Mediterranean Float Glass (Cevital Group), and state-owned NOVER and AFRICAVER, while smaller regional producers serve specialized applications and local markets.

The competitive environment benefits from government import-substitution policies that favor domestic production over imports, creating protective conditions for local manufacturers while encouraging investments in capacity expansion and modernization. Strategic differentiation emerges through specialization patterns, with NOVER focusing on pharmaceutical-glass packaging, Mediterranean Float Glass dominating flat glass with container-glass capabilities, and ALVER targeting beverage applications under Castel’s sustainability-focused strategy, which emphasizes bottle-return systems and reduced plastic packaging.

Technology adoption accelerates through foreign partnerships, exemplified by Falorni Tech’s furnace-refurbishment projects and potential Chinese investment through Kibing Group’s proposed solar-glass facility, indicating opportunities for knowledge transfer and modernization trends. White-space opportunities exist in premium packaging segments, export market development, and circular economy applications. Meanwhile, regulatory compliance requirements under Algeria’s investment law create barriers to entry that protect established players with proper licensing and environmental approvals.

Algeria Container Glass Industry Leaders

Société Algérienne des Verres, SpA (ALVER)

Nouvelle Verrerie de Chlef, SpA

INTER GLASS, Sarl.

Feemio Group Co., Ltd.

Changsha Kotto Glass Industrial Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kibing Group presented a proposal to Algeria’s Ministry of Energy for a 1.53 million-tonne annual-capacity solar-glass manufacturing facility, including an integrated 1.08 million-tonne ultrapure silica sand processing unit. The project is expected to create 3,000 direct jobs and achieve 90% local integration rates.

- December 2024: STM Pack delivered a complete automated mineral-water bottling line in Algeria with 14,000 bottles-per-hour capacity, featuring PET stretch-blow molding through palletization for still-water production targeting growing demand for high-quality bottled water.

- November 2024: Algeria’s solar-energy sector gained momentum, with 437 MW of installed capacity and awarded projects totaling approximately EUR 1.8 billion in investment, creating potential demand for solar-glass applications as the country develops its renewable-energy manufacturing capabilities.

- March 2024: Falorni Tech completed refurbishment of NOVER’s tableware furnace in Chlef, achieving the target output capacity of 50 tons per day for press-produced soda-lime tableware glass, with operations becoming fully operational before the end of 2024 \.

Algeria Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Algeria container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the projected demand for container glass in Algeria by 2031?

Total demand is forecast to reach 232.57 kilotons by 2031, rising from 181.36 kilotons in 2026 at a 5.09% CAGR.

How fast is the beverage segment growing within Algeria’s container-glass space?

Beverage applications already command 62.98% share in 2025 and continue to scale as mineral-water and carbonated-drink lines expand nationwide.

Why do Algerian producers enjoy a cost advantage over foreign competitors?

Industrial electricity averages USD 0.03 per kWh and natural gas about USD 0.50 per MMBtu, keeping furnace energy costs well below global norms.

Which glass color is expanding the quickest among Algerian manufacturers?

Amber containers drive growth at a 7.28% CAGR through 2031, supported by demand for UV-sensitive pharmaceuticals and premium beer packaging.

What investment incentives support new container-glass plants in Algeria?

The AAPI grants customs-duty and VAT exemptions plus up to three-year corporate-tax holidays for projects exceeding USD 63 million and creating at least 500 jobs.

How do sustainability policies influence packaging choices in Algeria?

The SNGID 2035 framework prioritizes recyclability, prompting brand owners to adopt reusable glass bottles and curb single-use plastics.

Page last updated on: