Iceland Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

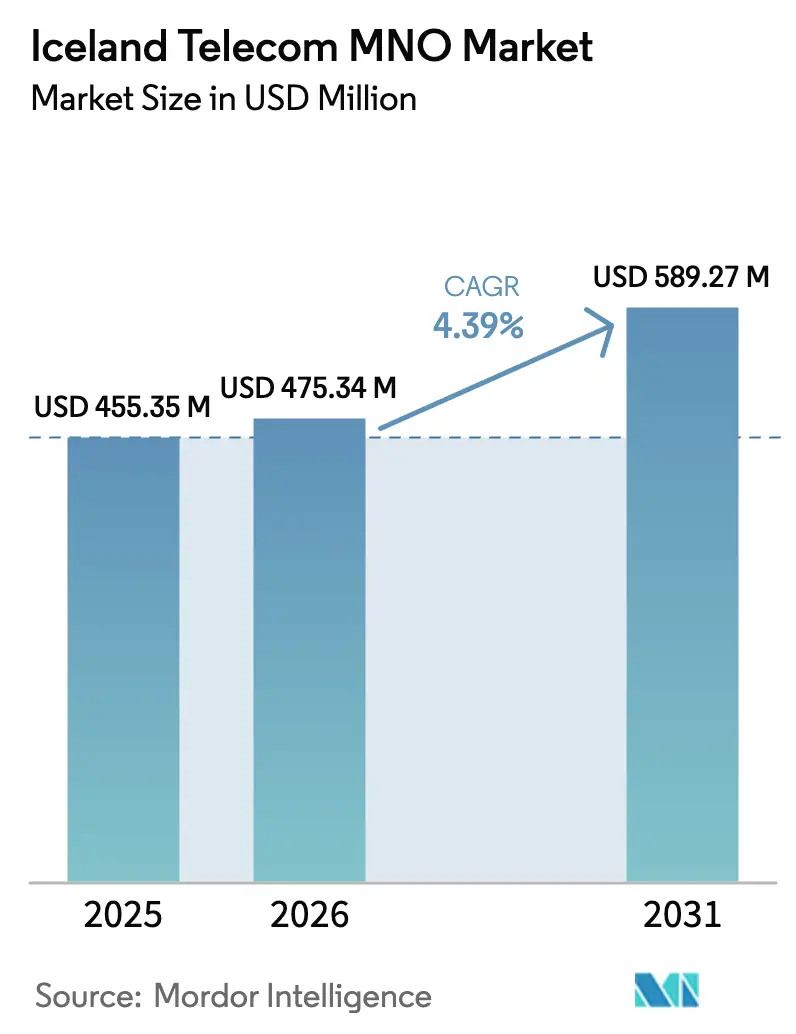

| Base Year Market Size (2025) | USD 455.35 Million |

| Market Size (2026) | USD 475.34 Million |

| Market Size (2031) | USD 589.27 Million |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

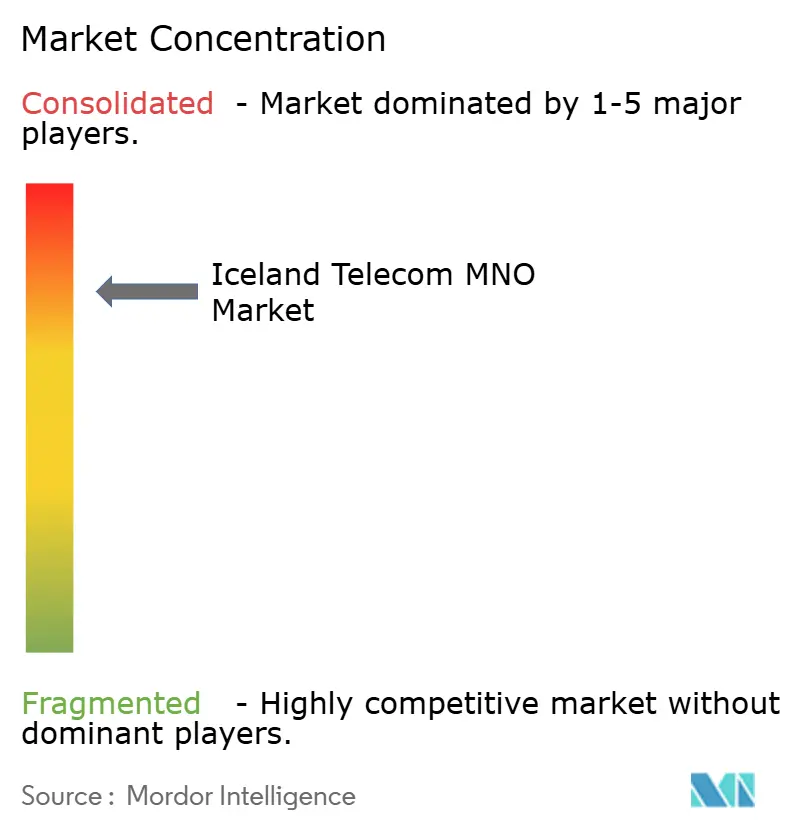

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iceland Telecom MNO Market Analysis by Mordor Intelligence

The Iceland Telecom MNO Market size is expected to grow from USD 455.35 million in 2025 to USD 475.34 million in 2026 and is forecast to reach USD 589.27 million by 2031 at 4.39% CAGR over 2026-2031.

Rising 5G coverage, fast-growing IoT connections, and sustained mobile-data appetite underpin this expansion. Operators are retiring 2G/3G networks by the end of 2025 to recycle spectrum for low-latency services, while fiber backhaul—present in 91% of premises—supports seamless fixed-mobile convergence. Enterprise demand for managed connectivity, cybersecurity, and edge solutions strengthens long-term revenue visibility, even as wholesale price caps keep consumer tariffs in check. Strategic investments such as the IRIS submarine cable bolster Iceland’s role as a renewable-energy data-center hub, attracting global players that need green compute capacity. Conversely, sparse population density elevates per-capita CAPEX and forces operators to innovate around site-sharing and vendor financing to protect margins.

Key Report Takeaways

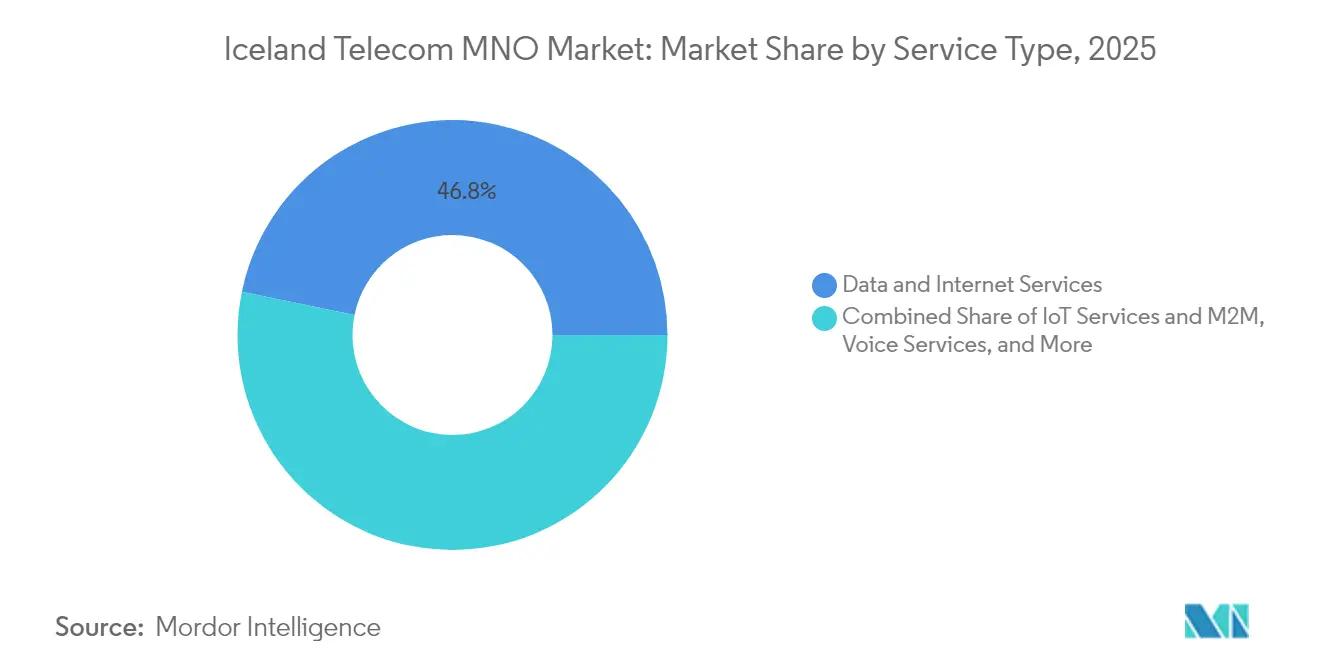

- By service type, data and internet services led with 46.78% revenue share in 2025, while IoT and M2M services are projected to expand at a 4.64% CAGR through 2031.

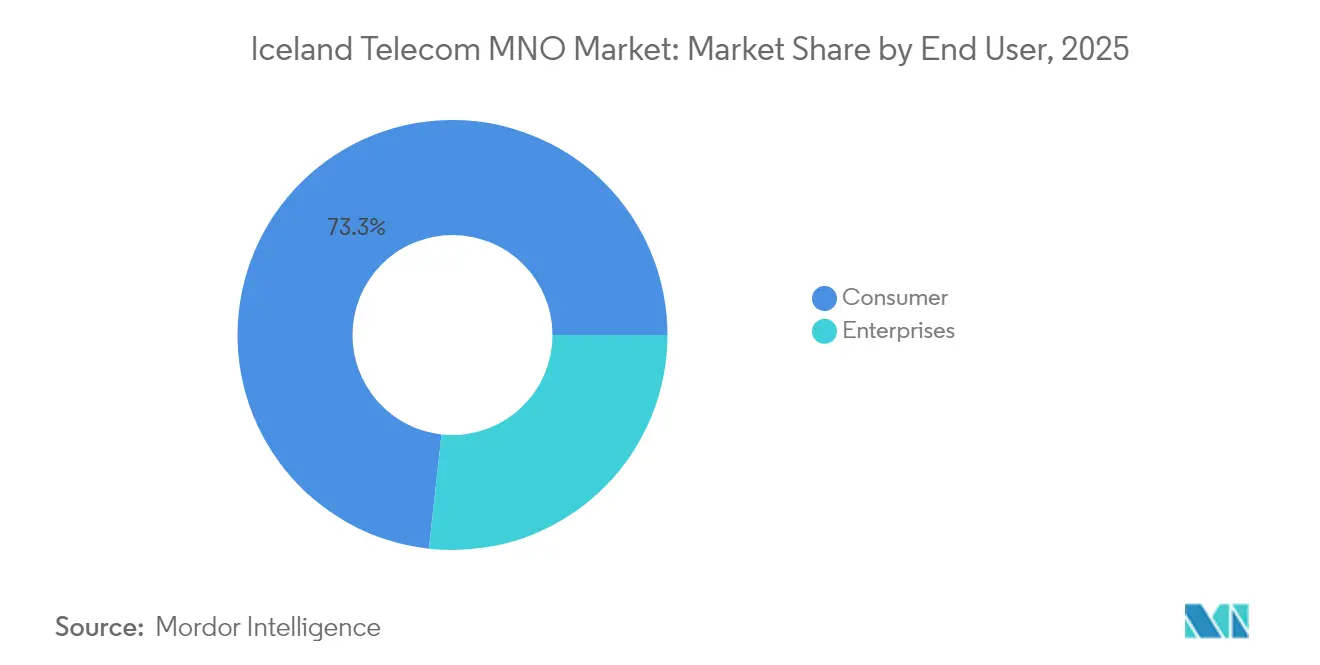

- By end-user, the consumer segment held 73.25% of the Iceland telecom MNO market share in 2025; enterprise connections are advancing at a 4.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iceland Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G network rollout and infrastructure modernization | +1.2% | National, priority in Capital Region | Medium term (2-4 years) |

| Growing IoT and M2M service adoption | +0.8% | National, industrial and smart-city hubs | Long term (≥ 4 years) |

| Increasing mobile-data consumption | +0.7% | National, consumer and enterprise users | Short term (≤ 2 years) |

| Digital transformation in the enterprise sector | +0.6% | National, government-led demand | Medium term (2-4 years) |

| Government Digital Iceland initiative | +0.5% | National, public-service digitalization | Long term (≥ 4 years) |

| Tourism recovery driving roaming revenue | +0.4% | National, seasonal peak in summer | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G network rollout and infrastructure modernization

Operators are fast-tracking 5G to replace costly legacy layers. Síminn and Ericsson plan 90% population coverage by mid-2025, and Nova already delivers gigabit speeds in Vestmannaeyjar. [1]Ericsson, “Síminn Selects Ericsson for Nationwide 5G,” ericsson.com More than 12,000 5G coverage areas were lit in six months, a tenfold leap that frees spectrum for ultra-low-latency enterprise use cases. Closing 2G/3G networks cuts energy costs and simplifies operations, allowing carriers to redirect OPEX toward densifying small-cell sites that serve smart-factory, mining, and maritime applications. Early 5G movers gain pricing power in enterprise deals and position Iceland as an Arctic test bed for trans-Atlantic connectivity pilots.

Growing IoT and M2M service adoption

With 109 machine-SIMs per 100 inhabitants, Iceland ranks among the world’s most connected societies. Utilities deploy sensors across geothermal plants, while fisheries monitor vessel routes in real time to comply with quota rules. Reykjavik’s smart-city roadmap uses cellular nodes for adaptive lighting and congestion analytics, and aluminum smelters contract premium links for predictive-maintenance data. Government procurement under the Digital Iceland framework ensures multiyear connectivity volumes, supporting carrier revenue certainty. The 5G-plus-fiber footprint lures overseas vendors seeking low-carbon edge locations, expanding wholesale traffic and partnership income.

Increasing mobile-data consumption

Average mobile usage doubled in two years to 17 GB per subscriber by June 2024, far above the Nordic mean.[2]OECD, “Fixed and Mobile Broadband Indicators 2024,” oecd.org Long winters encourage video streaming and gaming indoors, while near-universal fiber enables off-loading that keeps latency low for cloud collaboration. Tourism adds large-volume spikes: 460,000 foreign visitors in 1Q 2024 generated higher roaming earnings despite shorter stays. Enterprises running cloud-first operations backhaul workloads through Icelandic data centers, reinforcing capacity requirements on both macro and small-cell layers. Operators monetize traffic through tiered-speed plans but must continually tune spectrum assets to avoid congestion in high-footfall tourist zones.

Digital transformation in the enterprise sector

The Digital Iceland mandate requires agencies to shift all citizen interactions online, incentivizing private firms to modernize their workflows. [3]Digital Iceland, “Strategy 2025,” island.isSMEs in fisheries, travel, and renewable energy adopt SaaS platforms that rely on secure mobile links for remote crews. The 2024 corporate tax rise to 21% intensifies focus on efficiency, pushing businesses toward IoT-enabled asset tracking and AI-driven analytics. Foreign hyperscalers pick Iceland for green compute clusters and demand redundant 10-Gbps mobile back-up paths, which lift ARPU. Cross-selling of managed firewalls and SD-WAN solutions deepens carrier wallet share and locks in long-term contracts.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High network CAPEX per capita from sparse population and rugged terrain | -0.9% | National, acute in rural interiors | Long term (≥ 4 years) |

| Regulatory wholesale-price caps compressing margins | -0.6% | National, all operators | Medium term (2-4 years) |

| Limited sub-1 GHz spectrum hampering indoor coverage quality | -0.4% | National, dense urban zones | Medium term (2-4 years) |

| Small addressable market restricts economies of scale for vendors | -0.3% | National, vendor negotiations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High network CAPEX per capita from sparse population and rugged terrain

Just 3.6 residents per km² force carriers to spread towers across glaciers, lava fields, and fjords. Ruggedized hardware that withstands sub-zero winds inflates site costs, and helicopter logistics add further premiums. Síminn’s effort to push 5G to 90% of people therefore absorbs more capital per user than in any OECD peer. Ongoing maintenance is costly because storms and volcanic ash accelerate equipment wear. The burden weighs heaviest on Sýn, the smallest operator, raising consolidation speculation if funding gaps widen.

Regulatory wholesale-price caps compressing margins

The Post and Telecom Administration limits wholesale tariffs to foster competition, yet the rulebook pares revenue per bit at a time when 5G radio purchases peak. Operators cannot offset CAPEX through premium resale channels and must rely on consumer upselling and enterprise bundles to defend EBITDA. The 2024 tax hike further narrows net profit, pressuring boards to delay rural upgrades unless subsidies improve. Persistent cap compression could slow innovation and stretch payback periods for next-generation stand-alone 5G cores.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Dominate While IoT Accelerates

Data and internet services accounted for 46.78% of the Iceland telecom MNO market size in 2025, powered by higher video traffic and fixed-mobile substitution. Voice revenue stays resilient as carriers shift users to VoLTE packages that improve call quality without extra spectrum needs. Messaging continues to erode under OTT pressure, though bundled SMS in enterprise plans softens the decline. IoT and M2M subscriptions recorded the fastest 4.64% CAGR and are forecast to expand their contribution to 9.3% of the Iceland telecom MNO market by 2031, underpinned by connected-vessel monitoring and geothermal-plant telemetry.

The planned retirement of 2G/3G networks by end-2025 funnels all traffic onto LTE and 5G layers, simplifying cost structures and allowing premium pricing for guaranteed-throughput tiers. Operators experiment with network slicing for industrial customers, opening new monetization levers absent in consumer plans. OTT and PayTV services ride on nationwide fiber backhaul to deliver 4K streams, helping carriers bundle mobile with home entertainment for churn reduction. VAS offerings such as device insurance and identity management unlock incremental margins in a low-growth voice environment.

By End-User: Enterprise Momentum Outpaces Household Growth

Enterprises generated 26.75% of 2025 revenue but are projected to grow at 4.86% CAGR, eclipsing consumer growth despite the latter’s 73.25% share. Corporates value SLA-backed throughput, dual-link redundancy, and managed IoT stacks, enabling ARPU that is 3.2 times higher than the consumer average. The Digital Iceland program forces public bodies to adopt e-service platforms, creating anchor contracts for carriers supplying secure VPNs and M2M SIM fleets.

The Iceland telecom MNO market share of the consumer base is stable because population growth plateaued at 2.3% in 2024, and mobile penetration already exceeds 120%. Yet usage per line keeps rising; doubling of data volumes lifted blended ARPU by 4% in 2024 even without subscriber gains. Tourism-driven prepaid volumes add seasonal spikes that offset winter slowdowns. Consumer plans increasingly bundle streaming perks and international roaming, exploiting Iceland’s role as a stop-over hub between North America and Europe.

Geography Analysis

The entire country functions as a single licensing zone, but revenue density varies sharply. The Capital Region houses 64% of inhabitants and commands more than 60.12% of the Iceland telecom MNO market size in 2025, aided by dense small-cell layers that deliver sub-10 ms latency for fintech and media firms. Southwest corridors following the new Reykjanes highway saw 4.1% population growth and rapid suburban housing, opening corridors for 26 GHz millimeter-wave deployments that offload macro traffic.

Rural municipalities in the Westfjords and Eastfjords face depopulation, yet universal-service rules oblige carriers to maintain coverage. Microwave backhaul and satellite back-up links raise opex, and carriers negotiate cost-sharing to keep tariffs flat. Harsh weather narrows construction windows to summer months, forcing agile build planning and stockpiling of ruggedized radios that can operate at –40 °C.

Iceland’s mid-Atlantic location drives hefty investment in subsea cables such as IRIS, delivering 48 Tbps capacity to Ireland by 2026 and reinforcing the nation’s position as a renewable-powered data-center bridge between continents. Seasonal tourism flows concentrate demand in the Golden Circle, prompting temporary small-cell on wheels each June-August to prevent congestion. Winter shifts usage indoors, boosting indoor-coverage upgrades that rely on scarce sub-1 GHz spectrum.

Competitive Landscape

Competition centers on three national operators—Síminn hf., Nova, and Sýn hf.—that collectively control the radio-access market. Nova led mobile-internet traffic with 60.3% in 2021 thanks to early unlimited-data tariffs and extensive 3.5 GHz holdings. Síminn leverages its fixed-line dominance to bundle fiber and mobile, targeting enterprise contracts with Ericsson-built 5G slicing. Sýn focuses on content-driven bundles, partnering with streaming platforms to lift ARPU and reduce churn.

Infrastructure modernisation dictates strategic positioning. Síminn’s five-year Ericsson deal modernizes 4G and accelerates 5G roll-out to 90% of residents by mid-2025. Nova trials non-terrestrial network integrations to provide maritime coverage for the fishing fleet, while Sýn explores Open-RAN for cost efficiency.

Price competition is restricted by PTA wholesale caps, so operators differentiate via quality-of-service, value-added security, and co-innovation with data-center tenants. All three pursue green energy branding, aiming to power radio sites entirely with geothermal or hydroelectricity by 2027. Vendor partnerships extend to Nokia for core upgrades and to tower-sharing consortiums that lower rural build costs.

Iceland Telecom MNO Industry Leaders

Siminn hf.

Syn hf.

NOVA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nova unveiled high-speed business packages combining fiber, 4.5G, and 5G connectivity, plus VoLTE and VoWiFi, tailored for cloud-native enterprises.

- September 2024: Borealis Data Center and Modularity agreed to build a geothermal-powered AI campus and submarine-cable hub, first phase operational 2026.

- May 2024: Government confirmed the nationwide switch-off of 2G/3G networks by end-2025 to free spectrum for advanced services.

- February 2024: Farice signed a joint-marketing accord with Far North Digital to extend the IRIS link toward Japan via an Arctic route, enhancing trans-polar capacity.

Iceland Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.The Telecom Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. Several factors, including an increasing demand for 5G, are likely to drive the adoption of telecom services.

The Iceland telecom MNO market is segmented by services (voice services (wired, wireless), data and messaging services, OTT and PayTV services). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large will the Iceland telecom MNO market be in 2031?

It is projected to reach USD 589.27 million, expanding at a 4.39% CAGR during 2026-2031.

What segment is growing fastest in Iceland’s mobile market?

IoT and M2M services, forecast to post a 4.64% CAGR through 2031 on 5G and industrial demand.

When will Iceland shut down legacy mobile networks?

The government has mandated a nationwide 2G/3G shutdown by the end of 2025 to free spectrum for 5G.

What geographic area drives the most telecom revenue?

The Capital Region around Reykjavik accounts for more than 60.12% of market revenue in 2025 due to high population density and fiber coverage.

How is Iceland improving international connectivity?

The IRIS submarine cable to Ireland, due 2026, will add 48 Tbps of capacity and support the country’s data-center expansion.

Page last updated on: