Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 18.64 Billion |

| Market Size (2026) | USD 19.27 Billion |

| Market Size (2031) | USD 22.77 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Telecom MNO Market Analysis by Mordor Intelligence

Italy Telecom MNO Market size in 2026 is estimated at USD 19.27 billion, growing from 2025 value of USD 18.64 billion with 2031 projections showing USD 22.77 billion, growing at 3.39% CAGR over 2026-2031.

This uptrend stems from rising data consumption, expanding 5G coverage, government-backed fiber rollouts, and the shift toward converged fixed-mobile offerings. Consolidation moves, notably Swisscom’s EUR 8 billion (USD 9.22 billion) purchase of Vodafone Italia and KKR’s EUR 18.8 billion (USD 21.66 billion) acquisition of TIM’s NetCo, are reshaping the competitive landscape, improving capital efficiency, and stabilizing average revenue per user. Data and Internet services command the largest revenue share, while IoT connections and enterprise digitalization propel incremental growth. Operators are trimming energy bills through tower sharing and renewable sourcing, easing pressure from high electricity prices. Overall, a maturing yet reforming environment positions the Italy Telecom MNO market for steady, value-focused expansion.

Key Report Takeaways

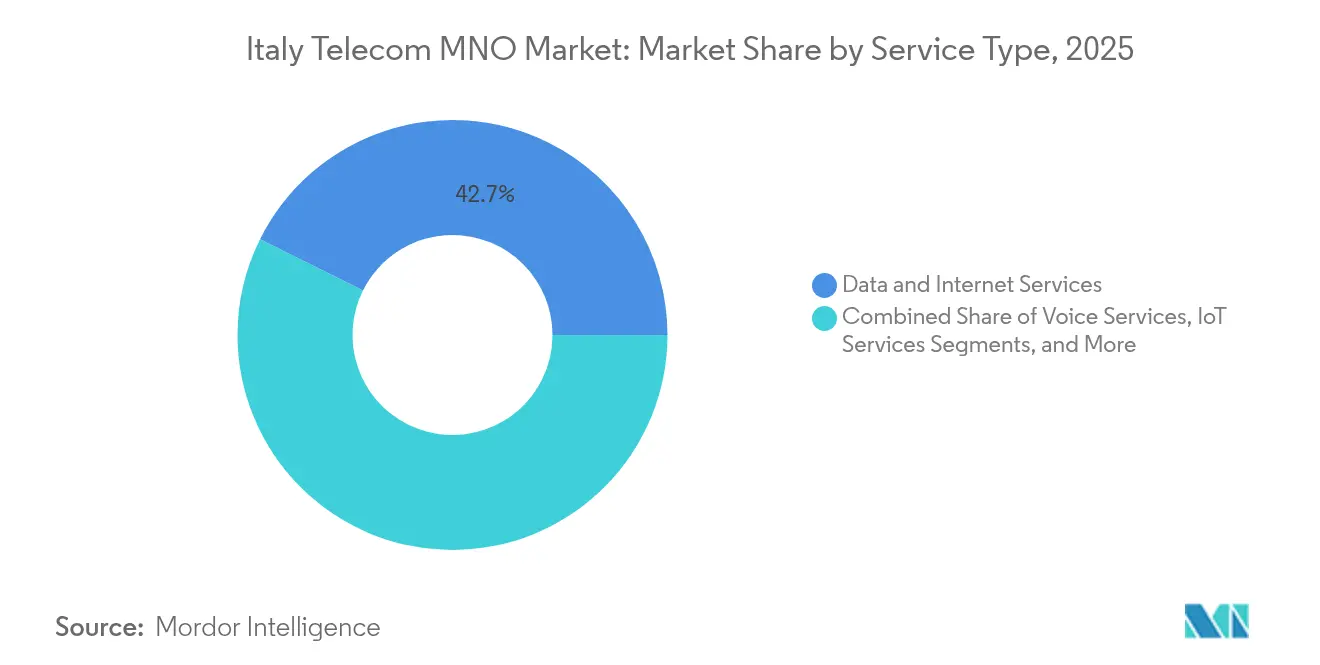

- Data and Internet services led with 42.65% revenue share in 2025, while IoT and M2M services are projected to expand at a 3.46% CAGR to 2031, underscoring the data-centric trajectory of the Italy Telecom MNO market.

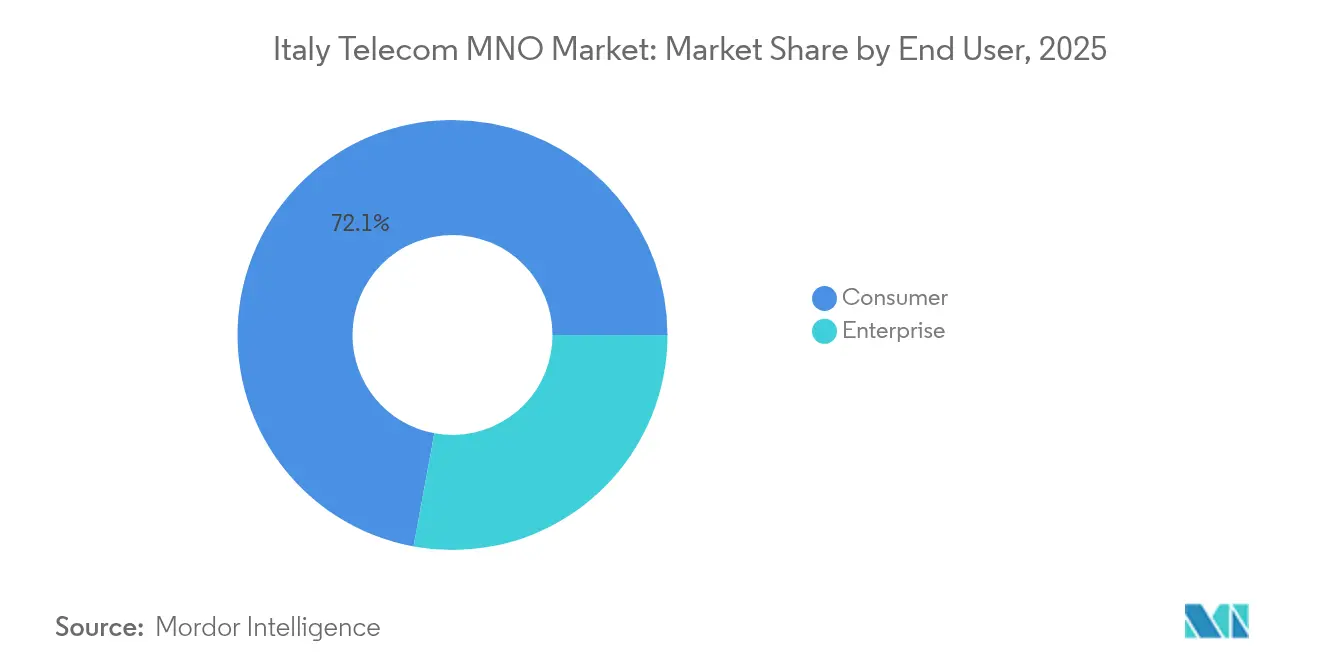

- The consumer segment held 72.10% of Italy Telecom MNO market share in 2025, whereas the enterprise segment is forecast to post the fastest growth at 3.72% CAGR through 2031, buoyed by industrial automation and cloud adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing 5G subscriber uptake | +1.2% | National, early gains in Milan, Rome, Naples | Medium term (2-4 years) |

| Convergent bundles sustaining ARPU | +0.8% | National, stronger in northern regions | Short term (≤ 2 years) |

| Govt. Italia a 1 Gbps FTTH funding | +0.6% | Rural south and underserved areas | Long term (≥ 4 years) |

| Rising enterprise IoT connectivity demand | +0.9% | Industrial north, expanding centrally | Medium term (2-4 years) |

| Surge in OTT video boosting data usage | +0.7% | National, urban concentration | Short term (≤ 2 years) |

| Tower sharing and NaaS lowering capex | +0.4% | Nationwide networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing 5G Subscriber Uptake

5G population coverage already exceeds 90%, placing Italy among the EU front-runners for next-generation access. TIM plans to raise outdoor 5G coverage to 95% by 2026, cutting cost per gigabyte by up to 50% compared with 4G operations. National Recovery and Resilience Plan (NRRP) funds worth EUR 2.02 billion (USD 2.33 billion) subsidize backhaul fiber to 21,900 radio sites, closing gaps where commercial returns are weak.[1]Digital Watch Observatory, “Italy 5G plan,” dig.watch Private 5G networks are gaining traction in factories and ports, raising data intensity and service revenues. Wider 5G adoption will therefore keep the Italy Telecom MNO market on a higher growth slope.

Convergent Bundles Sustaining ARPU

Bundling fixed broadband, mobile service, and content is lifting customer stickiness and supporting average revenue levels, particularly in affluent northern provinces. The Fastweb–Vodafone tie-up promises nationwide, converged propositions that reduce churn and spur cross-sell uptake. Operators leverage fiber footprints to upsell premium mobile data plans, limiting tariff erosion. Early success stories in Milan show a 10 percentage-point uplift in multi-play take-up when fiber and 5G are jointly promoted. Such dynamics keep the Italy Telecom MNO market on a value rather than volume footing.

Govt. Italia a 1 Gbps FTTH Funding

The Italia a 1 Gbps scheme targets universal gigabit-class connectivity by 2026, ahead of EU 2030 objectives. Open Fiber and FiberCop lead rollouts, with 40% of funds earmarked for southern regions to close the digital divide. Wholesale-only access terms encourage MNOs to introduce fiber-linked 5G and fixed-wireless access (FWA). This long-term subsidy raises addressable bandwidth and improves customer experience, underpinning the growth outlook for the Italy Telecom MNO market.

Rising Enterprise IoT Connectivity Demand

The Italian IoT sector generated EUR 8.9 billion (USD 10.25 billion) in 2023, logging 9% annual expansion with 41 million cellular connections. Industrial hubs in Lombardy and Emilia-Romagna deploy private 5G and NB-IoT solutions for robotics, asset tracking, and predictive maintenance. TIM Enterprise aims to double its ICT revenue share to 21% by 2026 by combining connectivity with cloud and cybersecurity offers. This enterprise digitization wave lifts high-margin service uptake and reinforces overall market resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense MNO price wars compressing margins | -0.9% | National, mainly mobile | Short term (≤ 2 years) |

| Regulatory cuts to mobile termination rates | -0.4% | National framework | Medium term (2-4 years) |

| Rural south fiber take-up lag | -0.3% | Southern regions | Long term (≥ 4 years) |

| High network energy costs vs. green targets | -0.5% | National operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense MNO Price Wars Compressing Margins

Fierce tariff battles since Iliad’s 2018 arrival sliced mobile ARPU and pushed churn upward. Although consolidation is reducing head-to-head discounts, entry-level offers remain aggressive, especially in prepaid segments. Operators respond with upsell tactics such as content bundles and speed tiers. Near-term profitability pressure, therefore, reduces the Italy Telecom MNO market CAGR by almost one percentage point until price equilibrium is reached.

High Network Energy Costs vs. Green Targets

Electricity accounts for a double-digit share of operating expenses, and Italy’s high-power prices tighten cost control. TIM reduced energy use by 28% and increased renewable sourcing to 65% by 2025, while INWIT launched a EUR 100 million (USD 115.21 million) solar program across its tower sites.[2]TowerXchange, “News: INWIT to develop telecommunications infrastructure with EIB financing,” towerxchange.com Network densification for 5G increases power consumption, prompting carriers to adopt more efficient radio units and shared passive infrastructure. Persistently high electricity pricing, therefore, tempers the profitability upside of the Italy Telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Use Dominates, IoT Accelerates

Data and Internet services represented the largest revenue slice, capturing 42.65% of Italy Telecom MNO market share in 2025. IoT and M2M solutions, while still small in absolute terms, deliver the highest 3.46% CAGR, underpinned by industrial automation and smart-city projects. The Italy Telecom MNO market size for data-centric services will expand steadily as streaming, cloud gaming, and remote work heighten gigabyte consumption. Declining voice and SMS uptake continues to free network capacity for richer data packages, while OTT messaging tightens pressure on legacy revenues. Operators monetize traffic growth through speed-tiered 5G plans and content tie-ups with Netflix, Amazon, and DAZN, strengthening average spending levels. Fixed-mobile convergence further cements data dominance by marrying fiber backhaul with 5G spectrum, ensuring robust user experience across devices.

Messaging and traditional voice revenues keep sliding because WhatsApp, Telegram, and similar applications meet most consumer needs at negligible incremental cost. Nonetheless, operators are leveraging rich communication services (RCS) and 5G standalone capabilities to introduce low-latency enterprise voice over New Radio (VoNR) and mission-critical push-to-talk. The Italy Telecom MNO market size, aligned with IoT gains, is expected to experience momentum in sectors such as logistics, smart agriculture, and utilities, where wide-area NB-IoT coverage provides economical and battery-efficient connectivity. Overall, service diversification based on data ecosystems will outweigh the contraction of legacy revenue lines and secure a balanced growth mix.

By End User: Consumers Still Rule, Enterprise Gains Speed

Consumers accounted for 72.10% of total revenue in 2025, retaining the bulk of SIM bases and broadband subscriptions. Attractive family bundles, handset financing, and rising video usage keep consumer lines stable. The enterprise segment, however, exhibits a faster 3.72% CAGR as Industry 4.0 investment accelerates. Demand for managed cloud, cybersecurity, and low-latency private 5G drives incremental spending among manufacturing, healthcare, and public-sector customers. The Italy Telecom MNO market size attributed to enterprise services is bolstered by NRRP incentives that earmark 27% of public funds for digital transformation in government entities.

Small and medium-sized enterprises tap 5G fixed wireless access to circumvent limited fiber availability, especially in industrial parks on city outskirts. Meanwhile, consumers benefit from expanding FWA options powered by millimeter-wave 5G, closing rural coverage gaps where fiber remains impractical. The expanding enterprise mix improves revenue quality because corporate contracts often involve multi-year terms and value-added solutions, dampening churn and reinforcing cash flow. As a result, a balanced split between mass-market connectivity and specialized B2B platforms supports sustainable progress for the Italy Telecom MNO market.

Geography Analysis

Regional divides remain a defining feature. Northern Italy shows the densest fiber footprint and earliest 5G launches, with Milan, Turin, and Bologna all surpassing 90% outdoor 5G population coverage by 2025. Industrial clusters in Lombardy and Emilia-Romagna adopt private 5G, boosting local demand for edge computing and latency-sensitive applications. The Italy Telecom MNO market size linked to these northern provinces, therefore, outpaces the national mean as factories digitize processes to enhance competitiveness.

Central Italy, anchored by Rome, benefits from infrastructure concessions such as INWIT’s 25-year Smart City Roma plan that delivers wholesale 5G across transport nodes. Improved connectivity supports tourism, public safety, and e-government solutions. FiberCop and Open Fiber continue to overbuild and upgrade pre-existing copper loops, attracting premium broadband uptake among households and small enterprises. Consequently, central regions register mid-single-digit growth, modestly above the national average.

Southern Italy still trails on adoption metrics because of sparse population density and lower disposable incomes. The Italia a 1 Gbps program allocates 40% of its EUR 2.02 billion (USD 2.33 billion) budget to the south, subsidizing fiber links to communities where private capital return expectations deter investment. EOLO’s 5G millimeter-wave FWA reaches 700,000 households, offering up to 1 Gbps speeds in mountain and coastal zones where trenching costs run high. While adoption lags, improving affordability and state-funded backhaul accelerate catch-up, raising total addressable demand for the Italy Telecom MNO market.

Competitive Landscape

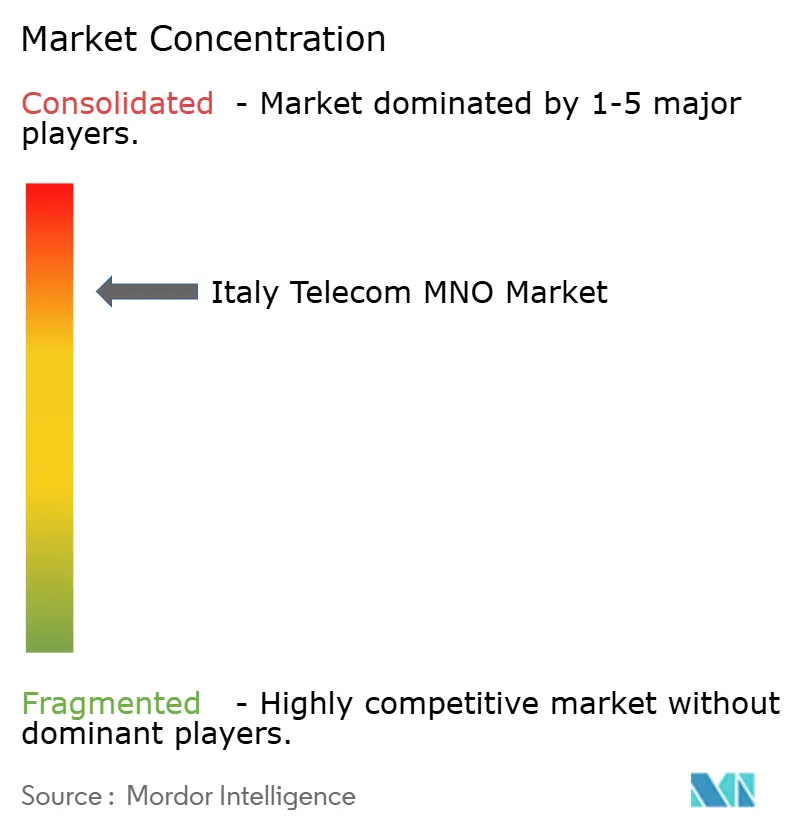

Four national operators—TIM, Vodafone-Fastweb (under Swisscom), WindTre, and Iliad—form a moderately concentrated market. The pending integration of Vodafone Italia with Fastweb will create a converged rival, holding robust fiber assets and 22,000 mobile sites, thereby narrowing the scale gap with TIM. TIM’s sale of NetCo to KKR slashes leverage toward the 1.6-1.7× range, freeing capital for 5G densification and cloud expansion within its consumer and enterprise entities.

Network-sharing agreements help curb capex. WindTre and Iliad formed Zefiro Net to build and run 5G coverage across 2,500 rural municipalities, reducing duplication and accelerating time-to-market.[4]Infrastrutture Wireless Italiane, “INWIT unveils 2025-2030 plans,” towerxchange.com Tower companies supply critical passive infrastructure. INWIT tops 25,000 sites, Cellnex follows, and Phoenix Tower International expands via Iliad partnerships. INWIT’s tenancy ratio jumped from 2.26× to 2.35× in 2025, proving the payoff from multi-operator colocation.

The strategic focus is shifting toward enterprise solutions. TIM Enterprise seeks EUR 1 billion (USD 1.15 billion) cloud revenue by 2026, leveraging alliances with Google Cloud, Microsoft Azure, Oracle, and VMware. Vodafone-Fastweb will push integrated offers, using Fastweb’s fiber backbone to cross-sell mobile to its 3.4 million broadband customers. Green-energy agendas also differentiate players: INWIT’s EUR 100 million (USD 115.21 million) solar roll-out lowers carbon output and stabilizes long-term opex. Together, these strategies reinforce a shift from price competition toward innovation, improving the health of the Italy Telecom MNO market.

Italy Telecom MNO Industry Leaders

Telecom Italia (TIM)

WindTre

Iliad Italia

Fastweb + Vodafone

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: INWIT secured EUR 350 million (USD 403.23 million) in financing from the European Investment Bank to speed up tower deployment and expand 5G and FWA coverage.

- March 2025: INWIT completed a EUR 750 million (USD 864.07 million) bond issue, attracting EUR 2.3 billion (USD 2.65 billion) in demand from over 200 institutional investors, which will fund the construction of 3,500 planned towers.

- November 2024: INWIT completed the acquisition of 52.08% of the Smart City Roma stake, securing a 25-year concession to build wholesale 5G infrastructure across the capital.

Italy Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.

The Italian telecom MNO market includes an in-depth trend analysis based on connectivity, like fixed networks, mobile networks, and telecom towers. Telecom services are divided into voice services (wired and wireless), data and messaging services, and OTT and PayTV services. Several factors, including an increasing demand for 5G, likely drive the adoption of telecom services. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Italy Telecom MNO market in 2026?

The Italy Telecom MNO market size stands at USD 19.27 billion in 2026 with a forecast CAGR of 3.39% through 2031.

Which service generates the highest revenue?

Data and Internet services dominate, capturing 42.65% revenue share in 2025 and continuing to outpace voice and messaging lines.

What is the fastest-growing service segment?

IoT and M2M services are set to grow at 3.46% CAGR through 2031, fueled by industrial automation and smart-city projects.

How does regional disparity affect growth?

Northern and central regions advance faster thanks to early 5G and dense fiber networks, while government subsidies help the south narrow its connectivity gap.

Which firms lead tower infrastructure?

INWIT holds the largest portfolio with over 25,000 sites followed by Cellnex, and Phoenix Tower International is expanding through Iliad contracts.

How will consolidation influence competition?

The Swisscom–Vodafone deal and TIM’s NetCo sale are expected to curb price wars, improve investment capacity, and foster value-based competition.

Page last updated on: