Aerospace and Defense Connectors Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 5.55 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

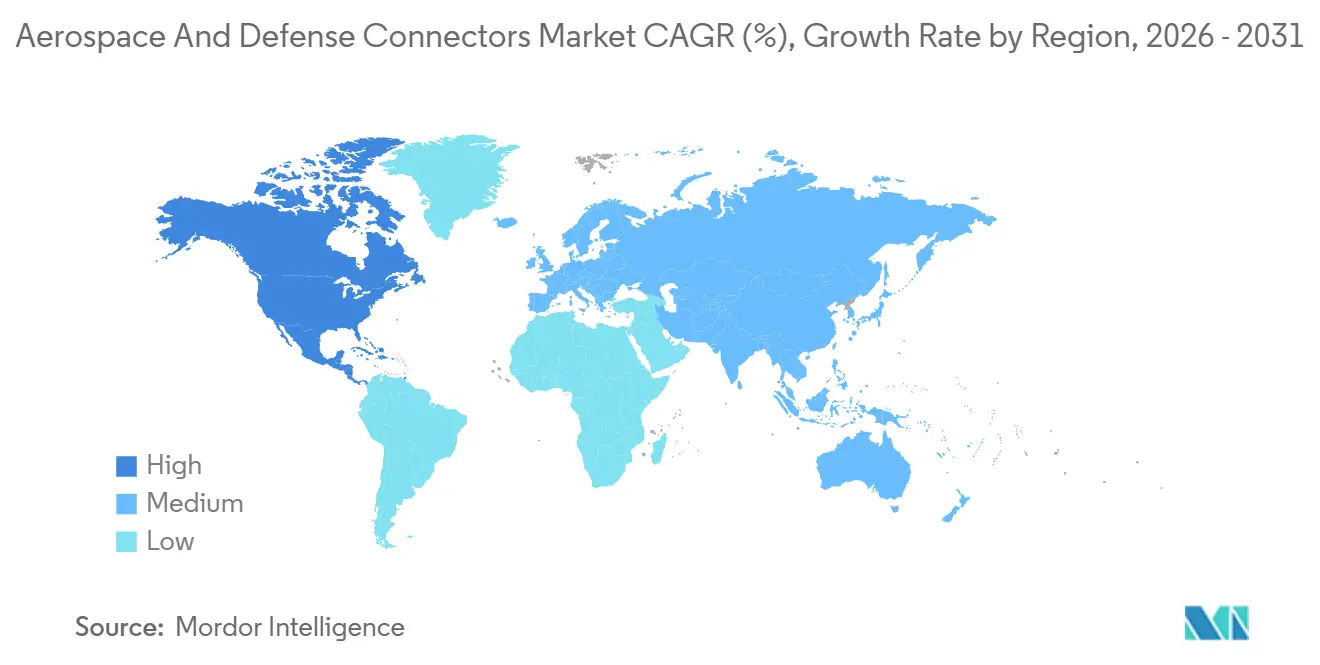

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace and Defense Connectors Market Analysis by Mordor Intelligence

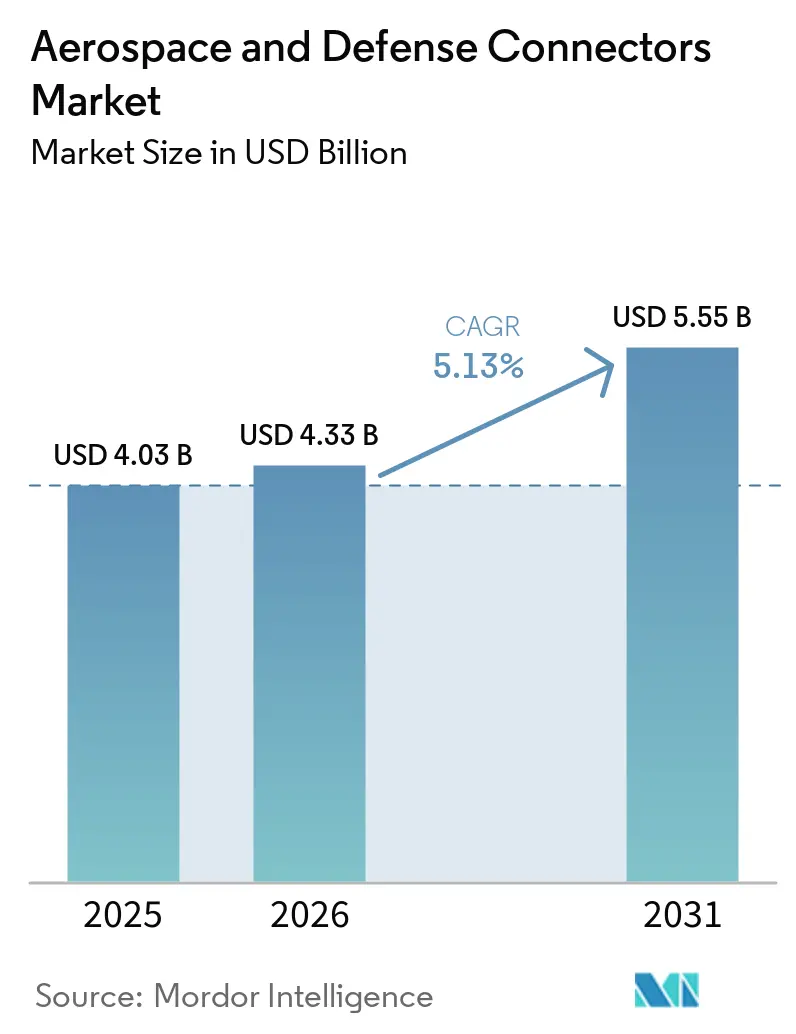

The aerospace and defense connectors market is expected to grow from USD 4.03 billion in 2025 to USD 4.33 billion in 2026 and to reach USD 5.55 billion by 2031, at a 5.13% CAGR over 2026-2031. Persistent investment in 6G-ready avionics, defense-platform electrification, and cybersecurity-by-design architectures sustains spending momentum across the aerospace and defense connectors market. Fiber-optic technology maintains its demand leadership by shielding mission-critical data streams from electromagnetic interference, while miniaturized hybrid solutions capitalize on the rapid digitalization of military and space assets. Regional procurement cycles remain synchronized with elevated defense outlays, particularly in the US, Japan, and the EU, while the commercial aerospace recovery further supports connector shipments. At the same time, additive-manufactured housings and digital-thread production models shorten design-to-qualification timelines, enabling suppliers to meet just-in-time requirements for newly launched platforms.

Key Report Takeaways

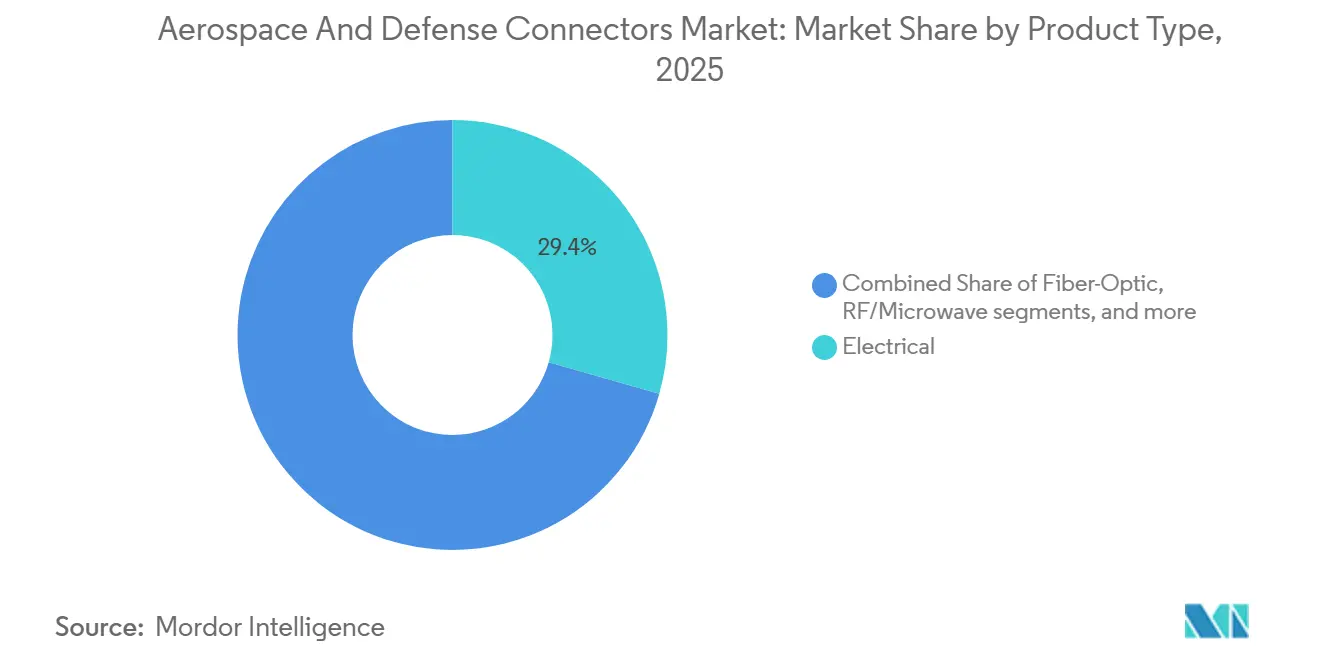

- By product type, electrical solutions led the aerospace and defense connectors market with a 29.40% share in 2025, while fiber-optics is projected to grow at a 5.55% CAGR through 2031.

- By connector shape, circular products accounted for 45.46% of the revenue in 2025; nano/micro-miniature designs are projected to grow at a 5.99% CAGR through 2031.

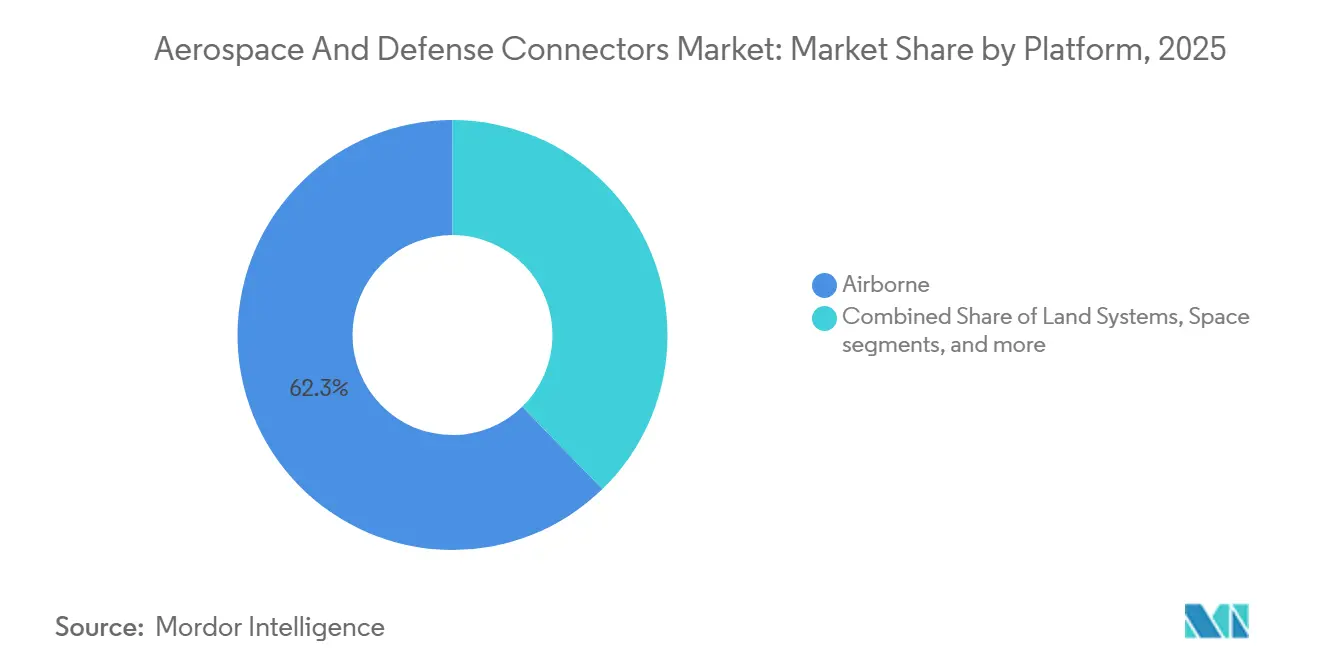

- By platform, airborne systems accounted for 62.28% of the aerospace and defense connectors market size in 2025, while space applications are forecast to expand at a 20.34% CAGR through 2031.

- By end user, OEM production accounted for 56.80% of 2025 revenue and is forecast to grow at a 5.68% CAGR through 2031.

- By geography, Asia-Pacific accounted for 31.76% of the market share in 2025, while North America is projected to grow at a 5.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerospace and Defense Connectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower-orbit satellite constellations driving nano-connector demand | +2.10% | Global, concentrated in US, EU, China space programs | Medium term (2-4 years) |

| Growing orders for 6G-ready high-bandwidth avionics links | +1.80% | Global (early adoption in North America and EU) | Medium term (2-4 years) |

| Electrification of defense platforms (e-Propulsion, e-APU) | +1.50% | North America and EU core, expansion to APAC | Long term (≥ 4 years) |

| Mandated cybersecurity-by-design for mission-critical connectors | +1.20% | Global, driven by US DoD CMMC | Short term (≤ 2 years) |

| Additive-manufactured metal housings slash lead-times | +0.90% | North America and EU manufacturing hubs | Short term (≤ 2 years) |

| Rapid prototyping hubs inside major OEMs (digital thread integration) | +0.70% | Global, concentrated at major aerospace OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

6G-Ready High-Bandwidth Avionics Links Drive Next-Generation Connectivity

The transition to 6G avionics necessitates connector specifications that cater to D-band millimeter-wave frequencies, requiring ultra-low insertion loss and phase stability.[1]Institute of Electrical and Electronics Engineers, “D-Band Applications for 6G Avionics,” ieee.org Militaries now request contactless architectures to serve phased-array radars and electronic-warfare payloads that cannot tolerate signal degradation. Multi-domain operations increase real-time data-fusion loads, boosting demand for high-density optical backbones in the aerospace and defense connectors market. Early adoption began in the US, and several European programs, and Asian primes followed as next-generation fighter development accelerated. CMMC 2.0 cybersecurity mandates add encryption and tamper-evident requirements to every interconnect, differentiating suppliers able to embed security hardware in standard footprints. Over the medium term, 6G avionics specifications will permeate transport and tanker fleets, sustaining long-tail replacement demand within the aerospace and defense connectors market.

Defense Platform Electrification Accelerates High-Power Connector Adoption

Hybrid and fully electric propulsion initiatives across rotorcraft, unmanned combat vehicles, and naval platforms create a steady pull for high-power interconnects that handle elevated voltage and current levels without thermal runaway. These connectors must also safeguard electromagnetic compatibility inside densely packed avionics bays.[2]US Navy, “Electrification Roadmap for Future Vertical Lift,” usnavy.mil European and North American integrators have already migrated secondary flight-control actuators from hydraulic to electric systems, and programs such as FLRAA embed electric drive systems as the baseline architecture. As acquisition cycles span decades, cumulative demand builds as successive production lots require identical qualified connectors, reinforcing long-run volume in the aerospace and defense connectors market.

Cybersecurity-by-Design Mandates Reshape Connector Architecture

Connectors must incorporate serialized traceability, tamper-evident seals, and embedded secure-authentication chips that deter spoofing. Suppliers without a certified information-assurance infrastructure face disqualification, which tightens supply and elevates barriers to entry. Early-compliant firms, such as Stress Aerospace, secured multi-year commitments, signaling a first-mover advantage. Therefore, the aerospace and defense connectors market rewards capital investments in cyber-audit readiness and drives consolidation as smaller vendors exit.

Satellite Constellation Growth Fuels Nano-Connector Innovation

The surge in low-Earth-orbit (LEO) constellations requires thousands of radiation-hardened nanoconnectors per launch vehicle, thereby magnifying the volume potential. For multi-year missions, these sub-miniature devices must withstand rapid thermal cycling, vibration, and vacuum. The US, European, and Chinese commercial launchers have prioritized standard socket footprints that simplify high-throughput assembly lines. Suppliers that co-locate rapid-prototype facilities near major space hubs meet aggressive design-freeze schedules and secure early design wins, thereby fortifying their long-term position within the aerospace and defense connectors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic tin-whisker and fretting corrosion failures in vibration zones | -0.80% | Global (high-vibration military platforms) | Short term (≤ 2 years) |

| EU “PFHxS” ban limits fluoropolymer sealants supply | -0.60% | EU core, indirect global impact | Medium term (2-4 years) |

| Skilled crimp-operator shortage at MRO depots | -0.40% | Global, concentrated in mature aerospace markets | Medium term (2-4 years) |

| Rising IP-theft risk deters open reference-design sharing | -0.30% | Global, particularly affecting US-China technology transfer | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tin-Whisker and Fretting Corrosion Failures Constrain Reliability

Lead-free solder regulations led to tin-rich surface finishes that can spawn conductive whiskers up to 10 millimeters in length, shorting neighboring contacts in tight MIL-DTL-38999 shells. Helicopter and fighter environments magnify fretting corrosion, degrading mating surfaces and electrical continuity. Maintenance depots report higher replacement rates and extended aircraft downtime, placing immediate pressure on readiness metrics. Novel nickel-phosphorus and gold-cobalt platings show promise, yet defense qualification can take over three years, delaying field availability. The aerospace and defense connectors market, therefore, contends with elevated quality costs until alternative finishes mature.

EU Fluoropolymer Restrictions Disrupt Sealing Solutions

The European Chemicals Agency has added PFHxS to its restricted list, curbing the use of fluoropolymer sealants integral to fuel system connectors.[3]European Chemicals Agency, “PFHxS Restriction Proposal under REACH,” echa.europa.eu Suppliers must redesign grommets and O-rings using alternative materials to maintain fuel resistance across -65 °C to +200 °C temperature cycles. Replacement compounds require costly validation, while US programs that share standard part numbers also face redesign to avoid dual BOMs. The two- to four-year certification window stalls product launches, acting as a medium-term drag on the aerospace and defense connectors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: High-Speed Innovations Drive Rapid Growth in Fiber-Optic Technology

The electrical segment held the largest share in 2025, at 29.40%. Electrical connectors in aerospace and defense are closely linked to the shift toward high-power electrical architectures, particularly in military aircraft and naval systems. Platforms such as the F-35 Lightning II and B-21 Raider increasingly rely on electrically driven subsystems, including electromechanical actuators, advanced radar systems, and onboard processing units. These platforms operate on 270 VDC and emerging 540 VDC architectures, replacing traditional hydraulic systems to enhance efficiency and survivability. Fiber-optic connectors will grow at the fastest CAGR of 5.55% through 2031, driven by their immunity to electromagnetic interference and the rising data-bus speeds that exceed copper's limits. This leadership endures as platforms integrate sensor fusion, secure networking, and real-time video streams that strain legacy cabling.

Legacy copper solutions still suit low-rate telemetry and safety-critical controls, particularly in rotorcraft, where maintenance familiarity underpins procurement. RF/microwave families support phased-array radars due to precise phase-matching tolerances, while high-power/HVDC units satisfy 800-volt e-propulsion buses. Suppliers that pair metal-matrix composite contacts with advanced dielectric inserts achieve lower weight and higher current density, capturing retrofit upgrades on aging fleets. Altogether, these product lines underpin the diverse performance envelope demanded by the aerospace and defense connectors market.

By Connector Shape: Circular Solutions Lead Despite Miniaturization Push

Circular connectors secured a 45.46% share in 2025, primarily driven by MIL-DTL-38999 variants, which remain the de facto interface across fixed-wing, rotorcraft, and armored vehicles. Their bayonet coupling and environmental sealing outperform alternatives during salt-spray and vibration trials. However, nano/micro-miniature packages are growing fastest, with a 5.99% CAGR, as satellite builders squeeze electronics into increasingly smaller form factors. Therefore, the aerospace and defense connectors market balances legacy standardization with aggressive miniaturization.

Rectangular solutions dominate avionics line-replaceable units, where panel density is a paramount consideration. Board-to-board mezzanine connectors complement modular electronics, facilitating rapid upgrade cycles. Additive manufacturing enables the creation of one-piece shells that integrate strain relief and heat sinks, thereby reducing the parts count. As digital-thread design proliferates, engineers model connector airflow and EMI performance upfront, minimizing late-stage redesign costs inside the aerospace and defense connectors market.

By Platform: Airborne Leadership Challenged by Space Expansion

Airborne programs generated 62.28% of 2025 sales, reflecting both legacy fleet sustainment and the introduction of new fighter, tanker, and trainer jets into production. Yet, space systems mark the highest trajectory at a 20.34% CAGR due to the mega-constellation launch cadence, which demands thousands of nano-connectors per vehicle. Electrical, optical, and high-speed data links must withstand the radiation and thermal extremes of repeated orbital cycles, driving the need for novel material science.

Land vehicles retain a steady share through the adoption of wheeled and tracked modernization, emphasizing rugged, circular shells with shock and dust mitigation. Naval and sub-surface platforms require hermetic sealing against saltwater ingress; stainless-steel and titanium shells dominate here. Across all domains, unmanned systems proliferate sensors and edge-computing nodes, boosting cumulative connector counts within the aerospace and defense connectors market.

By End User: OEM Production Drives Market Growth

OEM lines accounted for 56.80% of 2025 revenue and are expected to grow at a CAGR of 5.68% during the forecast period, underscoring the design-in advantage of suppliers aligned with platform development from the concept phase. Certified parts lists seldom change after qualification, resulting in long-term revenue. The aftermarket and MRO segments grow more slowly, hindered by technician shortages and prolonged maintenance intervals. Manufacturers that deliver tool-less, keyed, or self-diagnosing connectors reduce skill dependencies and may capture a significant share of retrofit spending, thereby bolstering continuity within the aerospace and defense connectors market.

Geography Analysis

Asia-Pacific accounted for 31.76% of the market in 2025. This dominance can be attributed to the rapid growth of the aviation and defense sectors in nations such as China, India, and Japan. Initiatives such as South Korea's KF-21 and Australia's REDSPICE cyber program have heightened demand for secure optical links. While India's Make in India initiative promotes local production, persistent technology gaps continue to drive reliance on imports from Western suppliers. Moreover, regional collaborations, particularly through ASEAN offsets, facilitate the local assembly of foreign designs. This strategy not only embeds dual-sourcing practices but also stabilizes the supply chain in the aerospace and defense connectors market.

North America, buoyed by its mature industrial base, prominent defense primes, and a surge in commercial output, is set to grow at a 5.35% CAGR. The region's aerospace and defense connectors market is reaping benefits from the ramp-ups of programs like the KC-46A, B-21, and CH-53K, each integrating hundreds of qualified part numbers. With the US enforcing CMMC, domestic suppliers gain early certifications, slashing procurement lead times. Canada excels in precision machining and harness assembly, while Mexico's maquiladoras craft molded inserts and contact sub-assemblies, seamlessly flowing north through USMCA lanes. These cross-border collaborations bolster resilience, all while upholding stringent cyber compliance.

Europe increases procurement in line with NATO targets, led by Germany's EUR 100 billion (USD 117.89 billion) Sondervermögen funding for high-value aircraft and air-defense batteries. France, Italy, and Sweden are pursuing next-generation fighter partnerships that stipulate European supply chains. REACH and PFAS rules are driving the adoption of alternative elastomers and platings, forcing redesigns that temporarily slow connector deliveries. However, once replacement materials obtain EN-9100 approval, European integrators will regain schedule traction. The Eastern European states' purchase of Abrams and HIMARS units spurs US-EU transatlantic collaboration, distributing connector production across both continents to ensure security of supply.

Competitive Landscape

The aerospace and defense connectors market remains moderately concentrated. TE Connectivity Corporation, Amphenol Corporation, and ITT Inc. leverage vertically integrated contact fabrication, plating, and over-molding lines to ensure control over quality and lead times. Molex's December 2024 purchase of AirBorn added MIL-SPEC fiber assemblies and high-speed backplane capability, signaling a strategic pivot toward high-reliability defense domains. Smiths Interconnect introduced ceramic-based contacts for elevated temperature margins, broadening exposure to hypersonic and engine-bay applications.

Mid-tier firms, such as Radiall and Fischer Connectors, exploit niche specialization in harsh-environment optical termini, while Glenair sustains its strength in quick-disconnect circulars for dismounted soldier systems. Collins Aerospace's additive-manufacturing investments enable agile turnaround of custom housings, differentiating it from catalog-only competitors. Cybersecurity compliance emerged as a critical moat once CMMC audits became mandatory in late 2024; Stress Aerospace's Level 2 accreditation positioned it favorably for classified programs. As illustrated by TE Connectivity's USD 5.8 million fine, export-control lapses underscore regulatory risk and reinforce the premium on robust trade-compliance programs.

Small innovators push the miniaturization envelope, yet rising qualification costs and a scarcity of skilled labor encourage licensing arrangements with larger incumbents. Consolidation will likely continue as primes insist on financially stable suppliers capable of multi-decade sustainment, shaping a progressively tighter market for aerospace and defense connectors.

Aerospace and Defense Connectors Industry Leaders

Amphenol Corporation

Eaton Corporation plc

TE Connectivity plc

Molex, LLC (Koch, Inc.)

ITT Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Molex, LLC, completed the acquisition of Smiths Interconnect, a subsidiary of the UK-based Smiths Group plc. This acquisition represents a significant step in Molex's strategy to advance technology that shapes the future and enhances lives. Smiths Interconnect adds a broad portfolio of complementary products and capabilities, including ruggedized custom connectors, contacts, RF components, and optical transceivers designed for harsh environments.

- October 2025: ITT Inc. showcased its latest aerospace and defense technologies at the 2025 AUSA Annual Meeting and Exposition in Washington, D.C. The company introduced the Ultra-High-Density C5 Warrior, a durable breakaway connector solution that delivers data rates exceeding 10 Gbps. This product is housed in the industry’s smallest sealed package, engineered to endure extreme shock and vibration.

- July 2025: Rosenberger Hochfrequenztechnik GmbH & Co. KG introduced its new EBM® connectors. These connectors are designed to enhance reliability, durability, and ease of use, addressing the increasing demand for high-speed, low-maintenance data transmission in challenging environments.

Global Aerospace and Defense Connectors Market Report Scope

Aerospace and defense connectors, engineered for aircraft, spacecraft, and military systems, excel in harsh environments. These specialized electrical connectors transmit power, signals, data, fiber-optics, and RF systems, all while withstanding extreme conditions: from vibrations and temperature fluctuations to moisture, dust, pressure, and electromagnetic interference.

The aerospace and defense connectors market is segmented by product type, connector shape, platform, end user, and geography. By product type, the market is segmented by electrical, fiber-optic, RF/microwave, hybrid, and high-power. By connector shape, the market is segmented into circular, rectangular, board-to-board, and nano/micro-miniature. By platform, the market is segmented into airborne, land systems, naval and sub-surface, and space. By end user, the market is segmented into OEM and aftermarket. The report also covers the market sizes and forecasts for the aerospace and defense connectors market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Electrical (Signal and Power) |

| Fiber-Optic |

| RF/Microwave |

| Hybrid |

| High-Power |

| Circular |

| Rectangular |

| Board-to-Board (BTB) |

| Nano/Micro-Miniature |

| Airborne |

| Land Systems |

| Naval and Sub-Surface |

| Space |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Electrical (Signal and Power) | ||

| Fiber-Optic | |||

| RF/Microwave | |||

| Hybrid | |||

| High-Power | |||

| By Connector Shape | Circular | ||

| Rectangular | |||

| Board-to-Board (BTB) | |||

| Nano/Micro-Miniature | |||

| By Platform | Airborne | ||

| Land Systems | |||

| Naval and Sub-Surface | |||

| Space | |||

| By End User | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the aerospace and defense connectors market?

The aerospace and defense connectors market reached USD 4.03 billion in 2025, USD 4.33 billion in 2026, and is projected to rise to USD 5.55 billion by 2031, registering a 5.13% CAGR.

Which connector type holds the largest share today?

Electrical led with 29.40% market share in 2025 due to shift toward high-power electrical architectures, particularly in military aircraft and naval systems.

Which platform is generating the fastest connector demand growth?

Space applications are expanding at an 20.34% CAGR, fueled by low-Earth-orbit satellite constellations.

Why are cybersecurity mandates influencing connector design?

CMMC 2.0 requires tamper-evident, traceable, and secure-authentication features in mission-critical connectors, reshaping supplier qualification.

How are additive-manufactured housings benefiting connector suppliers?

3D-printed metal housings cut prototype lead times by up to 20% and enable complex geometries without extra mass.

Which region held largest shares in aerospace and defense connectors market in 2025?

Asia-Pacific dominated the market with 31.76% in 2025 due to rising defense budgets in Japan, China, South Korea, and Australia.

Page last updated on: