Fire Fighting Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

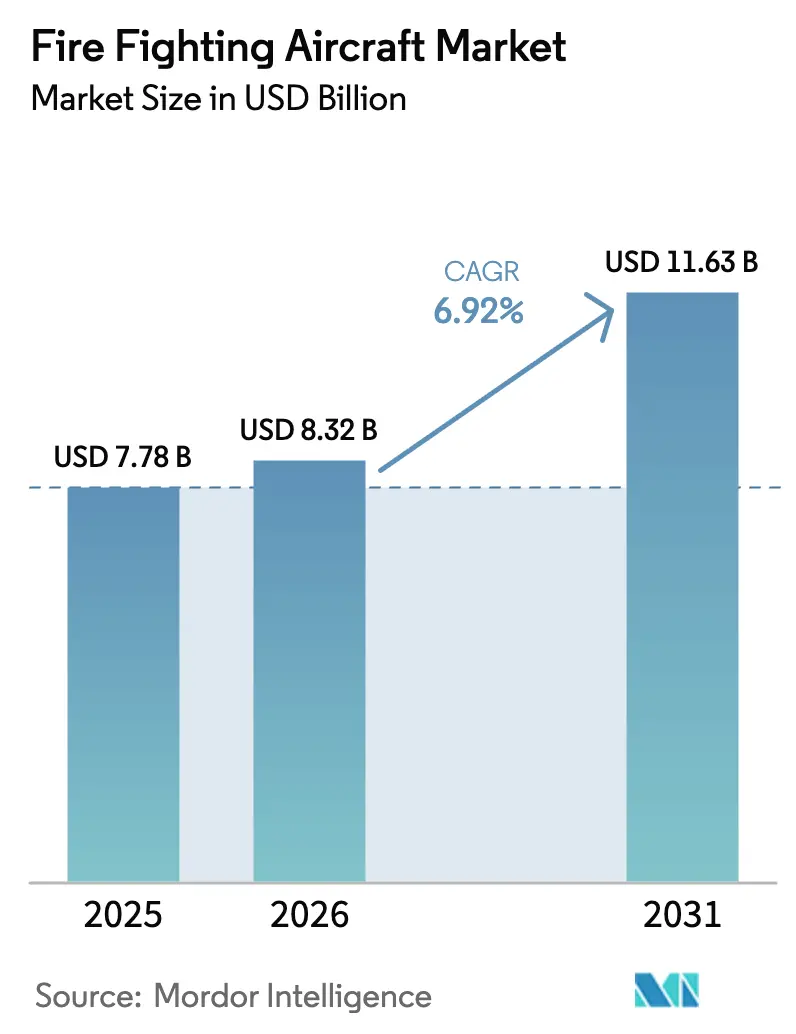

| Market Size (2026) | USD 8.32 Billion |

| Market Size (2031) | USD 11.63 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire Fighting Aircraft Market Analysis by Mordor Intelligence

The fire fighting aircraft market size is expected to grow from USD 7.78 billion in 2025 to USD 8.32 billion in 2026 and is forecast to reach USD 11.63 billion by 2031 at a 6.92% CAGR over 2026-2031. Growth stems from climate-driven wildfire escalation, rising government aerial-fire budgets, and the cost advantage of converting retired passenger jets into tankers. Accelerated procurement cycles in North America and Europe, coupled with sovereign fleet expansions in the Asia-Pacific region, are reshaping competitive dynamics. Conversion houses are narrowing acquisition costs compared to new-build platforms, while precision-drop avionics are enhancing effectiveness and driving the replacement of 1980s-era aircraft. Workforce shortages and tariff-induced avionics delays temper near-term capacity additions, yet expanding utility-liability exposure is unlocking a new private-contractor demand channel. Manufacturers that bundle lifecycle support and autonomy, as well as developers offering crew-risk mitigation, are best positioned to capture emerging opportunities as cross-border leasing frameworks shorten deployment timelines.

Key Report Takeaways

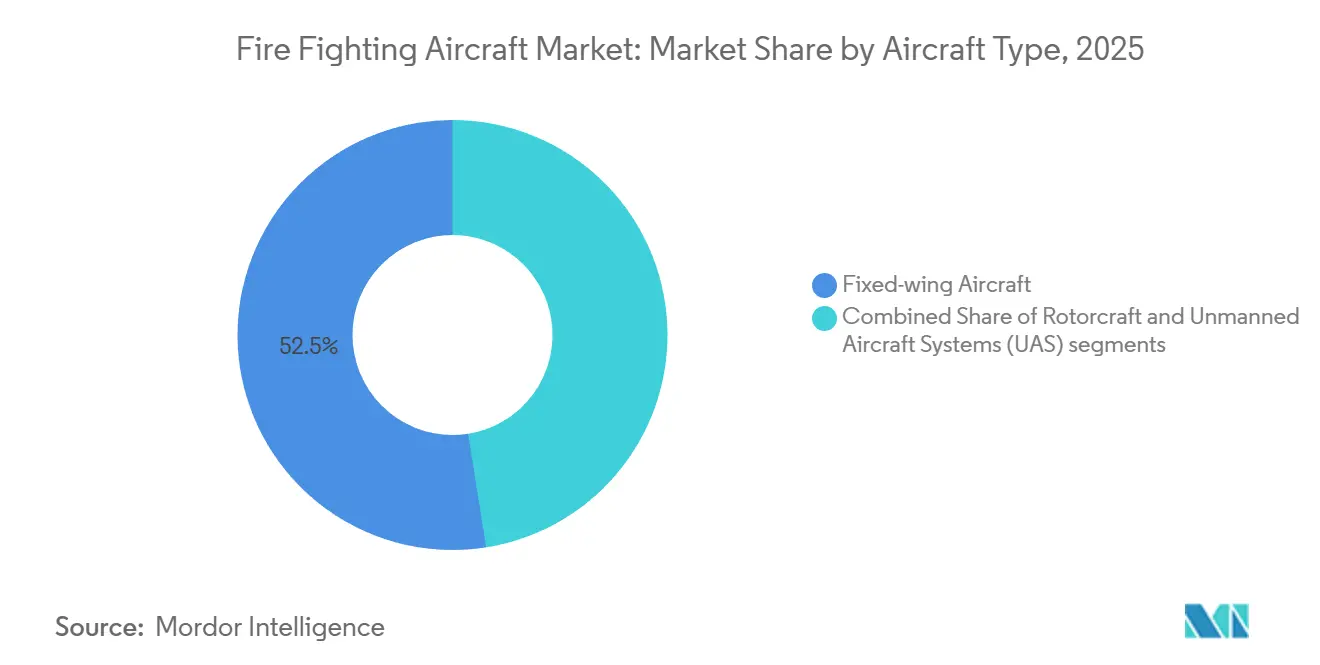

- By aircraft type, fixed-wing platforms commanded 52.50% of the fire fighting aircraft market share in 2025; unmanned aircraft systems are forecasted to expand at an 8.87% CAGR through 2031.

- By tank capacity, the less than 10,000 liter class accounted for 47.80% of the fire fighting aircraft market size in 2025, whereas platforms exceeding 40,000 liters are projected to advance at a 7.74% CAGR through 2031.

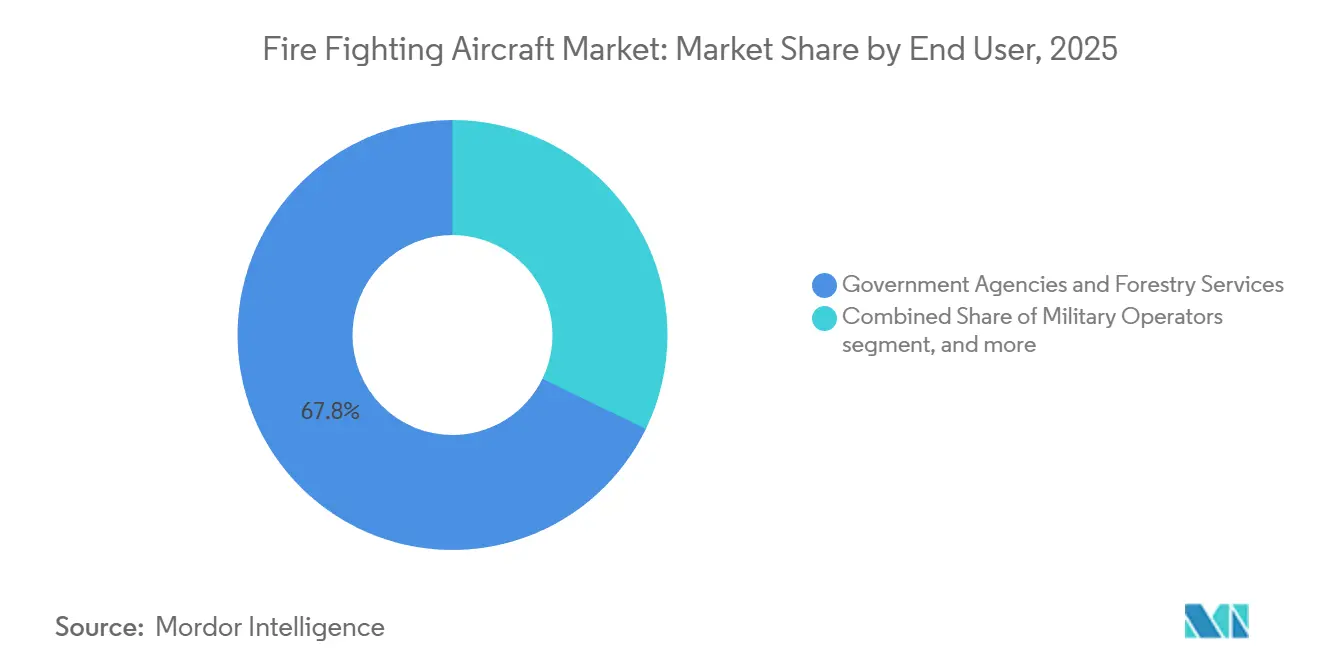

- By end user, government agencies held 67.80% of the fire fighting aircraft market share in 2025, while private contractors are projected to grow at a 7.65% CAGR through 2031.

- By operational range, the 1,000 to 3,000 kilometer class captured 55.45% of the fire fighting aircraft market size in 2025; platforms exceeding 3,000 kilometers are set to post an 8.20% CAGR by 2031.

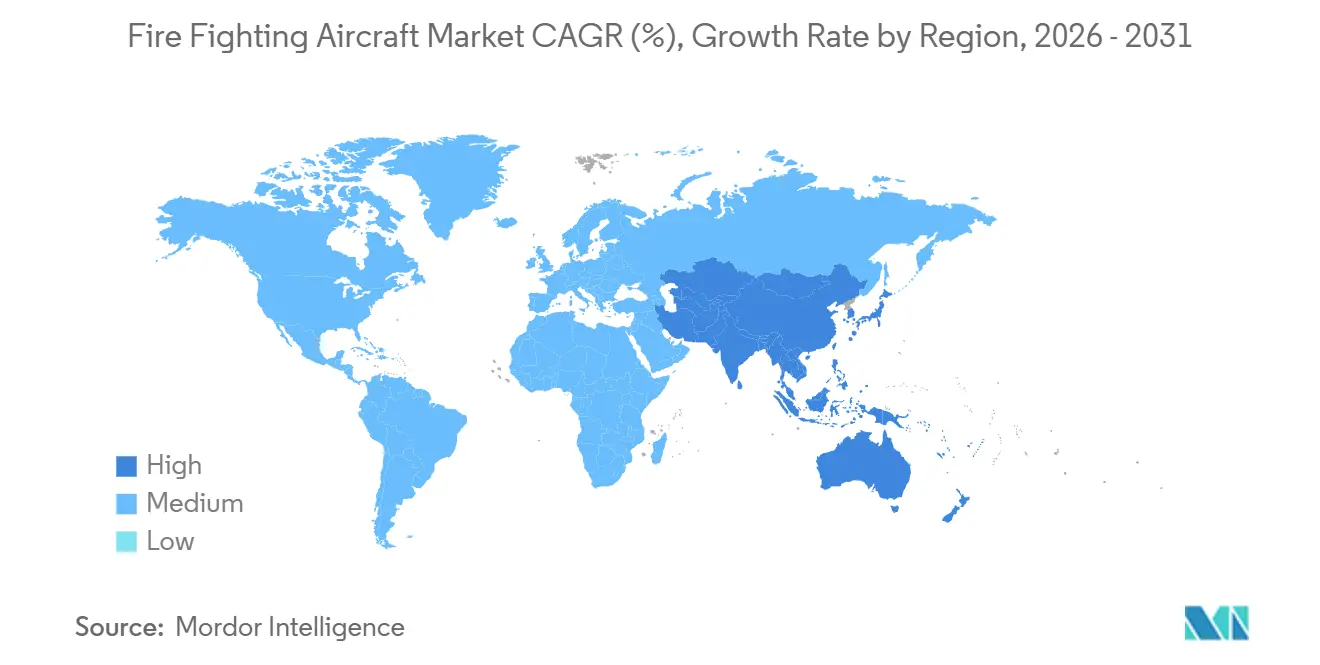

- By geography, North America led with a 47.10% revenue share in 2025; the Asia-Pacific region is the fastest-growing, with a 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fire Fighting Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating frequency and intensity of wildfires | +1.2% | North America, Mediterranean Europe, Australia | Medium term (2–4 years) |

| Expanding government aerial-fire budgets and long-term contracts | +1.0% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Next-gen airframes and precision-drop technologies | +0.8% | Global, early China adoption | Medium term (2-4 years) |

| Retired narrowbody feedstock enabling low-cost tanker conversions | +0.6% | North America, Australia, South America | Short term (≤ 2 years) |

| Utility-liability risk fuelling private-sector aircraft demand | +0.5% | North America, Mediterranean Europe | Short term (≤ 2 years) |

| ICAO I4F initiative easing cross-border aircraft leasing | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Frequency And Intensity Of Wildfires

Wildfire activity continues to challenge historical norms, transforming what was once a three-month issue into a threat that lingers throughout every season. Agencies now hold aircraft on alert all year because 2024 saw 7.5 million acres burn in the US and 18 million hectares in Canada, the worst totals ever logged. [1]Source: National Interagency Fire Center, “Wildfire Statistics,” nifc.gov Climate research links the surge to a 25% increase in fire-weather days since 2000, resulting in longer contracts and higher fixed costs.[2]Source: Nature Climate Change, “Increase in Fire-Weather Days,” nature.com Greece’s 175,000-hectare loss stretched tanker leases into October, and Australia adopted permanent basing, moves that lengthen utilization windows and improve return on large-platform investments.

Expanding Government Aerial-Fire Budgets And Long-Term Contracts

Public spending is climbing at every tier. Washington raised its fiscal-2025 aerial-fire allocation to USD 534 million, 12% above the 2024 level, while California surpassed USD 400 million to finance 12 helicopters and two large tankers. North of the border, Ottawa pledged CAD 257.6 million (USD 185.06 million) over five years for amphibious aircraft that can scoop remote lakes. Brussels’ rescEU program injected EUR 600 million (USD 648.40 million) to pre-position 24 platforms across the bloc, reducing costly spot leases. Spain’s 15-year DHC-515 package, bundling training and maintenance, signals a pivot toward lifecycle contracting that stabilizes OEM revenue.

Next-Generation Airframes And Precision-Drop Technologies

Technology upgrades are cutting chemical waste and widening mission profiles. Elbit’s HyDrop system, FAA-certified in 2024, narrows the dispersion of retardant to 10 meters, tripling the accuracy compared to gravity drops. The USDA’s third-generation FRDS senses wind shear in real time, trimming per-acre retardant use by 18% on C-130H trials. Autonomous craft enhance safety; EHang’s EH216-F flew 6,000 test sorties before receiving Chinese certification in 2025, enabling crew-free suppression within smoke-filled urban canyons. Agencies replacing 1980s airframes gain plug-and-play avionics, unlocking higher-margin infrastructure-protection contracts that reward precision and low collateral impact.

Retired Narrow-Body Feedstock Enabling Low-Cost Tanker Conversions

Fleet rationalization followed the pandemic, which flooded the market with A320s and B737s, thereby slashing acquisition costs for conversion houses. Neptune’s A319 program offers 4,500-gallon payloads at USD 12 million, roughly half the price of a new DHC-515, and secures three US state buyers for 2026 delivery. Coulson spent USD 48 million turning four B737-700s into 5,000-gallon tankers for Australia-Chile rotation, validating jet-speed economics. More than 200 surplus military C-130s worldwide sustain retrofit pricing of around USD 10–15 million, allowing operators to quickly field capacity while OEM lead times stretch to three years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and lifecycle costs | -0.7% | Global, emerging markets hardest hit | Medium term (2-4 years) |

| Shortage of experienced aerial-fire pilots and mechanics | -0.5% | North America, Australia, Mediterranean Europe | Short term (≤ 2 years) |

| Tariff-driven avionics/airframe supply-chain disruptions | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Weather-smoke grounding limits annual utilization | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition And Lifecycle Costs

Capital intensity remains the primary brake on expansion, especially in middle-income regions. A new DHC-515 lists at USD 37 million, while a converted B747 large air tanker, including structural work and delivery system, nears USD 50 million. Operational bills pile on: fuel, spares, and heavy checks burn USD 8,000-12,000 every flight hour, yet aircraft sit idle up to eight months, inflating the cost per gallon against ground crews. Brazil’s federal budget only covered USD 24 million in 2025 leases, underscoring how emerging markets struggle to finance fixed-wing fleets despite worsening fire risk.

Shortage Of Experienced Aerial-Fire Pilots And Mechanics

Workforce gaps are widening as airlines rebalance rosters and older captains retire. The FAA foresees a 12,000-pilot national shortfall by 2032, with seasonal aerial fire fighting hardest hit because it demands low-altitude, high-G maneuvering skills, which offer intermittent pay.[3]Source: Federal Aviation Administration, “Pilot Workforce Projections,” faa.gov The National Association of State Foresters puts average tanker-pilot age at 47, and retirements now outpace new entrants two-to-one. Mechanics lag too; Australia’s NAFC reported 15% vacancies in 2025, grounding some contracted aircraft during peak demand. Training costs, exceeding USD 100,000, deter recruits who are absent multi-year employment guarantees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Fixed-Wing Platforms Dominate Volume, UAS Segment Accelerates

Fixed-wing aircraft held a 52.50% market share in the fire fighting aircraft market in 2025, reflecting superior payload economics for large-area suppression. The segment’s longevity is reinforced by the C-130 and S-2T fleets, which performed the majority of US drops in 2025. Unmanned systems, though nascent, are expanding at an 8.87% CAGR as Chinese certification of the EH216-F and FAA sandbox trials in the US validate autonomous operations. Rotorcraft excel in precision structure defense and vertical reference missions, and AW139 deliveries to Italy and Los Angeles advance urban interface capability.

Fleet modernization favors conversion programs that extend service life and integrate precision-drop avionics. Fixed-wing operators capitalize on retired jets that combine jet speed with moderate operating costs, keeping the fire fighting aircraft market competitive. UAS deployments, backed by lower crew risk, are widening mission envelopes into smoke-obscured canyons where manned flight is untenable. Rotorcraft growth is tied to year-round vegetation-management contracts from utilities that demand immediate dispatch capability.

By Tank Capacity: Mid-Range Still Leads, VLAT Growth Outpaces

Aircraft under 10,000 liters represented 47.80% of the fire fighting aircraft market size in 2025, led by Air Tractor AT-802F fleets across North America and Australia. The 10,000-30,000 liter class, anchored by CL-415s and DHC-515s, strikes a balance between payload and lake-scooping agility; however, backlog constraints slow its growth. Huge air tankers with capacities above 40,000 liters are expanding at a 7.74% CAGR, as single-pass coverage of 3-kilometer firelines enhances cost efficiency during mega-fires.

Mid-capacity assets remain indispensable for rapid turnaround from proximal water bodies; yet, agencies are procuring VLATs to reduce crew flight hours and sortie counts. The scarcity of suitable B747 and DC-10 airframes caps the absolute VLAT fleet numbers, maintaining pricing power for operators. Lightweight categories thrive in emerging markets where runway infrastructure or budgets limit the adoption of heavy aircraft.

By End User: Private Contractors Gain Share Amid Liability Shifts

Government agencies accounted for 67.80% of the fire fighting aircraft market share in 2025; nonetheless, private operators are poised for a 7.65% CAGR as utilities and insurers secure dedicated fleets. Military support provides surge capacity but faces trade-offs in training readiness that limit annual flight allocations.

Private demand is price-inelastic, treating aircraft costs as insurance premiums. Erickson now derives over 60% of S-64 flying hours from private contracts, up from 30% in 2020. Government agencies, while still dominant, increasingly outsource initial-attack missions to contractors that guarantee scramble times, freeing public fleets for strategic perimeter drops.

By Operational Range: Ultra-Long-Range Platforms Unlock Hemispheric Utilization

Aircraft with a 1,000–3,000-kilometer range captured 55.45% of the fire fighting aircraft market share in 2025, striking a balance between fuel burn and repositioning reach. Platforms exceeding 3,000 kilometers are growing at an 8.20% CAGR as cross-border mutual-aid frameworks make hemispheric fleet rotation viable. Coulson’s C-130s flew from Canada to Australia and then to Chile within 12 months, doubling utilization and spreading fixed costs.

Short-range helicopters and light aircraft remain critical for rapid local response, while mid-range turboprops cover contiguous state missions. Ultra-long-range jets address strategic pre-positioning needs, enabling a single base to protect multiple jurisdictions and maximize aircraft asset utilization.

Geography Analysis

North America retained a 47.10% revenue share in 2025, as federal and state budgets surpassed USD 900 million; however, pilot shortages and airframe saturation moderated the regional CAGR. The US operated 23 large tankers, 8 VLATs, and more than 100 helicopters in 2025. Canada’s CAD 257.6 million (USD 185.06 million) investment focuses on amphibious platforms, while Mexico modestly expands helicopter leases. Utilization rates below 250 hours per season constrain new capital deployment, leading to a shift in procurement toward service contracts that prioritize availability over ownership.

The Asia-Pacific region is the fastest-growing region, with a 7.45% CAGR through 2031. Australia’s AUD 352.9 million (USD 236.37 million) plan builds sovereign capacity to cut reliance on leased North American assets. China has fielded the AG600 amphibious aircraft and has surpassed 50 fire fighting helicopters, with a concentration in Xinjiang and Heilongjiang. Japan, Indonesia, and Thailand expand helicopter fleets for mountainous and peatland fires, albeit from small bases.

Europe’s rescEU fleet fragments North American export dominance. Spain operates 73 aircraft and ordered six DHC-515s in 2025. France’s Sécurité Civile flies 23 amphibious aircraft and added three DHC-515s. Greece modernized its post-2024 fires with four new CL-415s. Russia’s Avialesookhrana maintains over 60 aircraft but faces hurdles in modernization. The Middle East and Africa markets are emerging slowly, with Saudi Arabia investing in helicopter capacity to protect its energy infrastructure.

Competitive Landscape

The fire fighting aircraft market is highly consolidated, with a few key players holding significant market shares. Lockheed Martin’s C-130J dominates large-tanker military-civil procurements, winning Romania’s USD 280 million order for five aircraft in 2025. De Havilland’s DHC-515 is the sole new-production amphibious aircraft, but it faces a three-year backlog. Leonardo and Airbus lead rotorcraft, while Erickson’s S-64 controls heavy-lift missions.

Conversion specialists disrupt pricing. Neptune’s A319 and Coulson’s 737 programs exploit abundant jet feedstock to undercut new builds by 50%. Precision-drop avionics from Elbit and USDA FRDS Gen III become mandatory specs, pushing legacy fleets toward retrofits. Autonomous entrants, such as EHang, target urban interface roles, and Rain develops AI drop algorithms that reduce chemical usage.

Regulatory streamlining accelerates VLAT approvals, reducing certification time from 36 to 24 months in 2025, thereby lowering entry barriers. Suppliers that combine airframe, training, and maintenance in turnkey packages gain an edge as agencies favor lifecycle contracting.

Fire Fighting Aircraft Industry Leaders

Airbus SE

Lockheed Martin Corporation

Leonardo S.p.A.

Textron Inc.

Air Tractor, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Spanish government awarded Avincis wildfire response contracts for the Ecological Transition and the Demographic Challenge (MITECO) and the regional government of Castilla-La Mancha, marking a significant addition to its emergency aerial services portfolio. This contract award strengthens Avincis’ operational presence in Spain, complementing its existing agreements with Andalusia, Aragon, the Valencian Community, and Galicia. With 39 fire fighting aircraft and over 300 professionals, the company is strategically positioned to meet the rising demand for aerial fire fighting services. This development underscores the increasing reliance on private operators to support government wildfire mitigation initiatives.

- April 2025: The Department of Transportation and Infrastructure’s USD 14.80 million contract with De Havilland Aircraft of Canada for repairing the province’s fifth CL-415 water bomber represents a strategic move to enhance wildfire management capabilities. Conducted locally by PAL Aerospace, the repair addresses structural damage sustained during a forest fire and ensures operational readiness for the 2026-27 fire season. This initiative highlights the growing demand for resilient fire fighting infrastructure amid escalating climate-related risks. By prioritizing the maintenance of critical assets, the government aims to strengthen disaster response frameworks and mitigate the economic and environmental impacts of forest fires.

Global Fire Fighting Aircraft Market Report Scope

Aerial fire fighting, also known as water bombing, utilizes aircraft and other aerial resources to combat wildfires. Fire fighting aircraft, which include both fixed-wing and rotary-wing aircraft, coordinate with ground crews to contain and extinguish wildfires. These aircraft often form the initial attack force for a fire or provide over-the-fire support during suppression activities for fire fighters on the ground.

The fire fighting aircraft market is segmented by aircraft type, tank capacity, end user, operational range, and geography. By aircraft type, the market is segmented into fixed-wing aircraft, rotorcraft, and unmanned aircraft systems (UAS). By tank capacity, the market is classified into the less than 10,000 liters, 10,000 to 30,000 liters, and more than 40,000 liters segments. By end user, the market is segmented by government agencies and forestry services, military operators, and private contractors and aerial fire fighting firms. By opeational range, the market is segmented into less than 1,000 km, 1,000 to 3,000 km and more than 3,000 km. The report also covers the market sizes and forecasts for the fire fighting aircraft market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Fixed-wing Aircraft |

| Rotorcraft |

| Unmanned Aircraft Systems (UAS) |

| Less than 10,000 liters |

| 10,000 - 30,000 liters |

| More than 40,000 liters |

| Government Agencies and Forestry Services |

| Military Operators |

| Private Contractors and Aerial Firefighting Firms |

| Less than 1,000 km |

| 1,000 to 3,000 km |

| More than 3,000 km |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Greece | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of South Africa | ||

| By Aircraft Type | Fixed-wing Aircraft | ||

| Rotorcraft | |||

| Unmanned Aircraft Systems (UAS) | |||

| By Tank Capacity | Less than 10,000 liters | ||

| 10,000 - 30,000 liters | |||

| More than 40,000 liters | |||

| By End User | Government Agencies and Forestry Services | ||

| Military Operators | |||

| Private Contractors and Aerial Firefighting Firms | |||

| By Operational Range | Less than 1,000 km | ||

| 1,000 to 3,000 km | |||

| More than 3,000 km | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| Spain | |||

| Greece | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| Australia | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of South Africa | |||

Key Questions Answered in the Report

How large is the fire fighting aircraft market in 2026?

The fire fighting aircraft market size reached USD 8.32 billion in 2026 and is projected to climb to USD 11.63 billion by 2031.

What is the expected growth rate for fire fighting aircraft through 2031?

The market is forecasted to register a 6.92% CAGR over the 2026–2031 period.

Which aircraft type is expanding the fastest?

Unmanned aircraft systems (UAS) are projected to post an 8.87% CAGR, the highest among all types, driven by new certifications.

Which region is experiencing the quickest growth?

Asia-Pacific leads with a 7.45% CAGR as Australia and China accelerate sovereign fleet build-outs.

Why are private utilities investing in their own fleets?

Liability exposure from wildfire ignition makes aircraft costs function as insurance, prompting utilities to secure dedicated year-round capacity.

What limits rapid fleet expansion despite rising budgets?

Shortages of experienced pilots and mechanics and tariff-driven avionics delays extend delivery timelines and ground ready aircraft.

Page last updated on: