Aircraft Towbar Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.66 Billion |

| Market Size (2030) | USD 6.06 Billion |

| Growth Rate (2025 - 2030) | 5.39% CAGR |

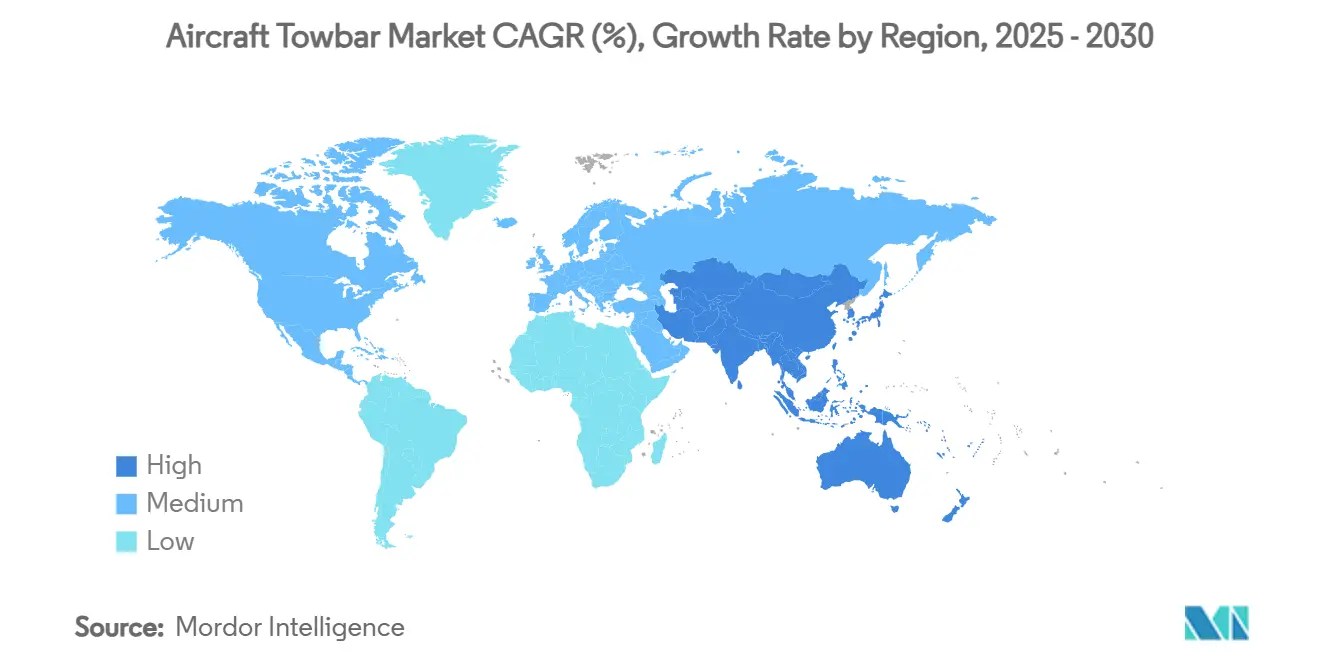

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

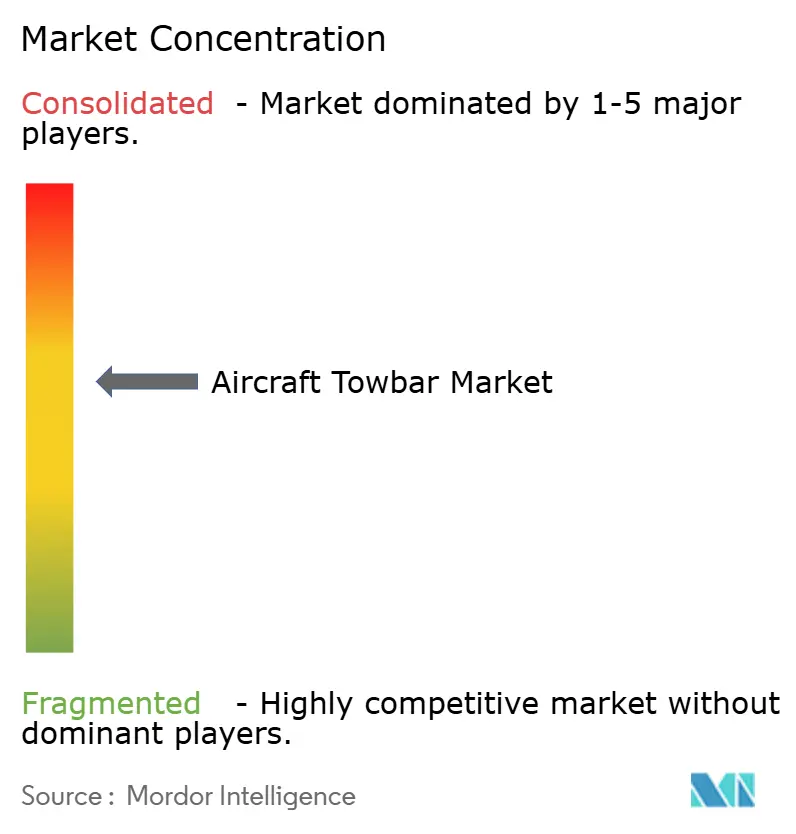

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Towbar Market Analysis by Mordor Intelligence

The aircraft towbar market size is USD 4.66 billion in 2025 and is forecasted to reach USD 6.06 billion by 2030, reflecting a 5.39% CAGR. Growth momentum stems from fleet expansion, sustainability mandates, and rapid airport-infrastructure modernization. Towbar specifications evolve as regulators press for zero-emission ground support equipment, prompting a shift toward electric and composite designs. Consolidation among operators is tightening procurement cycles, while multi-head compatibility solutions lower inventory costs for mixed fleets. Emerging advanced-air-mobility infrastructure, particularly vertiports, is beginning to influence design standards for next-generation equipment. Together, these forces sustain a positive outlook for the aircraft towbar market.

Key Report Takeaways

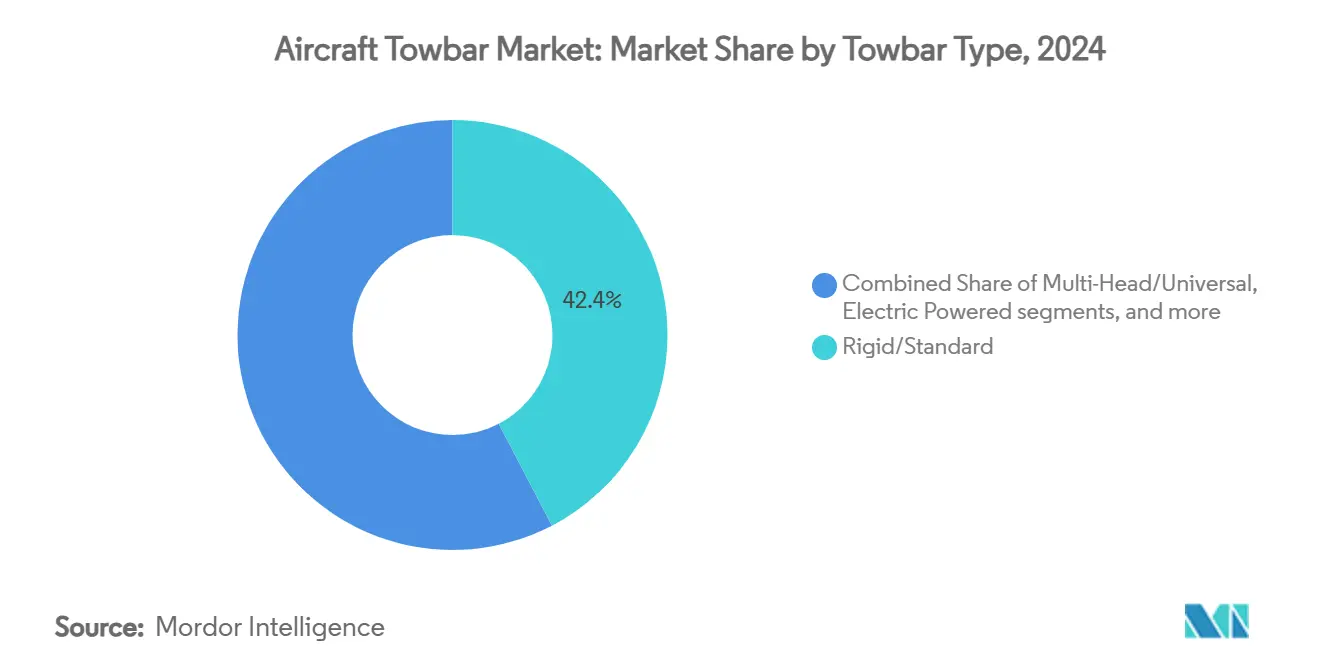

- By towbar type, rigid/standard captured 42.35% of the aircraft towbar market share in 2024; electric/self-powered variants are projected to grow at 7.24% CAGR through 2030.

- By aircraft type, commercial aviation led with 57.54% revenue share in 2024; eVTOL/light electric aircraft are forecasted to expand at 9.65% CAGR through 2030.

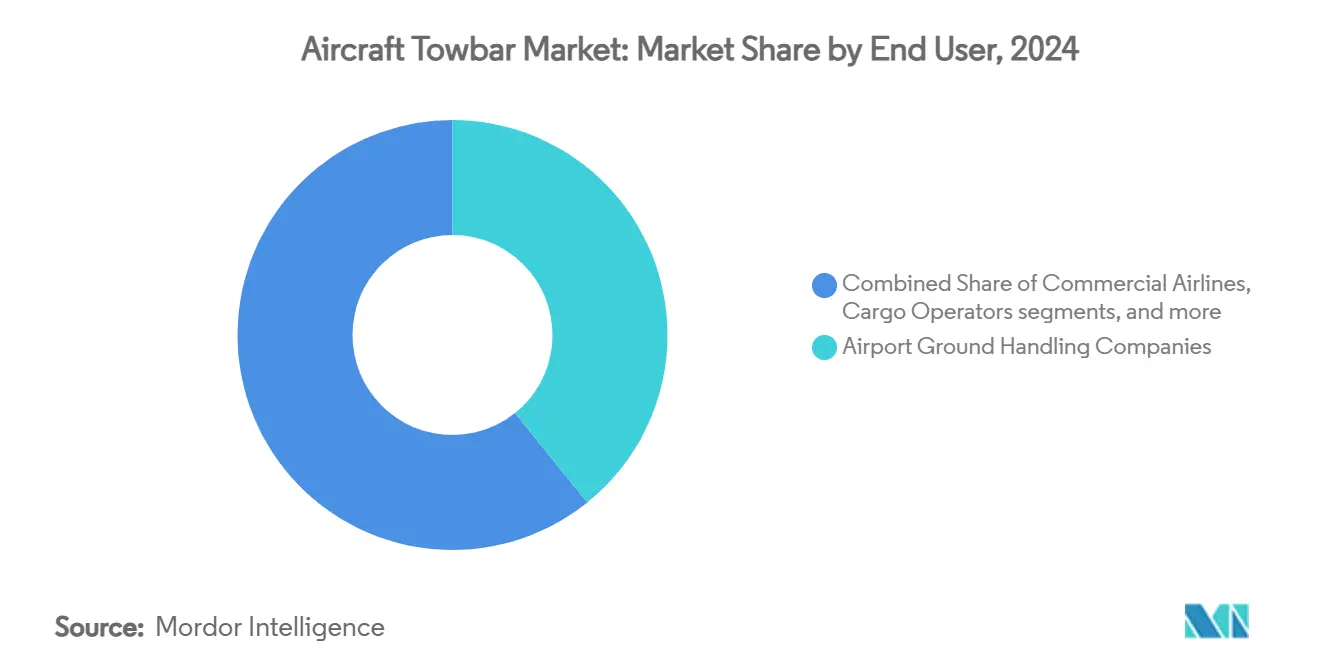

- By end user, airport ground-handling companies held a 39.23% share of the aircraft towbar market in 2024; cargo operators are advancing at a 6.61% CAGR through 2030.

- By material, high-strength steel/chromoly accounted for 34.72% of the aircraft towbar market's size in 2024; composite-fiber towbars are growing at a 7.26% CAGR between 2025 and 2030.

- By geography, North America commanded 42.22% of the aircraft towbar market share in 2024; Asia-Pacific is anticipated to rise at a 5.82% CAGR to 2030.

Global Aircraft Towbar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in global commercial aircraft fleet and MRO demand | +1.2% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Airport infrastructure expansion across emerging economies | +0.8% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Accelerating shift toward electric ground-support equipment mandates | +1.0% | North America and EU leading, expanding to APAC | Short term (≤ 2 years) |

| OEM push for mixed-fleet compatible multi-head towbars | +0.6% | Global, emphasis on major hub airports | Medium term (2-4 years) |

| Ground-handling demand from emerging eVTOL operations | +0.4% | North America and EU early adoption, selective APAC markets | Long term (≥ 4 years) |

| Emergence of towbar leasing/ “equipment-as-a-service” models | +0.5% | Global, faster adoption in cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid growth in global commercial aircraft fleet and MRO demand

Order books for commercial aircraft exceed 13,500 units, extending service lives and keeping legacy jets on the line longer. Older fleets raise maintenance costs about 8.0% per flight hour each additional year of age.[1]Ross A. Brown, “Maintenance Cost Growth in Aging Aircraft,” Defense Acquisition Research Journal, dau.edu As operators prolong aircraft utilization, towbar replacement cycles tighten because ground support equipment ages in tandem with the fleet. Delivery lags from OEMs further postpone retirement schedules, driving a steady requirement for adaptable towbars capable of handling mixed generations of aircraft. Consistent aftermarket demand secures a recurring revenue base for vendors in the aircraft towbar market.

Airport infrastructure expansion across emerging economies

Asia-Pacific hosts 575 active airport projects worth USD 488 billion, with Vietnam’s plan for 30 new airports leading the wave. Stand-alone megaprojects such as Long Thanh International Airport (USD 19.8 billion) and New Manila International Airport (USD 14 billion) integrate next-generation ground-support architecture from inception. New facilities bypass legacy constraints, enabling airports to specify electric and composite towbars at procurement. Scale procurement rounds boost bargaining power for buyers yet open a larger addressable pool for manufacturers. These long-term programs anchor demand visibility through the late-2020s, underpinning the aircraft towbar market.

Accelerating shift toward electric ground-support equipment mandates

California’s Air Resources Board requires zero-emission airport ground-support equipment by 2034, with rule design due in 2027. The Port Authority of New York and New Jersey will phase out internal-combustion airside vehicles by 2030. Delta Air Lines invested USD 385 million in electric GSE, reaching near-total electrification at two hubs.[2]Delta Air Lines Communications, “Tugs, Tractors and Belt Loaders Nearly All Electric at Two Delta Hubs,” news.delta.com Swissport secured EUR 170 million (USD 199.38 million) in revolving credit to finance its electrification roadmap. These regulatory and corporate commitments fuel a decisive pivot toward battery-powered towbars, lifting growth prospects for electric variants within the aircraft towbar market.

OEM push for mixed-fleet compatible multi-head towbars

Airlines increasingly operate diverse fleets spanning narrow-body, wide-body, and new eVTOL platforms. OEMs standardize attachment interfaces to reduce ramp complexity, enabling single towbars to service multiple aircraft types. Tronair markets five core towbar bodies that accept interchangeable heads, simplifying inventory management.[3]Tronair Engineering Team, “How to Choose Between Aircraft Towbar Types,” tronair.com Hub airports gain faster turns when equipment changeovers disappear, restoring operational resilience. Cross-compatibility further supports leasing models because providers can redeploy assets across customers with minimal adaptation, sustaining momentum in the aircraft towbar market.

Cyclic volatility in aircraft production affecting aftermarket sales

Production hiccups, material shortages, and labor disputes create inconsistent aircraft rollout schedules. As deliveries slip, airlines defer fleet renewals, temporarily reducing immediate towbar procurement. Upstream suppliers such as Meggitt and Rolls-Royce have flagged weaker aftermarket revenues, signaling cautious inventory strategies among ground-handling units. Uncertain build rates thus temper short-term purchasing in the aircraft towbar market until schedules stabilize.

Adoption of towbar-less tractors at major hubs

Towbar-less electric tugs eliminate the need for traditional towbars on some movements, lowering future unit demand at high-traffic airports. Taxibot trials at Schiphol and JFK promise up to 85% fuel savings during taxi operations.[4]Airbus Communications, “Taxibots Spool Up as Project HERON Winds Down,” airbus.com Autonomous electric tractors deployed in Hong Kong achieve 35% carbon-cutting performance and 90 km per charge. Though capital-intensive, these systems appeal to scale operators, diverting a slice of potential revenue away from the conventional aircraft towbar market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Towbar Type: Electric Variants Drive Innovation

Electric/self-powered models are forecasted to post a 7.24% CAGR from 2025 – 2030, outpacing rigid/standard designs that still hold a 42.35% baseline share. Rising electricity mandates, growing battery densities, and documented savings in fuel and maintenance costs underpin adoption. Delta’s shift to an all-electric fleet at two major hubs validates operational feasibility. Swissport’s procurement policy requiring electric variants from January 2025 widens the customer base. Rigid units remain essential for cost-sensitive or low-utilization scenarios, keeping volume steady. Multi-head or universal architectures complement both categories, streamlining inventory for mixed fleets and supporting the aircraft towbar market.

Adjustable or telescopic towbars occupy niche use cases where space or aircraft geometry demands extra flexibility. Although growth is modest, these products secure stable revenue among specialized operators. Other configurations—including military or bespoke variants—tap into defense-modernization budgets, where weight, corrosion resistance, and field servicing dominate specifications. Innovations in quick-change hitch systems and integrated diagnostics continue to differentiate offerings across the aircraft towbar industry.

By Aircraft Type: eVTOL Emergence Reshapes Requirements

Commercial aviation retains a 57.54% share, anchored by narrow-body workhorses that deliver high cycle counts and demand rugged equipment. Widebody fleets require heavy-duty towbars with elevated tensile limits, fostering premium price tiers. Meanwhile, the eVTOL/light electric segment will expand at a 9.65% CAGR through 2030, driven by vertiport roll-outs and supportive FAA design guidance.[5]FAA Office of Airports, “EB 105A Vertiport Design,” faa.gov As prototypes transition to certified vehicles, ground services will need ultra-compact, lightweight towbars adapted for tight stands and battery-charging environments.

Military requirements span fighter, transport, and rotorcraft missions, each requiring bespoke geometries and increased tactical durability. Regional jets and general aviation aircraft contribute to a consistent though fragmented demand. Convergence of commercial and emerging aerial-mobility standards will ultimately standardize attachment features, unifying production runs and lowering unit costs, strengthening the long-term trajectory for the aircraft towbar market.

By End User: Cargo Operators Accelerate Adoption

Airport ground-handling companies account for 39.23% of demand, reflecting multi-airline contracts and scale procurement efficiencies. Intensifying e-commerce volumes lift freighter utilization rates, propelling cargo operators to a 6.61% CAGR through 2030. Autonomous electric tractors piloted at Asia Airfreight Terminal showcase cargo-sector readiness to adopt advanced ground equipment. Airlines continue to purchase directly for hubs, where asset control reinforces on-time performance metrics.

Maintenance, repair, and overhaul facilities emphasize high-maneuverability towbars optimized for hangar positioning. Leasing firms are emerging as a fourth pillar, packaging equipment with integrated telematics, maintenance, and refresh guarantees. This service shift increases recurring revenue potential throughout the aircraft towbar market.

By Material: Composite Innovation Gains Momentum

High-strength steel/chromoly leads with 34.72% share, prized for reliability and favorable cost-to-strength ratios. Composite-fiber products, however, are expected to log a 7.26% CAGR as carbon-fiber reinforced polymer (CFRP) usage spreads across aerospace hardware. CFRP’s lightweight improves ergonomics and reduces aircraft damage risk during pushback. Recycling technologies are maturing, unlocking circular-economy pathways and offsetting premium pricing.

Aluminium alloys balance mass and durability, but price volatility driven by global supply bottlenecks threatens short-term affordability. Hybrid or specialty alloys address corrosion or extreme temperature demands in maritime and arctic operations. Environmental levies on carbon-intensive metals accelerate R&D into alternative matrices, sustaining innovation momentum inside the aircraft towbar market.

Geography Analysis

North America retains dominance due to robust infrastructure spending and determined regulatory timelines. The Port Authority of New York and New Jersey’s 2030 internal-combustion phase-out catalyzes early procurement cycles. California’s 2034 zero-emission deadline and 2027 program milestones prompt airports and handlers to prioritize battery-powered assets. Early pilots of towbar-less, semi-robotic solutions such as Taxibot confirm regional operational savings.

Asia-Pacific’s airport pipeline, including Vietnam’s 30-airport master plan and megaprojects in the Philippines and Singapore, guarantees sustained equipment orders through the decade. Cargo facilities in Hong Kong are already using autonomous electric tractors, proving readiness to implement sophisticated ground service technologies at scale. Regulators across the region increasingly echo US and EU sustainability targets, suggesting demand acceleration from the late 2020s onward.

Europe’s policy architecture, highlighted by AENA’s 2026 fully sustainable vehicle objective, drives near-term conversions to electric fleets. Meanwhile, EASA’s forthcoming ground-handling regulation codifies maintenance and training obligations that favor premium towbar suppliers with integrated support offerings. Funding instruments and cooperative purchasing initiatives lower adoption barriers, furthering consistent though moderate growth in the aircraft towbar market.

Competitive Landscape

The market is moderately consolidated, with technology, service depth, and financing terms differentiating leading brands. Tronair's modular towbars leverage interchangeable heads for cross-fleet compatibility, reducing handlers' inventory loads. TLD Group extends competitiveness with TractEasy autonomous tractors and TaxiBot semi-robotic tugs, blending automation with sustainability. JBT AeroTech complements its towbarless tug range by bundling predictive-maintenance software, enhancing lifecycle value.

Strategic alliances broaden portfolios: Lufthansa LEOS pairs aircraft-towing expertise with complete fleet-management services, positioning as a one-stop provider. Lockheed Martin and Lufthansa Technik jointly target integrated sustainment, underscoring cross-sector collaboration to capture aftermarket share.[6]Lockheed Martin, “Lockheed Martin and Lufthansa Technik Expand Cooperation,” lockheedmartin.com Disruptive entrants focus on autonomous robotic platforms and advanced powertrains, forging partnerships with incumbents to accelerate commercialization. Financing innovations such as equipment-as-a-service platforms gain traction, driving recurring income models across the aircraft towbar market.

Aircraft Towbar Industry Leaders

Clyde Machines Inc.

HYDRO Systems GmbH & Co. KG

TowFLEXX Inc.

AERO Specialties, Inc.

Tronair Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dnata allocated USD 210 million to sustainable ground-support equipment, marking one of the sector’s largest single electrification investments.

- April 2025: Air Canada converted Québec City ground operations to a fully electric main-GSE fleet, setting a replicable electrification template.

- January 2025: JFK Terminal One debuted the world’s first fully electric ground-handling fleet, intensifying competitive pressure on peer hubs.

- July 2024: Aurrigo delivered its autonomous Auto-DollyTug to Stuttgart Airport, expanding automated GSE adoption.

Global Aircraft Towbar Market Report Scope

| Rigid/Standard |

| Multi-Head/Universal |

| Adjustable/Telescopic |

| Electric/Self-Powered |

| Other Towbar Types |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Fighter Jets |

| Transport Aircraft | |

| Rotorcraft | |

| General Aviation | |

| eVTOL/Light Electric Aircraft |

| Commercial Airlines |

| Cargo Operators |

| Airport Ground Handling Companies |

| MRO and Line Maintenance Facilities |

| Other End-Users |

| Steel-Alloy Towbars |

| Aluminium-Alloy Towbars |

| High-Strength Steel/Chromoly |

| Composite-Fiber Towbars |

| Other Materials |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of South Africa | ||

| By Towbar Type | Rigid/Standard | ||

| Multi-Head/Universal | |||

| Adjustable/Telescopic | |||

| Electric/Self-Powered | |||

| Other Towbar Types | |||

| By Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Fighter Jets | ||

| Transport Aircraft | |||

| Rotorcraft | |||

| General Aviation | |||

| eVTOL/Light Electric Aircraft | |||

| By End User | Commercial Airlines | ||

| Cargo Operators | |||

| Airport Ground Handling Companies | |||

| MRO and Line Maintenance Facilities | |||

| Other End-Users | |||

| By Material | Steel-Alloy Towbars | ||

| Aluminium-Alloy Towbars | |||

| High-Strength Steel/Chromoly | |||

| Composite-Fiber Towbars | |||

| Other Materials | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of South Africa | |||

Key Questions Answered in the Report

What is the projected value of the aircraft towbar market by 2030?

The market is forecasted to reach USD 6.06 billion by 2030, growing at a 5.39% CAGR.

Which towbar segment is expanding the fastest?

Electric/self-powered units lead with a projected 7.24% CAGR through 2030 due to zero-emission mandates.

How significant is Asia-Pacific to future growth?

Asia-Pacific is expected to post a 5.82% CAGR thanks to USD 488 billion in airport construction, making it the fastest-growing regional market.

Why are composite-fiber towbars gaining momentum?

Composites cut weight, improve ergonomics and align with carbon-reduction policies, driving a 7.26% CAGR for this material segment.

What impact do towbar-less tractors have on the market?

Towbar-less tractors can displace traditional towbars at major hubs, exerting a -0.5% drag on overall CAGR yet presenting complementary opportunities for autonomous technology suppliers.

Which end-user group shows the highest growth?

Cargo operators are projected to grow at 6.61% CAGR as e-commerce logistics fuel freighter activity, boosting demand for specialized ground support equipment.

Page last updated on: