Tanker Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 4.98 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

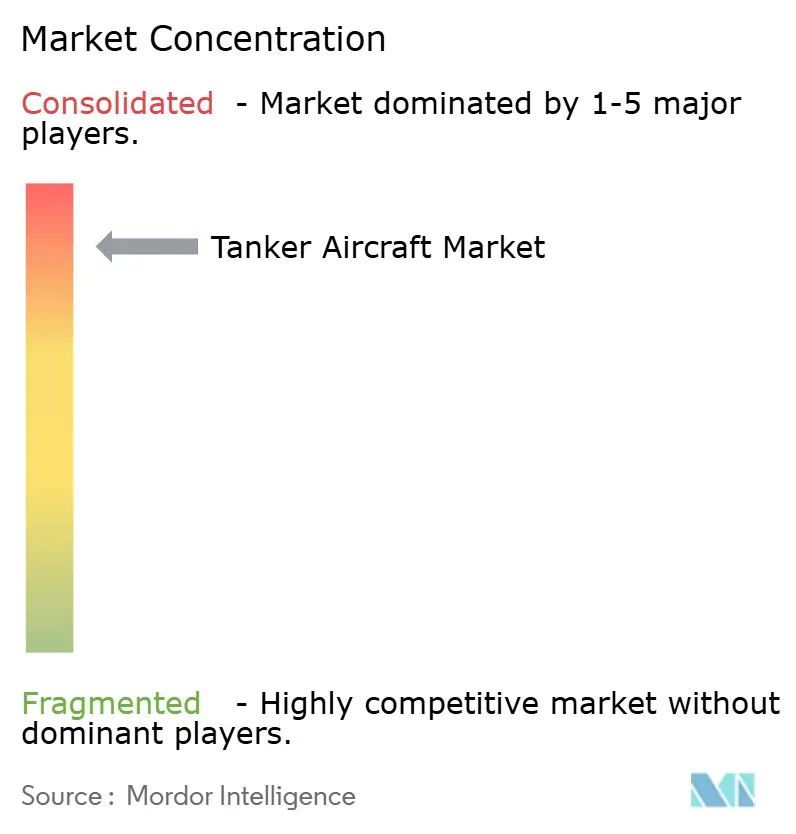

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tanker Aircraft Market Analysis by Mordor Intelligence

The tanker aircraft market size is expected to grow from USD 3.41 billion in 2025 to USD 3.69 billion in 2026 and is forecasted to reach USD 4.98 billion by 2031 at a 6.18% CAGR over 2026-2031. Modernization cycles are converging with fifth-generation integration requirements, keeping programs like the KC-46 under scrutiny as deliveries resume after a pause due to structural findings. Operational realities in the Indo-Pacific and Europe keep demand elevated, from NATO pooled fleets that expand shared capacity to US recapitalization agendas that bridge capability gaps through the next decade. Technology priorities are shifting toward automation and networked operations, as seen in Singapore’s certification of automatic boom refueling and the US Navy’s unmanned refueling roadmap for carrier operations. Cost pressure remains a theme, including fixed-price exposure on the KC-46 and the premium on sustainable aviation fuel, which sits well above that of conventional jet fuel, shaping fleet economics and sustainment plans in the tanker aircraft market.

Key Report Takeaways

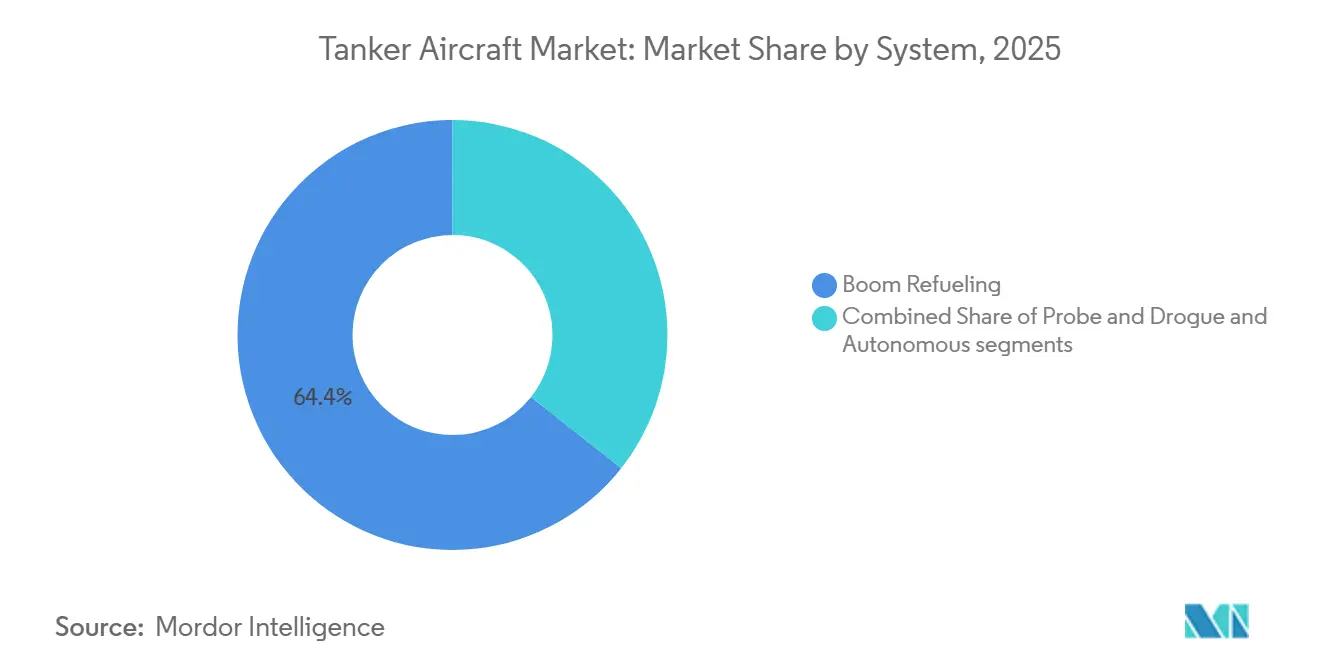

- By system, boom refueling accounted for 64.37% of the tanker aircraft market share in 2025, while autonomous configurations are set to expand at a 9.65% CAGR through 2031.

- By propulsion type, turbofan platforms commanded 76.55% market share in 2025 and are projected to grow at an 8.86% CAGR through 2031.

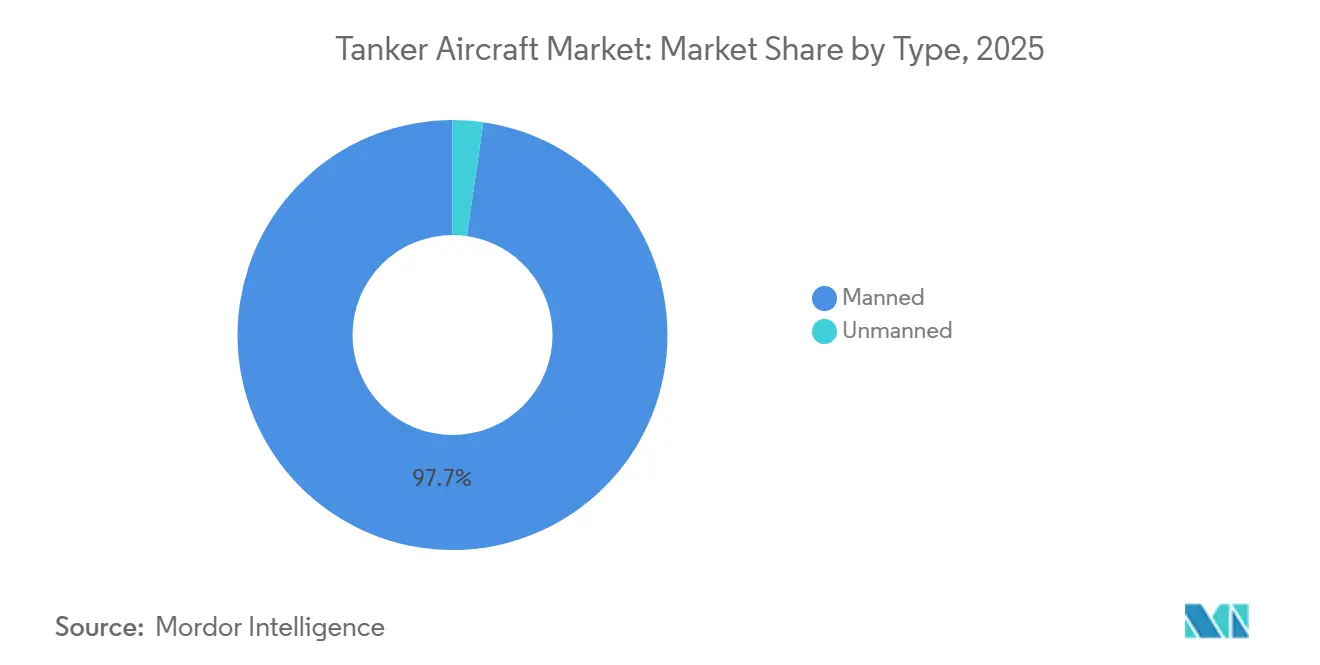

- By type, manned platforms held a 97.71% share of the tanker aircraft market in 2025, while unmanned platforms are projected to grow at a 10.01% CAGR through 2031.

- By point of sale, original equipment manufacturers captured 82.26% of the tanker aircraft market in 2025, while aftermarket services are forecasted to advance at a 7.98% CAGR through 2031.

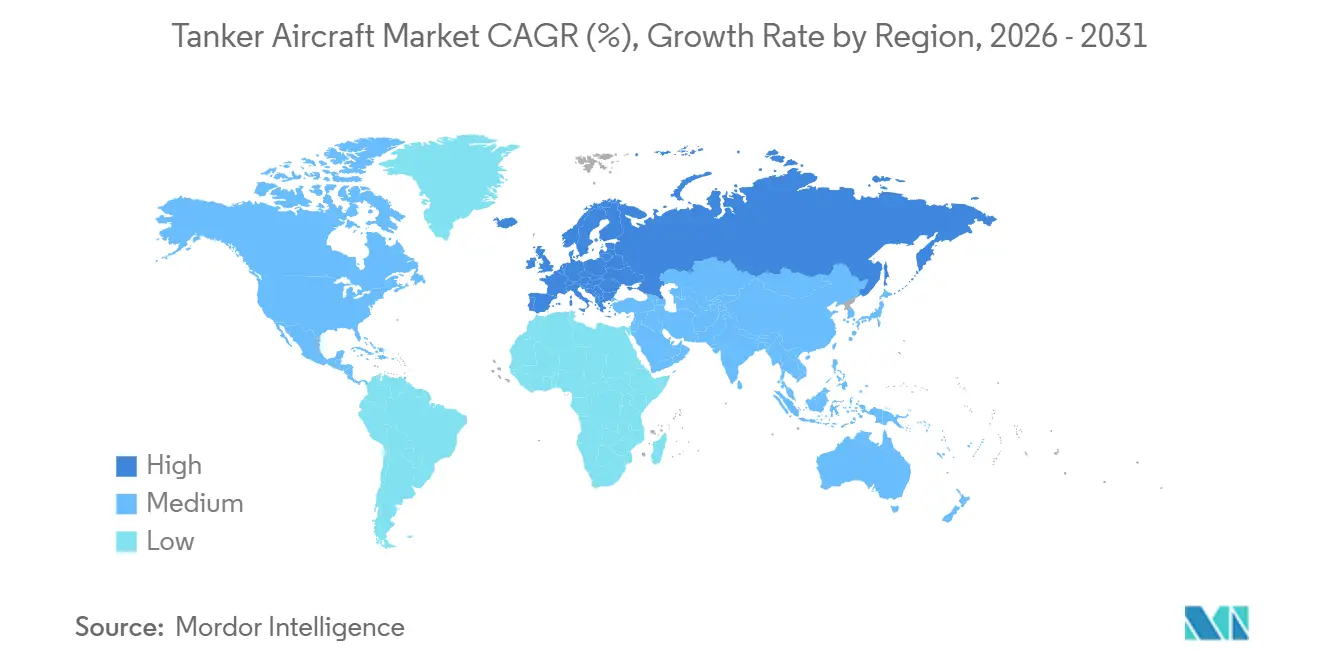

- By geography, North America held 34.47% in 2025, while Europe is the fastest-growing region at an 8.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tanker Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet recapitalization programs (KC‑46A, A330 MRTT) accelerating across US, NATO, and allies | + 2.1% | North America, Europe, APAC core | Medium term (2-4 years) |

| Asia-Pacific defense spending and Indo‑Pacific range requirements expanding tanker demand | + 1.3% | Asia-Pacific, spillover to North America | Long term (≥ 4 years) |

| NATO/European pooled capacity (MMF) and F‑35 adoption driving interoperability | + 0.9% | Europe, extending to NATO partners | Medium term (2-4 years) |

| 5th‑gen integration and networked ops requiring advanced boom/drogue and connectivity | + 0.7% | Global, concentrated in F-35 operators | Medium term (2-4 years) |

| Contractor‑operated AAR services for training, surge, and transits gaining traction | + 0.5% | North America with APAC and Europe expansion | Short term (≤ 2 years) |

| Autonomy and uncrewed tankers (MQ‑25 pathfinding; A3R/auto‑boom) enabling new CONOPS | + 0.8% | North America, Asia-Pacific, early Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Recapitalization Programs Accelerating Operational Readiness Amid Legacy Gaps

Recapitalization underpins readiness as air forces prioritize new airframes and capability insertions to replace legacy fleets that face age and integration constraints. The KC-46 program illustrates how certification timelines can govern delivery cadence more than appropriation trends, with 2026 marked by a new charge that kept attention on production and retrofit plans. Deliveries resumed after a 2025 halt due to structural findings, underscoring the need for stable manufacturing and test pipelines as operators aim to meet availability targets in the tanker aircraft market. NATO’s Multinational MRTT Fleet continues to expand pooled capacity to 12 aircraft by 2029, a model that increases access for smaller contributors and spreads operating hours across a common configuration.[1]“NATO Orders 2 Additional Airbus A330 MRTT Aircraft,” Airbus, airbus.com Program choices in 2026 also reflect fiscal signaling, as the US allocates limited funds for next-generation tanker studies while continuing near-term upgrades and buys that bridge to future concepts. European operators, meanwhile, are adding interoperable fleets aligned with A330 MRTT standards that support multi-nation missions and speed joint certification timelines for fifth-generation receivers.

APAC Defense Expenditure Fueling Long-Range Power Projection Infrastructure

Operational distances across the Indo-Pacific drive sustained demand for tanker capacity, as planners account for longer transit profiles and more distant tanker orbits to support strike and patrol missions, extending the emphasis on platforms that balance fuel offload, range, and interoperability with allied receivers, because coalition operations require consistent clearances and compliant refueling hardware in the tanker aircraft market. As programs evolve, automation is moving from demonstration to certification, as evidenced by Singapore’s full certification for automatic boom refueling, which anchors day-and-night operations with fighter receivers. Regional sustainment budgets continue to prioritize upgrades that add receiver types and datalink enhancements, which reduce certification bottlenecks during multi-asset missions. US budget documents in 2026 point to the continuing need to align platform capabilities with adversary range and survivability challenges, which keep tanker modernization closely tied to broader force design choices.

NATO Pooling Architectures Redefining European Strategic Autonomy

Pooling architectures are reshaping Europe’s tanker access by bringing additional aircraft into a shared fleet and distributing availability across several operating bases. The Multinational MRTT Fleet’s planned growth to 12 aircraft by 2029 improves access for smaller air forces through flight-hour sharing and standardizes technical baselines that ease multi-country operations. Exercises continue to highlight tanker density as a binding constraint for surge operations, thereby raising the premium on interoperability and mission-ready aircraft in the tanker market. European air forces are also emphasizing multi-role flexibility that covers refueling, transport, and medical evacuation, which supports budget efficiency and joint tasking. Airframers are leaning into configuration commonality across fleets to simplify training, spare parts, and depot activities, reducing downtime and easing multinational deployments. The net effect is a step-up in regional resilience and alignment with fifth-generation aircraft, with a path to greater operational autonomy.

Fifth-Generation Integration Demands Rewriting Boom-Operator Training and Certification

Fifth-generation receivers introduce specific requirements for contact loads, coating protection, and low-visibility operations, raising the bar for refueling systems and crew procedures. The KC-46 Remote Vision System 2.0 schedule slipped to summer 2027, underscoring the continued emphasis on retrofit timelines and operator training as units manage the transition while maintaining availability. In parallel, Singapore’s automatic boom refueling certification demonstrates how sensor fusion and autonomy reduce crew workload and improve consistency across contact conditions, which provides a model for future manned and unmanned concepts in the tanker aircraft market. OEMs are expanding night refueling and connectivity features that enable tankers to manage multi-asset flows and support C2 roles intertwined with logistics and ISR. NATO exercises continue to spotlight datalink interoperability and in-flight coordination as tasking becomes more dynamic, pushing standardization across mixed fleets. Together, these advances move the tanker role from a pure logistics function toward a networked force multiplier.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification/integration hurdles causing delays and cost overruns | - 1.2% | Global, acute in US and Europe | Short term (≤ 2 years) |

| Export controls/sovereignty limits on boom/RVS and mission systems tech transfer | - 0.6% | International markets | Medium term (2-4 years) |

| High acquisition and life‑cycle costs vs conversions/pooling/leases | - 0.4% | Global, smaller air forces impacted | Long term (≥ 4 years) |

| SAF availability and environmental/airspace constraints on tanker ops | - 0.2% | Global, stronger in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Certification Timelines and Cost Overruns Constraining Delivery Cadence

Fixed-price contracts and complex retrofit paths expose programs to financial charges and schedule pressure, which can ripple through fleet availability and training pipelines. In 2026, a new KC-46 charge underscored the challenge of maturing systems under firm pricing while sustaining deliveries and upgrades required for operational use in the tanker aircraft market.[2]Courtney Albon, “Boeing Takes First KC-46 Charge Since 2024,” Air & Space Forces Magazine, airandspaceforces.com Production and acceptance pacing is also influenced by the resolution of critical deficiencies and by the sequencing of certification activities that must be coordinated across service and regulatory stakeholders. Visual systems and boom control improvements remain a key dependency for fifth-generation receiver operations, which keeps fielding milestones tied to test campaigns and retrofit slots. These realities push planners to balance new procurement with sustainment upgrades, so training and mission availability do not suffer while programs advance through certification gates. The overall effect is a delivery cadence that must balance safety-first validation with near-term operational needs.

Export Controls and Sovereignty Constraints Fragmenting Supply Chains

Export licensing and sovereignty requirements shape platform selection, sustainment concepts, and timelines for international customers that need both interoperability and independent maintenance authority. In regions that emphasize pooled capacity and multi-national use, shared fleets reduce some sovereignty friction by anchoring on common configurations and centralized lifecycle management. OEM content and configuration control policies can limit third-party modifications, thereby concentrating aftermarket pathways with the original manufacturer and lengthening negotiation cycles for local industry participation in the tanker aircraft market. Budget plans and acquisition governance also influence whether nations prioritize new-build platforms or conversions, especially where strategic autonomy objectives guide industry. These factors combine to determine delivery timelines, cost structures, and the degree of domestic control over upgrades and mission systems throughout a fleet's lifespan.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Autonomous Configurations Challenge Boom Dominance Through Operational-Cost Arbitrage

Boom refueling captured 64.37% of the tanker aircraft market size in 2025, supported by high transfer rates that favor large receiver operations, while autonomous configurations are projected to grow at a 9.65% CAGR through 2031 as certification advances broaden use cases. Boom systems, engineered for high throughput, remain advantageous for heavy aircraft and extended-range fighter packages. Automation is shifting procedures and crew models, reducing operator workload and improving safety margins and mission timelines. The US Navy’s roadmap for unmanned refueling at sea highlights the potential for redirecting manned aircraft to primary missions while unmanned assets deliver fuel. Podded systems retain an edge with naval and European operators due to their integration with existing fighters and multi-point refueling capabilities. However, boom dominance persists for large offload missions and advanced fleets.

A mixed-method future is emerging as air forces require both methods for operations spanning strategic airlift support, distributed fighter patrols, and quick-turn transit refuelings. Automation is expected to expand as certification templates evolve, shortening approval timelines. Sensor fusion, including advanced imaging, is enhancing positioning and contact stability, reducing fatigue and training demands. With more networks and data links onboard, tankers now support deconfliction and task updates while airborne, emphasizing system interoperability alongside fuel-offload capacity. These advancements pave the way for autonomy and operator-assist functions to grow across both boom and probe-and-drogue systems as mission complexity increases.

By Propulsion Type: Turbofan Platforms Consolidate Through Supply-Chain Maturity

Turbofan platforms commanded 76.55% of the tanker aircraft market share in 2025 and are projected to grow at an 8.86% CAGR through 2031, supported by commercial airliner production lines and shared depot ecosystems. The underlying maintainability and time-on-wing advantages of mid to large turbofans support long mission cycles and predictable overhaul intervals, which reduce fleet downtime and stabilize sortie generation in the tanker aircraft market. Turboprop platforms remain valued for short-field operations and multi-role flexibility. Still, strategic refueling missions that require long range and high cruise speeds continue to favor turbofans for most national fleets. OEMs are adding fuel-burn improvements and electronics upgrades in mid-life packages, extending platform relevance and reducing per-sortie costs without requiring new airframe purchases. Where runway length is constrained, tactical transports with secondary tanking roles keep their utility for agile operations and dispersed basing.

Supply chains that serve both defense and commercial customers underpin the availability of engines, landing gear, avionics, and structures, thereby supporting lifecycle cost control over decades. Commercial heritage provides economies of scale in spares and maintenance, and supports standardization of training across mixed-use depots. Tactical transports that fill refueling roles meanwhile benefit from robust training device ecosystems that keep aircrew current at lower cost, which contributes to mission-ready rates even as airframes age. The net result is an installed base that remains biased toward turbofans for strategic missions and toward a mix of turbofans and turboprops for flexible, short-field assignments that complement mainline fleets.

By Type: Unmanned Systems Disrupt Crew-Cost Structures Despite 2027 IOC Horizon

Manned tankers retained 97.71% of the tanker aircraft market size in 2025, while unmanned platforms are projected to grow at a 10.01% CAGR as programs move from test points to operational integration. The US Navy’s MQ-25 program shows how unmanned refueling can reduce the tanking burden on manned strike fighters and improve deck-cycle efficiency during high-tempo operations. Carrier suitability, stored footprint, and integration with shipboard command centers are defining early-adopter criteria that influence the rollout pace and crew training models. As automation increases confidence, unmanned refuelers are set to shoulder more routine tanker sorties, allowing manned tankers to focus on longer offloads and operations in contested environments in the tanker aircraft market.

Integration will likely unfold in stages as navies and air forces qualify more receiver types and refine airspace procedures for mixed manned and unmanned operations. Data links, autonomy levels, and human-on-the-loop oversight will be tailored to mission risk, which shapes certification plans and crew resourcing. OEMs are already positioning for pilot-optional futures in which platforms can switch between crewed and uncrewed modes under specific conditions. Over time, this mix could rebalance fleet economics as operators distribute missions to the lowest-cost, lowest-risk asset that meets the task.

By Point of Sale: Aftermarket Gains Traction as Service-Life Extensions Delay Replacement Cycles

Original equipment manufacturers captured 82.26% in 2025, but aftermarket services are set to expand at a 7.98% CAGR as fleet-life extensions and connectivity upgrades absorb a larger share of budgets. The 2026 US budget outlines continued investments in capability improvements for in-service fleets, including communications and mission system enhancements that enhance the installed base in the tanker aircraft market. For several operators, mid-life upgrades to compatible receiver lists, avionics, and night refueling features extend the operational window and defer capital outlays. These upgrades also deepen OEM relationships through proprietary software and configuration control, which shapes long-term service contracts and parts pipelines.

Contractor-operated aerial refueling continues to add training capacity and backstop peacetime proficiency without drawing on military fleets. The landmark refueling of an Air Mobility Command C-17 from a commercial tanker in 2025 expanded the remit for contracted sorties. It introduced additional supply options for schedulers in the tanker aircraft market. This model is not a substitute for combat-ready capacity, but it reduces stress on military aircraft during training surges and pre-deployment workups. For OEMs, aftermarket expansion overlaps with these trends as new software drops, spare kits, and remote diagnostics blend with operator-specific mission needs.

Geography Analysis

North America accounted for 34.47% of the tanker aircraft market share in 2025 as the US sustained the largest global fleet and continued investments in modernization. The region’s priorities include addressing certification dependencies on critical systems like remote vision and connectivity, as well as balancing new procurement with retrofit activity to sustain mission-ready rates. Budget documents in 2026 reinforce a bridge strategy that funds near-term capability improvements while maintaining room for future concept maturation aligned with evolving survivability needs. Contractors are also playing a larger supporting role in peacetime, which expands options for training hours and easing fleet utilization cycles. This blend of procurement, sustainment, and contracted capacity underpins the tanker aircraft market in the region.

Europe is the fastest-growing region, with an 8.16% CAGR through 2031, propelled by pooled fleets and national programs that strengthen interoperability and readiness. The Multinational MRTT fleet’s expansion to 12 aircraft by 2029 enhances multi-country access and encourages standardization in equipment, training, and certification frameworks that can scale across allied operations. Exercises underscore the need for additional tanker density during surge operations, and mixed fleets are improving datalink compatibility and night operations to extend mission windows. OEM production plans and mid-life upgrade paths are designed to meet this demand curve, while common standards can shorten receiver certifications. The result is a stronger operating backbone that supports both national and alliance-level tasking in the tanker aircraft market.

Asia-Pacific adds demand linked to long-range mission profiles and allied interoperability aims, while individual nations calibrate fleet choices against basing constraints and mission mixes. Certified automation is emerging as a differentiator in the region, as seen with Singapore’s fully approved automatic boom refueling, which can be leveraged to improve consistency and reduce crew workload during extended sorties. Mid-life upgrades and additional receiver certifications are also in focus, broadening mission flexibility without major capital programs. Across the broader region, OEMs with commercial heritage are well-positioned due to shared depot infrastructure and spares ecosystems that support mission readiness and lifecycle cost control in the tanker aircraft market.

Competitive Landscape

The tanker aircraft market exhibits an oligopolistic structure, anchored by two global primes that dominate new-build programs, alongside niche and mid-market entrants. In the US, the KC-46 program's 2026 charge highlighted the strain of fixed-price terms as the program matured, systems were developed, and certifications pursued, while the US Air Force maintained momentum through upgrades and deliveries. In Europe and across many export markets, the A330 MRTT family continues to consolidate share as pooled fleets scale and additional aircraft join multinational programs that elevate interoperability and training commonality. The balance of power is reinforced by commercial-lineage supply chains, certification experience, and installed-base leverage that lower risk for buyers seeking predictable timelines in the tanker aircraft market.

Strategic moves in 2026 focus on automation, connectivity, and breadth of sustainment. Singapore's certified automatic boom capability has set a benchmark for autonomous assist in operational units, likely guiding future upgrades among current and prospective operators. The US Navy's MQ-25 effort underscores a complementary path where unmanned assets absorb deck-cycle tanking and free manned aircraft for strike and air-defense roles, which could influence force structure and procurement mixes over the medium term.[3]“MQ-25 Stingray,” Boeing, boeing.com In parallel, contractor-operated refueling added a new milestone with an AMC C-17 refueling event in 2025, which strengthens the case for contracted peacetime training capacity as services preserve organic tankers for deployment priorities.

OEMs are also positioning services and upgrades to build lifetime value around installed fleets, including new software builds, communications suites, and night refueling enhancements. These moves secure recurring revenues, support availability targets, and deepen ecosystem ties with air force customers in the tanker aircraft market. For entrants and conversion specialists, export control realities and configuration control policies shape market access and timelines, which place a premium on partnerships, shared standards, and pooled purchase frameworks for scale. The competitive pattern suggests that market share will remain concentrated among a small group of airframers with strong sustainment franchises and proven certification pathways.

Tanker Aircraft Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Airbus SE

Israel Aerospace Industries Ltd.

United Aircraft Corporation (Rostec)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Airbus and Singapore successfully obtained full certification for the Automatic Air-to-Air Refueling (A3R) capability on the A330 MRTT aircraft. The certification was issued by the Spanish National Institute for Aerospace Technology (INTA) after a comprehensive qualification and flight-test campaign conducted in collaboration with the Republic of Singapore Air Force (RSAF) and the Defence Science and Technology Agency (DSTA).

- September 2025: The Royal Thai Air Force (RTAF) placed an order for an A330 MRTT+ aircraft. This A330neo-based version of the proven aerial refueling and transport aircraft, the A330 MRTT, will feature both hose-and-drogue and boom refueling systems. Additionally, it will include the Airbus Medical Evacuation kit solution and will be configured with a VVIP cabin.

Global Tanker Aircraft Market Report Scope

The tanker aircraft provides air-to-air refueling, the process of transferring aviation fuel from one aircraft to another during flight.

The tanker aircraft market is segmented by system, propulsion type, type, point of sale, and geography. By system, the market is segmented into probe-and-drogue, boom refueling, and autonomous. By propulsion type, the market is segmented into turboprop and turbofan. By type, the market is segmented into manned and unmanned. By point of sale, the market is classified into OEM and aftermarket. The report also covers the market sizes and forecasts for the tanker aircraft market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Probe and Drogue |

| Boom Refueling |

| Autonomous |

| Turboprop |

| Turbofan |

| Manned |

| Unmanned |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System | Probe and Drogue | ||

| Boom Refueling | |||

| Autonomous | |||

| By Propulsion Type | Turboprop | ||

| Turbofan | |||

| By Type | Manned | ||

| Unmanned | |||

| By Point of Sale | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the tanker aircraft market growth outlook to 2031?

The tanker aircraft market is projected to grow from USD 3.69 billion in 2026 to USD 4.98 billion by 2031 at a 6.18% CAGR, supported by recapitalization, automation, and pooled European capacity.

Which refueling method leads in the tanker aircraft market and why?

Boom refueling leads due to higher transfer rates and alignment with fifth-generation receiver needs, while automation and multi-point pods expand the role of probe-and-drogue for naval and European fleets.

How are automation and unmanned systems changing tanker operations?

Certified automatic boom refueling reduces crew workload and improves consistency, and the MQ-25 roadmap shows how unmanned assets can take on deck-cycle tanking, freeing manned aircraft for primary missions.

Why is Europe the fastest-growing region in the tanker aircraft market?

Europe is scaling pooled MRTT fleets and standardizing across nations, which speeds certification and improves access for smaller air forces, lifting growth through 2031.

What constraints could slow tanker aircraft market expansion?

Certification timelines, life-cycle costs, export controls, and sustainable aviation fuel availability can strain schedules and budgets, which may temper growth in the near term.

How are contractors affecting tanker training capacity in the US?

Contractor-operated refueling expanded in 2025 when a commercial tanker refueled an AMC C-17, adding peacetime training capacity and easing utilization for military fleets.

Page last updated on: