Aircraft Mounts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

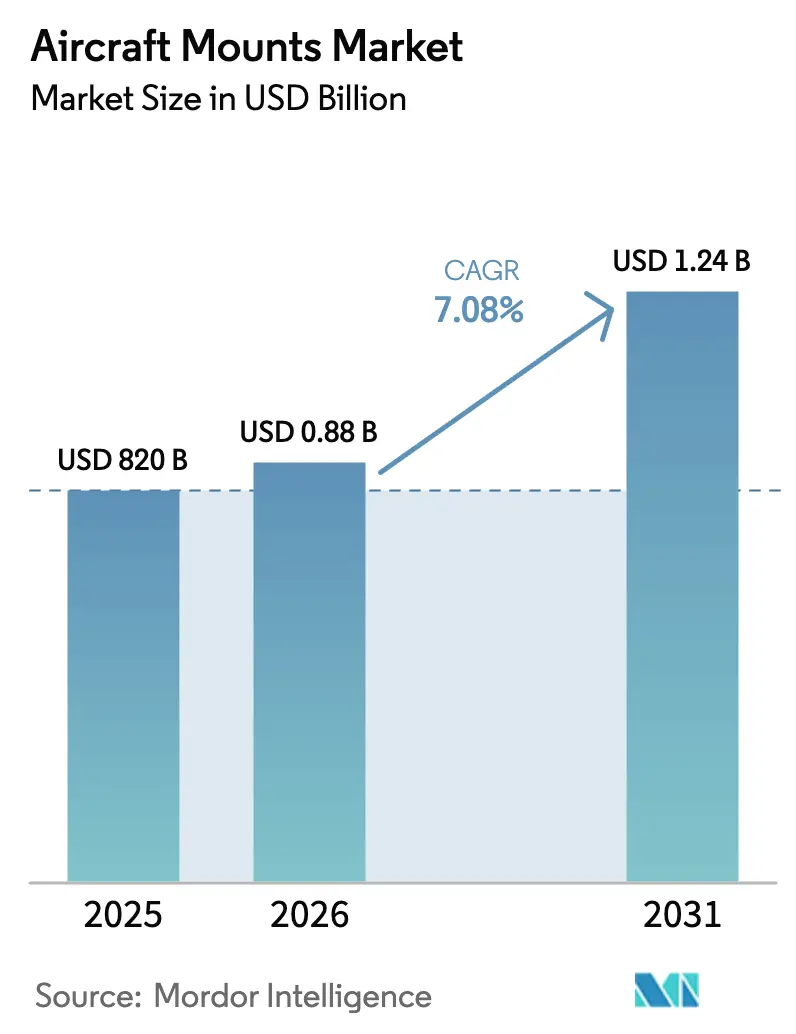

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

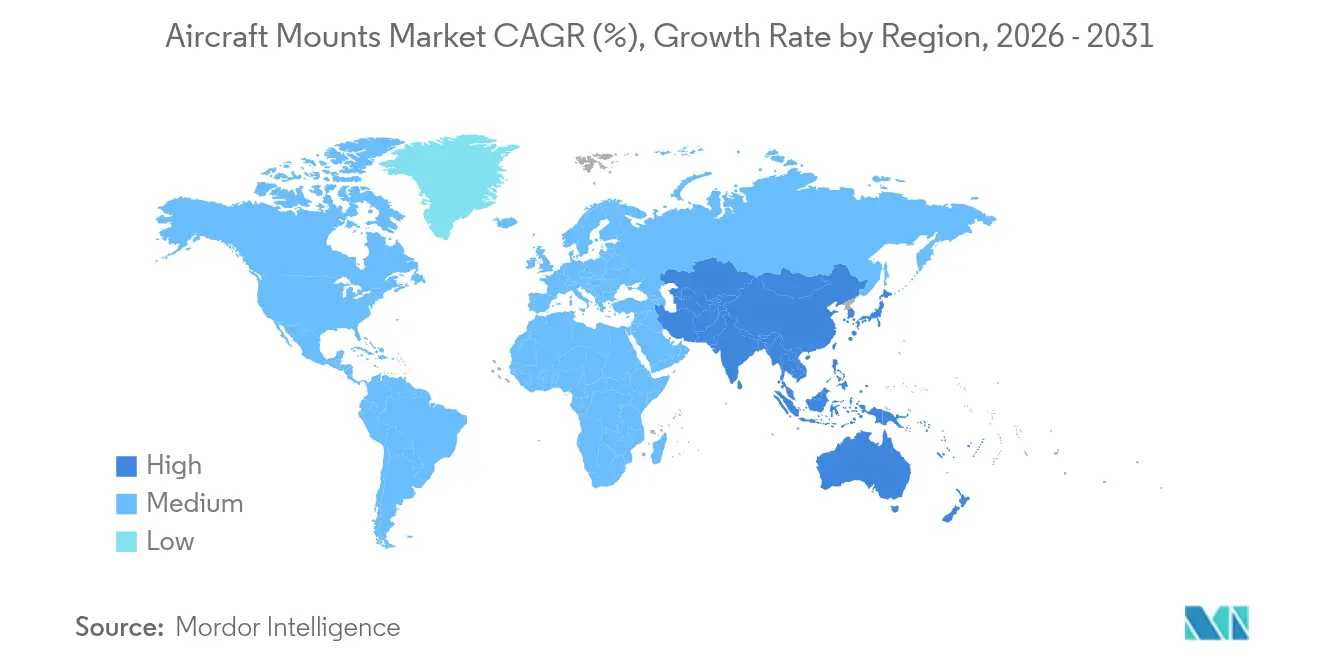

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Mounts Market Analysis by Mordor Intelligence

The aircraft mount market size was valued at USD 820 million in 2025 and estimated to grow from USD 880 million in 2026 to reach USD 1.24 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031). Elevated commercial aircraft build rates, expanding electrified-propulsion programs, and the surge in premium-cabin retrofits collectively lifted demand for mount systems that balance vibration isolation with rising thermal-management loads. Boeing’s plan to lift B737 output from 38 to around 50 jets a month by 2026 and Airbus’ ramp of A350 production to 12 units a month highlighted how OEM production intensity has eclipsed pre-2020 levels. Electrified propulsion placed new design pressure on mounts because battery packs generated 75% of total thermal loads during take-off and cruise transitions. At the same time, raw-material cost swings in titanium and specialty steels compressed supplier margins and extended lead times

Key Report Takeaways

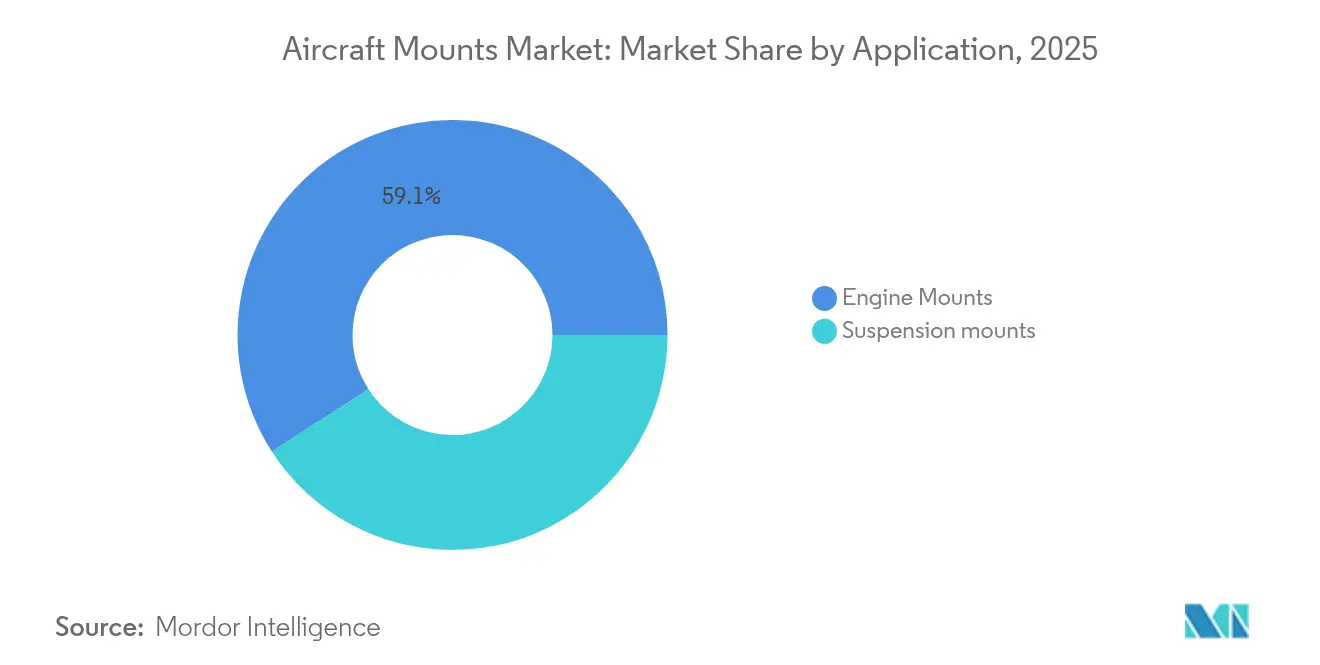

- By application, engine mounts led with 59.12% revenue share in 2025; suspension mounts are projected to expand at a 7.45% CAGR to 2031.

- By mount type, exterior applications captured 64.92% of the aircraft mount market share in 2025; interior mounts are advancing at a 7.85% CAGR through 2031.

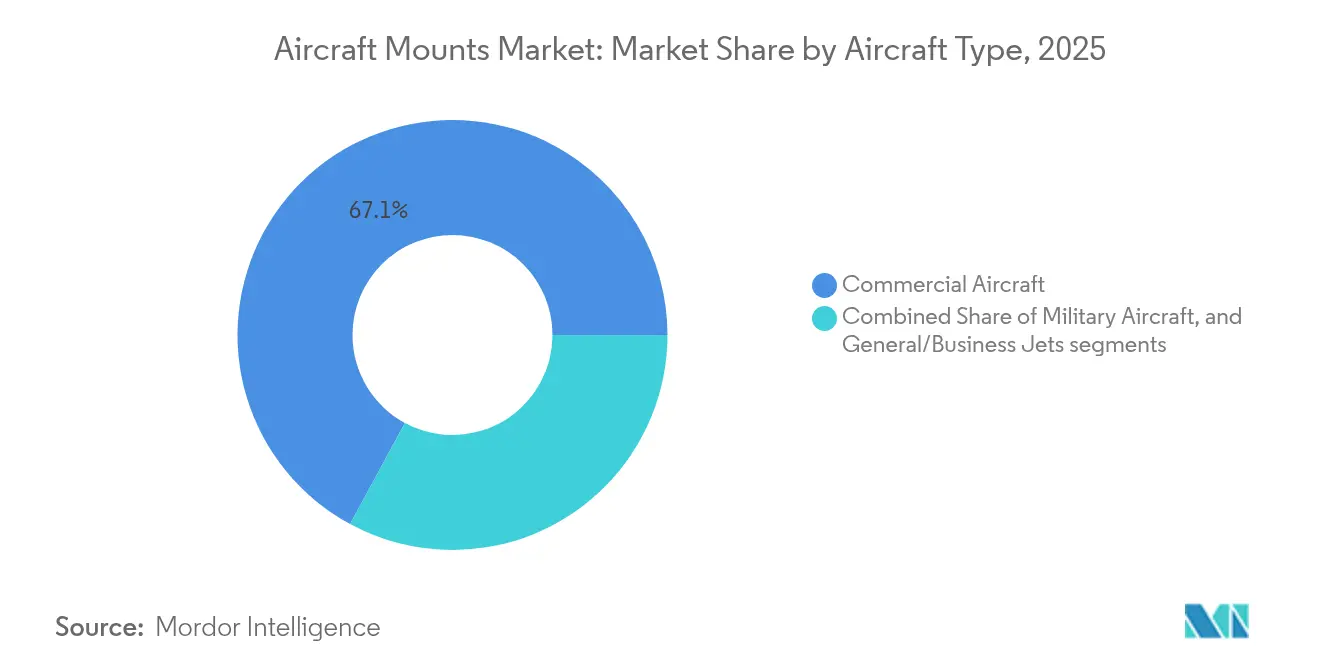

- By aircraft type, commercial platforms held 67.10% of the aircraft mount market size in 2025; general/business jets record the highest projected CAGR at 7.62% to 2031.

- By end user, OEM channels controlled 69.60% of the aircraft mount market in 2025; retrofit demand is growing at an 7.90% CAGR.

- By geography, North America accounted for 42.10% revenue share in 2025, while Asia-Pacific is forecast to see an 8.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Mounts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial aircraft build-rate surge | +2.1% | Global, focus in North America and Europe | Short term (≤ 2 years) |

| Shorter replacement cycle of legacy mounts | +1.3% | Global, especially North America and Europe | Medium term (2-4 years) |

| Tight vibration and cabin-noise regulations | +0.9% | Global, led by FAA and EASA | Long term (≥ 4 years) |

| Premium-cabin retrofit boom | +0.8% | Global, premium carriers in North America and Europe | Medium term (2-4 years) |

| Electrified propulsion thermal-load profiles | +1.1% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Additive-manufactured lattice mounts | +0.6% | Global, led by advanced manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercial aircraft build-rate surge

Commercial jet programs accelerated beyond pre-pandemic volumes, creating a demand spike for engine, suspension, and equipment mounts across narrow-body and wide-body fleets. Airlines ordered replacements to cut fuel burn and meet emissions targets, pushing order backlogs to roughly 10 years on many platforms. Higher utilization rates shortened maintenance cycles, lifting aftermarket demand for replacement mounts. OEMs asked suppliers to align capacity with rolling production-rate targets, rewarding firms that could guarantee on-time delivery. These conditions sustained a dependable baseline for the aircraft mount market.

Electrified propulsion creating new thermal-load profiles

Hybrid-electric and full-electric powertrains shifted mount design priorities by introducing continuous thermal loading and vibration isolation. NASA analysis showed thermal-management systems consumed 9% of propulsion power at take-off, with batteries as the dominant heat source.[1]Source: NASA, “Thermal management considerations for electrified aircraft,” nasa.gov Research on series-hybrid architectures suggested centralized cooling could cut system weight by 12 kg versus decentralized solutions.[2]Source: The Aeronautical Journal, “Thermal-management system design for a series hybrid-electric propulsion architecture,” cambridge.org Mount suppliers began integrating heat-sink channels and conductive lattice skins to dissipate battery-induced heat while preserving acoustic dampening. This integration opened fresh revenue streams and widened the aircraft mount market addressable base.

Tight vibration and cabin-noise regulations

Revisions to FAA and EASA interior-noise directives compelled airframe builders to demand mounts that smooth high-frequency vibrations from new geared-turbofan engines. Compliance tests required suppliers to validate mount damping across broader frequency ranges, extending qualification cycles but locking premium pricing for compliant solutions. Airlines viewed quieter cabins as a brand differentiator on long-haul routes, sustaining a structural demand pull for next-generation mounts.

Premium-cabin retrofit boom

Major carriers reinstated high-end cabin refits to capture premium revenue. Airbus expected 390 A350s to undergo cabin upgrades by 2028, each project involving heavy seat-frame and IFEC hardware swaps that rely on specialized interior mounts. Lufthansa and Qantas unveiled flagship suites demanding mounts capable of supporting 2,000 lb seat loads while meeting slimline weight budgets. As retrofit wave volume intensified, dedicated retrofit-grade mount kits featuring simplified installation hardware emerged as a profitable sub-segment of the aircraft mount market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost swings | -1.4% | Global, titanium-dependent regions | Short term (≤ 2 years) |

| Lengthy FAA/EASA certification cycles | -0.9% | North America and Europe | Medium term (2-4 years) |

| Specialty-silicone supply crunch | -0.6% | Advanced manufacturing regions | Short term (≤ 2 years) |

| Longer-life composite airframes | -0.5% | Next-generation platforms worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy FAA/EASA certification cycles

Regulators heightened scrutiny of structural systems following recent safety directives, extending new-design certification to 18–24 months on average. Mandated failure-mode analyses and separate environmental compliance reports pushed non-recurring engineering spend by nearly 20% for bespoke mounts. While bilateral agreements cut duplicate testing, smaller suppliers faced resource bottlenecks that limited product-launch cadence and tempered the overall aircraft mount market growth rate.

Raw-material cost swings

Titanium ingot prices spiked after sanctions disrupted Russian supply, compelling buyers to dual-source or stockpile material at elevated cost. Airbus noted that steel lead times had lengthened beyond 45 weeks, complicating production schedules. Procurement surveys showed a 60% jump in working capital tied up in safety stock among Tier 2 machinists, eroding profitability and delaying shipment commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Engine mounts sustain leadership

Engine mounts accounted for 59.12% of the aircraft mount market in 2025 because they integrate high-value titanium, elastomer, and composite linkages that manage thrust loads while isolating vibration. The aircraft mount market size for engine-related hardware is projected to expand steadily, supported by narrow-body production surges and the introduction of ultra-high bypass geared-turbofan engines. Although smaller today, Suspension mounts are pegged for a 7.45% CAGR as cabins add heavier monuments and larger IFEC racks requiring upgraded vibration dampers.

Second-generation electric powertrains presented fresh design envelopes. Electric motors produce high-frequency harmonics, prompting suppliers to redesign elastomer stacks and add integral cooling fins that bleed heat into surrounding airflow. NASA simulations showed that integrated cooling slashed the combined propulsion-mount system weight by half compared to legacy discrete architectures. Early adopters in demonstrator programs contracted mount makers for prototype lots, seeding longer-term demand once type certification arrives.

By Mount Type: Exterior hardware dominates

Exterior mounts held 64.92% market share in 2025, driven by their role on engines, pylons, landing gear, and external antennae. These mounts faced temperature swings from -60 °C at altitude to 200 °C near bleed-air ducts, dictating exotic alloy solutions and multilayer elastomer stacks. The segment delivered predictable volume because every new airframe required a baseline of four to six engine mounts plus dozens of ancillary fittings. The aircraft mount market share of interior applications is poised to climb as airlines retrofit connectivity routers, wide-screen IFEC, and smart-galley inserts, all of which need vibration-safe attachment.

Interior mounts posted an 7.85% CAGR outlook, aided by lightweight composite skins and quick-change bracket systems that reduce downtime during cabin modifications. Cabin-electronics suppliers collaborated with mount makers to develop vibration-tuned brackets that isolate 20–600 Hz bands common to fuselage flexure, safeguarding sensitive SSD-based servers.

By Aircraft Type: Commercial jets remain anchor demand

Commercial programs contributed 67.10% of 2025 revenue as Boeing and Airbus raised single-aisle output and reopened wide-body lines. The commercial jet aircraft mount market holds the largest market share, driven by record order backlogs, highlighting the growing demand for new aircraft. This trend underscores the increasing reliance on advanced mounting systems to support the expanding global aviation industry, ensuring operational efficiency and safety standards are met. General/business jets deliver the fastest 7.62% CAGR, reflecting the premium-travel rebound and the influx of super-mid-size models with higher-thrust engines and advanced vibration requirements.

Defense programs stabilized revenue through rotorcraft and surveillance-platform vibration-isolation projects. The US Army’s HADES high-altitude ISR initiative relied on customized mounts for sensor pallets, demonstrating defense-driven niche opportunities.

By End User: OEM supply dominates but retrofit accelerates

OEM channels commanded 69.60% of revenue in 2025 because mounts are usually designed into the airframe and co-qualified with engines. Long-term agreements protected capacity allocations, delivering visibility over multi-year horizons. The retrofit market is experiencing an 7.90% CAGR as airlines increasingly extend fleet lifespans beyond 20 years and prioritize more frequent cabin upgrades to enhance passenger experience and operational efficiency.

Retrofit growth accelerated after IATA released best-practice guides simplifying Supplemental Type Certificate paths for cabin retrofit, which cut downtime by up to 30%. Mount suppliers responded with modular kits that bundle bracketry, elastomer inserts, and load-path shims, shortening labor hours and reducing re-certification paperwork.

Geography Analysis

North America retained a 42.10% share in 2025, underpinned by Boeing’s single-aisle production surge and robust defense procurement budgets. The region also led early adoption of additive manufacturing for lattice-structured mounts, supported by a dense network of powder-bed fusion facilities and metal-powder suppliers. Supply-chain partnerships between Parker-Hannifin and major OEMs streamlined qualification, enabling quick transition from prototype mounts to full-rate production.

Asia-Pacific generated the fastest 8.15% CAGR outlook through 2031 as regional carriers expanded fleets and airframe OEMs localized more work packages. Singapore’s Seletar Aerospace Park attracted USD 810 million of manufacturing investment, including GE Aerospace’s smart-factory upgrade and Pratt & Whitney’s capacity increases for GTF turbine disks. Workforce pipelines delivered 1,800 aerospace graduates annually, ensuring talent supply for mount design, machining, and nondestructive testing roles.

Europe sustained a meaningful share through Airbus’ industrial footprint and a robust Tier 1 ecosystem in France, Germany, and the UK. Airbus disclosed longer steel lead times and titanium scarcity issues, but also expanded A350 output to 12 aircraft monthly, sustaining mounting demand. The region’s advanced composites and additive-manufacturing capabilities positioned European suppliers to supply weight-optimized mounts for next-generation hybrid-electric concepts. Harmonized FAA-EASA certification protocols reduced duplicative test campaigns, easing market access for transatlantic suppliers.

Competitive Landscape

Industry competition remained consolidated. Parker-Hannifin’s aerospace segment posted USD 1.57 billion sales in Q3 2025 with a 23.7% operating margin, highlighting scale advantages and broad aftermarket reach. Hutchinson delivered over 3,000 vibro-acoustic products for engines and cabins, benefiting from proprietary elastomer formulations.

Strategic mergers and acquisitions reshape portfolios. In February 2025, TriMas acquired GMT Aerospace to deepen vibration-control expertise and extend the European footprint. Honeywell partnered with Vertical Aerospace to certify VX4 eVTOL systems, underscoring the value of mount solutions tailored to electric-propulsion layouts.

Innovation focus shifted to additive-manufactured lattice structures, thermal-conductive elastomers, and digital twins that predict remaining useful life. Suppliers investing in in-house printing lines and model-based qualification frameworks secured early design wins on demonstrator programs, planting seeds for long-term revenue as electrified propulsion matures.

Aircraft Mounts Industry Leaders

GMT Rubber-Metal-Technic Ltd.

Mayday Manufacturing Co.

HUTCHINSON AEROSPACE & INDUSTRY INC.

ITT Inc.

Shock Tech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Airbus unveiled its next-generation single-aisle aircraft development program, which features advanced aerodynamics, hybridization, and electrification technologies. These include engines that consume 20% less fuel and the use of lighter, stronger materials for improved performance.

- February 2025: Pratt & Whitney announced a USD 20 million investment to expand manufacturing capacity in Singapore for GTF engine high-pressure turbine disks, targeting a 45% increase in annual output by January 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft mount market as the value of new and replacement interior and exterior hardware that fastens engines, equipment, and structural sub-assemblies to fixed-wing and rotor-craft airframes, while also absorbing vibration and shock. The valuation is expressed in constant 2025 US dollars.

Scope exclusion: Consumable elastomer bushings and mounts used solely in ground test rigs are not included.

Segmentation Overview

- By Application

- Suspension Mounts

- Engine Mounts

- By Mount Type

- Interior Mounts

- Exterior Mounts

- By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General/Business Jets

- By End User

- OEM

- Retrofit

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed air-frame engineers, MRO procurement heads, and mount material suppliers across North America, Europe, and Asia. These discussions verified average service lives, premium pricing for lightweight alloys, and the pace at which commercial narrow-body backlogs convert to deliveries. Insights closed data gaps flagged during desk work.

Desk Research

We started with open data streams such as FAA and EASA airframe certification files, UN Comtrade trade codes 880330 and 880390, and fleet statistics released by the International Air Transport Association. Production forecasts from Airbus and Boeing, flight-hour tallies issued by the U.S. Bureau of Transportation Statistics, and defense budget line items from SIPRI added volume and replacement clues. Subscription databases that Mordor analysts access, notably D&B Hoovers for company financials and Questel for patent trends, provided spend signals and technology diffusion timing. Many additional public and proprietary documents were consulted; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A single top-down demand pool was built from active fleet counts, yearly production, and retirement schedules, then cross-checked with selective bottom-up supplier revenue roll-ups for calibration. Key variables like annual aircraft deliveries, military modernization outlays, passenger-kilometer growth, average replacement cycle (in flight hours), aluminum alloy price index, and civil certification lead times influence both base year value and scenario ranges. Multivariate regression projected each driver, after which scenario analysis adjusted for fuel-price shocks.

Data Validation & Update Cycle

Model outputs pass three filters: variance versus historical spend, peer ratio checks, and senior analyst review. Updates occur annually, with interim refreshes if OEM build rates or regulatory rulings shift materially. A fresh validation is completed just before report release.

Why Mordor's Aircraft Mounts Baseline Earns Client Trust

Published values often diverge because firms choose different mount categories, forecasting windows, and refresh cadences.

Key gap drivers include varied inclusion of retrofit demand, differing aircraft delivery forecasts, and currency year mismatches. Mordor's model aligns mount categories with ICAO maintenance rules, applies segment-specific replacement cycles, and refreshes every twelve months, yielding a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.82 B (2025) | Mordor Intelligence | - |

| USD 0.89 B (2024) | Regional Consultancy A | Focuses on engine mounts, omits retrofit channel |

| USD 0.65 B (2020) | Trade Journal B | Uses pre-pandemic baseline, limited regional splits |

| USD 0.96 B (2025) | Global Consultancy C | Applies uniform growth rate, no replacement cycle check |

In sum, the side-by-side view shows that when scope breadth, update frequency, and variable depth are weighed together, Mordor Intelligence delivers a clear, reproducible baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the aircraft mount market?

The aircraft mount market was valued at USD 880 million in 2026 and is expected to reach USD 1.24 billion by 2031, reflecting a 7.08% CAGR.

Which segment holds the largest share of the aircraft mount market?

Engine mounts led with 59.12% revenue share in 2025, reflecting their critical role in powerplant integration.

Which region is growing fastest?

Asia-Pacific shows the highest growth with an anticipated 8.15% CAGR through 2031, driven by expanding fleets and manufacturing investments.

How is electrification affecting mount design?

Hybrid-electric and electric aircraft create higher thermal loads, pushing suppliers to integrate heat-dissipation features alongside vibration isolation.

Why are certification cycles considered a restraint?

Enhanced FAA and EASA requirements extend approval times to up to two years, delaying new mount introductions and raising non-recurring engineering costs.

What technological trends are shaping future mount systems?

Additive-manufactured lattice structures, thermal-conductive elastomers, and predictive-maintenance digital twins are emerging as key differentiators.

Page last updated on: