Fighter Aircraft IRST Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

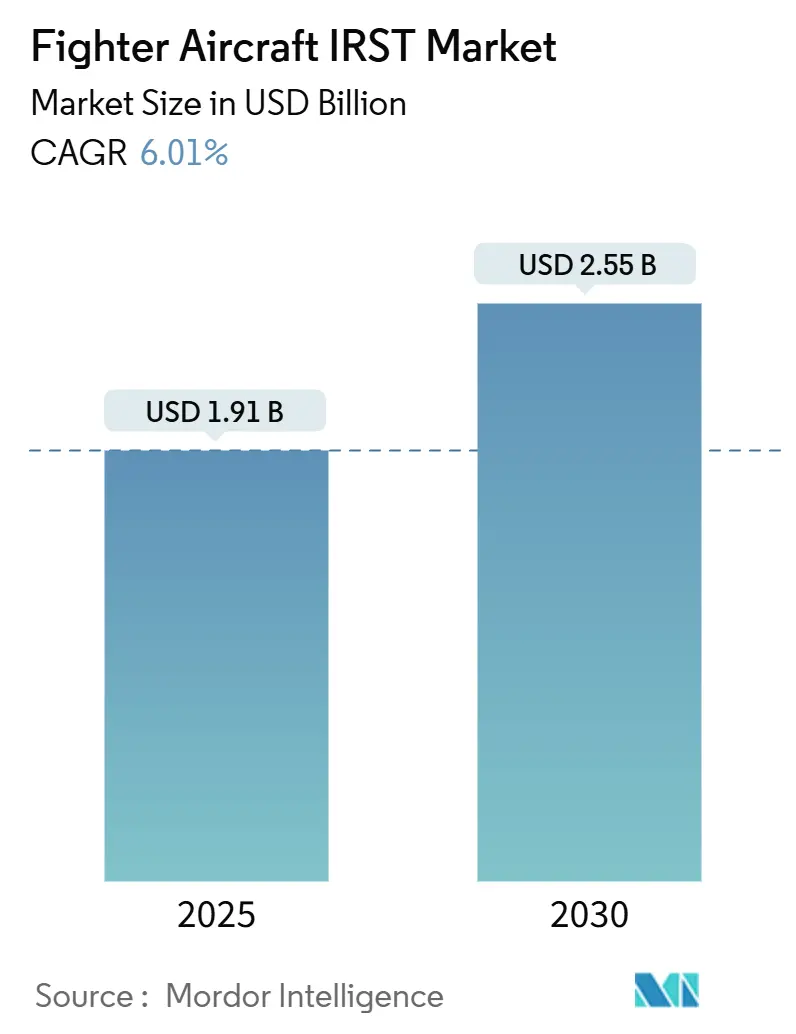

| Market Size (2025) | USD 1.91 Billion |

| Market Size (2030) | USD 2.55 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fighter Aircraft IRST Market Analysis by Mordor Intelligence

The fighter aircraft IRST market size reached USD 1.91 billion in 2025 and is forecasted to hit USD 2.55 billion by 2030, advancing at a 6.01% CAGR. Demand accelerates as passive detection becomes vital against proliferating stealth platforms; miniaturized high-operating-temperature (HOT) detectors and AI-enabled sensor fusion now allow internal installations that preserve low-observable profiles. North America holds primacy, propelled by F/A-18 and F-22 upgrades, while Asia-Pacific records the fastest climb on the back of expanding indigenous 5th-generation programs. Scanning sensors continue to dominate procurement choices, yet staring arrays are gaining traction because their solid-state design boosts reliability under 9G maneuvers. Concurrently, growth in processing electronics mirrors the push for real-time AI algorithms that merge infrared and radar tracks at the edge.

Key Report Takeaways

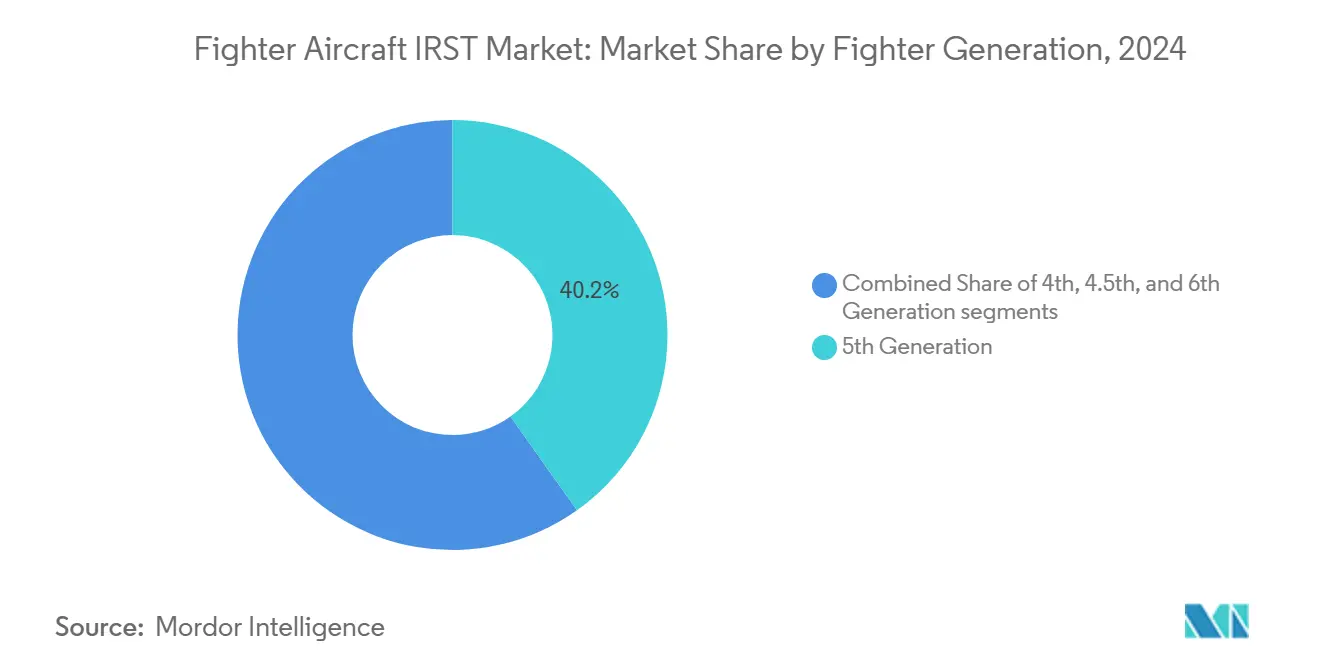

- By fighter generation, 5th-generation aircraft captured 42.47% of the fighter aircraft IRST market share in 2024, whereas 6th-generation platforms are projected to expand at a 9.87% CAGR through 2030.

- By sensor technology, scanning systems led with a 52.87% share of the fighter aircraft IRST market size in 2024; staring sensors represent the fastest element, with a 7.28% CAGR to 2030.

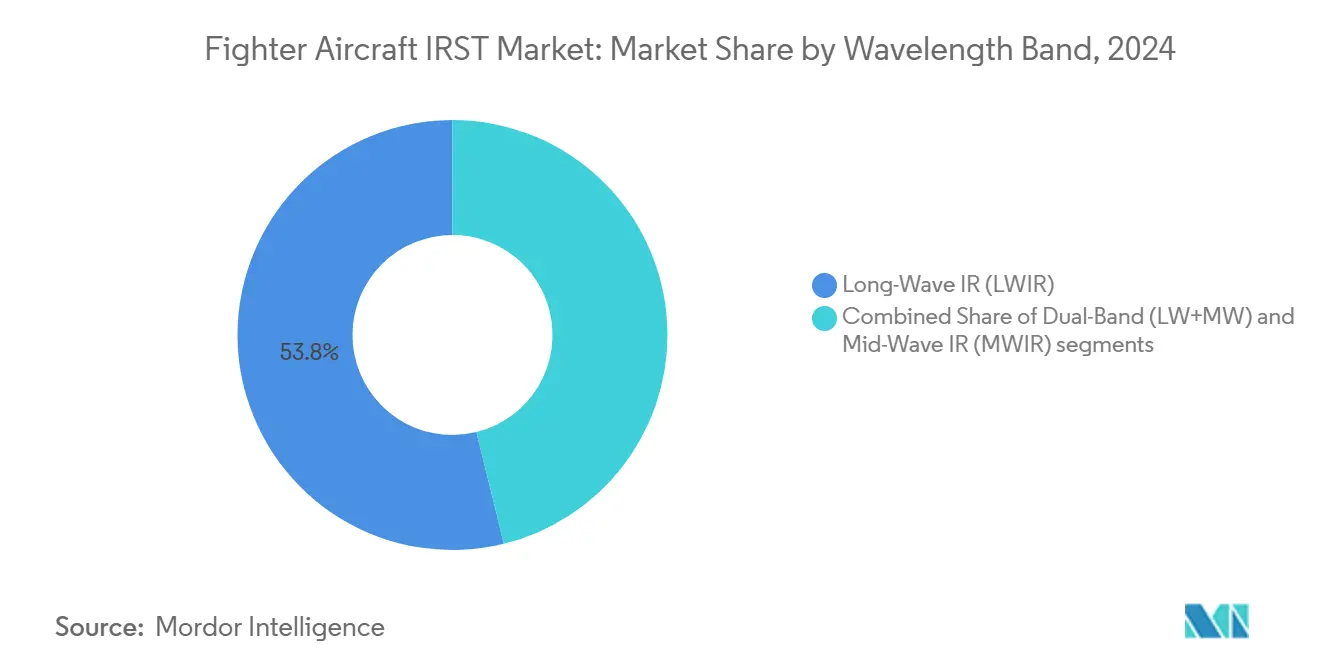

- By wavelength band, long-wave infrared held a 53.84% share in 2024, while dual-band configurations are set to post a 9.2% CAGR through 2030.

- By component, scanning head assemblies accounted for 43.83% of the fighter aircraft IRST market size in 2024, and processing electronics show a 6.55% CAGR outlook to 2030.

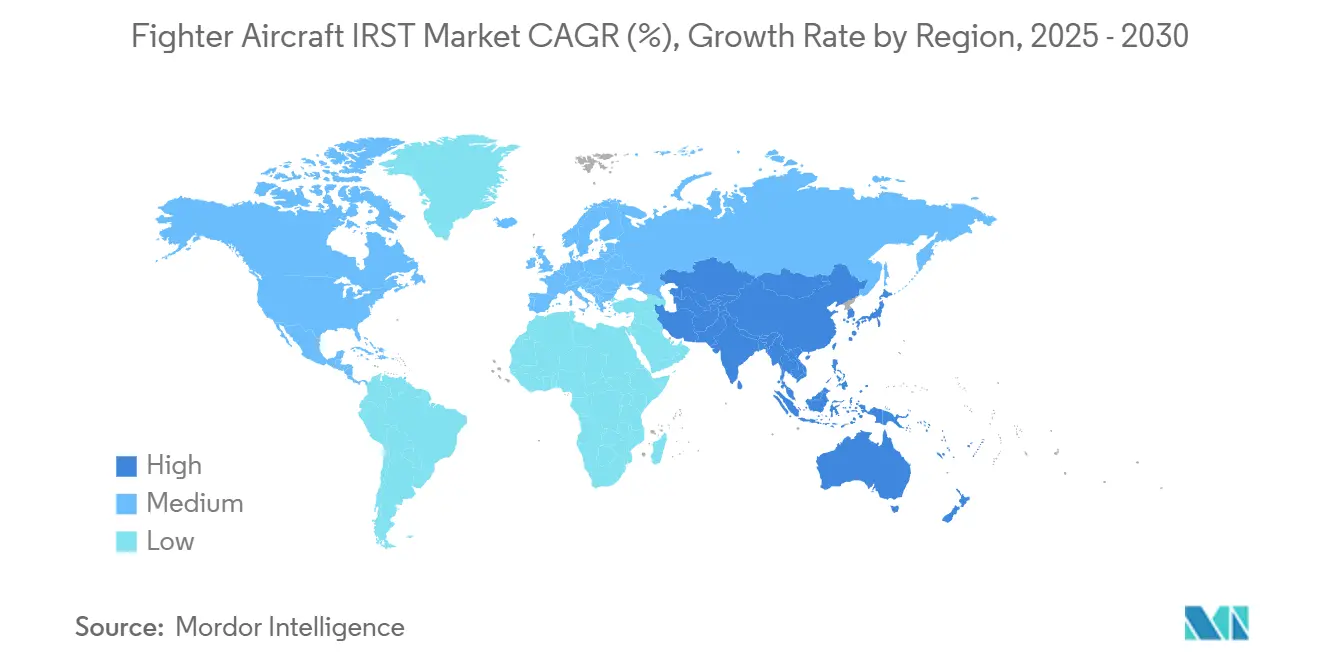

- Geographically, North America commanded 36.75% of the fighter aircraft IRST market share in 2024, whereas Asia-Pacific is forecasted to lead growth at a 7.98% CAGR between 2025 and 2030.

Global Fighter Aircraft IRST Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for passive detection against stealth threats | +1.30% | North America, Asia-Pacific | Medium term (2-4 years) |

| Global combat aircraft fleet life-extension and upgrade programs | +1.10% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of 5th-gen export programs requiring IRST as baseline | +0.90% | Middle East, Asia-Pacific | Medium term (2-4 years) |

| AI-enabled sensor fusion improving detection and false-alarm rates | +0.80% | North America, Europe | Short term (≤ 2 years) |

| Miniaturized HOT detectors enabling internal installations | +0.70% | Global | Medium term (2-4 years) |

| IRST adoption on HALE/UCAV platforms for adjunct air combat roles | +0.60% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Passive Detection Against Stealth Threats

Low-observable fighters such as China’s J-20 and Russia’s Su-57 limit radar effectiveness, so air forces pivot toward passive infrared search and track systems that do not reveal an electromagnetic signature. The US Navy’s Initial Operational Capability declaration for F/A-18 IRST Block II in November 2024 underscores this doctrinal shift despite reliability issues that required multiple pod restarts during testing.[1]InsideDefense Staff, “IRST Block II Reaches IOC,” InsideDefense, insidedefense.com Retrofitting legacy 4th-generation fleets and integrating distributed aperture sensors on next-generation jets sustain multiyear procurement pipelines. Because IRST imposes no emissions, it becomes pivotal for survival in contested electronic-warfare environments, driving continuous investments across major programs and export bids. That imperative elevates the fighter aircraft IRST market as nations seek stealth-countering capabilities without compromising platform visibility.

Global Fighter-Fleet Life-Extension and Upgrade Programs

Thousands of aging fighters are moving through 15- to 20-year service-life extensions, and IRST now sits near the top of every avionics upgrade list. Leonardo’s Skyward IRST on Top Aces’ F-16 Advanced Aggressor Fighter, integrated in September 2024, shows how even contracted training providers pursue passive detection to stress 5th-generation students. Eurofighter Typhoon Tranche 3, Gripen E, and India’s Su-30 MKI MAKE-II dual-band program echo the trend. Retrofit kits run USD 2-5 million per jet versus USD 80-120 million for a new aircraft, so budget-constrained air arms see an attractive cost-benefit path. Because upgrade cycles tie into depot visits, suppliers enjoy predictable long-run spares and sustainment revenue, which underpins steady fighter aircraft IRST market growth.

Expansion of 5th-Generation Export Programs Requiring IRST as Baseline

Export buyers now insist on IRST because it levels the playing field with Russian and Chinese offerings. The F-35’s Electro-Optical Distributed Aperture System sets the benchmark, and any future F-22 export proposal will carry a next-generation IRST now in Lockheed Martin development. Customers value the sensor’s silent tracking in GPS-denied or jammed settings. As Middle Eastern and Asia-Pacific states modernize, IRST becomes a purchase differentiator, nudging suppliers to bundle the technology in standard packages and opening licensed-production channels for allies.

AI-Enabled Sensor Fusion Improving Detection and False-Alarm Rates

Machine learning (ML) algorithms elevate IRST from situational-awareness aid to primary targeting source. Models that filter clutter push classification accuracy beyond 95% in ideal conditions. Boeing’s F-47 NGAD demonstrator, unveiled in March 2025, places AI fusion at the system core so a single pilot or remote operator can manage multi-band cues without overload. Processing electronics, therefore, clocks the highest component growth as graphics processors and field-programmable arrays migrate into conduction-cooled boards sized for fighter bays. Suppliers that master low-latency fusion claim a prime competitive edge.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and integration cost per aircraft | -0.90% | Global | Long term (≥ 4 years) |

| Cryocooler reliability issues under sustained high-G maneuvers | -0.70% | Global | Medium term (2-4 years) |

| Centerline-tank IRST pods cut fuel by greater than 30%, reducing endurance | -0.50% | Global | Short term (≤ 2 years) |

| Export-control restrictions on advanced IR detectors | -0.40% | Non-allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Development and Integration Cost Per Aircraft

End-to-end IRST integration can add USD 2-8 million per fighter, straining budgets of smaller air forces that cannot leverage large production lots. The F/A-18 Block II program saw overruns that required supplemental US congressional funding, illustrating how test-flight expansions and software revisions inflate life-cycle costs. International customers also shoulder training, spares, and depot-level sustainment, pushing small-fleet outlays above USD 50 million. These economics prompt some procurement offices to defer IRST in favor of less expensive radar refresh or electronic warfare pods, slowing near-term orders even when doctrinal need is clear. The expenditure hurdle, therefore, tempers expansion of the fighter aircraft IRST market outside tier-one defense budgets.

Cryocooler Reliability Issues Under Sustained High-G Maneuvers

Fighter-grade cryocoolers show 20-30% failure rates during protracted 9G sorties because flexure bearings and clearance seals fatigue under rapid pressure cycling.[2]R.G. Ross, “Cryocooler Reliability Issues,” sciencedirect.com Mean time to failure ranges from 2,500 to 8,000 hours, far below space-rated units. Each removal disrupts sortie generation and increases life-cycle cost, so air forces demand redundant cooling loops or hardened designs, adding weight and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fighter Generation: 5th-Generation Dominance, 6th-Generation Acceleration

5th-generation jets owned 42.47% of the fighter aircraft IRST market share in 2024 as F-35 global deliveries and F-22 upgrades cemented demand. 6th-generation projects led by NGAD and Tempest show a 9.87% CAGR to 2030, reflecting design blueprints that embed multi-spectral apertures from day one.

Legacy 4th-generation fighters still form the numerical backbone of global fleets, so retrofit programs keep volume steady. Meanwhile, 4.5th-generation refresh packages bridge capability gaps by adding podded or semi-flush IRST options at a fraction of new-build cost. Because 6th-generation roadmaps call for manned–unmanned teaming, sensor standards will likely propagate into drone wingmen, multiplying future installed bases.

By Sensor Technology: Scanning Heads Prevail, Staring Arrays Climb

Scanning mechanisms captured 52.87% of the fighter aircraft IRST market size in 2024 thanks to their proven gimbal coverage and long-range acuity. Staring arrays, advancing at 7.28% CAGR, attract interest for solid-state resilience and zero-maintenance bearings under cyclic 9G loads.

Recent focal-plane manufacturing advances deliver larger formats, allowing staring systems to challenge scanning for wide-area surveillance while trimming part counts that historically drove sustainment expense. As reliability metrics tighten, the fighter aircraft IRST market advantages suppliers who can balance detection range with mechanical simplicity.

By Wavelength Band: LWIR Leads, Dual-Band Gains Favor

Long-wave infrared systems accounted for 53.84% of the fighter aircraft IRST market size in 2024, thanks to their high humidity tolerance over maritime environments.[3]Army Recognition Editorial Team, “IRIS-T Block II Contract,” armyrecognition.com Dual-band payloads climb at 9.2% CAGR as forces demand spectral cross-checks to defeat new flare formulas.

Manufacturing advances have narrowed the cost gap, so European and Asian tenders now include dual-band readiness clauses. Suppliers who package two focal-plane stacks within legacy volume constraints gain an inside track on future awards.

By Component: Processing Electronics Become the Growth Engine

Scanning head assemblies still delivered 43.83% revenue in 2024, yet processing electronics exhibit a robust 6.55% CAGR, mirroring the surge of AI-driven classification software that demands edge-compute horsepower.

Field-programmable gate arrays and GPU-based accelerators pack into conduction-cooled modules qualified to MIL-STD-810, enabling real-time multi-sensor fusion without bloating weight budgets. Vendors that co-design optics and processors lock in higher content per tail, reinforcing competitive barriers within the fighter aircraft IRST market.

Geography Analysis

North America maintained 36.75% of the fighter aircraft IRST market share in 2024 through sustained F-22, F/A-18, and forthcoming NGAD investments that embed passive sensors from program inception.[4]Defense Post Staff, “F-22 IRST Contract Award,” thedefensepost.com Fleet refresh cycles and mission-package upgrades ensure a predictable pipeline even as export controls restrict technology diffusion, anchoring the regional revenue base for incumbent primes.

Asia-Pacific shows a 7.98% CAGR outlook, the fastest region, buoyed by India’s HAL-BEL dual-band prototype flights, Japan’s F-35 acquisitions, and South Korea’s KF-21 roadmap. Indigenous content rules compel local assembly and subsystem co-development, broadening the supplier map while expanding the overall fighter aircraft IRST market opportunity.

European programs such as Eurofighter Tranche 4 and the GCAP collaboration sustain steady demand by specifying distributed infrared apertures alongside electronic-warfare suites. Although aggregate spending lags in the US, multinational frameworks streamline certification across partner nations, keeping the fighter aircraft IRST market cohesive and open to shared upgrades over the long term.

Competitive Landscape

The fighter aircraft IRST market exhibits high consolidation; Lockheed Martin Corporation, Leonardo S.p.A., HENSOLDT AG, Elbit Systems Ltd., and Thales Group collectively occupy a substantial revenue block through vertically integrated detector, optics, and processor portfolios. Their proprietary HOT super-lattice arrays and cryogenic cooling IP create technology moats that deter late entrants.

Tier-two challengers pursue white-space in unmanned combat air vehicles, where loyal-wingman concepts favor smaller, low-power sensors. Partnerships such as General Atomics–Lockheed on Avenger demonstrations illustrate how established primes extend dominance into adjacent domains while nurturing ecosystem allies.

Sustained barriers stem from MIL-STD qualification costs, multi-year export-license cycles, and the need to validate reliability under 9G, 1,000 Hz vibration regimes. As a result, newcomers must either license mature designs or target niche subsystems, leaving overall fighter aircraft IRST market leadership largely in incumbents’ hands.

Fighter Aircraft IRST Industry Leaders

Lockheed Martin Corporation

Leonardo S.p.A.

Thales Group

Elbit Systems Ltd.

HENSOLDT AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lockheed Martin won a contract to equip the F-22 fleet with next-generation IRST sensors, reinforcing the aircraft’s stealthy passive-detection edge.

- September 2024: Leonardo Electronics US integrated Skyward IRST on Top Aces’ F-16 Advanced Aggressor Fighter, raising 5th-generation training fidelity.

Global Fighter Aircraft IRST Market Report Scope

| 4th Generation |

| 4.5th Generation |

| 5th Generation |

| 6th Generation (Projected) |

| Scanning Sensor |

| Staring Sensor |

| Long-Wave IR (LWIR) |

| Mid-Wave IR (MWIR) |

| Dual-Band (LW+MW) |

| Scanning Head |

| Processing and Control Electronics |

| Display and Human-Machine Interface |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Fighter Generation | 4th Generation | ||

| 4.5th Generation | |||

| 5th Generation | |||

| 6th Generation (Projected) | |||

| By Sensor Technology | Scanning Sensor | ||

| Staring Sensor | |||

| By Wavelength Band | Long-Wave IR (LWIR) | ||

| Mid-Wave IR (MWIR) | |||

| Dual-Band (LW+MW) | |||

| By Component | Scanning Head | ||

| Processing and Control Electronics | |||

| Display and Human-Machine Interface | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the fighter aircraft IRST space today, and what growth pace is expected to 2030?

Current spending totals USD 1.91 billion in 2025 and is projected to climb at a 6.01% CAGR through 2030.

Which region is forecast to post the fastest IRST procurement gains?

Asia-Pacific shows a 7.98% CAGR outlook as India, Japan, and South Korea scale 5th-generation programs.

Which sensor architecture is eroding scanning heads’ lead?

Solid-state staring arrays, growing at 7.28% CAGR, are closing the gap thanks to higher reliability in 9G flight.

What performance edge drives demand for dual-band infrared seekers?

Dual-band payloads improve target discrimination and countermeasure rejection, supporting a 9.20% CAGR for that segment.

Why do operators favor internal or conformal IRST installs over podded versions?

Internal placements avoid the 29% fuel-capacity loss and drag penalties linked to centerline pods on legacy fighters.

What cost range must air forces budget per aircraft for a full IRST upgrade?

End-to-end retrofit packages typically add USD 2–8 million per jet, covering hardware, software, and flight certification.

Page last updated on: