Commercial Aircraft Floor Panels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 373.98 Million |

| Market Size (2031) | USD 504.27 Million |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

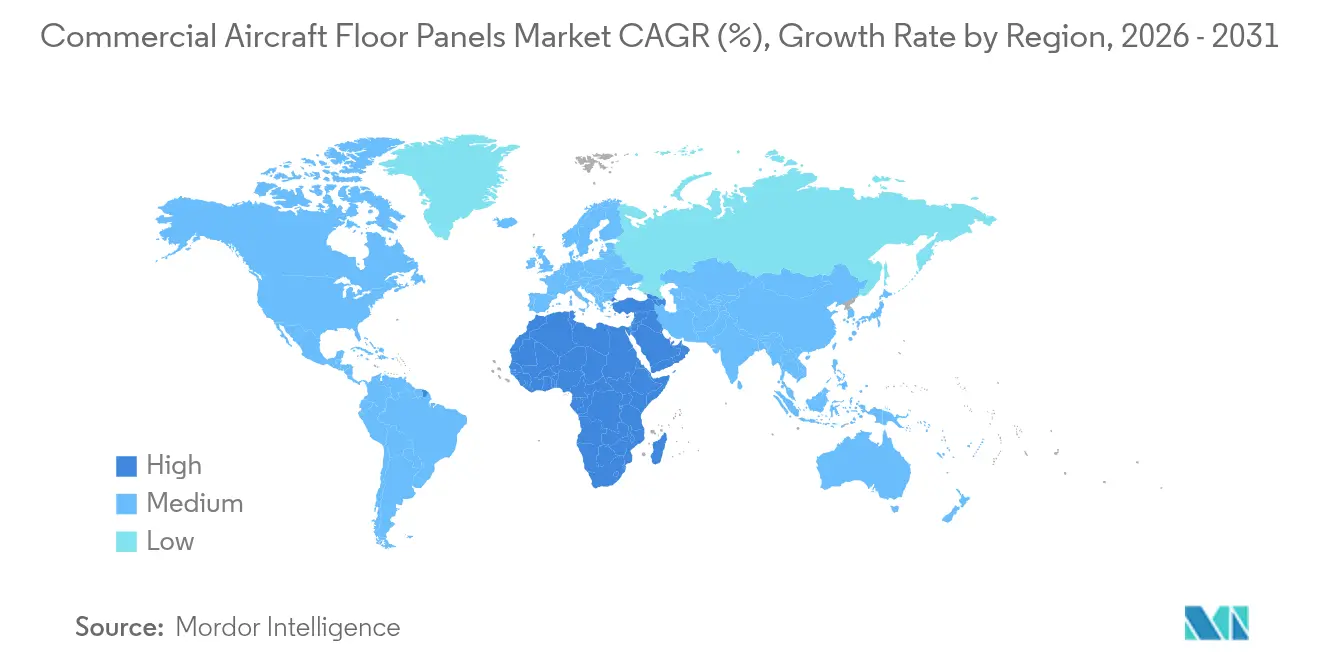

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Floor Panels Market Analysis by Mordor Intelligence

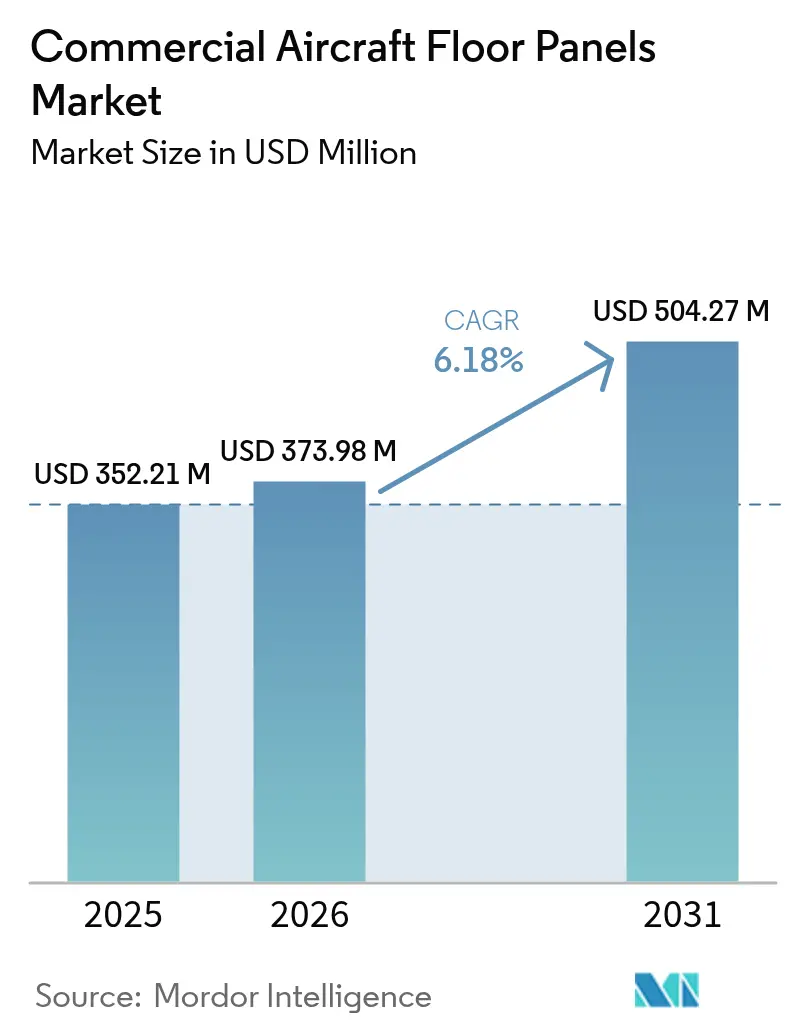

The commercial aircraft floor panels market size was valued at USD 352.21 million in 2025 and estimated to grow from USD 373.98 million in 2026 to reach USD 504.27 million by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). Growing aircraft backlogs, stringent fire-safety rules, and the industry-wide shift toward lighter cabin interiors underpin this expansion. Airlines are accelerating their retrofit programs to reduce fuel burn, while next-generation wide-body platforms adopt composite-rich structures that rely on advanced floor panels to achieve weight parity. Supply-chain consolidations, such as Boeing’s purchase of Spirit AeroSystems and Airbus’s acquisition of Spirit’s European assets, realign sourcing power and help de-bottleneck panel deliveries. Meanwhile, recyclable thermoplastic honeycomb cores transition from prototype to line-fit status as operators pursue circular economy targets.

Key Report Takeaways

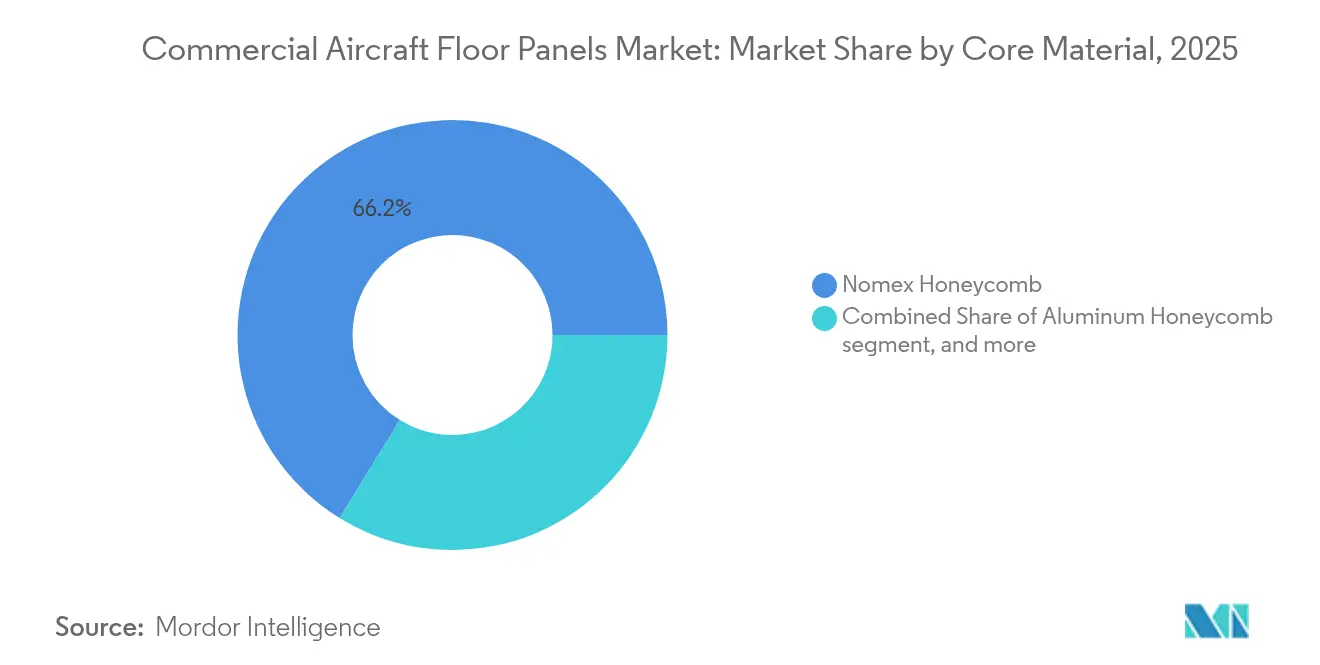

- By core material, Nomex honeycomb led the commercial aircraft floor panels market with a 66.20% share in 2025; carbon-fiber honeycomb is projected to expand at an 8.42% CAGR through 2031.

- By fitment, the OEM channel held 60.70% of the commercial aircraft floor panels market in 2025, while the aftermarket is forecasted to grow at an 7.76% CAGR to 2031.

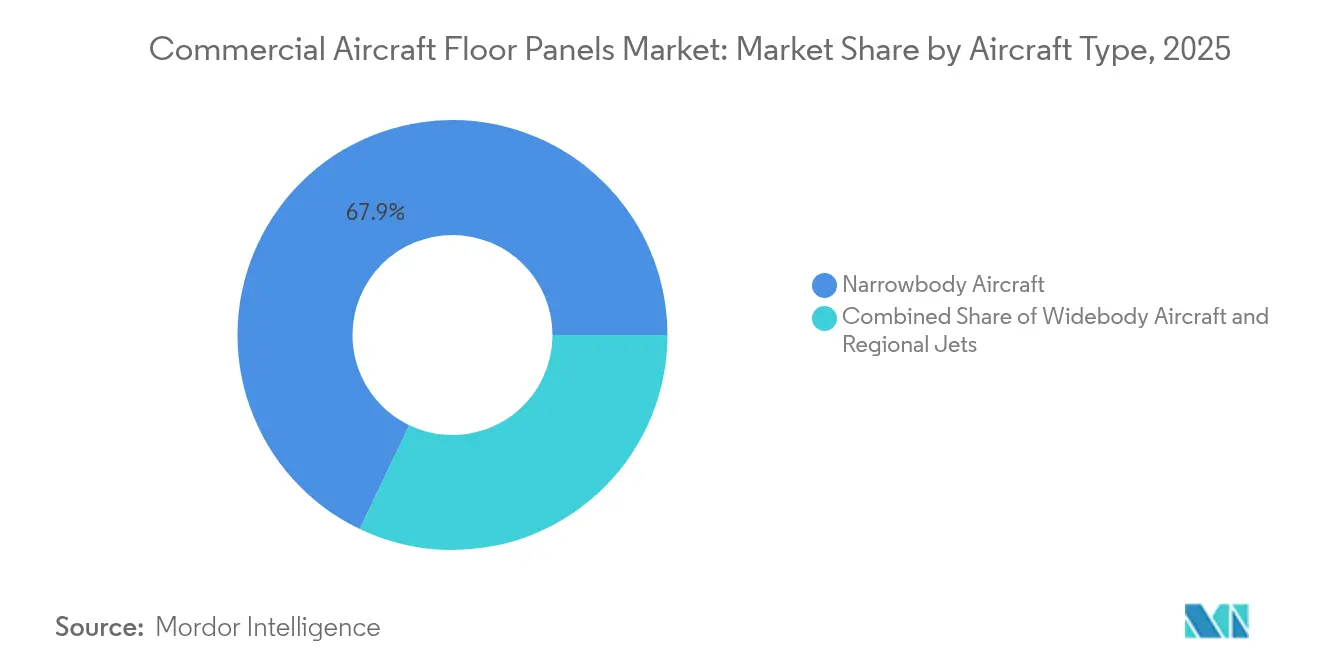

- By aircraft type, narrowbody programs accounted for 67.90% of the commercial aircraft floor panels market size in 2025; widebody programs are set to rise at a 6.43% CAGR during 2026-2031.

- By geography, the Asia-Pacific region dominated with a 30.85% revenue share in 2025; the Middle East and Africa region is poised for the fastest growth, with a 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Floor Panels Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in narrowbody aircraft production backlog | +1.8% | Global with focus on Asia-Pacific and North America | Medium term (2-4 years) |

| Airline retrofit cycles focused on lightweight cabin refurbishment | +1.2% | North America and EU, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Ramp-up of composite-rich models requiring advanced floor panel solutions | +1.5% | Global, led by B787 and A350 lines | Long term (≥ 4 years) |

| Rising adoption of recyclable thermoplastic honeycomb cores for circularity goals | +0.9% | Europe leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

| Expansion of integrated MRO and PMA supply chains shortening global TAT | +0.8% | Global, strong growth in Middle East and Asia-Pacific | Medium term (2-4 years) |

| Stricter flammability regulations accelerating phase-out of legacy panels | +0.4% | Global regulatory harmonization (FAA, EASA, ICAO) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Narrowbody Aircraft Production Backlog

Narrowbody order books now span nearly 13 years of output, locking in sustained demand for commercial aircraft floor panels market installations. Each single-aisle jet needs 15-20 panels across the cabin and belly compartments, so every incremental production slot translates into tangible material volumes. The restart of B737 MAX production and the Airbus A320neo family’s targeted 75-per-month cadence intensify sourcing pressures, even as select component suppliers continue to struggle with electronics, forgings, and honeycomb cores. The US Government Accountability Office notes that nine of 15 tier-one vendors cite labor and material shortages as persistent constraints, which extend lead times and prompt airframers to dual-source qualified panel lines where possible.[1]U.S. Government Accountability Office, “Aviation Supply Chain Challenges,” gao.gov Operators in Asia-Pacific and North America absorb the bulk of fresh deliveries, reinforcing the geographic skew toward those supply corridors.

Airline Retrofit Cycles Focused on Lightweight Cabin Refurbishment

Cabin refresh intervals range from eight to 12 years, and the current wave coincides with record fuel price volatility. Airlines, therefore, prioritize mass-reduction options, making lightweight floor systems a core feature of retrofit kits. Collins Aerospace displayed an integrated seating-plus-floor concept at the Aircraft Interiors Expo that reuses structural seat rails while replacing the original panels with next-generation phenolic-resin laminates. Safran’s interiors division booked 25.2% revenue growth in 2024, underpinned by similar retrofit demand as carriers such as Delta Air Lines chose smart-cabin modules over full fleet reconfigurations. Regulatory updates to FAR 25.853 test protocols also force older panels out of service sooner, lifting near-term replacement volumes in North America and several EU jurisdictions.

Ramp-Up of Composite-Rich Models Requiring Advanced Floor Panel Solutions

Widebody programs, such as the B787 and A350, comprise roughly 50% of the composite content by mass. Their floor structures must deliver comparable stiffness while absorbing point loads from premium-class monuments. Carbon-fiber honeycomb cores paired with phenolic skins exceed the weight savings of legacy Nomex by 8-10 kg per aircraft, yet sustaining those benefits requires high-precision bonding and tight supply coordination. Hexcel reported USD 1,194.20 million in commercial aerospace sales for 2024, representing a 12% year-over-year increase.[2]Investor Relations, “2024 Annual Report,” Hexcel Corporation, hexcel.com Continuous-autoclave curing and automated tape laying now enter mainstream floor panel production, boosting throughput and reducing rework rates to meet airframe schedules.

Rising Adoption of Recyclable Thermoplastic Honeycomb Cores for Circularity Goals

Europe’s Green Deal and comparable North American ESG frameworks motivate airlines and lessors to pursue panels with end-of-life recovery pathways. EconCore, Toray, and Bostik co-developed a flame-safe thermoplastic honeycomb solution that passes vertical burn tests without phenolic resins, paving the way for heat-welded disassembly. The ECO-COMPASS research consortium targets 50% weight trim and 20% CO₂ cuts via recycled carbon-fiber inserts across interior panels. At the same time, Collins Aerospace operates twin thermoplastic composite (TPC) lines in California and the Netherlands, producing 2,500 part numbers. Close to 700 commercial aircraft retire each year, and that tally is set to climb as early 2000s-built aircraft come due, creating a stream of recyclable panel scrap ready for circular processing.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Nomex and carbon-fiber pricing compressing supplier margins | -1.1% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Persistent supply-chain constraints for aerospace-grade honeycomb cores | -0.9% | Global, acute in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Lengthy certification and qualification cycles for new core materials and bonding processes | -0.7% | Global regulatory harmonization led by FAA, EASA, ICAO | Long term (≥ 4 years) |

| Adhesive-bond delamination and moisture-ingress incidents triggering fleet-wide inspection directives | -0.5% | Global, with heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Nomex and Carbon-Fiber Pricing Compressing Supplier Margins

Nomex paper and aerospace-grade carbon fiber rely on petroleum-based feedstocks and specialized precursor capacity, exposing prices to crude oil swings and energy price fluctuations. Hexcel has trimmed its 2025 revenue outlook to USD 1.88–1.95 billion, citing rising raw-material costs and extended receivable cycles as airframers accelerate deliveries. DuPont likewise signals continued cost pass-through for its Nomex portfolio after capacity outages at select meta-aramid plants. Tier-two panel assemblers operate on thinner margins and often lack long-term supply contracts, forcing them to hedge or absorb volatility, which dilutes the capital available for R&D.

Persistent Supply-Chain Constraints for Aerospace-Grade Honeycomb Cores

Aerospace-grade honeycomb production requires proprietary expansion equipment and multiple clean-room bond lines, limiting the pool of qualified global suppliers. The US Government Accountability Office lists core material shortages among the top three impediments to Boeing and Airbus rate increases. Certification of novel core geometries can stretch 18–24 months under FAA and EASA test regimes, dissuading new entrants. Recent FAA directives on adhesive-bond delamination further tighten inspection cycles, adding process complexity and driving rework expenses in panel deliveries, especially in high-growth Asia-Pacific final-assembly centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Core Material: Nomex Dominance Faces Carbon-Fiber Challenge

Nomex honeycomb held a 66.20% slice of the commercial aircraft floor panels market in 2025, reflecting decades of compliance with FAR 25.853 flammability rules and broad line-fit approvals. Nomex’s low smoke toxicity and favorable handling encourage continued use, anchoring baseline demand even as weight-saving pressures intensify. Hexcel and DuPont supply most aramid paper worldwide, granting them scale economies that small rivals struggle to match. However, the segment’s growth plateaus as operators pivot toward higher specific-modulus alternatives for premium cabins and long-range jets.

Carbon-fiber honeycomb combines thinner cell walls with superior compressive strength, unlocking cabin weight reductions of up to 10 kg per aircraft. Research published in the Journal of Sandwich Structures and Materials demonstrates that thicker-walled carbon cores avert shear-type instability under service loads, sustaining fatigue life across 90,000 flight cycles. The commercial aircraft floor panels market size for carbon-fiber cores is forecast to widen at an 8.42% CAGR. However, qualification costs and resin-film-adhesive compatibility still limit penetration on legacy narrowbody fleets. Aluminum cores remain relevant for cargo floors where impact tolerance outweighs the potential for fuel savings, while emerging thermoplastic and bio-derived variants are testing recycling pathways crucial to European circular economy mandates.

The innovation frontier centers on thermoplastic honeycomb options, such as EconCore’s ThermHex, which integrates recycled polypropylene feedstock and passes vertical burn tests without the use of phenolics. Panel makers pair these cores with PEI or PPS skins to produce fully weldable assemblies that airlines can shred and re-melt after decommissioning. Full-scale static and dynamic load trials on 9-g tie-down seats confirm equivalent structural margins, clearing an early hurdle toward line-fit status. As regulatory bodies fine-tune cradle-to-grave emissions accounting, the commercial aircraft floor panels market may progressively reward suppliers that offer transparent recycling certificates alongside performance guarantees.

By Fitment: OEM Leadership with Aftermarket Acceleration

Original equipment installations captured 60.70% of the commercial aircraft floor panels market revenue in 2025, reflecting the sheer volume of factory-fresh deliveries at Airbus and Boeing lines. Every assembled fuselage ships with a complete, certified panel kit, locking suppliers into multi-year pricing and volume frameworks. Tier-one conglomerates manage direct lineside deliveries and often assume kitting responsibility, bundling seat tracks, insulation blankets, and fastening hardware into just-in-sequence shipments. Despite holding this anchor position, OEM demand is sensitive to temporary rate dips when airframers troubleshoot production quality issues.

Conversely, the aftermarket reflects a compound pull from cabin retrofits, heavy checks, and in-service damage events, leading to an 7.76% CAGR through 2031. Maintenance shops inside the Lufthansa Technik, HAECO, and ST Engineering networks blend OEM and PMA panel sources depending on customer cost targets. FAA data show PMA floor panel approvals rising 11% yearly as design-data packages from retired airframes become publicly available. Triumph Group recorded a spike in spares shipments tied to B737 and B787 cabin refresh programs, validating how larger fleets propel baseline aftermarket volumes. Crucially, the commercial aircraft floor panel industry now sees airlines negotiating total-cost-of-ownership packages that combine the purchase price with the end-of-lease residual value, amplifying the appeal of recyclable thermoplastic concepts.

By Aircraft Type: Narrowbody Dominance with Widebody Recovery

Narrowbody jets such as the B737 and A320 families accounted for 67.90% of the commercial aircraft floor panels market demand in 2025, supported by dense order books from low-cost carriers and network airlines. Each single-aisle airframe’s shorter cabin length moderates the absolute panel count, yet production volumes exceed those of widebody aircraft by roughly four-to-one, preserving the segment’s revenue heft. Route expansion plans in India, Vietnam, and Saudi Arabia underpin forward demand, while fleet-standardization strategies maintain consistent panel part numbers across sub-fleets, simplifying inventory management.

Widebody types are rebounding with international traffic normalization and slot scarcity at hub airports, and they are projected to grow at a 6.43% CAGR between 2026 and 2031. Emirates’ USD 1.2 billion cabin-upgrade package, covering the A350 and B777X platforms, pivots on premium-class branding, prompting bespoke floor panel layouts that integrate larger monument footprints and under-aisle wire conduits. Carbon-fiber honeycomb finds its earliest large-scale adoption in these long-range cabins, where every kilogram shaved translates into sizable mission fuel savings. Regional jets and turboprops remain a niche. However, they provide a steady baseline demand for aluminum-core variants used in lower-life-cycle platforms, especially in North American Essential Air Service routes and European PSO contracts.

Geography Analysis

The Asia-Pacific region retained a 30.85% share of the commercial aircraft floor panels market in 2025, underpinned by aggressive fleet growth in China, India, Indonesia, and Japan. Airbus projects that the region’s aircraft services spending will surge from USD 52 billion in 2025 to USD 129 billion by 2043, with maintenance spending alone climbing to USD 109 billion. Significant narrowbody backlogs, a vibrant low-cost carrier (LCC) sector, and offset agreements that favor local composites production extend procurement cycles for panel suppliers in Tianjin, Hyderabad, and Nagoya. Government-backed R&D documents emphasize the increased adoption of digital design and highlight cost gaps compared to Western peers, signaling a further localization of floor panel finishing and inspection activities.

The Middle East and Africa are expected to deliver the fastest forecast expansion at a 7.08% CAGR through 2031. Boeing forecasts 2,370 new-build aircraft, valued at USD 470 billion, entering the region by 2031, with 69% of these expected to stem from passenger traffic growth and the maturation of hub-and-spoke networks. Emirates, Qatar Airways, and Saudia collectively hold more than 880 widebody airframes on order or option, translating into high-value panel kits tailored for premium-class cabins. Concurrent investments in MRO free zones at Jeddah and Addis Ababa reduce turnaround times and facilitate localized panel repairs, thereby reinforcing the region’s complete value chain.

North America ranks third in revenue but commands significant technical influence; many panel design approvals are held by US or Canadian authorities. Consolidation through Boeing’s USD 8.3 billion acquisition of Spirit AeroSystems brings strategic stockholding of honeycomb core capacity onshore, smoothing OEM deliveries while rearranging competitive bidding for independent shops. Europe maintains a strong sustainability focus, championing the adoption of recyclable thermoplastics through ECO-COMPASS grants and mandating more transparent life-cycle analysis labels, which push suppliers to co-develop closed-loop recovery hubs adjacent to Hamburg and Toulouse assembly lines. Collectively, these mature regions stabilize the commercial aircraft floor panels market by balancing cyclical production swings with predictable retrofit cycles.

Competitive Landscape

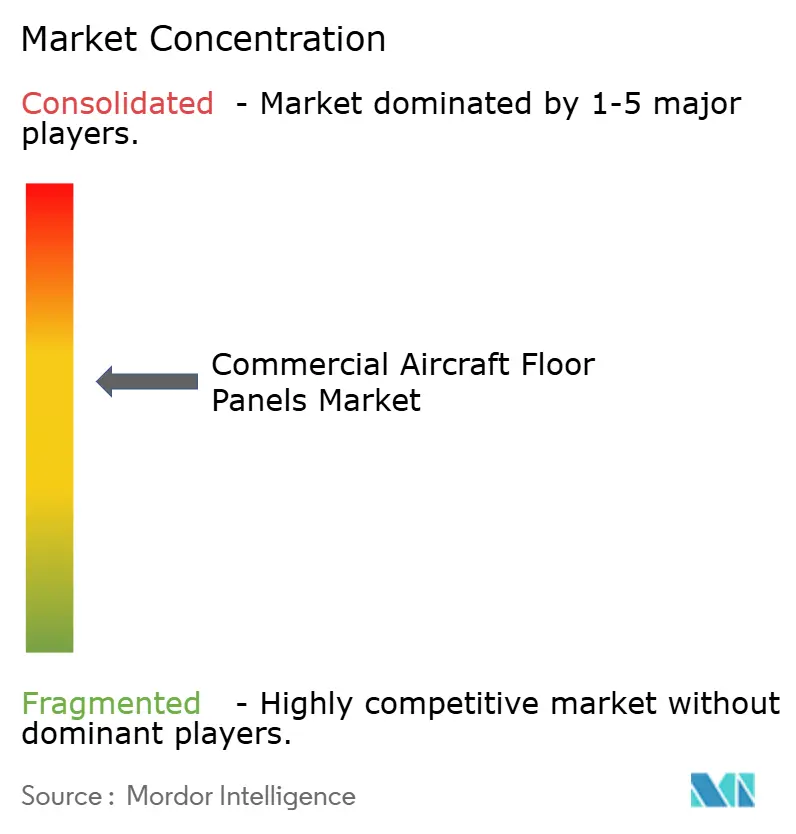

The commercial aircraft floor panels market features a moderate level of concentration. The top five suppliers collectively command over 40% of the market share, reflecting high certification barriers and entrenched line-fit contracts. Boeing’s acquisition of Spirit AeroSystems and Airbus’s parallel purchase of Spirit’s Northern Ireland and Morocco units consolidate vertically integrated supply chains and amplify purchasing leverage. Hexcel Corporation, Collins Aerospace, Safran S.A., and Triumph Group Inc. are the leading companies, each utilizing proprietary material chemistries or automated cell-expansion techniques that maintain a competitive edge.

Technology differentiation pivots on advanced composites, adhesive innovations, and continuous-flow manufacturing. Collins Aerospace deploys automated thermoplastic tape placement in California, reducing cycle times by 30% compared to batch autoclave processes. MTorres’ Torreswing concept eliminates molds and fasteners by curing panels on dynamic kinematic frames, hinting at future cost compression. EconCore champions recyclable polypropylene honeycomb cores that meet aviation flame-smoke-toxicity thresholds without the use of phenolics, carving a sustainability niche that legacy aramid products cannot match at the end of their life cycle.

Strategic collaboration remains a preferred growth lever. Satair leverages Telair’s cargo-handling know-how to bundle floor and side-wall solutions within unified inventory pools. Safran integrates reclaimed LEAP engine blades into decorative panel veneers to showcase circular-economy credentials while shrinking Scope 3 emissions. Meanwhile, PMA specialists forge alignments with independent MRO shops to win share in price-sensitive narrow-body fleets, expanding data-supported reliability dossiers that reassure cautious lessors.

Commercial Aircraft Floor Panels Industry Leaders

The Gill Corporation

Collins Aerospace (RTX Corporation)

Triumph Group, Inc.

Safran S.A.

Hexcel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Airbus SE finalized a deal to acquire industrial assets from Spirit AeroSystems, specifically targeting its commercial aircraft programs.

- October 2024: Comtek Advanced Structures Ltd., a subsidiary of Latecoere Company, received a contract from De Havilland Aircraft of Canada Limited to design and manufacture composite floors for the DHC-6 Twin Otter Classic 300-G aircraft. The agreement covers the entire flooring system for both the cabin and cockpit sections.

- May 2024: In collaboration with SHD, JCB Aero unveiled a lightweight floorboard panel system utilizing FRVC411 prepreg material, which is compliant with BMS4-17/20/23 standards. The EASA-certified system is compatible with 95% of Boeing cabin configurations, including B737, B747, and B777 aircraft models.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the commercial aircraft floor panels market as factory-built or retrofitted sandwich panels, typically aluminum or Nomex honeycomb with glass or carbon skins, that form the primary walkable deck in passenger and belly-cargo zones of civil jet-powered aircraft. These panels must meet FAR 25 fire, smoke, and toxicity limits while minimizing weight for better fuel burn.

Scope exclusions: The analysis leaves out floor structures for military, business aviation, rotorcraft, and all non-floor interior sandwich panels (lavatory, galley, sidewall).

Segmentation Overview

- By Core Material

- Nomex Honeycomb

- Aluminum Honeycomb

- Carbon-Fiber Honeycomb

- Others

- By Fitment

- OEM

- Aftermarket

- By Aircraft Type

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed aircraft interior engineers, MRO sourcing heads in North America, Europe, and Asia-Pacific, and tier-one panel fabricators. These discussions clarified average ship-set sizes, Nomex-to-aluminum adoption rates, and aftermarket price bands, helping us validate conversion factors and stress-test secondary findings.

Desk Research

We began by compiling production and in-service fleet statistics from bodies such as the FAA, EASA, and ICAO, then overlaid import-export codes for "aircraft parts, composite panels" drawn from UN Comtrade. Airframer build logs, OEM annual reports, and airline retrofit bulletins supplied baseline delivery counts and replacement cycles. To refine material splits, we extracted patent activity through Questel and reviewed technical papers in SAE Aerospace Proceedings. Finally, news archives in Dow Jones Factiva traced panel contract values and pricing trends. The sources named are illustrative; many additional open datasets were tapped to cross-check volumes and values.

Market-Sizing & Forecasting

A top-down model began with commercial jet deliveries and active fleet counts, which are then multiplied by typical floor-panel area per aircraft and unit-area pricing to build the demand pool. Supplier revenue roll-ups and select channel checks supplied a bottom-up reasonableness check before final adjustment. Key inputs include narrow-body production schedules, cabin reconfiguration intervals, composite material cost indices, regulatory burn-through limits driving redesigns, and passenger-to-freighter conversion rates. A multivariate regression, anchored on GDP-weighted RPK growth and oil-price-linked fuel-efficiency incentives, generates the 2025-2030 forecast path. Data gaps, such as limited disclosure on retrofit volumes, were bridged with triangulated interview ranges and conservative midpoint assumptions.

Data Validation & Update Cycle

Outputs pass variance screens against historical ASPs and independent shipment signals, then go through a two-person analyst review. The dataset refreshes annually, with interim pulse checks triggered by major OEM schedule shifts or regulatory mandates, ensuring clients access the latest vetted view.

Why Our Commercial Aircraft Floor Panels Baseline Commands Reliability

Published estimates often diverge because firms choose different aircraft mixes, retrofit assumptions, and refresh cadences.

Key gap drivers include wider "aerospace" scopes that fold in defense fleets, reliance on vendor revenue extrapolation without fleet alignment, and single-shot models that miss OEM rate changes mid-cycle. Mordor's delivery-linked build and yearly refresh temper optimism when production slips or material costs swing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 352.21 Mn (2025) | Mordor Intelligence | - |

| USD 419.6 Mn (2023) | Regional Consultancy A | Includes military and biz-jet panels; limited geographic split |

| USD 506.0 Mn (2024) | Trade Journal B | Uses supplier revenue roll-ups without delivery normalization |

Taken together, the comparison shows that our fleet-anchored, variable-rich approach delivers a balanced, transparent baseline that decision-makers can trace back to clearly stated volumes, prices, and refresh logic.

Key Questions Answered in the Report

What is the current size of the commercial aircraft floor panel market?

The market stands at USD 373.98 million in 2026 and is set to grow to USD 504.27 million by 2031 at a 6.18% CAGR.

Which core material dominates floor panel demand?

Nomex honeycomb cores lead with 66.20% market share, although carbon-fiber honeycomb is the fastest riser at an 8.42% CAGR.

Why is the Middle East a high-growth region for floor panels?

Boeing forecasts 2,370 aircraft deliveries to the region by 2031, many of them wide-bodies that require premium-grade panels, fueling a 7.08% CAGR.

How do PMA parts influence aftermarket growth?

FAA-approved PMA floor panels cost up to 40% less than OEM parts, helping push aftermarket revenue toward an 7.76% CAGR through 2031.

What sustainability measures are impacting panel design?

Airlines and regulators favor recyclable thermoplastic honeycomb cores and bio-derived skins, encouraging suppliers to develop panels with validated end-of-life recovery routes.

How concentrated is the supplier landscape?

The top five vendors control more than 40% of revenue, signaling moderate concentration.

Page last updated on: