Aircraft Galley Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

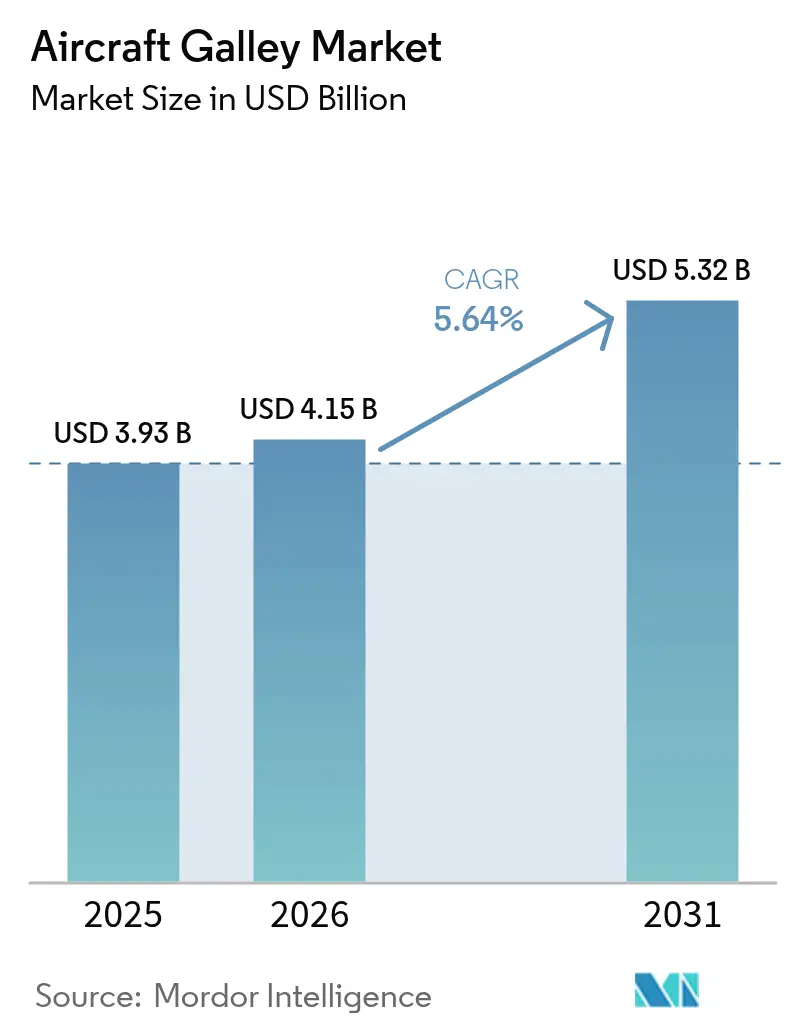

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 5.32 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

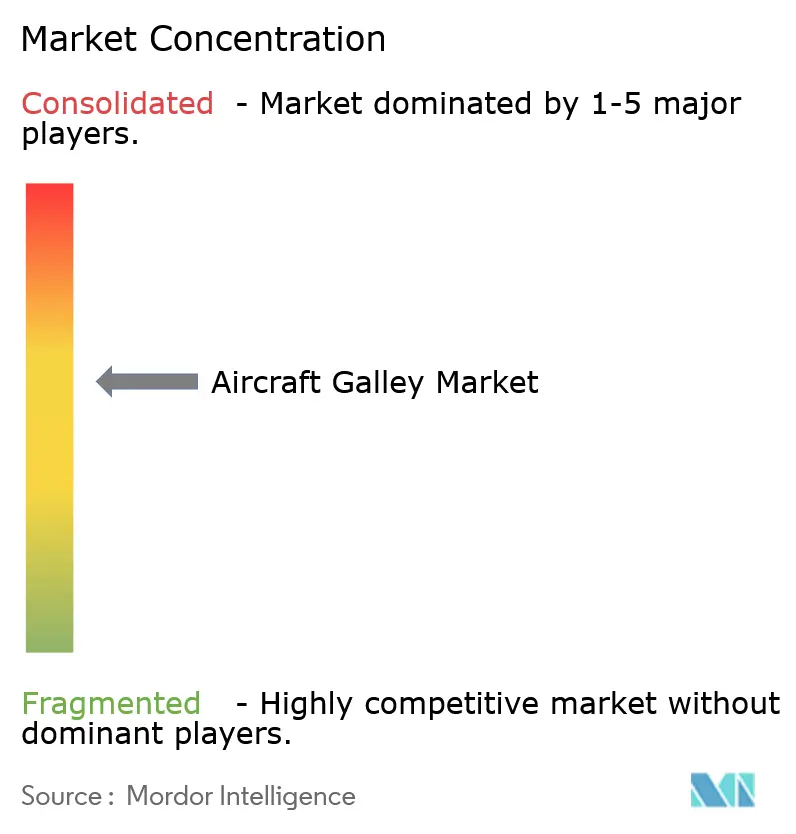

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Galley Market Analysis by Mordor Intelligence

Aircraft galley market size in 2026 is estimated at USD 4.15 billion, growing from 2025 value of USD 3.93 billion with 2031 projections showing USD 5.32 billion, growing at 5.64% CAGR over 2026-2031. Airlines channel post-pandemic cash flows into cabin modernization, with weight-saving composite monuments, connected inserts, and end-of-life retrofits forming the pillars of near-term demand. A sustained narrowbody backlog, electrification roadmaps that favor power-efficient appliances, and premium-class differentiation on new widebody programs all reinforce a stable replacement cycle. Makers that provide integrated digital platforms are winning long-term service contracts, while supply-chain stress around aerospace-grade composites is nudging OEMs toward vertical integration strategies. Sustainability pressures—from fuel-burn reduction to mandated waste segregation—remain the dominant design lens shaping the aircraft galley equipment market.

Key Report Takeaways

- By aircraft type, single-aisle platforms led with 61.05% revenue share in 2025, while twin-aisle programs are poised to log a 6.13% CAGR through 2031.

- By galley insert type, electric inserts commanded a 67.40% share in 2025; the segment is advancing at a 6.58% CAGR to 2031, outpacing non-electric alternatives.

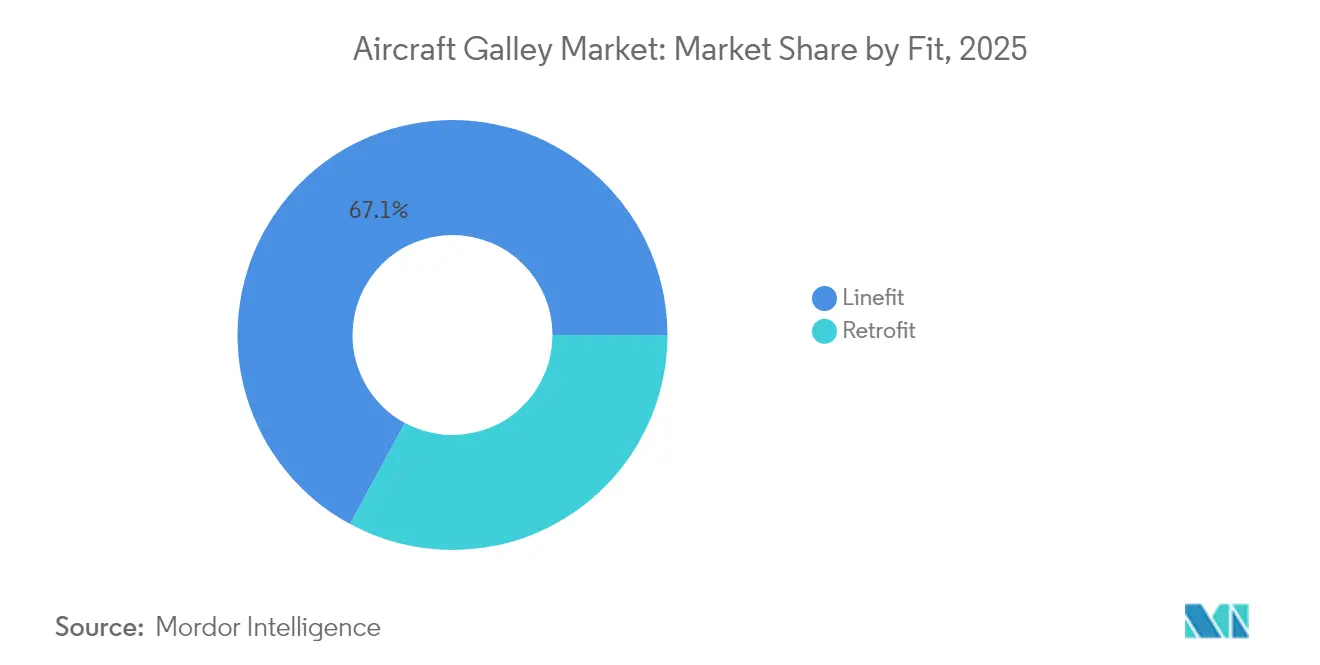

- By fit, linefit installations captured 67.10% of 2025 deliveries, whereas retrofit activity is projected to deliver a 6.05% CAGR over the forecast window.

- By material, aluminum retained 43.30% of 2025 revenue, yet composites and thermoplastics are projected to post a 6.67% CAGR through 2031.

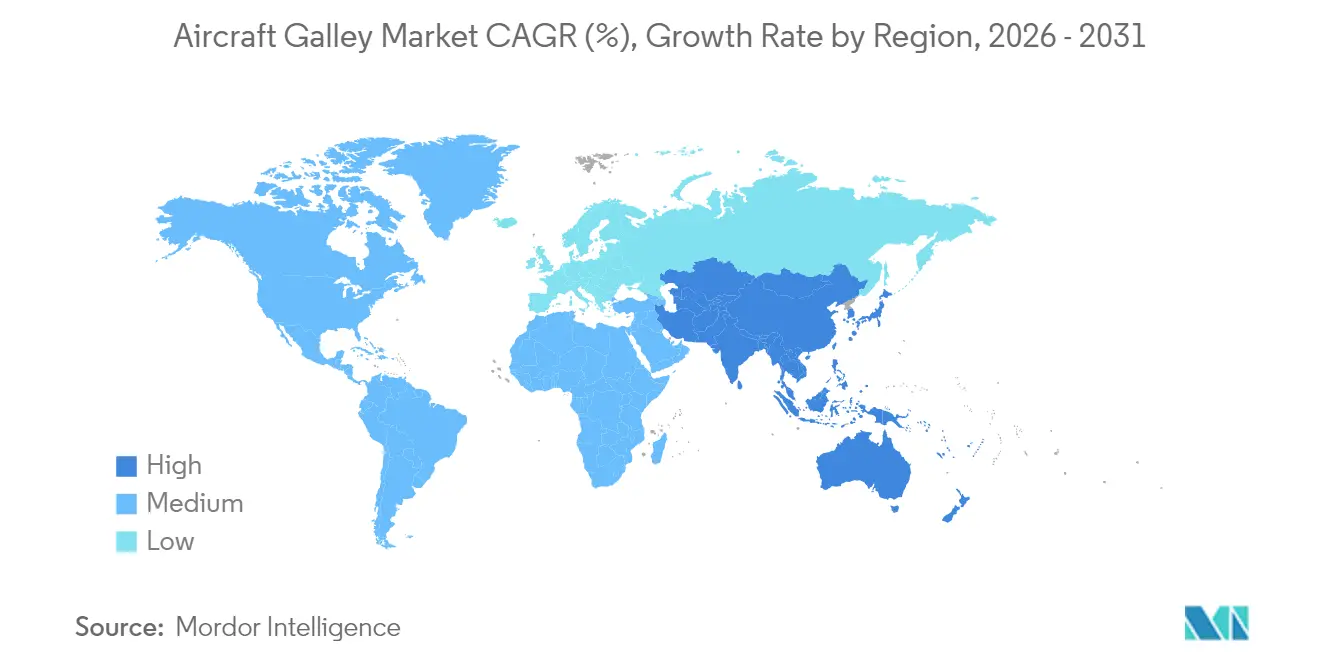

- By geography, North America topped the 2025 revenue table with a 31.30% share, while Asia-Pacific is forecasted to be the fastest-growing region at a 6.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Galley Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward lightweight composite and thermoplastic galley structures | +1.2% | Global; early adopters in North America and EU | Medium term (2-4 years) |

| Rising demand for smart galley inserts in new single-aisle aircraft programs | +1.5% | Global; led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Widebody fleet renewals driving adoption of premium-class service galleys | +0.9% | North America, Europe, Middle East | Medium term (2-4 years) |

| Growth in airline ancillary revenue models supporting self-service galley modules | +1.1% | Global; focus on North America and Europe | Short term (≤ 2 years) |

| Regulatory pressure to implement cabin waste segregation solutions | +0.6% | Global, with EU leading implementation | Long term (≥ 4 years) |

| Electrification roadmaps driving the need for load-shedding compatible galley appliances | +0.7% | Global, aligned with OEM electrification timelines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Lightweight Composite and Thermoplastic Galley Structures

Cabin monuments fabricated from carbon-fiber reinforced plastics and advanced thermoplastics trim 20–30% off legacy aluminum ship-sets, cutting airline fuel burn on every cycle.[1]Collins Aerospace, “Seamless Passenger Journey,” collinsaerospace.com Operating-cost relief dovetails with environmental targets as carriers chase fleet-wide CO2 reductions. Premium cabin operators also prize composites for their design flexibility, enabling integrated branding, bionic partitions, and sculpted self-service counters that amplify passenger touch-points. Fire-safety testing, higher raw material outlays, and limited autoclave capacity temper adoption. However, OEM roadmaps now bundle lighter galleys as the default, signaling an irreversible shift in the aircraft galley equipment market.

Rising Demand for Smart Galley Inserts in New Single-Aisle Aircraft Programs

The latest generation of ovens, chillers, and beverage makers embeds IoT sensors that stream performance data to cabin and ground portals. Collins Aerospace’s connected galley suite links to an AI assistant that alerts crews to inventory gaps and optimizes service sequencing, reducing unscheduled maintenance events by up to 15%. Airbus’s Skywise environment further stitches these appliances into a cabinwide data fabric, giving operators predictive insights and shortening turn times.[2]Airbus, “Skywise Connected Experience,” airbus.com Airlines deploying such smart galleys unlock higher ancillary sales while lowering lifetime support costs—an advantage set to accelerate fleet-wide digital retrofits.

Widebody Fleet Renewals Driving Adoption of Premium-Class Service Galleys

As passenger yield pivots to the front of the cabin, long-haul carriers specify mezzanine-style pantries, espresso stations, and chef-grade ovens that lift culinary standards. Custom monuments integrate chilled carts, induction cooking, and plated-meal staging shelves, enabling restaurant-quality service on 12-hour sectors. Upscale materials add 30–40% to unit cost, translating into more substantial brand equity and higher business class load factors. With B777-9 and A350-1000 deliveries cresting, the aircraft galley equipment market is seeing an uptick in bespoke premium galleys configured to maximize galley-to-seat ratios without compromising crew workflow.

Growth in Airline Ancillary Revenue Models Supporting Self-Service Galley Modules

Digital ordering applications and cashless payment nodes are driving a redesign of galley space into retail alcoves stocked with pre-packed meals, merchandised snacks, and wellness products. Airlines report double-digit uplifts in average basket size when passengers browse and collect items during free cabin movement phases. Monetization success hinges on secure storage, rapid-cool mini-fridges, and NFC-enabled dispensers, pushing suppliers to bundle hardware with inventory tracking software. As ancillary revenue share rises above 15% of total airline turnover, demand for mixed-use galleys that combine catering, retail, and waste-segregation functions gains momentum across the aircraft galley equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long certification timelines for innovative galley monument designs | -0.8% | Global; FAA vs EASA variances | Long term (≥ 4 years) |

| High raw material costs for aerospace-grade composites | -0.5% | Global; supply concentration in North America | Short term (≤ 2 years) |

| Supply chain concentration among a small number of Tier-1 galley manufacturers | -0.6% | Global, with critical dependencies in North America and Europe | Medium term (2-4 years) |

| Deferral of retrofit programs due to airline cash flow volatility | -0.4% | Global, with higher impact in emerging markets and low-cost carriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Long Certification Timelines for Innovative Galley Monument Designs

Galley structures must clear rigorous flammability, decompression, and evacuation-path testing governed by ICAO cabin safety protocols.[3] International Civil Aviation Organization, “ICAO Requirements Related to Cabin Safety,” icao.int Novel composite partitions or integrated lighting layouts often extend certification loops to 30 months, tying up capital and delaying entry into service. The process advantages incumbents with deep regulatory expertise, creating a barrier for start-ups offering disruptive concepts. Airlines weigh these risks when scheduling retrofit downtime, slowing the cadence of next-gen galley roll-outs.

High Raw Material Costs for Aerospace-Grade Composites

Advanced carbon fabrics and phenolic resin systems attract 15–20% premiums over aluminum sheet. Supply is concentrated among a handful of qualified US and European mills, exposing programs to price spikes and lead-time instability. While long-term fuel-burn savings frequently justify the up-front spend, airlines facing tight capex cycles may defer retrofits, dampening near-term orders in the aircraft galley equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Single-Aisle Backlog Underpins Volume

The aircraft galley market size attributed to single-aisle platforms accounted for 61.05% of 2025 revenue. B737 MAX and A320neo output keeps assembly lines buzzing, anchoring a 4.49% CAGR through 2031. Compact monument footprints, modular inserts, and lightweight carts dominate specifications as airlines optimize turnaround times on high-cycle routes. The aircraft galley equipment market share for twin-aisles remains smaller today. Still, it is expanding at a 6.13% CAGR due to the deliveries of the B787-9, A350-900, and B777-9, which feature premium-service galleys with larger chilled volumes and digital diagnostics. Business jet demand is a niche yet lucrative market, with bespoke veneers, induction cooktops, and barista modules generating higher margins per ship-set.

Second-generation narrowbody cabins are increasingly featuring self-service pantries adjacent to forward galleys, creating new aftermarket potential. On long-haul quad-crew missions, operators prioritize ergonomic layouts that shorten service cycles and reduce fatigue. VIP airframers translate lessons from commercial programs into high-touch materials—marble-look surfaces, electrochromic dispensers—that later filter back into linefit catalogues, driving continuous innovation in the aircraft galley equipment market.

By Galley Insert Type: Electrification Accelerates

Electric inserts represented 67.40% of global shipments in 2025, reflecting airlines’ tilt toward power-efficient ovens, espresso machines, and chillers that integrate with cabin–power distribution systems. This cohort is tracking a 6.58% CAGR, dwarfing mechanically driven or propane-based equipment still used by select legacy fleets. Electric architectures enable real-time energy monitoring and intelligent load shedding, ensuring system resilience during peak usage. As OEMs pursue more-electric aircraft concepts, certified insert suppliers position connected appliances as standard, strengthening the aircraft galley equipment market share of electric solutions.

Mechanical inserts persist where retrofit budgets are constrained or cabin-power upgrades would extend downtime. Still, rising spare-parts costs and regulatory carbon targets are tilting total-cost-of-ownership math toward electrified replacements. Leasing companies now bundle digital inserts into return-condition clauses, further normalizing the transition and supporting sustained growth across the aircraft galley equipment market.

By Fit: Retrofit Momentum Builds

Linefit accounted for 67.10% of installations in 2025, leveraging factory integration and streamlined certification pathways. Yet retrofit programs are mounting the fastest climb—6.05% CAGR—as carriers extend aircraft economic lives while refreshing cabin appeal. Quick-turn modified monuments, plug-and-play connected inserts, and pre-certified composite doors enable overnight installation, lowering aircraft-on-ground exposure. The aircraft galley equipment market size for retrofits is rising with global narrowbody lease extensions and widebody premium refresh cycles.

Regulatory triggers also lift retrofit spending. New waste-segregation mandates compel operators to add sealed biohazard units and recycling bins, while cybersecurity guidelines for connected appliances require upgraded firewalls and data-bus protectors. Supplier-financed retrofit kits help smaller carriers bridge capital gaps, ensuring broad diffusion of next-gen galley technologies through 2031.

By Material: Composites Gain Strategic Ground

Aluminum retained 43.30% of 2025 shipments thanks to its favorable cost-to-strength ratio and established supply chains. Even so, composite and thermoplastic assemblies are posting a forecast 6.67% CAGR, underpinned by airline fuel-burn targets and ESG scorecards. Novel resin systems achieve low-temperature cure cycles, reducing energy use during manufacturing while improving part recyclability. These gains amplify the aircraft galley equipment market’s appeal to carriers publishing sustainability reports.

Combining aluminum frames with composite door skins, hybrid stacks offer a transition path that balances cost and weight. In parallel, flame-retardant thermoplastics pass updated heat-release standards, opening fresh design territory for curved surfaces and integrated lighting recesses. Material innovations continue to reshape competitive dynamics in the aircraft galley equipment market.

Geography Analysis

North America led the 2025 revenue table at 31.30%, buoyed by large cabin-upgrade budgets and proximity to Boeing’s final assembly lines. The region’s early adoption of innovative galley ecosystems and stringent FAA oversight favors suppliers with deep retrofit credentials.

Asia-Pacific, however, is charting the fastest 6.18% CAGR as rising middle-class travel stimulates fleet additions and local MRO hubs proliferate. Chinese airframers partner with global insert vendors to localize supply, broadening the regional aircraft galley equipment market size.

Europe maintains a technology leadership posture, anchoring R&D into low-carbon materials and circular-economy cabin solutions aligned with EASA roadmaps. Middle East carriers fuel premium-galley demand as they chase super-connector status on intercontinental trunk routes, while Africa’s nascent fleets adopt lightweight monuments to offset high fuel costs. These dynamics ensure a geographically diversified growth pattern for the aircraft galley equipment market.

Competitive Landscape

The aircraft galley market is moderately concentrated: Safran SA, Collins Aerospace (RTX Corporation), Bucher Leichtbau AG, Diehl Stiftung & Co. KG, and JAMCO Corporation jointly control the majority of global revenue. Scale affords these firms robust certification track records and integrated service networks. JAMCO’s strength in widebody monuments delivers competitive insulation in long-haul programs, while Safran leverages vertical integration to de-risk composite material supply. Collins Aerospace differentiates through its galley.ai software layer, securing aftermarket royalties and deepening operator lock-in.

Second-tier suppliers such as Diehl Aviation and Iacobucci HF Aerospace carve out a share via niche product excellence—coffee brewers, chillers, and connectivity nodes that bolt into larger OEM ecosystems. Strategic alliances are forming around cybersecurity and data analytics modules, foreshadowing a service-centric revenue remix in the aircraft galley equipment market. Private-equity entries signal confidence in expanding retrofit volumes and digital-service annuities, although high certification hurdles continue to deter green-field disruptors.

Aircraft Galley Industry Leaders

Collins Aerospace (RTX Corporation)

Bucher Leichtbau AG

JAMCO Corporation

Diehl Stiftung & Co. KG

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: AMETEK Ameron, a manufacturer of aviation safety equipment and provider of repair and overhaul solutions, expanded its aircraft galley equipment repair facility to include aircraft faucet assembly capabilities. The company has operated in the aviation industry for 50 years.

- October 2023: AJW Group, an independent aircraft component, parts, repair, and supply chain solutions provider, signed a three-year Specific Business Arrangement (SBA) with Collins Aerospace to provide comprehensive repairs for galley inserts. The SBA will deliver several key benefits, including enabling AJW Group to streamline repair processes to reduce turnaround times and enhance operational efficiency.

Global Aircraft Galley Market Report Scope

The aircraft galley market considers the different companies that offer electrical and non-electrical galley inserts to provide a comprehensive qualitative outlook. Market estimates are based on line-fit installations of galleys into the cabin of new-generation aircraft being procured by airline operators around the globe. They are exclusive of the retrofitment of individual galley inserts.

The aircraft galley market is segmented by type and geography. By type, the market is segmented into single-aisle, twin-aisle, and business jets. The report also covers the market sizes and forecasts for the aircraft galley market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Single-Aisle |

| Twin-Aisle |

| Business Jets |

| Electric Inserts |

| Non-Electric Inserts |

| Linefit |

| Retrofit |

| Aluminum |

| Composites and Thermoplastics |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Single-Aisle | ||

| Twin-Aisle | |||

| Business Jets | |||

| By Galley Insert Type | Electric Inserts | ||

| Non-Electric Inserts | |||

| By Fit | Linefit | ||

| Retrofit | |||

| By Material | Aluminum | ||

| Composites and Thermoplastics | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft galley market in 2026?

The aircraft galley market size is USD 4.15 billion in 2026.

What is the forecast CAGR for aircraft galley market through 2031?

The market is projected to expand to USD 5.32 billion and register a 5.64% CAGR between 2026 and 2031.

Which aircraft type dominates demand for galley equipment?

Single-aisle platforms account for 61.05% of 2025 revenue, making them the largest demand driver.

Why are electric galley inserts gaining popularity?

Electric inserts provide energy monitoring, load-shedding compatibility, and digital diagnostics, supporting airline sustainability and maintenance goals.

Which region is expected to grow fastest?

Asia-Pacific is the fastest-growing region, forecasted to post a 6.18% CAGR through 2031.

Page last updated on: