Aircraft Synthetic Vision Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

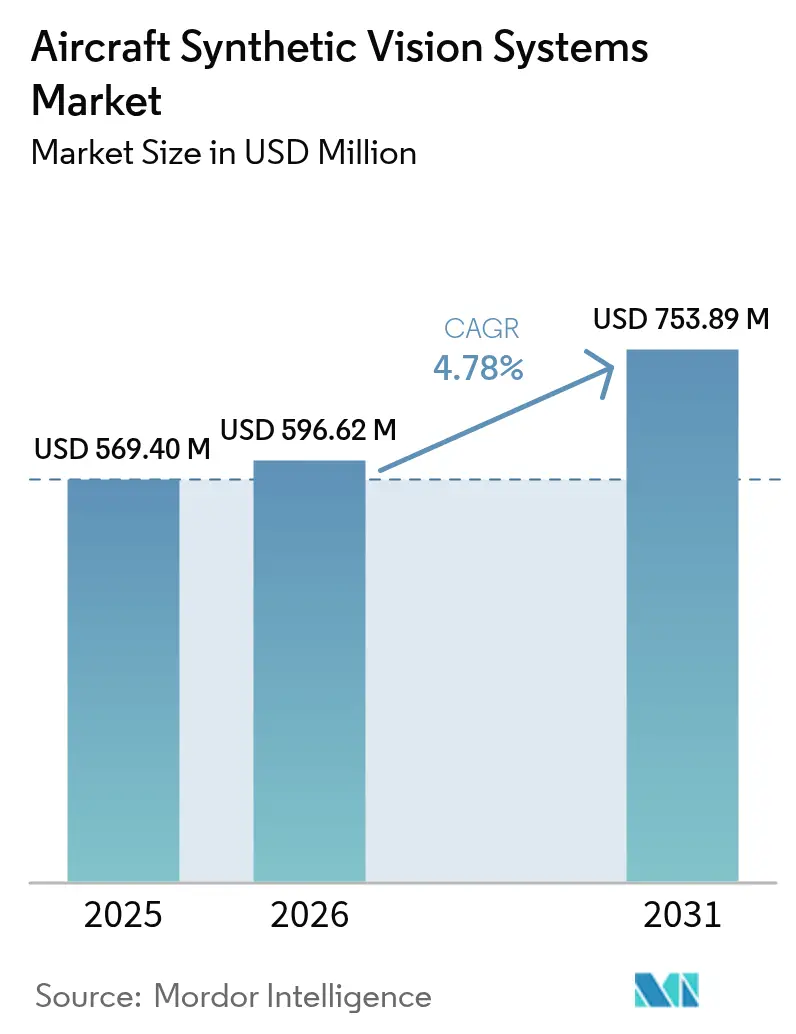

| Market Size (2026) | USD 596.62 Million |

| Market Size (2031) | USD 753.89 Million |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

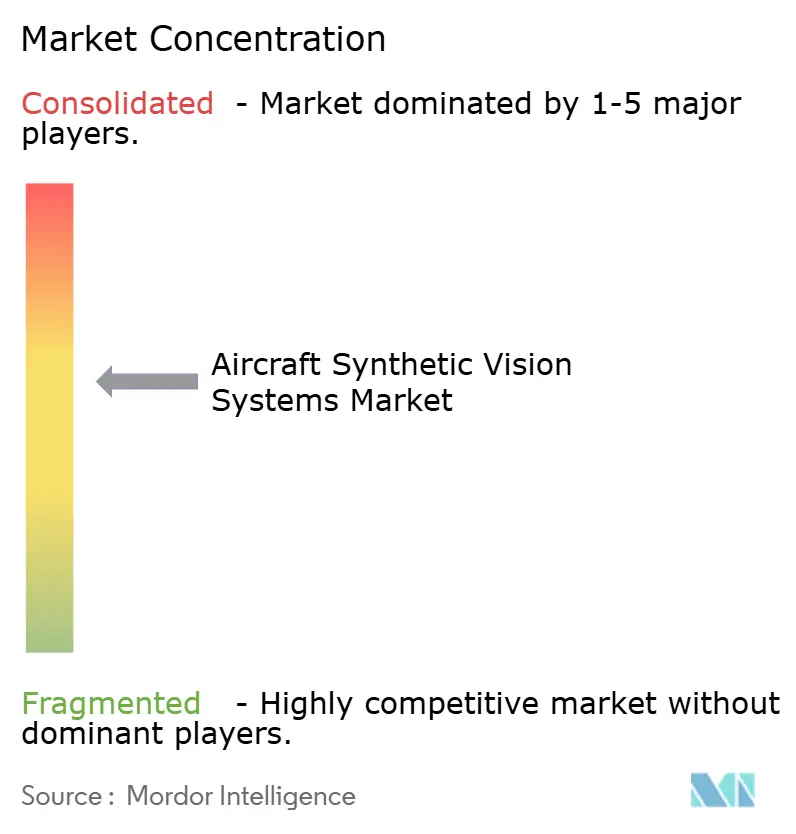

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Synthetic Vision Systems Market Analysis by Mordor Intelligence

The aircraft synthetic vision systems market size is expected to grow from USD 569.40 million in 2025 to USD 596.62 million in 2026 and is forecast to reach USD 753.89 million by 2031 at 4.78% CAGR over 2026-2031. Adoption is accelerating as US and European regulators mandate cockpit upgrades that deliver higher situational awareness during low-visibility operations. Airline and business-jet operators view synthetic vision as the most cost-effective path to compliance because the software can be embedded in existing flight-deck architectures, minimising downtime. Concurrently, air-framer partnerships focused on AI-driven terrain-rendering engines are lowering pilot workload while opening ancillary revenue streams for data-subscription services. Growth prospects are also buoyed by advanced air-mobility programs and sixth-generation fighter projects that treat synthetic vision as a core safety layer. These factors underpin a solid outlook for the Aircraft Synthetic Vision Systems market across OEM line-fit and retrofit channels.

Key Report Takeaways

- By type, primary flight displays held 45.02% of the aircraft synthetic vision systems market share in 2025, while heads-up and helmet-mounted displays are projected to grow at 10.82% CAGR from 2026 to 2031.

- By component, display systems commanded 39.68% revenue share in 2025; software/terrain-obstacle databases are forecasted to expand at a 9.09% CAGR through 2031.

- By platform, fixed-wing aircraft accounted for 52.74% of the aircraft synthetic vision systems market size in 2025, whereas advanced air-mobility/eVTOL platforms are poised to rise at 9.78% CAGR.

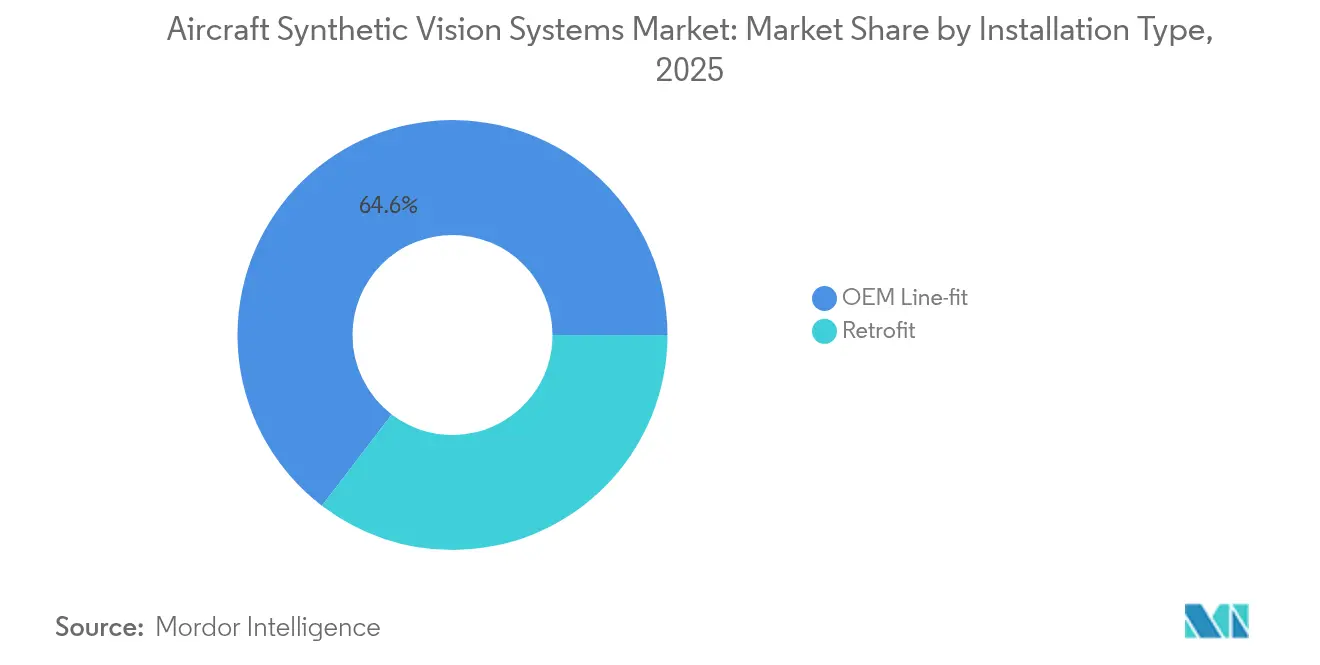

- By installation type, OEM line-fit solutions led with a 64.61% share of the aircraft synthetic vision systems market size in 2025; retrofit programs will advance at a 7.27% CAGR.

- By end user, military applications retained a 35.21% share in 2025, but general aviation is the fastest-growing segment, with a 6.89% CAGR.

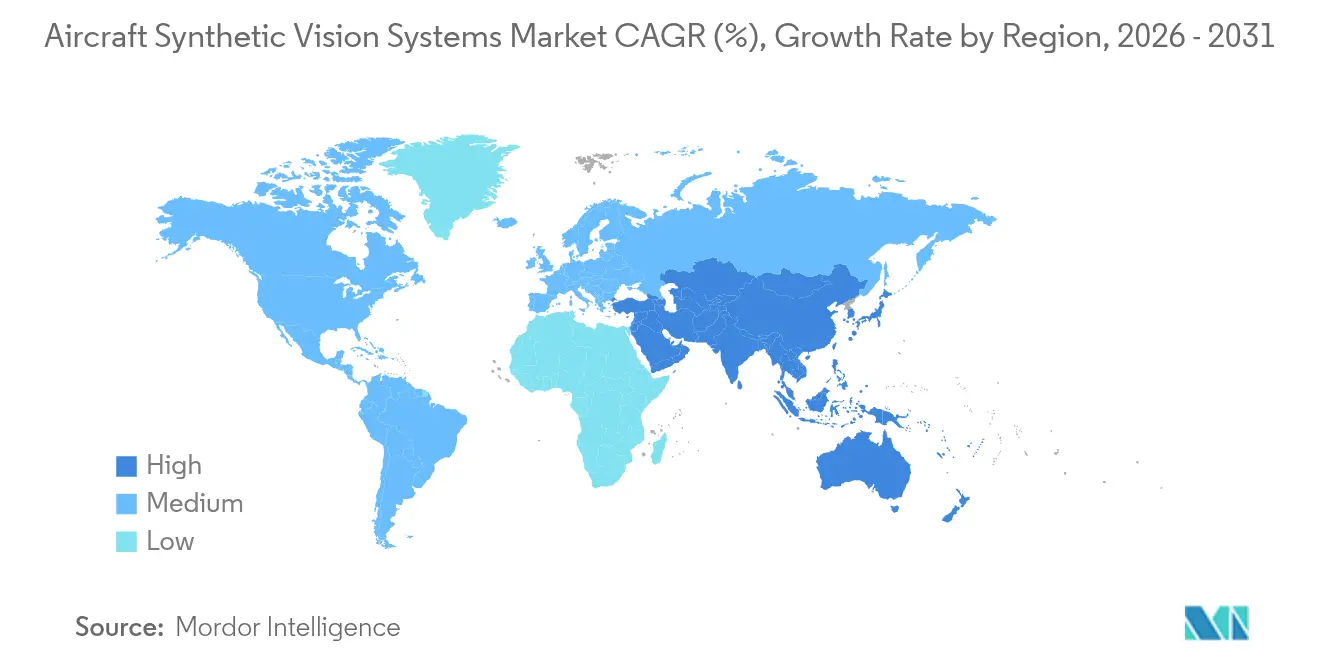

- By geography, North America dominated with a 34.92% revenue share in 2025; Asia-Pacific is the fastest-growing region, with an 8.33% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Synthetic Vision Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising business-jet deliveries with factory-fitted combined vision suites | +0.8% | North America and Europe; spill-over to APAC | Medium term (2-4 years) |

| Rapid adoption of SVS-enabled HUDs in Gen-6 fighter cockpits | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Demand for low-visibility approach credits at Tier-2 airports | +0.5% | Global; early gains in APAC secondary cities | Medium term (2-4 years) |

| Urban-air-mobility eVTOL programs requiring high-integrity SVS | +0.7% | Global; concentrated in North America and Europe | Long term (≥ 4 years) |

| OEM partnerships around AI-based terrain-rendering engines | +0.4% | Global | Short term (≤ 2 years) |

| Mandated retrofit of SVS under FAA NextGen and EASA SESAR timelines | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Business-Jet Deliveries with Factory-Fitted Combined Vision Suites

Deliveries of new business jets now routinely include combined vision suites that merge synthetic and enhanced vision on a single display. Bombardier’s Global 8000 and Cessna’s Citation Ascend integrate these features as baseline equipment, eliminating costly aftermarket installations.[1]Bombardier, “Global 8000 Programme Details,” bombardier.com Operators benefit from lower pilot workload, while manufacturers capture recurring upgrade revenue on legacy fleets scheduled for retrofits in 2025-2026.

Rapid Adoption of SVS-Enabled Huds in Gen-6 Fighter Cockpits (US And EU)

Sixth-generation fighter programs like the NGAD F-47 rely on helmet-mounted displays that fuse tactical data with real-time terrain imagery. Collins Aerospace’s Gen III helmet for the F-35 already demonstrates how synthetic vision replaces night-vision gear, paving the way for wider military adoption.[2]Collins Aerospace, “Gen III Helmet Mounted Display,” collinsaerospace.com Subsequently, civil platforms inherit these hardened technologies, shortening certification cycles.

Demand for Low-Visibility Approach Credits at Tier-2 Airports

Regulators now allow synthetic-vision-equipped aircraft to use lower minima without adding instrument-landing systems. The FAA’s Enhanced Low Visibility Operations rules and EASA’s All Weather Operations guidance let smaller airports boost capacity without infrastructure outlays.[3]Federal Aviation Administration, “Enhanced Flight Vision System Regulations,” faa.gov Airlines gain schedule resilience, and equipment makers tap a fresh retrofit market.

Urban-Air-Mobility eVTOL Programs Requiring High-Integrity SVS

eVTOL developers need synthetic vision to navigate congested low-altitude corridors with minimal pilot input. Honeywell’s Anthem flight deck targets failure rates 10^-9 for partners such as Vertical Aerospace, Archer, and Lilium. Certification special conditions issued by EASA explicitly reference synthetic vision as a primary navigation aid for urban operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification bottlenecks for database-centric vision algorithms | -0.7% | Global; stringent in North America and Europe | Medium term (2-4 years) |

| Cost sensitivity in turboprop and light-helicopter retrofits | -0.5% | Global; focused in emerging markets | Short term (≤ 2 years) |

| Limited GPU thermal budgets in cockpit-mounted hardware | -0.3% | Global | Medium term (2-4 years) |

| Cyber-hardening gaps in connected avionics buses | -0.4% | Global; heightened in defence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Certification Bottlenecks for Database-Centric Vision Algorithms

Machine-learning terrain databases do not fit neatly into deterministic DO-178C frameworks, prolonging approvals and raising development costs. In some cases, OEMs and avionics vendors limit the complexity of SVS features to reduce certification risk. Thus, features like dynamic terrain rendering, urban 3D modeling, or integration with EO/IR feeds are delayed. For instance, Mercury Systems’ image-integrity tools provide partial relief but still require Design Assurance Level C validation, a hurdle for smaller suppliers. Certification costs are passed on to operators in most cases, making SVS upgrades more expensive. This limits their commercial viability in the markets for small turboprop aircraft and helicopters.

Cost Sensitivity in Turboprop and Light-Helicopter Retrofits

Upgrade costs often exceed residual aircraft values in price-sensitive markets. For instance, full integration may exceed USD 60,000 to USD 100,000 for light helicopters with analog cockpits, making SVS retrofits highly cost-sensitive. Aircraft already undergoing panel modernization are the most likely to adopt SVS as part of a bundled upgrade strategy. Universal Avionics and Genesys have introduced lower-cost bundles, yet adoption lags in the business jet and airline segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Primary Flight Displays Dominate Integration

Primary flight displays held 45.02% of the aircraft synthetic vision systems market share in 2025 because pilots rely on these central screens for all critical flight cues. Heads-up and helmet-mounted displays exhibit the fastest growth at 10.82% CAGR, largely due to defence orders and the trickle-down of military technology into civil variants. Garmin’s SVT upgrade path shows operators adding 3-D terrain onto existing PFDs without re-wiring the cockpit. The aircraft synthetic vision systems market size for helmet-mounted solutions is projected to increase by 2031 as advanced air-mobility platforms favour wearable displays for weight savings.

The segment’s momentum extends to integrated combined-vision products that overlay infrared imagery onto synthetic terrain, delivering all-weather capability without added monitors. Universal Avionics’ ClearVision set a precedent for wearable HUD adoption in commercial jets, while Collins Aerospace adapts fighter-grade helmets for civil rotorcraft. These developments reinforce the aircraft synthetic vision systems market as a technology continuum rather than a discrete product, enabling cross-platform learning and volume efficiencies.

By Component: Display Systems Lead, Software Accelerates

Display hardware captured 39.68% revenue in 2025 because every installation still needs certified screens. Yet software and terrain-obstacle databases are growing at 9.09% CAGR, reflecting a pivot toward AI-rich content that refreshes during flight. This shift explains why the aircraft synthetic vision systems market size linked to software is forecast to overtake hardware-only packages in the late 2020s.

Suppliers increasingly licence rendering engines separate from displays, allowing operators to swap in lower-cost commercial-off-the-shelf monitors. Honeywell’s MEMS-based KSG7200 reference system highlights a broader trend toward sensor-fusion modules that package processing power within existing LRUs. Database subscriptions create recurring cash flows and cement customer relationships, underscoring software’s strategic value in the aircraft synthetic vision systems industry.

By Platform: Fixed-Wing Dominance, eVTOL Acceleration

Fixed-wing aircraft maintained 52.74% market dominance in 2025 because commercial airlines and business jet fleets already possess certified installation paths. Advanced air mobility and eVTOL platforms, however, are on track for a 9.78% CAGR, signalling a rapid broadening of the addressable aircraft synthetic vision systems market.

Urban air-taxi developers design synthetic vision from day one, bypassing legacy retrofit hurdles. Rotorcraft adoption remains driven by mission-critical operations in emergency medical and offshore transport. Unmanned aircraft increasingly depend on synthetic perception for beyond-visual-line-of-sight approvals, again enlarging the future aircraft synthetic vision systems market.

By Installation Type: OEM Integration Preferred

OEM line-fit solutions claimed 64.61% revenue share in 2025 because integrating synthetic vision during production avoids expensive downtime later. Retrofits grow at 7.27% CAGR as regulators compel legacy fleets to comply with NextGen and SESAR standards. Collins Aerospace’s King Air modernisation bundle demonstrates how a single STC covering synthetic vision can extend asset life by a decade.

Component miniaturisation and standardised data buses will lower installation time, encouraging operators to modernise rather than retire. Therefore, the Aircraft Synthetic Vision Systems market size linked to retrofit kits is set to climb steadily, albeit from a lower base.

By End User: Military Leadership, General Aviation Growth

Military customers accounted for 35.21% of revenue in 2025, reflecting defence priorities around contested airspace where visibility aids support survivability. General aviation leads growth at 6.89% CAGR as affordable retrofit packages enter the piston-twin and turboprop segments. As price points fall, the synthetic-vision benefit of shorter decision times and fewer weather diversions resonates with charter operators and flight schools.

Commercial airlines balance synthetic-vision deployments against other cockpit-upgrade initiatives, yet rising Tier-2 airport operations tilt the economics to favor adoption. Accordingly, the aircraft synthetic vision systems market diversifies, reducing over-reliance on military budgets.

Geography Analysis

North America generated 34.92% of global sales in 2025, supported by the FAA's clear rules on Enhanced Flight Vision and robust business-jet utilisation. Operators embrace synthetic vision to secure approach credits that keep schedules intact during winter storm activity. Defence contracts such as the F-47 program deepen the regional expertise pool, allowing suppliers to amortise R&D across civil and military lines.

Asia-Pacific is the fastest-growing arena at 8.33% CAGR because governments in China, India, and Indonesia are upgrading secondary airports while encouraging ACMI carriers to expand fleets. The aircraft synthetic vision systems market finds fertile ground in these nations, where low-visibility procedures were once the preserve of flagship hubs. Satellite-based augmentation and new GNSS constellations further boost uptake as ground-based ILS rollouts slow.

Europe grows steadily on the back of SESAR directives and strong defence programs. EASA's All Weather Operations framework gives carriers economic incentives to add synthetic vision without installing CAT II/III ground systems. Sustainability goals add another driver: optimised flight paths enabled by accurate terrain models cut fuel burn and CO₂. These factors sustain a balanced expansion of the continent's aircraft synthetic vision systems market.

Competitive Landscape

Competitive intensity is moderate, with collaboration eclipsing outright consolidation. Honeywell’s USD 17 billion strategic pact with Bombardier anchors a joint roadmap for AI-ready avionics, while the NXP tie-up secures semiconductor supply for next-generation GPUs. Collins Aerospace partners with military primes to advance helmet-mounted systems, then adapts the technology for civil rotorcraft, illustrating a virtuous cycle between defence and commercial lines.

Software-centric newcomers such as Daedalean and Lynx exploit gaps in AI certification and cloud-connected data services. Their algorithms offer finer obstacle detection, challenging legacy players to accelerate their own roadmaps. Meanwhile, Universal Avionics and Astronics focus on affordability, targeting mid-life business jets with constrained capital budgets. The Aircraft Synthetic Vision Systems market, therefore, rewards firms that master both regulatory nuance and real-time graphics processing.

Looking forward, white-space remains in Tier-2 airport operations and autonomous eVTOL corridors where incumbents lack local relationships. Expect joint ventures between avionics majors and regional service providers to capture these opportunities, further blurring the line between equipment vendor and data-service supplier.

Aircraft Synthetic Vision Systems Industry Leaders

Honeywell International Inc.

Thales Group

Collins Aerospace (RTX Corporation)

L3Harris Technologies, Inc.

Garmin Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vertical Aerospace and Honeywell deepened cooperation on the VX4 eVTOL, targeting 0.1 e-9 system-failure rates for the Honeywell Anthem flight deck.

- May 2025: Boeing secured a USD 20 billion NGAD contract to develop the F-47 sixth-generation fighter featuring AI-enabled autonomy.

- October 2024: Universal Avionics released upgrades to InSight and ClearVision aimed at extending jet lifespans by 20 years.

- May 2024: Textron Aviation scheduled Garmin SVGS upgrades for the Citation Latitude in 2025 and Longitude in 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the aircraft synthetic vision systems (SVS) market as all cockpit-installed hardware, software, and terrain-obstacle databases that create a real-time, 3-D digital view of runways, terrain, and airspace for piloted fixed-wing, rotary-wing, and unmanned aircraft. This digital overlay improves crew situational awareness during night or degraded visibility operations.

Scope exclusion: enhanced or combined vision units that rely primarily on external infrared or radar sensors without an embedded 3-D database have been kept outside the sizing.

Segmentation Overview

- By Type

- Primary Flight Display

- Navigation Display

- Heads-up and Helmet-mounted Display

- Other Types

- By Component

- Synthetic Vision Computer/Processing Unit

- Air-data and GPS Sensor Suite

- Display System

- Software/Terrain-Obstacle Databases

- Other Components

- By Platform

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

- Unmanned Aerial Vehicles (UAV)

- Advanced Air-Mobility/eVTOL

- By Installation Type

- OEM Line-fit

- Retrofit

- By End User

- Military

- Commercial

- General Aviation

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- Egypt

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed airline MRO managers, rotary-wing avionics engineers, and flight safety inspectors across North America, Europe, and Asia. These discussions refined penetration assumptions, retrofit lead times, and regional price corridors, letting us validate secondary findings before triangulation.

Desk Research

We first mapped the global fleet, production, and retrofit activity using open datasets such as FAA aircraft registry, EASA AD lists, ICAO traffic statistics, UN Comtrade avionics trade codes, and defense budget papers, which anchor the potential install base. Supplementary insights flowed from company 10-Ks, investor decks, and accident records. Paid libraries that Mordor analysts access, including D&B Hoovers for operator financials and Aviation Week for program timelines, helped cross-check adoption timing. Many more public and proprietary sources were referenced; the list above is illustrative, not exhaustive.

A second pass collated typical ship set prices, regulatory advisory circulars, and patent filings (Questel), giving us reference points for average selling prices and technology diffusion curves.

Market-Sizing & Forecasting

Top-down modelling begins with active aircraft counts by class, multiplies them with validated SVS penetration rates, and then with region-specific average selling prices; supplier roll-ups on sample programs offer a bottom-up sense check. Key variables include annual OEM deliveries, average retrofit age, cockpit upgrade budgets, regulatory equipage mandates, and ASP erosion trends. A multivariate regression blended with ARIMA smoothing projects each driver forward to 2030, and gaps in bottom-up evidence are filled through calibrated indexation to nearest proxy segments.

Data Validation & Update Cycle

Outputs pass a three-layer review: analyst peer checks, model variance flags against independent fleet or trade signals, and final manager sign-off. Reports refresh every twelve months, with interim reruns triggered by material events like major mandate announcements.

Why Mordor's Aircraft Synthetic Vision Systems Baseline Commands Reliability

Published estimates vary because firms pick different product mixes, pricing ladders, and update cadences. We acknowledge those differences up front so readers see exactly where numbers diverge.

Key gap drivers include whether portable tablet apps are counted, how retrofit timing is treated, currency conversion years, and if military research budgets are rolled into revenue. Our model, refreshed annually and scoped strictly to line fit and certified retrofit ship sets, therefore lands between conservative fleet-only views and broader avionics valuations.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 569.4 mn (2025) | Mordor Intelligence | - |

| USD 496.3 mn (2024) | Global Consultancy A | Excludes UAV platforms and uses 2024 FX rates |

| USD 461.8 mn (2025) | Trade Journal B | Counts only primary flight displays, omits database licensing revenue |

| USD 2.14 bn (2024) | Industry Association C | Bundles enhanced vision hardware and broader avionics suites |

Taken together, the comparison shows that Mordor's disciplined scope selection, dual-track modelling, and annual refresh produce a balanced, decision-ready baseline that clients can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the present size of the Aircraft Synthetic Vision Systems market?

The market was valued at USD 596.62 million in 2026 and is projected to reach USD 753.89 million by 2031, reflecting a 4.78% CAGR.

Which segment holds the largest Aircraft Synthetic Vision Systems market share?

Primary flight displays led with 45.02% share in 2025, underscoring their centrality in cockpit upgrades.

Why is Asia-Pacific the fastest-growing region?

Infrastructure modernisation and fleet expansion across China, India and Southeast Asia drive an 8.33% regional CAGR, with regulatory support for low-visibility operations accelerating adoption.

How do regulations influence market growth?

FAA NextGen and EASA SESAR mandates require enhanced situational awareness, creating non-discretionary demand for synthetic-vision retrofits and OEM installations.

What technological trend is reshaping competition?

AI-based terrain-rendering engines running on certified GPUs are shifting value creation toward software and data services rather than display hardware alone.

Page last updated on: