Commercial Aircraft Leasing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

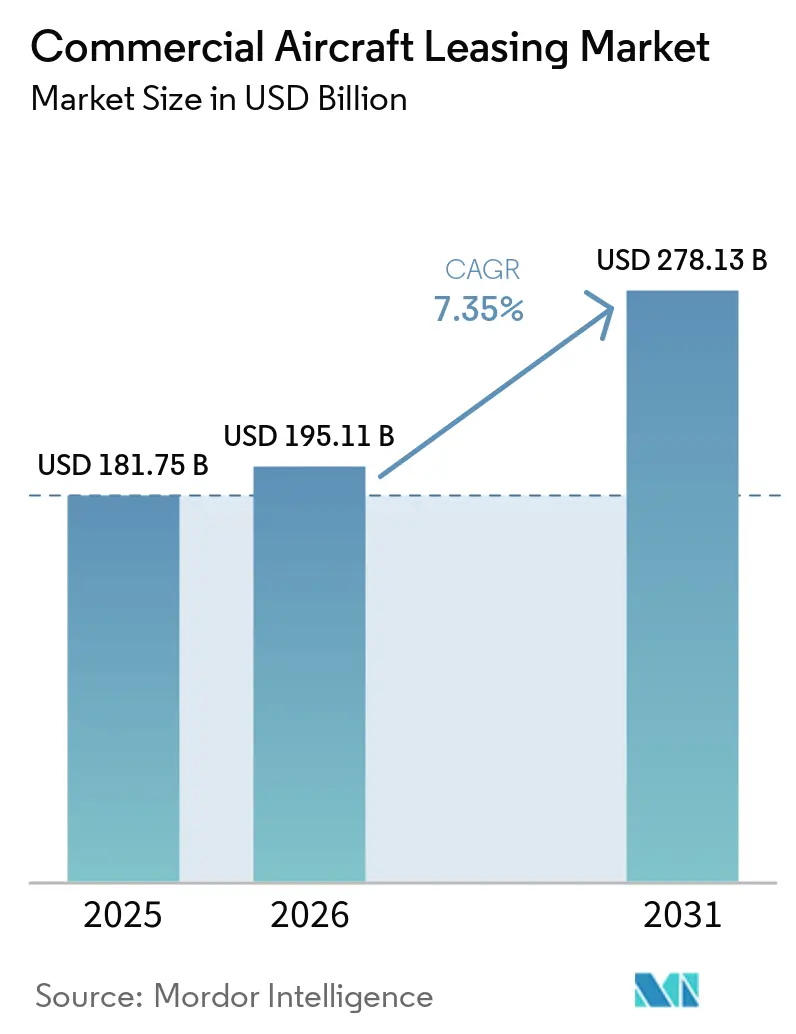

| Market Size (2026) | USD 195.11 Billion |

| Market Size (2031) | USD 278.13 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

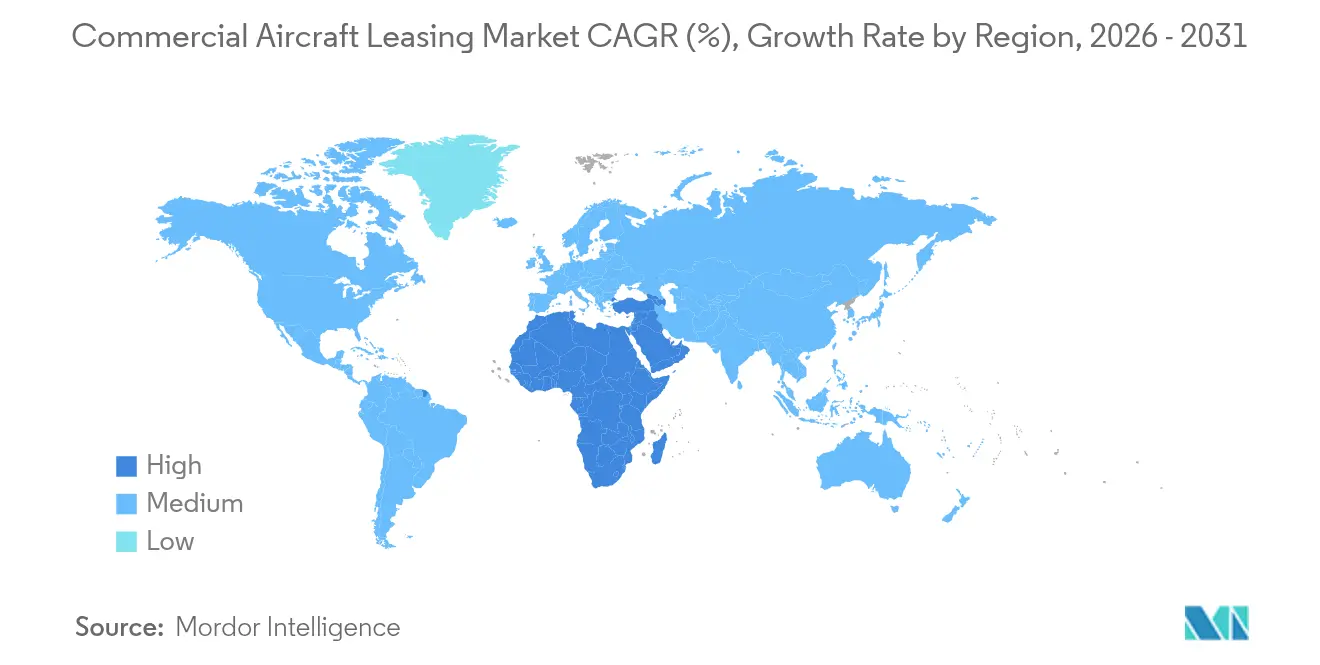

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Leasing Market Analysis by Mordor Intelligence

The commercial aircraft leasing market size in 2026 is estimated at USD 195.11 billion, up from 2025's USD 181.75 billion, with 2031 projections showing USD 278.13 billion, growing at a 7.35% CAGR over 2026-2031. Persistent production shortages at Airbus and Boeing, the rapid spread of low-cost carriers (LCCs), and a structural shift toward asset-light airline balance sheets continue to propel the commercial aircraft leasing market. Lessors benefit from extended average lease terms, firmer lease-rate factors, and stronger residual values as airlines accept longer commitments to secure scarce capacity. Institutional investors are deepening their exposure because leased aircraft generate predictable cash flows that remain resilient during economic cycles, while next-generation aircraft lower carbon intensity in line with airline decarbonization roadmaps. Rising demand for passenger-to-freighter (P2F) conversions and harmonized repossession frameworks under the Cape Town Convention further underpin the growth outlook.

Key Report Takeaways

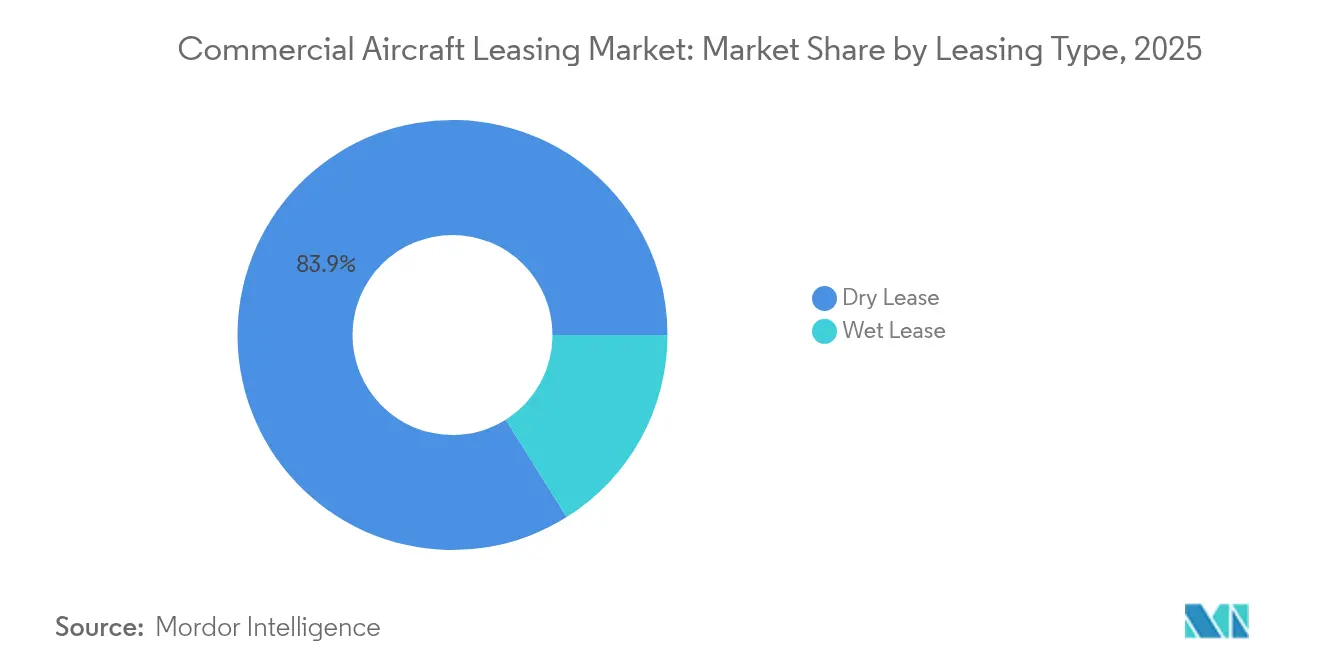

- By leasing type, dry leases held 83.92% of the commercial aircraft leasing market share in 2025, whereas wet-lease contracts are projected to expand at an 8.31% CAGR through 2031.

- By aircraft type, narrowbodies accounted for 61.22% of the commercial aircraft leasing market in 2025; freighter and P2F aircraft are forecast to grow at a 9.08% CAGR to 2031.

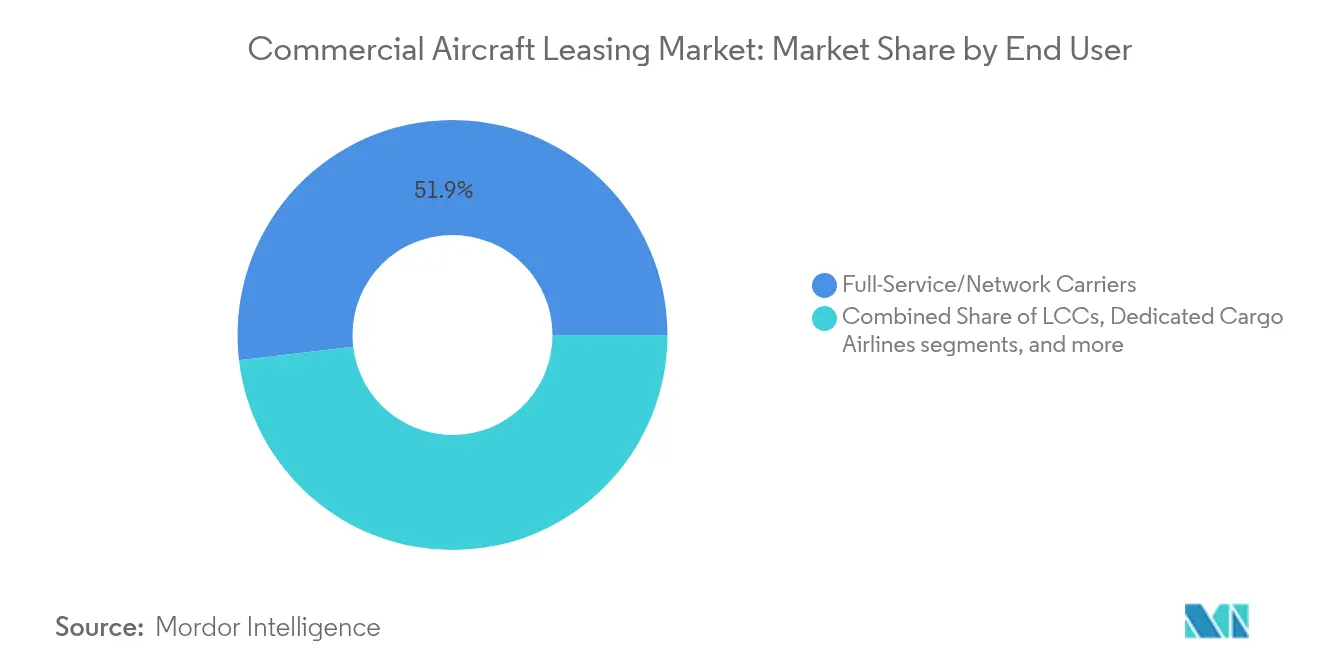

- By end user, full-service carriers led with 51.88% share in 2025, while the LCC segment is advancing at 8.41% CAGR.

- By lease duration, medium-term led with 45.32% share in 2025, while the short-term segment is advancing at 7.62% CAGR.

- By geography, Asia-Pacific commanded 35.12% revenue in 2025; the Middle East and Africa region is set to register the fastest 9.33% CAGR through 2031.

- AerCap, SMBC Aviation Capital, and Avolon collectively controlled about 30% of the global fleet in 2024, reflecting a moderately concentrated competitive arena.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid global adoption of the low-cost-carrier model boosting leased-fleet penetration | +1.8% | Global; strongest in Asia-Pacific and MEA | Medium term (2-4 years) |

| OEM production bottlenecks extending average lease terms and elevating lease-rate factors | +2.1% | Global; sharpest for narrowbody deliveries | Long term (≥ 4 years) |

| Strong demand for passenger-to-freighter conversions creating secondary leasing boom | +0.9% | Global; concentration in Asia-Pacific and North America | Short term (≤ 2 years) |

| Airline decarbonization roadmaps triggering accelerated replacement cycles | +0.7% | Led by Europe and North America | Long term (≥ 4 years) |

| Rising lease-rate factors attracting institutional investors | +1.2% | Global; with focus on developed capital markets | Medium term (2-4 years) |

| Harmonized legal protections reducing repossession risk and lowering cost of capital | +0.8% | Cape Town Convention signatory countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid low-cost-carrier expansion increases leasing penetration

Low-cost carriers rely on leasing to conserve cash and scale quickly, driving a structural preference that supports the commercial aircraft leasing market. IndiGo’s agreement with BOC Aviation for four A320neo jets and Southwest Airlines’ 2025 sale-and-leaseback with BBAM exemplify how carriers secure lift without large upfront capital outlays.[1]BOC Aviation, “Order for 70 A320neo Family Aircraft,” bocaviation.com Leasing also allows LCCs to recalibrate fleets in response to volatile demand, a key advantage during traffic shocks. Rising middle-class disposable incomes in India, Southeast Asia, and sub-Saharan Africa underpin a route-expansion cycle that will keep the LCC segment growing at an 8.78% CAGR through 2030, reinforcing demand for narrowbody lift and supporting lessor bargaining power.

OEM production bottlenecks elevate lessor pricing power

Quality-control issues and supply-chain disruptions have trimmed Airbus and Boeing output, leaving airlines with delivery shortfalls and pushing lease-rate factors higher. SMBC Aviation Capital reports 7-12% lease-rate growth for new wide-bodies since late 2023, while average lease terms have climbed to 12 years, locking in cash-flow visibility for lessors. Secondary-market valuations are firm because carriers choose to keep older aircraft longer rather than risk capacity gaps. The bottlenecks are unlikely to ease before 2028, underscoring a multi-year tailwind for lease pricing.

P2F conversions unlock a secondary growth engine

E-commerce parcel volumes call for additional freighters, yet new-build slots remain scarce. Converting an ageing B737-800 into a freighter costs roughly USD 25 million—far below the USD 150-200 million price for a new wide-body freighter, creating a compelling arbitrage for lessors. AerCap’s lease of four B737-800BCFs to JD Airlines highlights the strategy, while Boeing projects conversions will supply more than 50% of the world freighter fleet by 2043.[2]Boeing, “Commercial Market Outlook 2024,” boeing.com P2F activity extends asset life by up to 20 years and diversifies lessor revenue streams across passenger and cargo cycles.

Decarbonization roadmaps accelerate fleet renewal

IATA’s Net-Zero 2050 pathway and rising sustainable aviation-fuel mandates are pushing airlines toward new-technology aircraft with 15-25% lower fuel burn. AerCap has invested USD 50 billion in these models since 2014, and its fleet is now 70% new-technology, cutting per-seat emissions materially.[3]AerCap, “ESG Report 2024,” aercap.com Operating leases give carriers flexibility to rotate into progressively greener models without burdening balance sheets with stranded assets. Sustainability-linked financing further rewards airlines that meet emissions targets with lower borrowing costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating OEM list prices and interest-rate volatility compressing lessor yield margins | -1.40% | Global; pronounced in USD-denominated transactions | Short term (≤ 2 years) |

| Complex geopolitical sanctions heightening repossession and redeployment risk | -0.80% | Global; concentrated in Russia/CIS exposure | Medium term (2-4 years) |

| ESG-driven lending policies restricting financing for older, less-efficient aircraft | -0.60% | Primarily Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technology uncertainty around next-generation propulsion depressing residual-value outlooks | -0.50% | Global; higher impact on current-generation narrowbodies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interest-rate volatility erodes yield spreads

Federal Reserve tightening lifted lessor funding costs during 2024, and OEM price hikes outpaced lease-rate growth in certain segments. Air Lease Corporation’s net income slipped to USD 372 million in 2024 even as revenues climbed, illustrating the squeeze. Debt-heavy lessors face the sharpest margin pressure, though constrained aircraft supply partly offsets the impact.

Geopolitical sanctions complicate asset recovery

Over 400 Western-owned aircraft remain stranded in Russia, with outstanding claims topping USD 8 billion. Although London’s High Court sided with lessors in 2025, litigation timelines of two-plus years reveal enforcement difficulties. Lessors now model heightened exposure caps for high-risk jurisdictions and rely on Cape Town protections to shorten repossession timelines where possible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Leasing Type: Dry-lease dominance amid wet-lease upswing

Dry leases held 83.92% of the commercial aircraft leasing market in 2025 as airlines prioritized cockpit-and-cabin standardization, training synergies, and cost control. This dominance translates into USD 152.5 million of the commercial aircraft leasing market size, giving lessors predictable long-run cash flows. The wet-lease niche—comprising ACMI agreements—expands at 8.31% CAGR because carriers need seasonal capacity and contingency lift during maintenance peaks or pilot shortages. Norse Atlantic’s decision to return three B787-8s while retaining B787-9s shows how airlines recalibrate portfolios for optimum gauge and trip economics. Wet-lease providers are increasingly important during peak summer schedules in Europe and West Asia, enabling network carriers to plug capacity gaps without fresh capital outlays.

Over the forecast period, wet-lease operators will keep leveraging ACMI flexibility. Still, dry leasing will remain the bedrock of the commercial aircraft leasing market because it meets airline cost-efficiency targets and lessor asset-management preferences.

By Aircraft Type: Narrowbody leadership with cargo momentum

Narrowbodies represented 61.22% of total leased units in 2025, equivalent to USD 111.3 million of the commercial aircraft leasing market size, reflecting their unmatched economics on high-frequency routes. A321neo and B737 MAX deliveries drive fleet renewal, while strong residual liquidity makes them the least risky assets for lessors’ balance sheets. However, freighters and P2F aircraft are the fastest climbers at 9.08% CAGR as express-parcel operators rush to capture cross-border e-commerce flows. AviLease joined the segment with A350F orders during 2025, signalling that wide-body freighters will anchor growth for Middle-East hubs. Wide-body passenger aircraft face muted near-term output, yet premium long-haul demand supports lease-rate endurance. Regional jets serve point-to-point connectivity in Brazil, India, and the US, but their share remains below 5% of the commercial aircraft leasing market.

Boeing projects 2,800 additional freighters by 2043, with more than half coming from P2F conversions, executing a virtuous cycle of asset-life extension and residual-value uplift. Lessors that can secure early conversion slots will lock in attractive yields and diversify income away from cyclical passenger demand.

By End User: Network-carrier scale meets LCC velocity

Full-service carriers (FSCs) accounted for 51.88% of 2025 demand, translating into USD 94.3 million of the commercial aircraft leasing market size. FSCs continue to rely on operating leasing for fleet harmonization and balance-sheet relief, even while maintaining premium cabins and complex hub-and-spoke operations. The LCC cohort, however, is racing ahead at an 8.41% CAGR, spearheaded by massive orders such as Cebu Pacific’s 152-unit A321neo commitment. The commercial aircraft leasing industry thereby aligns its portfolio growth with the ascendancy of LCCs in Asia, South America, and select African corridors. Dedicated cargo airlines and ACMI specialists fill logistic white spaces left by integrators, especially for cross-border e-commerce flows that require bespoke hub strategies.

Network carriers also experiment with hybrid models, creating “value” subsidiaries that use dense single-class cabins. Leasing allows them to ring-fence aircraft in separate entities, shielding premium brands from low-fare dilution while tapping fast-growing middle-class traffic.

By Lease Duration: Medium-term preference, short-term agility

Medium-term contracts captured 45.32% of 2025 transactions because they balance cost advantages against the need to incorporate new-technology aircraft in under a decade. Short-term contracts, while only 18.27% of volume, are the fastest riser at 7.62% CAGR as airlines value agility during demand swing-outs. Long-term leases above twelve years historically delivered the lowest dollar-per-month rates; however, extended OEM delays now make such tenors more acceptable. United Airlines’ 12-year A321neo leases underline how scarcity reshapes tenor tolerance.

During the forecast window, high interest-rate volatility will keep airlines favouring medium-term structures to refinance when capital costs fall. Lessors, for their part, like the balanced risk-return profile: medium-term contracts capture a strong portion of an aircraft’s cash-generating life but allow remarketing before heavy-maintenance milestones.

Geography Analysis

Asia-Pacific held 35.12% of global revenue during 2025 as rapid traffic expansion, averaging 4.8% annually, and an order pipeline of 19,500 aircraft through 2043 reinforced fleet-growth needs. Leasing penetration already approaches 60% of the active fleet, well above the global average, demonstrating the centrality of the commercial aircraft leasing market to regional airline strategies. China’s CDB Aviation order for 80 A320neo jets and India’s Aircraft Objects Bill 2025, which aligns domestic repossession law with Cape Town provisions, strengthen the region’s attractiveness for foreign capital.

The Middle East and Africa region is the fastest-growing, posting a 9.33% CAGR through 2031. Saudi-owned AviLease placed its first Boeing order for 30 B737-8 jets and signed for A350F freighters in 2025, supporting the Kingdom’s Vision 2030 strategy. Africa’s fleet is set to double, and its freighter count will triple, opening a major frontier for lessors specializing in narrowbody cargo conversions.

North America and Europe remain mature yet innovative. Lessors based in Dublin, London, New York, and Los Angeles continue to anchor global funding. Sustainability-linked loans and green bonds originated in these regions and drive environmental transparency throughout the commercial aircraft leasing market. Consolidation, such as Dubai Aerospace Enterprise’s acquisition of Nordic Aviation Capital, indicates that economies of scale and funding access remain decisive.

Competitive Landscape

The ten largest lessors control most leased assets globally, implying moderate market concentration and leaving scope for nimble mid-tier entrants. Recent deals—SMBC Aviation Capital’s USD 6.7 billion purchase of Goshawk Aviation and Avolon’s acquisition of Castlelake—underline the quest for scale, portfolio diversification, and cheaper funding. Operating lessor orderbooks exceeded 2,000 aircraft by early 2025, but most frames are already placed with airlines, limiting speculative overhang.

Technology is emerging as a key differentiator: predictive-maintenance analytics, blockchain-based parts tracing, and digital customer portals lift fleet uptime and cut operating costs. Lessors also embed environmental metrics in lease covenants, offering rate discounts for fleets meeting emissions benchmarks. White-space opportunities exist in engine leasing, where high technical barriers grant robust margins, and in emerging markets with local financing incentives.

Institutional capital—sovereign wealth funds, pension funds, and private equity—maintains a strong appetite for aviation assets because their cash flows are dollar-denominated and partially inflation-linked. BOC Aviation’s 70-unit A320neo order, expanding its backlog to 200 aircraft, exemplifies major lessors' long-run confidence in the commercial aircraft leasing market.

Commercial Aircraft Leasing Industry Leaders

AerCap Holdings N.V.

SMBC Aviation Capital

Avolon Aerospace Leasing Limited

Air Lease Corporation

BOC Aviation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SpiceJet inked a damp-lease agreement for three Airbus A320 aircraft, set to bolster its fleet by July 2026.

- March 2025: BOC Aviation ordered 70 A320neo family aircraft for delivery through 2032, lifting its orderbook around 200 units.

- February 2025: Air Lease Corporation ordered five A321neo aircraft with Qanot Sharq Airlines, scheduled for delivery in 2026-27.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the commercial aircraft leasing market as the aggregate annual value of operating and finance leases on fixed-wing passenger and freighter aircraft placed with airlines and charter operators worldwide. Transactions involving narrow-body, wide-body, regional jets, and passenger-to-freighter conversions are counted when the lessor retains legal title and the lessee pays recurring rentals. Values are expressed in USD at 2024 constant exchange rates, covering both new lease originations and extensions executed during the year.

Scope Exclusion: Business-jet, military, helicopter, and sale-and-lease-back arrangements on engines or components fall outside this boundary.

Segmentation Overview

- By Leasing Type

- Wet Lease

- Dry Lease

- By Aircraft Type

- Narrowbody

- Widebody

- Regional Jets

- Freighter/P2F Converted Aircraft

- By End-User

- Full-Service/Network Carriers

- Low-Cost Carriers (LCCs)

- Dedicated Cargo Airlines

- Charter and ACMI Operators

- By Lease Duration

- Short-Term

- Medium-Term

- Long-Term

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Ireland

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East and Africa

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and surveys with airline fleet-planning heads, independent appraisers, senior executives at global lessors, and MRO contract managers across North America, Europe, Asia-Pacific, and the Middle East supply real-time lease-rate factors, utilization patterns, and renewal intentions. These conversations validate secondary ratios, plug data gaps on private placements, and temper early model outputs with on-ground sentiment.

Desk Research

Mordor analysts first map the global active fleet using tier-1 public sources such as ICAO traffic statistics, IATA World Air Transport, Bureau of Transportation Statistics, Eurostat aviation tables, and UN Comtrade aircraft trade codes, supported by company filings and OAG schedule data. Supplemental insights on lessor portfolios are drawn from paid databases like D&B Hoovers, Dow Jones Factiva, Aviation Week, and Marklines for finance and delivery timelines. Government gazettes, EASA safety directives, and patent filings on passenger-to-freighter conversions help clarify regulatory and technical shifts. This list is illustrative; many additional sources are consulted for cross-checks, clarifications, and historical depth.

Market-Sizing & Forecasting

A top-down rebuild starts from the active and on-order fleet by aircraft class, overlaid with average lease penetration and weighted lease-rate factors to derive 2024 rental value pools, which are then sense-checked with selective bottom-up samples of disclosed lease contracts. Key variables like revenue passenger kilometers, OEM delivery backlog, weighted average fleet age, residual-value index, and 12-month SOFR trend drive a multivariate regression that projects lease values through 2030. Scenario bands consider divergent interest-rate paths; gaps in bottom-up data are bridged using normalized utilization multipliers sourced from primary interviews.

Data Validation & Update Cycle

Outputs undergo anomaly screens, variance tests against independent capacity and traffic indicators, and two-step peer review before sign-off. Reports refresh annually; interim updates trigger if OEM production forecasts, fuel prices, or major airline bankruptcies materially shift the baseline, ensuring clients receive a current viewpoint.

Why Mordor's Commercial Aircraft Leasing Baseline Commands Reliability

Published estimates often differ because firms choose unique scopes, cost assumptions, currency bases, and refresh cadences.

Key gap drivers include whether freighter conversions are counted, how lease extensions are valued, the treatment of damp leases, and the rigor of cross-checking lessor disclosures against airline financials. Mordor's disciplined use of fleet-level penetration ratios, multi-source lease-rate benchmarks, and annual refresh cadence delivers a balanced, repeatable figure that decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 181.75 B (2025) | Mordor Intelligence | - |

| USD 183.23 B (2024) | Global Consultancy A | Converts OEM order book to revenue without adjusting for lease renewals, limited geographic splits |

| USD 210.40 B (2025) | Research Firm B | Uses headline transaction values and excludes finance-lease depreciation, single-scenario forecast |

| USD 52.95 B (2022) | Regional Consultancy C | Counts only operating leases on active passenger jets and omits freighter and extension contracts |

Taken together, the comparison shows that scope breadth, depreciation logic, and update rhythm explain most variance. Our approach, anchored to transparent fleet metrics and validated by primary voices, offers the most dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the commercial aircraft leasing market?

The commercial aircraft leasing market reached USD 195.11 billion in 2026 and is projected to grow to USD 278.13 billion by 2031, reflecting a 7.35% CAGR.

Which region leads the commercial aircraft leasing market?

Asia-Pacific commands the largest share at 35.12% thanks to rapid traffic growth, high leasing penetration and large forward orderbooks.

Why are passenger-to-freighter conversions important for lessors?

P2F conversions cost about USD 25 million versus up to USD 200 million for new freighters, extend aircraft life by up to 20 years and meet booming e-commerce cargo demand, creating attractive returns for lessors.

How do supply-chain constraints affect lease rates?

Production delays at Airbus and Boeing limit new aircraft availability, pushing lease-rate factors up by 7-12% for certain models, and extending average lease terms to around 12 years.

What role does sustainability play in aircraft leasing?

Airlines rely on operating leases to upgrade into fuel-efficient models that help meet IATA’s Net-Zero 2050 goals, and sustainability-linked loans now offer interest-rate discounts tied to emissions reductions.

Is the commercial aircraft leasing market highly concentrated?

No, the market is moderately concentrated; the top ten lessors hold majority of assets, leaving room for mid-size specialists to gain share through regional focus or niche strategies.

Page last updated on: