Hybrid Aircraft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

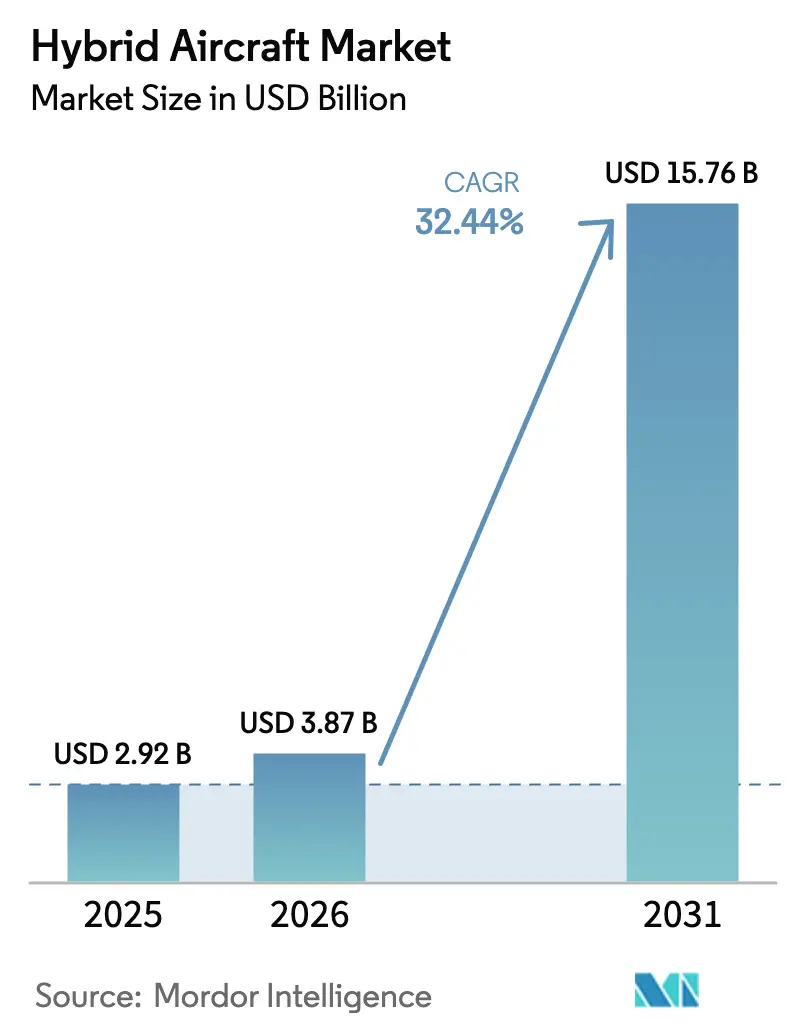

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 15.76 Billion |

| Growth Rate (2026 - 2031) | 32.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Aircraft Market Analysis by Mordor Intelligence

The hybrid aircraft market size was valued at USD 2.92 billion in 2025 and estimated to grow from USD 3.87 billion in 2026 to reach USD 15.76 billion by 2031, at a CAGR of 32.44% during the forecast period (2026-2031). Commercial viability accelerated because the European Union’s Taxonomy Regulation began steering capital toward zero-carbon aviation projects in 2024, while breakthroughs such as CATL’s 500 Wh/kg battery doubled the energy density available to designers. Airlines also sought alternatives because the International Civil Aviation Organization advanced a global long-term emissions goal and published harmonized standards that simplify multi-country certification. Investment followed: venture, strategic, and ESG-linked debt reduced financing costs, enabling start-ups and incumbents to accelerate prototypes into flight-test programs. North America led adoption, yet Asia-Pacific generated the fastest demand as China’s low-altitude economy moved into large-scale infrastructure build-out.

Key Report Takeaways

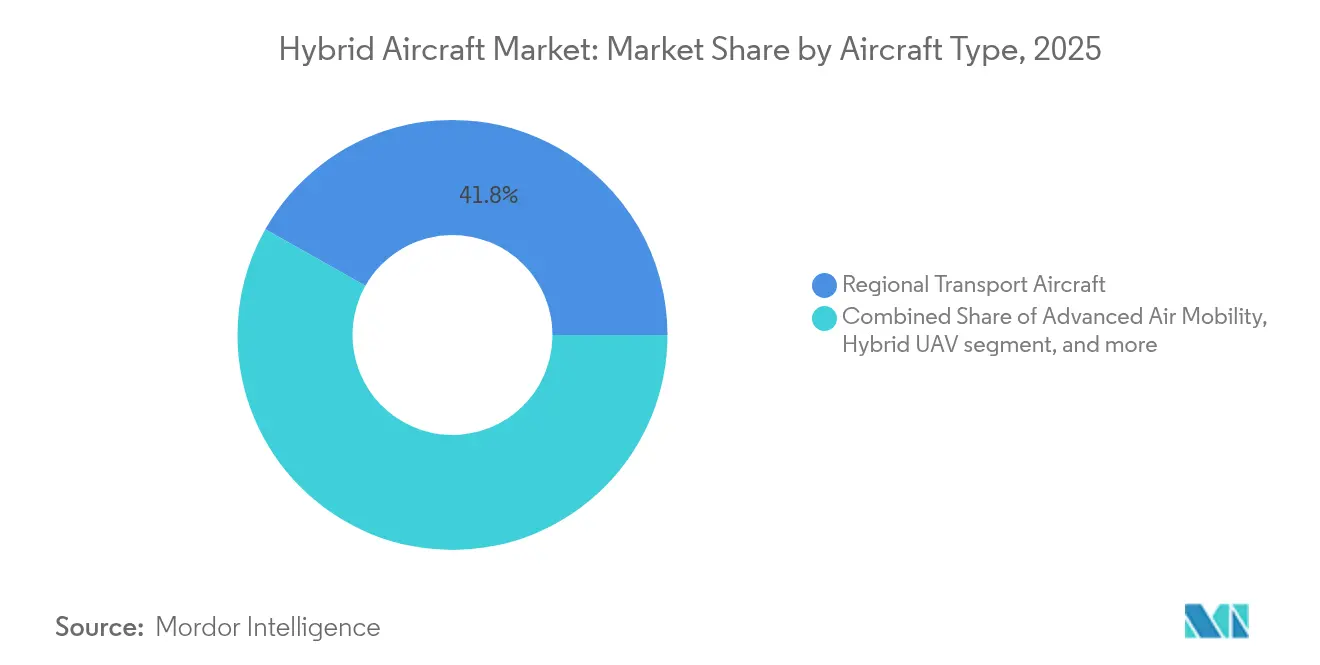

- By aircraft type, regional transport aircraft led 41.82% of the hybrid aircraft market share in 2025, while advanced air mobility (eVTOL/ Air Taxi) captured the fastest 39.58% CAGR to 2031.

- By mode of operation, piloted platforms dominated with a 74.68% share in 2025; autonomous systems posted the top 40.92% growth pace.

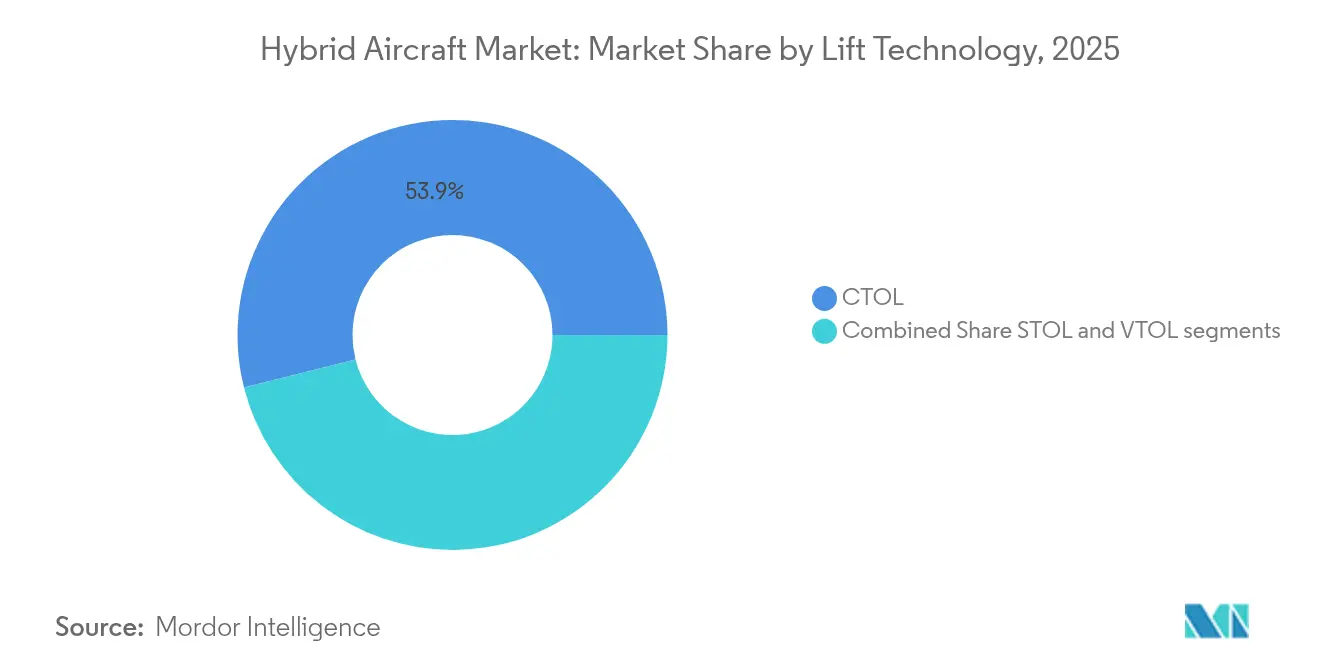

- By lift technology, CTOL held 53.92% share of the hybrid electric aircraft market in 2025, but VTOL is projected to expand at 39.21% CAGR.

- By propulsion architecture, parallel hybrids commanded 50.76% share of the hybrid electric aircraft market size in 2025; series hybrids are forecasted to grow 37.45% through 2031.

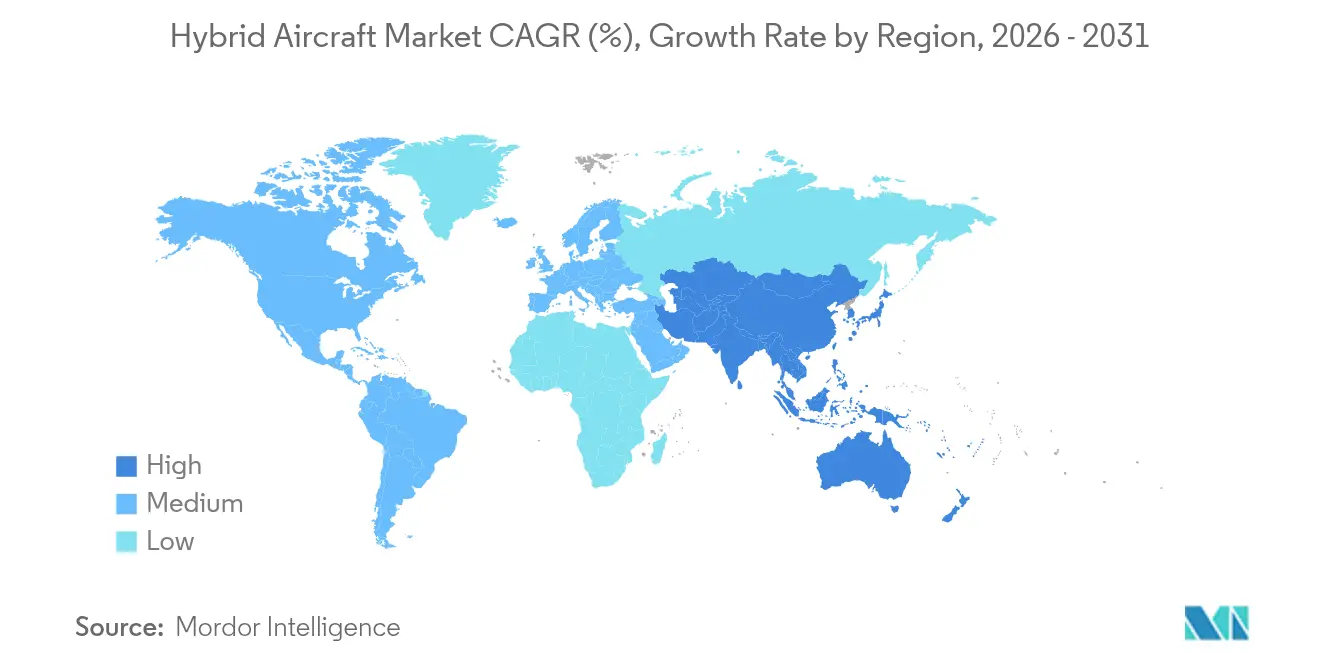

- By geography, North America accounted for 40.12% of revenue share in 2025, whereas Asia-Pacific led growth at 35.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hybrid Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global emissions regulations | +8.2% | Global; EU and California leading | Medium term (2-4 years) |

| Rapid advances in battery and electric-drive density | +7.5% | US, China, Europe | Long term (≥ 4 years) |

| Surging regional and short-haul connectivity demand | +6.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Military demand for low-acoustic ISR platforms | +4.3% | US, NATO allies, Asia-Pacific | Medium term (2-4 years) |

| Secondary-airport STOL/VTOL slot opportunities | +3.8% | North America, Europe | Medium term (2-4 years) |

| ESG-linked finance lowering capital costs | +3.1% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Global Emissions Regulations

Carbon-reduction mandates fundamentally changed airline fleet plans. The EU Taxonomy Regulation, effective January 2024, specified that only aircraft demonstrating zero direct CO₂ emissions qualify for green financing, steering capital toward hybrid and electric programs. EASA proposed amendments covering electric propulsion in 2024, giving manufacturers a known pathway for type certification. At the multilateral level, ICAO’s Advanced Air Mobility Study Group harmonized safety requirements, smoothing cross-border deployment. Together, these actions reduced policy risk and shortened payback periods for fleet operators.

Rapid Advances in Battery and Electric-Drive Density

CATL revealed a condensed-battery chemistry that delivered 500 Wh/kg and promised 2,000–3,000 km range for 8-ton aircraft, effectively doubling the design envelope for regional routes. NASA’s sulfur-selenium solid-state project matched that energy density while removing flammable electrolytes, enhancing safety. GE Aerospace’s MW-class inverter advanced silicon-carbide power electronics and met NASA power-density targets, reducing onboard weight.[1]Source: GE Aerospace, “Electrical-Power Systems,” geaerospace.com magniX supplemented the supply with 300 Wh/kg aviation-grade batteries tested for 1,000 cycles. The convergence of chemistry, inverters, and motors enabled hybrid systems that exceed the economics of turboprops on sub-regional stages.

Surging Regional and Short-Haul Connectivity Demand

Airlines prioritized thinner routes between secondary airports to capture post-pandemic demand for direct city pairs. Electra secured USD 9 billion in letter-of-intent orders for its EL9, an ultra-short take-off hybrid, showing operators’ appetite for aircraft that fit neglected 1,000 km markets. JSX, meanwhile, agreed to acquire 300 hybrid airplanes to bridge underserved West Coast destinations. AURA Aero reported operating-cost models that cut expenses by 30–50% versus turboprops, validating the value proposition for regional carriers. Fleet managers are thus locked in hybrid deliveries to future-proof route economics.

Military Demand for Low-Acoustic ISR Platforms

Defense procurement catalyzed technology readiness. The US Air Force Research Laboratory awarded USD 99.2 million for GHOST, a hybrid UAV capable of quieter loiter and strike operations. DARPA followed with the XRQ-73 SHEPARD demonstrator, proof that distributed electric fans can meet long-endurance ISR profiles. Military test data accelerated component qualification and de-risked supply chains for civilian certification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification framework immaturity | -4.7% | Global; especially complex in emerging markets | Medium term (2-4 years) |

| Hybrid powertrain weight penalties | -3.2% | Global; severe in smaller aircraft | Long term (≥ 4 years) |

| Shortage of aerospace-grade HV wiring | -2.8% | Global supply chain constraint | Short term (≤ 2 years) |

| Insurance-premium uncertainty | -1.9% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Certification Framework Immaturity

The FAA issued special-class criteria for Joby in March 2024, yet broader hybrid categories still lacked harmonized rules, forcing manufacturers to pursue multiple paths.[2]Source: Federal Aviation Administration, “Special-Class Airworthiness Criteria for Joby,” federalregister.gov ASTM began drafting hybrid-engine standards, but gaps remained in thermal-runaway containment and high-voltage electromagnetic interference. EASA identified further research areas, delaying a fully prescriptive framework. In response, original-equipment manufacturers budgeted parallel certification programs that stretched timelines and capital.

Hybrid Power-Train Weight Penalties

Dual propulsion introduced structural weight that reduced payload. VoltAero’s Cassio testing showed integration challenges when combining batteries, thermal systems, and combustion engines. Concepts such as structural batteries promised relief but remained laboratory-scale. Until next-generation chemistries migrate from automotive to aviation, designers balanced range, seating, and economics in ways that dampened mass-market adoption outside the regional segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Regional Transport Remained the Commercial Beachhead

Regional transport platforms represented a 41.82% hybrid electric aircraft market share because their turboprop baselines simplified conversion and certification. Airlines prioritized them to satisfy sub-1,500 km requirements without infrastructure overhauls. Deutsche Aircraft started constructing the first D328eco test airframe in February 2025, advancing a 40-seat derivative that leverages existing runway networks. The program’s Leipzig final assembly line positioned Germany to support volume deliveries from 2026. In parallel, business-jet OEMs retrofitted electric boosters to reduce approach noise at urban airports, while light-aircraft developers marketed trainer models that cut fuel bills for flight schools.

The Advanced Air Mobility (eVTOL/Air Taxi) category clocked a 39.58% CAGR. Vertical Aerospace secured USD 90 million in fresh equity in January 2025, funding VX4 certification flights at Cotswold Airport. Cargo operators evaluated lift-plus-cruise configurations for middle-mile logistics, targeting autonomous entry before passenger service. Hybrid UAVs, meanwhile, gained traction in maritime patrol where endurance outweighed cabin volume.

By Mode of Operation: Piloted Dominance Faces Automated Momentum

Piloted platforms hold 74.68% of the hybrid electric aircraft market. CAE launched dedicated type-rating syllabi that blended high-voltage safety with multi-engine emergency drills. Etihad Aviation Training added eVTOL modules covering vertiport arrival procedures and battery-fire response. Operators valued crew oversight while unfamiliar technologies matured.

Autonomous platforms expanded 40.92% annually, albeit from a smaller base. Military ISR contracts demanded pilot-optional designs, demonstrating airworthiness for detect-and-avoid algorithms. ICAO’s March 2025 performance-based SARPs for remotely piloted aircraft removed a key regulatory bottleneck. Cargo carriers considered night-time utilization to increase asset productivity while mitigating public acceptance risks.

By Lift Technology: CTOL Maturity Meets VTOL Acceleration

CTOL units reflect 53.92% of the hybrid electric aircraft market size, because operators reused existing runway slots and maintenance infrastructure. Electra’s demonstrator completed ultra-short eSTOL hops, proving that turbo-electric assist could clear 200-m runways with 7 kg/seat block fuel burn. The approach enlarged the addressable airport network without requiring new vertiports.

VTOL units chased a 39.21% CAGR as municipalities commissioned test hubs. Rotterdam Port opened Europe’s first commercial vertiport a year before schedule, validating passenger-handling procedures and energy-resupply logistics. Beta Technologies doubled its charging-station network across the US eastern seaboard, de-risking cross-country ferry flights during certification. The network effect prompted municipalities to earmark funding for additional sites.

By Propulsion Architecture: Parallel Today, Series Tomorrow

Parallel hybrids accounted for 50.76% of the 2025 hybrid electric aircraft market size. GE Aerospace’s partnership with NASA embedded electric motor-generators into a commercial turbofan core, offering airlines redundancy without wholesale architectural change. Airlines favored the model because existing maintenance providers could adapt procedures quickly.

Series hybrids, however, grew 37.45% annually as smart-grid control reduced conversion losses. Safran Electrical & Power released the ENGINeUS family that scaled from 100 kW to 1 MW, complementing GENeUS generators suited for distributed sources. Turbo-electric concepts explored boundary layer ingestion to trim cruise drag. Investors perceived a pathway to single-aisle class aircraft once battery gravimetric density crosses 600 Wh/kg, projected near 2028.

Geography Analysis

North America holds the market share of 40.12% of revenue, because NASA’s Electrified Powertrain Flight Demonstration funded full-scale propulsion ground tests and flight articles. American Airlines’ conditional purchase of 100 hydrogen-electric engines signaled mainline-carrier endorsement. United Airlines added momentum by ordering 200 blended-wing hybrids from JetZero, underscoring network ambitions. Parallel state support attracted supply-chain expansion: JetZero chose Greensboro, North Carolina, for a 14,500-job factory in June 2025.

Asia-Pacific booked the fastest 35.72% CAGR, driven by China’s CNY 2 trillion (USD 279.02 billion) low-altitude economy plan. The Civil Aviation Administration of China prioritized eVTOL routes linking coastal megacities, and EHang secured the world’s first type certificate for an autonomous passenger aircraft in 2024. CATL pledged serial production of an 8-ton electric aircraft by 2028, leveraging domestic battery scale. Australia’s Victoria allocated grants to Dovetail Electric Aviation, expanding regional-aircraft retrofits for the Pacific market.

Europe retained a strategic role through public finance instruments. The European Investment Council injected EUR 17.5 million (USD 20.47 million) into AURA Aero, while the EUR 40 million (USD 46.80 million) HECATE program focused on electric distribution system research. Airbus, Daher, and Safran completed the EcoPulse flight campaign in December 2024, logging 100 flight hours that validated six-motor distributed propulsion. VoltAero opened a final-assembly hall for the Cassio family in Nouvelle-Aquitaine a month earlier, signaling Europe’s readiness to shift from prototypes to serial output.

Competitive Landscape

Competition remained fragmented, leaving ample space for differentiation. Incumbents Airbus, Safran, and GE Aerospace leveraged certification know-how, yet internal processes slowed rapid iteration. Start-ups Ampaire, Heart Aerospace, and Vertical Aerospace secured venture rounds that funded unconventional designs and accelerated sprints. Patent filings by RTX, Rolls-Royce, and GE tripled between 2019 and 2024, highlighting a race to protect electric-motor cooling, hydrogen fuel-cell integration, and power-management software.

Strategic alliances addressed supply-chain gaps. GKN Aerospace deepened its partnership with Archer to fabricate key Midnight airframe components, combining composites expertise with start-up agility. Honeywell and Vertical Aerospace expanded their avionics agreement to cover flight-control compute and actuation, a USD 1 billion pipeline over ten years. White-space opportunities arose in cargo feeder lines, disaster-relief airlift, and offshore wind-farm maintenance, where hybrid noise and cost advantages were decisive.

Supply-chain maturity still lagged, particularly in aerospace-grade high-voltage cabling and silicon-carbide semiconductor production. Tier-one suppliers accelerated investments to localize component factories near final assembly lines, responding to geopolitical concerns and export-control regimes. The next competitive phase may see consolidation as larger OEMs acquire nimble entrants once certification milestones reduce technical risk.

Hybrid Aircraft Industry Leaders

RTX Corporation

General Electric Company

Airbus SE

Safran SA

Rolls-Royce plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vertical Aerospace and Honeywell expanded their VX4 partnership worth USD 1 billion.

- January 2025: Vertical Aerospace raised USD 84 million in new capital for VX4 development.

- November 2024: Electra introduced the EL9, a hybrid-electric aircraft for ultra-short takeoffs and landings. The nine-passenger aircraft combines hybrid-electric propulsion with blown lift technology, enabling operations from spaces as small as a soccer field. The EL9 is an alternative to helicopters and eVTOLs while providing the safety features of fixed-wing aircraft. Building on flight tests with its EL2 Goldfinch prototype, Electra is developing the EL9 for passenger and cargo transport in urban and regional areas. The aircraft can operate from various surfaces, including grass fields and parking lots, while featuring low emissions, reduced noise levels, and in-flight battery recharging capabilities. This advancement enables the potential establishment of numerous new air service locations, enhancing connectivity in the aviation sector.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hybrid aircraft market as all new fixed-wing or rotorcraft platforms that employ a combination of onboard fossil-fuel power and electric drive to propel the airframe through any flight phase. Both parallel and series power-split architectures, whether CTOL or VTOL, are included because they presently anchor most near-term certification programs.

Scope exclusion: Fully battery-electric, hydrogen-electric, and conventional turbofan aircraft without an integrated electric drivetrain fall outside this analysis.

Segmentation Overview

- By Aircraft Type

- Regional Transport Aircraft

- Business Jets and Light Aircraft

- Advanced Air Mobility (eVTOL/Air Taxi)

- Hybrid UAV

- By Mode of Operation

- Piloted

- Autonomous

- By Lift Technology

- Conventional Take-off and Landing (CTOL)

- Short Take-off and Landing (STOL)

- Vertical Take-off and Landing (VTOL)

- By Propulsion Architecture

- Series Hybrid

- Parallel Hybrid

- Turbo-Electric

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed aircraft OEM engineers, propulsion system suppliers, regional airline fleet planners, and civil-aviation regulators across North America, Europe, and Asia. These exchanges validated realistic battery energy densities, expected hybrid penetration rates, and certification milestones, filling gaps left by desk sources.

Desk Research

We began by pulling fleet statistics, prototype certification filings, and technology road maps from public sources such as FAA aircraft registry feeds, EASA environmental rule makings, ICAO aircraft emissions databank, and NASA's ongoing Electrified Propulsion Flight Demonstrator notes. Trade association white papers from AIAA and GAMA, patent analytics through Questel, plus listed company 10-Ks and investor decks provided insight on planned entry into service timelines and adoption hurdles. Select paid feeds, notably Aviation Week for program schedules and D&B Hoovers for company revenues, sharpened baseline inputs. This list is illustrative; many other open and premium references were tapped during data gathering.

Market-Sizing & Forecasting

One blended top-down production plus trade reconstruction established the total addressable fleet, which we then cross-checked with selective bottom-up supplier roll-ups and sampled average selling price × volume calculations. Key variables like battery specific energy progression, hybrid powertrain weight to thrust ratios, regional RPK growth, near-term fleet replacement cycles, and certification issuance cadence feed a multivariate regression model that projects value through 2030. Where supplier data proved patchy, weighted channel checks and ASP proxies bridged the shortfall before final triangulation.

Data Validation & Update Cycle

Outputs undergo anomaly scans, senior analyst peer review, and variance tests against independent fuel burn benchmarks. Reports refresh annually, while any major technology or regulatory shock triggers an interim model revision so clients receive the latest view.

Why Mordor's Hybrid Aircraft Baseline Commands Reliability

Published estimates differ because each firm chooses its own scope, base year, and battery cost outlook. Some count experimental prototypes, others fold in electric or hydrogen concepts; a few apply straight-line ASP escalations without verifying weight penalties.

Key gap drivers include differing inclusion of retrofit conversions, variance in assumed energy density learning curves, and contrasting currency conversion dates.

Mordor's disciplined refresh cadence and strict scope filters limit such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.92 B (2025) | Mordor Intelligence | - |

| USD 1.20 B (2023) | Global Consultancy A | counts prototypes only, aggressive CAGR extrapolation from a smaller base |

| USD 1.90 B (2025) | Industry Association B | excludes VTOL segment, uses list prices without volume discounts |

| USD 1.70 B (2025) | Regional Consultancy C | mixes hybrid and fully electric aircraft, older currency rates |

Taken together, the comparison shows how our tighter definition, current year currency conversion, and dual track sizing cross checks yield a balanced, transparent baseline that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the hybrid aircraft market in 2026, and what revenue level is it projected to reach by 2031?

The market generated USD 3.87 billion in 2026 and is projected to climb to USD 15.76 billion by 2031.

What compound annual growth rate supports the market’s climb from 2026 to 2031?

The market growth is forecasted at a 32.44% CAGR for the period, reflecting rapid commercial adoption and technology maturation.

Which aircraft segment dominates hybrid adoption today?

Regional transport aircraft lead with 41.82% market share because they can retrofit proven turboprop designs quickly.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest 35.72% CAGR, driven by China’s low-altitude economy investments and supportive certification frameworks.

What is the biggest technological barrier to widespread hybrid adoption?

Weight penalties from dual propulsion architectures limit payload and range until higher-density batteries or structural-energy solutions mature.

Are autonomous hybrid aircraft close to commercial service?

Autonomous hybrids will likely enter cargo operations first; ICAO adopted performance-based standards in 2025, yet passenger service awaits additional public-acceptance milestones.

Page last updated on: