Aircraft Fairings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

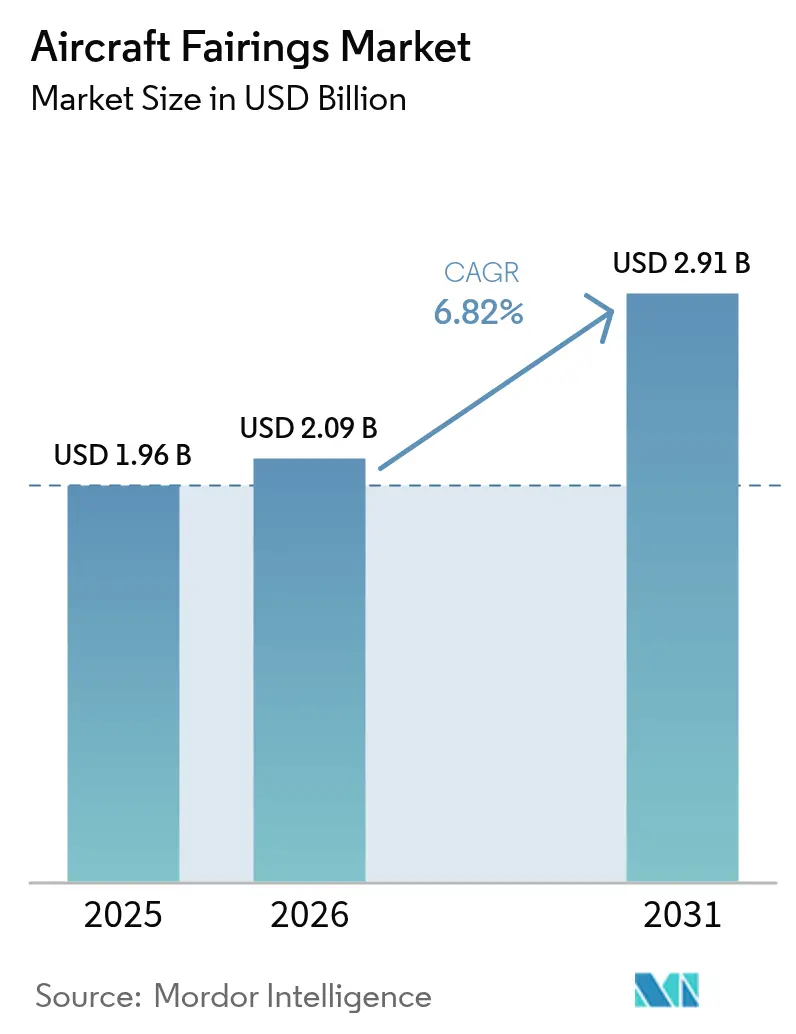

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Fairings Market Analysis by Mordor Intelligence

The aircraft fairings market size was valued at USD 1.96 billion in 2025 and estimated to grow from USD 2.09 billion in 2026 to reach USD 2.91 billion by 2031, at a CAGR of 6.82% during the forecast period (2026-2031). Robust production backlogs exceeding 15,000 commercial jets, rising fuel-efficiency mandates, and an accelerated push to replace aging fleets provide long-term demand visibility. Composite innovation is central to this growth pattern: carbon-fiber-reinforced polymer (CFRP) already accounts for 70% of fairing materials in service, a shift that cuts structural weight and improves corrosion resistance. Rising dependence on narrow-body programs, which contributed 48% of volumes in 2024, favors suppliers that can scale production while controlling costs. Meanwhile, the surge of UAV and eVTOL concepts—each prioritizing rapid prototyping and small-batch runs—creates premium niches that command higher margins per unit. As a result, the aircraft fairings market keeps bifurcating into high-volume commercial programs and fast-moving advanced-air-mobility demand pools, compelling suppliers to hedge capacity across both segments.

Key Report Takeaways

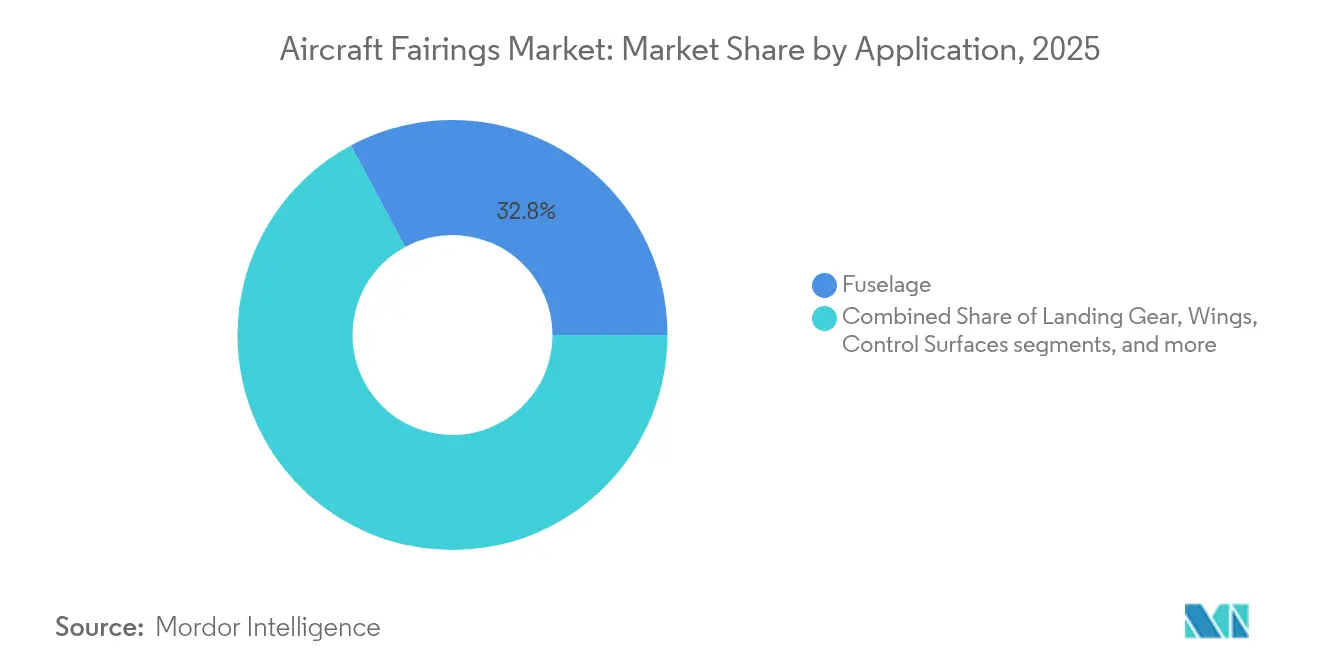

- By application, fuselage fairings led with 32.84% of the aircraft fairings market share in 2025; landing gear fairings are projected to post the highest 6.94% CAGR to 2031.

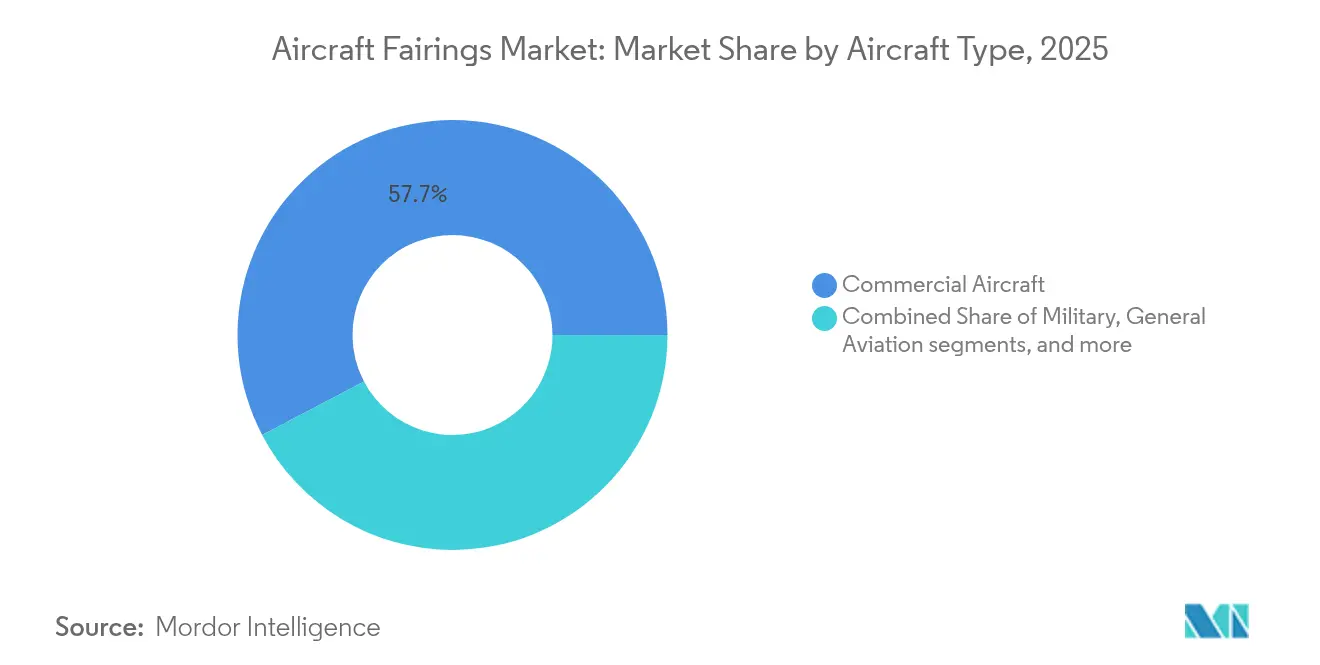

- By aircraft type, commercial aircraft accounted for 57.69% of the aircraft fairings market size in 2025, whereas the unmanned systems category is advancing at an 8.29% CAGR through 2031.

- By material, CFRP captured 62.78% of the revenue share in 2025; thermoplastic composites are forecast to expand at 8.86% CAGR through 2031.

- By sales channel, OEM deliveries represented 67.39% of the aircraft fairings market size in 2025, while aftermarket MRO is growing fastest at an 7.98% CAGR.

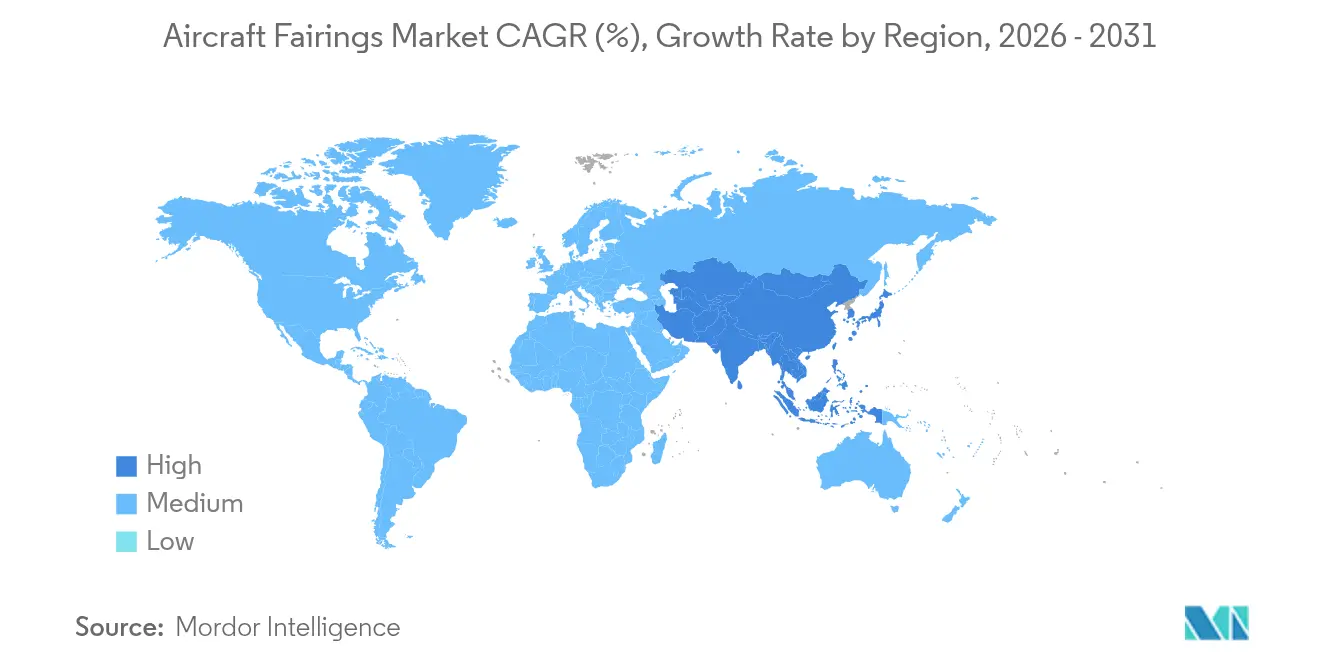

- By region, North America held a 36.24% share in 2025; Asia-Pacific is the fastest-growing geography, with an 8.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Fairings Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging composite adoption to meet fuel-efficiency targets | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rapid fleet-wide replacement of aging aircraft | +1.5% | Global, particularly North America and Asia-Pacific | Long term (≥ 4 years) |

| Proliferation of UAV, advanced air mobility, and eVTOL platforms | +0.9% | North America and Europe leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth of aftermarket MRO expenditure on replacement fairings | +1.2% | Global | Short term (≤ 2 years) |

| Hybrid-electric aircraft programs spur new fairing designs | +0.7% | Europe and North America | Long term (≥ 4 years) |

| Record commercial single-aisle backlog underpins production visibility | +0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Composite Adoption to Meet Fuel-Efficiency Targets

Airlines under acute fuel-cost pressure are switching from aluminum to CFRP fairings, lifting composite content on next-generation aircraft from 13% on legacy A330s to more than 50% today.[1]Airframer, “Airbus A330/A340 Aircraft Detail,” airframer.com Airbus’ Multifunctional Fuselage Demonstrator shows that thermoplastic skins can cut a further 10% weight while supporting automated welding for 100-per-month build rates. Economic benefits remain compelling: lifetime fuel savings can offset 15-20% of an aircraft’s purchase price when installed composite fairings.[2]CompositesWorld Editors, “Aviation Outlook: Fuel Pricing Ignites Demand for Composites,” compositesworld.com Yet this transition demands heavy capital outlays for autoclaves, robotic lay-up cells, and specialized labor, heightening entry barriers and prompting OEMs to favor partners owning mature composite ecosystems

Rapid Fleet-Wide Replacement of Aging Aircraft

More than 700 jets retire yearly, triggering component harvesting and refurbishment demand that enlarges the retrofit market. Wide-body fairings see sharper wear from long-haul cycles, pushing operators toward aerodynamic upgrade kits rather than new-build orders amid delivery delays. Circular-economy programs that reclaim composite fairings for secondary markets, exemplified by Sumitomo’s tie-up with Werner Aero, are gaining traction but face the hard reality that CFRP recycling is limited and cost-intensive.

Hybrid-Electric Aircraft Programs Spur New Fairing Designs

Emerging propulsion architectures require redesigned nacelles and cooling pathways, broadening fairing complexity. GE Aerospace’s blended-wing-body demonstrator integrates novel nacelle fairings that promise up to 50% fuel-burn improvements. Suppliers co-design thermal-management features alongside structural fairings to gain early-mover status in this new propulsion era.

Record Commercial Single-Aisle Backlog Underpins Production Visibility

Global single-aisle backlogs surpassing 15,000 units guarantee stable volume ordering for at least the next decade. Stable run rates help justify automation investments across composite fairing lines, pushing labor content per unit down and sustaining the aircraft fairings market as production footprints expand in the Americas and Asia.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High and volatile prices of carbon fiber, epoxy, and high-temperature resins | -1.1% | North America and Europe | Short term (≤ 2 years) |

| Stringent certification cycles delaying new fairing technologies | -0.8% | Global | Medium term (2-4 years) |

| Supply-chain consolidation reducing sourcing optionality and compressing margins | -0.9% | Global, with primary effects in North America and Europe | Medium term (2-4 years) |

| Geopolitical trade tensions and tariffs inflating raw-material costs | -0.7% | Global, particularly affecting US-China trade and Europe-Asia supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High and Volatile Prices of Carbon-Fiber, Epoxy, and High-Temperature Resins Compress Supplier Margins

Carbon-fiber demand in aerospace is projected to grow 17% annually, but capacity additions require expensive, long-cycle investments. Geopolitical tension and tariff exposure complicate price forecasting, prompting suppliers to adopt cost-plus contracts yet forcing smaller firms into untenable working-capital positions.

Stringent Certification Cycles Delaying New Fairing Technologies

FAA Advisory Circular 20-62E and mirrored EASA rules extend validation timelines for novel thermoplastics or additive-manufactured fairings to 24-36 months, doubling compliance costs where dual approvals are required. Although the bilateral Technical Implementation Procedures streamline some paperwork, smaller innovators still struggle with the documentation rigor needed to satisfy global regulators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Integration-Driven Dominance of Fuselage Fairings

Fuselage fairings generated 32.84% of the aircraft fairings market size in 2025, thanks to their complex wing-body junction geometries and high OEM integration hurdles. Demand remains sticky because any design change obliges full aerodynamic retesting, making incumbent suppliers difficult to displace. Landing-gear fairings are accelerating at 6.94% CAGR, propelled by tighter airport noise limits and eVTOL program requirements for retractable struts. Wing-body and control-surface fairings stay aligned with mainstream build rates, whereas engine fairings pick up incremental growth from hybrid-electric demonstrators that mandate cooled fairing shells.

Emerging mobility platforms skew design briefings toward rapid manufacturing. Wichita State University’s research shows UAV operators prefer printable modular fairings in days, not weeks. Deutsche Aircraft’s D328eco contract bundling fuselage and landing-gear doors into a single award underlines OEM moves toward integrated supplier packages. Such bundling favors vendors with broad design toolsets and test-article capacity.

By Material: Carbon-Fiber Reinforced Polymer (CFRP) Strength Meets Thermoplastic Agility

CFRP’s 62.78% share underscores its entrenched status across wide-body, narrow-body, and even rotorcraft programs. Yet thermoplastic composites and additively manufactured polymers—growing 8.86% annually—remove autoclave bottlenecks and enable part-count consolidation that slashes assembly labor. For lightweight UAV fairings, cost sensitivity keeps glass fiber viable, while critical damage-tolerant locations (such as lower fuselage chine panels) still rely on aluminum-lithium alloys.

Hexcel’s HexAM PEKK-laser-sintering platform prints complex fairing brackets that are impossible to machine conventionally, cutting scrap and weight simultaneously. EU-funded DOMMINIO efforts extend this digital thread by embedding structural-health sensors into thermoplastic fairings, bringing predictive integrity monitoring directly to line-fit installations. Over time, blended material stacks that mate laminated CFRP skins to printed thermoplastic ribs could dominate the aircraft fairings market.

By Aircraft Type: Commercial Aviation Drives Market Foundation Amid Emerging Platform Disruption

Commercial aircraft represented 57.69% of the aircraft fairings market share in 2025, with narrow-body programs alone providing 48% and wide-body lines adding another 17%. This dominance stems from sustained production backlogs and airline fleet-renewal plans that translate into reliable, long-term demand for fairings across fuselage, wing, and nacelle locations. Boeing’s latest outlook points to more than 44,000 new jetliners entering service by 2038, of which 32,400 will be single-aisle models—a visibility window that underpins capacity commitments for fairing suppliers. At the same time, narrow-body output is ramping to ease capacity constraints. In contrast, wide-body assembly rates remain tempered because carriers are still trimming long-haul exposure and favoring fuel-efficient alternatives on medium-range missions.

UAV and eVTOL platforms introduce the fastest-growing pocket of demand with an 8.29% CAGR through 2031, creating opportunities for fairings that emphasize rapid fabrication and lower cost structures rather than the exhaustive certification path followed in commercial programs. Military aircraft provide a steady baseline supported by elevated defense budgets amid geopolitical tensions, while general aviation benefits from renewed interest in business travel. Airbus delivered 766 aircraft in 2024 and retained a backlog of 8,658 units, underscoring the depth of commercial production that continues to anchor the aircraft fairings market size. Concurrently, the company’s focus on next-generation designs and sustainable aviation fuel keeps composite fairing specifications advancing. JetZero’s blended-wing-body demonstrator, which targets a 50% fuel-burn reduction by tightly integrating nacelle and body fairings supplied by Collins Aerospace, highlights how commercial performance requirements accelerate technology cross-pollination across the wider aircraft fairings market. For suppliers, the challenge is to balance the rigorous qualification schedules of established airliner programs with the fast-track, iterative development cycles favored by emerging mobility platforms, forcing dual expertise in traditional certification and rapid prototyping.

By Sales Channel: OEM Dominance and Aftermarket Momentum

OEM lines consumed 67.39% of fairing shipments in 2025, reflecting line-fit installation efficiencies and tight engineering change controls at Airbus and Boeing. Nonetheless, aftermarket revenue grows at 7.98% CAGR as airlines extend asset lives amid delivery bottlenecks and capital rationing. VSE Aviation’s USD 750 million distribution wins illustrate the scale of logistics hubs required to stock varied fairings across global depots.

Higher aftermarket margins attract tier-2 players, yet the service imperative is onerous: FCAH Aerospace’s tie-in with Cobalt Aero Services spans nacelles, thrust reversers, and fairings, demanding 24-hour dispatch windows. Balancing inventory positions against working-capital drain becomes a critical success factor as component SKUs proliferate.

Geography Analysis

North America captured 36.24% of the aircraft fairings market share in 2025, supported by Boeing’s production recovery and a USD 1 billion GE Aerospace manufacturing commitment that boosts composite capacity in multiple US states. Long-established clusters in Washington and South Carolina give suppliers a mature ecosystem, although tariff policies and skilled-labor gaps continue to strain cost bases. RTX’s USD 2 billion facilities expansion highlights OEM faith in sustained demand even as the near-term operating environment remains inflationary.

Asia-Pacific is the fastest-growing region, showing 8.51% CAGR to 2031. Indigenous programs such as China’s C919 or India’s HTT-40 intensify localization mandates, drawing Western tier-1s into joint-venture factories. Strata Manufacturing recorded 38% output growth, exporting 11,774 structures across Airbus and Boeing models, signaling the Gulf’s ambition to become a composites powerhouse. Hanwha Aerospace’s new 100,000 m² Vietnam site for GE and Rolls-Royce components further validates the shift.

Europe benefits from Airbus’ production tempo and focuses on green materials. Airbus’ bio-based carbon-fiber feasibility trials for helicopter fairings mark early steps toward carbon-neutral supply chains. Japan preserves a niche as a high-grade carbon-fiber supplier, with Mitsubishi Chemical targeting 12% composite growth on future mobility programs. Meanwhile, Middle East and Africa markets leverage free-trade zones and proximity to long-haul routes to win offset work from OEMs. However, achieving certification parity with Western peers remains an ongoing task.

Competitive Landscape

The aircraft fairings market is moderately concentrated, with tier-1 leaders—FACC AG, GKN Aerospace, and Collins Aerospace (RTX Corporation)—holding long-standing life-of-program contracts that deter new entrants. Nonetheless, supply-chain fragility since 2020 has prompted OEM reassessment of single-source dependencies. Some OEMs explore partial insourcing of critical fairings, while others seed new Asian suppliers for resilience. Capital-intensive composite expansions underline the widening capability gap; Collins’ USD 200 million Spokane brake-material upgrade enlarges capacity 50% and embeds further automation.

Operational excellence becomes a differentiator. FACC’s 2025 Aero Excellence Award shows how rigorous quality frameworks shorten cycle times and win OEM accolades. Additive manufacturing also disrupts cost structures; Hexcel’s HexAM demonstrations validate printed thermoplastic fairings ready for high-temperature zones, signaling a future where tooling-light processes break even at lower volumes.

The competitive chessboard further fragments along program lines: incumbent suppliers chase high-volume narrow-body awards, while agile specialists pivot toward eVTOL prototypes needing rapid turnaround. Cross-pollination of workforce and digital twins between these silos will decide margin leadership through 2030.

Aircraft Fairings Industry Leaders

Spirit AeroSystems, Inc.

FACC AG

Collins Aerospace (RTX Corporation)

GKN Aerospace

Airbus Aerostructures (Airbus SE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: RTX Corporation signed with JetZero to supply engine-integration and nacelle structures for a blended-wing-body demonstrator, including advanced fairings for 2027 test flights.

- June 2023: Strata Manufacturing PJSC (Strata) and SABCA signed a contract to manufacture and assemble A350-1000 Flap Support Fairings, expanding upon their existing partnership for A350-900 Flap Support Fairings and reinforcing their collaboration in delivering aviation components.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aircraft fairings market as global revenue generated from newly manufactured and certified replacement aerodynamic covers that streamline airflow around fixed-wing civil and military aircraft wing-to-body joints, flap tracks, landing gear, engine pylons, and other flight-control surfaces. According to Mordor Intelligence, we track value in current US dollars across both OEM shipments and qualified aftermarket sales through the entire service life.

Scope Exclusion: Rocket or payload fairings used in launch vehicles and missiles fall outside this definition.

Segmentation Overview

- By Application

- Fuselage

- Landing Gear

- Wings

- Control Surfaces

- Engine

- By Material

- Carbon-Fiber Reinforced Polymer (CFRP)

- Glass-Fiber Composites

- Metal Alloys

- Thermoplastic Composites

- Additively-Manufactured Thermoplastics

- By Aircraft Type

- Commercial

- Narrow-Body Commercial Aircraft

- Wide-Body Commercial Aircraft

- Military

- Combat

- Non-Combat

- General Aviation

- Unmanned Systems

- Commercial

- By Sales Channel

- OEM Production

- Aftermarket MRO

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed aerostructure engineers, fairing tooling specialists, and senior MRO buyers across North America, Europe, and Asia-Pacific. These discussions confirmed composite cost spreads, typical ship-set pricing, and replacement intervals, while clarifying how fleet retrofits or groundings sway annual demand.

Desk Research

We relied on first-tier public sources such as the FAA Aerospace Forecast, EASA Annual Safety Review, ICAO Air-Transport Monitor, UN Comtrade HS-8807 trade data, and General Aviation Manufacturers Association shipments. Company 10-Ks, Aviation Week delivery logs, D&B Hoovers financials, and Questel patent analytics helped us profile suppliers and material shifts. This is an illustrative list; numerous additional datasets and journals informed data validation.

Market-Sizing & Forecasting

A blended top-down and bottom-up construct is applied. We begin with annual aircraft deliveries, active fleet counts, and major overhaul schedules, then derive fairing demand by multiplying platform volumes with representative ship-set values. Supplier roll-ups of sampled composite and metallic part volumes act as a reasonableness check. Key variables include OEM build rates, narrow-body versus wide-body mix, composite penetration ratio, average selling price drift, and HS-8807 export movements. Multivariate regression against revenue passenger kilometers and defense outlay trends shapes the 2025-2030 outlook, while any data gaps are bridged through conservative replacement-rate caps.

Data Validation & Update Cycle

Mordor analysts subject every model to variance checks against historical deliveries, airline MRO spend, and trade statistics before peer sign-off. Reports refresh annually, with interim updates triggered by material events such as abrupt OEM rate changes, ensuring clients receive the latest vetted view.

Why Mordor's Aircraft Fairings Baseline Remains Dependable

Published estimates often diverge because firms adopt different item lists, pricing curves, and refresh cadences.

We lock scope, currency, and build-rate inputs up front and disclose them, letting users trace each figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.96 billion | Mordor Intelligence | - |

| USD 2.43 billion | Global Consultancy A | Includes retrofit kits and BFE interior fairings |

| USD 2.70 billion | Industry Publisher B | Groups nacelles and radomes with fairings |

| USD 2.09 billion | Research Firm C | Excludes aftermarket MRO revenue |

The comparison shows that our disciplined scope choices and transparent variable selection deliver a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the aircraft fairings market?

The aircraft fairings market is valued at USD 2.09 billion in 2026 and is forecasted to grow to USD 2.91 billion by 2031.

Which application segment commands the largest share?

Fuselage fairings hold 32.84% of revenue in 2025, reflecting their integration complexity and critical aerodynamic role,

Why are thermoplastic composites gaining traction?

Thermoplastics enable faster cycle times, automated welding, and easier recycling, supporting a 8.86% CAGR through 2031

Which region is growing fastest?

Asia-Pacific leads growth at 8.51% CAGR, powered by indigenous jet programs and supply-chain localization.

How will hybrid-electric aircraft affect fairing design?

Hybrid propulsion architectures require new nacelle and cooling fairings, opening design-win opportunities for suppliers that can integrate thermal management with structural integrity.

What are the key challenges for new entrants?

Volatile carbon-fiber pricing and protracted FAA/EASA certification cycles extend ROI horizons and favor incumbents with capital and regulatory expertise.

Page last updated on: