Aircraft Antenna Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

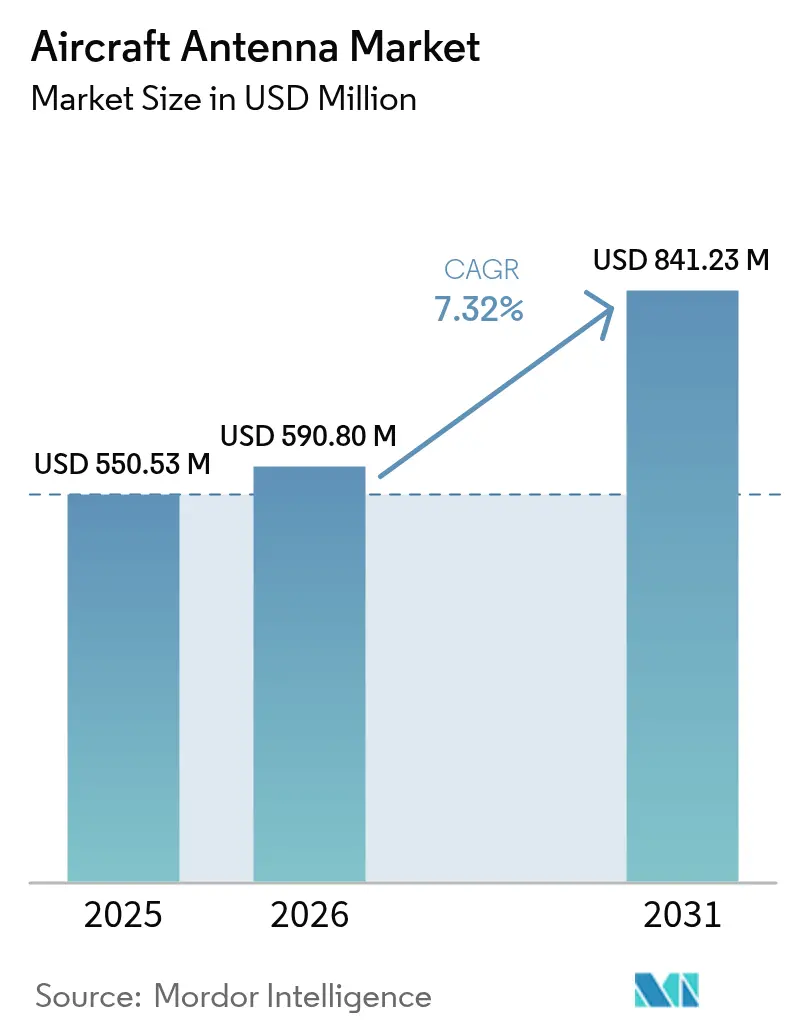

| Market Size (2026) | USD 590.8 Million |

| Market Size (2031) | USD 841.23 Million |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Antenna Market Analysis by Mordor Intelligence

The aircraft antenna market size was valued at USD 550.53 million in 2025 and estimated to grow from USD 590.8 million in 2026 to reach USD 841.23 million by 2031, at a CAGR of 7.32% during the forecast period (2026-2031). Current growth stems from airline commitments to multi-orbit connectivity, regulator-driven surveillance upgrades, and rising unmanned aerial system demand that requires always-on links for beyond-visual-line-of-sight operations. Segment leaders now design antennas into digital flight decks at the blueprint stage, shifting procurement earlier in the aircraft life cycle. Operators prioritize equipment supporting geostationary, medium, low Earth orbit, and emerging 5G air-to-ground links in a single terminal, creating a replacement pull across legacy fleets. Supply-chain disruption in gallium and specialty RF substrates continues to influence pricing. It encourages vertical integration among tier-one suppliers and additive-manufacturing adoption for low-weight conformal arrays.

Key Report Takeaways

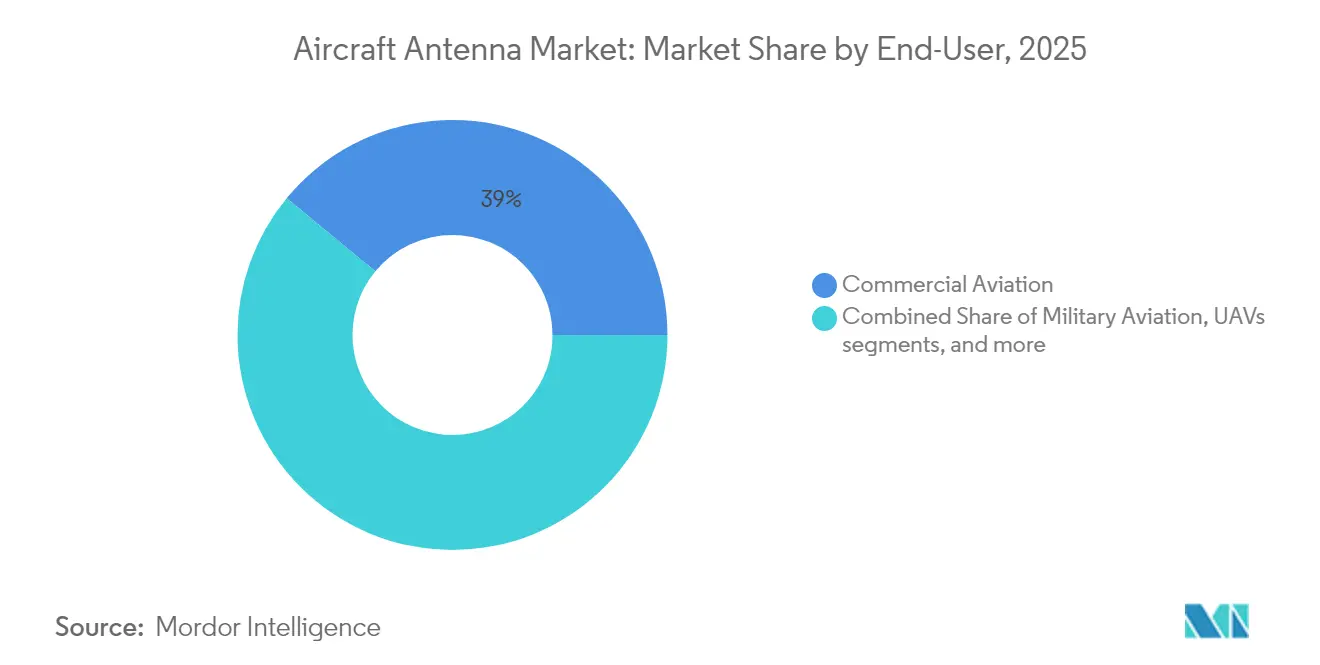

- By end user, commercial aviation held 39.02% of the aircraft antenna market share in 2025, while unmanned aerial vehicles are projected to expand at a 8.82% CAGR through 2031.

- By application, surveillance and reconnaissance accounted for a 40.86% share of the aircraft antenna market size in 2025; electronic warfare antennas are forecasted to grow at an 8.28% CAGR to 2031.

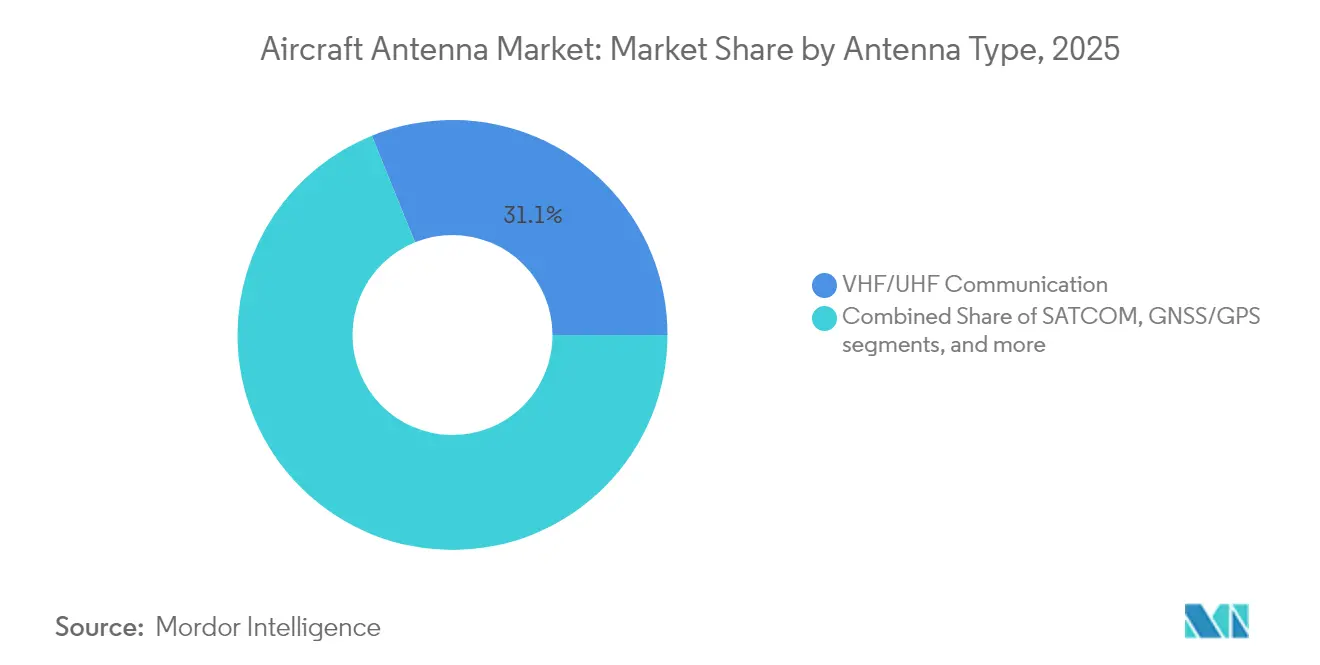

- By antenna type, VHF/UHF communication units captured 31.12% of the aircraft antenna market in 2025, whereas 5G airborne antennas are poised to rise at a 7.39% CAGR over the same period.

- By frequency band, X-band solutions led with 38.74% revenue share in 2025; Ku/Ka-band systems are anticipated to register a 9.21% CAGR up to 2031.

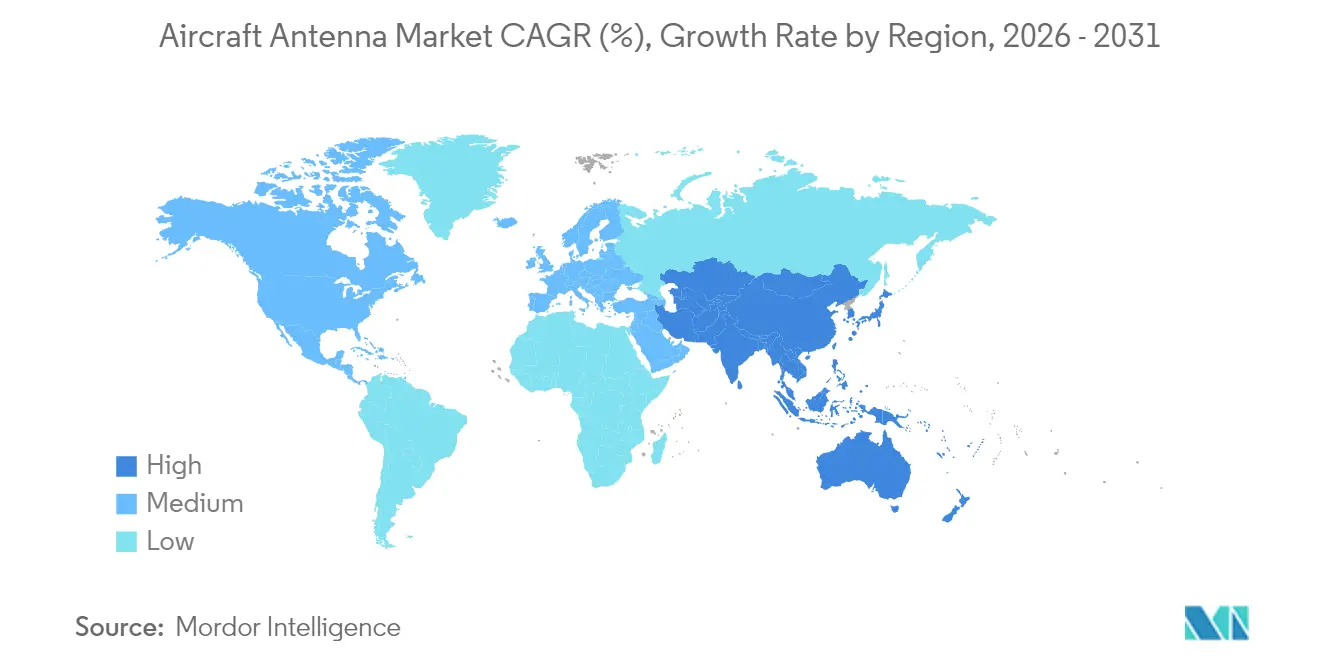

- By geography, North America commanded a 35.22% share in 2025, while Asia-Pacific is tracking the fastest expansion at an 7.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global aircraft deliveries | +1.8% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| Next-gen SATCOM and 5G airborne-connectivity roll-outs | +2.1% | Global, early adoption in North America and China | Short term (≤ 2 years) |

| Fleet-wide ADS-B/Mode-S transponder mandates | +1.2% | Global, with regulatory variations by region | Short term (≤ 2 years) |

| Surging UAV demand for BVLOS mission profiles | +1.5% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Ultra-light conformal antennas for eVTOL platforms | +0.6% | North America and EU, pilot programs in urban centers | Long term (≥ 4 years) |

| Additive-manufactured printed antennas lowering SWaP | +0.9% | Global, with R&D concentration in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Aircraft Deliveries

Boeing’s 2024 outlook sets demand for 43,975 new airplanes over two decades, dominated by single-aisle jets that rely on weight-optimized antennas for cockpit and passenger connectivity. During initial design reviews, airlines are locking in multi-band, software-defined arrays because antenna choices are now seen as a thirty-year strategic decision rather than an afterthought. This design-finish migration pulls revenue recognition forward for suppliers and compresses retrofit cycles in the aftermarket. High passenger growth forecasts in Asia-Pacific, led by 4.8% annual traffic gains, translate directly into first-fit antenna volume and recurring spares demand. The scale of impending deliveries lifts the aircraft antenna market by securing baseline orders for each airframe produced and by accelerating replacement needs for fleets approaching midlife.

Next-gen SATCOM and 5G Airborne-Connectivity Roll-outs

Multi-orbit satellite constellations and terrestrial 5G air-to-ground networks converge, forcing antenna vendors to develop electronically steerable systems that roam seamlessly across disparate spectra. China Telecom and partner OEMs demonstrated network hand-off between tower and LEO links, proving higher throughput and lower latency than legacy GEO-only configurations; this benchmark is pushing North American carriers to field dual-mode arrays within the next fleet retrofit window. The ViaSat-3 launch and the first commercial service activation in 2024 underscore the bandwidth leap GEO craft can still deliver when paired with agile flat-panel apertures.[1]Viasat Inc., “ViaSat-3 F1 Enters Commercial Service,” viasat.com Airlines view multi-orbit agility as an insurance policy against coverage gaps and a foundation for real-time analytics, making antenna upgrades core to digital transformation strategies. Aggressive roll-outs add 2.1 percentage points to forecast CAGR by unlocking premium service revenues across passenger cabins and operational data pipes.

Fleet-wide ADS-B/Mode-S Transponder Mandates

The Federal Aviation Administration’s ADS-B rule, finalized in 2023, obliges aircraft in controlled airspace to broadcast precise position, triggering a global replacement cycle for antennas that must handle high-integrity navigation signals. Canada’s move to space-based ADS-B reception further tightens the specification, demanding diversity installations capable of simultaneous ground and satellite interrogation. In parallel, European regulators call for enhanced accuracy categories requiring 0.05 nautical mile positional tolerance, steering OEMs toward antennas that fuse GPS, Galileo, and WAAS sources. Compliance timetables stagger through the decade, spreading demand and ensuring a stable pipeline for retrofit kits. Mandates contribute 1.2 percentage points to market CAGR by guaranteeing baseline upgrading activity independent of macroeconomic cycles.

Surging UAV Demand for BVLOS Mission Profiles

US lawmakers have instructed the FAA to publish final beyond-visual-line-of-sight rules, removing a regulatory bottleneck that has curtailed commercial drone scale. BVLOS missions need resilient command links that often ride Ku or Ka satellites when terrestrial coverage is absent. Start-ups integrating geofencing, detect-and-avoid sensors, and satcom-backed control loops rely on low-profile, low-power antennas purpose-built for sub-55 lb airframes. Honeywell’s counter-swarm solution selected by the US Air Force demonstrates technology spill-over from civilian to defense UAVs, enlarging addressable volume.[2]Honeywell International, “Counter-Swarm UAS Press Statement,” honeywell.com These factors raise the CAGR by 1.5 percentage points as small-format antennas move from prototype to production scale, attracting a cluster of new entrants and venture funding.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antenna-radome integration complexity in composite airframes | -1.4% | Global, particularly affecting next-gen aircraft programs | Medium term (2-4 years) |

| Spectrum-congestion in L- and C-bands | -0.8% | Global, with acute issues in dense air traffic regions | Short term (≤ 2 years) |

| Long qualification cycles for aerospace hardware | -0.9% | Global, with varying regulatory timelines by region | Long term (≥ 4 years) |

| Supply-chain shortages of specialty RF materials | -1.1% | Global, with concentration in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Antenna-radome Integration Complexity in Composite Airframes

The shift from aluminum to carbon-fiber fuselages complicates RF propagation because conductive mesh layers introduce new attenuation paths. The ACASIAS consortium embedded Ku-band arrays directly into a 1.2 m × 3 m panel, proving feasibility yet highlighting lengthy qualification and bonding verification steps.[3]National Aeronautics and Space Administration, “ACASIAS Composite Antenna Panel Test,” nasa.gov Structural integrity must pair with radiation efficiency, which can demand costly electromagnetic simulations, prototype coupons, and destructive testing. Recent FAA directives on broadband antenna adapter plate corrosion illustrate continuing reliability hurdles even for metal airframes, let alone novel composites. These engineering burdens extend time-to-market and deter smaller suppliers without in-house materials labs, subtracting 1.4 percentage points from potential CAGR until certified design toolchains mature.

Spectrum Congestion in L- and C-bands

The 1030/1090 MHz corridor supports Mode S, ADS-B, and many air navigation aids, yet terrestrial 5G macro-cells target the same slice. EUROCONTROL flags interference risk from non-aviation transmitters that can desensitize airborne receivers on busy routes, compelling stricter out-of-band rejection requirements that older antennas cannot meet. Developing adaptive filters or software-defined radios raises the cost of the bill-of-materials, a burden amplified by gallium supply constraints since China controls the bulk of refined output. Certification authorities are cautious, slowing approval of frequency-agile designs until exhaustive coexistence tests are passed. Resulting uncertainty removes 0.8 percentage points from forecast CAGR because some retrofit programs are paused awaiting final spectrum-sharing outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Commercial Aviation Drives Volume

Commercial aviation held 39.02% of the aircraft antenna market in 2025, thanks to standardized certification pathways and the sheer quantity of narrow-body jets entering fleets. Airlines procure multi-orbit and 5G-ready antennas parallel with cabin refits that add Wi-Fi portals and real-time telemetry, assuring predictable replacement cycles. Business and general aviation buyers have begun migrating toward airline-grade broadband links as charter clients demand consistent connectivity, but smaller cabin footprints still limit multi-antenna architectures. Military aviation delivers fewer units yet commands higher margins because of encryption, anti-jam, and electronic warfare specifications; programs like the F-16 Viper Shield upgrade illustrate the value of integrated broadband apertures.

Unmanned aerial vehicles represent the fastest-growing slice, advancing at a 8.82% CAGR. Regulations that once confined drones to visual line-of-sight now allow longer routes, enabling package logistics, pipeline inspection, and precision agriculture. Lightweight aerogel antennas field-tested by NASA cut system mass while sustaining Ka-band links, meeting the strict size, weight, and power targets for electric multicopters. Defense buyers also scale swarming platforms that rely on phase-aligned networks for cooperative flight. This crossover lets producers amortize R&D across civil and military channels, anchoring UAV momentum as a durable growth lever for the aircraft antenna market.

By Application: Surveillance Dominance Faces Electronic Warfare Growth

Surveillance and reconnaissance made up 40.86% of revenues in 2025 because ADS-B, traffic collision avoidance systems, and space-based radar rely on dedicated apertures to collect positional data. Mandatory carriage across commercial and business fleets ensures stable annual replacements, while border-security agencies add orders for high-gain synthetic aperture radar pods. Communication applications sit close behind as passenger broadband usage spikes and airlines shift operational messaging to IP links. Navigation antennas enjoy consistent demand through multi-constellation upgrades that improve resilience to spoofing and jamming.

Electronic warfare shows the highest upside at an 8.28% CAGR. Block upgrades to existing fighters require modular antenna units that house transmitter and receiver elements for active protection suites. The aircraft antenna market size for electronic warfare rises as programs migrate toward digital arrays capable of real-time beamforming, enabling simultaneous search, track, and jam functions. Civil platforms also integrate threat-monitoring hardware to comply with evolving security directives, blending commercial and defense spending streams. These trends induce suppliers to build common core chipsets that can be scaled from regional jet radomes to drone pylons, gaining cost efficiency.

By Antenna Type: Legacy Systems Face Next-Gen Disruption

VHF/UHF communication arrays retained a 31.12% share in 2025, underpinned by universal air-traffic-control voice mandates. Replacement demand is tied to service life rather than innovation, making it a cash-flow anchor for incumbents. SATCOM antennas, ranging from mechanically steered parabolas to flat electronically scanned panels, occupy the second largest slot as airlines roll out streaming-grade bandwidth. Traditional navigation antennas—VOR, ILS, and marker beacon—keep steady, although growth is capped by maturation in the ground infrastructure.

5G airborne antennas, however, are set to rise at 7.39% CAGR via early deployments over China and Europe. Their sub-meter form factor and software-definable waveforms enable fusion with existing radome space, protecting aerodynamics. Multiband conformal variants secure long-term interest because they reduce drag and maintenance while adding capacity and align with carbon reduction efforts. Thales securing sole-source status for the Lilium eVTOL jet validates a design language in which antennas become an invisible skin element rather than a bolt-on pod.

By Frequency Band: X-band Leadership Challenged by Higher Frequencies

X-band antennas delivered 38.74% revenue in 2025, driven by weather radar, maritime patrol, and airborne ground-mapping missions that require good cloud penetration. Air forces worldwide keep X-band stockpiles for compatible legacy radars, ensuring repeat production. Lower frequencies, including VHF and UHF, remain essential for command-and-control networks, though capacity ceilings limit new growth. L-band retains a navigation niche, bolstered by GNSS augmentation projects.

Ku/Ka-band units will expand at a 9.21% CAGR as high-throughput satellites proliferate. Delta Air Lines’ decision to equip A350 and A321neo jets with a simultaneous LEO–GEO solution based on Ku and Ka illustrates demand for maximal bandwidth at consistent latency. Ka-band opens doors to real-time cloud gaming and edge analytics, services that produce ancillary revenue for carriers. Antenna OEMs, therefore, pivot R&D toward broadband multi-band feed chains able to handle 20 GHz and above, while maintaining backward compatibility with legacy services to smooth airline certification pathways.

Geography Analysis

North America contributed 35.22% of global revenue in 2025 as Boeing line-fit programs and sustained Pentagon outlays kept production lines busy. Airlines in the region have led the early adoption of low Earth orbit constellations and have begun equipping regional jets with phased-array panels certified for passenger Wi-Fi and flight-critical communications. United Airlines’ plan to retrofit more than 300 aircraft with Starlink terminals underscores a willingness to fast-track innovation. Government contracts, including a USD 568 million Viasat framework for C5ISR hardware, add volume and validate next-generation aperture concepts. Canadian mandates for space-based ADS-B further boost diversity antenna installations across business and helicopter fleets, anchoring replacement sales.

Asia-Pacific is projected to grow the fastest at an 7.96% CAGR, reflecting structural fleet growth and escalating technology ambitions. China is forecasted to more than double its active aircraft to 9,740 by 2043, translating to a multibillion-dollar pipeline for cockpit, cabin, and drone antennas. Regional suppliers leverage domestic 5G advances to leapfrog directly to hybrid tower-satellite architectures, compressing the product cycle. Japan’s target of launching ad-hoc airborne telecommunications base stations by 2026 shows policy support for aerial network layers beyond traditional satellite. India and Southeast Asia also order new narrow-body fleets to serve fast-rising middle-class travel, extending the demand base for standardized connectivity kits.

Europe retains a large installed base through Airbus production, but growth pivots toward sustainability and urban mobility. Regulatory pushes on carbon impact drive the adoption of lighter, flush-mounted antennas that reduce drag. The European Satellite Services Provider consortium’s move toward space-based traffic surveillance requires new dual-frequency arrays to satisfy orbital and terrestrial link diversity needs. Lilium’s selection of a single-supplier strategy for its eVTOL program magnifies European focus on integrated antenna skins. Middle East and Africa remain smaller today, yet host major hub expansions that rely on broadband-enabled passenger experience, positioned to increase antenna uptake as infrastructure matures.

Regulatory Landscape

Aircraft antenna design and installation are shaped by aviation safety certification requirements alongside spectrum regulation. In the United States, the Federal Aviation Administration (FAA) uses Technical Standard Orders (TSOs) as minimum performance standards for avionics articles, but TSO authorization does not by itself approve installation, which must be supported through aircraft-level type certification or supplemental type certification. In Europe, EASA frames the compliance basis for airborne communications, navigation, and surveillance around CS-ACNS (Issue 5), which is used to demonstrate conformity for CNS and ADS-B related installations and can call for unit-level evidence beyond ETSO-style article compliance depending on the aircraft and operational intent.

On spectrum, aircraft radio operations and emissions are governed by Federal Communications Commission (FCC) rules for aviation services (47 CFR Part 87), including requirements for aircraft stations and associated RF equipment such as frequency stability constraints for VHF systems. This framework also determines how higher-frequency links are handled through defined emission and operational constraints, which in turn shapes antenna filtering, isolation, and qualification testing as multiband and multi-orbit terminals expand RF coexistence complexity.

Value Chain Analysis

The aircraft antenna value chain begins with raw materials and RF components (specialty RF substrates, radome and composite materials, and RF semiconductors), then moves into antenna design, fabrication, and qualification. It is followed by integration with modems, avionics, and radome or fuselage provisions. Tier suppliers and avionics primes such as Collins Aerospace, Honeywell, and L3Harris package antennas into certified connectivity, navigation, surveillance, and electronic warfare subsystems, with line-fit pathways tied to aircraft OEM production processes and retrofit pathways executed via MROs and STC holders. Aftermarket support covers spares provisioning, repairs, and configuration control over multi-year service lives, which is increasingly important for software-enabled terminals where antenna, modem, and network profiles must remain interoperable.

Recent programs emphasize electronically steerable antennas (ESAs) and multi-orbit architectures, shifting more value toward RF system engineering, certification management, and integration tooling rather than stand-alone antenna hardware. In 2026-related activity, ThinKom Solutions moved from product development into network readiness through SES Open Orbits type approval for its ThinAir Ka2517 and also unveiled the ThinAir Nexus multi-orbit platform. The same direction appears in ESA roadmaps discussed by Intellian for Panasonic Avionics, along with an ESA-based Aviation Antenna Terminal Solution concept from Hughes. These changes raise the role of qualification labs, production test automation, and secure access to constrained RF inputs, reinforcing vertical integration and dual-sourcing strategies among higher-tier suppliers.

Competitive Landscape

The aircraft antenna market is moderately fragmented. L3Harris, Honeywell, and Collins Aerospace combine qualification track records and avionics portfolios to preserve lead share. Meanwhile, niche innovators like ThinKom Solutions target electronically steered apertures that disrupt legacy mechanical offerings. Vertical acquisitions, such as Honeywell's USD 1.9 billion purchase of CAES, illustrate a race to secure gallium nitride and phased-array competencies inside corporate walls, protecting supply lines and intellectual property.

Mid-tier vendors pursue additive manufacturing and conformal array breakthroughs. NASA's successful 3D-printed aerogel test flight points to a paradigm in which antennas are produced concurrently with airframe sections, reducing part count and shipping overhead. Partnerships between hardware makers and AI-driven network orchestration firms foster integrated value propositions, blending antenna, modem, and cloud analytics as a single deliverable.

Competitive intensity also rises from regulatory uncertainty that favors suppliers with in-house policy teams able to anticipate certification rule shifts. Boeing's patents filed for structural antenna provisions hint that airframe OEMs may internalize certain antenna functions, potentially squeezing traditional suppliers. However, innovators offering software-defined beam steering and easy over-the-air upgrades can capture share by promising future-proof paths within a tightening regulatory climate.

Aircraft Antenna Industry Leaders

L3Harris Technologies, Inc.

Honeywell International Inc.

Collins Aerospace (RTX Corporation)

Thales Group

HR Smith Group of Companies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most visible opportunity is in factory-offerable, multi-orbit inflight connectivity terminals that reduce retrofit friction and better match antenna decisions to aircraft production cycles. In April 2026, Viasat entered a Boeing technical evaluation process to qualify its AERA electronically steered antenna terminal for 737 MAX, 777X, and 787 programs, and SES and Boeing announced a milestone toward line-fit offerability for a multi-orbit ESA connectivity system on Boeing 737 and 787 production lines. Together, these initiatives create whitespace for suppliers that can package antenna hardware, modem interoperability, and certification artifacts into repeatable line-fit kits, particularly as airlines prioritize terminals that roam across GEO, MEO, and LEO networks without major structural rework.

Another opportunity is the rising pull for low-profile and conformal ESAs that preserve aerodynamics while meeting higher-throughput Ku/Ka needs across commercial and defense platforms. ThinKom introduced the ThinAir Nexus multi-orbit ESA with an installation approach designed around four fuselage lugs, and in May 2026 it was selected by Neo Space Group to supply Ka2517 phased-array antennas for narrow-body aircraft operated by Saudia and Riyadh Air, pointing to regional programs that can scale hardware shipments across fleets. On the defense side, modernization programs that require resilient, high-power communications and specialized apertures, including a USD 20.3 million U.S. Navy contract to Collins Aerospace in January 2026 tied to E-6B Mercury communications upgrades, continue to support missionized antenna integration and certification-ready upgrade kits.

Recent Industry Developments

- April 2026: ThinKom Solutions announced SES Open Orbits network type approval for its ThinAir Ka2517 aircraft antenna and also unveiled the ThinAir Nexus space-optimized, multi-orbit aircraft antenna platform. The approvals and new platform launch strengthen the shift toward electronically steerable antennas that can operate across multiple satellite networks, improving airline and integrator readiness for multi-orbit connectivity deployments.

- December 2025: L3Harris was selected as a subcontractor to provide assured communications for the U.S. Air Force E-4C fleet, with Collins Aerospace as prime contractor. The award supports continued investment in hardened airborne communications architectures, reinforcing demand for tightly integrated antenna and avionics subsystems across strategic mission aircraft upgrades.

- May 2024: Thales and Collins Aerospace announced the first installation of the Thales AVIATOR 700S system, including a high-gain antenna, for a Collins Aerospace commercial aircraft program. The milestone highlighted momentum for high-throughput satcom terminals in commercial aviation and validated the path from system selection to installed hardware on in-service aircraft.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of antennas installed on aircraft to support communication, navigation, and surveillance functions, covering both line-fit and retrofit demand. Revenues are counted for aircraft antenna hardware supplied for civil and defense aviation use, reported in USD.

Scope exclusions: excludes non-airborne ground infrastructure equipment and test benches that are not installed on an aircraft.

Segmentation Overview

- By End User

- Commercial Aviation

- Military Aviation

- Business and General Aviation

- Unmanned Aerial Vehicles (UAVs)

- By Application

- Communication

- Navigation

- Surveillance and Reconnaissance

- Electronic Warfare

- Passenger Connectivity/IFE

- By Antenna Type

- VHF/UHF Communication

- SATCOM

- Navigation (VOR/ILS/MB)

- Transponder and ADS-B

- GNSS/GPS Antennas

- Multiband Conformal

- 5G Airborne

- By Frequency Band

- HF

- VHF

- UHF

- L-band

- C-band

- X-band

- Ku/Ka-band

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean view of aircraft deliveries, in-service fleet, and upgrade cycles, since antenna demand follows build rates and retrofit needs. We mainly rely on public aviation and trade sources such as ICAO, FAA databases and airworthiness publications, EASA references, and defense procurement disclosures where available.

To link aircraft activity to antenna demand, we also review customs and trade statistics, plus standards and spectrum-related documents from bodies such as ITU and RTCA-style committees, along with peer-reviewed papers on airborne communications and navigation systems. Company filings, investor presentations, and reputable press are used to confirm which aircraft programs and avionics upgrade themes are active. Where needed, we use paid subscriptions covering company financials and a patent database to cross-check product focus and timing, and the sources listed here are illustrative since many other references were reviewed for validation and clarification.

Primary Interviews and Surveys

Primary discussions are used to confirm the demand signals behind the model, especially how antenna content changes by aircraft type and by communication, navigation, and surveillance fit. We interview a mix of antenna suppliers, aircraft and avionics ecosystem participants, and downstream operators and maintainers across APAC, EMEA, and the Americas, so assumptions on pricing, replacement cycles, and program timing can be corrected.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 46% |

| Mid tier: 41% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 21% | Managers: 42% | Americas: 22% |

Market-Sizing & Forecasting

Sizing uses top-down logic where aircraft production and fleet activity are converted into an addressable antenna demand pool, then valued using representative pricing. For each major aircraft category, we apply antenna shipset content by application (communication, navigation, surveillance), then adjust for retrofit intensity, since many upgrades land during scheduled maintenance windows.

A set of model inputs is used repeatedly because each is traceable: aircraft deliveries by region, in-service fleet by platform, penetration of SATCOM and connectivity upgrades, typical replacement or upgrade intervals, and indicative average selling price ranges by antenna type and frequency band. Forecasting is handled through scenario analysis, where build-rate outlook, defense budget direction, and connectivity adoption are varied within realistic ranges agreed in expert calls. Bottom-up checks are applied selectively, using sampled program-level demand and supplier revenue cues. Where data is thin for smaller aircraft programs, we apply conservative content assumptions and validate them with follow-up discussions to avoid overstating totals.

Data Validation & Update Cycle

Outputs are checked against independent signals such as aircraft delivery totals, fleet growth, and known retrofit campaigns, then variances are investigated before finalization. When a large gap appears, we re-check the mapping between aircraft platforms and antenna content, and we may reconnect with interviewees to confirm whether the change is real or driven by timing effects.

A multi-step internal review is followed so the final numbers stay consistent across segments and regions, and assumptions are documented so they can be repeated. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major aircraft program rate changes or regulatory and spectrum-related shifts. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Aircraft Antenna Market Size Versus Other Published Estimates

Published market sizes for aircraft antennas can vary because analysts do not always count the same hardware items, and they also use different timing for aircraft build rates and retrofit uptake. Differences also come from how pricing is treated across antenna types, especially when programs shift toward higher-frequency SATCOM and connectivity equipment.

Ground infrastructure antennas and non-airborne test equipment are kept outside Mordor Intelligence's scope, which can reduce value versus estimates that blend aircraft antennas with adjacent ground-side and lab revenue. On top of that, some published figures hold pricing flat across the forecast window or use an older fleet and delivery baseline, which can misstate value when retrofit cycles and aircraft production move year to year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 590.80 M (2026) | |

| Global Consultancy A | USD 537.60 M (2024) | Uses a different base year and a longer forecast window, and the extract does not clarify antenna type coverage or whether aftermarket retrofits are valued with updated pricing, which can pull the headline number down. |

| Industry Publisher B | USD 471.50 M (2025) | Reported base year and sizing year differ from this study, and the published summary provides limited detail on how SATCOM and connectivity antenna penetration is applied across the fleet, which can shift totals meaningfully. |

The spread across the three values is mainly explained by what gets counted with the antenna hardware set, plus the timing of fleet, delivery, and retrofit inputs used to build the demand pool. By keeping the steps tied to observable aircraft activity and by cross-checking pricing and adoption assumptions with expert feedback, our estimate stays easy to trace and repeat when the market environment changes.

Key Questions Answered in the Report

What is the current value of the aircraft antenna market?

The aircraft antenna market stands at USD 590.8 million in 2026, supported by growing demand for multi-orbit connectivity and mandatory surveillance upgrades.

How fast will the market grow through 2031?

The market is forecasted to expand at a 7.32% CAGR during 2026-2031, reaching a USD 841.23 million aircraft antenna market size by 2031.

Which end-user segment offers the highest growth potential?

Unmanned aerial vehicles lead growth at a 8.82% CAGR because BVLOS regulations and commercial drone services require certified, low-power communication links.

Why are Ku and Ka bands gaining momentum?

High-throughput satellites operating in Ku and Ka bands enable streaming-grade inflight connectivity, pushing airlines to adopt antennas that support higher frequencies and driving a 9.21% CAGR for this segment.

What challenges could impede market expansion?

Complex antenna-radome integration in composite airframes and mounting spectrum congestion in L- and C-bands impose engineering and certification hurdles that can lengthen product cycles.

Which region will add the most incremental revenue?

Asia-Pacific is expected to post the fastest growth, at 7.96% CAGR, thanks to China’s large aircraft backlog and regional investments in hybrid 5G and satellite networks.

Page last updated on: