Air Taxi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.47 Billion |

| Market Size (2031) | USD 10.56 Billion |

| Growth Rate (2026 - 2031) | 18.79% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Taxi Market Analysis by Mordor Intelligence

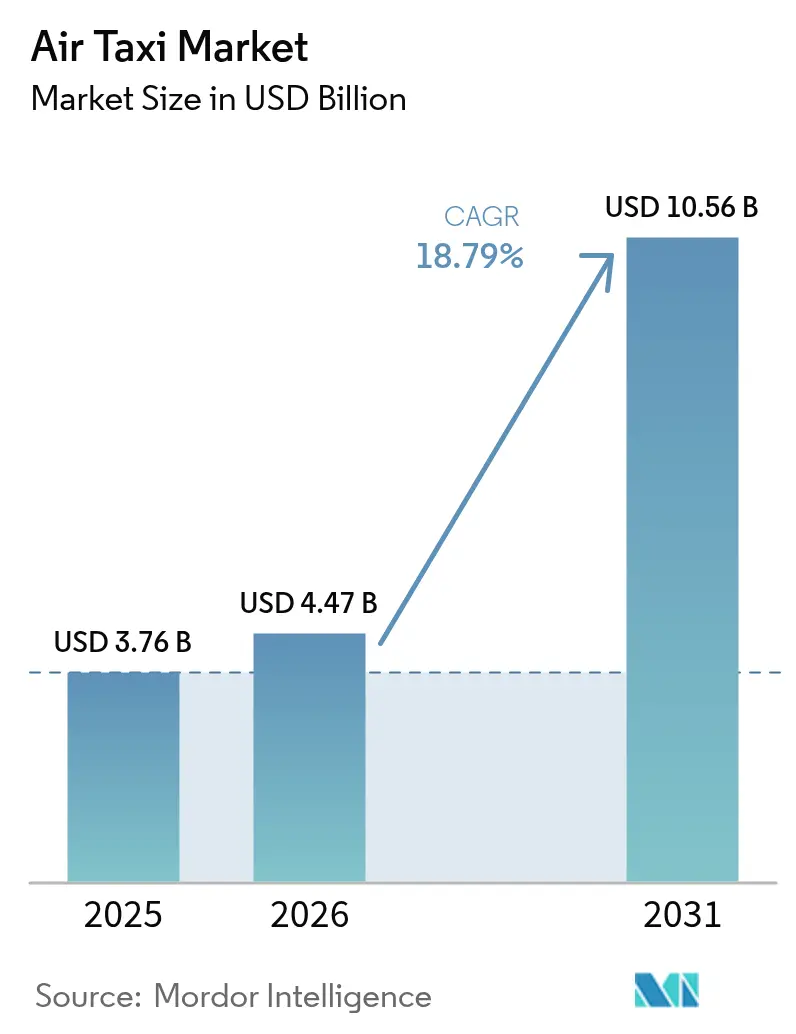

The air taxi market size is expected to grow from USD 3.76 billion in 2025 to USD 4.47 billion in 2026 and is forecast to reach USD 10.56 billion by 2031 at 18.79% CAGR over 2026-2031.

Intensifying prototype-to-production momentum, widening public-private vertiport investment, and early airline route commitments lift near-term demand together. Battery-electric aircraft still anchor most commercial plans, yet hydrogen fuel-cell demonstrations have broadened investor confidence in longer‐range models. North America will keep the revenue lead in 2025, thanks to clear FAA-powered-lift rules and United–Archer route launches. Asia-Pacific shows the sharpest growth curve as China’s low-altitude-economy initiative and Japan’s Osaka Expo trials fast-track certification. Competition is chiefly execution-driven rather than technology-driven now that most OEMs converge on distributed-electric architectures. Venture capital continues to flow despite isolated test setbacks, signaling sustained faith in the maturing air taxi market.

Key Report Takeaways

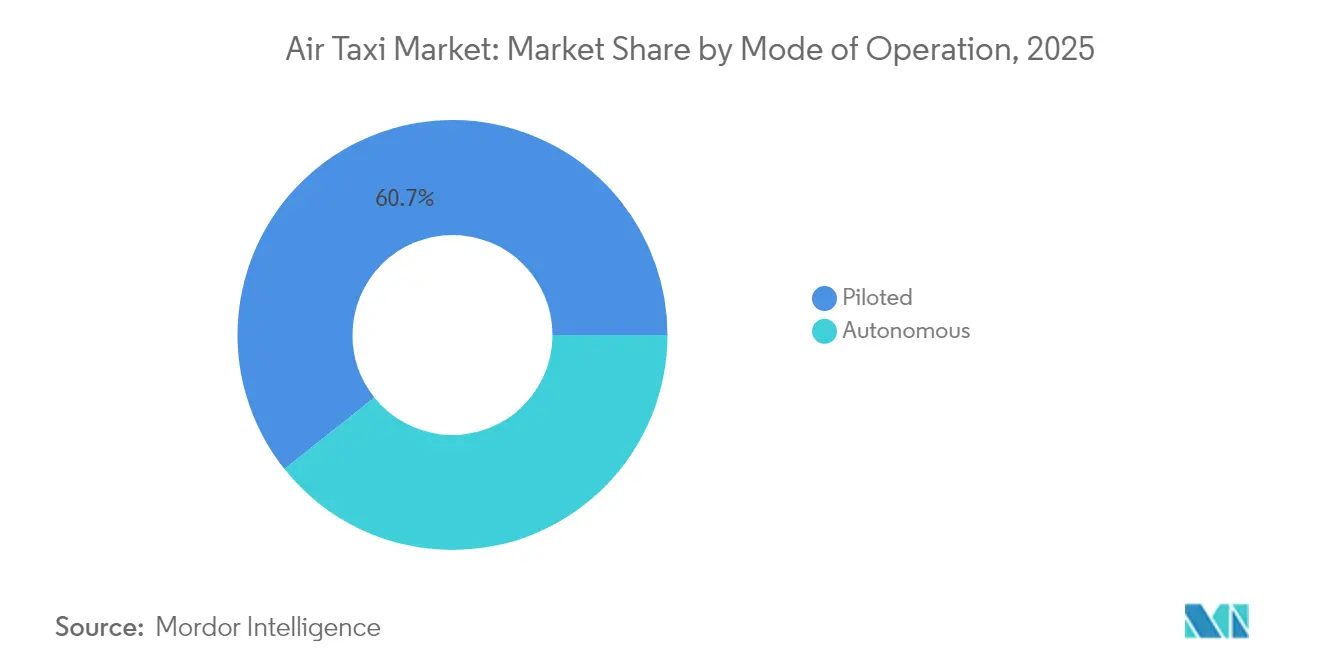

- By mode of operation, piloted aircraft held 60.72% of the air taxi market share in 2025, but autonomous platforms are on course for the quickest 24.10% CAGR through 2031.

- By propulsion type, battery-electric systems captured 54.88% of the air taxi market size in 2025; hydrogen fuel-cell models are forecasted to expand at a 20.85% CAGR.

- By passenger capacity, the 3 to 4-seat layouts commanded 42.30% of 2025 revenue, while the 5 to 6-seat designs led growth with a 19.05% CAGR outlook.

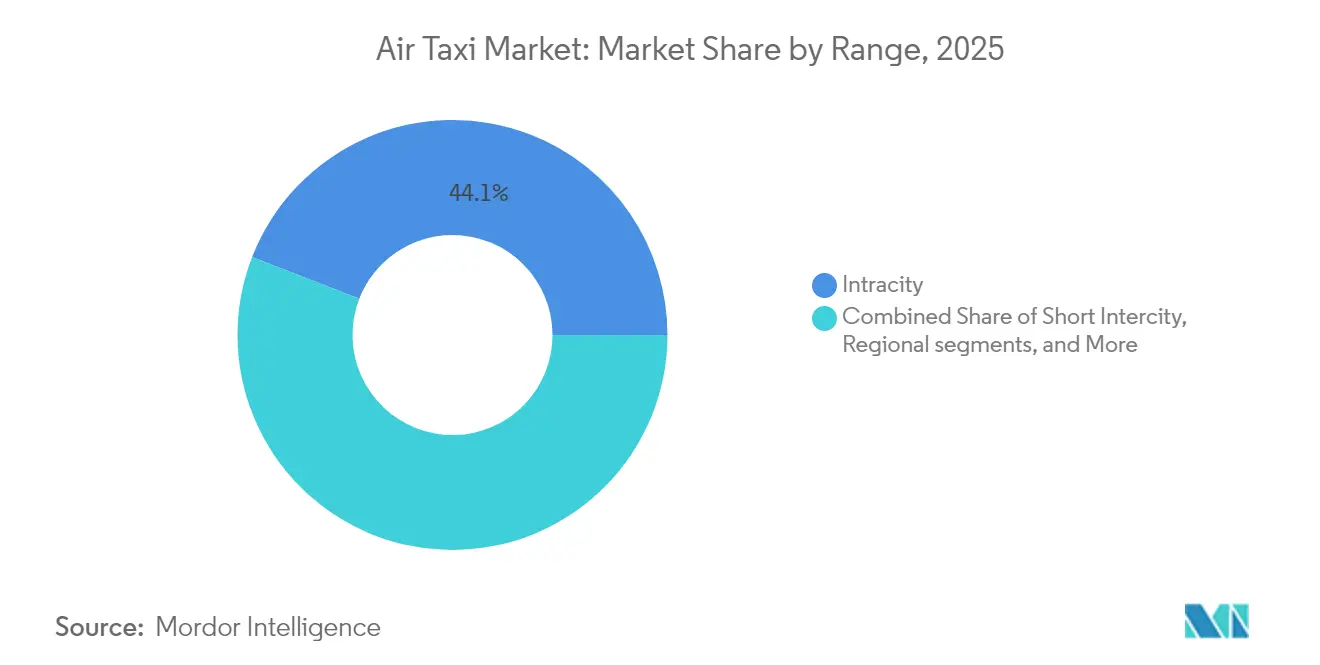

- By range, sub-50 km intracity legs accounted for 44.10% of 2025 spending as the regional 150 to 300 km band accelerates at 19.95% CAGR.

- By end-use, airport shuttles led with 44.70% revenue share in 2025; corporate shuttles are projected to widen fastest at a 21.15% CAGR.

- By lift technology, multicopters delivered 45.20% of 2025 sales, whereas lift-plus-cruise airframes are advancing at a 22.40% CAGR.

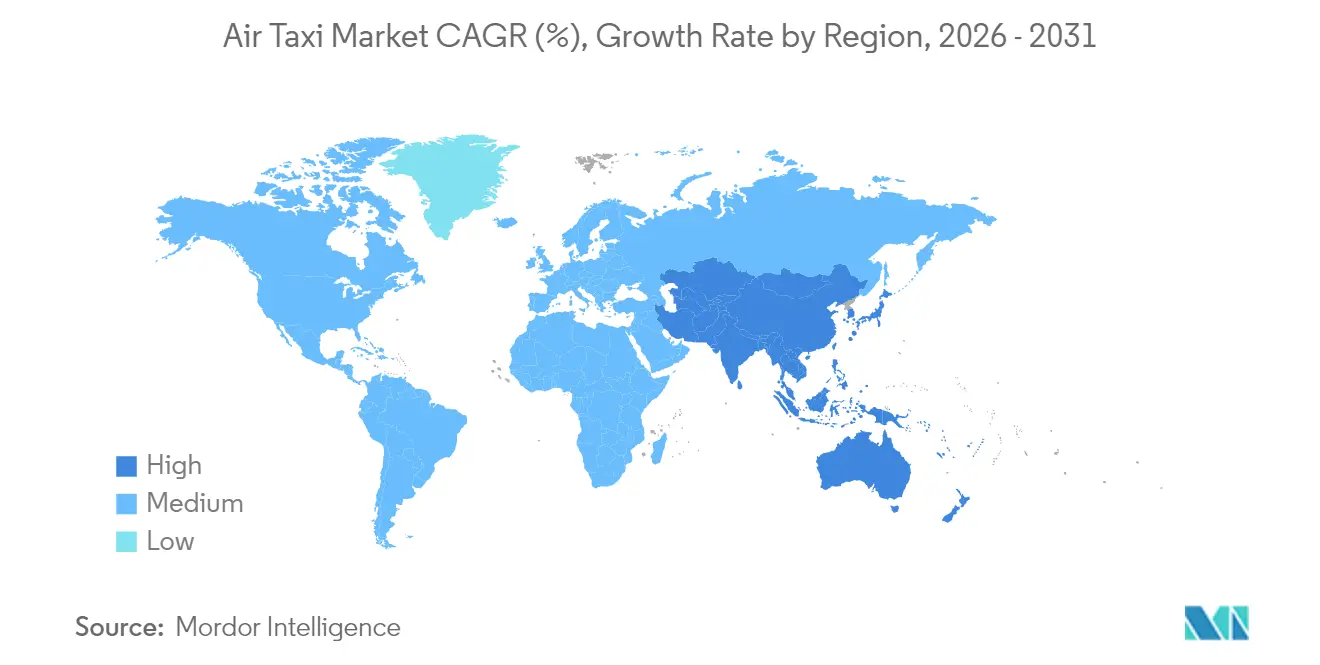

- By geography, North America accounted for 45.10% of 2025 revenue, driven by the FAA's finalization of powered-lift frameworks, while Asia-Pacific is accelerating at a 25.20% CAGR, driven by China's low-altitude economy blueprint, which enables scaling commercial fleets beyond pilot programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery-density breakthroughs extend practical range | +4.2% | North America and Europe, wider global spill-over | Medium term (2-4 years) |

| Vertiport public-private partnerships accelerate infrastructure rollout | +3.8% | North America and EU, early adopters in Asia-Pacific | Medium term (2-4 years) |

| Airline and airport integration for premium first-mile/last-mile service | +3.5% | Global metro hubs | Short term (≤2 years) |

| Noise-abatement eVTOL designs gain fast-track certification | +2.9% | Global under FAA and EASA leadership | Medium term (2-4 years) |

| Post-COVID decentralized work patterns spur regional mobility demand | +2.7% | North America and Europe | Short term (≤2 years) |

| Corporate ESG mandates prioritize zero-emission mobility solutions | +2.1% | Worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Battery-density breakthroughs extend practical range

Present lithium-ion packs deliver 250–300 Wh/kg, capping many urban trips at roughly 30 km. CATL’s 500 Wh/kg Qilin cell and emerging lithium-sulfur chemistries promise to double usable range by 2027, trimming energy cost per seat-kilometer and opening regional city pairs. Structural battery modules in Joby’s S4 airframe remove 15-20% structural weight, while solid-state prototypes meet FAA thermal-runaway criteria and unlock accelerated certification.

Vertiport public-private partnerships accelerate infrastructure rollout

More than 1,500 vertiports sit in global pipelines, but Manhattan’s EB 105A pilot site proves that co-funded models can cut build times to three to five years.[1]Skyports, “Infrastructure Report 2024,” skyports.net Similar frameworks in Dubai and Osaka hint at replicability, ensuring the air taxi market is not supply-constrained by pads and chargers. As infrastructure expands, it will unlock new routes and reduce travel times. Collaboration between the private and public sectors is essential to foster innovation and streamline regulatory processes.

Airline and airport integration for premium first-/last-mile service

United Airlines and Archer plan 10-minute hops from Newark to lower Manhattan at USD 200–300 per seat, embedding eVTOL tickets directly into airline booking flows.[2]United Airlines, “United Announces Plans to Bring eVTOL Flights to Chicago,” united.com Integrated offers slash customer-acquisition costs by roughly two-thirds and monetize dwell time at under-utilized heliports, supplying a quick-win path for incumbent carriers to up-sell loyalty tiers. Airport authorities favor such links because each eVTOL passenger yields USD 15–25 in incremental fee income.

Noise-abatement eVTOL designs gain fast-track certification

NASA ground-treatment trials record 26–36 dB noise reductions relative to legacy helicopters, helping manufacturers meet the FAA’s 62 dB residential overflight ceiling.[3]NASA, “Advanced Air Mobility Noise Studies,” nasa.gov Rotor-blade tip shaping and variable-rpm profiles further cut acoustic signatures, lifting community acceptance scores in German pilot surveys from 2.6 to 3.8 on a five-point scale. Regulators offer abbreviated flight-test plans if prototypes beat helicopter noise footprints by 10 dB or more, bringing forward service-entry dates in core urban corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification bottlenecks for novel flight-control software | -2.6% | Global | Medium term (2-4 years) |

| Limited high-power grid capacity at candidate vertiport sites | -2.3% | Dense urban settings worldwide | Long term (≥ 4 years) |

| Scarcity of aviation-grade lithium and rare-earth materials | -1.7% | Global supply chain | Medium term (2-4 years) |

| Public safety perception after any high-profile incident | -1.5% | Global, risk tolerance varies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Certification bottlenecks for novel flight-control software

Each eVTOL hosts over 10,000 lines of safety-critical code that must comply with DO-178C Level A processes. Scarcity of qualified software assessors forces FAA and EASA to rely on external consultants, sometimes extending approval cycles by two to three years.[4]Government Accountability Office, “Advanced Air Mobility: Federal Agencies Should Take Additional Steps,” gao.gov Predictive cost overruns can consume USD 200–300 million of pre-revenue cash, elevating bankruptcy risk for under-capitalized entrants.

Limited high-power grid capacity at vertiport sites

A single downtown vertiport can draw 1–20 MW during peak charging windows, on par with a mid-size data center. Utilities need 18–36 months to install high-voltage feeders, and upgrades run USD 2–5 million per location. Without on-site storage or micro-grids, launch timelines may slip, dampening the near-term penetration of the air taxi market in power-constrained cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Operation: Autonomous flight poised for the long game

Piloted flights generated 60.72% of segment revenue in 2025, leveraging well-known rotorcraft training pipelines. Autonomous systems, however, are tracking a 24.10% CAGR because they strip USD 150,000-plus in annual pilot wages from the cost stack and support round-the-clock operations without crew-rest bottlenecks. The US corridor trials and China's EHang deployments validate remote oversight concepts, gradually building the safety data regulators require. Rising confidence in autonomy widens the air taxi market size for late-decade deployments aimed at logistics, emergency response, and commuter pools.

Scalability improves as software candidates prove robust across mixed traffic. When autonomy matures, operators could redeploy human pilots into fleet-services roles, boosting aircraft utilization and reducing cancellation risks tied to crew availability. Training and insurance costs should compress in lock-step, though early adopters will maintain a safety pilot on board until regulators sign off on full hands-free operations.

By Propulsion Type: Electric leads, hydrogen breaks range barriers

Battery-electric platforms captured 54.88% of 2025 shipments, buoyed by falling cell costs and simple drivetrain maintenance. Yet hydrogen fuel-cell aircraft, spurred by Joby’s 523-mile demo flight, are advancing at 20.85% CAGR, attracting interest from regional carriers that need multi-hundred-kilometer legs. Battery swaps and 350-kW fast-charge specs keep electric models competitive on urban missions, while hybrid architectures provide a bridge for operators hedging range anxiety.

Infrastructure dictates pace: Battery chargers piggyback on EV build-outs, whereas hydrogen demands new storage and dispensing. Oil majors like BP and Shell see synergies with heavy-truck networks, giving hydrogen a realistic path to a 15–20% air taxi market share post-2030.

By Passenger Capacity: Mid-size cabins optimize yield

Three—to four-seat layouts account for 42.30% of 2025 revenue because they balance airframe weight, vertiport pad size, and high load factors. Corporate shuttle pilots highlight tangible productivity gains when four colleagues can share a private cabin. However, larger 5—to 6-seat cabins lead growth at 19.05% CAGR by unlocking per-seat prices below USD 300, a threshold at which travel managers approve regular use for regional meetings.

Beyond six seats, weight penalties and stricter certification steps converge, eroding margins unless battery densities hit the 500 Wh/kg mark. Cabin flexibility becomes an emerging differentiator, with modular seating that toggles between passenger and light-cargo missions, offering operators new revenue buffers.

By Range: Regional missions gather momentum

Sub-50 km hops still account for 44.10% of flights: city-center connections where congestion premiums justify fares of USD 5–8 per seat-kilometer. As solid-state batteries scale up, the 150–300 km band will expand at 19.95% CAGR, catalyzing services between secondary cities and satellite manufacturing hubs. The evolving range mix increases aircraft utilization, a primary driver of positive cash flow in the air taxi market.

Charging-time economics intersect with route choices. Intracity operators depend on 10–15-minute pit stops, favoring battery-swap concepts. Regional players accept 30-minute turnaround slots as part of passenger boarding sequences, aligning naturally with high-power plug-in architectures.

By End Use: Corporate shuttles in the spotlight

Airport transfers controlled 44.70% of 2025 sales by tapping existing security and baggage channels at major hubs. Yet, a distributed work culture propels corporate shuttles to a 21.15% CAGR, especially on the US West Coast corridors, where technology firms seek low-carbon mobility perks to attract talent. A 5-seat eVTOL that cuts a 90-minute road slog to 20 minutes can reclaim two billable hours per employee, yielding a compelling ROI against premium seat pricing.

Tourism and aerial sightseeing remain reliable shoulder-season fillers, while emergency medical services gain traction as helicopters age out and hospitals adopt ESG targets. This diversity smooths revenue cyclicality, mitigating risk for debt investors underwriting vertiport projects.

By Lift Technology: Multicopters today, lift-plus-cruise tomorrow

Multicopters supplied 45.20% of 2025 deliveries because they echo drone simplicity and require fewer moving parts. Their downside is cruise inefficiency: a level-flight energy burn roughly double that of lift-plus-cruise rivals. Therefore, operators seeking 200–300 km stage lengths gravitate to lift-plus-cruise airframes that promise 40–60% energy savings and lower per-mile wear. The latter segment is pacing at 22.40% CAGR and may overtake multicopters late in the decade if certification stays on course.

Tilt-rotors inherit proven military pedigrees and deliver runway-like speeds, though their mechanical complexity and higher parts count deter first-time owners. Ducted-fan concepts fill niche roles where noise suppression supersedes raw range, notably in European heritage districts with strict acoustic ordinances.

Geography Analysis

North America generated 45.10% of 2025 revenue after the FAA finalized powered-lift frameworks and metropolitan vertiport pilots moved past environmental-review hurdles. The US airlines act as anchor customers, creating predictable demand curves that investors leverage for project-finance structures. Canada and Mexico contribute incremental growth through cross-border tourism routes and supportive test corridors.

Asia-Pacific is accelerating at a 25.20% CAGR. China’s low-altitude economy blueprint green-lights EHang and AutoFlight to scale commercial fleets beyond pilot programs, while Japan’s Osaka Expo is set to showcase daily passenger services in 2025. India’s tier-2 city network opens new miles under mild air traffic density, offering startup-friendly test beds before shifting into crowded skies.

Europe ranks third but wields regulatory influence via EASA’s SC-VTOL code, shaping safety baselines worldwide. Germany hosts flagship players Volocopter and Lilium, although the latter’s insolvency underscores capital-intensity challenges. The EU’s Connecting Europe Facility earmarks USD 1.29 billion for vertiport grants, raising baseline infrastructure readiness across the bloc.

Competitive Landscape

Competitive Landscape

The five most prominent players control less than 20% of global revenue, leaving the air taxi market fragmented. Airline alliances provide validation: United backs Archer, Delta funds Joby, and Embraer’s Eve enjoys regional-carrier support. Technology differentiation is narrowing, shifting competition toward production scalability and supply-chain resilience. Cash burn remains the principal threat—Lilium’s insolvency illustrates the USD 75–100 million annual outlay typical of the flight-test phase. Consolidation looms as aerospace primes, automakers, and energy majors scout bolt-on acquisitions to secure electric-propulsion footholds.

White space remains in regional routes under 300 km, a gap that helicopters seldom fill, and ground travel cannot match in time. Software firms such as Wisk and autonomy specialists from automotive spheres bet on pilot-free operations for an operating-cost edge. Component leaders like Honeywell and Garmin pivot into turnkey flight decks, ensuring supply-chain leverage even if airframe economics stay volatile.

Air Taxi Industry Leaders

Guangzhou EHang Intelligent Technology Co. Ltd.

Volocopter GmbH (Diamond Aircraft Industries GmbH)

Airbus SE

Archer Aviation Inc.

Joby Aviation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: At Expo 2025 in Osaka, Kansai, Japan, ANA Holdings (ANA HD) and Joby Aviation, Inc. showcased a successful public flight demonstration of Joby's air taxi.

- September 2025: Joby Aviation, Inc. partnered with the Ras Al Khaimah Transport Authority (RAKTA) to establish a passenger air taxi service network in the Emirate of Ras Al Khaimah (RAK) by 2027.

- February 2024: The UAE awarded Joby Aviation, Inc., a contract to launch an air taxi service in Dubai. The network is anticipated to launch in 2026, paving the way for a new era of urban mobility.

- January 2024: Hyundai Motor Group unveiled its S-A2 flying taxi prototype. The S-A2 flying taxi is a unique hybrid aircraft that combines the features of a helicopter and a fixed-wing plane.

Global Air Taxi Market Report Scope

An air taxi is an aerial, on-demand transport vehicle for commuting passengers over a shorter distance. It provides a comfortable and efficient air travel option for short distances, bridging the gap between commercial airlines and private jets.

The air taxi market is segmented by mode of operation, and by geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). By mode of operation, the market is segmented into piloted and autonomous. The report also covers the market sizes and forecasts for the air taxi market in major countries across different regions.

For each segment, the market size is provided in terms of value (USD).

| Piloted |

| Autonomous |

| Electric |

| Hybrid |

| Turboshaft |

| Hydrogen Fuel Cell |

| 1 to 2 Seats |

| 3 to 4 Seats |

| 5 to 6 Seats |

| More than 6 Seats |

| Intracity (Less than 50 km) |

| Short Intercity (50 to 150 km) |

| Regional (150 to 300 km) |

| Extended (More than 300 km) |

| Airport Shuttle |

| On-Demand Air Taxi |

| Corporate Shuttle |

| Emergency Medical Services |

| Tourism and Sightseeing |

| Multicopter |

| Tilt-Rotor |

| Lift + Cruise |

| Ducted Fan Jet |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Mode of Operation | Piloted | ||

| Autonomous | |||

| By Propulsion Type | Electric | ||

| Hybrid | |||

| Turboshaft | |||

| Hydrogen Fuel Cell | |||

| By Passenger Capacity | 1 to 2 Seats | ||

| 3 to 4 Seats | |||

| 5 to 6 Seats | |||

| More than 6 Seats | |||

| By Range | Intracity (Less than 50 km) | ||

| Short Intercity (50 to 150 km) | |||

| Regional (150 to 300 km) | |||

| Extended (More than 300 km) | |||

| By End-Use | Airport Shuttle | ||

| On-Demand Air Taxi | |||

| Corporate Shuttle | |||

| Emergency Medical Services | |||

| Tourism and Sightseeing | |||

| By Lift Technology | Multicopter | ||

| Tilt-Rotor | |||

| Lift + Cruise | |||

| Ducted Fan Jet | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the air taxi market in 2026?

The air taxi market size is valued at USD 4.47 billion in 2026.

What growth rate is projected through 2031?

Revenue is expected to rise at a 18.79% CAGR, reaching USD 10.56 billion by 2031.

Which region will see the fastest expansion?

Asia-Pacific is forecasted to grow at a 25.20% CAGR, driven by supportive Chinese and Japanese policies.

What propulsion technology will dominate longer routes?

Hydrogen fuel-cell aircraft are advancing at a 20.85% CAGR, offering 150 km-plus range advantages over battery-only models.

What is the main regulatory hurdle?

Certification of advanced flight-control software remains the biggest bottleneck, capable of adding two–three years to approval timelines.

How concentrated is competition among eVTOL makers?

The field is highly fragmented; no single player holds more than 15% share, resulting in a concentration score of 3/10.

Page last updated on: