Air Cushion Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 6.95 Billion |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Cushion Packaging Market Analysis by Mordor Intelligence

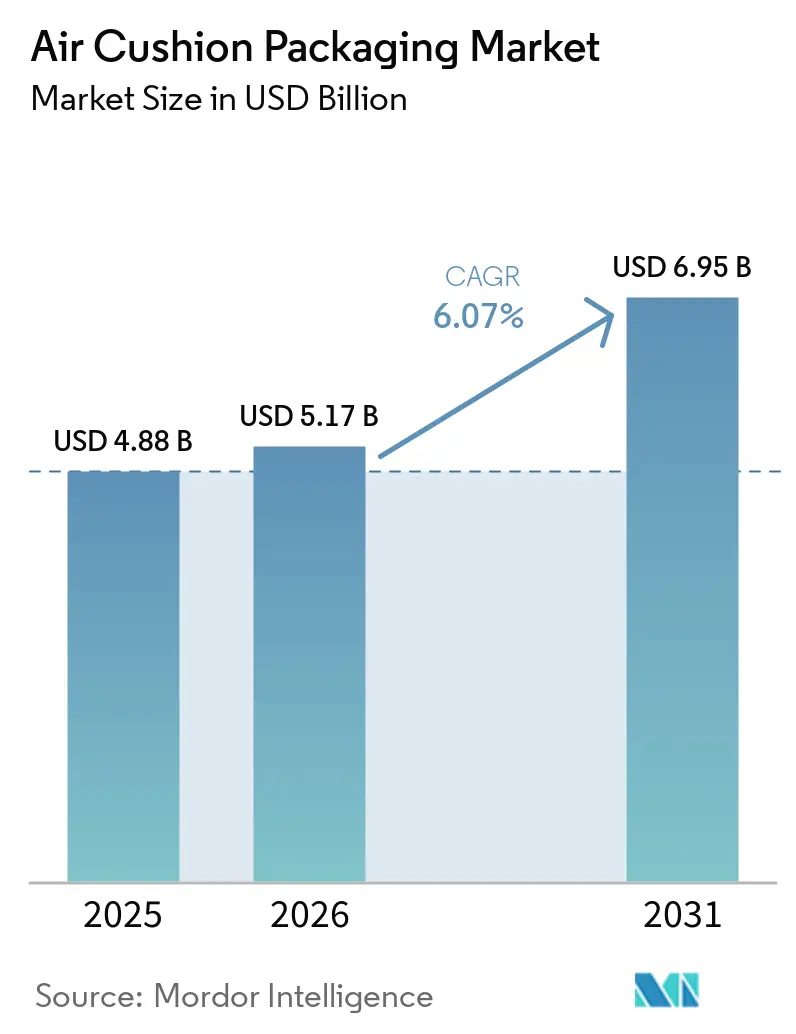

The air cushion packaging market size is expected to grow from USD 4.88 billion in 2025 to USD 5.17 billion in 2026 and is forecast to reach USD 6.95 billion by 2031 at 6.07% CAGR over 2026-2031. The air cushion packaging market is being shaped by rising parcel volume, broader warehouse automation, and tighter rules on plastic waste, which together sustain demand even as material preferences shift. The shift away from conventional PE air pillows toward paper-based, recycled-content, and bio-based formats is reducing part of the legacy volume base, but it is also creating higher-value product space for suppliers that can combine protection performance with compliance. The air cushion packaging market is also seeing greater differentiation between companies that sell integrated inflation systems and film consumables, and those that compete mainly on film price. That pattern favors suppliers with installed machine bases, service coverage, and proprietary formats because replacement decisions tend to affect both equipment and consumables simultaneously. The air cushion packaging market will continue to find opportunities in specialized fulfillment environments, especially where fragile products, cold-chain shipping, and right-sized packaging programs require more precise protective formats.

Key Report Takeaways

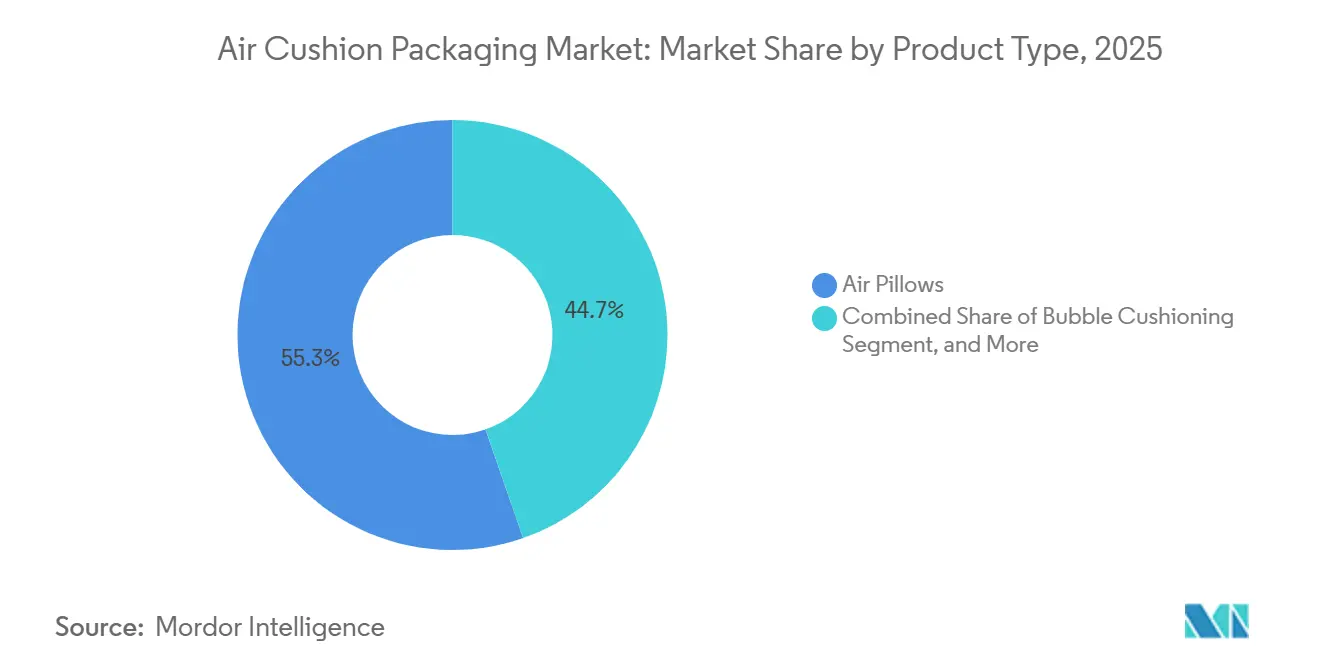

- By product type, air pillows accounted for 55.34% of the air cushion packaging market share in 2025.

- By material type, the air cushion packaging market for polylactic acid and starch blends is projected to grow at a 7.13% CAGR through 2031.

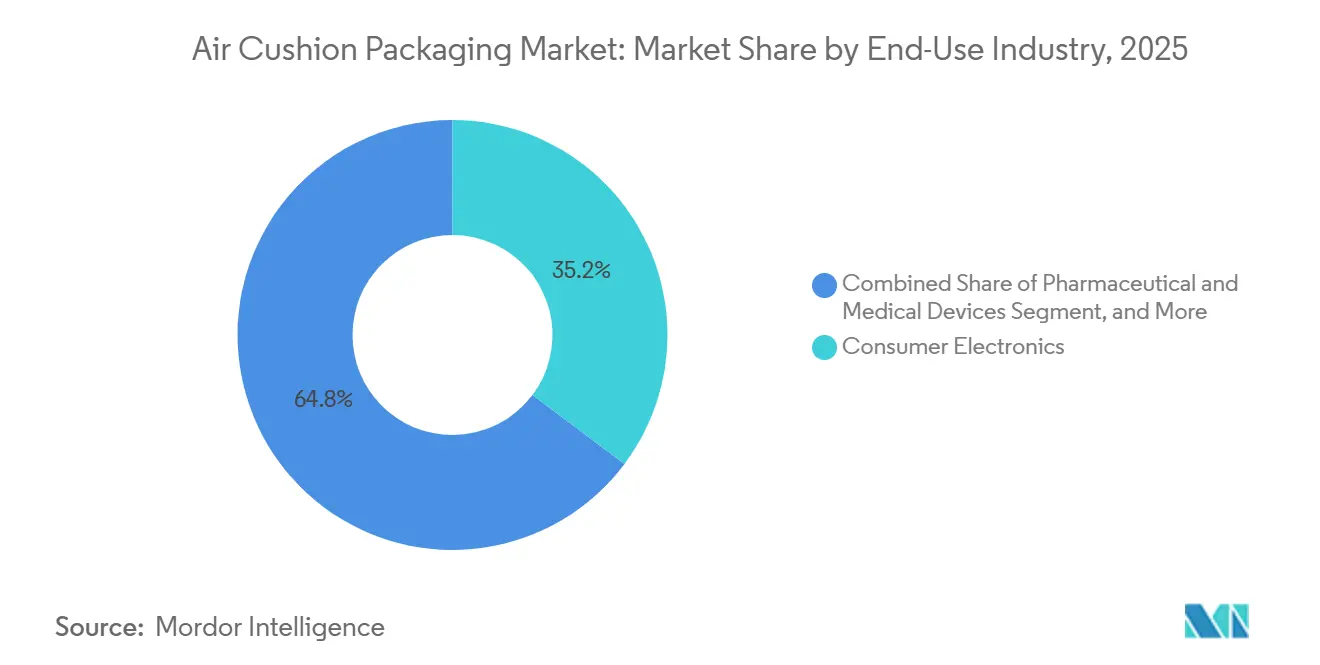

- By end-use industry, consumer electronics accounted for 35.24% of the air cushion packaging market in 2025.

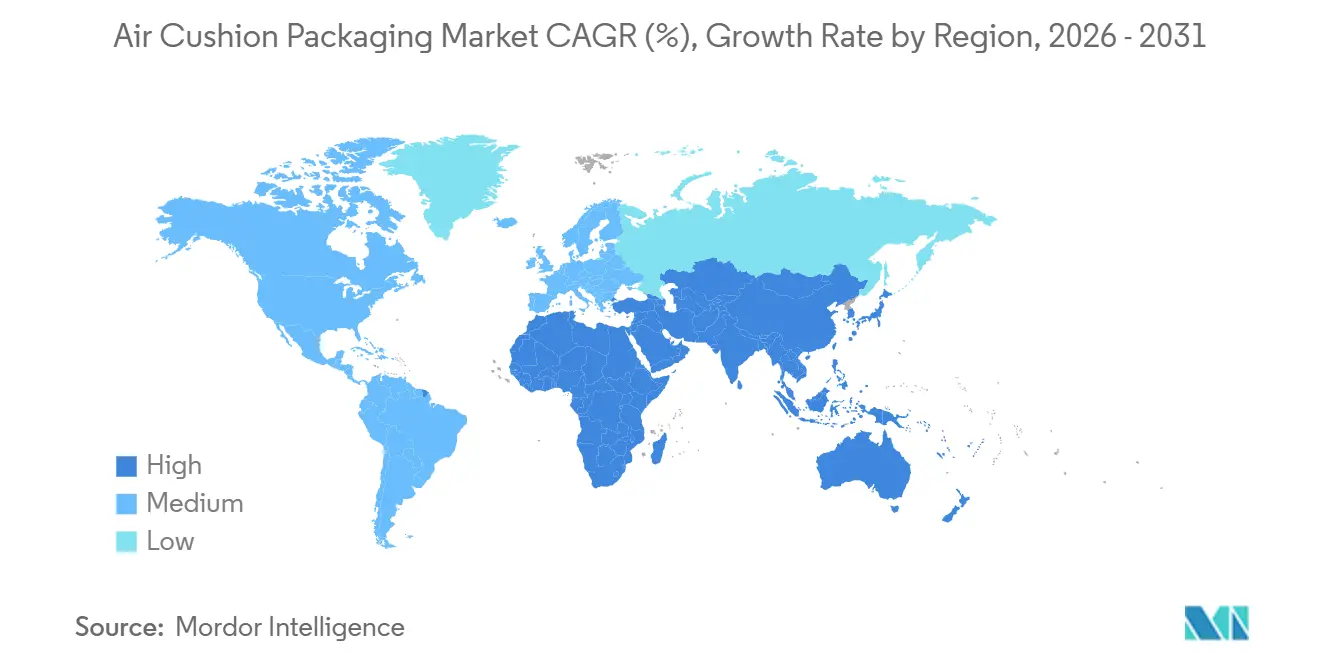

- By geography, the air cushion packaging market for Asia-Pacific is projected to grow at a 7.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air Cushion Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel Growth and Damage Prevention Needs | +2.2% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Warehouse Automation and On-Demand Inflation Adoption | +1.2% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Recycled-Content and Recyclable Film Innovation | +0.7% | Global, strongest in the EU and North America | Medium term (2-4 years) |

| Freight Weight and Cube Reduction Priorities | +0.5% | Global, strongest in North America and the EU | Short term (≤ 2 years) |

| Pack-Station Space Compression and SKU Rationalization | +0.3% | North America and the EU core, spill-over to APAC | Medium term (2-4 years) |

| Precision Void-Fill Optimization for Right-Sized Packaging Operations | +0.2% | Global, concentrated in the EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel Growth and Damage Prevention Needs

Rising online order volumes remain the strongest demand base for the air cushion packaging market, as each additional shipment creates another need for transit protection. The pressure increases as basket sizes shrink and shipments contain fewer items, because loosely packed cartons are more prone to movement and breakage than dense multi-item orders. That makes the air cushion packaging market more relevant in categories where product damage quickly turns into returns, replacement costs, and customer service expenses. Amazon's earlier use of plastic air pillows at very large scale showed how central inflatable void-fill had become in high-throughput fulfillment before the company moved to another material path. The economic logic remains favorable for suppliers that can provide precise cushioning with low material use, because protective packaging still costs far less than reverse logistics and product loss. In the air cushion packaging market, this keeps demand tied not only to parcel growth itself but also to the cost of avoiding preventable damage in high-volume shipping networks.

Warehouse Automation and On-Demand Inflation Adoption

Warehouse automation is changing how the air cushion packaging market is deployed across fulfillment centers, not just how much material is used. A 2025 warehouse automation study indicated that 37% of surveyed logistics operators planned to implement automation as a core operational improvement, which supports continued interest in inline protective packaging systems. In practice, automated lines favor on-demand inflation because they reduce storage requirements, lower the risk of deflation before use, and allow output to more closely match carton requirements. Storopack expanded its module in September 2025 with AI-powered vision scanning that calculates void volumes before dispensing air or paper padding, which reflects the direction of the air cushion packaging market toward higher accuracy and lower waste. The air cushion packaging market also benefits from the fact that machine installations often lead to recurring consumable purchases, which strengthens supplier retention and raises switching costs after a system is in place. As more fulfillment operators automate pack stations, the air cushion packaging market is likely to reward suppliers that combine hardware reliability, software control, and film performance in a single offering.

Recycled-Content and Recyclable Film Innovation

Recycled-content and recyclable film development is moving the air cushion packaging market away from a narrow cost discussion and toward compliance-ready product design. Pregis expanded its AirSpeed Renew PCR portfolio in September 2024 with films containing 80% post-consumer recycled content and reported a carbon footprint reduction of more than 40% compared with virgin-resin equivalents.[1]Pregis, “Pregis Expands AirSpeed Renew PCR Portfolio with New Sustainable Films,” Pregis, pregis.com Storopack achieved full RecyClass certification for all its recycled air cushion films in May 2025, aligning its offering with the EU Packaging Framework's recyclability requirements. The European Commission has also set a clear compliance path through Regulation (EU) 2025/40, including recycled-content targets for plastic packaging and full recyclability requirements that apply to packaging placed on the EU market from August 2026. This matters for the air cushion packaging market because it allows suppliers to protect volumes inside the broader shift away from conventional flexible plastics. It also supports premium pricing where film design, certification, and reporting help customers reduce regulatory risk.

Freight Weight and Cube Reduction Priorities

Freight cost pressure continues to support the air cushion packaging market, as inflatable formats offer protection with very little material weight. The logic is especially strong when shippers compare air-filled formats with heavier paper or foam solutions across long transport routes and multi-node distribution networks. US, Canada, and Mexico cross-border freight reached USD 1.6 trillion in 2024, up 1.8%, and land transport accounted for 77.1% of total freight value, underscoring the size of the cost-sensitive logistics base in North America. The air cushion packaging market also benefits when operators try to reduce dimensional weight exposure through tighter pack design, because inflatable systems can fill remaining gaps without adding much mass. At the same time, the air cushion packaging market is being pushed to use less excess void, as regulators increasingly link packaging efficiency to waste reduction. The result is a more selective growth pattern, with suppliers that help customers manage both cube and protection better placed than those that rely on high fill volumes alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Amazon's North America Plastic Air Pillow Phaseout | -0.4% | North America (US, Canada, Mexico) | Short term (≤ 2 years) |

| EU Empty-Space and EPR Rules | -0.3% | EU-27 and the United Kingdom | Medium term (2-4 years) |

| Plastic Waste Scrutiny and Flexible-Film Recycling Gaps | -0.2% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Resin Price Volatility and Equipment Switching Costs | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Amazon's North America Plastic Air Pillow Phaseout

Amazon completed the replacement of 95% of plastic air pillows with 100% recycled paper filler in North America by mid-2024 and reached full elimination by the end of 2024, removing an estimated 15 billion plastic air pillows a year from around 2 billion shipments. This is a meaningful restraint on the air cushion packaging market because it shows that one large buyer can quickly reset material demand across a major fulfillment network. The transition also mattered beyond Amazon's own procurement because sellers and service partners inside the same logistics ecosystem faced pressure to align their own packaging choices with the platform's direction. The air cushion packaging market therefore lost part of a large-volume North American void-fill pool even though broader demand for protective packaging remained intact. Amazon had already phased out plastic air pillows in Europe in 2022 and in India in 2020, which reinforced the signal that large e-tailers may continue to reduce exposure to conventional plastic air formats. For the air cushion packaging market, this increases the urgency of shifting toward recyclable, paper-hybrid, and other compliance-friendly formats rather than relying on legacy PE air pillows.

EU Empty-Space and EPR Rules

The EU Packaging and Packaging Waste Regulation 2025/40 entered into force on February 11, 2025, and applies from August 12, 2026, creating the most important packaging-minimization framework yet for the air cushion packaging market in Europe. Article 24 sets a maximum 50% void space ratio for e-commerce, grouped, and transport packaging by January 1, 2030, and the Commission's guidance explicitly treats filling materials such as air cushions, bubble wrap, foam, and paper padding as empty space. The regulation also requires effective penalties and strengthens producer responsibility obligations, which raises the cost of keeping harder-to-recycle formats in market circulation. For the air cushion packaging market, the practical effect is that demand growth in Europe will depend more on right-sized packaging design and certified recyclable formats than on simple fill volume. Similar fee-based pressure is also emerging in the United Kingdom, which adds another layer of commercial risk for conventional PE air pillows. This means the air cushion packaging market will still find opportunities in Europe, but they will increasingly sit in redesigned systems that minimize empty space and improve material recovery outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Air Pillows Lead While Bubble Cushioning Expands Faster

Air pillows held 55.34% of the air cushion packaging market share in 2025, which kept them well ahead of the other product types. Their lead came from flat-pack storage efficiency, compatibility with automated inline inflation, and a low cost-per-cubic-foot protection profile that remains attractive in high-volume fulfillment. The air cushion packaging industry also favors this format because deflated film rolls use far less floor space than pre-inflated stock, which helps operators simplify pack-station replenishment. Proprietary machine ecosystems from leading suppliers strengthen that position because customers often buy the hardware, film, and service model together. This installed base advantage keeps air pillows firmly embedded in the air cushion packaging market, even as material preferences evolve.

Bubble cushioning is projected to expand at 6.75% CAGR through 2031, making it the fastest-growing product category in the air cushion packaging market. Its appeal lies in its dual-use performance: it can serve as both void fill and surface wrap for shipments that require scratch protection and impact absorption. Air tubes and inflatable air bags remain smaller in revenue terms, but they are gaining ground in industrial equipment and pharmaceutical device transport where axial load distribution matters more than simple gap filling. Storopack's AIRfiber launch in February 2025 also showed that the air cushion packaging market is moving toward paper-based hybrid formats that blur the old line between inflatable plastic protection and recyclable paper solutions.[2]Storopack, “AIR Pillows Made of Paper, AIRfiber,” Storopack, storopack.com That convergence gives brand owners a way to preserve cushioning performance while adapting the air cushion packaging market to stricter recyclability expectations.

By Material Type: PE Remains the Base While Bio-Based Films Move Faster

Polyethylene retained a 52.64% revenue share in 2025, making it the anchor material in the air cushion packaging market. Its position reflects cost efficiency, heat-sealability, clarity, and compatibility with high-speed inflation systems that rely on consistent film performance during sealing and chamber formation. The air cushion packaging industry is not treating polyethylene as a single, static category, because pressure is strongest on virgin polyethylene, while recycled-content polyethylene and mono-material polyethylene structures are improving their position within the same material family. PP remains useful where higher stiffness and puncture resistance matter, especially in heavier industrial transit applications. PET continues to serve niche uses where clarity is important alongside cushioning performance.

Polylactic acid and starch blends formulations are forecast to grow at 7.13% CAGR through 2031, making them the fastest-growing material group in the air cushion packaging market. Storopack launched FOAMplus 7008-BIO in November 2025, with more than 83% certified bio-based carbon content in its B-Component, demonstrating that bio-based protective packaging is reaching commercially viable performance levels. The commercial push behind this shift is reinforced by EU rules that combine recyclability requirements with recycled-content targets and future performance grades for packaging design. In the air cushion packaging market, that framework supports continued substitution toward materials that can help brand owners meet regulatory and procurement goals without giving up transit protection.

By End-Use Industry: Consumer Electronics Holds Scale While Beauty Products Grow Faster

Consumer electronics accounted for 35.24% of revenue in 2025, making it the largest end-use category in the air cushion packaging market. This leadership is tied to the category's sensitivity to shock, vibration, and handling damage during express shipping, especially in cross-border channels. Inflatable formats remain well-suited to these shipments because they can provide non-conductive protection options and distribute impact energy across multiple chambers. The air cushion packaging market also benefits from the fact that electronics shipments often move through automated, tightly timed fulfillment systems, where consistent pack formats matter. That keeps consumer electronics as a stable demand anchor even as material choices change.

Personal care and cosmetics are forecast to expand at 7.82% CAGR through 2031, making it the fastest-growing end-use segment in the air cushion packaging market. Premium beauty shipments often use glass and ceramic packaging, which increases breakage costs in direct-to-consumer channels where returns are expensive and product presentation matters. Suppliers in the air cushion packaging market are benefiting from demand for precision-fit inflatable solutions that reduce movement without adding excessive box weight or bulk. Pharmaceutical and medical device shipments are also becoming more important, while home décor, furnishings, and automotive continue to provide steady demand for specialized inflatable air bags and tube formats. Together, these patterns broaden the air cushion packaging market beyond standard e-commerce void-fill and support demand in applications where the value of damage prevention is high.

Geography Analysis

Asia-Pacific led the air cushion packaging market with 39.14% revenue share in 2025 and is also expected to post the fastest regional CAGR at 7.66% through 2031. The region benefits from a large manufacturing base, robust export activity, and a broad e-commerce fulfillment network, which continues to drive demand for protective packaging across multiple product categories. China remains the central contributor because of its scale in online retail logistics and electronics production, which supports both standard void-fill demand and more specialized inflatable formats. India is becoming an important growth engine as pharmaceutical manufacturing, organized retail logistics, and domestic packaging capability continue to expand. Japan and South Korea add stable demand for precision protective solutions in electronics and semiconductor-related shipments, which keeps the air cushion packaging market tied to higher-value industrial uses as well as volume fulfillment demand.

North America remained the second-largest regional market for air cushion packaging. The United States anchors the region, but Amazon's full North American phaseout of plastic air pillows by the end of 2024 created a near-term headwind for conventional plastic void-fill demand and redirected attention toward recyclable and right-sized alternatives. At the same time, the region still offers a large logistics base, and US, Canada, and Mexico freight flows remained substantial at USD 1.6 trillion in 2024, which supports the use of lightweight protective formats across integrated distribution networks. Mexico is also gaining attention as a nearshoring hub, which adds new fulfillment and packaging demand nodes for the air cushion packaging market.

Europe is the geography most directly shaped by regulation in the air cushion packaging market because PPWR 2025/40 changes both packaging design priorities and material economics. Germany remains a leading European demand center, while the United Kingdom, France, and the Benelux countries continue to matter because major suppliers already have dense service and distribution coverage across those markets.[3]European Commission, “Packaging Waste - Environment,” European Commission, environment.ec.europa.eu The Commission's guidance makes it clear that void-fill materials count toward empty-space limits, which will push customers toward more precise packaging systems and higher-recyclability formats from August 2026 onward. South America and the Middle East and Africa remain smaller in absolute scale, but they still offer moderate growth opportunities as suppliers look for diversification beyond mature core regions.

Competitive Landscape

The air cushion packaging market is moderately concentrated globally, with Sealed Air Corporation, Pregis LLC, and Storopack Hans Reichenecker GmbH holding durable positions through hardware-film bundles that tie machine placements to recurring consumable sales. This model gives leading suppliers an advantage because customers often face format incompatibility, retraining needs, and service disruptions when considering switching providers. Sealed Air Macfarlane Group represents the service-led mid-tier approach, and its 2025 annual report showed GBP 300.8 million (USD 381.3 million) in revenue while also highlighting a customer project that removed 178 tonnes of packaging material each year through void-space optimization.[4]Sealed Air Corporation, “Sealed Air to Be Acquired by CD&R for USD 10.3 Billion,” Sealed Air, sealedair.com Regional Asian manufacturers continue to compete aggressively on film pricing, which keeps the air cushion packaging market competitive even where global players hold stronger system positions.

A second layer of competition in the air cushion packaging market is now forming around material circularity and packaging intelligence. Storopack's AIRfiber launch in February 2025 gave the company an early position in paper-based air pillows certified for paper-stream recycling, directly addressing the compliance requirements of European customers. Storopack also secured full RecyClass certification for all its recycled air cushion films in May 2025, which strengthened its standing in the recyclable film segment of the air cushion packaging market. Pregis expanded its paper manufacturing footprint in September 2025 with a 477,000-square-foot converting center in Illinois that can produce more than 1 billion curbside recyclable paper packaging solutions a year, showing how suppliers are preparing for broader substitution away from conventional plastic formats.

Competition in the air cushion packaging market is therefore moving beyond film price alone and toward measurable system value. Suppliers that can help customers reduce material use, meet reporting requirements, and maintain damage-prevention performance are in a better position than suppliers that compete only on consumable cost. The air cushion packaging market is also seeing more overlap between paper-based protective products and inflatable systems, which broadens the competitive field and raises the importance of application engineering. Overall, the air cushion packaging market remains open enough for regional challengers to win price-sensitive business, but the installed machine base, service reach, and compliance-ready product portfolios of leading companies still create meaningful barriers to rapid share shifts.

Air Cushion Packaging Industry Leaders

Sealed Air Corporation

Smurfit Westrock plc

Macfarlane Group UK Ltd

Pregis LLC

Aeris Protective Packaging Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit Westrock launched ActiBlu, a glueline-free, water-activated adhesive packaging solution at its 2026 Innovation Event in the Netherlands, reducing adhesive use by up to 60% relative to traditional hot-melt gluing and improving recyclability of paper-based secondary packaging.

- March 2026: Pregis expanded its wind energy program to cover 100% of electricity consumed at 22 US manufacturing facilities, reducing an estimated 11,700 metric tons of market-based Scope 2 emissions in 2025, approximately 20% of the company's total Scope 2 footprint, advancing its 2040 net-zero commitment.

- November 2025: Sealed Air Corporation announced a definitive agreement to be acquired by CD&R for USD 10.3 billion, representing a 41% premium to its unaffected stock price as of August 14, 2025, the transaction, approved by Sealed Air shareholders in February 2026 and by the European Commission, is expected to close in mid-2026 and will take Sealed Air private.

- November 2025: Storopack launched RENATURE® Honeycomb, a protective packaging solution combining honeycomb paper panels with vegetable starch-based shock absorbers, certified recyclable under the CEPI method by Interzero, the product uses 43% less water, 38% fewer resources, and emits 32% less CO2 than conventional honeycomb panels.

Global Air Cushion Packaging Market Report Scope

The scope of the report includes an analysis of the air cushion packaging market, which refers to the use of air-filled cushions as protective packaging materials. These cushions are designed to safeguard products during storage and transportation by providing shock absorption and minimizing damage. The study covers market trends, growth drivers, challenges, and opportunities, along with a detailed examination of the supply chain, competitive landscape, and key market players.

The Air Cushion Packaging Report is Segmented by Product Type (Air Pillows, Bubble Cushioning, and Air Tubes), Material Type (Polyethylene, Polypropylene, Polyethylene terephthalate, and Polylactic Acid and Starch Blends), End-Use Industry (E-commerce, Consumer Electronics, Food and Beverages, Pharmaceutical and Medical Devices, Personal Care and Cosmetics, Home Decor and Furnishings, Automotive, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Air Pillows |

| Bubble Cushioning |

| Air Tubes |

| Polyethylene |

| Polypropylene |

| Polyethylene terephthalate |

| Polylactic Acid and Starch Blends |

| Food and Beverages |

| Consumer Electronics |

| E-commerce |

| Pharmaceutical and Medical Devices |

| Personal Care and Cosmetics |

| Home Decor and Furnishings |

| Automotive |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Air Pillows | ||

| Bubble Cushioning | |||

| Air Tubes | |||

| By Material Type | Polyethylene | ||

| Polypropylene | |||

| Polyethylene terephthalate | |||

| Polylactic Acid and Starch Blends | |||

| By End-Use Industry | Food and Beverages | ||

| Consumer Electronics | |||

| E-commerce | |||

| Pharmaceutical and Medical Devices | |||

| Personal Care and Cosmetics | |||

| Home Decor and Furnishings | |||

| Automotive | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the air cushion packaging market?

The air cushion packaging market stood at USD 4.88 billion in 2025, is valued at USD 5.17 billion in 2026, and is projected to reach USD 6.95 billion by 2031 at a 6.07% CAGR.

Which product type leads demand for air cushion packaging?

Air pillows led the air cushion packaging market in 2025 with a 55.34% revenue share because they fit automated inflation systems and use very little storage space before inflation.

Which material category is growing the fastest in protective inflatable packaging?

Polylactic Acid and Starch Blends formulations are the fastest-growing material segment, with a projected 7.13% CAGR through 2031, supported by compliance pressure and sustainability procurement goals.

Why is Asia-Pacific ahead in this space?

Asia-Pacific held 39.14% of 2025 revenue and is also forecast to grow the fastest at 7.66% CAGR, supported by its manufacturing base, export activity, and large fulfillment network.

What is the main risk facing suppliers of conventional plastic air pillows?

The biggest near-term pressure comes from material substitution and packaging rules, especially Amazon's North America phaseout of plastic air pillows and the EU's tighter empty-space and recyclability requirements.

Which end-use segment is expanding the fastest?

Personal care and cosmetics is projected to grow at 7.82% CAGR through 2031 because premium, fragile packaging in direct-to-consumer channels needs precise protection and has high breakage costs.

Page last updated on: