Aluminum Foil Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.63 Billion |

| Market Size (2031) | USD 38.56 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Foil Packaging Market Analysis by Mordor Intelligence

The aluminum foil packaging market size in 2026 is estimated at USD 30.63 billion, growing from 2025 value of USD 29.25 billion with 2031 projections showing USD 38.56 billion, growing at 4.72% CAGR over 2026-2031. Demand momentum arises from the material’s barrier properties that limit oxygen, moisture, and light ingress, safeguarding food shelf life and pharmaceutical efficacy. Electric-vehicle battery pouches, reflective films for vertical farming, and e-commerce heat-seal liners widen the application base, keeping capacity-addition plans active among Tier-1 producers. Raw aluminum price swings and stricter European recycling mandates introduce near-term cost pressure, yet integrated smelter-to-foil strategies protect margins for leading converters. Rising disposable incomes in Asia-Pacific and growing pharmaceutical output in India and China underpin volume resilience even as bio-based barrier films nibble at less demanding niches.

Key Report Takeaways

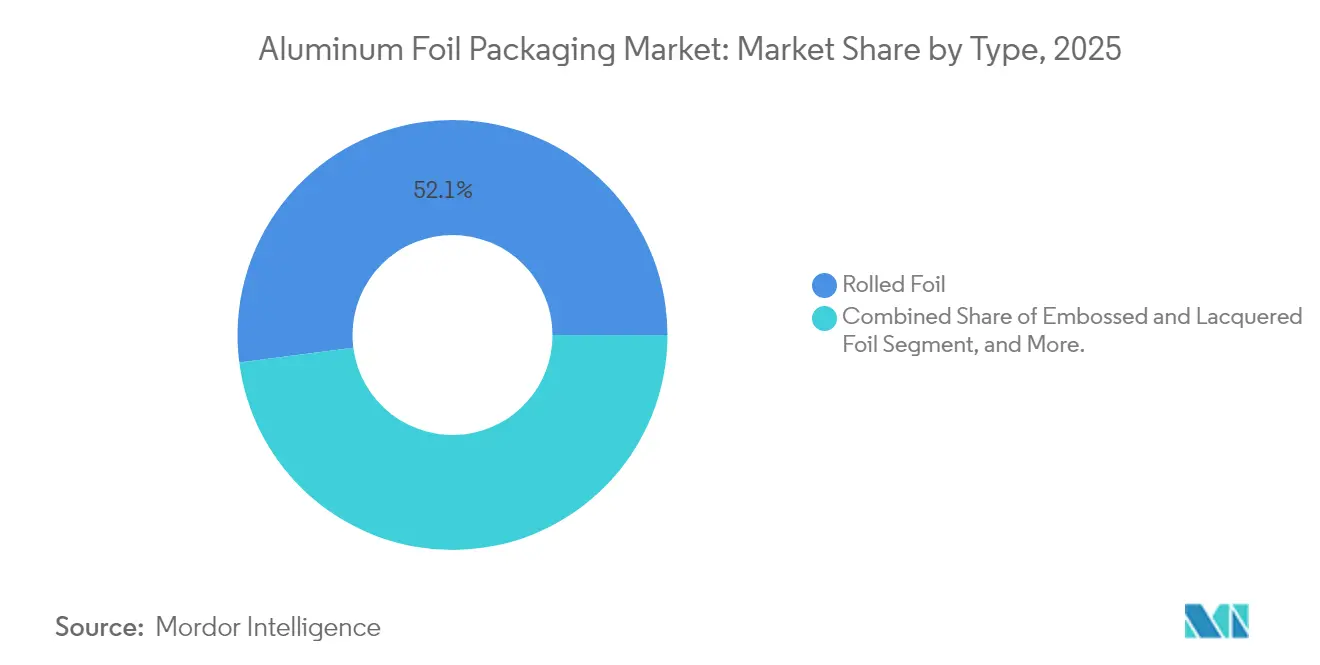

- By type, rolled foil commanded 52.05% of the aluminum foil packaging market share in 2025, while backed foil is forecast to expand at a 4.98% CAGR through 2031.

- By application, converter foils led with 41.01% revenue in 2025, and container foils are set to post a 5.71% CAGR to 2031.

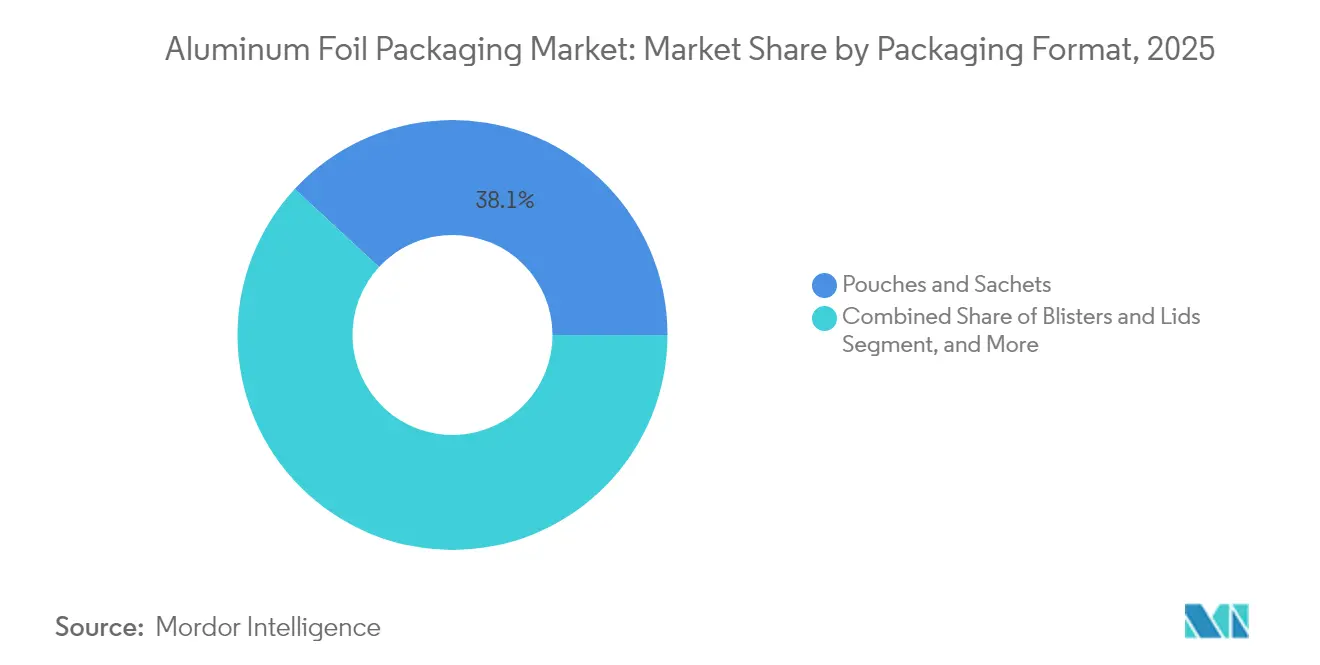

- By packaging format, pouches and sachets held 38.12% of 2025 revenue, and blisters and lids are projected to grow at a 5.86% CAGR until 2031.

- By end user, food applications accounted for 32.15% of 2025 sales, whereas pharmaceutical packaging is poised for a 6.41% CAGR until 2031.

- By geography, Asia-Pacific dominated with 39.88% revenue in 2025; the Middle East and Africa is expected to record a 6.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminum Foil Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for ready-to-eat and convenience foods | +1.2% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Growth in pharmaceutical blister demand | +0.8% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Superior barrier properties and shelf-life extension | +0.9% | Global | Long term (≥ 4 years) |

| Induction heat-seal liners for e-commerce liquids | +0.4% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| EV battery pouch-foil adoption | +0.3% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Vertical-farming reflective foil demand | +0.2% | North America and Europe, emerging in Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Ready-to-Eat and Convenience Foods

Convenience-oriented lifestyles elevate consumption of heat-and-eat meals, baked goods, and deli products. Aluminum foil’s thermal conductivity enables uniform reheating up to 200 °C, adding value for foodservice trays, lidding films, and retort pouches. In Saudi Arabia, packaged food retail sales are projected to reach USD 34.2 billion by 2028, 38% above 2024 levels.[1]Food Export–Midwest and Food Export–Northeast, “2025 UES Middle East Market Assessment,” foodexport.org Volume upticks translate directly into higher foil tonnage for trays and lidding. Major processors in North America and Asia-Pacific embed foil trays into chilled and frozen meal lines, reinforcing bulk procurement contracts that stabilize converter order books.

Growth in Pharmaceutical Blister Demand

Cold-form aluminum foil of 20-25 microns thickness offers unrivaled moisture and oxygen barriers, preserving drug potency across harsh climates. The U.S. FDA’s emphasis on stability data propels the adoption of deeper-draw blister formats that require ductile, scratch-free foil grades.[2]Speira, “Aluminium Foil for Medical and Pharmaceutical Packaging,” speira.com Emerging generics hubs in India and Indonesia commission new blister lines, raising call-off volumes for coated and laminated foil reels. Premium pricing in this segment cushions converters against metal price volatility.

Superior Barrier Properties and Shelf-Life Extension

Aluminum foil forms an impermeable layer that blocks gases, UV radiation, and aromatic migration, critical for extended supply chains. Food processors leverage the barrier to eliminate preservatives, aligning with clean-label trends. Shelf-life gains are especially valuable in humid regions where polymer films face permeability spikes. Converters therefore market foil-based laminate rolls as a waste-reduction tool that complements corporate sustainability pledges.

Induction Heat-Seal Liners for E-Commerce Liquids

Rapid e-commerce penetration raises leakage-prevention standards for edible oils, nutraceutical liquids, and OTC syrups. Aluminum induction liners create hermetic seals and tamper evidence, improving brand reputation in last-mile delivery. North American nutraceutical fillers reported double-digit growth in foil-seal demand for 2024, a pattern now mirrored by Southeast Asian cosmetics exporters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative bio-based flexible materials | -0.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Raw aluminum price volatility | -0.8% | Global | Short term (≤ 2 years) |

| Stricter EU recycling targets on foil scrap | -0.4% | Europe, influencing global standards | Long term (≥ 4 years) |

| ESG risks from energy-intensive smelting | -0.5% | Global, largest in coal-reliant regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Alternative Bio-Based Flexible Materials

Brands targeting eco-conscious consumers explore paper-foil hybrids and compostable barrier films. In snacks and confectionery, moderate oxygen protection suffices, allowing partial substitution. While bio-films cannot yet equal foil’s full barrier profile, marketing narratives around renewability accelerate trials in Europe and North America. The threat intensifies once recycling legislation rewards renewable inputs through tax incentives or labeling advantages.

Raw Aluminum Price Volatility

Energy costs, trade sanctions, and shifts in Chinese export policy drive LME aluminum fluctuations that compress converter margins. China’s 2024 removal of foil export tax rebates re-routed supply flows and lifted spot premiums in Europe. Converters hedge metal exposure via long-term supply agreements with integrated smelters, yet smaller players face tighter working capital cycles, occasionally prompting material light-weighting or temporary production curtailments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type : Rolled Foil Retains Scale Advantage

Rolled Foil captured 52.05% of 2025 revenue, anchoring the aluminum foil packaging market through its role as feedstock for printing, laminating, and forming lines. The output spectrum spans 6-micron household sheets to 200-micron industrial grades, letting suppliers tailor gauge to end-use. Strong converter demand keeps mills in China, India, and Germany running near 90% capacity utilization. The aluminum foil packaging market size attributed to Backed Foil is projected to widen at a 4.98% CAGR as pharmaceutical cold-form and premium coffee capsule demand reward laminate designs.

Embossed and Lacquered variants address decorative confectionery wraps and tamper-evident lidding, generating niche price premiums. Seasonal patterns, such as holiday-pattern foil launched by Reynolds Consumer Products in November 2024, illustrate how surface texture and color enhance shelf appeal. Other Types, including perforated ventilation foils and capacitor foils, remain small but technically stringent, reinforcing supplier specialization.

By Application : Converter Foils Form Market Core

Converter Foils generated 41.01% of 2025 sales, confirming their place at the center of the aluminum foil packaging market. Laminators and printers transform master coils into rollstock for pouches, sachets, and cartons, driving consistent tonnage flow. Rising adoption of solvent-free adhesives and electron-beam curing elevates functional layering without sacrificing throughput. Container Foils, mainly for trays and semi-rigid dishes, are forecast at a 5.71% CAGR as ready-to-eat meals penetrate emerging middle-income urban zones.

Household Foil remains a legacy staple, held in 95% of U.S. kitchens per Reynolds Consumer Products’ internal data. Volume is flat in mature markets but expands in Africa and South Asia, where consumer foil rolls still gain first-time buyers. Industrial and Insulation Foils link demand to building energy codes that specify reflective barriers in HVAC and roofing, a niche yet resilient outlet during construction cycles.

By Packaging Format : Pouches Dominate Flexible Demand

Pouches and Sachets accounted for 38.12% of 2025 revenue thanks to single-serve coffee, gel supplements, and instant condiments. Lightweight, easy-tear formats lower logistics emissions, helping brand owners reach scope-3 reduction targets. Blisters and Lids will record the fastest 5.86% CAGR, propelled by pharmaceutical serialization mandates that favor individual dose visibility. The aluminum foil packaging market size for tray formats also grows as dark kitchens and airline caterers standardize foil containers for reheating safety.

Wraps keep relevance in restaurant and arthouse bakery segments, but polymer cling films bite into lower-barrier needs. Continuous-cast tray blanks enter the supply for airline catering, merging weight reduction with rigidity. Format diversification permits converters to balance order pipelines, reducing reliance on any single downstream sector.

By End User : Food Holds Volume Leadership

Food applications delivered 32.15% of 2025 turnover, benefiting from aluminum’s FDA-cleared food-contact status and temperature resilience during retort. The aluminum foil packaging market share held by Pharmaceuticals rose steadily as blister infrastructure in Vietnam, Egypt, and Brazil scaled up. Generic producers specify 25-micron coated foil with push-through resistance, creating high-margin reels for converters.

Beverage closures exploit foil’s malleability for roll-on aluminum caps, yet total foil tonnage is minor versus cans. Cosmetics adopt foil-laminated sachets for high-sensitivity serums, extending shelf life once opened. Tobacco foil inner liners decline in the European Union under plain-pack regulations, offset by stable demand in Indonesia and Nigeria.

Geography Analysis

Asia-Pacific contributed 39.88% of the 2025 value, driven by China’s integrated smelter-converter clusters and India’s USD 10 billion Hindalco capacity expansion aimed at battery foil lines. Lower freight costs and proximity to bauxite mines reinforce export competitiveness despite occasional power-price spikes. The aluminum foil packaging market size attached to the region is set for mid-single-digit growth, underpinned by processed food uptake and vaccine production localization.

North America remains technology-led, hosting advanced scrap-sorting plants that lift post-consumer foil recovery yields above 35%. U.S. consumption benefits from chilled-meal subscriptions and nutraceutical liquids shipped in induction-sealed jars. Canada’s maple-products sector likewise shifts from glass to foil laminate pouches to trim freight weights.

Europe faces the tightest regulatory lens under the Packaging and Packaging Waste Regulation. Mandatory minimum recycled content targets spur investments in continuous pyrolysis and de-lacquering units that reclaim clean aluminum for remelt. While compliance costs strain small converters, multinational groups use closed-loop programs such as Austria’s coffee-capsule recycling pilot that collected 5 million units in three months. The Middle East and Africa, expanding at 6.78% CAGR, leverages food-processing FDI and burgeoning pharmaceutical clusters in Saudi Arabia and Egypt that require high-barrier packs to suit hot-climate logistics.

Regulatory Landscape

Food-contact and packaging compliance for aluminum foil continues to be shaped by chemical-safety rules alongside packaging waste mandates. In the European Union, the Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40) starts applying from August 2026, tightening requirements relevant to foil laminates and lidding through measures such as a 100 mg/kg cap on the sum of heavy metals (cadmium, lead, mercury, hexavalent chromium) in packaging and new limits on PFAS in food-contact packaging. For converters serving EU food and pharma customers, these changes increase testing and documentation burdens, particularly for multilayer structures where inks, coatings, and adhesives sit adjacent to the foil layer.

Outside Europe, standards and enforcement are also becoming more test-driven for cross-border trade. In Japan, JIS S 2029:2026 (METI) introduces batch-level oxygen transmission rate (OTR) reporting expectations for food packaging aluminum foil composite films exported into the country, which elevates the need for JIS-certified laboratory reporting from suppliers. In the United States, FDA food additive regulations for indirect additives used in metallic foil manufacturing (including 21 CFR 178.3910 for surface lubricants used during rolling or forming) remain a key baseline for food-contact foil, reinforcing process control over rolling oils and residuals when supplying food, nutraceutical, and pharmaceutical packaging streams.

Value Chain Analysis

The aluminum foil packaging value chain runs from upstream bauxite and alumina, through primary aluminum smelting, to midstream casting and rolling into thin-gauge foil, and then into downstream converting where printing, coating, laminating, and forming turn master coils into packaging formats such as pouches and sachets, blisters and lidding, and trays and containers. Critical process inputs include rolling oils and lubricants, as well as coatings, primers, and adhesives that enable heat sealability and barrier retention in laminate structures. Compliance constraints on these chemistries link manufacturing choices directly to food-contact and pharma-packaging requirements.

Downstream, converters sell to brand owners and packers in food, beverage, pharmaceuticals, cosmetics, and other emerging uses where foil functions as a barrier layer, including induction heat-seal liners and battery pouch structures. Industry bodies such as the European Aluminium Foil Association (EAFA), The Aluminum Association (Foil Committee), and the Global Aluminium Foil Roller Initiative (GLAFRI) support market development and sustainability alignment. At the same time, the visible shift toward integration (smelter-to-foil and foil-to-converting) helps manage metal-price volatility and recycled-content demands. The 2026 launch of a small-format aluminum packaging recycling alliance by EAFA with Flexible Packaging Europe also highlights collection and sorting constraints as a practical bottleneck for the value chain, not only a downstream waste-management issue.

Competitive Landscape

Global supply is moderately fragmented: the top five players command close to 55% of revenue, enough to influence price but short of oligopoly. Novelis, Hindalco, and Reynolds Consumer Products leverage vertical integration from hot mill to foil roll, securing metal input and recycling streams. Novelis’ partnership with Germany-based TSR for 75,000 tonnes of recycled aluminum annually highlights a pivot toward circular sourcing.

Acquisition activity reshapes regional footprints. One Rock Capital Partners took over Constantia Flexibles in January 2024, deepening exposure to pharmaceutical lidding foils. In April 2025, Sonoco divested its Thermoformed and Flexibles unit to TOPPAN Holdings for USD 1.8 billion, sharpening Sonoco’s focus on metal and fiber packaging while giving TOPPAN 700 patents across ten countries.[3]Sonoco Products Company, “Investor News,” sonoco.com

Technology priorities cluster around indirect chill casting to cut energy per tonne, water-based primers that remove VOCs, and nanoscale coatings that boost barrier ratings without extra gauge. Investments in Indian battery-foil mills illustrate the search for higher-value niches. Competitors also market life-cycle-assessment dashboards to help brand owners quantify carbon savings when swapping from multi-material laminates to mono-foil structures.

Aluminum Foil Packaging Industry Leaders

China Hongqiao Group Limited

Novelis Inc.

Amcor plc

Constantia Flexibles Group GmbH

Hindalco Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven redesign and recycling infrastructure are creating near-term whitespace in high-barrier foil structures that can satisfy both performance needs and emerging substance restrictions. The EU PPWR (Regulation (EU) 2025/40), applicable from August 2026, adds specific constraints around heavy metals and PFAS for food-contact packaging. This pushes brand owners and converters to revisit coatings, inks, and laminate constructions while tightening documentation and test readiness. Alongside that regulatory work, industry-backed collection and sorting initiatives are expanding: in January 2026, EAFA and Flexible Packaging Europe launched a recycling alliance focused on small-format aluminum packaging, targeting a known leakage point in current recycling streams and supporting designs that sort and recycle more easily.

Capacity localization and supply-chain resilience are also widening corridors for foil packaging supply, particularly in fast-growing food and pharma hubs. In January 2026, Tahweel Metal Industry Corporation awarded Achenbach Buschhutten a contract for a 106,000 tonnes per annum aluminum foil production plant in Dammam, Saudi Arabia, linking regional demand growth with local foil rolling investment and equipment modernization. In June 2026, Ghana Integrated Aluminium Development Corporation and Danieli signed an MoU for a 300 million Euro aluminum foil plant in Tema, planned at 45,000 tonnes per year, signaling new African manufacturing nodes that can shorten lead times for converters and reduce reliance on imported foil for packaging applications. In the United States, proposed scrutiny of scrap aluminum exports (HB 9161 introduced in June 2026) further raises the strategic value of domestic recycled feedstock and closed-loop sourcing for foil and foil-based packaging supply chains.

Recent Industry Developments

- April 2026: China Hongqiao Group Limited published key unaudited Q1 2026 financial data for Shandong Hongqiao Aluminum Industry, reporting RMB 40.93 billion in revenue for the three months ended March 31, 2026. While not product-line specific, the update underscores the scale of upstream aluminum operations that underpin foil-roller feedstock availability and pricing dynamics for packaging-grade foil.

- November 2025: Hindalco Industries Limited authorized a USD 750 million equity infusion into Novelis to support cash flow as the Bay Minette, Alabama, rolling and recycling facility progresses and as the company manages higher project costs. The funding strengthens a major North American aluminum sheet and recycling buildout that influences foil and broader packaging-material supply strategies through recycled metal access and regional capacity additions.

- June 2024: Amcor Capsules initiated the launch of ESSENTIELLE, a plastic-free aluminum-paper foil for the wine and spirits market, with production scheduled to start at the Mareuil-sur-Ay site in October 2024. The launch broadens foil-based closure and overwrap options positioned around material reduction, reinforcing converter demand for paper-foil composite structures in premium beverage packaging.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this study, the market covers packaging solutions where aluminum foil is the main barrier layer used to protect and preserve products, and it is sized in value terms across end-use packaging demand.

Scope exclusions: It excludes bulk aluminum foil sold for non-packaging industrial uses where there is no packaging conversion or packaging function.

Segmentation Overview

- By Type

- Rolled Foil

- Backed Foil

- Embossed and Lacquered Foil

- Other Types

- By Application

- Converter Foils

- Container Foils

- Household Foils

- Industrial/Insulation Foils

- By Packaging Format

- Wraps

- Pouches and Sachets

- Blisters and Lids

- Trays and Containers

- Other Packaging Fomrats

- By End User

- Food

- Beverage

- Pharmaceutical

- Cosmetics and Personal Care

- Tobacco

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Vietnam

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building the demand context for packaged food, beverages, and pharma, since these are common pull areas for foil-based packs. We used public sources such as the US Census Bureau manufacturing data, USITC trade statistics, UN Comtrade, Eurostat, and FAO food supply indicators to map production, trade flows, and consumption direction.

After that, we cross-checked the packaging angle using industry association publications, regulatory notes on food contact and recycling rules, company annual reports and investor presentations, and reputed business press. Where needed, we referenced paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data to sanity check capacity additions and major trade routes. These examples are not exhaustive, and other public documents and datasets were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what the secondary indicators were implying, especially around mix shifts between household foil, converter foil, and container foil, and around how pricing moved in response to aluminum and energy costs. We spoke with a balanced set of stakeholders across converters, packaging buyers, and distribution channels, and then rechecked assumptions with regional experts across APAC, EMEA, and the Americas to reduce blind spots in fast-changing demand pockets.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 42% |

| Mid tier: 48% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 17% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

The model is built by reconstructing the addressable packaging demand pool through packaging conversion activity and end-use consumption signals, and then mapping that to foil usage intensity by format. A top-down approach was applied by linking packaged food and beverage output, pharma pack volumes, and flexible packaging penetration to foil-containing formats, which are then converted into value using observed price bands.

To keep the totals realistic, we corroborated results with selective bottom-up approximations like sampled converter revenue checks, channel pricing for key foil gauges, and spot checks of announced capacity and utilization direction. Inputs that mattered in this market included aluminum price trends and pass-through timing, shifts between pouches and wraps versus rigid trays and containers, blister pack demand in pharma, gauge downtrending and barrier substitution, recycling and food-contact compliance costs, and regional mix changes between APAC export-led volumes and mature-market replacement demand.

For forecasting, scenario analysis was used because cost cycles and substitution risk can move faster than end-use volumes. Growth paths were set using consensus from expert views on packaged food growth, pharma output, and expected price normalization, with gaps handled by using proxy ratios from similar foil-based packaging formats when a sub-segment lacked clean public time series.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, so the market total is checked against trade balances, conversion activity indicators, and end-use packaging consumption direction before sign-off. When a region shows an unexpected jump or drop, we trace it back to a small set of drivers like pricing, gauge mix, or an end-use shock, and we re-contact sources when the variance cannot be explained cleanly.

A second analyst review is run to catch unit issues, currency timing problems, and double counting between converter foil and container foil value pools. Reports are refreshed on an annual cycle, with interim updates when material events occur such as major capacity moves, regulatory changes, or sharp raw material swings. Before delivery, a final pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Aluminum Foil Packaging Market Size Versus Other Published Estimates

It is normal to see different market numbers for aluminum foil packaging because studies do not always count the same formats, end uses, and value layers, and they may also pick different base years. Differences also show up when one model relies more on production signals while another leans more on pricing assumptions.

By tracking packaging-format level demand signals and refreshing price pass-through timing, Mordor Intelligence keeps the value build tied to actual foil-in-pack usage and avoids counting adjacent aluminum packaging categories that do not use foil as the barrier layer.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 30.63 B (2026) | |

| Global Consultancy A | USD 51.62 B (2025) | Uses a broader scope that can blend foil-based packs with wider aluminum packaging spend, and the earlier base year can amplify the impact of cost inflation on the total. |

| Industry Research Group B | USD 28.32 B (2025) | Appears to run a narrower conversion-led view with limited clarity on included packaging formats, and it can understate value if household foil and certain lidding and blister applications are not fully captured. |

The spread in values mainly comes from what is counted as foil packaging, how much of the value chain is included, and how pricing is carried into the base year. A transparent model that ties format volumes to observable end-use signals, and then applies defensible price bands, gives decision makers a number that can be repeated and stress-tested as inputs change.

Key Questions Answered in the Report

What is the current value of the aluminum foil packaging market?

The market stands at USD 30.63 billion in 2026.

How fast is the sector expected to grow by 2031?

It is forecast to reach USD 38.56 billion, registering a 4.72% CAGR.

Which region leads consumption?

Asia-Pacific accounts for 39.88% of 2025 revenue, driven by food processing and pharmaceutical output.

What end-use segment is growing fastest?

Pharmaceutical packaging is projected to rise at a 6.41% CAGR through 2031 due to blister-pack expansion.

Who are the key players in this space?

Novelis, Hindalco, Constantia Flexibles, Reynolds Consumer Products, and Sonoco anchor the competitive field.

How are sustainability pressures influencing suppliers?

Producers invest in recycling technology and lightweight laminates to meet EU waste directives and brand carbon goals.

Page last updated on: