AI In Video Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

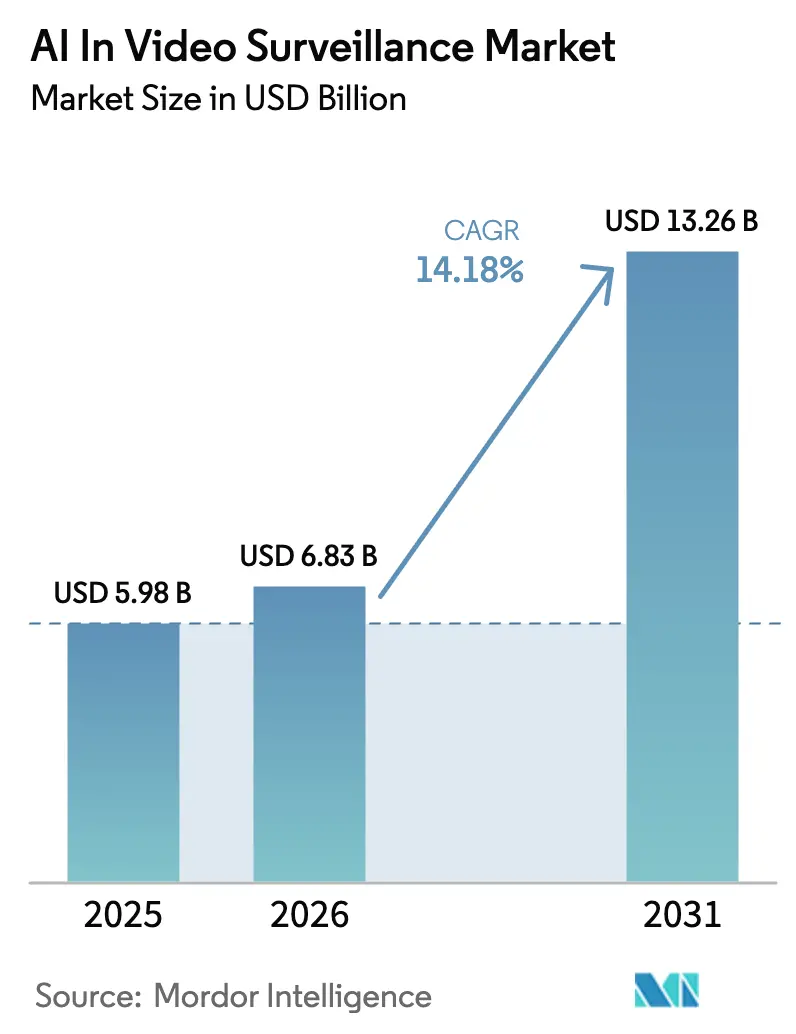

| Market Size (2026) | USD 6.83 Billion |

| Market Size (2031) | USD 13.26 Billion |

| Growth Rate (2026 - 2031) | 14.18% CAGR |

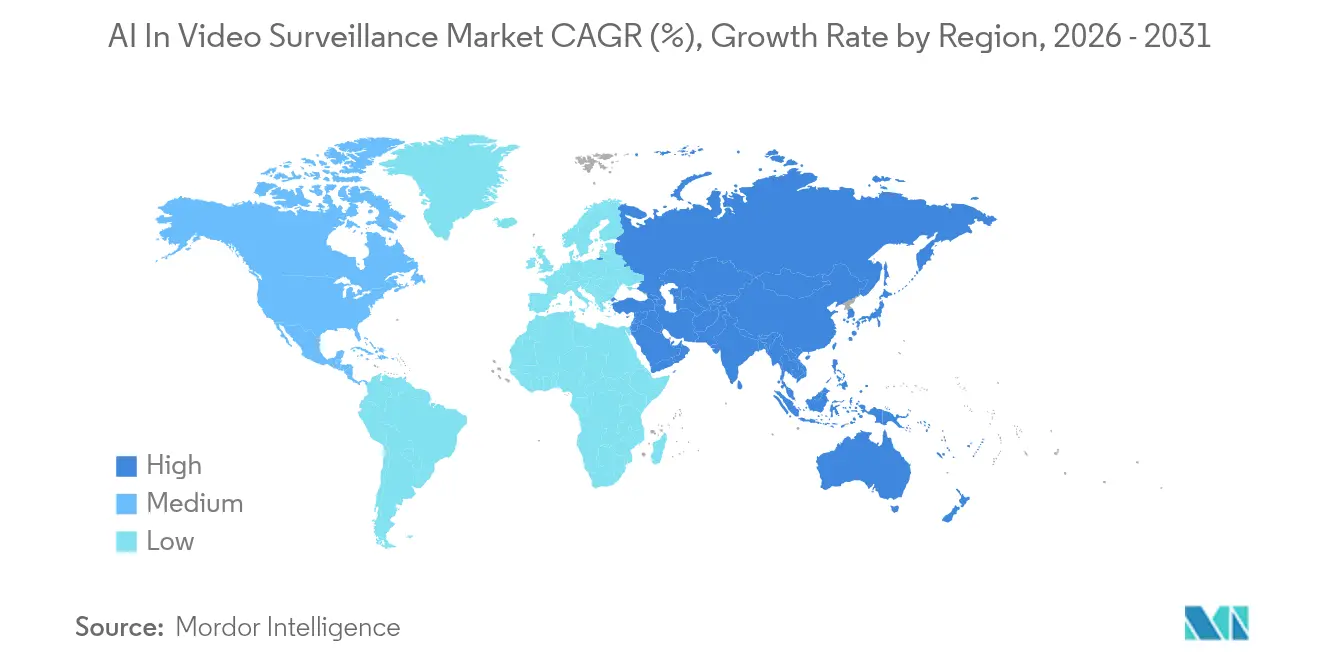

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

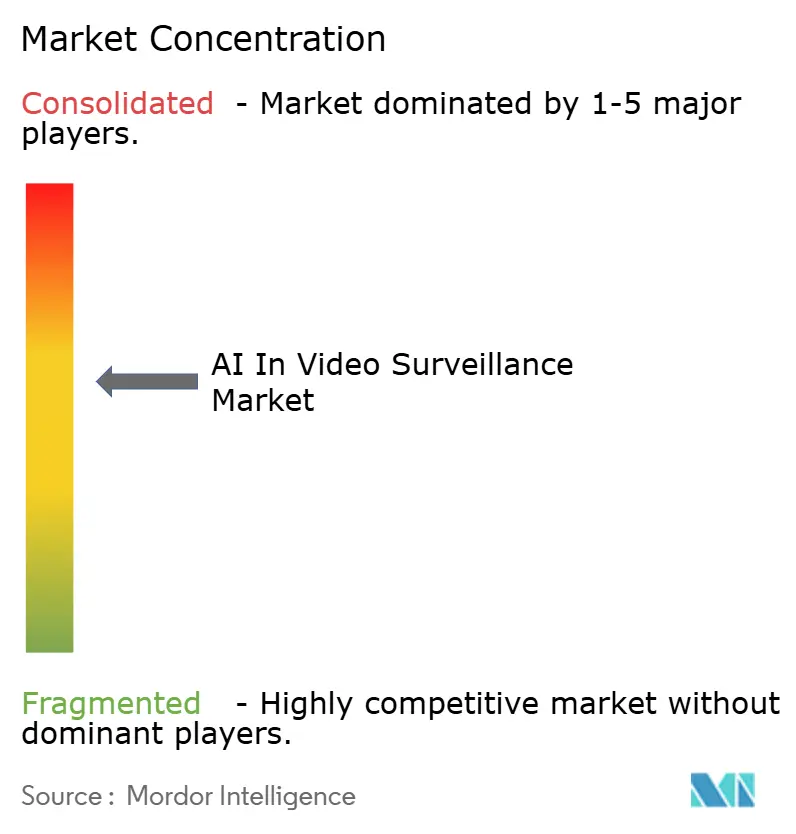

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Video Surveillance Market Analysis by Mordor Intelligence

AI in video surveillance market size in 2026 is estimated at USD 6.83 billion, growing from 2025 value of USD 5.98 billion with 2031 projections showing USD 13.26 billion, growing at 14.18% CAGR over 2026-2031. Ongoing smart-city roll-outs, the drop in edge-AI chipset costs, and the migration toward cloud-based video-surveillance-as-a-service (VSaaS) collectively reinforce that trajectory. Hardware continues to supply most of the revenue, yet spending is tilting toward software intelligence as buyers prioritise analytics that convert camera feeds into operational insights. Hybrid edge-cloud architectures, tighter cyber-security mandates, and rising demand for integrated situational-awareness platforms further widen the scope of surveillance systems beyond crime prevention to traffic, infrastructure, and environmental monitoring. These dynamics accelerate the transition from passive video capture to predictive decision support, creating new revenue pools for value-added services and algorithm licensing.

Key Report Takeaways

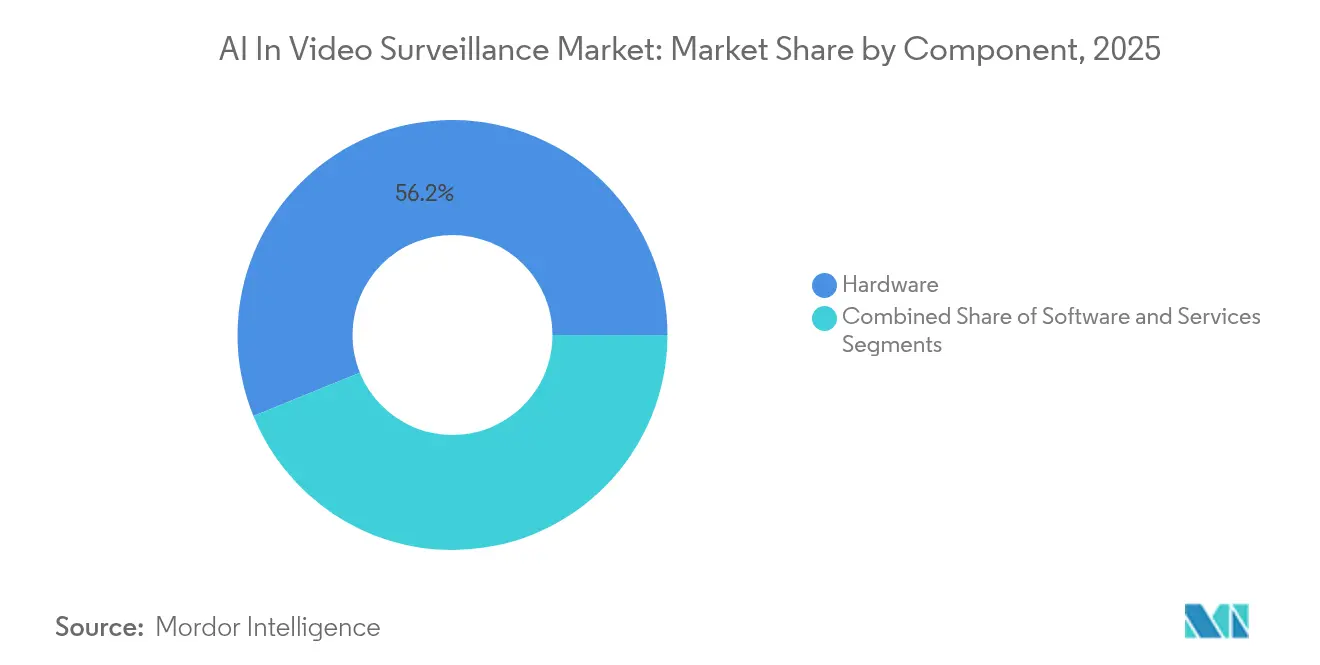

- By component, hardware retained 56.15% of the AI in video surveillance market share in 2025, while software is forecast to expand at an 17.85% CAGR through 2031.

- By deployment model, on-premises systems held 64.35% revenue share in 2025; cloud solutions are projected to grow at 22.1% CAGR to 2031.

- By end-user, commercial facilities led with 43.05% of the AI in video surveillance market size in 2025; residential demand is the fastest riser at 15.05% CAGR.

- By camera type, dome units accounted for 32.25% share of the AI in video surveillance market size in 2025, whereas panoramic/fisheye cameras should progress at 15.85% CAGR through 2031.

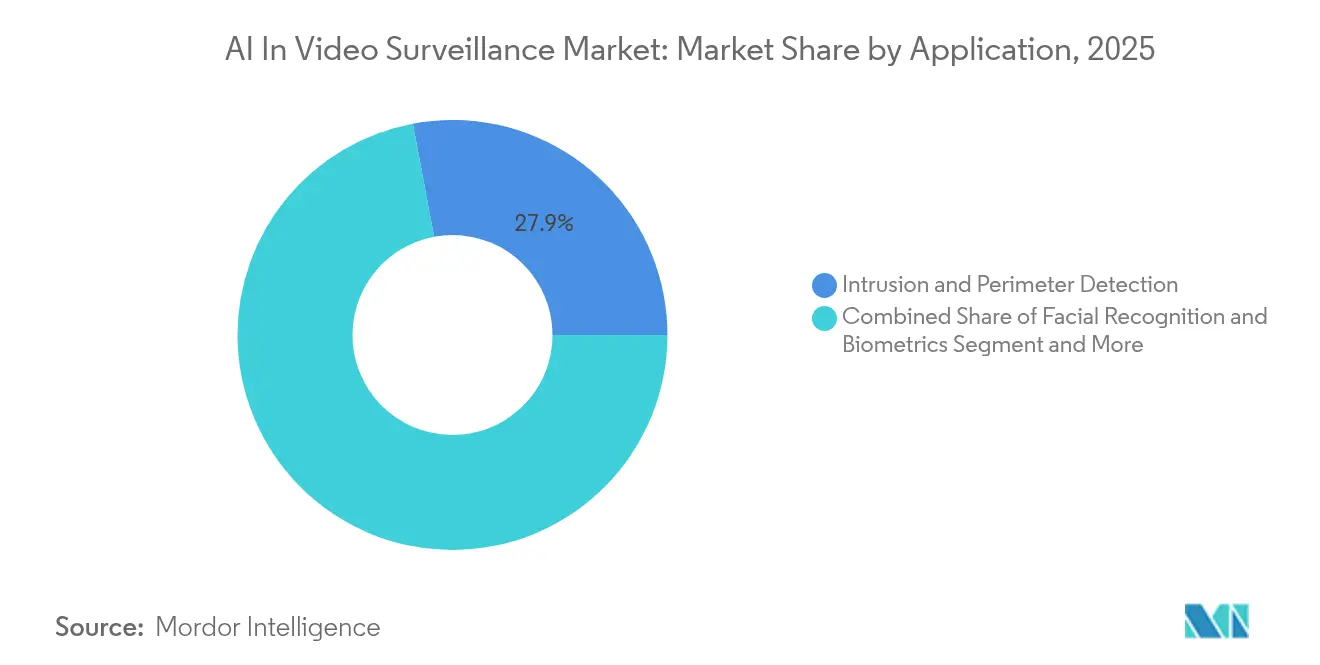

- By application, perimeter security captured 27.95% of the AI in video surveillance market share in 2025; facial recognition and biometrics are forecast to advance at 23.85% CAGR.

- Asia-Pacific commanded 36.55% of global revenue in 2025, and the Middle East is expected to register the highest regional CAGR at 13.55% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AI In Video Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integrated AI-powered security analytics | +3.2% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Smart-city surveillance infrastructure rollout | +2.8% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Declining cost and higher power of edge-AI chipsets | +2.1% | Global | Short term (≤ 2 years) |

| Expansion of VSaaS | +1.9% | North America and EU, spreading to APAC | Medium term (2-4 years) |

| Multi-sensor fusion (AIoT) | +1.6% | Global, early smart-city adoption | Long term (≥ 4 years) |

| Generative-AI synthetic data for model training | +1.4% | Global, concentrated in RandD hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for integrated AI-powered security analytics

- Municipal programmes increasingly embed analytics that link surveillance feeds to traffic control, emergency dispatch, and infrastructure diagnostics. Pilot deployments in Virginia demonstrate real-time detection of anomalous public-space behaviour, improving incident response and resource allocation[1]Tech-Xplore Staff, “SMAST system raises bar for real-time behaviour detection,” techxplore.com. European towns such as Las Rozas use smart cameras to quantify pedestrian density for urban-planning decisions. These multipurpose systems justify higher capital budgets because one installation serves safety, mobility, and planning mandates simultaneously. New procurement records show municipal purchases for robotic patrol devices and AI-enabled licence-plate readers exceeding USD 465,000 across New York and Missouri in 2024. Budget efficiencies and data-driven governance objectives therefore reinforce analytics adoption within the AI in video surveillance market.

Rapid deployment of smart-city surveillance infrastructures

Government stimulus in emerging economies is standardizing AI-ready CCTV networks as foundational digital infrastructure. Saudi Arabia’s localization of surveillance equipment manufacturing through partnerships with Chinese suppliers reflects a policy focus on domestic value creation. Across the Gulf, mandatory camera installation regulations underpin a 6.2% regional surveillance CAGR to 2025. China’s “Skynet 2.0” even extends camera-based situational monitoring to lunar exploration programs, highlighting the scale of state-backed investment. South Korea plans a nationwide migration to AI-enabled CCTV by 2026, locking in supplier certification requirements that guarantee a pipeline of public contracts. These programs both expand immediate hardware volumes and set technical standards that shape the global AI in video surveillance market.

Declining cost and power of edge-AI chipsets

New video-centric system-on-chips deliver multi-model inference inside the camera body, cutting network load and latency. Ambarella’s CV72S doubles concurrent AI model throughput versus its predecessor while lowering power draw. Qualcomm’s industrial IoT reference designs bundle on-device analytics with secure connectivity for enterprise roll-outs. Such silicon advances put high-accuracy object detection within reach of small businesses, broadening the total addressable market. They also enable large campuses to offload computation from data centres, shrinking recurring cloud spend. As forecast by semiconductor vendors, energy-efficient accelerators will catalyse new use cases across 2025, especially video-heavy security workloads.

Expansion of VSaaS lowering adoption barriers

Fifteen years of VSaaS evolution show how improvements in broadband, browser protocols, and 5G have eliminated the frame-rate and latency issues that once limited cloud surveillance[3]. The 2025 merger of Milestone Systems and Arcules illustrates the convergence of mature video-management software with native cloud architecture, giving mid-market users enterprise-grade analytics without infrastructure overhead. Subscription pricing, automatic feature updates, and elastic storage appeal to residential and small commercial buyers. The model also lets vendors introduce AI upgrades without touching customer-site hardware, accelerating the feature refresh cycle across the AI in video surveillance market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and ethical regulation on biometric analytics | -2.1% | EU and North America, widening globally | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in IP networks | -1.8% | Global | Short term (≤ 2 years) |

| High energy consumption under carbon rules | -1.2% | EU and developed markets | Medium term (2-4 years) |

| Algorithmic bias driving procurement hesitancy | -0.9% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating privacy and ethical regulation on biometric analytics

The EU AI Act imposes strict approval thresholds for remote facial recognition in public areas, limiting deployments to narrowly defined law-enforcement exceptions with judicial oversight. Additional clauses restrict emotion detection in workplaces and schools, prompting vendors to rethink product road maps. Because the regulation has extraterritorial scope, suppliers worldwide must validate compliance before selling into Europe, inflating certification costs and elongating the sales cycle. While top-ranked algorithm vendors such as IDEMIA meet accuracy and bias thresholds, many municipal buyers still prefer behaviour-based analytics that avoid biometric data capture. Regulatory uncertainty, therefore, suppresses near-term demand for facial-recognition modules inside the AI in the video surveillance market.

Cyber-security vulnerabilities in IP surveillance networks

Recurring disclosures of exploitable firmware gaps in network cameras undermine buyer confidence. A 2024 CISA advisory flagged actively weaponized Dahua flaws that persisted since 2021, underscoring patch-management challenges. Researchers similarly showed how unpatched Edimax devices could join Mirai botnets and launch volumetric attacks. These incidents drive stricter procurement criteria that demand end-to-end encryption, auto-update pipelines, and zero-trust architecture. Organizations often defer or resize projects until vendors demonstrate hardened cyber postures, trimming short-term equipment orders inside the AI in video surveillance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Intelligence Drives Value Migration

Hardware preserved 56.15% of 2025 revenue because cameras, recorders, and network gear remain physical prerequisites, yet the software segment is on track for an 17.85% CAGR to 2031, reflecting a decisive shift toward algorithm-centric value. All major video-management platforms have embedded real-time analytics, automated event triage, and cloud connectors, features that command service-subscription premiums. Industry demonstrations by IronYun, NVIDIA, and Verkada illustrate how generative models can classify complex behaviours in milliseconds, elevating software differentiation.

Hardware road-maps increasingly integrate deep-learning accelerators on the PCB, creating edge devices that execute detection and classification locally. Vendors such as Hikvision combine visible-light, thermal, and radar modules inside a single enclosure, freeing central servers for forensic analytics rather than basic object recognition. Services revenue, though smallest today, scales with the number of AI deployments that require model tuning, cyber-security audits, and regulatory documentation. Thus, software, services, and intelligent hardware form a mutually reinforcing stack that should lift the AI in video surveillance market over the forecast horizon.

By Deployment Model: Cloud Acceleration Reshapes Architecture

On-premises video storage and processing still hold 64.35% of the AI in video surveillance market share, yet cloud and hybrid configurations register the fastest expansion at 22.1% CAGR. Corporate adopters increasingly separate latency-critical inference at the edge from compute-intensive analytics in the cloud, an architecture that balances bandwidth, sovereignty, and cost. Smaller organisations migrate fully to VSaaS to avoid capital outlays, while campus-scale users adopt gateway appliances that forward selected metadata to central clouds for pattern mining.

Early concerns about real-time streaming quality have largely dissipated as 5G roll-outs and HTML5 improvements provide consistent throughput. Cloud providers release quarterly AI feature packs, offering anomaly detection, licence-plate recognition, and occupancy analytics without hardware swaps. This cadence materially shortens innovation cycles, making VSaaS the preferred growth engine for the AI in video surveillance market.

By End-user: Residential Surge Transforms Market Dynamics

Commercial sites—office parks, retail malls, and hospitality venues—delivered 43.05% of 2025 revenue. However, residential uptake, propelled by smart-home platforms and lower device prices, is projected to rise at 15.05% CAGR. Video doorbells and affordable Wi-Fi cameras now rank among the top two connected-home devices in ownership surveys, reflecting consumer confidence in DIY security systems.

Military and defence operators continue to buy ruggedized, specialized optics, while government agencies finance expansive citywide networks that integrate traffic, public-safety, and environmental sensors. Industrial facilities emphasize fail-safe design and cyber hardening. These diverse requirements sustain a broad solution mix, yet residential momentum is shifting volume leadership within the AI in video surveillance market.

By Application: Biometric Analytics Accelerates Despite Regulatory Headwinds

Perimeter-intrusion detection commanded 27.95% of 2025 sales because fence-line monitoring remains the first layer of defence for facilities. Facial-recognition and biometric modules, already delivering 98.39% accuracy in controlled conditions, are set for a 23.85% CAGR through 2031. Traffic and crowd analytics aid urban planning and emergency evacuation, while retail chains deploy heat-maps and path tracking to sharpen merchandising.

Machine-learning-based anomaly detection is the fastest-maturing use case. Research prototypes such as AnomalyRuler demonstrate how large language models can explain detection logic, boosting operator trust in alerts. Integrated AI suites that bundle multiple applications in one licence give buyers a single pane of glass and accelerate cross-function budget approval, adding resilience to the AI in video surveillance market.

By Camera Type: Multi-Sensor Integration Defines Next Generation

Recent product launches showcase cameras that blend optical, thermal, radar, and acoustic inputs, processed by on-board AI accelerators. Hikvision’s AIoT concept pairs 5G connectivity with multi-spectral sensors to create scenario-based digital twins of monitored assets. Similar designs from MileSight stream real-time traffic data to cloud dashboards with sub-second latency.

Academic work on sensor fusion for autonomous vehicles informs algorithm design for surveillance, underscoring how cross-disciplinary innovation benefits the AI in video surveillance market. Compression schemes that leverage coordinate-based neural nets also reduce storage requirements for UHD feeds, allowing longer retention without disproportionate cost increases.

Geography Analysis

Asia-Pacific held 36.55% of global revenue in 2025, fueled by China’s massive urban-camera grid and regional smart-city programs. Skynet expansion to lunar research illustrates the ambition and public funding mobilized for surveillance infrastructure. South Korean mandates to retrofit all public CCTV with AI by 2026 imply at least 20% annual spending lifts in that country. Japan and India add further weight through railway, airport, and urban-renewal projects, while ASEAN municipalities apply surveillance data to flood management and public-health monitoring.

North America remains the technology innovation hub, with federal research on autonomous multi-camera tracking and city budgets that finance robotic patrol units. Canadian border agencies expand AI video analytics to improve throughput at land crossings, and Mexican megacities install integrated command centers that coordinate traffic lights with predictive crime mapping. Venture funding flows to AI-native startups, reflecting market confidence in software-led growth inside the AI in video surveillance market.

The Middle East is on course for a 13.55% CAGR to 2031, anchored by Gulf smart-city visions that bundle surveillance with IoT-based public-service delivery. Mandatory camera regulations, easy access to capital, and public-sector backing accelerate adoption. Saudi Arabia’s plan to co-manufacture cameras domestically through Dahua tie-ups signals an appetite for local value capture. Despite privacy debates, large-scale deployments continue as governments prioritize security and urban optimization objectives.

Competitive Landscape

Market concentration remains moderate. Hikvision, Dahua, and Axis Communications lead due to global channels and sustained RandD outlays. Hikvision’s 2023 annual disclosures confirm heavy spending on AIoT feature integration that combines thermal, radar, and optical streams. Dahua builds similar multi-sensor portfolios and partners with Gulf manufacturers to deepen regional penetration.

Western incumbents focus on software, cloud, and vertical solutions. Motorola Solutions acquired Silent Sentinel for long-range thermal imaging, while Axon added Dedrone to extend perimeter security into airspace. Cloud-first challengers such as Flock Safety secured USD 275 million in 2025 to scale domestic manufacturing and RandD, reaching USD 300 million recurring revenue. GardaWorld folded Stealth Monitoring into its portfolio, creating a global leader in proactive remote video response[2]Stealth Monitoring Press Office, “GardaWorld deal expands proactive video monitoring,” stealthmonitoring.com.

Patent filings from Qualcomm reveal innovations in cross-camera attention mechanisms that underpin next-generation multi-view tracking. Competition, therefore, hinges on AI depth, cloud delivery, and vertical integration across hardware, software, and services.

AI In Video Surveillance Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd

Dahua Technology Co., Ltd.

Avigilon Corporation

Milestone Systems A/S

YITU Tech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Flock Safety raised USD 275 million to build U.S. manufacturing lines and lift annual recurring revenue beyond USD 300 million.

- February 2025: Milestone Systems merged with Arcules to unify on-premises video management and cloud VSaaS under one brand.

- January 2025: Metropolis purchased AI vision specialist Oosto for USD 125 million to bolster smart-parking and mobility analytics.

- January 2025: Hikvision unveiled AIoT scenario-based solutions at Intersec Dubai, showcasing multi-sensor fusion and 5G connectivity.

Global AI In Video Surveillance Market Report Scope

AI in video surveillance refers to the integration of artificial intelligence technologies into video monitoring systems to enhance security and operational efficiency.

The AI in video surveillance market is segmented by component (hardware, software, services), by deployment (cloud, on-premises), by end-user (commercial, residential, military & defense, government & public facilities, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| On-premises |

| Cloud |

| Commercial |

| Residential |

| Military and Defense |

| Government and Public Facilities |

| Industrial and Critical Infrastructure |

| Fixed Box |

| Dome |

| Bullet |

| PTZ |

| Panoramic / Fisheye |

| Thermal and Infrared |

| Intrusion and Perimeter Detection |

| Facial Recognition and Biometrics |

| Traffic and Crowd Management |

| Retail and Behavioural Analytics |

| Anomaly and Incident Detection |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Model | On-premises | ||

| Cloud | |||

| By End-user | Commercial | ||

| Residential | |||

| Military and Defense | |||

| Government and Public Facilities | |||

| Industrial and Critical Infrastructure | |||

| By Camera Type | Fixed Box | ||

| Dome | |||

| Bullet | |||

| PTZ | |||

| Panoramic / Fisheye | |||

| Thermal and Infrared | |||

| By Application / Function | Intrusion and Perimeter Detection | ||

| Facial Recognition and Biometrics | |||

| Traffic and Crowd Management | |||

| Retail and Behavioural Analytics | |||

| Anomaly and Incident Detection | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size of the AI in video surveillance market?

The market stands at USD 6.83 billion in 2026 and is projected to reach USD 13.26 billion by 2031.

Which component segment is growing the fastest?

Software is forecast to expand at an 17.85% CAGR through 2031 as buyers prioritise analytics and cloud connectivity.

How quickly are cloud deployment models gaining ground?

Cloud-based and hybrid solutions are expected to grow at 22.1% CAGR, transforming traditional architecture toward VSaaS.

Which region will see the highest growth rate?

The Middle East is projected to post a 13.55% CAGR, driven by smart-city initiatives and supportive regulation.

Page last updated on: