Video Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

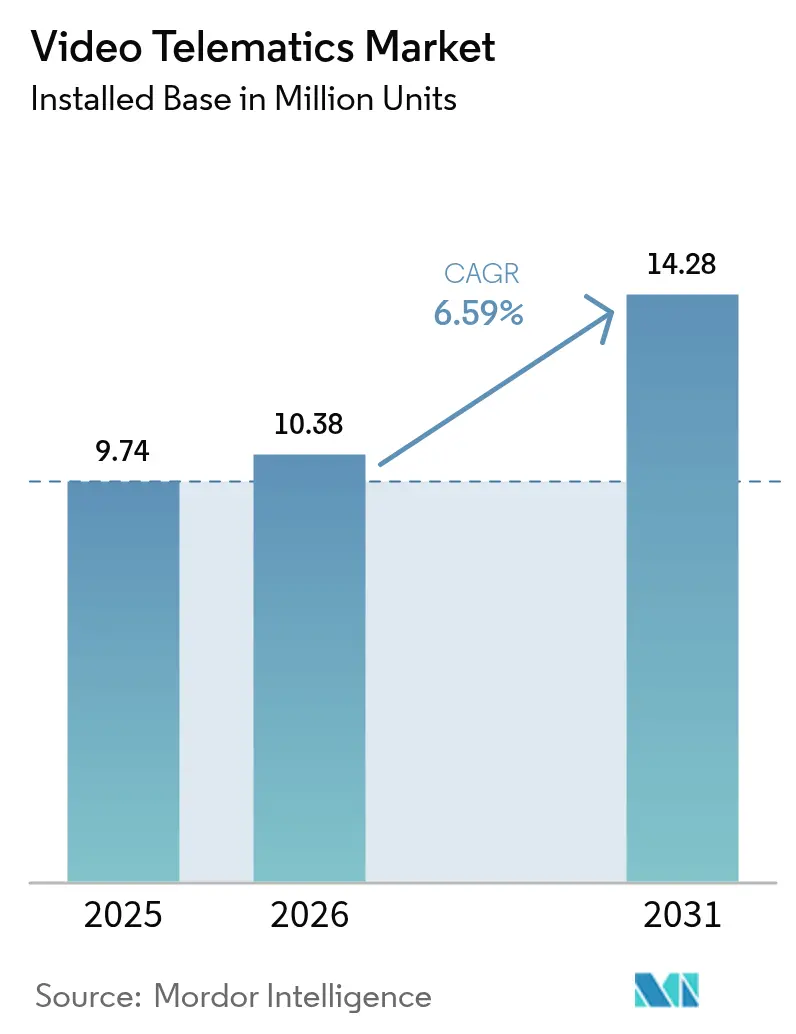

| Market Volume (2026) | 10.38 Million units |

| Market Volume (2031) | 14.28 Million units |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

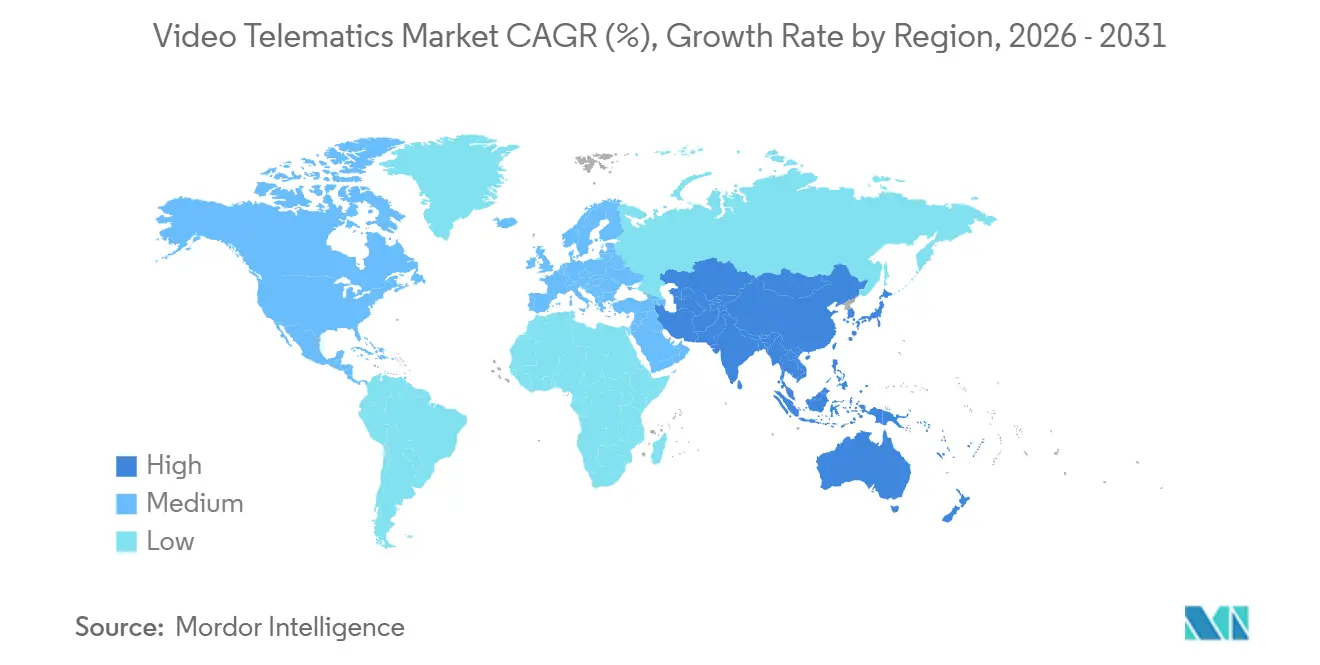

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Telematics Market Analysis by Mordor Intelligence

The Video Telematics Market size in terms of installed base is projected to expand from 9.74 Million units in 2025 and 10.38 Million units in 2026 to 14.28 Million units by 2031, registering a CAGR of 6.59% between 2026 to 2031. A tightening web of safety regulations across North America, Europe, and Asia-Pacific is repositioning on-board video from a nice-to-have to a line item for legal compliance. Fleets that once refreshed camera hardware every five years are now bringing forward purchase cycles as regulators compress implementation timelines. Larger carriers are also shifting away from outright ownership toward subscription bundles that convert capital expense into predictable operating costs. At the same time, insurers are increasing the commercial value of video evidence by tying premium discounts directly to video-verified driver-behavior metrics, thereby strengthening the business case for real-time analytics delivered through cloud dashboards.

Key Report Takeaways

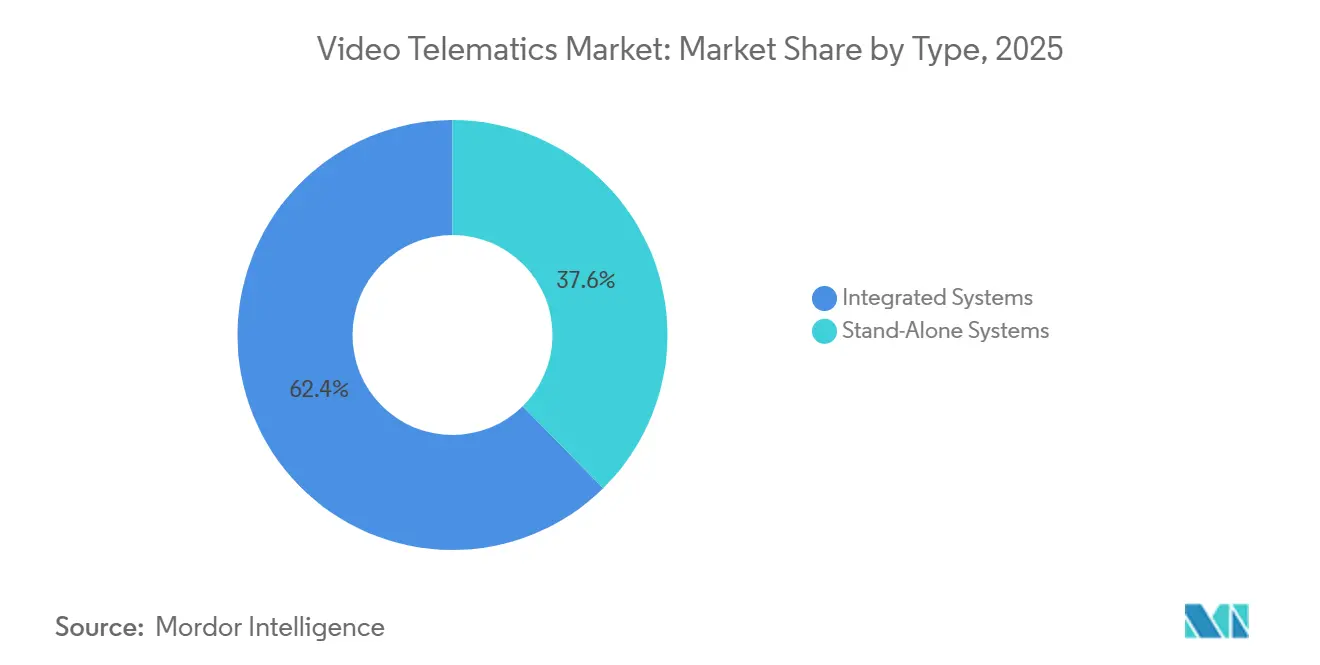

- By type, integrated systems led with 62.37% revenue share in 2025, and stand-alone systems are forecast to expand at a 6.91% CAGR through 2031.

- By vehicle type, heavy trucks captured 33.68% of the video telematics market share in 2025, while light commercial vehicles are projected to advance at a 7.33% CAGR to 2031.

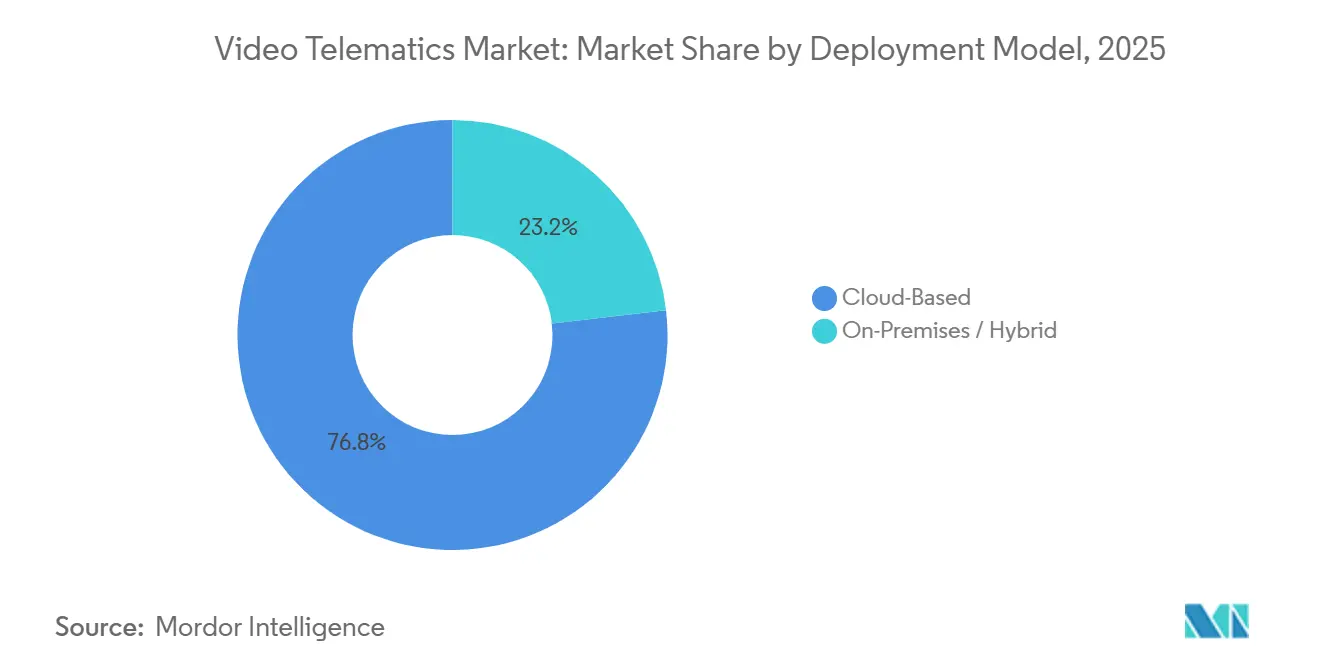

- By deployment model, cloud-based platforms commanded 76.83% of 2025 revenue and are expected to grow at a 6.96% CAGR over the forecast period.

- By component, hardware accounted for 53.62% of the video telematics market share in 2025, whereas software and analytics are set to register a 7.16% CAGR through 2031.

- By geography, North America accounted for 38.91% of the video telematics market share in 2025, and Asia-Pacific is anticipated to post the fastest CAGR of 7.57% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Video Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of Fleet Telematics-Integrated Video Solutions | +1.8% | Global, especially North America and Europe | Medium term (2-4 years) |

| Regulatory Mandates for Driver-Monitoring and ADAS Data Logging | +1.5% | Europe, North America, China, India | Short term (≤ 2 years) |

| Falling Camera and Edge-AI Costs | +1.2% | Global | Medium term (2-4 years) |

| Growing Safety-Compliance Focus among Commercial Fleets | +1.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Usage-Based Insurance Shift to Video-Verified Claims | +0.9% | North America, Europe | Long term (≥ 4 years) |

| Road-Image Data Monetisation and Smart-City Partnerships | +0.3% | Select North America and Asia-Pacific cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Fleet Telematics-Integrated Video Solutions

Enterprise fleets are consolidating vendor relationships by embedding cameras inside existing telematics dashboards. Samsara’s January 2026 Asset Gateway added video coverage to trailers and containers, expanding surveillance beyond the cab.[1]Samsara, “Asset Gateway Release,” samsara.com Lytx’s April 2025 link-up with Geotab lets operators replay harsh-braking events alongside synchronized clips inside a single portal. The integrated approach reduces investigation time, cuts software costs, and pressures stand-alone camera vendors to open their APIs. Integrated platforms already captured 62.37% of 2025 revenue and will widen that lead as multiyear software subscriptions replace one-off hardware sales.

Regulatory Mandates for Driver-Monitoring and ADAS Data Logging

The European Union’s General Safety Regulation requires Data Event Recorders on all new vehicles from July 2026, accelerating camera upgrades across the continent.[2]European Commission, “General Safety Regulation,” europa.eu United States regulators have not mandated video yet, but ongoing Hours-of-Service audits by FMCSA keep domestic carriers on high alert. China’s Ministry of Transport rules from 2025, and India’s Road Transport Ministry guidelines are generating similar urgency in Asia. Hard deadlines are compelling fleets to retire pre-2020 trucks earlier than planned and to purchase systems capable of capturing 5 seconds of pre-crash footage, steering inputs, and speed data.

Falling Camera and Edge-AI Costs

Automotive-grade image sensors and low-power inference chips are pushing down bill-of-materials prices. Motive’s AI Dashcam Gen 3 runs local distraction detection while sending only flagged clips to the cloud, cutting cellular bills without sacrificing insight.[3]Motive, “AI Dashcam Gen 3 Launch,” gomotive.com Garmin’s Dash Cam Live blends on-device storage with selective LTE uploads to balance quality against bandwidth. Lower component costs are particularly impactful in South America and Southeast Asia, where fleets have historically delayed adoption until hardware prices dropped below USD 1,000 per vehicle.

Growing Safety-Compliance Focus among Commercial Fleets

Insurers now offer 20-30% premium reductions for fleets that provide video-verified driver scores, quickly offsetting the cost of cameras. A 2025 case study by 3 Sisters Logistics reported a 30% premium reduction following a full-fleet rollout. Progressive Commercial tailors premiums to video-confirmed risk profiles, strengthening the ROI narrative for real-time analytics. Australia’s National Heavy Vehicle Regulator encourages voluntary programs that award safety credits to camera-equipped operators. As litigation awards rise, carriers treat exoneration footage as critical evidence rather than ancillary data.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Data-Protection Compliance Hurdles | -0.8% | Europe, California, Canada | Short term (≤ 2 years) |

| High Hardware and Installation Costs for SMB Fleets | -0.6% | Global, acute in South America and Africa | Medium term (2-4 years) |

| Bandwidth or Storage Burdens for HD and 4K Streaming | -0.4% | Regions with limited cellular coverage | Medium term (2-4 years) |

| Lack of Open Standards for Video-Analytics Interoperability | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy and Data-Protection Compliance Hurdles

GDPR Article 88 requires European employers to limit worker monitoring, prompting some carriers to switch off driver-facing cameras during breaks. California’s Assembly Bill 1651 requires written consent and access to footage within 24 hours, adding extra paperwork to onboarding. Vendors must therefore build consent toggles, data-residency paths, and footage redaction, all of which inflate software timelines and raise engineering costs. Fleets that operate across borders face overlapping privacy codes, driving up compliance budgets and extending sales cycles.

High Hardware and Installation Costs for SMB Fleets

A five-camera set with professional wiring can cost USD 5,000 or more per truck, an outlay many operators with fewer than 50 vehicles cannot absorb up front. Geotab’s 2025 Latin American subscription package bundles hardware, installation, and software into a monthly fee, but multiyear lock-ins deter some owners. Retrofitting older trucks can double installation hours, while ongoing maintenance remains a hurdle for companies without dedicated IT teams. These pain points explain the 6.91% CAGR logged by stand-alone systems that reuse existing telematics back-ends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Integrated Suites Consolidate Demand, Stand-Alone Cameras Fill Retrofit Niches

Integrated platforms accounted for a commanding 62.37% of 2025 revenue, underscoring fleet demand for single dashboards that align video with GPS, maintenance alerts, and driver scorecards. Enterprise buyers prefer a single contract that covers hardware, cloud storage, and analytics updates, turning a patchwork of point solutions into a unified compliance engine. Subscription pricing reinforces that pull by exchanging up-front camera purchases for predictable monthly operating costs, an approach championed by vendors such as Samsara. At the same time, the focus on real-time coaching rather than delayed incident reviews is steering development road maps toward tighter links between telematics data and video clips that can be surfaced within seconds.

Stand-alone systems are expanding at a 6.91% CAGR through 2031, slightly outpacing overall market growth, as they easily integrate into mixed fleets that already run third-party electronic logging devices. Garmin’s LTE-enabled Dash Cam Live exemplifies this bolt-on model by storing routine footage locally and uploading only flagged events, a design that saves bandwidth in regions with expensive cellular data. Smaller carriers value the flexibility to deploy a single forward-facing unit today and add side or driver cameras later without ripping out legacy hardware. As edge-AI processors bring analytics to the device, performance gaps with integrated suites are narrowing, putting fresh pressure on pricing and feature differentiation.

By Vehicle Type: Heavy Trucks Dominate Revenues, Light Commercial Vehicles Accelerate

Heavy trucks accounted for 33.68% of 2025 revenue, driven by long-haul exposure to high-severity crashes and stringent insurance audits that require video documentation. Continuous lane-departure warnings, blind-spot monitoring, and driver-fatigue detection now ship as bundled options because motor carriers see clear correlations between onboard footage and courtroom defense costs. Regulatory attention from the Federal Motor Carrier Safety Administration keeps the momentum for adoption strong, even without a formal federal camera mandate. Multiple-camera arrays covering trailer doors and cargo bays are also becoming standard as freight owners insist on proof against theft and spoilage claims.

Light commercial vehicles are on track for a 7.33% CAGR between 2026-2031, the fastest of any vehicle class, as e-commerce operators such as Amazon wire delivery vans with AI-powered cabin cameras that score distraction, tailgating, and harsh braking. The dense stop-and-go profile of parcel routes produces richer event data per mile than highway driving, feeding machine-learning models that predict future collisions. Insurers respond by tailoring premium discounts to van fleets that share driver-behavior clips, effectively financing hardware rollouts in the last-mile sector. Buses, coaches, and passenger cars remain smaller slices today, but incoming safety mandates in Europe are set to raise their camera penetration later in the decade.

By Deployment Model: Cloud Strengthens Lead, Hybrid Holds Niche Roles

Cloud-based platforms dominated the 2025 revenue, accounting for 76.83%, and are projected to expand at a CAGR of 6.96% during the forecast period. Verizon Connect leverages its cellular footprint to bundle connectivity and storage, creating high switching costs that lock customers into multiyear plans. Cloud dashboards also simplify compliance audits by storing 6+ months of searchable footage without taxing in-house IT resources. As 4K sensors become mainstream, gigabyte-heavy files favor elastic cloud pipelines over fixed on-premises servers that can choke on peak loads.

Hybrid and on-premises deployments, which make up the remaining 23.17%, persist where patchy mobile coverage or strict data-residency laws prevent fleets from streaming continuously. Intelligent buffering that stores baseline video locally and pushes only incident clips upstream is extending camera adoption into rural haulage corridors and privacy-sensitive European states. Vendors now expose granular policies that let operators tune frame rates, upload windows, and retention periods for each asset, bridging the gap between cost control and regulatory duty of care. Although growth lags cloud options, hybrid models remain vital for fleets that cross borders or operate outside reliable LTE footprints.

By Component: Hardware Still Tops Revenue, Software Drives Future Margins

Hardware contributed 53.62% of 2025 turnover, anchored by durable cameras, ruggedized wiring, and edge processors that withstand vibration, moisture, and extreme temperatures. Falling sensor prices let fleets upgrade to dual-HD or quad-view rigs without doubling budgets, but installation labor still inflates capital requirements for small operators. Bulk buyers mitigate that cost by standardizing mounting locations across new vehicle orders, compressing fit-out timelines, and reducing truck downtime during retrofits.

Software and analytics, however, post a steeper 7.16% CAGR, confirming that value is migrating toward insights rather than optics. When Lytx clips surface automatically inside Geotab’s telematics console, safety managers spend less time chasing files and more time coaching drivers, a workflow efficiency that commands premium subscription tiers. Predictive risk scores that flag deteriorating trends before accidents occur are unlocking additional revenue streams, such as pay-as-you-drive insurance and automated compliance certifications. Services covering installation, training, and 24-hour support round out the stack, often bundled into fixed monthly fees that further smooth fleet cash flow.

Geography Analysis

North America accounted for 38.91% of the global video telematics market share in 2025. The region’s mature insurance ecosystem rewards fleets with 20-30% premium discounts for video-verified safety scores, which shortens payback periods to roughly 18 months. Federal audits that spotlight driver fatigue and hours-of-service records keep long-haul carriers on a steady upgrade path for dual-facing cameras and real-time alerting. Subscription bundles that bundle hardware, connectivity, and analytics into a single monthly fee appeal to small operators who lack the capital for large cash purchases. Cross-border fleets moving between the United States and Canada juggle diverging privacy rules, which sustains demand for configurable consent workflows and localized data storage.

Asia-Pacific is projected to post the fastest CAGR of 7.57% through 2031, lifting the regional video telematics market well above its 2025 baseline. China’s 2025 mandate for telematics devices in commercial vehicles has already sparked bulk orders from domestic logistics giants, while India’s ADAS guidelines are nudging heavy-goods carriers toward multi-camera configurations. Local suppliers gain an edge by offering dashboards in multiple languages and pricing that aligns with cost-sensitive owner-operators. Japan, South Korea, and Australia add further momentum with voluntary smart-transportation programs that emphasize accident reconstruction and real-time driver coaching.

Europe occupies a middle ground, with demand anchored by the July 2026 General Safety Regulation, which makes Data Event Recorders compulsory on all new vehicles. Onerous privacy requirements under GDPR Article 88 temper growth for driver-facing cameras, so vendors differentiate through granular privacy modes and automated data-redaction tools. South America, the Middle East, and Africa remain smaller outlets where limited cellular coverage slows live-streaming adoption, yet zero-upfront subscription models are beginning to unlock volume among cost-conscious fleets. Hybrid architectures that store routine footage on local devices and upload only flagged events help address both bandwidth constraints and sovereignty rules.

Regulatory Landscape

Regulation is increasingly shaping the minimum data-capture and recordkeeping capabilities tied to video telematics deployments across major fleet markets. In the European Union, the General Safety Regulation framework (Regulation (EU) 2019/2144, supported by Delegated Regulation (EU) 2024/2220) hardens requirements around Event Data Recorders for new vehicle types in heavier categories, with compliance milestones landing through 2026. This is pushing OEMs and fleet operators toward systems that can synchronize video with crash-relevant parameters. In parallel, UNECE Regulation No. 46 continues to set the technical baseline for camera-monitor systems in UNECE-aligned markets, reinforcing the need for type-approved hardware and documented installation practices.

Operational compliance obligations also affect how fleets store and share inspection and driving-record data alongside video. In the United States, FMCSA actions in 2026 advance digitization of compliance workflows, including a final rule enabling electronic creation and maintenance of Driver Vehicle Inspection Reports (DVIR) and a separate change removing the requirement to carry a printed ELD operator manual in-cab. In Great Britain, the UK Government has confirmed it will proceed with mandating a package of vehicle safety technologies for GB type approval, and the Information Commissioner’s Office (ICO) began reviewing vehicle surveillance guidance following the commencement of core provisions under the Data (Use and Access) Act 2025 (effective February 2026). Together, these steps elevate consent, retention, and access controls for driver-facing footage.

Value Chain Analysis

The video telematics value chain spans component suppliers (image sensors, processors, CAN and GNSS modules, cellular modems, and storage), device and camera manufacturers, connectivity providers, cloud infrastructure, and application-layer software that delivers safety scoring, incident workflows, and compliance reporting. Hardware OEMs and device makers integrate optics, edge compute, and local storage into dashcams and multi-camera systems. Telematics platform providers package devices with installation, connectivity, and recurring software subscriptions to deliver unified dashboards that combine GPS, ELD/DVIR-related data, and video clips. Downstream, fleets, insurers, and third-party service partners (installers, maintenance, and training providers) influence specification choices through underwriting requirements, claims workflows, and audit readiness.

Supply constraints and data-governance obligations are currently the most visible friction points in the chain. In 2025/2026, lead times for automotive-grade components such as CAN transceivers and GNSS modules have been reported at 20 to 30 weeks, and memory availability has tightened. This is raising per-unit device costs and pushing some vendors to tune storage footprints and edge-AI workloads. On the compliance side, evolving surveillance and data-handling expectations (for example, the UK Data (Use and Access) Act 2025 provisions effective February 2026 and UNECE-aligned technical rules for camera-monitor systems) increase demand for documented configurations, secure access controls, and retention policies, which shifts differentiation toward software, cloud governance, and services rather than camera hardware alone.

Competitive Landscape

The vendor environment remains fragmented, with no player controlling more than a mid-teens slice of global revenue. This dispersion leaves room for regional specialists and new entrants to target niches such as last-mile delivery or refrigerated trailers. Subscription economics continue to reshape buyer expectations by turning one-time capex into predictable opex, which increases customer lifetime value for software-centric platforms. Rising demand for edge-AI analytics shifts the competitive axis from camera hardware toward proprietary computer-vision models and large training datasets. As a result, providers that master both imaging and analytics enjoy a defensible moat even when hardware components become commoditized.

Samsara anchors the integrated-platform segment, turning USD 1.264 billion in annual recurring revenue and a 31% year-over-year jump in fiscal-Q3 2026 sales into sustained R and D outlays for driver-behavior scoring. Verizon Connect leverages its mobile network footprint to bundle connectivity and video, locking more than 3.5 million vehicles into multiyear agreements that are difficult to unwind. Lytx concentrates on AI-driven coaching that flags tailgating and phone distraction, while NetraDyne’s Driver-i platform emphasizes edge inference to reduce bandwidth needs. Smaller innovators such as Nauto and MiX Telematics continue to carve out share by focusing on urban safety analytics and region-specific compliance features.

Strategic alliances multiply as vendors seek faster access to new customer pools. Geotab’s integration of Surfsight cameras brings real-time clips into existing telematics dashboards without forcing fleets to rip out legacy hardware. Motive’s AI Dashcam Gen 3 pushes distraction detection to the device, proving that low-power inference silicon can cut cellular bills by streaming only critical incidents. Partnerships with truck OEMs, trailer builders, and insurance carriers strengthen distribution channels and embed cameras deeper into fleet workflows. Vendors that invest early in consent management, data-residency options, and over-the-air security updates are best positioned to win enterprise contracts in privacy-sensitive territories.

Video Telematics Industry Leaders

Sensata Technologies

Verizon Communications Inc.

Solera Holdings Inc.

FleetCam Pty Ltd

VisionTrack Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace sits in operationalizing video evidence beyond post-incident review by embedding it into day-to-day fleet workflows such as coaching, incident response, and compliance reporting. In 2026, vendors are productizing this shift through automation layers on top of installed camera fleets. NetraDyne, for instance, is launching an AI-agent driven workflow platform (Netradyne Intelligence) aimed at automating coaching, incident response, and safety reporting using existing Driver-i hardware. This creates room for solution bundles that combine edge AI event detection, standardized report generation, and role-based access controls for safety managers, claims teams, and dispatch, particularly for fleets that already use cloud telematics dashboards.

Regulatory and privacy change management also opens opportunities for differentiated consent and data-governance features in markets where worker monitoring is sensitive. The EU General Safety Regulation deadlines landing in 2026 raise the baseline for event data capture on new vehicles, while the UK Data (Use and Access) Act 2025 provisions effective February 2026 triggered an ICO review of vehicle surveillance guidance, increasing attention on access, retention, and transparency for in-cab footage. Products that offer configurable privacy modes, auditable access logs, and flexible retention by geography can support cross-border fleets operating under overlapping enforcement regimes, and help insurers and fleets operationalize video-verified claims and coaching without expanding compliance risk.

Recent Industry Developments

- July 2026: Verizon, through a partnership with KDDI, was named the U.S. connectivity provider for newly manufactured BMW Group vehicles, supporting 5G Standalone and LTE telematics. The move underlines how connectivity players are positioning automotive-grade network services as a foundation for data-intensive in-vehicle applications, including video-enabled safety and fleet workflows.

- May 2026: Solera introduced SmartDrive Pedestrian Collision Warning, adding an AI-driven driver assistance capability targeted at pedestrian-risk detection for fleets. Expanding ADAS-like functions inside video telematics ecosystems raises the value of software subscriptions by tying cameras to proactive risk reduction rather than only incident documentation.

- October 2025: Geotab announced the acquisition of Verizon Connect's international commercial operations in Europe and Australia. The deal strengthens Geotab's distribution and installed base outside North America and accelerates consolidation around unified fleet platforms where video, compliance, and telematics data are managed in a single environment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the video telematics market covers in-vehicle video capture plus connected telematics that transmit footage and event data for fleet safety, driver behavior review, incident investigation, and operational monitoring across commercial and passenger vehicles.

Scope exclusions: We exclude consumer-only dashcams that do not enable connected analytics workflows, and we also exclude pure ADAS hardware that is not sold as part of a video telematics solution.

Segmentation Overview

- By Type

- Integrated Systems

- Stand-Alone Systems

- By Vehicle Type

- Heavy Trucks

- Buses and Coaches

- Light Commercial Vehicles

- Passenger Cars

- By Deployment Model

- Cloud-Based

- On-Premises / Hybrid

- By Component

- Hardware

- Software and Analytics

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to lock the market boundary, map initial demand, and set adoption and pricing ranges before interviews started. We leaned on public, non-paywalled sources such as the International Transport Forum (OECD) for fleet and road-safety context, the US DOT and NHTSA for crash and compliance signals, Eurostat for regional vehicle and transport indicators, and UN Comtrade for electronics trade direction where it helped explain supply movement.

Alongside that, we reviewed company filings, earnings call transcripts, product brochures, and credible press to understand how offerings are bundled (hardware plus software and services) and how deployment is shifting toward cloud. To sanity-check company scale and deal momentum, we also referenced paid subscriptions for company financials and intelligence, news and financials, and patent databases for camera, AI, and analytics activity. The sources listed here are illustrative, and many other public references were used to collect data, validate assumptions, and clarify gaps during the study.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with fleet operators, channel partners, system integrators, insurers and safety program stakeholders, and solution teams involved in pricing and deployments. Since we are sizing a global market, coverage was balanced across major adoption regions so that usage patterns, camera count per vehicle, and subscription attach rates could be confirmed, then fed back into the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 22% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

The core model uses a top-down approach where the addressable vehicle parc and active fleet counts are converted into an adoption pool for video-enabled telematics, then translated into annual revenue using priced bundles. We then corroborate the totals using selective bottom-up approximations, including sampled ASP x volume checks based on channel feedback, and a roll-up of a limited set of supplier scale indicators to see if the total looks realistic.

Key inputs used in the model include the installed base in units (for example, 9.74 million units in 2025), the split of cloud versus on-premises deployments, average camera count per vehicle, subscription attach rates for software and analytics, and renewal behavior for service contracts. We also tracked mix shifts across vehicle types (such as heavier fleets versus light commercial fleets) because they affect camera density, data usage, and pricing.

Where bottom-up information was patchy for smaller countries, gaps were handled through proxy adoption rates tied to fleet intensity and enforcement signals, followed by regional consistency checks. For forecasting, scenario analysis was used, and the scenarios were anchored to expert consensus on how quickly cloud adoption, AI-enabled video analytics, and safety-driven procurement cycles are likely to progress. The base case was then smoothed with short-run trend checks so that year-on-year jumps only occur when they can be tied to a clear demand driver.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as installed base progression, cloud share direction, and typical subscription pricing ranges, then reviewed for outliers at the country and regional level. When a variance was too wide, we re-opened the assumption that caused it, and we re-contacted respondents to confirm whether the issue came from currency timing, bundle structure, or camera-per-vehicle differences.

Before sign-off, the model and its assumptions go through multi-step analyst review to remove math errors, double counting, and mix inconsistencies. Reports are refreshed annually, and interim updates are triggered when material changes affect adoption or pricing patterns. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Global Video Telematics Market Size Compared With Other Published Estimates

Published market sizes for video telematics can look far apart because they are not always counting the same thing, even when the titles sound similar. The biggest differences usually come from whether the estimate is built from installed base units or only annual shipments, whether software and services are counted consistently, and how currency conversion and price changes are handled over time.

In this study, the refresh cadence and currency timing were treated as first-order controls, and ASP logic was updated for cloud subscription mix and hardware share before totals were finalized, which is where the spread typically narrows for Mordor Intelligence. Some published figures also appear to blend adjacent categories like basic dashcams or broader fleet telematics, which can inflate or deflate the value depending on what gets pulled in and how renewals are treated.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.38 M (2026) | |

| Global Consultancy A | USD 0.62 B (2026) | Often values the market as annual revenue across hardware, software, and services, and may include wider fleet telematics bundles that are not strictly video-led, which pushes totals higher than an installed-base unit view. |

| Trade Journal B | USD 0.28 B (2025) | Typically uses shipment-led or camera hardware-only sizing with limited visibility into recurring subscriptions, and it may apply a single global ASP without adjusting for cloud mix and regional pricing. |

The table shows that the biggest swing comes from mixing unit-based installed base metrics with revenue-based definitions, and from how software subscriptions are counted. By keeping the scope tight and validating price and mix assumptions through interviews and consistency checks, the final numbers remain traceable to clear variables that can be re-run when conditions change.

Key Questions Answered in the Report

How large is the video telematics market today and how fast will it grow?

The sector stands at USD 10.38 million in 2026 and is projected to reach USD 14.28 million by 2031, reflecting a 6.59% CAGR during 2026-2031.

Which deployment model is most popular with fleet operators?

Cloud-based platforms dominate with 76.83% revenue share in 2025 because fleets value real-time streaming, centralized analytics, and seamless over-the-air updates.

What region will add users the fastest over the next five years?

Asia-Pacific is forecast to register the quickest expansion at a 7.57% CAGR through 2031, propelled by China’s 2025 telematics mandate and India’s ADAS guidelines.

Why are integrated systems preferred over stand-alone cameras?

They captured 62.37% of 2025 revenue because unified dashboards that blend video with GPS, maintenance, and driver-behavior data simplify investigations and reduce software overlap.

What are the biggest adoption hurdles for small and mid-size fleets?

Upfront hardware and installation costs that exceed USD 5,000 per vehicle, plus ongoing cellular fees for HD video, strain tight capital budgets.

How are regulations shaping product requirements?

Mandates such as the EU General Safety Regulation, FMCSA driver-monitoring rules, and China’s telematics laws are converting cameras from optional add-ons into compliance necessities that must log pre-crash data and driver activity.

Page last updated on: