Artificial Intelligence In Robotics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.25 Billion |

| Market Size (2031) | USD 51.8 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

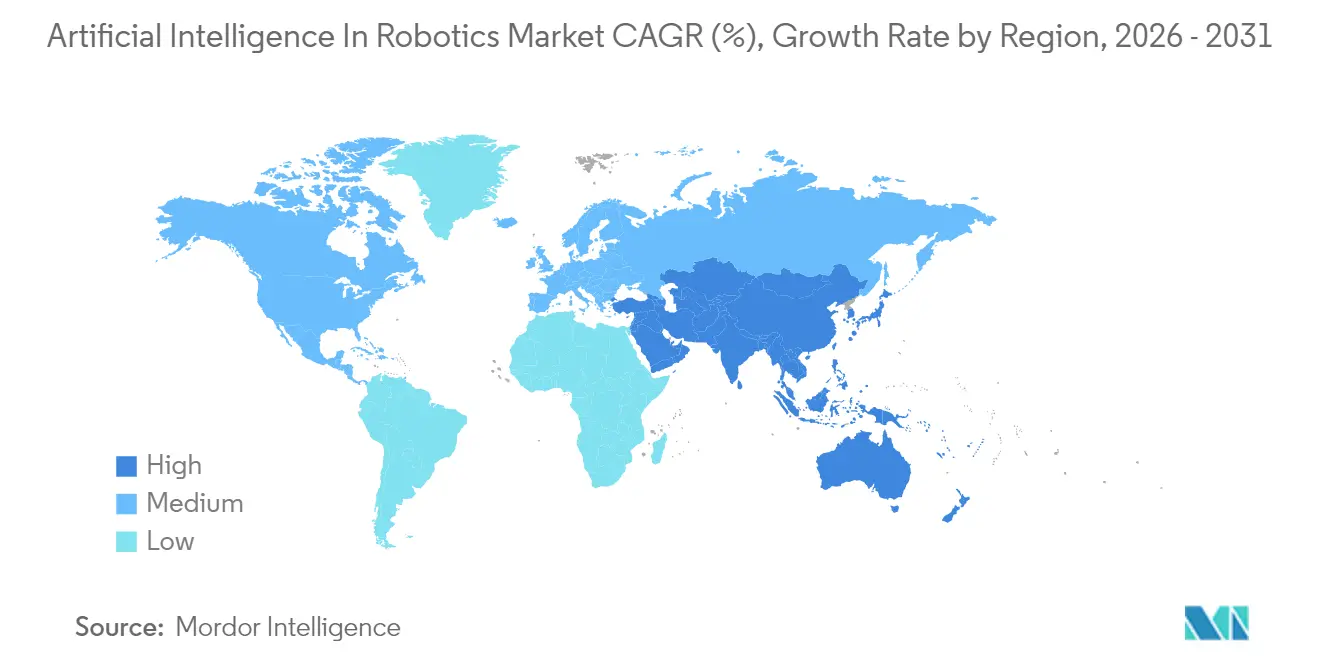

| Fastest Growing Market | Asia |

| Largest Market | Asia |

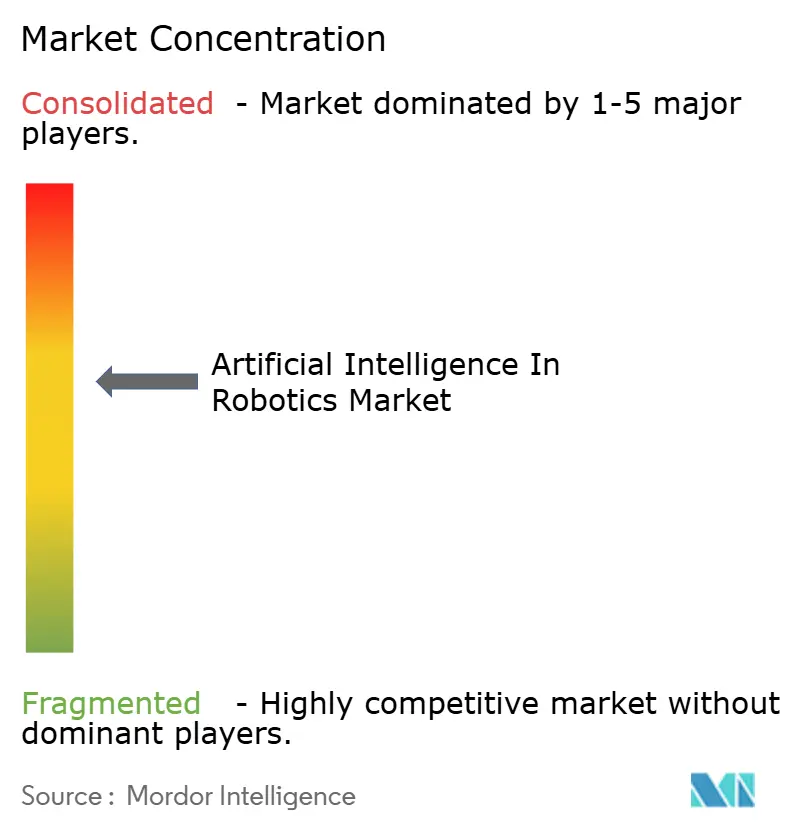

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence In Robotics Market Analysis by Mordor Intelligence

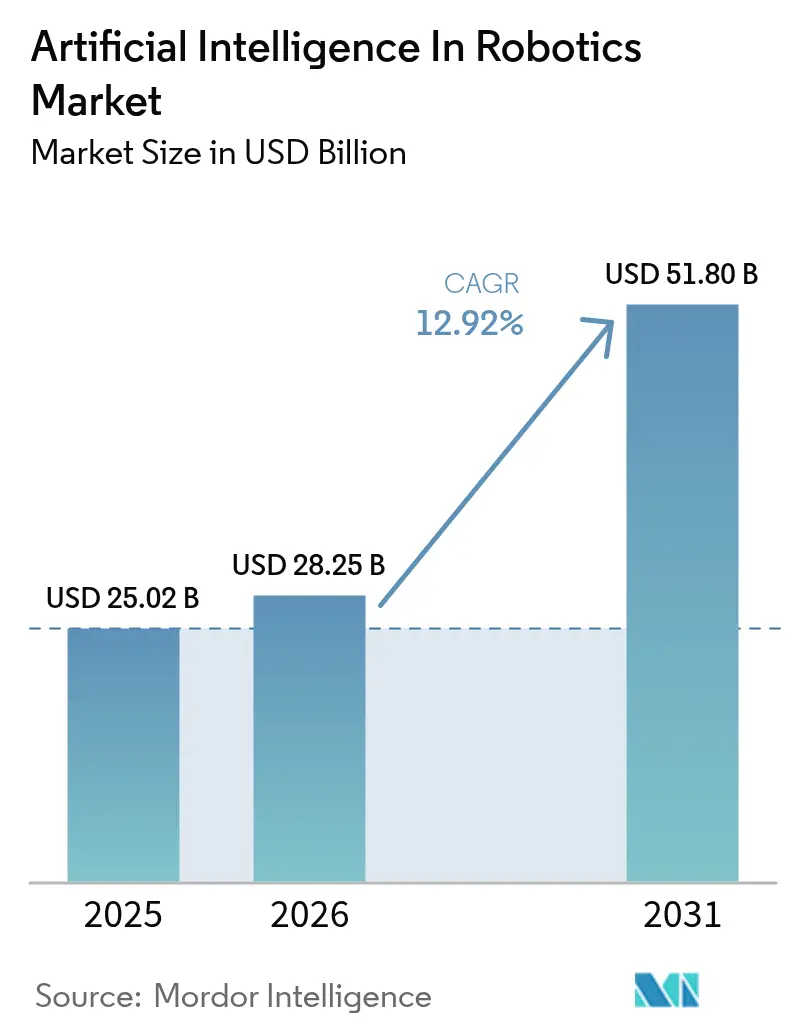

The Artificial Intelligence In Robotics Market size was valued at USD 25.02 billion in 2025 and estimated to grow from USD 28.25 billion in 2026 to reach USD 51.8 billion by 2031, at a CAGR of 12.92% during the forecast period (2026-2031).

Momentum is underpinned by rapid advances in edge computing, machine learning algorithms, and high-resolution sensor suites that allow robots to interpret their surroundings and act autonomously in milliseconds. Manufacturers are shifting from purely mechanical upgrades to intelligence-centric improvements, embedding custom AI processor modules that shorten decision latency on production lines and in service environments. Asia’s manufacturing investments, North America’s e-commerce boom, and Europe’s coordinated research programs are converging to expand deployment scenarios and accelerate time-to-value. Hardware remains a large cost driver, yet rising software attach rates illustrate how value creation is migrating toward perception, reasoning, and adaptive‐control stacks, turning robots into continuously learning assets within connected factory and logistics ecosystems. The combined effect of these trends is creating an ever-larger installed base of intelligent machines that complement, rather than displace, human operators, widening addressable demand for the AI in robotics market.

Key Report Takeaways

- By geography, Asia led with 46.55% revenue in 2025 and is forecast to grow at an 17.45% CAGR to 2031.

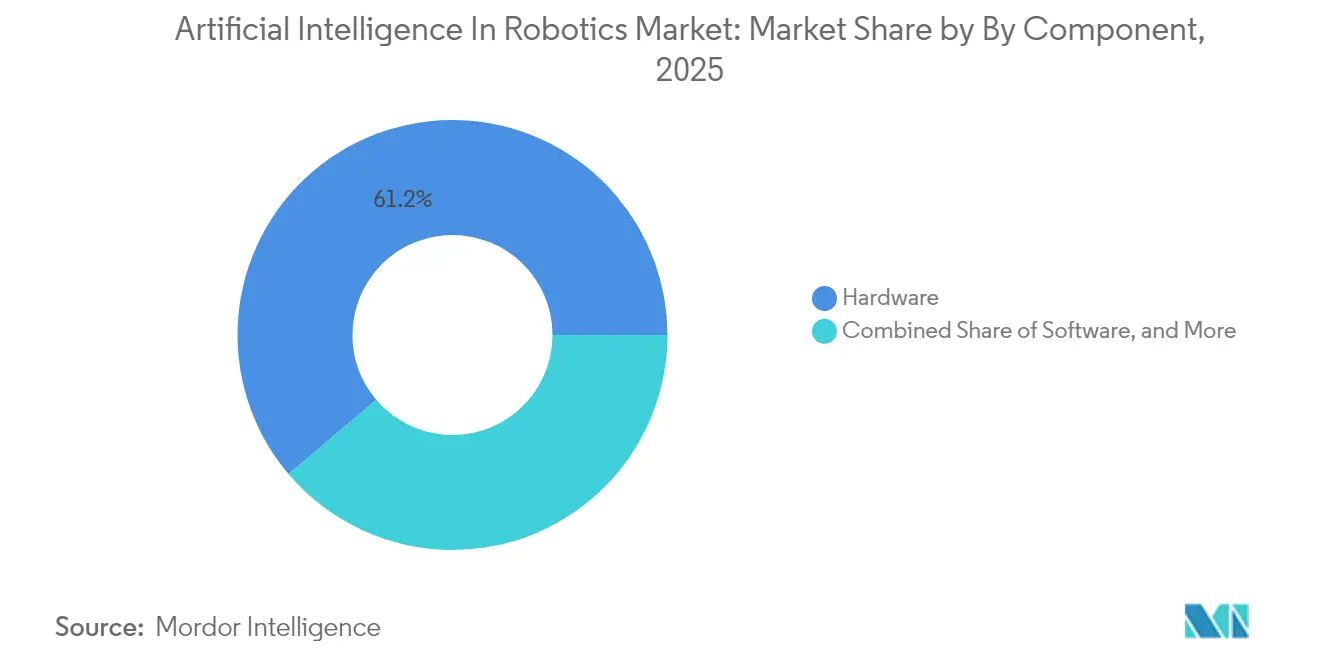

- By component, hardware captured 61.20% of the AI in robotics market share in 2025, while Machine Learning & Deep Learning software is expanding at a 23.10% CAGR through 2031.

- By robot type, industrial robots commanded 67.30% of the AI in robotics market size in 2025; medical & healthcare robots are projected to advance at a 24.85% CAGR through 2031.

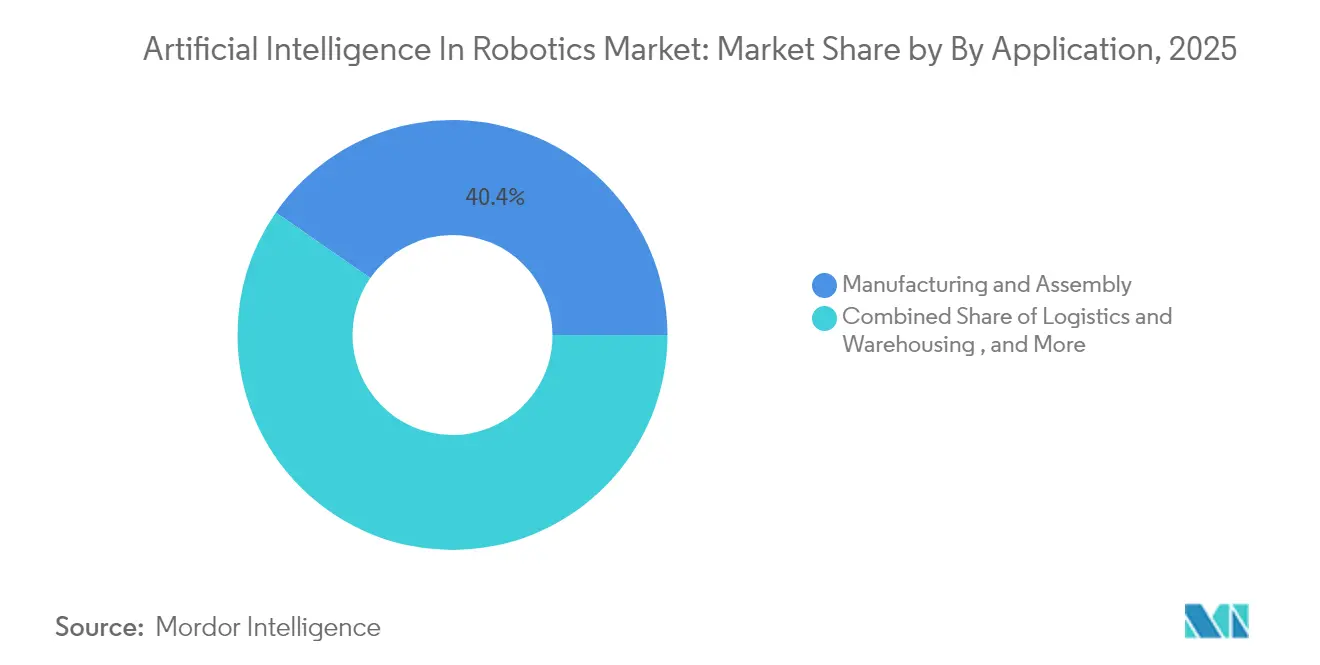

- By application, manufacturing and assembly accounted for 40.35% share of the AI in robotics market size in 2025, and logistics and warehousing are growing at a 23.95% CAGR to 2031.

- By end-user, automotive retained a 27.40% share in 2025, whereas healthcare is the fastest-growing end-user at 24.60% CAGR from 2026-2031.

- The top four industrial robot vendors (Fanuc, ABB, KUKA, Yaskawa) collectively held 56.75% market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence In Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Edge-AI Chips Enabling Real-Time Robot Decision-Making | +2.10% | Asia, spillover to North America | Medium term (2-4 years) |

| Rapid Aging Population Accelerating Demand for Elder-Care Robots | +1.80% | Japan, South Korea, spillover to Europe | Long term (≥ 4 years) |

| EU Horizon Europe Funding Streamlining Collaborative AI-Robot Research | +1.50% | Europe, global implications | Medium term (2-4 years) |

| E-Commerce Fulfilment Boom Driving AI-Enabled Warehouse Automation | +2.40% | North America, spillover to Europe & Asia | Short term (≤ 2 years) |

| Surge in Autonomous Mobile Robots within German Automotive Final Assembly Lines | +1.20% | Europe, spillover to North America | Medium term (2-4 years) |

| Falling Vision-Sensor Costs Allowing SMB AI-Retrofit Kits for Legacy Robots Globally | +1.70% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration of Edge-AI Chips Enabling Real-Time Robot Decision-Making

Edge-AI processors cut decision-making latency from seconds to milliseconds, enabling autonomous mobile robots (AMR) to navigate dynamic production floors without cloud dependence. Advantech’s 2025 showcase highlighted 75% faster response times after integrating NVIDIA Jetson Thor modules into AMR fleets. Electronics manufacturers in Shenzhen and Suwon report measurable gains in first-pass yield and takt-time reduction when vision and motion data are processed locally. Lower latency also tightens feedback loops for predictive maintenance, decreasing unscheduled downtime in precision assembly lines. As edge-optimized AI models mature, processor costs are falling, encouraging mid-tier suppliers to retrofit existing robots instead of purchasing new units. The driver, therefore, widens adoption across diverse factory footprints and contributes positively to the AI in robotics market .[1]NVIDIA, “Jetson ThNVIDIA, “Jetson Thor Product Brief,” nvidia.comor Product Brief,” nvidia.com

Rapid Aging Population Accelerating Demand for Elder-Care Robots

Japan’s share of residents aged 65 plus exceeded 29% in 2025, amplifying a projected shortfall of 377,000 caregivers.[2]Stat Bureau of Japan, “Population Estimates 2025,” stat.go.jpPanasonic, SoftBank, and startups backed by the Japanese government are rolling out mobility and social-companion robots that use deep neural networks to detect falls, remind medication schedules, and interact through natural speech. Clinical pilots show robots increase staff efficiency by reallocating repetitive lifting or monitoring tasks, letting nurses focus on direct patient engagement. South Korea faces similar demographic headwinds and is investing in AI robotic caregivers through its “Robot Industry Vision 2030” plan, which subsidizes hospital deployments and homecare trials. Success in these two cultural early adopters sets benchmarks for healthcare providers in Europe as their populations age, broadening future addressable demand for AI in the robotics market.

EU Horizon Europe Funding Streamlining Collaborative AI-Robot Research

The European Commission earmarked €550 million within Horizon Europe for digital research, allocating €50 million specifically to AI robotics testbeds. Projects such as EUROBIN and IntelliMan link universities, SMEs, and corporations in a shared-learning framework, lowering duplication of effort and accelerating prototype-to-market cycles. Consortia participants gain access to pan-European robot data repositories and common reference architectures, which improve interoperability and shorten certification timelines. Initial outputs include modular grippers and soft-robot manipulators that can handle diverse objects without reprogramming. The funding model also rewards knowledge sharing, subtly shifting competition from siloed R&D toward collaborative gains, which benefits the AI in robotics market through faster commercialization.

E-Commerce Fulfilment Boom Driving AI-Enabled Warehouse Automation

North America’s e-commerce parcels rose by 17% YoY in 2024, straining traditional labor-intensive fulfillment centers. FedEx’s minority stake in Nimble Robotics illustrates how logistics incumbents now embed AI robots for autonomous pick-pack-ship workflows. Reinforcement-learning algorithms allow each robot to refine grip strategies and traversal paths in live operations, improving throughput without floor layout changes. Warehouse operators report 2-digit gains in line-item accuracy and same-day shipping metrics. Importantly, AI robots work alongside humans, with safety-certified perception layers that pause or reroute when workers enter shared aisles, preserving ergonomic standards. The driver is expected to maintain momentum as retailers adopt micro-fulfilment centers closer to urban customers, underpinning sustained expansion of the AI in robotics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of High-Quality Domain Data for Niche Robot-Perception Tasks | −1.3% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| Fragmented Safety Standards Hindering Cross-Border Cobot Deployment | −1.5% | Europe & North America primarily | Short term (≤ 2 years) |

| High Up-Front Cost of AI Processor Modules for Low-Margin Food Processors | −0.8% | Global, higher impact in developing economies | Short term (≤ 2 years) |

| Cyber-Physical Security Concerns Limiting Cloud-Connected Service Robots in Hospitals | −1.1% | North America & Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of High-Quality Domain Data for Niche Robot-Perception Tasks

Frontiers in Robotics and AI highlights that inconsistent, incomplete datasets reduce the reliability of human-robot collaboration, especially where robots must recognize uncommon objects. For example, agricultural harvesters struggle to gauge ripeness across diverse crop varieties, limiting commercial deployment beyond pilot farms. Data gaps also impede safety validation, forcing vendors to over-engineer perception stacks and prolong time-to-market. Proprietary datasets give large incumbents a moat, making it harder for smaller innovators to match performance benchmarks. While synthetic data generation and transfer learning mitigate the barrier, the shortage remains a drag on the overall expansion of AI in the robotics market.

Fragmented Safety Standards Hindering Cross-Border Cobot Deployment

Collaborative robots must meet ISO 10218 mechanical safety rules and emerging AI governance principles, yet regional interpretations vary widely. An analysis in the European Journal of Risk Regulation argues for a unified “SmaCob” framework that marries robot safety with AI transparency requirements. Today, identical cobot models may need separate assessments for CE marking, OSHA compliance, and Canadian CSA standards, adding months to deployment schedules. Small and midsize integrators lack the compliance staff to navigate overlapping rules, narrowing their export ambitions. Harmonization talks within the EU and between IEC and IEEE committees are ongoing, but progress is incremental, leaving the restraint to weigh on near-term adoption in the AI in robotics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Masks Software Value Creation

Hardware accounted for 61.20% of the AI in robotics market share in 2025, reflecting the sensors, actuators, drives, and structural frames that give robots their physical presence. Capital-intensive industrial arms with integrated force-torque sensors remain indispensable for welding, painting, and precision material handling. Vendors are now shipping modular designs that let manufacturers swap grippers, cameras, or AI edge modules without full system overhauls, lowering total cost of ownership and prolonging equipment life cycles. Hardware roadmaps emphasize power-efficient servo controllers and lightweight composite joints, enabling higher payload-to-weight ratios crucial for mobile robots in tight factory aisles. Machine Learning & Deep Learning software is expanding at a 23.10% CAGR and is increasingly bundled as pre-trained perception and motion-planning libraries. These stacks extract more value from existing machines by enabling defect detection, predictive maintenance, and adaptive grasping without external programming. Early adopters report that software upgrades alone can raise overall equipment effectiveness by double digits, illustrating why software is outpacing physical spend despite its smaller baseline. Services covering integration, remote monitoring, and continuous model retraining form a rising annuity stream for vendors as customers seek lifecycle support. The shift underlines how intelligence rather than mechanics now differentiates competitors in the AI in robotics market.

By Robot Type: Industrial Robots Maintain Lead While Service Robots Accelerate

Industrial robots commanded 67.30% of the AI in robotics market size in 2025, led by articulated arms deployed in automotive and electronics production. Their installed base surpassed 4.28 million units in factories worldwide, a 10% annual gain that highlights entrenched demand. AI upgrades are letting these systems handle variable part geometries without downtime for re-teaching, boosting asset utilization. Cobots, still a minority of shipments, enjoy outsized growth as flexible automation becomes essential for high-mix, low-volume environments. Medical & healthcare robots represent the fastest-growing class at a 24.85% CAGR for 2026-2031. Surgical systems incorporating computer vision and force feedback assist clinicians in minimally invasive procedures, trimming post-operative complications and length of stay. Hospital logistics robots autonomously ferry linens and medications through crowded corridors using simultaneous localization and mapping (SLAM) fused with AI decision engines. Consumer acceptance is widening, evidenced by homecare robots that support daily living tasks for seniors. Altogether, these trends diversify revenue pools and mitigate cyclicality inherent in automotive-centric demand, benefiting the AI in robotics market.

By Application: Manufacturing Dominance Challenged by Logistics Growth

Manufacturing and assembly applications delivered 40.35% of revenue in 2025 as plants adopt AI for inline quality inspection, process optimization, and self-diagnosing maintenance cycles. Embedded vision stacks detect micro-cracks invisible to human inspectors and trigger immediate tool-path adjustments, preventing scrap accumulation. Edge analytics also pair with vibration sensors to predict bearing failures hours before catastrophic breakdowns, minimizing lost production. Those gains justify continued investments despite shorter product life cycles and higher customization requirements. Logistics & warehousing stands out with a 23.95% CAGR through 2031, fueled by e-commerce’s demand for accurate, same-day order fulfillment. Autonomous mobile robots navigate dynamic aisle layouts using LIDAR, ultrasonic sensors, and AI-enhanced routing algorithms that adapt to changing inventory positions in real time. Data gathered from tag-reading and vision systems feeds machine-learning models that refine pick sequencing and zone balancing on each shift. Healthcare & surgery, retail operations, and in-situ inspection services also scale rapidly, but logistics shows the clearest path from pilot to enterprise roll-out. These developments broaden commercial momentum for the AI in robotics market.

By End-User: Automotive Leadership Faces Healthcare Challenge

Automotive manufacturers retained a 27.40% revenue share in 2025 as they leverage AI robots for body-in-white welding, paint booths, and final assembly inspection. Integration of generative AI now accelerates programming of new model variants, cutting launch timelines and lowering engineering hours. Electric vehicle growth further boosts automation needs because battery pack assembly demands speed, cleanliness, and precision beyond conventional drivetrains. Consequently, robot density in leading German assembly plants rose to 1,500 units per 10,000 employees, the highest worldwide.Healthcare is rising fastest at a 24.60% CAGR, powered by demographic shifts and advances in minimally invasive tools. AI-guided surgical robots enable sub-millimeter accuracy and haptic feedback that enhance outcomes for orthopedics, cardiology, and oncology. Hospital administrations adopt robot fleets to sterilize rooms with UV-C light, reducing healthcare-associated infections without adding headcount. Electronics manufacturers, retailers, and food processors follow closely, each applying robots to unique pain points such as micro-component placement, on-shelf inventory scanning, and hygienic packaging. Collectively, diverse end-user uptake spreads risk and sustains long-term expansion of the AI in robotics market.

Geography Analysis

Asia Pacific generated 46.55% of global revenue in 2025 driven by extensive automation programs in China, Japan, and South Korea. China alone installed 276,288 industrial robots in 2023, equal to 51% of world shipments, as local authorities provide tax incentives and low-interest loans to upgrade manufacturing competitiveness ifr.org. Korean electronics firms add edge-AI vision to pick-and-place cells to manage wafer-level tolerances measured in microns, while Japanese automakers deploy AI cobots for final trim operations that require human-like dexterity. The region’s projected 17.45% CAGR reflects not only manufacturing dominance but also fast-emerging healthcare and service robotics pilots. North America ranks second, anchored by the United States where AI software expertise seeds robust startup formation and venture funding. Logistics giants retrofit existing conveyor grids with AI mobile robots to meet two-hour delivery windows. Automakers accelerate adoption as factories retool for battery electric vehicles, using AI to monitor weld quality on new lightweight materials. Canada’s mining sector pilots autonomous haulage trucks that leverage AI perception stacks to navigate open-pit sites in low-GPS conditions, extending AI in robotics market penetration beyond factory walls. Mexico’s industrial corridors likewise embrace AI retrofits to stay competitive following USMCA content rules. Europe emphasizes ethical, safe, and trustworthy AI, shaping both technology development and regulatory frameworks. Germany leads robot density with 28,355 new installations in 2023, aided by government subsidies for Mittelstand automation projects. Horizon Europe grants encourage academic-industry clusters in robotics for agri-tech, healthcare, and green manufacturing. Nonetheless, diverging interpretations of CE marking and AI liability delay cross-border deployments, particularly for cobots. Growth potential in Central and Eastern Europe remains high as labor shortages push factories to invest. Smaller markets in South America, the Middle East, and Africa are nascent but benefit from turnkey Robot-as-a-Service contracts that lower upfront capital barriers, nudging global uptake of the AI in robotics market.

Competitive Landscape

The AI in robotics market tilts toward moderate concentration, with the four largest industrial robot producers holding 57% share yet facing nimble AI software entrants. Fanuc and ABB embed proprietary edge controllers to add vision and force-control features without rewriting legacy ladder logic, protecting installed bases. NVIDIA’s Jetson ecosystem attracts a wide developer pool, making it the de facto standard for AI accelerator cards inside cobots and AMRs. IBM and Microsoft pivot from cloud-first strategies toward hybrid architectures, linking digital-twin simulations with on-premise inference to satisfy latency and sovereignty requirements.

Strategic alliances are multiplying. Siemens joined with IBM to couple OPC UA-based plant data with AI analytics, delivering predictive quality modules. KUKA cooperates with Orange Business for 5G private networks that connect swarm robots on automotive stations. Disruptors such as Boston Dynamics showcase quadruped robots for industrial inspection, while Hanson Robotics tests expressive humanoid greeters in hospitality. Specialized vertical players, including Blue River Technology in agriculture and Veo Robotics in safety-rated co-monitoring, carve niches via domain knowledge. Robot-as-a-Service subscription models, embraced by Universal Robots and Brain Corporation, shift budget conversations from capital to operating expenditure, broadening penetration among small and medium enterprises. Generative AI integration is the next battleground, with companies racing to combine large language models and multimodal perception to produce robots that can execute verbally described tasks, signaling an innovation cycle that will further expand the AI in robotics market.

Artificial Intelligence In Robotics Industry Leaders

Vicarious AI

Neurala, Inc.

Veo Robotics, Inc.

NVIDIA Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Rockwell Automation acquired Clearpath Robotics and OTTO Motors for USD 600 million, integrating autonomous navigation into its industrial portfolio.

- May 2025: Etron Technology unveiled its DeCloakBrain AipA Robotic System at Computex 2025, emphasizing privacy-preserving AI training for healthcare robots.

- April 2025: AeroVironment completed its USD 120 million takeover of Tomahawk Robotics, expanding AI-enabled control of heterogeneous unmanned systems.

- March 2025: Advantech demonstrated Edge-AI AMR platforms using NVIDIA Jetson Thor to enable millisecond decision loops in logistics applications.

Global Artificial Intelligence In Robotics Market Report Scope

Artificial intelligence in robotics refers to the seamless integration of robots with artificial intelligence (AI) technology. These robots learn to perform a few repetitive tasks that can be done without any human intervention and can even communicate with humans or, in some cases, with other robots.

The Artificial Intelligence in Robotics Market is segmented by Robot Type (Industrial Robots, Service Robots), End-User Industry (Automotive, Retail & Ecommerce, Healthcare, Food & Beverage), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

The market sizes and forecasts are provided in terms of value (in USD million) for all the above segments.

| Hardware | Sensors |

| Actuators | |

| Power Systems | |

| Control Systems | |

| Software | Machine Learning and Deep Learning |

| Computer Vision | |

| Natural Language Processing | |

| Context Awareness / Decision-Making | |

| Services | Integration and Deployment |

| Support and Maintenance |

| Industrial Robots | Articulated Robots | |

| SCARA Robots | ||

| Cartesian Robots | ||

| Collaborative Robots (Cobots) | ||

| Service Robots | Professional Service Robots | Logistics Robots |

| Medical and Healthcare Robots | ||

| Defense and Security Robots | ||

| Field Robots (Agriculture and Mining) | ||

| Personal and Domestic Robots | Household Robots | |

| Entertainment and Companion Robots | ||

| Manufacturing and Assembly |

| Logistics and Warehousing |

| Healthcare and Surgery |

| Retail and E-Commerce Operations |

| Food and Beverage Processing |

| Inspection and Maintenance |

| Other Applications |

| Automotive |

| Electronics and Semiconductors |

| Retail and E-Commerce |

| Healthcare |

| Food and Beverage |

| Aerospace and Defense |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| ASEAN | |

| Rest of Asia Pacific |

| By Component | Hardware | Sensors | |

| Actuators | |||

| Power Systems | |||

| Control Systems | |||

| Software | Machine Learning and Deep Learning | ||

| Computer Vision | |||

| Natural Language Processing | |||

| Context Awareness / Decision-Making | |||

| Services | Integration and Deployment | ||

| Support and Maintenance | |||

| By Robot Type | Industrial Robots | Articulated Robots | |

| SCARA Robots | |||

| Cartesian Robots | |||

| Collaborative Robots (Cobots) | |||

| Service Robots | Professional Service Robots | Logistics Robots | |

| Medical and Healthcare Robots | |||

| Defense and Security Robots | |||

| Field Robots (Agriculture and Mining) | |||

| Personal and Domestic Robots | Household Robots | ||

| Entertainment and Companion Robots | |||

| By Application | Manufacturing and Assembly | ||

| Logistics and Warehousing | |||

| Healthcare and Surgery | |||

| Retail and E-Commerce Operations | |||

| Food and Beverage Processing | |||

| Inspection and Maintenance | |||

| Other Applications | |||

| By End-user Industry | Automotive | ||

| Electronics and Semiconductors | |||

| Retail and E-Commerce | |||

| Healthcare | |||

| Food and Beverage | |||

| Aerospace and Defense | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East | United Arab Emirates | ||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

Key Questions Answered in the Report

What is the current size of the AI in robotics market and how fast is it growing?

The market stands at USD 28.25 billion in 2026 and is projected to expand to USD 51.8 billion by 2031, representing a 12.92% CAGR.

Which region leads the AI in robotics market today?

Asia holds 46.55% of global revenue in 2025 and is forecast to grow at an 17.45% CAGR, driven by large-scale manufacturing automation and supportive government policies.

Which application segment is expanding the fastest?

Logistics and warehousing is the fastest-growing application, advancing at a 23.95% CAGR as e-commerce operators deploy AI-enabled autonomous mobile robots for high-speed order fulfillment

How are edge-AI chips influencing industrial adoption?

Edge-AI processors slash decision latency from seconds to milliseconds, allowing robots to operate without cloud connections and boosting first-pass yields and throughput on production lines.

Who are the key vendors shaping competitive dynamics?

Industrial leaders such as Fanuc, ABB, KUKA, and Yaskawa command 56.75% market share, while AI specialists like NVIDIA and IBM are partnering with hardware makers to deliver end-to-end solutions.

Is the market highly concentrated or fragmented?

With the top five suppliers controlling just over 60% of revenue, the sector scores 6 on a 1–10 concentration scale, indicating moderate concentration and room for emerging players to gain share.

Page last updated on: