AI Protein Engineering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 4.75 Billion |

| Growth Rate (2026 - 2031) | 21.20% CAGR |

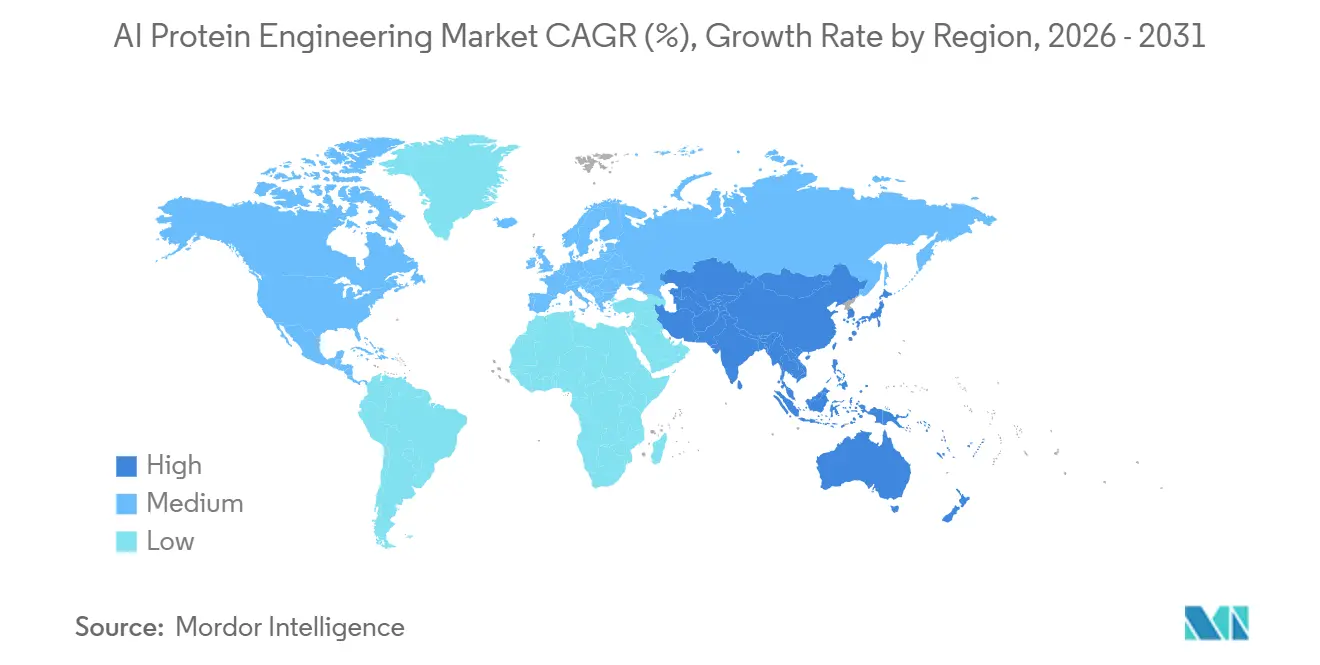

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

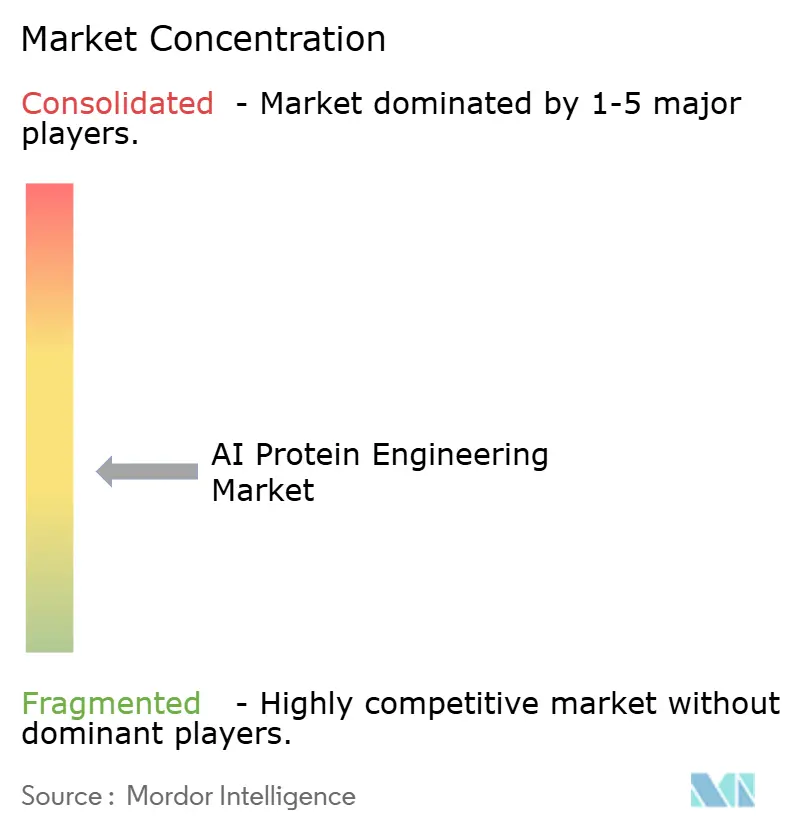

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Protein Engineering Market Analysis by Mordor Intelligence

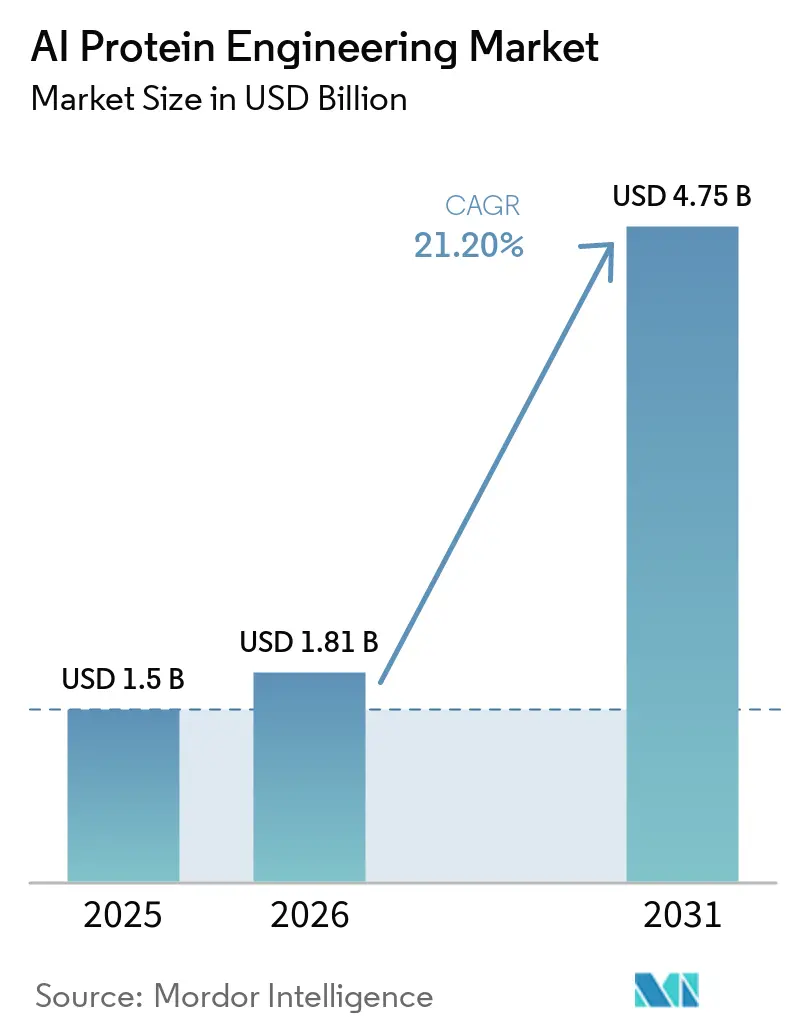

The AI Protein Engineering Market size is projected to expand from USD 1.5 billion in 2025 and USD 1.81 billion in 2026 to USD 4.75 billion by 2031, registering a CAGR of 21.20% between 2026 to 2031.

AI-designed molecules are now entering late-stage clinical development, marking a pivotal shift in how large biopharma companies evaluate platform risk and partnership value. By December 2025, GENERATE:BIOMEDICINES advanced GB-0895 into global Phase 3 trials, enrolling 1,600 patients across over 40 countries. This demonstrates the efficiency of their "design-build-test-learn" infrastructure in accelerating the development of assets compared to traditional protein engineering timelines.[1]Generate:Biomedicines, “Generate:Biomedicines To Initiate Global Phase 3 Studies Of GB-0895, A Long-Acting Anti-TSLP Antibody For Severe Asthma Engineered With AI,” PR Newswire, prnewswire.com Regional momentum remains uneven, with North America maintaining the strongest commercial base. Meanwhile, the Asia-Pacific region benefits from policy support for AI and biomanufacturing integration, which expands the long-term demand for platforms that combine software, automation, and translational execution.

Key Report Takeaways

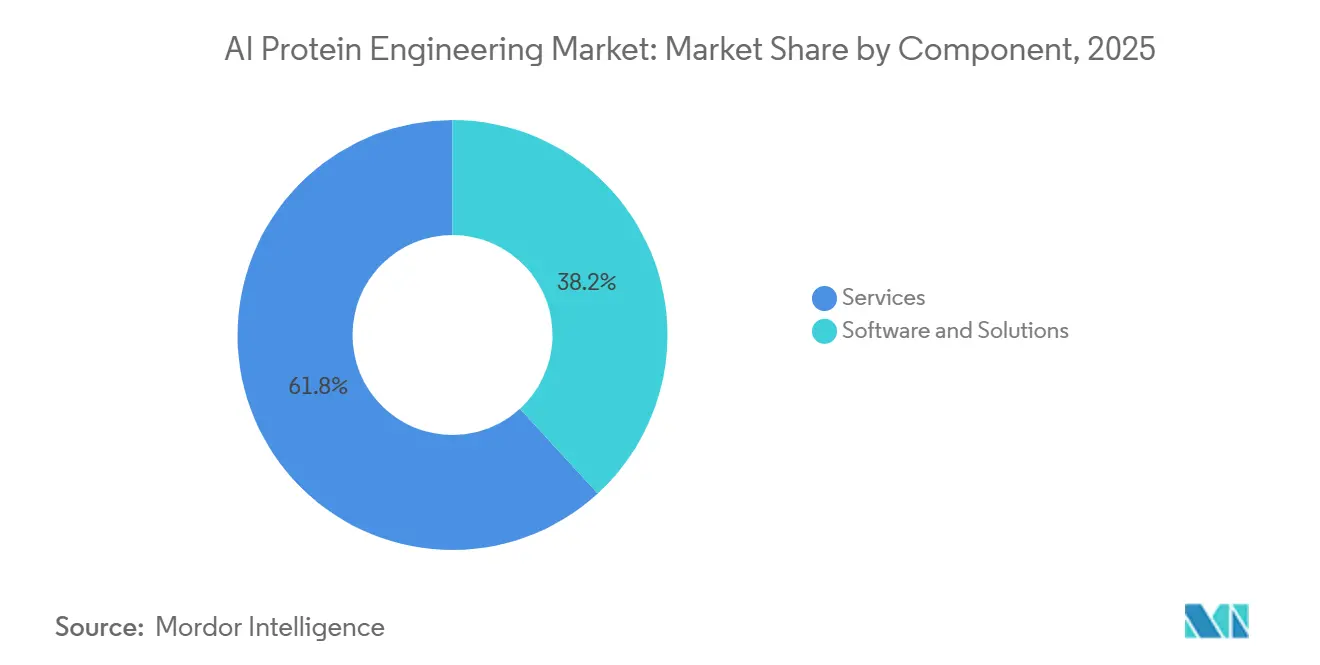

- By component, software & solutions held 38.2% revenue share in 2025, while services is projected to expand at a 21.05% CAGR through 2031.

- By protein type, monoclonal antibodies led with 39.78% revenue share in 2025, while vaccines & antigens is projected to grow at a 21.76% CAGR through 2031.

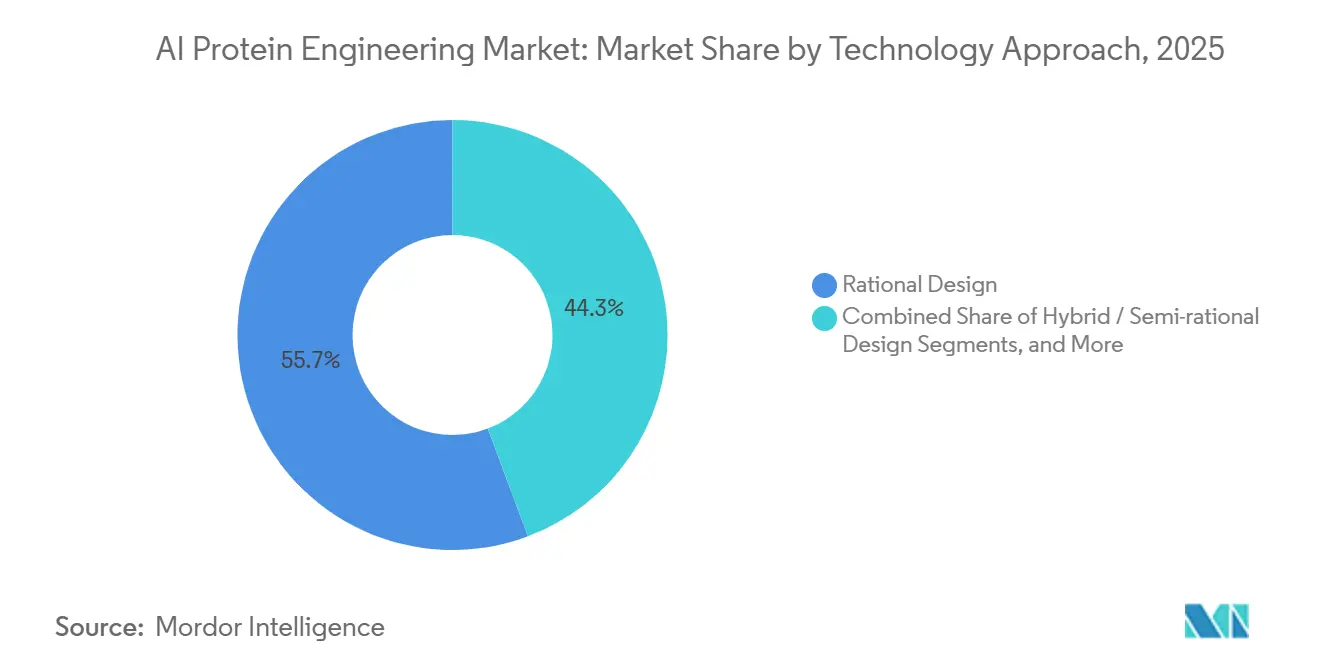

- By technology approach, rational design held 55.72% of the AI in protein engineering market share in 2025, while hybrid or semi-rational design recorded the highest projected CAGR at 22.15% through 2031.

- By application, drug discovery & biologics accounted for 46.1% share of the AI in protein engineering market size in 2025 and is projected to grow at a 22.75% CAGR through 2031.

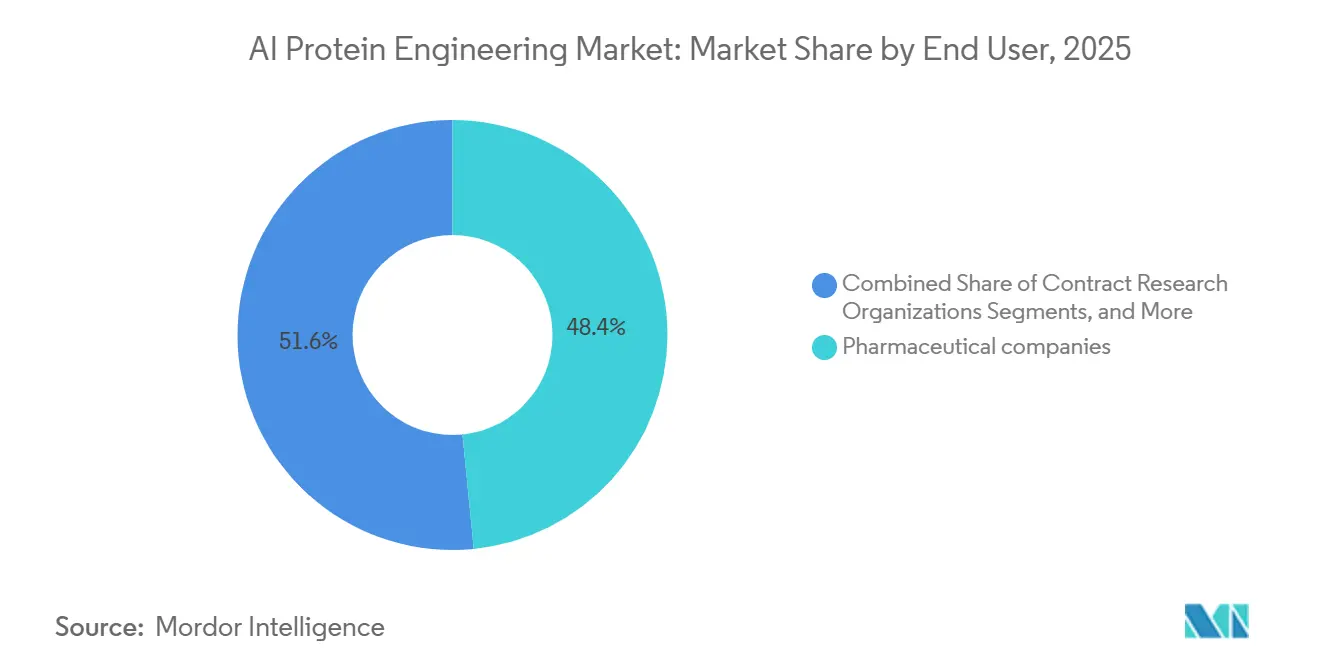

- By end user, pharmaceutical companies held 48.42% revenue share in 2025, while contract research organizations are projected to grow at a 23.67% CAGR through 2031.

- By deployment mode, cloud captured 77.9% of 2026 revenues and is also the fastest-growing sub-segment with a 23.55% CAGR through 2031.

- By geography, North America held 44.32% revenue share in 2025, while Asia-Pacific is projected to expand at a 24.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Protein Engineering Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Biopharma demand for faster biologics discovery | +5.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Protein foundation models improving de novo hit generation | +4.8% | Global, with Asia-Pacific catching up rapidly | Medium term (2-4 years) |

| Wet-lab automation closing the design-build-test loop | +4.2% | North America, United Kingdom, China, Japan | Medium term (2-4 years) |

| Multispecific antibody complexity favoring AI-native design stacks | +3.9% | North America and Europe core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of enzyme engineering in industrial biotech and food systems | +2.5% | Asia-Pacific core, North America, Europe | Long term (≥ 4 years) |

| Proprietary assay-data network effects strengthening platform economics | +1.8% | Global, with North America ahead | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biopharma Demand for Faster Biologics Discovery

The AI in protein engineering market is growing as drug developers prioritize faster biologics discovery, reduced iteration burdens, and access to challenging targets. Absci demonstrated its platform's ability to advance ABS-201 from a preclinical concept to three dosed Phase 1 cohorts in two years, showcasing AI's role in shortening development cycles. The platform also showed that fewer than 100 designs per target could generate candidates for zero-prior epitopes, reducing reliance on large-scale screening.[2]Absci Corporation, “Absci Reports Business Updates And Fourth Quarter And Full Year 2025 Financial And Operating Results,” GlobeNewswire, globenewswire.com Partnerships with major pharmaceutical companies and significant funding indicate that this demand is integral to R&D strategies. Platforms integrating model output, experimental follow-up, and delivery are gaining traction over those offering standalone software.

Protein Foundation Models Improving De Novo Hit Generation

Advancements in foundation models that integrate sequence, structure, and function are driving the AI in protein engineering market. EvolutionaryScale's ESM3, trained on 2.8 billion protein sequences with 1.1 x 10^24 FLOPS, created novel fluorescent proteins equivalent to 500 million years of natural evolution, marking a leap in de novo design.[3]Daniel J. Hayes et al., “Simulating 500 Million Years Of Evolution With A Language Model,” Science, science.org This progress narrows the gap between AI-designed and traditionally discovered proteins, increasing AI's credibility for therapeutic and industrial applications. As model quality improves across the industry, proprietary experimental feedback is becoming a key differentiator. Companies with robust internal validation processes are better positioned to maintain competitive advantages.

Wet-lab Automation Closing the Design-build-test Loop

Wet-lab automation is critical for converting digital designs into commercial outputs, making it a cornerstone of the AI in protein engineering market. A study combining ESM-2 with a robotic biofoundry achieved four iterative design-build-test-learn cycles in 10 days, with a 62.5% positive hit rate in the third round compared to 2.2% for random mutagenesis. Ginkgo Bioworks is expanding its autonomous lab with over 50 Reconfigurable Automation Carts by 2026 and installing customized systems for clients. Government investments in automation further highlight its strategic importance. Companies that scale computational and experimental layers together are better positioned to control the entire process and enhance pricing power.

Multispecific Antibody Complexity Favoring AI-native Design Stacks

Rising interest in multispecific and bispecific antibodies is driving demand for AI-driven design systems in the AI in protein engineering market. These systems handle complex combinatorial spaces while managing constraints like affinity, stability, and manufacturability. Profluent's ProGen3, trained on over 3.4 billion protein sequences, achieved single-shot antibody designs across 20 drug targets, supporting broader generative applications. Latent Labs' Latent-X2 model generated antibodies and nanobodies that passed immunogenicity assessments without post-generation optimization, reducing designs per target to 4–24. These advancements make complex formats economically viable, expanding commercial opportunities for the market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Experimental validation bottlenecks and wet-lab cost intensity | -1.8% | Global, most acute in emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Biosecurity and regulatory scrutiny for novel proteins | -1.4% | North America and Europe primarily | Medium term (2-4 years) |

| Training-data provenance and IP ambiguity | -1.6% | Global, most acute in emerging Asia-Pacific markets | Short term (≤ 2 years) |

| GPU access and sovereign-compute constraints | -1.5% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Experimental Validation Bottlenecks and Wet-lab Cost Intensity

The AI in protein engineering market faces bottlenecks as in silico sequence generation outpaces laboratory validation. Each design-build-test-learn cycle of 96 variants still requires 59 hours of wet-lab processing, making the process capital-intensive even with robotics. This limits smaller biotech firms and academic teams that lack funding for automated infrastructure or repeated experimental rounds. Consequently, activity is concentrated in well-funded hubs with advanced resources like cloud computing and automation. Until cost-effective validation models are accessible, regional growth in this market will remain uneven.

Biosecurity and Regulatory Scrutiny for Novel Proteins

The AI in protein engineering market is under scrutiny due to generative systems creating de novo sequences that differ significantly from natural proteins. Current DNA synthesis screening systems may not reliably detect structurally novel but potentially harmful proteins. Existing governance frameworks are not equipped to handle algorithmic protein design and lack enforcement mechanisms for AI-generated sequence data. This regulatory uncertainty complicates intellectual property strategies, outsourced synthesis, and international collaborations. As a result, commercialization in this market faces delays, particularly in areas requiring cross-border manufacturing and regulatory alignment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Software on Partnership Intensity

In 2025, Software & Solutions held a 38.20% share of the AI in protein engineering market, reflecting early adoption trends. Biopharma users preferred software access to integrate protein language models rather than outsourcing entire programs. Schrödinger reported USD 199.5 million in software revenue, with top 20 pharma contract value rising 15.3% to USD 80.8 million. This phase allowed companies to test AI within existing workflows, aligning with internal procurement structures. Services are projected to grow at a 21.05% CAGR through 2031, as buyers increasingly seek end-to-end support for AI-designed programs nearing clinical use.

By Protein Type: Monoclonal Antibodies Lead While Vaccines Accelerate

Monoclonal antibodies accounted for 39.78% of revenue in 2025, leading due to their established development and regulatory pathways. AI is reshaping this mature protein class, reducing experimental burdens in workflows. Vaccines & Antigens are expected to grow at a 21.76% CAGR through 2031, driven by regulatory approvals like SKYCovione. This growth expands the market from therapeutic antibodies to include prophylactic and antigen design programs, making vaccine-related work a credible extension of protein design.

By Technology Approach: Rational Design Remains the Base While Hybrid Methods Gain Ground

Rational Design held a 55.72% market share in 2025, maintaining its role as the foundational computational approach in biopharma. Its dominance stems from interpretable workflows that align with scientific practices. Hybrid or Semi-rational Design is forecast to grow at a 22.15% CAGR through 2031, combining physics-based and generative methods to address complex design challenges. This approach balances speed and scientific rigor, integrating AI into trusted workflows without replacing established methods.

By Application: Drug Discovery and Biologics Keep the Core Position

Drug Discovery & Biologics captured 46.1% of the market in 2025, reflecting the pharmaceutical sector's focus on clinical-stage assets. AI-enabled rapid discovery processes are reshaping target selection economics. This segment is projected to grow at a 22.75% CAGR through 2031, as AI-designed molecules in development reduce risk premiums for partnerships. The focus on therapeutics ensures drug discovery remains central to capital allocation and platform differentiation.

By End User: Pharmaceutical Companies Lead While CROs Scale Quickly

Pharmaceutical Companies represented 48.42% of end-user revenues in 2025, driven by their ability to fund multi-year AI collaborations and integrate new platforms. Contract Research Organizations are projected to grow at a 23.67% CAGR through 2031, aggregating demand from smaller biotechs lacking internal resources. This trend highlights the growing importance of outsourced execution models, even as large pharmaceutical companies remain the largest buyers.

By Deployment Mode: Cloud Remains Dominant and Continues to Accelerate

Cloud accounted for 77.90% of deployment mode revenues in 2026, driven by the computational demands of large protein models. Its projected 23.55% CAGR through 2031 reflects the shift toward hosted environments, as users prioritize scalability and collaboration. On-premises systems retain niche value for specific needs, but the market remains centered on cloud delivery due to its advantages in model size and workflow orchestration.

Geography Analysis

In 2025, North America held a 44.32% share of the AI in protein engineering market, maintaining its position as the largest regional cluster by revenue, company concentration, and commercial readiness. This leadership is driven by strong biopharma ecosystems, significant venture capital investments, and a high density of foundational model start-ups collaborating with drug developers and translational labs. The region benefits from efficient integration between platform companies, wet-lab infrastructure, and capital providers, which accelerates the transition from discovery to funded development programs. Large-scale funding rounds further highlight the region's ability to attract global capital.

Europe holds a smaller share of the AI in protein engineering market but remains technically significant due to public research funding, academic expertise in protein engineering, and active translational projects feeding commercial pipelines. Funding initiatives, such as support for general-purpose protein engineering and autonomous bioprocess development, strengthen the scientific base that supports start-ups and collaborative industry programs. Research groups are advancing tools and systems for translational use, extending Europe’s role from basic science to commercialization pathways. While smaller in scale, Europe contributes to method development, talent creation, and spin-out opportunities.

Asia-Pacific is forecast to grow at a 24.25% CAGR through 2031, making it the fastest-growing region in the AI in protein engineering market. Growth is driven by policy support, expanding biosynthetics capabilities, and the development of local datasets and platform companies in key countries like China, Japan, South Korea, and Australia. Regional initiatives, such as directives to integrate AI and biomanufacturing and advancements in protein sequence databases, are accelerating progress. While still in early stages, the Middle East, Africa, and South America are building familiarity with AI-designed biologics through participation in global clinical trial networks.

Competitive Landscape

The AI in protein engineering market is moderately fragmented. A few well-capitalized platform companies operate alongside a diverse group of specialist model developers, design providers, and research-driven entrants. Leading players like Isomorphic Labs, Recursion Pharmaceuticals, Generate:Biomedicines, and Schrödinger leverage strong capital access, data assets, and clear translational pathways. Competitive advantages are being built across software, data generation, automation, and partnerships, creating a market where a few leaders influence direction without any single entity dominating.

Several strategic moves since 2025 highlight this evolving structure. In May 2026, Isomorphic Labs raised USD 2.1 billion to scale its AI drug design engine and advance clinical development programs, strengthening its competitive position. Schrödinger’s 2026 launch of Bunsen and its focus on LiveDesign Biologics reflect a deeper move into biologics and workflow automation, increasing competition for newer protein design firms. Ginkgo Bioworks emphasized autonomous laboratory infrastructure in 2026, showcasing experimental capacity as a strategic asset. Tsinghua University’s iAutoEvoLab patent activities demonstrate a shift in defensibility toward hardware-software systems supporting continuous evolution workflows.

Open space remains in industrial enzyme design, food protein design, CRO-embedded services, and deployment models adhering to data-residency rules across jurisdictions. In July 2025, Lesaffre’s internal use of protein language model-guided engineering indicates that some food-sector demands are still managed internally, leaving room for specialist vendors to offer effective workflow solutions. BioGeometry achieved a 52.3-fold improvement in transaminase catalytic activity and 99.7% stereoselectivity gains in 55 days using AI-driven optimization, proving that impactful solutions can emerge outside major funding circles.

AI Protein Engineering Industry Leaders

Absci

Cradle

Evozyne

EvolutionaryScale

Insilico Medicine

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Isomorphic Labs secured USD 2.1 billion in Series B funding led by Thrive Capital, with participation from Alphabet, Temasek, MGX, and the UK Sovereign AI Fund. The investment aims to scale its IsoDDE drug design engine and accelerate therapeutic pipeline programs toward clinical trials, following partnerships with Novartis, Eli Lilly, and Johnson & Johnson valued at nearly USD 3 billion.

- April 2026: ProQR Therapeutics announced a partnership with Ginkgo Bioworks, gaining access to Ginkgo's Nebula autonomous laboratory with over 50 instruments. The collaboration includes a strategic equity investment by Ginkgo, with ProQR expecting a clinical trial application from an AI-generated program by mid-2026.

- February 2026: Ginkgo Bioworks announced a strategic refocus on autonomous laboratory technology, replacing manual lab benches with a large-scale autonomous lab. The company divested its biosecurity business and highlighted a collaboration with OpenAI using GPT-5, which improved cell-free protein synthesis by 40%.

Global AI Protein Engineering Market Report Scope

As per the scope of the report, AI protein engineering is the use of machine learning and deep learning to design, predict, and optimize synthetic proteins with specific biological functions. It replaces traditional trial-and-error lab methods by predicting how amino acid sequences fold into 3D structures and generating custom proteins for medicines or sustainable materials.

The AI protein engineering market is segmented by component, protein type, technology approach, application, end-user, and geography. By component, the market includes software & solutions and services. By protein type, the market is categorized into monoclonal antibodies, enzymes, peptides & miniproteins, vaccines & antigens, and cytokines & growth factors. By technology approach, the market is segmented into rational design, directed evolution, de novo design, hybrid/semi-rational design, and physics-informed simulation. By application, the market includes drug discovery & biologics, enzyme engineering & industrial biotechnology, agricultural & food proteins, vaccines & immunotherapy design, synthetic biology & research tools, and diagnostics & biosensors. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, contract research organizations, academic & research institutes, and agri-food & industrial biotechnology companies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software & Solutions |

| Services |

| Monoclonal Antibodies |

| Enzymes |

| Peptides & Miniproteins |

| Vaccines & Antigens |

| Cytokines & Growth Factors |

| Rational Design |

| Directed Evolution |

| De Novo Design |

| Hybrid / Semi-rational Design |

| Physics-informed Simulation |

| Drug Discovery & Biologics |

| Enzyme Engineering & Industrial Biotechnology |

| Agricultural & Food Proteins |

| Vaccines & Immunotherapy Design |

| Synthetic Biology & Research Tools |

| Diagnostics & Biosensors |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Contract Research Organizations |

| Academic & Research Institutes |

| Agri-food & Industrial Biotechnology Companies |

| Cloud |

| On-premises |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software & Solutions | |

| Services | ||

| By Protein Type | Monoclonal Antibodies | |

| Enzymes | ||

| Peptides & Miniproteins | ||

| Vaccines & Antigens | ||

| Cytokines & Growth Factors | ||

| By Technology Approach | Rational Design | |

| Directed Evolution | ||

| De Novo Design | ||

| Hybrid / Semi-rational Design | ||

| Physics-informed Simulation | ||

| By Application | Drug Discovery & Biologics | |

| Enzyme Engineering & Industrial Biotechnology | ||

| Agricultural & Food Proteins | ||

| Vaccines & Immunotherapy Design | ||

| Synthetic Biology & Research Tools | ||

| Diagnostics & Biosensors | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Contract Research Organizations | ||

| Academic & Research Institutes | ||

| Agri-food & Industrial Biotechnology Companies | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of AI in protein engineering?

The AI in protein engineering market stands at USD 1.81 billion in 2026 and is forecast to reach USD 4.75 billion by 2031 at a 21.2% CAGR.

Which region leads revenue generation in this space?

North America led with 44.32% share in 2025, supported by strong biopharma clusters, deep capital access, and a high concentration of AI-native platform companies.

Which region is expanding the fastest through 2031?

Asia-Pacific is projected to grow at a 24.25% CAGR through 2031, driven by policy support, local dataset expansion, and rising commercialization activity.

Which application area contributes the most revenue?

Drug Discovery & Biologics was the largest application area with 46.1% share in 2025 and is also the fastest-growing application segment at 22.8% CAGR.

Why are services growing faster than software tools?

Services are growing faster because biopharma buyers increasingly prefer end-to-end design and execution support instead of only licensing software into internal workflows.

What is the biggest operational constraint on adoption?

The main constraint is still experimental validation capacity, since wet-lab throughput, automation access, and validation cost remain limiting factors even when in silico design becomes faster.

Page last updated on: