AI In Bioinformatics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.89 Billion |

| Market Size (2031) | USD 25.21 Billion |

| Growth Rate (2026 - 2031) | 16.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Bioinformatics Market Analysis by Mordor Intelligence

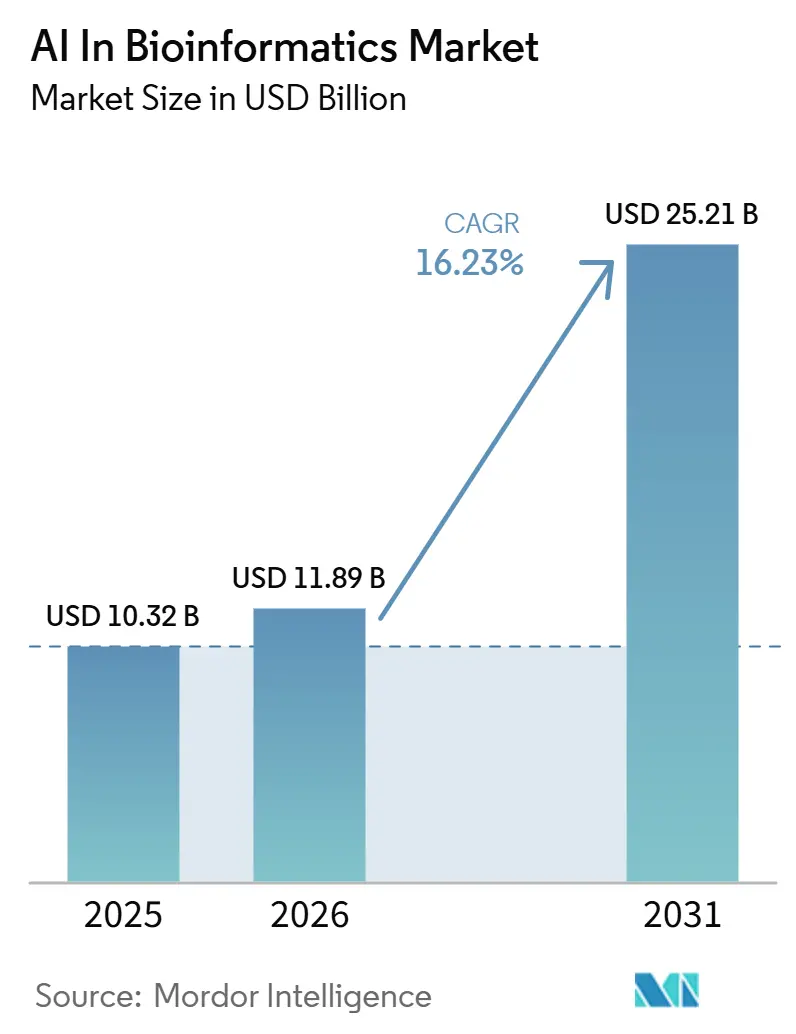

The AI in bioinformatics market is expected to grow from USD 10.32 billion in 2025 to USD 11.89 billion in 2026 and is forecasted to reach USD 25.21 billion by 2031 at 16.23% CAGR over 2026-2031. The AI in bioinformatics market is being reshaped by AI-native platforms that are replacing rule-based bioinformatics tools in core analysis workflows. The AI in bioinformatics market is also expanding because genomic sequencing volumes now exceed what human analysts can interpret with manual or rules-driven methods. Pharmaceutical companies are moving beyond software procurement and are taking direct ownership positions in AI-driven discovery infrastructure, which is changing how value is captured across the AI in bioinformatics market. Competition remains split between genomics and diagnostics incumbents on one side and AI-native specialists on the other, while acquisition activity shows that larger healthcare companies are increasingly buying AI capability instead of building it internally. Regulatory validation demands remain the main brake on deployment in clinical and GxP settings, which favors vendors that already have strong compliance, documentation, and audit frameworks in place.

Key Report Takeaways

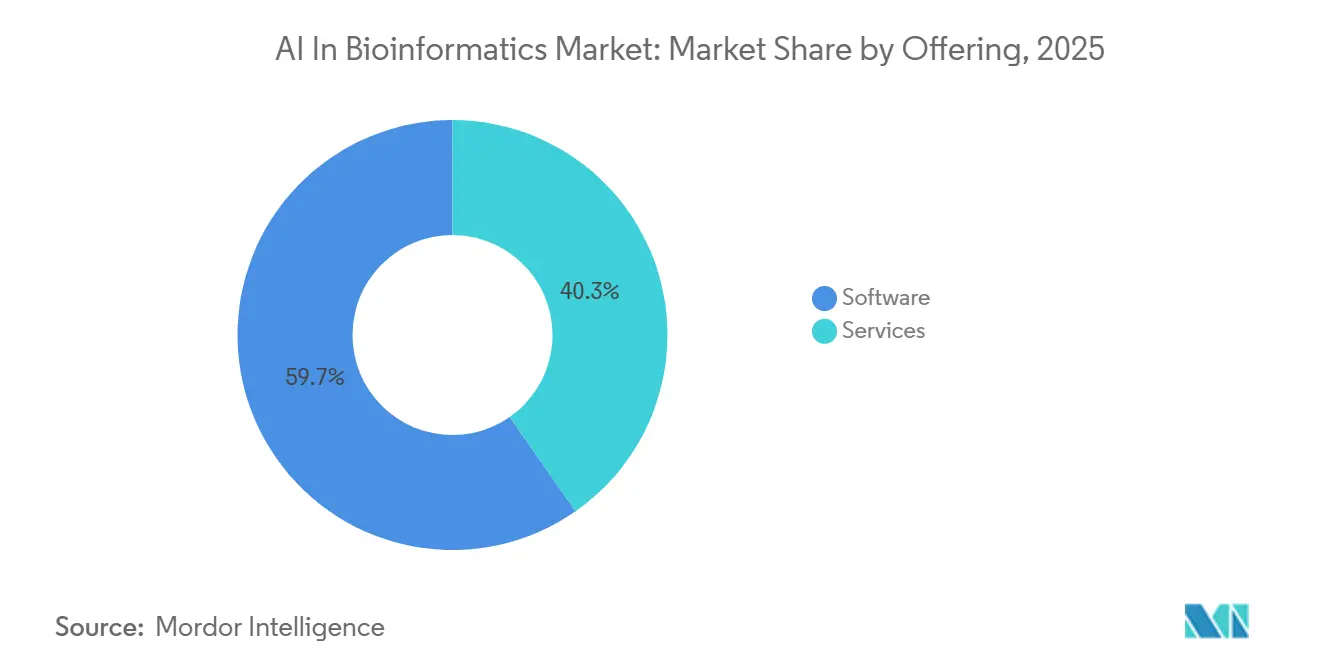

- By offering, software led with 59.73% share, while services are forecasted to expand at 16.58% CAGR through 2031.

- By technology, machine learning held 44.38% share in 2025, while natural language processing is projected to grow at 16.82% CAGR through 2031.

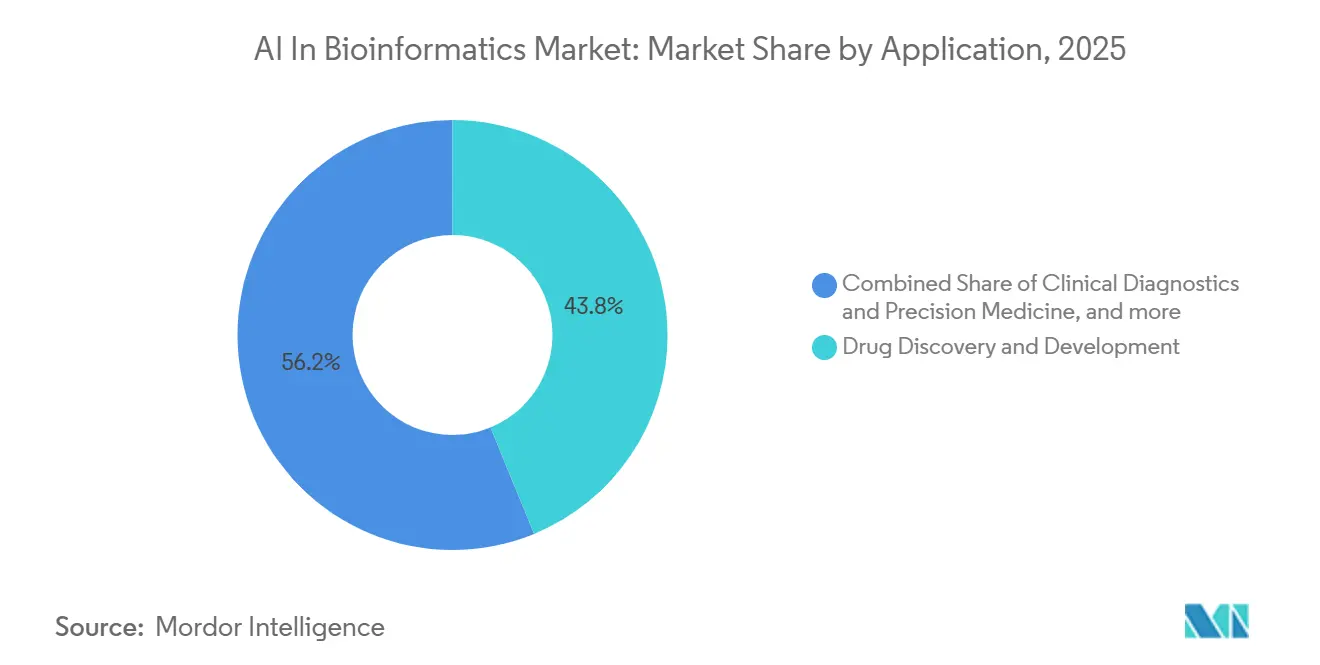

- By application, drug discovery and development accounted for 43.82% share in 2025, while biomarker discovery and validation are forecasted to expand at 17.34% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies held 51.25% share in 2025, while academic and research institutes are projected to grow at 17.22% CAGR through 2031.

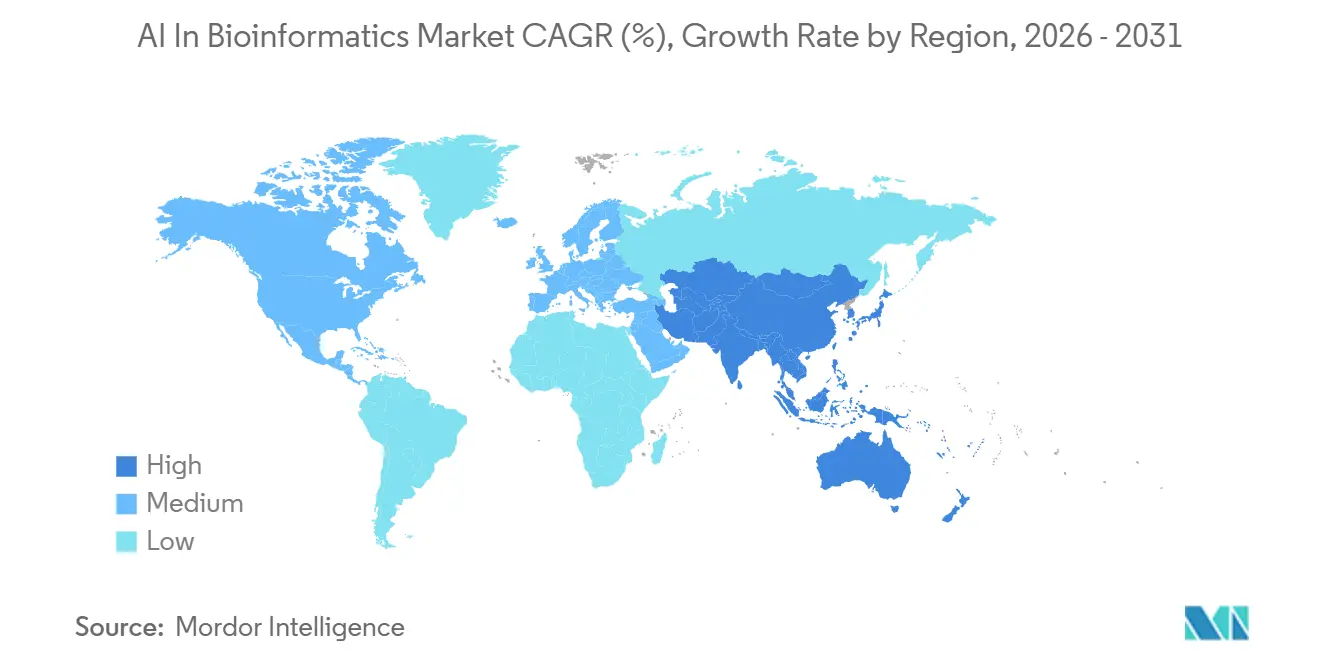

- By geography, North America held 48.55% of the AI in bioinformatics market share in 2025, while Asia-Pacific is projected to grow at 18.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Bioinformatics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Led Interpretation of Multi-Omics Data at Scale | +3.2% | Global, with concentrated gains in North America and Europe | Medium term (2-4 years) |

| Clinical Trial Stratification and Cohort Matching | +2.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Foundation Models for Biological Sequence and Structure Prediction | +3.5% | Global, led by North America and East Asia | Short term (≤ 2 years) and Medium term (2-4 years) |

| Federated Learning Across Hospital and Biobank Data Silos | +2.2% | Europe, North America, with early adoption in Japan and South Korea | Medium term (2-4 years) and Long term (≥ 4 years) |

| Closed-Loop Wet Lab and In Silico Workflow Automation | +1.8% | North America and Europe | Medium term (2-4 years) |

| Cross-Ancestry Model Expansion for Population-Scale Genomics | +1.5% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Led Interpretation of Multi-Omics Data at Scale

The AI in bioinformatics market is being pushed forward by the merging of genomics, transcriptomics, proteomics, and metabolomics into unified AI workflows. Multi-omics analysis was previously limited because models struggled to reconcile different statistical properties and batch effects across data types. A 2026 study in Cell Metabolism showed unified multi-omics modeling across 425,258 individuals, with strong performance in predicting aging trajectories, metabolic health, and intervention response at a scale that single-modality approaches could not reach.[1]“A Generative AI Framework Unifies Human Multi-Omics to Model Aging, Metabolic Health, and Intervention Response,” Cell Metabolism, cell.comThis is moving pharmaceutical companies toward AI-integrated multi-omics as a more routine step in target validation and reducing dependence on slower in vitro screening paths. The 2025 Flexynesis toolkit also showed how bulk multi-omics data can support precision oncology stratification, which points to earlier clinical use in cancer indication selection.[2]Anne-Christin Hauschild et al., “Flexynesis, A Deep Learning Toolkit for Bulk Multi-Omics Data Integration for Precision Oncology and Beyond,” Nature Communications, nature.comThe remaining challenge has shifted from data generation to semantic harmonization, because vendors now need to align inconsistent clinical phenotyping and metadata standards across large cohort datasets.

Clinical Trial Stratification and Cohort Matching

The AI in bioinformatics market is also gaining support from the need to improve patient subgroup selection in drug development. Conventional epidemiological tools often fail to isolate pharmacogenomically defined responder populations inside heterogeneous trial pools, and that weakness has contributed to Phase II failures. The FDA’s April 2026 pilot program on AI in clinical trials directly addressed dose selection, safety monitoring, and early go or no-go decisions, which gives clearer regulatory support for AI bioinformatics tools used in trial design and execution.[3]U.S. Food and Drug Administration, “Artificial Intelligence in Clinical Trials, Pilot Program,” Federal Register, govinfo.govCommercial platforms are responding by combining genomic, transcriptomic, imaging, and clinical data into cohort definitions that can be used much faster than traditional workflows. This raises demand for explainable software, because AI-defined cohorts that enter regulatory submissions will need fixed model parameters, auditable logic, and clear lineage records.

Foundation Models for Biological Sequence and Structure Prediction

The AI in bioinformatics market is moving quickly as foundation models extend from single-protein prediction into broader biological sequence and genome modeling. NVIDIA expanded its BioNeMo platform in January 2026 to RNA structure prediction and retrosynthesis optimization, which shows how biological model development is being turned into usable commercial infrastructure. Basecamp Research’s EDEN models, trained on up to 9.7 trillion nucleotide tokens across 28 billion parameters, showed how large model scale is now being applied to difficult problems such as large DNA segment insertion. Open-weight releases from academic groups are narrowing the gap with proprietary systems, so commercial vendors are being pushed to compete more on exclusive data access and clinical-grade deployment rather than model ownership alone. This shift is shortening the monetization window for proprietary model developers across the AI in bioinformatics market.

Federated Learning Across Hospital and Biobank Data Silos

The AI in bioinformatics market is also benefitting from federated learning because it creates population-scale statistical power without requiring sensitive genomic data to be moved into one central repository. In 2025, SF-GWAS demonstrated secure genome-wide association analysis on a UK Biobank cohort of 410,000 individuals with a strong runtime improvement over earlier federated methods. Spain’s IIS La Fe also launched OmicSpace as a federated platform connecting biobanks and clinical genomic registries across 5 autonomous communities without centralizing data, which gives a direct national proof point for this deployment model. The practical limit is that rare disease use cases still suffer when local sample sizes stay too small at each node, which reduces model performance even when federation is technically sound.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Sovereignty Friction in Cross-Border Genomic Collaboration | -1.5% | Europe, APAC (China specifically), MEA | Medium term (2-4 years) and Long term (≥ 4 years) |

| Model Validation Burden Across Clinical, Research, and GxP Use Cases | -1.0% | Global, most acute in North America and Europe | Short term (≤ 2 years) and Medium term (2-4 years) |

| GPU And High-Performance Compute Constraints for Large Omics Pipelines | -1.2% | Global, most limiting in cost-constrained settings in MEA and South America | Short term (≤ 2 years) |

| Limited Labeled Biological Datasets For Rare Variant and Rare Disease Use Cases | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Sovereignty Friction in Cross-Border Genomic Collaboration

The AI in bioinformatics market faces a major constraint from cross-border genomic data rules that were built on different assumptions about privacy, re-identification risk, and secondary data use. The EU’s GDPR, China’s Personal Information Protection Law and Human Genetic Resources Administration rules, and the U.S. NIH genomic data sharing framework do not align well in practice, which stretches governance timelines for multinational model training and validation programs. China’s genetic resources rules are especially restrictive for foreign-involved research because they impose export controls and domestic localization requirements on relevant data flows. As a result, the AI in bioinformatics market is moving toward country-specific data partnership structures rather than simple global licensing arrangements. This raises development costs and extends time to market for vendors that want globally relevant training datasets.

Model Validation Burden Across Clinical, Research, and GxP Use Cases

The AI in bioinformatics market also faces slower deployment because the FDA’s January 2025 draft guidance introduced a 7-step risk-based credibility assessment framework for AI used in drug and biological product development. Sponsors are now expected to define context of use, assess the model’s influence on decision-making, and provide validation evidence that matches the risk of the use case. That documentation burden is much harder for AI-native startups than for established vendors that already operate under quality management systems. The problem is magnified because a model validated for one regulated context cannot be moved into an adjacent use case without a new validation cycle. GxP requirements such as computer system validation, 21 CFR Part 11 compliance, and audit trail integrity also fit poorly with continuous learning architectures, which creates extra engineering work before deployment. This is likely to push more share toward vendors that can offer pre-built regulated deployment environments across the AI in bioinformatics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Acceleration Signals a Shifting Value Chain

Software held 59.73% of the AI in bioinformatics market share in 2025, supported by SaaS genomic interpretation platforms, cloud-native variant annotation tools, and AI-powered sequencing analysis pipelines that scale efficiently after deployment. Its position is also reinforced by switching costs created by large genomic databases and by proprietary model weights embedded within software platforms. These factors make software the most entrenched offering in the AI in bioinformatics market at present. The value proposition has been strongest where customers need repeatable analysis, faster throughput, and centralized model updates across multiple research programs.

Services are expected to be the fastest-growing sub-segment at 16.58% CAGR from 2026 to 2031, which shows that complex model deployment is pushing buyers toward external support. The AI in bioinformatics industry is moving toward bundled platform and service contracts because model customization, pipeline integration, and managed analysis are harder to standardize than software alone. Revenue is moving away from software-only models and toward recurring service-based engagement structures in the AI in bioinformatics market.

By Technology: NLP's Ascent Reflects Biomedical Literature as an Actionable Data Layer

Machine learning held 44.38% share in 2025 and remained the most established technology base across sequencing pipelines, variant classification, biomarker association studies, and phenotype prediction. Supervised models such as gradient-boosted trees and random forests still matter because clinical genomics workflows often favor interpretability and calibration. Deep learning has delivered stronger relative performance in protein structure prediction, whole-slide image analysis, and single-cell tasks, which keeps it important even when not leading overall share. This mix shows that the AI in bioinformatics market still uses multiple technical approaches rather than converging on one dominant model class.

Natural language processing is expected to be the fastest-growing technology segment at 16.82% CAGR through 2031 because biomedical literature, clinical notes, and knowledge graphs are becoming active data layers in research workflows. Computer vision remains a smaller segment, but it is growing alongside AI-powered digital pathology and whole-slide imaging in clinical workflows. The AI in bioinformatics industry is therefore broadening from sequence analysis alone into text, image, and graph reasoning tasks that support more of the research and diagnostic process.

By Application: Biomarker Discovery Emerges as the Fastest Commercial Growth Vector

Drug discovery and development accounted for 43.82% of the AI in bioinformatics market size in 2025, which reflects long-standing pharmaceutical spending on target identification, lead optimization, translational informatics, and ADMET prediction. This segment remains the largest because it sits close to commercial value creation and already has established budgets inside large pharmaceutical organizations. The application also benefits from the move by pharma companies toward direct platform ownership rather than limited software procurement. That keeps drug discovery at the center of demand in the AI in bioinformatics market.

Biomarker discovery and validation is projected to be the fastest-growing application segment at 17.34% CAGR from 2026 to 2031 as precision oncology pipelines place more weight on companion diagnostics and liquid biopsy. Demand is rising because AI-driven multi-omics models can shorten discovery timelines and help validate biomarkers across more heterogeneous patient groups. Clinical diagnostics and precision medicine, laboratory informatics and workflow automation, and biological network modeling all remain material application areas in the AI in bioinformatics market.

By End-User: Academic Institutions Accelerate on Open Foundation Model Infrastructure

Pharmaceutical and biotechnology companies accounted for 51.25% share in 2025 because they can absorb high upfront integration costs and secure large-scale data licensing arrangements. They also have the strongest business incentive to shorten development timelines and improve R&D productivity. This makes them the most commercially important buyer group in the AI in bioinformatics market today. Strategic platform relationships are becoming more important than one-off software purchases as vendors move closer to embedded R&D support.

Academic and research institutes are anticipated to be the fastest-growing end-user segment at 17.22% CAGR through 2031, helped by open-weight and open-source biological foundation models that reduce the cost of advanced AI capability. Within the AI in bioinformatics industry, this lowers the barrier for non-commercial researchers that do not have large software licensing budgets. Hospitals and diagnostic laboratories are also becoming a larger customer group as AI-powered genomic interpretation and digital pathology move into regulated clinical environments.

Geography Analysis

North America accounted for 48.55% of the AI in bioinformatics market size in 2025, giving it the largest regional position. The region benefits from dense pharmaceutical R&D activity, deep venture funding, and strong NIH-backed genomics infrastructure. The United States remains the anchor of the regional AI in bioinformatics market, while Canada adds support through Genome Canada and related precision medicine activity. Access to high-end GPU infrastructure at major cloud providers also strengthens North America’s cost and speed advantage for large omics workloads, and the EuroHPC MeluXina project showed that GPU-accelerated whole-genome analysis can reduce runtime from 14.6 hours to 4.7 hours with Parabricks on 3 GPU nodes.

Europe is the second-largest regional block in the AI in bioinformatics market, led by Germany, the UK, and France. In the UK, NHS England’s blood-test-first cancer program and SOPHiA GENETICS’ May 2026 partnership with Synnovis show how public health systems can create direct demand for AI-enabled genomic diagnostics at scale. Germany has taken a leading role in federated genomics through the German Biobank Alliance and the Genomic Data Infrastructure project, which completed a 2026 demonstration of privacy-preserving federated GWAS across multiple national nodes.

Asia-Pacific is projected to be the fastest-growing region at 18.43% CAGR from 2026 to 2031, making it the fastest-rising part of the AI in bioinformatics market. Growth is being driven by government-backed genomics programs in China, Japan, India, and South Korea and by continued investment in national health data infrastructure. A 2025 Nature study on Han Chinese ancestry showed how population-specific polygenic risk scoring can support non-European model development at large scale, which is important for region-specific precision medicine tools. China’s large cohort programs and cross-ancestry research are expanding the training base for local models, while South America and the Middle East and Africa are showing earlier-stage demand through hospital partnerships and precision medicine infrastructure investment, including PathAI’s 2026 Brazil collaboration.

Competitive Landscape

The AI in bioinformatics market has a moderately concentrated structure, with Illumina, Thermo Fisher Scientific, QIAGEN, and Oxford Nanopore forming a strong infrastructure layer around instruments, diagnostics, sequencing workflows, and curated data assets. At the same time, AI-native companies such as Insilico Medicine, Owkin, Tempus AI, and SOPHiA GENETICS compete on exclusive data access, model architecture, and the depth of pharmaceutical partnerships. This creates a two-tier competitive pattern in the AI in bioinformatics market where incumbents control important workflows and challengers try to capture value in software, analytics, and model outputs. A clear strategic pattern is that platform vendors are trying to convert data relationships into downstream revenue in drug discovery and companion diagnostics. That is changing commercial models from fixed platform fees toward longer-term relationships tied to research productivity and clinical deployment.

Partnership activity shows how fast the AI in bioinformatics market is being reorganized around hardware, software, and data integration. QIAGEN’s May 2026 collaboration with NVIDIA joined graph-based retrieval AI with QIAGEN’s curated biomedical knowledge assets, while Illumina’s January 2025 collaboration with NVIDIA showed the same push toward multi-omics analytics at scale. These moves raise the competitive bar because success now depends on combined access to compute, high-quality data, and validated deployment channels.

M&A is tightening boundaries across the AI in bioinformatics market as larger diagnostics and healthcare companies absorb specialized AI capabilities. The same environment is increasing the value of governance, because vendors with stronger auditability and model control are better placed under European procurement and compliance scrutiny. Patent activity is also rising in biological foundation models, ancestry-aware genomics methods, and federated systems, including MIT’s PRISM work on ancestry-aware polygenic score integration. Commercial gaps still remain in federated learning for rare disease sample sizes, population-specific models for non-European ancestries, and GxP-compliant clinical decision support tools, which means the competitive picture is active even as consolidation accelerates.

AI In Bioinformatics Industry Leaders

Illumina, Inc.

Thermo Fisher Scientific Inc.

QIAGEN N.V.

SOPHiA GENETICS SA

Tempus AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Owkin announced a multi-year collaboration with Sanofi to co-develop next-generation biopharma AI agents, including a five-year license for K Pro, Owkin's AI Scientist platform. The deal builds on a prior EUR 90 million (USD 96 million) strategic partnership covering oncology target identification and immunology drug positioning, marking a significant expansion of AI agent deployment in pharma R&D workflows.

- June 2026: SOPHiA GENETICS signed a Memorandum of Understanding with Memorial Sloan Kettering Cancer Center to establish a joint venture combining SOPHiA DDM AI and analytics with MSK's clinical oncology leadership, targeting next-generation precision oncology diagnostics at a global scale.

- May 2026: Roche entered a definitive merger agreement to acquire PathAI for USD 750 million upfront plus up to USD 300 million in milestone payments. The transaction integrates PathAI's AI-powered digital pathology platform into Roche Diagnostics, expanding AI-enabled companion diagnostic algorithm development.

- May 2026: QIAGEN announced a collaboration with NVIDIA at the BIO-IT World Conference to integrate NVIDIA BioNeMo and GPU-accelerated GraphRAG into QIAGEN Digital Insights' biomedical knowledge graph platform, enabling natural-language querying across genes, diseases, pathways, and compounds for AI-driven drug discovery.

Global AI In Bioinformatics Market Report Scope

According to the report’s scope, the AI in bioinformatics market refers to the industry focused on the development and adoption of artificial intelligence technologies, including machine learning, deep learning, and generative AI, to analyze, interpret, and manage complex biological data. These solutions support applications such as genomics, proteomics, drug discovery, biomarker identification, disease prediction, and precision medicine by improving the speed, accuracy, and scalability of bioinformatics workflows.

The AI in bioinformatics market is segmented into offering, technology, application, end-user, and geography. By offering, the market is segmented into software and services. By technology, the market is segmented into machine learning, deep learning, natural language processing, computer vision, and other technologies. By application, the market is segmented into drug discovery and development, clinical diagnostics and precision medicine, biomarker discovery and validation, multi-omics data integration and interpretation, biological network and systems biology modeling, laboratory informatics and workflow automation, and other applications. By end-user, the market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, hospitals and diagnostic laboratories, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Other Technologies |

| Drug Discovery and Development |

| Clinical Diagnostics and Precision Medicine |

| Biomarker Discovery and Validation |

| Multi-Omics Data Integration and Interpretation |

| Biological Network and Systems Biology Modeling |

| Laboratory Informatics and Workflow Automation |

| Other Applications |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Hospitals and Diagnostic Laboratories |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Services | ||

| By Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Other Technologies | ||

| By Application | Drug Discovery and Development | |

| Clinical Diagnostics and Precision Medicine | ||

| Biomarker Discovery and Validation | ||

| Multi-Omics Data Integration and Interpretation | ||

| Biological Network and Systems Biology Modeling | ||

| Laboratory Informatics and Workflow Automation | ||

| Other Applications | ||

| By End-User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Hospitals and Diagnostic Laboratories | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for AI in bioinformatics?

The AI in bioinformatics market is forecasted to reach USD 25.2 billion by 2031 from USD 10.32 billion in 2025 to USD 11.9 billion in 2026, growing at a 16.2% CAGR.

Which application area leads revenue today?

Drug discovery and development lead with 43.82% share in 2025 because pharmaceutical spending remains concentrated in target identification, lead optimization, and translational informatics.

Which segment is growing the fastest?

Biomarker discovery and validation are expected to be the fastest-growing applications at 17.34% CAGR, while Asia-Pacific is the projected to be the fastest-growing region at 18.43% CAGR through 2031.

Why are pharmaceutical and biotechnology companies the largest buyers?

Pharmaceutical and biotechnology companies held 51.25% share in 2025 because they can fund platform integration, manage large data licensing arrangements, and tie AI deployment directly to R&D productivity.

Page last updated on: