AI In Biomarker Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

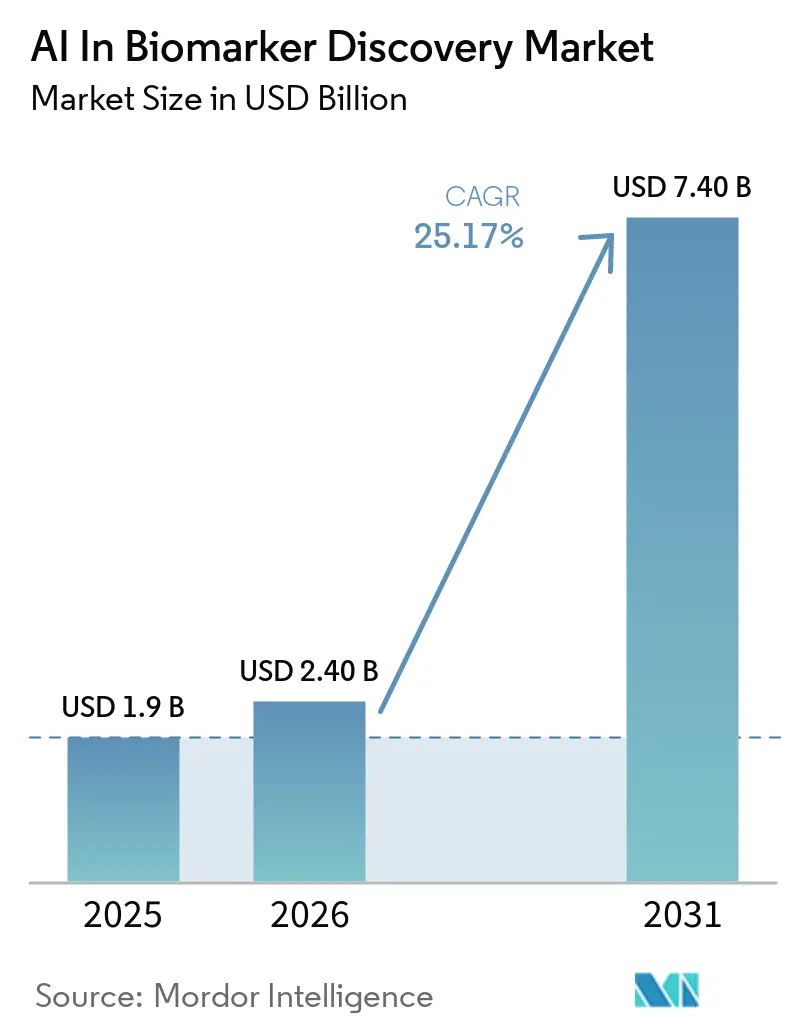

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 7.40 Billion |

| Growth Rate (2026 - 2031) | 25.17% CAGR |

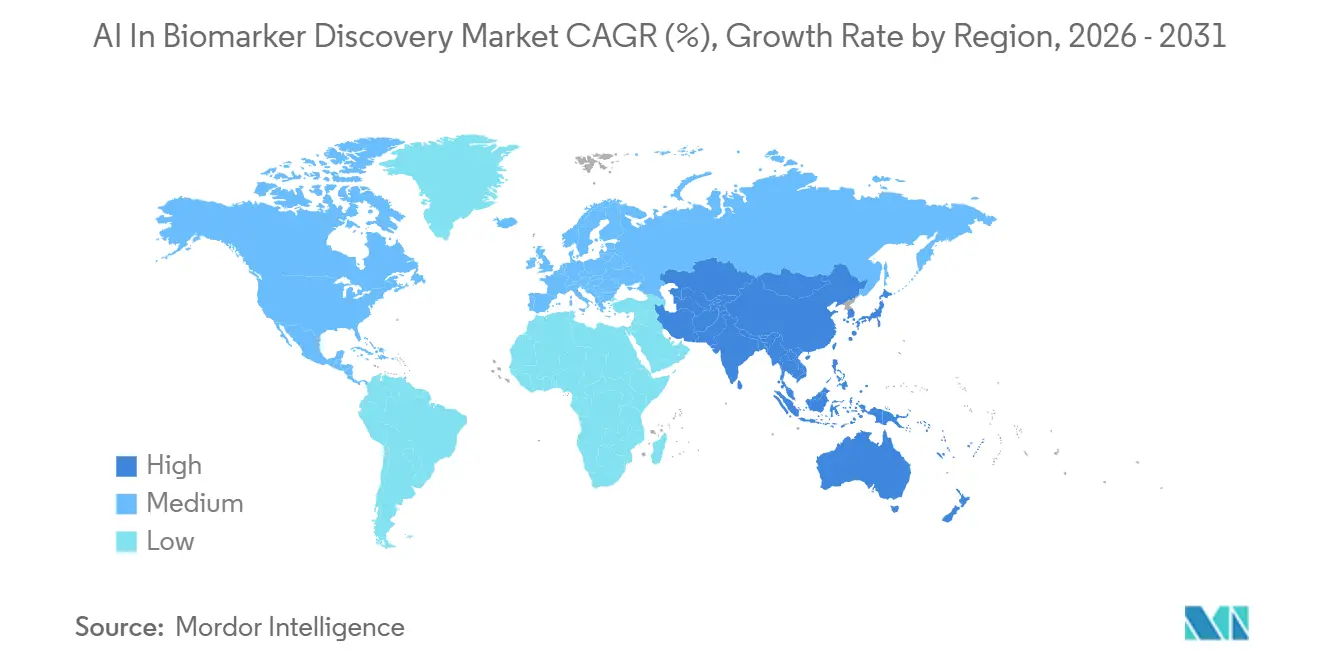

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

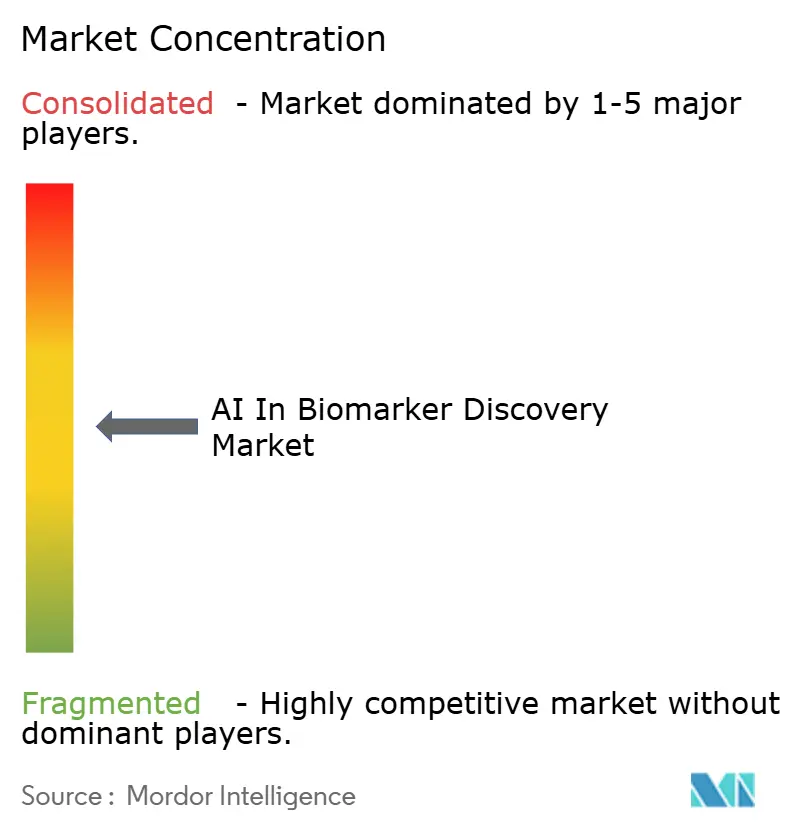

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Biomarker Discovery Market Analysis by Mordor Intelligence

The AI In Biomarker Discovery Market size is expected to grow from USD 1.9 billion in 2025 to USD 2.40 billion in 2026 and is forecast to reach USD 7.40 billion by 2031 at 25.17% CAGR over 2026-2031.

Demand accelerates as regulators publish clearer AI/ML pathways, biopharma sponsors embed computational endpoints into early-phase protocols, and foundation models trained on multi-modal data match specialist accuracy. Oncology dominates spending, but rare and genetic disorders are scaling the fastest because synthetic data generation and federated registries turned production-ready in late 2024. Clearer reimbursement rules for AI-enabled companion diagnostics, pay-per-sample cloud economics, and nation-level precision-medicine initiatives are broadening end-user adoption of AI in the biomarker discovery market.

Key Report Takeaways

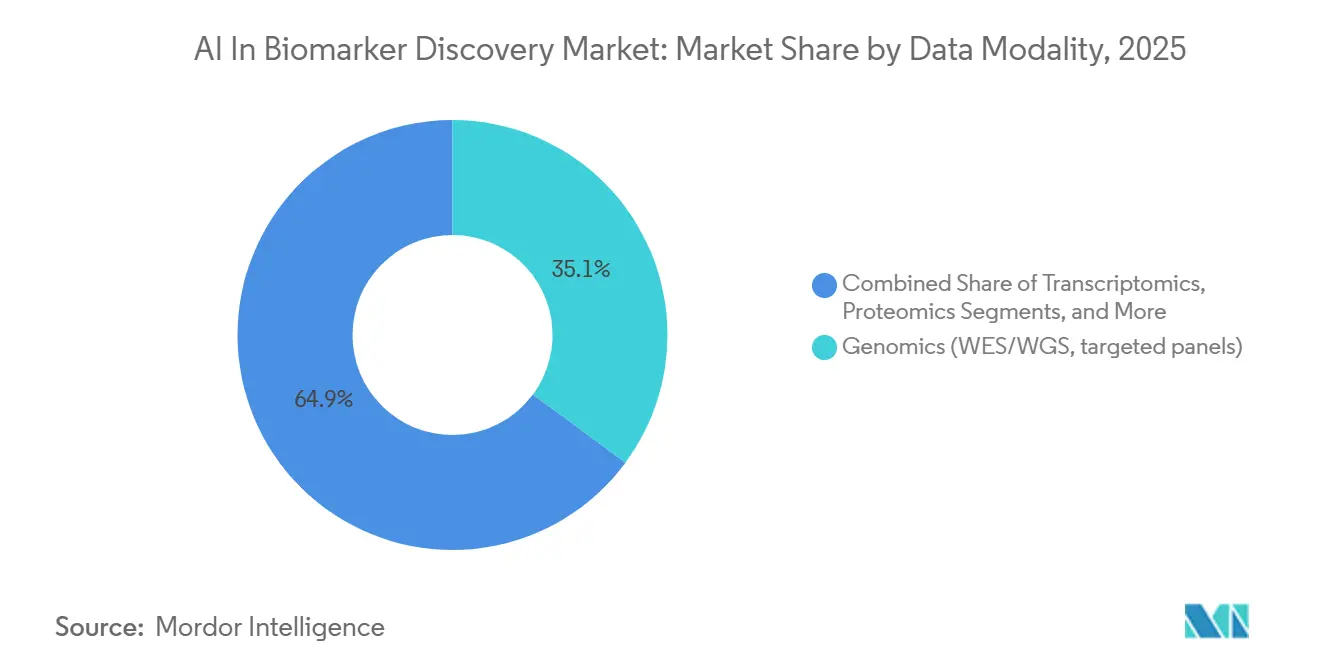

- By data modality, genomics accounted for 35.12% of the AI in the biomarker discovery market size in 2025, and transcriptomics is projected to grow at a 28.16 % CAGR through 2031.

- By disease area, oncology led with 43.18% of the AI in biomarker discovery market share in 2025.

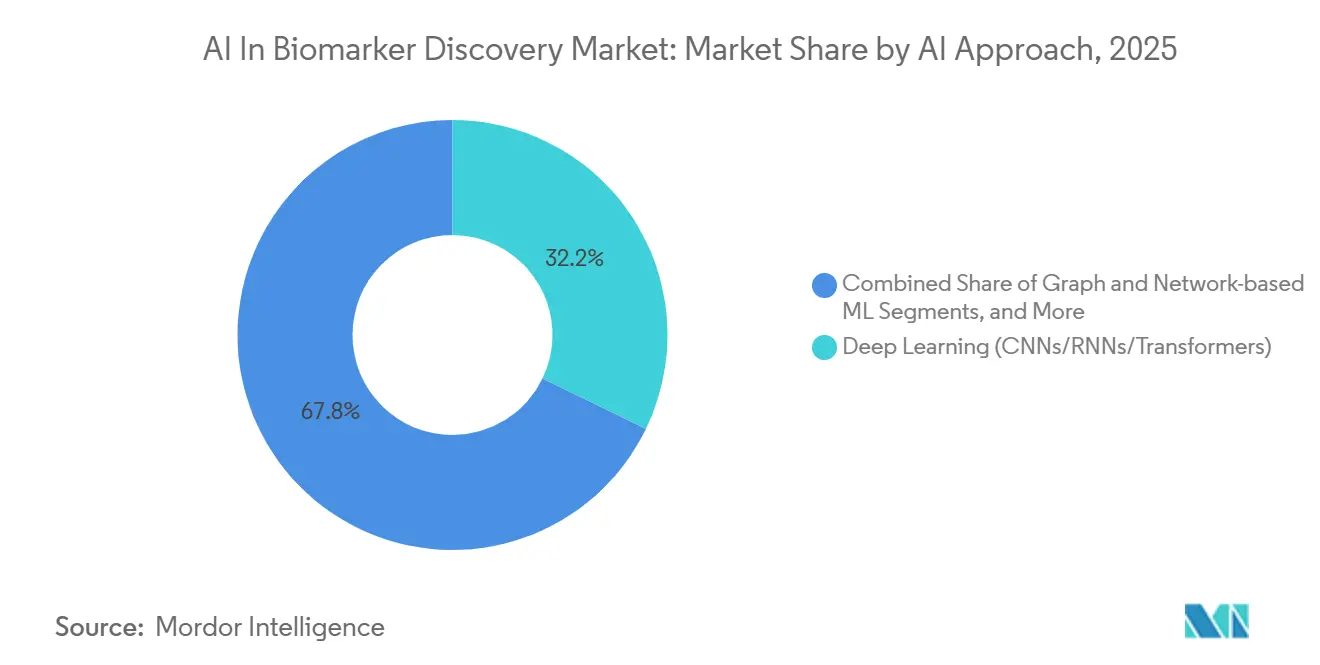

- By AI approach, deep learning (CNNs/RNNs/Transformers) held 32.18% of 2025 revenue, while foundation models (pathology, radiology, omics) are projected to grow at a 28.43% CAGR to 2031.

- By biomarker type, prognostic tests held 37.16% of 2025 revenue, while predictive assays are projected to grow at a 28.11% CAGR to 2031.

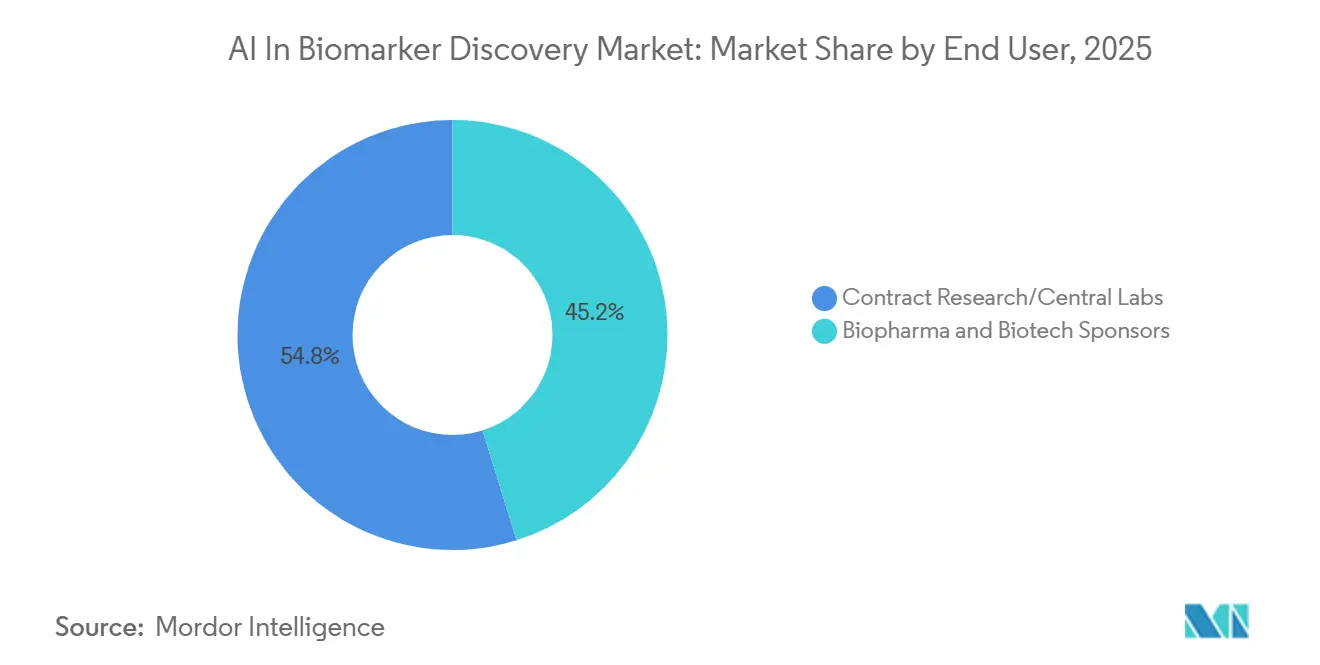

- By end user, biopharma and biotech sponsors held 45.17% of 2025 revenue, while diagnostics and CDx developers are projected to grow at a 29.37% CAGR to 2031.

- By deployment/access model, cloud/SaaSheld 53.19% held of 2025 revenue, while federated/edge deployments is projected to grow at a 31.65% CAGR to 2031.

- By geography, North America held 43.16% of 2025 revenue, while Asia-Pacific is projected to grow at a 30.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Biomarker Discovery Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Oncology-led precision-medicine demand | +4.5% | North America, Western Europe | Medium term (2-4 years) |

| Expansion of multi-omics datasets and digital pathology | +3.8% | Global, fastest in Asia-Pacific | Long term (≥4 years) |

| Regulatory tailwinds (FDA BQP, AI/ML SaMD guidance) | +3.2% | North America, EU | Short term (≤2 years) |

| Cloud/SaaS-native analytics and scalable compute | +2.9% | Global | Medium term (2-4 years) |

| Federated learning unlocking cross-institution discovery | +2.6% | EU, APAC | Long term (≥4 years) |

| Multimodal foundation models linking omics–imaging–clinical | +4.1% | North America, EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oncology-Led Precision Medicine Demand

Clinical practices are increasingly adopting AI-driven molecular subtyping over traditional histopathology. In 2025, the FDA approved 17 oncology AI biomarker tests, up from 9 in 2024. Of these, 12 focused on immunotherapy responses, while 5 targeted minimal residual disease.[1]U.S. Food and Drug Administration, “Artificial Intelligence and Machine Learning (AI/ML)-Enabled Medical Devices,” FDA.gov Whole-slide imaging combined with spatial transcriptomics now achieves an 82% positive predictive value for predicting checkpoint-inhibitor efficacy, a 14-point improvement over traditional PD-L1 staining. Liquid-biopsy panels, with a sensitivity of 1 ppm in detecting circulating tumor DNA, are growing at an annual rate of 31%, driven by their ability to replace invasive biopsies. Additionally, multi-omic panels have significantly reduced discovery timelines from 36 months to under a year, enhancing the protection of drug-patent life.

Expansion of Multi-Omics Datasets and Digital Pathology

High-resolution scanners now archive gigapixel images at a cost-effective rate, enabling hospitals to utilize their archived slide libraries. Single-cell RNA sequencing has advanced to process 1 million cells per run, while spatial platforms map 5,000 genes per cell, uncovering localized niches that bulk profiling often misses. Large-scale initiatives, such as those in the UK and China, are projected to add 1.5 million genomes this decade, strengthening the ability to detect rare-variant associations. Plasma-proteome assays, capable of quantifying 7,000 proteins from minimal sample volumes, are narrowing the functional gap between transcriptomics and proteomics.

Regulatory Tailwinds (FDA BQP; Evolving AI/ML SaMD Guidance)

In 2025, the FDA's Biomarker Qualification Program approved four AI-derived biomarkers, validating machine-learned radiomic features as credible endpoints. New regulatory guidance introduced in January 2025 allows sponsors to pre-specify triggers for model updates, reducing regulatory delays from nine months to 30 days.[2]U.S. Food and Drug Administration, “Biomarker Qualification Program,” FDA.gov In Europe, upcoming exemptions for decision-support software are expected to accelerate IVDR timelines. Japan has also aligned its PCCP framework with the U.S. as of March 2025. The ISTAND pilot program is enabling the use of synthetic patients in rare-disease studies, provided specific covariate balance thresholds are met.

Cloud/SaaS-Native Analytics and Scalable Compute

Elastic compute solutions are eliminating the capital expenses associated with on-premises GPU clusters. Cloud-based platforms now align whole genomes at significantly reduced costs and faster speeds compared to traditional core-lab pricing. Advanced AI models allow businesses to fine-tune solutions without compromising data privacy. Confidential-computing technologies ensure compliance with data protection regulations by encrypting data during use. Edge deployments are enhancing operational efficiency, delivering inferences in under 200 milliseconds for surgical guidance by locally caching models and synchronizing updates nightly.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data silos, privacy, and cross-border transfer limits | −1.8% | EU, APAC | Medium term (2-4 years) |

| Analytical/clinical validation burden under IVDR and LDT reforms | −2.1% | EU, North America | Short term (≤2 years) |

| Batch effects and assay drift causing model non-stationarity | −1.6% | Global | Long term (≥4 years) |

| Explainability and lifecycle change control for AI biomarkers | −1.4% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Silos, Privacy, and Cross-Border Data Transfer Limits

Multi-national data pooling remains uncertain due to regulations such as GDPR, PIPL, and the fragile EU–US Data Privacy Framework. Hospitals increasingly treat omics archives as competitive assets, while re-identification studies indicate that 83% of “anonymized” genomes can be traced, leading to stricter terms for data usage. In the biomarker discovery market, where deployments depend on extensive training datasets, differential-privacy noise can reduce AUROC by up to seven points at stringent epsilon levels. This creates a trade-off between compliance and utility, slowing AI advancements in the sector.

Analytical/Clinical Validation Burden Under IVDR and LDT Reforms

AI biomarker tests, re-classified into higher-risk categories, now require performance studies involving 200 to 500 subjects. Combined with notified-body fees ranging from USD 0.5 to 2 million, these costs pose significant challenges for many start-ups. In the United States, court challenges to proposed LDT oversight delayed new test launches for 18 months, resulting in a backlog that is currently being addressed by the FDA. Furthermore, analytical-validity matrices, which include up to 100 assay combinations, add an additional 12 months to development timelines to ensure cross-platform consistency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Modality: Genomics Anchors, Transcriptomics Accelerates

In 2025, Genomics accounted for 35.12% of the revenue, solidifying its foundational role in precision oncology. Meanwhile, Transcriptomics, driven by single-cell and spatial methods, is advancing with a 28.16% CAGR. As per-cell costs decrease below USD 0.10, Transcriptomics is expected to close the gap with Genomics. The integration of these two modalities is uncovering causal signals previously overlooked, driving the growth of AI in the biomarker discovery market, particularly for multi-omic platforms.

Paige’s Virchow2 demonstrated that unlabeled slide archives can be utilized to develop models for rare cancers. This indicates that pathology images could play a significant role in providing weak labels for future multimodal pipelines. However, fewer than 5% of cancer patients currently have fully matched genomic, transcriptomic, proteomic, and metabolomic profiles, which limits comprehensive foundation-model training.

By Disease Area: Oncology Dominates, Rare Diseases Surge

Oncology accounted for 43.18% of the 2025 expenditure, reflecting the emphasis on biomarker-guided therapy approvals and the complexity of tumor heterogeneity. Rare disorders are experiencing strong growth at a 29.61% CAGR, driven by sponsors increasingly adopting synthetic cohorts and federated registries to address the challenges of small patient populations. These strategies matured in late 2024 and are now scaling across the AI in biomarker discovery market.

Immunology applications are benefiting from single-cell RNA-seq techniques that effectively profile T-cell clonotypes. In contrast, cardiometabolic projects remain underdeveloped due to reimbursement processes lagging behind oncology by approximately two years. However, with AI-driven polygenic-risk engines achieving a 0.75 AUROC for 10-year cardiovascular predictions, this segment is positioned for significant growth once payer codes are introduced.

By AI Approach: Deep Learning Leads, Foundation Models Gain

Deep learning held a 32.18% market share in 2025, with convolutional and transformer networks automating feature extraction across image, sequence, and time-series data. Foundation models are growing at a 28.43% CAGR, achieving benchmark accuracy with significantly fewer labels, which is critical in scenarios where expert annotation costs are high, reaching up to USD 100 per sample.

Classical machine-learning models remain relevant in regulatory submissions due to their transparent decision boundaries, which align with explainability requirements. Self-supervised pre-training combined with contrastive learning is reducing annotation burdens and enabling broader participation from mid-sized clinics in the AI-driven biomarker discovery market.

By Biomarker Type: Prognostic Leads, Predictive Grows Fastest

Prognostic markers accounted for 37.16% of the 2025 revenue, as payers use risk stratification to reduce overtreatment. Predictive biomarkers, directly linked to drug responses, are growing at a 28.11% CAGR and are expected to gradually narrow the gap with prognostic markers as more therapies align with validated companion diagnostics. Safety biomarkers, while niche, remain critical as AI models predict toxicity and enable timely interventions that reduce hospitalization rates.

By End User: Biopharma Leads, Diagnostics Developers Accelerate

Biopharma and biotech sponsors represented 45.17% of total spending, driven by the ability of AI biomarkers to reduce trial sizes by up to 50%, saving approximately USD 80 million on a typical Phase III protocol. Diagnostics developers are the fastest-growing segment, with a 29.37% CAGR, following regulatory guidance in January 2025 that allows algorithm updates under predetermined plans without requiring new 510(k) filings. This regulatory clarity marks a significant milestone for the AI in biomarker discovery market. Contract research organizations are leveraging AI in pathology to standardize scoring across sites, improving inter-reader concordance from 78% to 94%.

By Deployment Model: Cloud Dominates, Federated Architectures Rise

Cloud and SaaS deployments accounted for 53.19% of the 2025 revenue, driven by per-sample pricing and elastic GPUs that enhance accessibility. Federated and edge approaches are growing at a 31.65% CAGR, supported by regulations in EU and APAC regions that restrict raw-data exports. Encrypted-gradient aggregation ensures data sovereignty while enabling efficient model training. Hybrid setups preprocess data locally before transitioning to the cloud for intensive training, but round-trip latency of 50 to 200 milliseconds limits their use in real-time intraoperative applications.

Geography Analysis

In 2025, North America accounted for 43.16% of the revenue, driven by the expansion of the NIH's "All of Us" cohort and Medicare's coverage of multi-cancer early-detection tests. A strong flow of venture capital and the FDA's expedited PCCP pathway enable startups to maintain a competitive edge, reinforcing the region's leadership in the AI-driven biomarker discovery market.

Asia-Pacific, supported by significant investments such as China's USD 9.2 billion Precision Medicine Initiative and the rise of AI-focused diagnostic ventures in India, is projected to grow at a robust 30.08% CAGR through 2031. The implementation of data-sovereignty laws is accelerating the adoption of privacy-preserving machine learning and federated computing, driving innovation in product development. Additionally, Japan's alignment with FDA guidelines for 2025 simplifies dual-filing strategies for global developers.

Europe is experiencing steady growth, although the IVDR's stringent evidence requirements pose challenges. Meanwhile, genomics projects in the Gulf Cooperation Council and AI-based tuberculosis screening initiatives in Brazil highlight how emerging markets are rapidly adopting AI in biomarker applications. While these regions currently contribute less than 15% of the total revenue, they represent high-growth opportunities as infrastructure development progresses.

Competitive Landscape

The top five vendors, including Tempus, Guardant Health, Foundation Medicine, SOPHiA GENETICS, and PathAI, collectively hold a 38% market share. Their competitive advantage is driven by exclusive data partnerships that provide access to cohorts exceeding 10,000 patients, platforms that demonstrate cross-assay analytical validity, and intellectual property that meets FDA special-controls requirements.

Tempus has vertically integrated its operations by acquiring Ambry Genetics to establish in-house sequencing capabilities. The MELLODDY consortium has demonstrated the effectiveness of federated chemistry data, achieving a 15% increase in identified hit compounds compared to individual members. Providers of foundation models are employing a dual strategy by licensing encoders for USD 0.5–2 million per indication while also launching branded tests to achieve higher per-sample margins.

Regulatory arbitrage is evident as companies secure faster approvals in regions such as Israel or Singapore and then leverage mutual-recognition agreements to enter North American and European markets. Opportunities remain in cardiometabolic and neurodegenerative segments, where delays in payer codes contribute to moderate fragmentation in the AI-driven biomarker discovery market.

AI In Biomarker Discovery Industry Leaders

Tempus AI, Inc.

Owkin Inc.

PathAI Inc.

Recursion

ArteraAI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Imagene AI and Daiichi Sankyo begun a precision-oncology biomarker partnership.

- January 2026: Debiopharm deployed Genialis Expressions to accelerate multi-omics analytics.

- January 2026: Recursion raised USD 200 million Series F and expanded its BioHive-2 foundation model to 10 million proteomic perturbations.

- November 2025: Tempus launched an AI-powered minimal-residual-disease service and signed eight NCI-designated centers.

Global AI In Biomarker Discovery Market Report Scope

As per the scope of the report, AI in Biomarker Discovery refers to the use of artificial intelligence, specifically machine learning (ML) and deep learning (DL), to identify, validate, and analyze biological indicators (biomarkers) from vast, complex, and high-dimensional datasets. It transforms biomarker identification by moving beyond single-marker analysis to finding complex, multi-modal patterns that indicate disease presence, progression, or therapeutic response.

The AI in biomarker discovery market is segmented by data modality, disease area, AI approach, biomarker type, end-user, and deployment/access model. By data modality, the market includes genomics, transcriptomics (bulk, single-cell), proteomics, metabolomics/lipidomics, epigenomics, and others. By disease area, the market is segmented into oncology, immunology/inflammation, cardiometabolic, neurology/neurodegeneration, infectious diseases, rare/genetic disorders, and others. By AI approach, the market is categorized into supervised and classical ML, deep learning (CNNs/RNNs/Transformers), self-/weakly-supervised and transfer learning, foundation models (pathology, radiology, omics), graph and network-based ML, and others. By biomarker type, the market is segmented into predictive biomarkers, prognostic biomarkers, safety biomarkers, surrogate endpoints, and other types. By end-user, the market includes biopharma and biotech sponsors, diagnostics and CDx developers, contract research/central labs, academic and research institutes, and others. By deployment/access model, the market is segmented into cloud/SaaS, hybrid, on-premises, and federated/edge deployments. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Genomics (WES/WGS, targeted panels) |

| Transcriptomics (bulk, single-cell) |

| Proteomics |

| Metabolomics/Lipidomics |

| Epigenomics |

| Others |

| Oncology (solid and hematologic) |

| Immunology/Inflammation |

| Cardiometabolic (CVD, diabetes, NASH) |

| Neurology/Neurodegeneration |

| Infectious Diseases |

| Rare/Genetic Disorders |

| Others |

| Supervised and Classical ML |

| Deep Learning (CNNs/RNNs/Transformers) |

| Self-/weakly-supervised and Transfer Learning |

| Foundation Models (pathology, radiology, omics) |

| Graph and Network-based ML |

| Others |

| Predictive Biomarkers |

| Prognostic Biomarkers |

| Safety Biomarkers |

| Surrogate Endpoints |

| Other Types |

| Biopharma and Biotech Sponsors |

| Diagnostics and CDx Developers |

| Contract Research/Central Labs |

| Academic and Research Institutes |

| Others |

| Cloud/SaaS |

| Hybrid |

| On-premises |

| Federated/Edge Deployments |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Data Modality | Genomics (WES/WGS, targeted panels) | |

| Transcriptomics (bulk, single-cell) | ||

| Proteomics | ||

| Metabolomics/Lipidomics | ||

| Epigenomics | ||

| Others | ||

| By Disease Area | Oncology (solid and hematologic) | |

| Immunology/Inflammation | ||

| Cardiometabolic (CVD, diabetes, NASH) | ||

| Neurology/Neurodegeneration | ||

| Infectious Diseases | ||

| Rare/Genetic Disorders | ||

| Others | ||

| By AI Approach | Supervised and Classical ML | |

| Deep Learning (CNNs/RNNs/Transformers) | ||

| Self-/weakly-supervised and Transfer Learning | ||

| Foundation Models (pathology, radiology, omics) | ||

| Graph and Network-based ML | ||

| Others | ||

| By Bimarker Type | Predictive Biomarkers | |

| Prognostic Biomarkers | ||

| Safety Biomarkers | ||

| Surrogate Endpoints | ||

| Other Types | ||

| By End User | Biopharma and Biotech Sponsors | |

| Diagnostics and CDx Developers | ||

| Contract Research/Central Labs | ||

| Academic and Research Institutes | ||

| Others | ||

| By Deployment / Access Model | Cloud/SaaS | |

| Hybrid | ||

| On-premises | ||

| Federated/Edge Deployments | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI in biomarker discovery market today?

The AI in biomarker discovery market size stood at USD 2.4 billion in 2026 and is projected to reach USD 7.4 billion by 2031.

What is the expected growth rate of this field?

Between 2027 and 2031, the market is forecast to grow at a 25.17% CAGR, driven by clear AI/ML regulatory guidance and multi-omics data expansion.

Which disease area contributes the most revenue?

Oncology leads with 43.18% of 2025 revenue, reflecting payers demand for biomarker-guided therapies and the high heterogeneity of tumors.

Which biomarker category is expanding fastest?

Predictive biomarkers are advancing at a 28.11% CAGR as companion diagnostics tie reimbursement directly to molecular evidence of response.

Who are the leading companies in this space?

Tempus, Guardant Health, Foundation Medicine, SOPHiA GENETICS, and PathAI collectively command 38% of global revenue, positioning them as key incumbents.

Why is Asia-Pacific a high-growth region?

Government-funded precision-medicine programs and data-sovereignty laws that favor federated AI are propelling Asia-Pacific to a 30.08% CAGR through 2031.

Page last updated on: