AI In Proteomics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.72 Billion |

| Market Size (2031) | USD 12.51 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

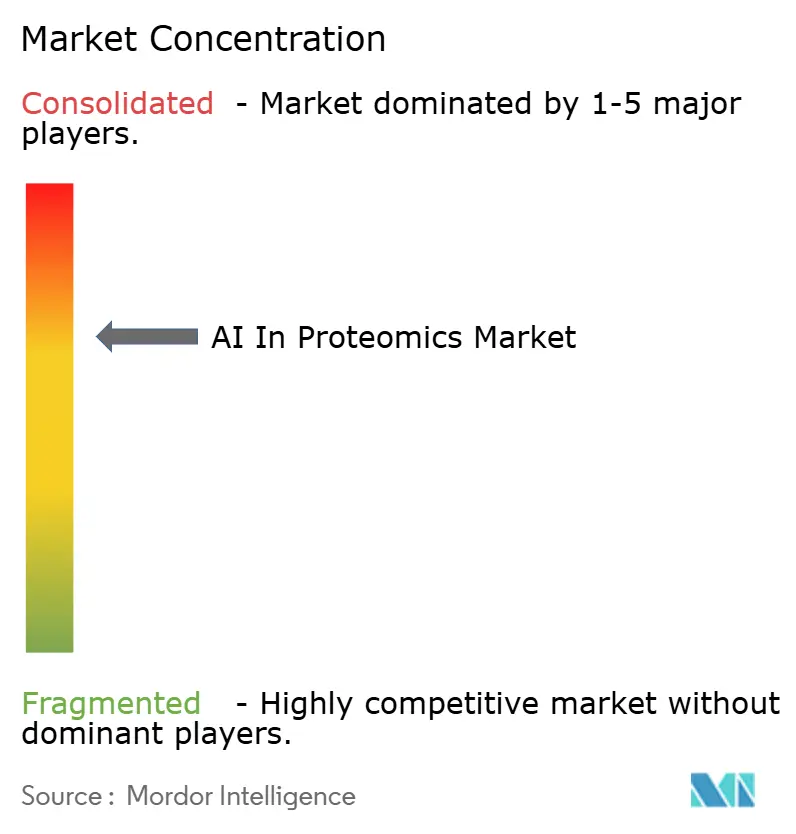

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Proteomics Market Analysis by Mordor Intelligence

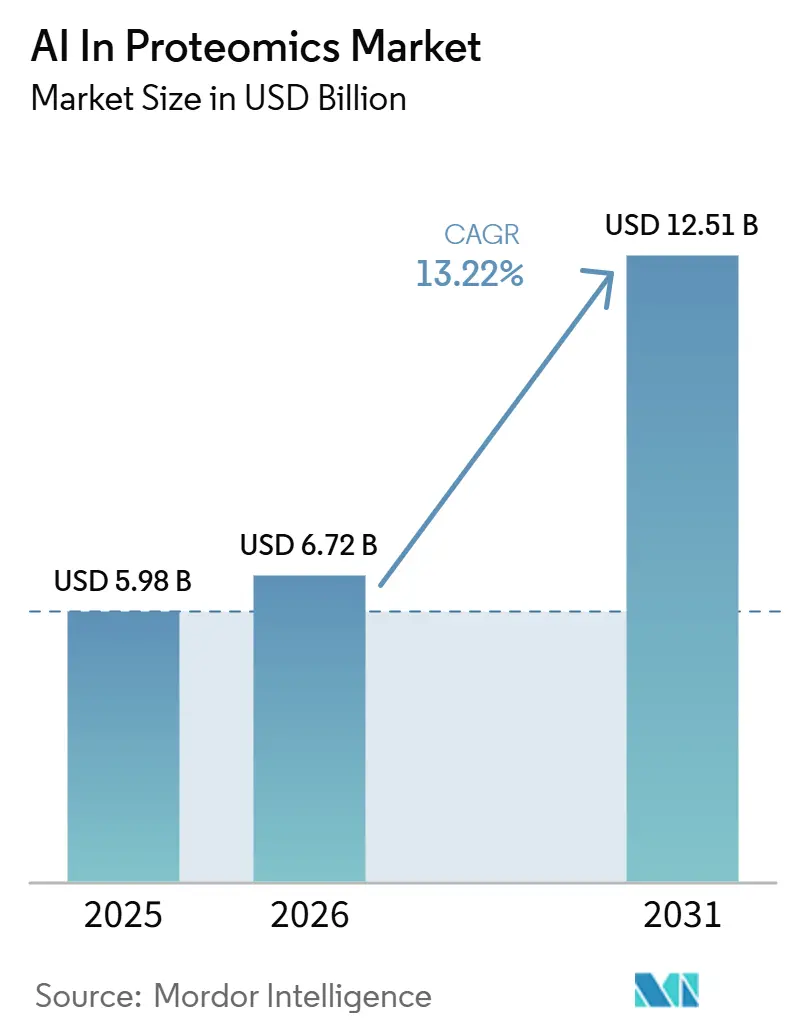

The AI in proteomics market is expected to grow from USD 5.98 billion in 2025 to USD 6.72 billion in 2026 and is forecasted to reach USD 12.51 billion by 2031 at 13.22% CAGR over 2026-2031. The AI in proteomics market is expanding because protein-level analysis now supports disease modeling, target validation, and patient stratification in ways that extend beyond genomics-only workflows. Faster translational research programs, stronger demand for AI-native analytics, and wider use of high-sensitivity mass spectrometry are increasing the volume of complex datasets that require automated interpretation. Data residency rules in the European Union, China, and India are also changing platform design, because buyers increasingly want regional deployment options and on-premise inference for sensitive research and clinical data. Regulatory review for software used in clinical proteomics is becoming a larger part of procurement, which means technical performance alone is no longer enough to win enterprise contracts. In the AI in proteomics market, these conditions favor vendors that combine analytics, workflow integration, compliance support, and flexible infrastructure into one commercial offering.

Key Report Takeaways

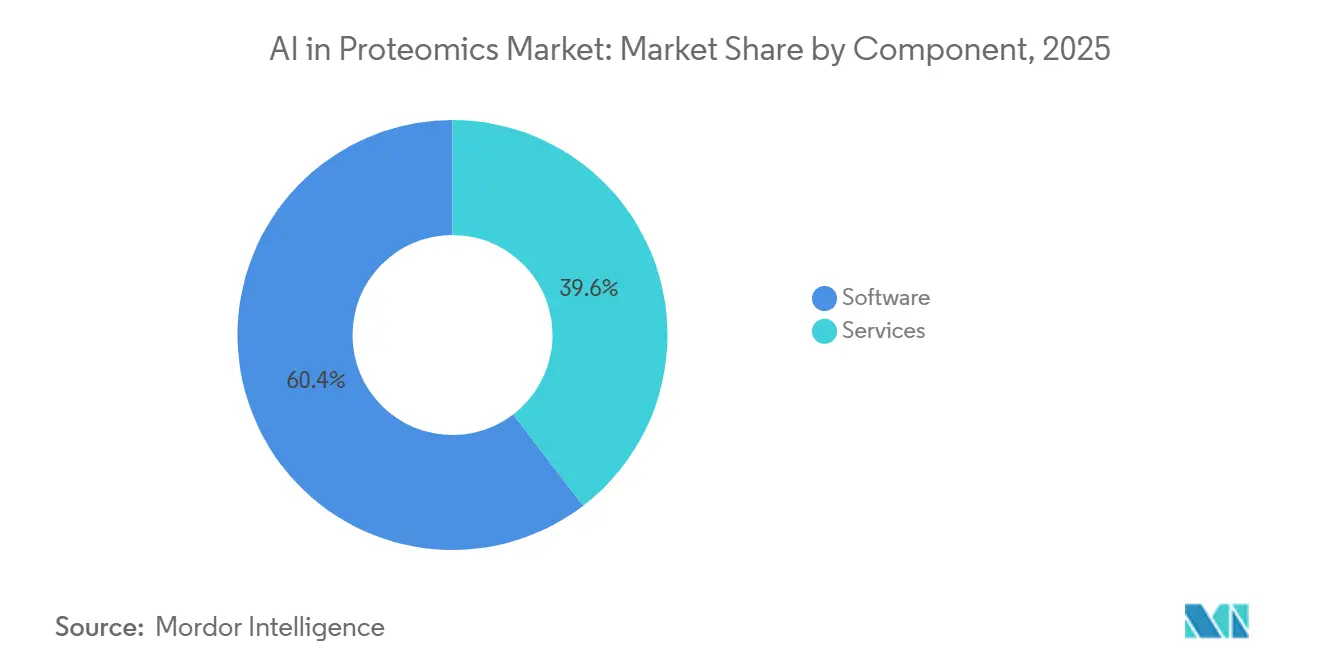

- By component, software held 60.37% of revenue in 2025, while services are projected to record the fastest growth at a 13.49% CAGR through 2031.

- By technology, mass spectrometry accounted for 41.83% of revenue in 2025, while next-generation sequencing is forecasted to expand at a 13.76% CAGR through 2031.

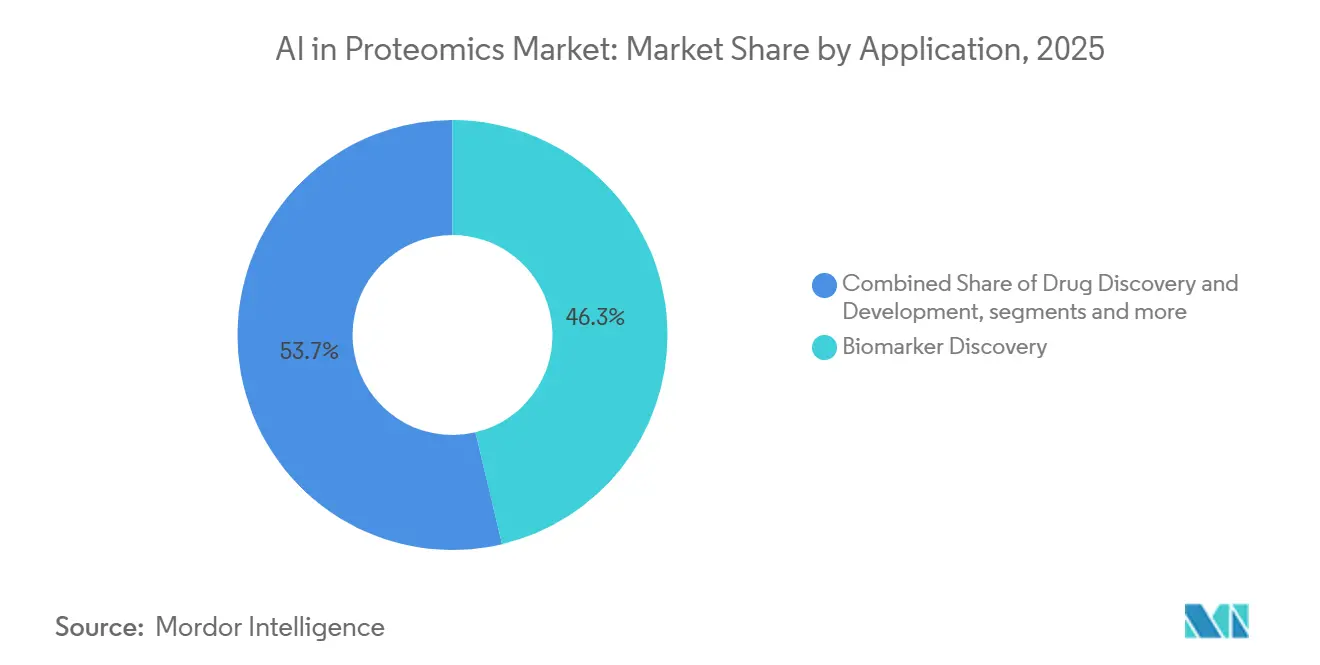

- By application, drug discovery and development captured 46.28% of revenue in 2025, while biomarker discovery is expected to grow at a 15.6% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies represented 48.52% of revenue in 2025, while academic and research institutes are projected to advance at a 14.28% CAGR through 2031.

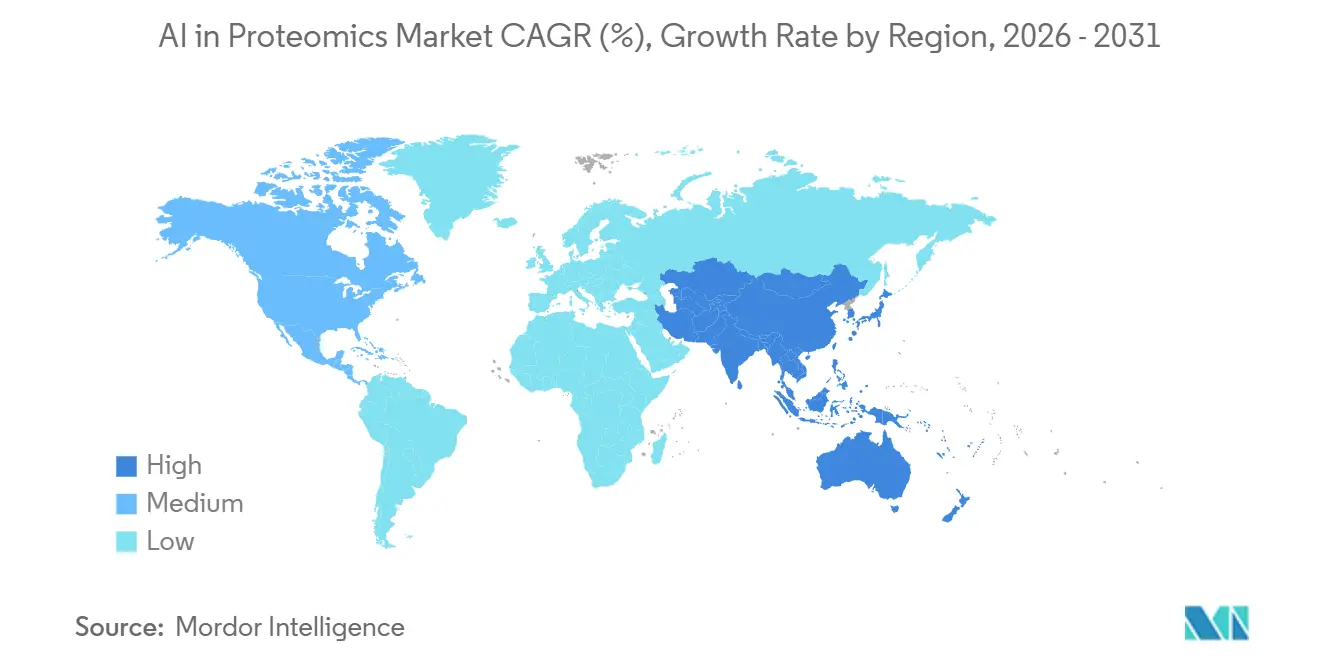

- By geography, North America held 50.14% of revenue in 2025, while Asia-Pacific is forecasted to post the fastest regional growth at a 16.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Proteomics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Precision Medicine and Translational Biomarkers | +3.2% | Global, with concentrated early gains in North America and Europe | Long term (≥ 4 years) |

| AI-Enabled Deconvolution of High-Dimensional Proteomics Data | +2.8% | Global, with early adoption in North America and Asia-Pacific, especially China and Japan | Medium term (2-4 years) |

| Expansion of Single-Cell and Spatial Proteomics Workflows | +2.1% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Automated Drug Discovery Target Validation | +2.4% | Global, with primary uptake in North America and Europe | Short term (≤ 2 years) |

| Cloud-Native Bioinformatics and Federated Analytics Adoption | +1.5% | Global, with faster adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Sovereign Data Infrastructure and On-Premise AI Deployment Requirements | +0.8% | Europe, China, and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Precision Medicine and Translational Biomarkers

Population-scale biobanking has changed the economics of biomarker work in the AI in proteomics market because large cohorts now provide the training depth needed for stronger model development and validation. Studies built on cohorts ranging from 5,000 to 50,000 samples, including work linked to UK Biobank and FinnGen, show that broader and deeper proteomic datasets can support clinically relevant biomarker panel development at a pace that was harder to achieve a few years earlier.[1]Müller-Reif et al., “ADAPT-MS Study on Proteome-Wide Biofluid Data and Continuous-Learning Clinical Decision Support,” Nature Communications, nature.comThermo Fisher Scientific’s collaboration with Precision Health Research Singapore for the PRECISE-SG100K initiative extends the same pattern into Asia through 10,000 plasma samples profiled with complementary Olink assay and Orbitrap mass spectrometry workflows.[2]Thermo Fisher Scientific, “PRECISE-SG100K Collaboration for Plasma Proteomics Profiling,” Business Wire, businesswire.comThis matters for the AI in proteomics market because validated panels are moving beyond research publication cycles and into companion diagnostic and regulated clinical development programs. That shift expands commercial demand from one-time discovery projects toward repeat software usage, model refinement, and workflow monitoring across study stages. As the AI in proteomics market moves closer to clinical deployment, vendors with stronger biomarker interpretation tools and cleaner audit trails are positioned to capture a larger share of recurring spending.

AI-Enabled Deconvolution of High-Dimensional Proteomics Data

The AI in proteomics market continues to face a core data challenge because model performance depends on the quality, structure, and interoperability of the underlying proteomics datasets as much as on the model itself. A 2026 Proteomes commentary argued that AI readiness should begin at the point of data capture, and it also noted that proteoform-resolved inputs can outperform broader protein-group approaches in pathway inference and cross-cohort generalization.[3]Proteomes Editorial Team, “Framework for Next-Generation Mass Spectrometry-Based Proteomics,” Proteomes, mdpi.com In the AI in proteomics market, this kind of tool matters because database-independent interpretation helps researchers work with poorly annotated organisms, rare disease states, and complex immunopeptidomics samples. Neural network-based spectral prediction is also lowering the effort required to build high-quality reference libraries, which can shorten setup times for new programs. As a result, the AI in proteomics market is seeing more value move toward software environments that can standardize raw input quality and improve confidence in downstream biological interpretation.

Expansion of Single-Cell and Spatial Proteomics Workflows

The AI in proteomics market is also being pushed forward by spatial and single-cell workflows because bulk protein profiling often misses tissue context and cell-state variation that affect target relevance. Deep Visual Proteomics, published in Nature in 2025, showed that up to 5,000 proteins could be quantified in single cells within tissue context, which gives researchers a more workable route to spatially resolved target validation at preclinical scale. In the AI in proteomics market, these advances increase demand for software that can combine image-derived context, spatial protein patterns, and mass spectrometry output in one analytical environment. That requirement is important because instrument vendors and pure-play bioinformatics companies still do not fully cover the same workflow breadth. As spatial proteomics moves into broader preclinical use, the AI in proteomics market is likely to reward vendors that can reduce the integration burden across multiple modalities without weakening result traceability.

Rising Demand for Automated Drug Discovery Target Validation

The AI in proteomics market is gaining from faster target validation cycles because pharmaceutical teams want shorter timelines between protein target nomination and early development decisions. In the AI in proteomics market, those developments reinforce a shift toward software-led target evaluation and more automated biologics design support. They also strengthen the role of specialist service providers and contract research groups that can package target discovery, proteomic analysis, and AI interpretation into one faster engagement model. As discovery organizations try to improve program productivity, the AI in proteomics market is benefiting from demand for tools that can connect biological evidence generation with decision-ready outputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Multimodal Instrumentation and Compute Infrastructure | -2.1% | Global, with the sharpest pressure in emerging Asia-Pacific markets and South America | Medium term (2-4 years) |

| Lack of Cross-Platform Data Standardization for AI Model Training | -1.8% | Global | Long term (≥ 4 years) |

| Shortage of Proteomics-Bioinformatics Talent | -1.2% | Global, with the greatest strain in Asia-Pacific and other emerging markets | Medium term (2-4 years) |

| Data Provenance, Privacy, and IP Ambiguity in AI Model Development | -1.0% | Europe under GDPR, North America under FDA oversight, and China under PIPL | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Multimodal Instrumentation and Compute Infrastructure

The AI in proteomics market still faces a meaningful adoption barrier because next-generation mass spectrometry systems, supporting compute layers, and managed data infrastructure require large capital commitments. Single-cell proteomics and spatial proteoform analysis depend on high-specification instrumentation, and the combined cost of instruments, compute, and data handling can exceed the annual proteomics budgets of many hospitals and academic centers outside North America and Western Europe. That cost issue matters in the AI in proteomics market because growth assumptions rely on broader geographic participation, including countries where research budgets and procurement flexibility are more limited. Leasing models and cloud-based laboratory service structures reduce some of the upfront burden, but they do not yet remove the full cost gap for end-to-end AI proteomics workflows. The region with the fastest projected growth, Asia-Pacific, still reflects strong public investment ambition rather than a fully balanced cost structure today. Until the total deployment cost falls further, the AI in proteomics market will remain more accessible to well-funded biopharma groups, national programs, and top research centers than to mid-tier institutions.

Lack of Cross-Platform Data Standardization for AI Model Training

The AI in proteomics market is also constrained by inconsistent data standards because model accuracy often drops when training data and deployment data come from different instruments, assay chemistries, or sample preparation protocols. In the AI in proteomics market, this means large pharmaceutical users still need custom harmonization layers when they run multi-vendor workflows, and those layers add cost, time, and implementation risk. The burden is often underestimated during early vendor selection, especially when buyers focus more on benchmark performance than on downstream integration effort. As a result, the AI in proteomics market continues to favor vendors that can align instruments, software, and data management under one more standardized operating environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Economics Define Platform Differentiation

Software held 60.37% of AI in proteomics market share in 2025, which shows that value creation has moved toward interpretation, workflow orchestration, and decision support rather than remaining centered on hardware alone. In the AI in proteomics market, this revenue mix reflects a clear change in buying priorities because researchers and biopharma teams need tools that can turn large proteomic datasets into usable outputs across discovery and translational programs. Regional specialists are also gaining room to compete, and aiwell Japan’s integrated proteomics analytics platform shows how unified interfaces for mass spectrometry, affinity assays, and pathway analysis can answer customer demand that larger OEMs have not fully addressed. This makes the software layer the most defensible category in the AI in proteomics market because it shapes daily workflow use, data portability, and customer switching costs.

The AI in proteomics market for services is projected to expand at a 13.49% CAGR from 2026 to 2031, which shows how strongly customers are leaning toward outsourced and outcome-based operating models. Pharmaceutical teams increasingly want support that runs from sample preparation through AI-assisted interpretation, because this can shorten early-stage project timelines without requiring internal platform buildout. Over time, the AI in proteomics market is likely to see a wider mix of hybrid models where software subscriptions, managed analytics, and project-based scientific support are sold together rather than as separate offers.

By Technology: Mass Spectrometry Anchors Revenue, NGS Scales at Volume

Mass spectrometry accounted for 41.83% of revenue in 2025, and that lead remains central to the AI in proteomics market because no competing platform offers the same combination of proteome depth, post-translational modification visibility, and broad discovery utility. The technology remains the reference layer for discovery-heavy programs, especially where researchers need to quantify thousands of proteins in parallel and retain detailed molecular resolution

The AI in proteomics market for next-generation sequencing is projected to expand at a 13.76% CAGR from 2026 to 2031, driven by closer operational convergence between proteomics and genomics. Illumina’s completed acquisition of SomaLogic in January 2026 created an NGS-based proteomics platform that can measure up to 11,000 proteins using aptamer sequencing on standard NovaSeq infrastructure. That move matters in the AI in proteomics market because it overlays proteomic measurement on existing sequencing workflows and can improve cost efficiency at high sample volumes. It also gives multiomics programs a more unified instrument layer, which is attractive for population studies and large translational datasets. Protein microarrays, chromatography, X-ray crystallography, and microfluidics continue to hold defined niche roles, and microfluidics is gaining more attention as smaller-format proteomics workflows move closer to point-of-care and constrained-sample use cases.

By Application: Drug Discovery Anchors Revenue, Biomarker Discovery Leads Growth

Drug discovery and development accounted for 46.28% of revenue in 2025, which keeps it as the largest application area in the AI in proteomics market because pharmaceutical users have already embedded proteomic analysis into target identification, lead optimization, and biomarker validation. The segment benefits from long-standing demand for tools that can connect protein expression data with mechanism understanding and candidate prioritization. In the AI in proteomics market, this creates a stable revenue base because discovery teams need repeated analytical support across several stages rather than only at one experimental step. Clinical diagnostics and precision and personalized medicine remain meaningful applications, but their pace is steadier because clinical evidence, reimbursement progress, and regulatory clarity still shape adoption timing. Agricultural and environmental proteomics remain smaller contributors, yet they provide a useful diversification path because their demand drivers are not tied as directly to pharmaceutical spending cycles.

The AI in proteomics market for biomarker discovery is projected to expand at a 15.16% CAGR through 2031, making it the fastest-growing application as large cohort studies produce richer AI-ready datasets. RyboDyn’s USD 10 million seed round in March 2026 also shows that venture capital sees dark-proteome target and biomarker discovery as a distinct commercial opportunity with its own intellectual property value. As these programs scale, the AI in proteomics market is likely to see more software demand tied to panel refinement, cohort comparison, and model governance across research and preclinical environments.

By End-User: Pharma Anchors Spend, Academia Scales Platform Volume

Pharmaceutical and biotechnology companies represented 48.52% of revenue in 2025, which keeps them as the largest spending group in the AI in proteomics market because proteomics is already tied to discovery and clinical development budgets at large global firms. Their buying behavior is shaped by a tension between platform consolidation and performance specialization, since many want fewer vendors but still seek best-in-class AI capability for selected workflow steps. In the AI in proteomics market, suppliers that can show validated performance within a regulatory-grade framework hold an advantage because clinical-stage teams place heavy weight on documentation, repeatability, and traceability. The result is a buyer group that remains large and stable, but also demanding, which raises the bar for newer entrants that want to sell directly into late-stage development settings.

Academic and research institutes are projected to grow at a 14.28% CAGR from 2026 to 2031, which gives them an outsized role in expanding installed base and workflow familiarity across the AI in proteomics market. Contract research organizations continue to play a durable role between academia and pharma, and their software-related service revenue is likely to rise faster than hardware-linked revenue as analytics becomes more central to project delivery. Over time, the AI in proteomics market gains from this end-user mix because academic growth broadens platform usage while pharmaceutical demand continues to anchor higher-value commercial contracts.

Geography Analysis

North America accounted for 50.14% of AI in proteomics market share in 2025, which kept it as the leading regional contributor because it combines major biopharma headquarters, academic medical centers, and established AI software ecosystems in one dense operating environment. The region also benefits from clearer regulatory direction, because evolving FDA Software as a Medical Device guidance gives pharmaceutical users a more structured route for integrating software outputs into regulated development workflows. Europe remained the second-largest region because Horizon Europe funding, a dense pharmaceutical base, and GDPR-driven interest in on-premise and federated deployments continue to support local demand patterns.

Asia-Pacific is projected to grow at a 16.34% CAGR from 2026 to 2031, which makes it the fastest-growing regional block in the AI in proteomics market because government biobanking, domestic AI investment, and contract research expansion are moving in parallel. The region’s growth pattern differs from North America because it relies more visibly on coordinated national initiatives and infrastructure-building programs. China’s National Supercomputer Center in Tianjin launched the GalaxyVS AI platform in May 2026, using the DrugCLIP deep learning framework from Tsinghua University to enable virtual screening of 100 billion synthesizable compounds in support of faster target validation pipelines. Singapore’s PRECISE-SG100K collaboration is also important because it is building a large and ethnically diverse plasma proteome reference set that can improve biomarker model relevance for Asian populations. As the AI in proteomics market expands in Asia-Pacific, buyers are likely to put increasing weight on local data control, regional deployment options, and scalable partnerships with CROs and academic networks.

Middle East and Africa remains an early-stage part of the AI in proteomics market, but sovereign health investments tied to precision medicine programs are creating an initial base for proteomics infrastructure and analytics demand. South America is still constrained by high instrument import costs and limited domestic proteomics talent, even though university groups in Brazil and Argentina continue to support active research linked to oncology biomarker programs. Both regions are growing from a low base in the AI in proteomics market, and their progress depends more heavily on cloud-native delivery models that can reduce upfront capital needs. This pattern suggests that platform familiarity and skills development may arrive before large-scale laboratory buildout, which is similar to how other advanced life science workflows spread into these regions over earlier adoption cycles.

Competitive Landscape

The AI in proteomics market is moderately concentrated at the platform and instrument layer, but it remains more fragmented at the analytics and software tier where new entrants continue to emerge. Thermo Fisher Scientific’s acquisitions of MSAID and Proteinaceous in 2026 show how large vendors are buying specialized capabilities rather than relying only on internal software development for AI-led interpretation and top-down protein characterization. Illumina’s integration of SomaLogic introduced a large-scale NGS-native proteomics option, which changes the basis of competition by forcing mass spectrometry incumbents to emphasize proteomic depth, biological resolution, and workflow flexibility. Bruker’s ProteoScape v2026b, with an AI-enhanced scoring model trained on more than 7 million MS/MS spectra, also shows that proprietary model weights are becoming an intellectual property asset alongside instruments and assay chemistry. In the AI in proteomics market, this has raised the strategic value of software ownership because model performance, training data quality, and workflow interoperability now shape commercial differentiation almost as much as instrument design.

White-space opportunities in the AI in proteomics market remain concentrated where spatial proteomics, multimodal AI, and federated data infrastructure overlap, because no single supplier fully covers that combined operating space today. Open foundation model efforts such as KRONOS also suggest that more platform-agnostic analytical approaches will continue to develop, especially for image-rich and spatially resolved datasets. Vendors that can prove cross-platform model generalization and support compliance-grade documentation are better placed to win enterprise budgets as more programs move toward regulated use cases. The pattern of acquisitions across 2025 and 2026 indicates that large incumbents recognize a speed disadvantage in software innovation and are using capital deployment to close that gap faster.

Regional fragmentation is becoming a larger competitive factor in the AI in proteomics market because sovereign data rules and differing compliance expectations are shaping where models can be trained, deployed, and updated. Buyers are increasingly comparing vendors on deployment flexibility, local infrastructure compatibility, and the ability to document performance across mixed instrument environments. That pushes competition away from a simple hardware-versus-software split and toward broader workflow accountability across data generation, interpretation, and reporting. As a result, the AI in proteomics market is likely to remain mixed in structure, with a handful of strong integrated leaders at the top and a wide field of specialized analytics providers continuing to compete below them.

AI In Proteomics Industry Leaders

Thermo Fisher Scientific Inc.

Danaher Corporation

Agilent Technologies, Inc.

Bruker Corporation

Waters Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: OpenProtein.AI was selected as a performer on DARPA's Network of Optimal Dynamic Energy Signatures (NODES) program, tasked with developing next-generation AI models that predict protein function through structural dynamics, the program began in March 2026.

- April 2026: 10x Science closed a USD 4.8 million seed round led by Initialized Capital and Y Combinator (W26 batch) to build an AI-native platform for automated protein characterization, targeting proteoform-resolved mass spectrometry data analysis for biologics drug developers.

- March 2026: RyboDyn closed a USD 10 million seed financing round to advance AI-powered discovery of hidden cancer protein targets in the dark proteome, operating within Lilly's AI TuneLabs consortium and NVIDIA's Inception Program, with a disclosed strategic collaboration with Moffitt Cancer Center.

- March 2026: OpenProtein.AI expanded its strategic partnership with Boehringer Ingelheim to co-develop antibody discovery and optimization workflows, building on a successful 2025 deployment and integrating AI foundation models directly into Boehringer Ingelheim's end-to-end therapeutic development process.

Global AI In Proteomics Market Report Scope

According to the report’s scope, the AI in proteomics market is the application of artificial intelligence to protein science, using machine learning and deep learning to accelerate structure prediction, biomarker discovery, and drug design by analyzing complex proteomic datasets. It enhances accuracy, efficiency, and innovation in research and healthcare.

The AI in proteomics market is segmented into component, technology, application, end-user, and geography. By component, the market is segmented into software and services. By technology, the market is segmented into mass spectrometry, protein microarrays, chromatography, next-generation sequencing, x-ray crystallography, microfluidics, and other technologies. By application, the market is segmented into biomarker discovery, drug discovery and development, clinical diagnostics, precision and personalized medicine, agricultural and environmental proteomics, and other applications. By end-user, the market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, contract research organizations, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Mass Spectrometry |

| Protein Microarrays |

| Chromatography |

| Next-Generation Sequencing |

| X-Ray Crystallography |

| Microfluidics |

| Other Technologies |

| Biomarker Discovery |

| Drug Discovery and Development |

| Clinical Diagnostics |

| Precision and Personalized Medicine |

| Agricultural and Environmental Proteomics |

| Other Applications |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Contract Research Organizations |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Technology | Mass Spectrometry | |

| Protein Microarrays | ||

| Chromatography | ||

| Next-Generation Sequencing | ||

| X-Ray Crystallography | ||

| Microfluidics | ||

| Other Technologies | ||

| By Application | Biomarker Discovery | |

| Drug Discovery and Development | ||

| Clinical Diagnostics | ||

| Precision and Personalized Medicine | ||

| Agricultural and Environmental Proteomics | ||

| Other Applications | ||

| By End-User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Contract Research Organizations | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the AI in proteomics market by 2031?

The AI in proteomics market is forecasted to reach USD 12.51 billion by 2031, rising from USD 5.98 billion in 2025 to USD 6.72 billion in 2026 at a 13.22% CAGR over 2026-2031.

Which component generates the most revenue in AI-driven proteomics?

Software led the revenue mix with 60.37% in 2025, showing that interpretation, workflow integration, and analytics are more central than instruments alone.

Why is biomarker discovery expanding faster than other proteomics AI applications?

Biomarker discovery is projected to grow at 15.16% CAGR because large cohort studies and adaptive AI models are improving the speed and depth of clinical and translational biomarker work.

Which region is growing fastest for proteomics AI adoption?

Asia-Pacific is the projected to be the fastest-growing region with a 16.34% CAGR through 2031, supported by biobanking, domestic AI programs, and expanding CRO capacity.

Page last updated on: