AI CRISPR Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

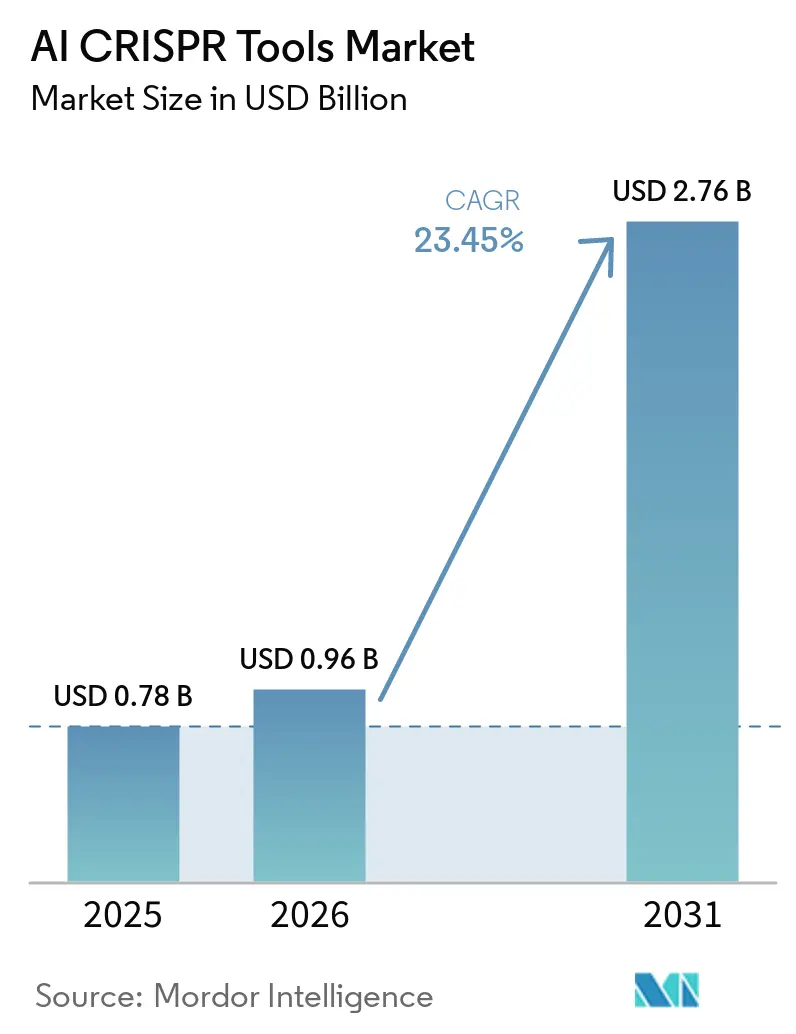

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 23.45% CAGR |

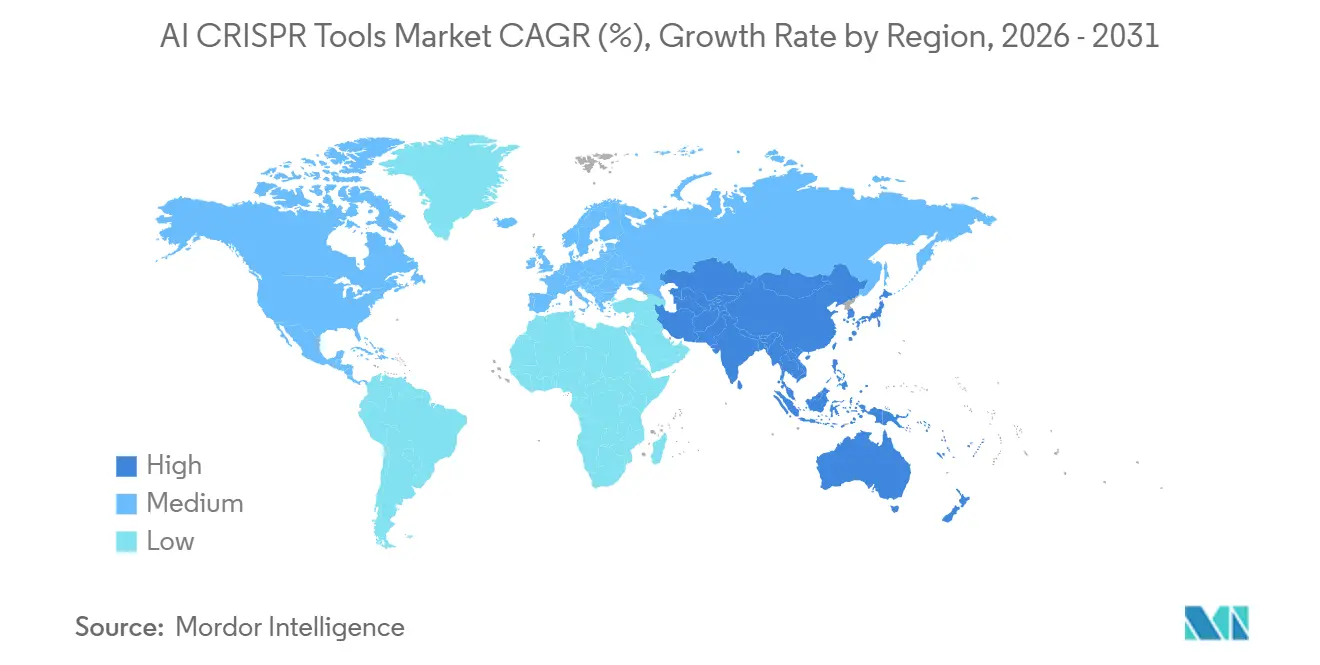

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

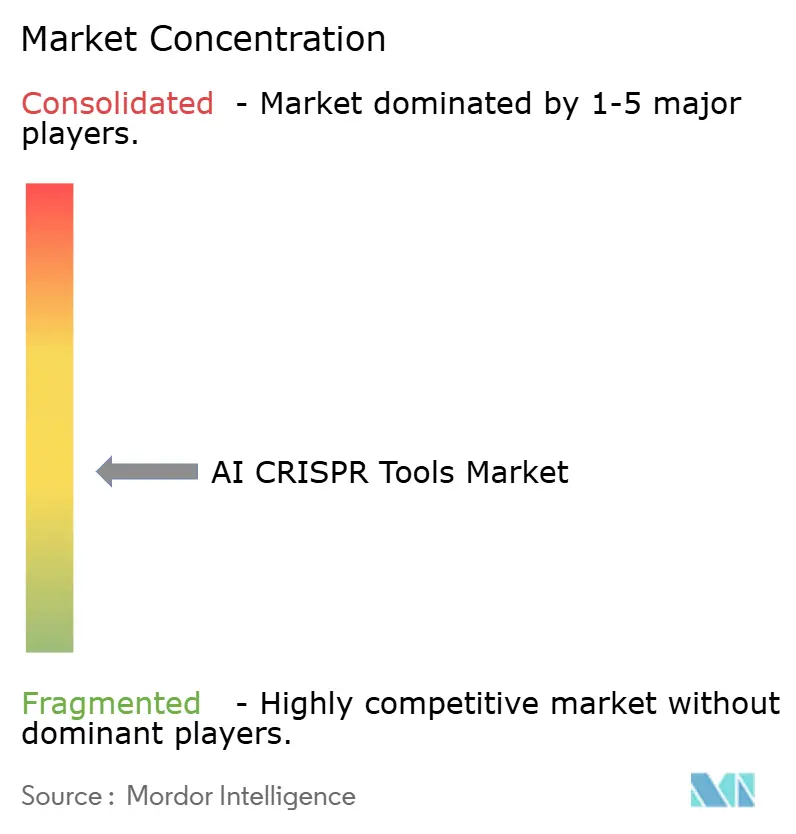

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI CRISPR Tools Market Analysis by Mordor Intelligence

The AI CRISPR Tools Market size is projected to be USD 0.78 billion in 2025, USD 0.96 billion in 2026, and reach USD 2.76 billion by 2031, growing at a CAGR of 23.45% from 2026 to 2031.

The AI CRISPR tools market is expanding as genome editing work moves away from trial-and-error lab cycles and toward computational design that can guide decisions earlier in the workflow. Large language models trained on protein sequences and high-throughput CRISPR screening datasets are now shaping guide RNA selection, Cas protein engineering, and synthetic nuclease discovery in the same platform environment. This shift is changing the commercial model of the AI CRISPR tools market because software, data infrastructure, and workflow services are becoming more central than standalone reagent sales.

Key Report Takeaways

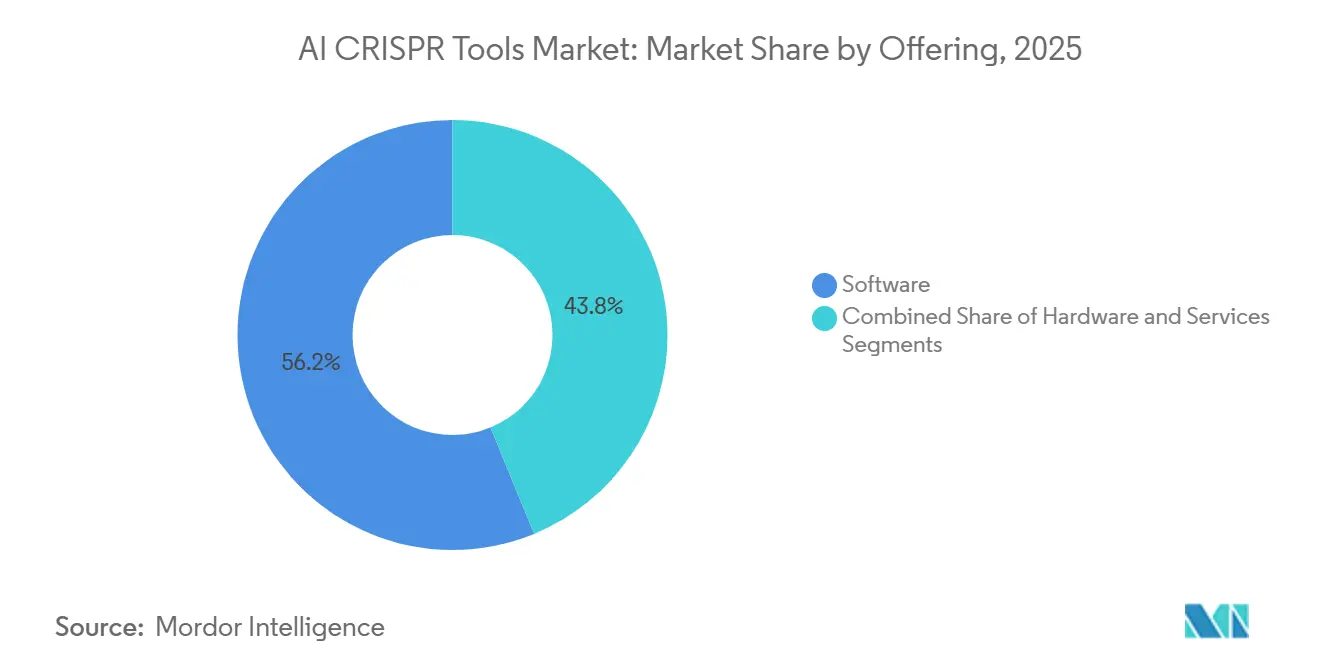

- By offering, software led with 56.20% share in 2025, while services is projected to expand at a 25.05% CAGR through 2031.

- By CRISPR technology, CRISPR-Cas9 held 37.78% share in 2025, while CRISPR-Cas12 is projected to grow at a 25.76% CAGR through 2031.

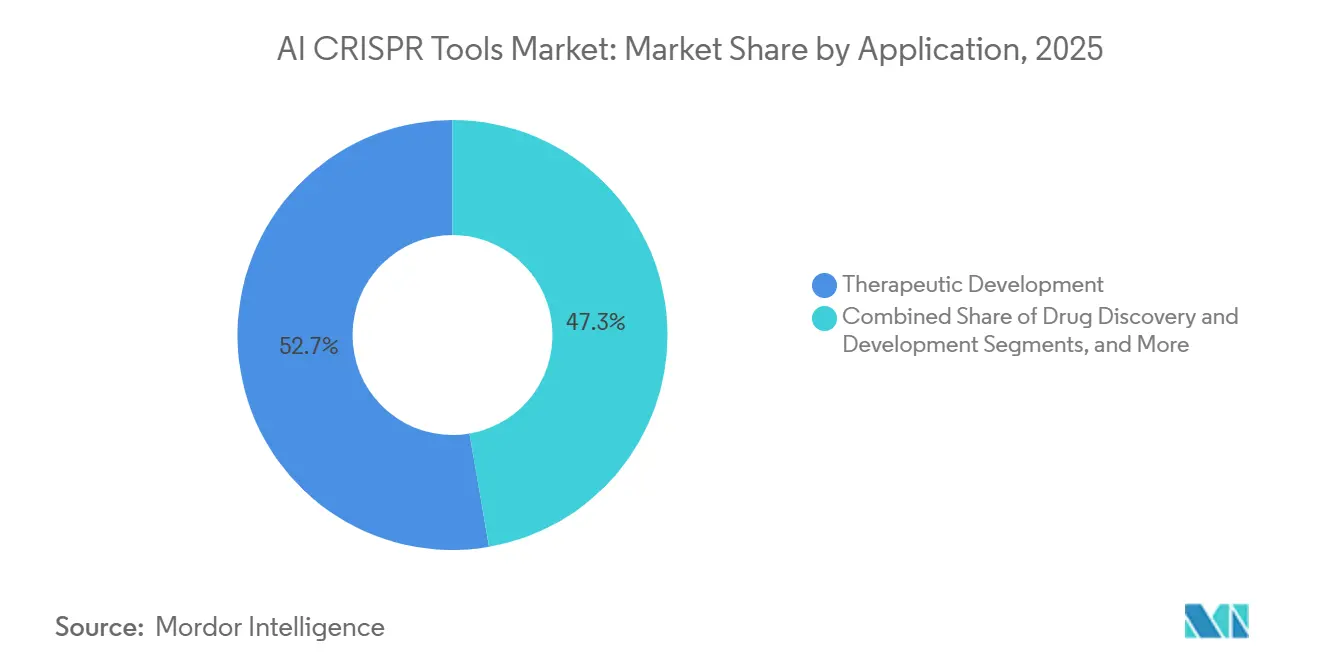

- By application, therapeutic development accounted for 52.72% share in 2025, while drug discovery and development is projected to advance at a 26.15% CAGR through 2031.

- By deployment model, cloud-based deployment held 40.95% share in 2025, while on-premises deployment is projected to grow at a 26.75% CAGR through 2031.

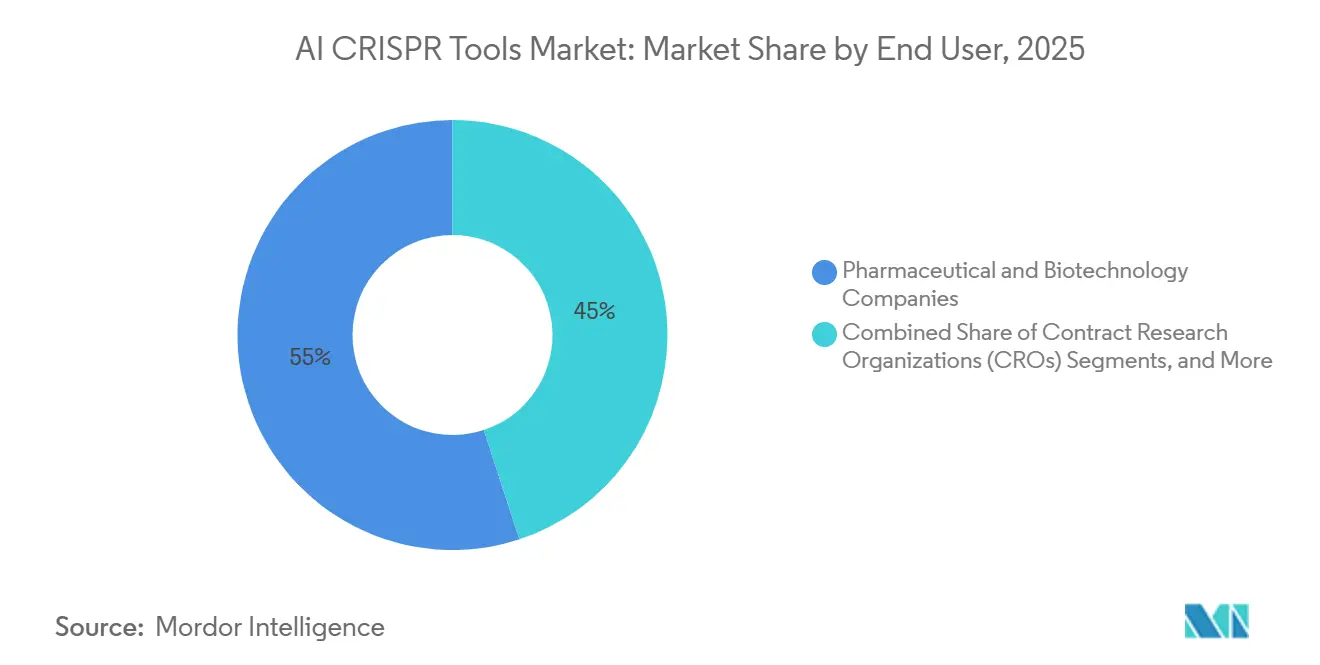

- By end user, pharmaceutical and biotechnology companies held 55.04% share in 2025, while contract research organizations and CDMOs are projected to grow at a 23.95% CAGR through 2031.

- By geography, North America held 42.30% share in 2025, while Asia-Pacific is projected to expand at a 27.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI CRISPR Tools Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing adoption of AI for guide RNA design and off-target prediction | +5.2% | Global, with highest intensity in North America and Europe | Short term (≤ 2 years) |

| Expansion of CRISPR therapeutic clinical pipelines driving platform demand | +4.5% | North America and Europe, with accelerating APAC contribution | Medium term (2-4 years) |

| Rising investment in AI-driven functional genomics and target validation | +3.2% | Global, particularly strong in North America, China, and South Korea | Medium term (2-4 years) |

| Falling compute costs democratizing AI-enabled CRISPR tool access | +2.6% | Global, most impactful in APAC and South America research ecosystems | Short term (≤ 2 years) |

| Emergence of foundation model-based and generative AI nuclease design platforms | +3.8% | North America core, with spillover to Europe and APAC | Medium term (2-4 years) |

| Strategic pharma-biotech alliances accelerating AI CRISPR workflow adoption | +2.9% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of AI for Guide RNA Design and Off-Target Prediction

The AI CRISPR tools market is advancing due to improvements in guide RNA design and off-target prediction models. In 2025, a deep learning model, CCLMoff, achieved an AUROC of 0.985 on CIRCLE-seq off-target datasets across 418 single-guide RNAs using sequence input alone.[1]Jeffrey A. Ruffolo, Stephen Nayfach, Joseph Gallagher, Aadyot Bhatnagar, et al., “Design of Highly Functional Genome Editors by Modelling CRISPR-Cas Sequences,” Nature, doi.org This high prediction accuracy reduces the need for repeated wet-lab screenings, shifting preclinical safety evaluations to in silico filtering. This transition enhances the scalability of design libraries and drives demand for design software and predictive services in therapeutic and discovery programs. Researchers can now test more candidates earlier, minimizing weaker guides in downstream processes.

Expansion of CRISPR Therapeutic Clinical Pipelines Driving Platform Demand

The expansion of clinical CRISPR programs across diverse diseases is driving platform demand in the AI in CRISPR tools market. Each therapeutic program requires ongoing design support for target selection, guide optimization, safety modeling, and manufacturing readiness. Computational engines now support multiple targets, increasing platform demand faster than wet-lab spending. This shift elevates the value of recurring software and workflow services over single product sales. AI tools are becoming critical in rare diseases and personalized medicine, where rapid redesigns and evidence generation are essential. Vendors with validated workflows are positioned to secure larger, long-term contracts as programs approach clinical milestones.

Emergence of Foundation Model-Based and Generative AI Nuclease Design Platforms

The AI CRISPR tools market is evolving with foundation models enabling genome editor designs beyond natural limits. In 2025, OpenCRISPR-1, an AI-generated genome editor, demonstrated a 95% reduction in off-target indels compared to SpCas9.[2]Stephen Nayfach, Aadyot Bhatnagar, Andrey Novichkov, et al., “Customizing CRISPR-Cas PAM Specificity with Protein Language Models,” Nature Biotechnology, doi.org In 2026, Protein2PAM enabled the engineering of Cas variants with up to 50-fold higher DNA cleavage kinetics than wild-type counterparts.[3]Algen Biotechnologies, “Algen Biotechnologies Announces Multi-Target Partnership to Advance AI-Powered Drug Discovery in Immunology with AstraZeneca,” Business Wire, businesswire.com These advancements address PAM restrictions, expanding the design space for therapeutic, research, and diagnostic applications. Vendors controlling both model development and experimental validation gain a competitive edge as performance increasingly relies on the integration of prediction and testing.

Strategic Pharma-Biotech Alliances Accelerating AI CRISPR Workflow Adoption

Strategic alliances are accelerating the adoption of AI CRISPR workflows in the market. In 2025, AstraZeneca partnered with Algen Biotechnologies in a deal worth up to USD 555 million, focusing on AI-identified immunology targets. Similarly, ElevateBio collaborated with AWS to leverage protein language models for optimizing CRISPR systems. These partnerships provide proprietary data streams and enhance the credibility of AI-assisted workflows in regulated development. Smaller vendors without strong partnerships face challenges in competing on validation, speed, and access. These alliances are driving the market toward platform standardization across pharmaceutical, biotech, and service sectors.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High complexity and large dataset requirements for AI model training in genomics | -2.8% | Global, disproportionately limiting in resource-constrained APAC and South America markets | Medium term (2-4 years) |

| Regulatory ambiguity around AI-assisted gene editing workflows and data governance | -2.5% | Global, with highest compliance burden in North America and Europe | Short term (≤ 2 years) |

| Ethical and IP landscape complexity limiting commercialization speed | -2.1% | North America and Europe primarily, emerging in APAC as IP frameworks evolve | Long term (≥ 4 years) |

| Off-target effect and safety concern | -2.6% | Global, with regulatory influence under FDA and EMA scrutiny for therapeutic applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Complexity and Large Dataset Requirements for AI Model Training in Genomics

The AI CRISPR tools market faces significant challenges due to insufficient data coverage across various editing tasks. A 2025 review analyzed 50 AI predictor studies from 3,456 papers and identified only 80 public benchmark datasets across 10 CRISPR tasks. This limitation causes many models to perform well under specific training conditions but fail to generalize across diverse cell types, species, and CRISPR modalities. Vendors require extensive proprietary datasets to develop reliable tools, but the high cost of generating such datasets favors established players and hinders new entrants. As a result, the market's growth potential is constrained by the difficulty of accessing critical biological data.

Regulatory Ambiguity Around AI-Assisted Gene Editing Workflows and Data Governance

The AI CRISPR tools market also encounters obstacles due to unclear regulatory frameworks for AI-driven biological outputs. The FDA's 2026 draft guidance emphasizes detailed bioinformatics methods for off-target characterization but does not clarify how AI-predicted profiles should compare to empirical findings. Similarly, the 2025 draft guidance on AI for regulatory decision-making excludes its application in drug discovery, leaving developers to build evidence packages on a case-by-case basis. This lack of standardization increases costs, delays, and uncertainty, creating compliance challenges that slow the market's broader clinical adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Emerge as the Growth Engine Behind Dominant Software Platforms

In 2025, software dominated the AI CRISPR tools market, capturing 56.20% of the market share. This reflects the critical role of design, analytics, and data management platforms in research and pharmaceutical workflows. Software serves as the control layer for guide design, editing analysis, workflow automation, and data traceability, driving early adoption and higher switching costs. The market is increasingly shaped by platforms that integrate models, experimental data, and compliance requirements.

Benchling's launch of Benchling AI in October 2025 highlighted the evolution of offerings, with features like deep research agents and automated data entry integrated into workflows. The platform served over 1,300 biotech companies and 7,500 academic institutions globally, including major players like Merck and Moderna. Services are projected to grow faster at a 25.05% CAGR through 2031, driven by demand for bundled design, analysis, and execution models. The industry is shifting toward a hybrid model where software anchors workflows, and services expand access for customers lacking internal capabilities.

By CRISPR Technology: Cas12's IP and Diagnostic Versatility Drive Faster Adoption Than Cas9

In 2025, CRISPR-Cas9 held a 37.78% share of the AI CRISPR tools market, maintaining its position as the leading technology. Its dominance is supported by established delivery protocols, safety profiles, and extensive guide design work, which instill user confidence. Many AI models remain optimized around Cas9 datasets, benefiting from the industry's existing knowledge base.

CRISPR-Cas12 is forecast to grow at a 25.76% CAGR through 2031, making it the fastest-growing segment. Its single-stranded DNA collateral cleavage activity supports diagnostics and expands use cases beyond traditional editing workflows. Cas12 is gaining traction due to its precision, diverse targeting behavior, and adaptable platform economics, reflecting a market shift toward broader functional diversity.

By Application: Therapeutic Development Leads, but Drug Discovery Commands the Fastest Growth

In 2025, Therapeutic Development accounted for 52.75% of the AI CRISPR tools market, remaining the largest application segment. This reflects sustained investments in cell and gene therapy programs, where computational design accelerates preclinical work. Repeated demand for guide optimization and design revisions anchors spending in this segment.

Drug Discovery and Development is projected to grow at a 26.15% CAGR through 2031, driven by AI-enabled functional genomics replacing slower target identification methods. This growth aligns with the need for faster hypothesis testing across a broader range of genes and pathways, signaling a shift toward earlier discovery activities.

By Deployment Model: Cloud Leads, but On-Premises Gains as Data Sovereignty Concerns Mount

In 2025, cloud-based deployment accounted for 40.95% of the AI CRISPR tools market, making it the leading delivery model. Cloud adoption remains strong due to ease of deployment, simplified updates, and seamless integration with laboratory systems. Vendors can quickly release model improvements, and customers benefit from reduced IT burdens.

On-premises deployment is forecast to grow faster at a 26.75% CAGR through 2031, driven by the need for local compute control in regulated environments. This model addresses concerns over proprietary genomic data and sensitive records, creating a split between cloud flexibility and on-premises control to meet diverse customer needs.

By End User: Pharma and Biotech Concentration Drives Platform Depth, CROs Scale Access

In 2025, Pharmaceutical and Biotechnology Companies held a 55.04% share of the AI CRISPR tools market, making them the largest end-user group. Their investments in target discovery, IND-enabling studies, and manufacturing development drive demand for premium AI platforms and integrated datasets.

Contract Research Organizations and CDMOs are expected to grow at a 24.25% CAGR through 2031, marking the fastest growth among end users. This reflects the expansion of AI-enabled CRISPR design into outsourced research channels, broadening access for smaller or less digitally advanced customers.

Geography Analysis

In 2025, North America held a 42.30% share of the AI CRISPR tools market, maintaining its position as the largest regional contributor. The region benefits from a strong ecosystem of platform developers, financing networks, and advanced cloud infrastructure. The U.S. plays a key role in establishing evidence standards for clinical-stage gene editing programs, further strengthening North America's leadership in commercial adoption of AI CRISPR tools. Asia-Pacific is forecast to grow at a 27.25% CAGR through 2031, making it the fastest-growing region in the AI CRISPR tools market. This growth is driven by increased bioscience investments, expanding development capacity, and rising demand for outsourced research and manufacturing. The region's ability to scale quickly, without legacy system constraints, positions it as a key player in offering service-led solutions.

Europe ranked as the second-largest regional market, supported by research activities in Germany, the United Kingdom, France, Italy, and Spain. Academic and translational research centers in the region contribute significantly to editing design, repair prediction, and target validation. Strong cross-border collaborations further enhance Europe's role as a hub for computational biology and clinical research. South America remained smaller and more nascent, with activity concentrated in Brazil and Argentina. The region is supported by expanding CRO networks and collaborations between government and academia in gene editing applications. These developments highlight the diverse dynamics of the AI CRISPR tools market, with North America leading in commercial depth, Asia-Pacific excelling in growth, and Europe serving as a critical research base.

Competitive Landscape

In the AI-driven CRISPR tools market, software and services exhibit moderate fragmentation, whereas premium nuclease supplies and clinical-grade reagents see a higher concentration. Established players like Thermo Fisher Scientific and Merck KGaA leverage global distribution, regulatory-grade portfolios, and integrated supply chains to maintain their edge. In contrast, AI-native firms focus on model performance, proprietary datasets, and swift design workflows, creating a dual-layered market where incumbents emphasize product depth, and startups pursue computational advantages and faster iterations.

Strategic paths are diversifying. In 2025, Benchling expanded its molecular design capabilities through acquisitions, enhancing AI features within its R&D platform. Profluent demonstrated a distinct approach by showcasing generative biology advancements that significantly improved editing system specificity. Similarly, Metagenomi reported breakthroughs in large-gene integration using compact CRISPR-associated transposase systems, achieving over 50-fold efficiency improvements compared to natural baselines. These developments highlight the shift from merely selling tools to mastering data loops, accelerating design, and validating biological performance.

Companies in the market adopt varied approaches to validation and commercialization. AI-centric vendors excel in software development but often rely on manufacturing or regulatory partners for clinical-grade deployment. This creates opportunities for hybrid models, combining computational expertise with established reagent or therapy developers. Key growth areas include on-premises AI inference for regulated biomanufacturing, CRISPR diagnostics, and large-gene integration workflows. The market remains competitive, with companies that integrate model capabilities, proprietary data, and seamless workflows best positioned to lead.

AI CRISPR Tools Industry Leaders

Synthego Corporation

Mammoth Biosciences

ArsenalBio

Integrated DNA Technologies / IDT

Metagenomi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: PerturbAI, emerging from stealth mode, introduced the world's largest in vivo CRISPR atlas with 8 million brain-wide cells. Developed with NVIDIA, Allen Institute for Brain Science, and 10x Genomics, this atlas supports causal AI models for drug discovery targeting complex metabolic and chronic diseases.

- February 2026: Profluent Bio's Protein2PAM, featured in Nature Biotechnology, presented an AI model trained on 45,816 Cas protein PAM pairs. It engineered Nme1Cas9 variants with up to 50-fold higher cleavage kinetics and expanded PAM recognition, enabling advancements in personalized genome editing with an open-source webserver and Python API.

- October 2025: Benchling AI launched as the first AI command center for scientific workflows, integrating deep research agents, automated data entry, and predictive model connectors. The company partnered with Anthropic to embed Claude AI into lab workflows via Amazon Bedrock, enabling natural-language querying of experimental data.

Global AI CRISPR Tools Market Report Scope

As per the scope of the report, AI CRISPR tools are artificial intelligence and machine learning applications that streamline, optimize, and expand the capabilities of CRISPR gene-editing technology. By analyzing massive genomic datasets, these tools predict editing outcomes, design highly precise guide RNAs (gRNAs), and discover entirely new gene-editing enzymes.

The AI CRISPR tools market is segmented by offering, CRISPR technology, application, deployment model, end-user, and geography. By offering, the market includes software, hardware, and services. By CRISPR technology, the market is segmented into CRISPR-Cas9, CRISPR-Cas12 (Cpf1 / Cas12a), CRISPR-Cas13, base editing systems (CBE and ABE), prime editing systems, and other CRISPR systems (CRISPRi/CRISPRa, epigenome editing, and novel AI-designed variants). By application, the market is categorized into drug discovery and development, therapeutic development, functional genomics and target identification, CRISPR-based diagnostics (rapid detection tools), and other applications. By deployment model, the market is segmented into cloud-based, hybrid, and on-premises. By end-user, the market is segmented into pharmaceutical and biotechnology companies, academic and government research institutes, contract research organizations (CROs) and CDMOs, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Hardware |

| Services |

| CRISPR-Cas9 |

| CRISPR-Cas12 (Cpf1 / Cas12a) |

| CRISPR-Cas13 |

| Base Editing Systems (CBE and ABE) |

| Prime Editing Systems |

| Other CRISPR Systems (CRISPRi/CRISPRa, Epigenome Editing, Novel AI-Designed Variants) |

| Drug Discovery and Development |

| Therapeutic Development |

| Functional Genomics and Target Identification |

| CRISPR-Based Diagnostics (Rapid Detection Tools) |

| Other |

| Cloud-based |

| Hybrid |

| On-Premises |

| Pharmaceutical and Biotechnology Companies |

| Academic and Government Research Institutes |

| Contract Research Organizations (CROs) and CDMOs |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Hardware | ||

| Services | ||

| By CRISPR Technology | CRISPR-Cas9 | |

| CRISPR-Cas12 (Cpf1 / Cas12a) | ||

| CRISPR-Cas13 | ||

| Base Editing Systems (CBE and ABE) | ||

| Prime Editing Systems | ||

| Other CRISPR Systems (CRISPRi/CRISPRa, Epigenome Editing, Novel AI-Designed Variants) | ||

| By Application | Drug Discovery and Development | |

| Therapeutic Development | ||

| Functional Genomics and Target Identification | ||

| CRISPR-Based Diagnostics (Rapid Detection Tools) | ||

| Other | ||

| By Deployment Model | Cloud-based | |

| Hybrid | ||

| On-Premises | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Academic and Government Research Institutes | ||

| Contract Research Organizations (CROs) and CDMOs | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for AI in CRISPR tools?

The AI in CRISPR tools market is projected to reach USD 2.76 billion by 2031, rising from USD 0.96 billion in 2026 at a 23.5% CAGR.

Which offering leads revenue generation in this space?

Software led with 56.2% share in 2025 because design, analytics, workflow automation, and data management are becoming core parts of genome editing programs.

Which CRISPR technology is growing the fastest?

CRISPR-Cas12 is forecast to grow at a 25.76% CAGR through 2031, while CRISPR-Cas9 remained the largest technology segment in 2025 with 37.8% share.

Why is therapeutic development still the largest application area?

Therapeutic Development held 52.72% share in 2025 because cell and gene therapy programs require repeated support for guide optimization, off-target modeling, and manufacturing readiness.

Why is on-premises deployment gaining traction if cloud still leads?

Cloud led with 40.95% share in 2025 because it is easier to deploy and update, but On-Premises is growing faster at 26.8% CAGR as regulated users need local control over sensitive genomic data.

Which region offers the strongest growth potential through 2031?

Asia-Pacific is the fastest-growing region with a 27.25% CAGR through 2031, while North America remained the largest regional market with 42.30% share in 2025.

Page last updated on: