AI In Molecule Design Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 6.37 Billion |

| Growth Rate (2026 - 2031) | 25.52% CAGR |

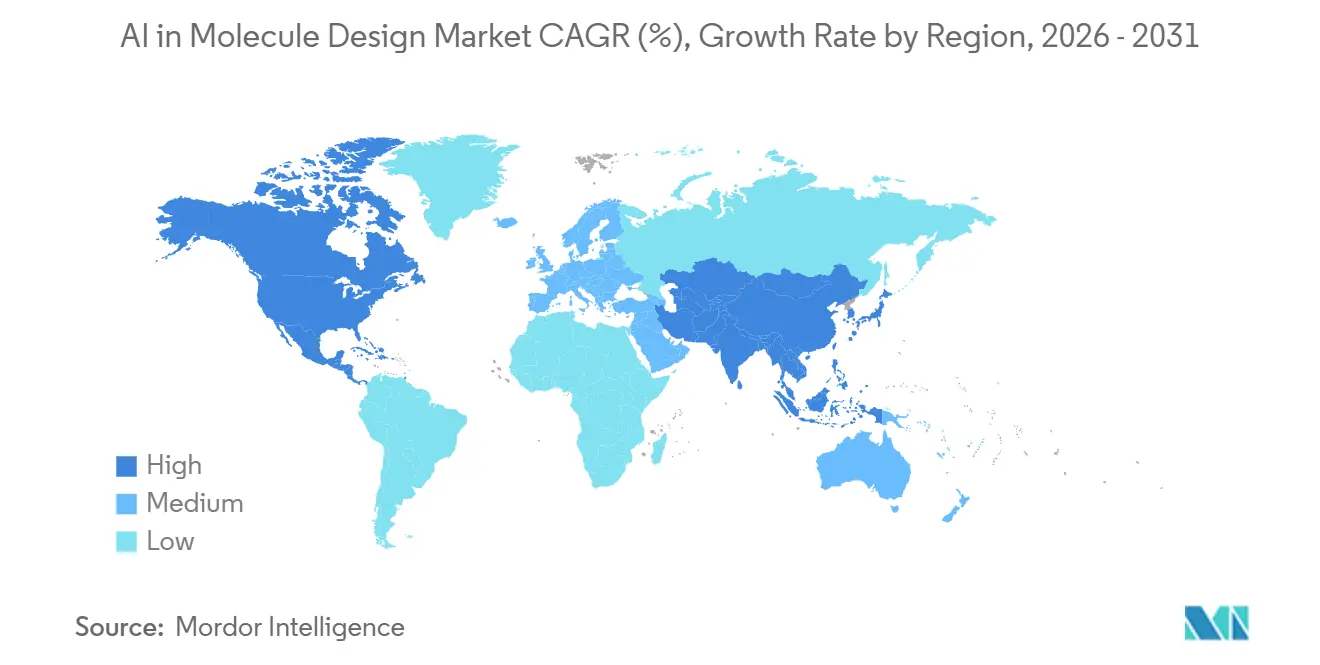

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Molecule Design Market Analysis by Mordor Intelligence

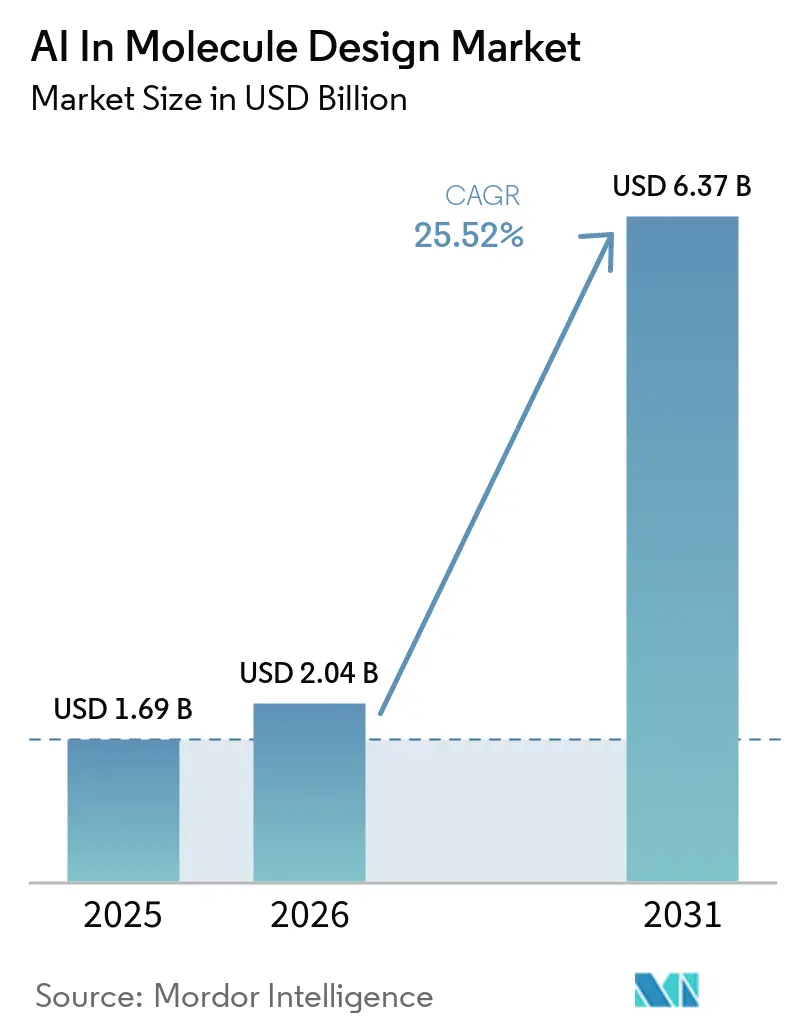

The AI in molecule design market size was USD 1.69 billion in 2025 and is forecast to reach USD 6.37 billion by 2031 at a 25.52% CAGR, reflecting a multi-year transition from pilots to embedded discovery workflows across pharma pipelines. Capital commitments and platform adoption are accelerating as foundation models like AlphaFold 3 and cloud-scale microservices make structure prediction and generative chemistry accessible to large and mid-size R&D teams, reducing barriers to experimentation and iteration in the design-make-test-analyze loop. Early adopters are compressing screening and optimization cycles through autonomous and semi-autonomous lab integration that links model inference to robotic synthesis and high-throughput analytics, which raises throughput and improves data fidelity for successive cycles. Structural biology advances are widening the addressable scope for AI, with AlphaFold-scale resources enabling structure-guided design across proteins, nucleic acids, and protein-ligand complexes, while benchmarking continues to clarify where hybrid physics-AI workflows are needed for accuracy in flexible or ternary complex systems. Competitive focus is shifting toward data moats and lab-in-the-loop execution, as companies formalize wet-lab validation pipelines and proprietary datasets that reinforce platform differentiation and increase the yield of de novo design across small molecules, proteins, and RNA modalities.

Key Report Takeaways

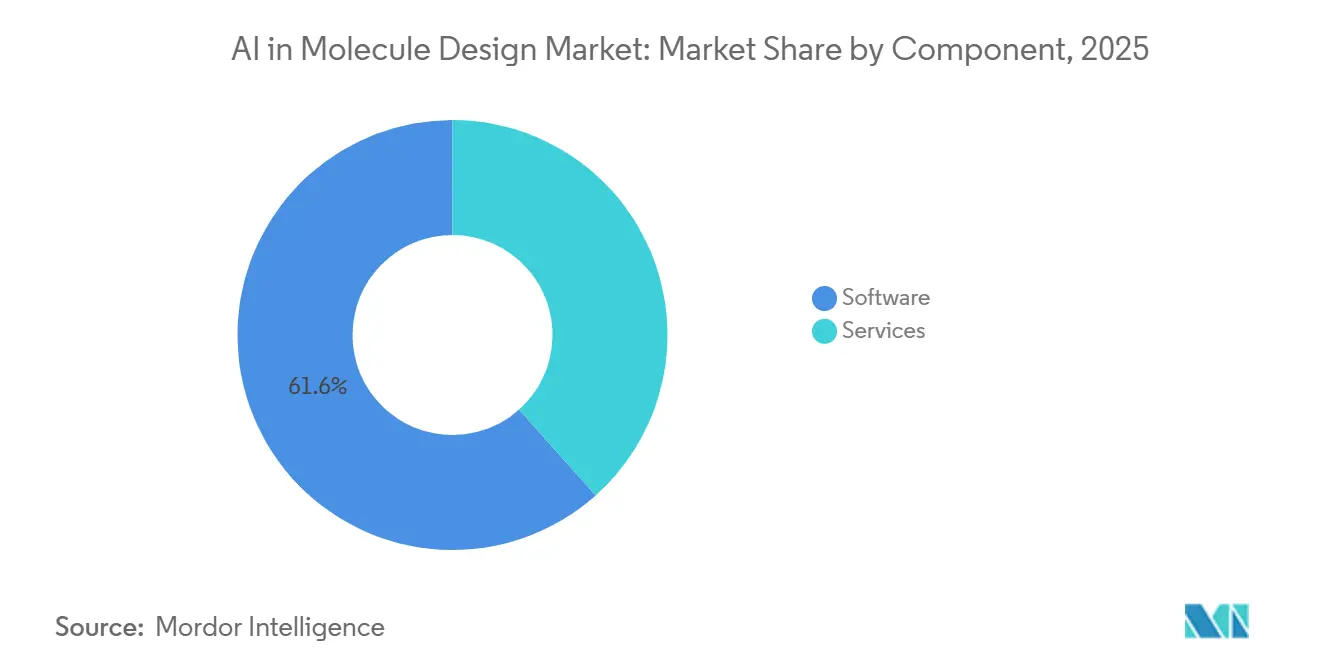

- By component, software led with 61.56% share in 2025 while services recorded the fastest projected growth at a 26.14% CAGR through 2031.

- By application, small-molecule drug design accounted for 55.32% share in 2025 and biologics or protein design is forecast to expand at a 27.10% CAGR to 2031.

- By molecule type, small molecules held 54.34% in 2025 and proteins or biologics posted the highest projected growth at 27.32% CAGR.

- By technology, generative models captured 48.27% deployment in 2025 while structure-based deep learning is projected to grow at a 27.06% CAGR.

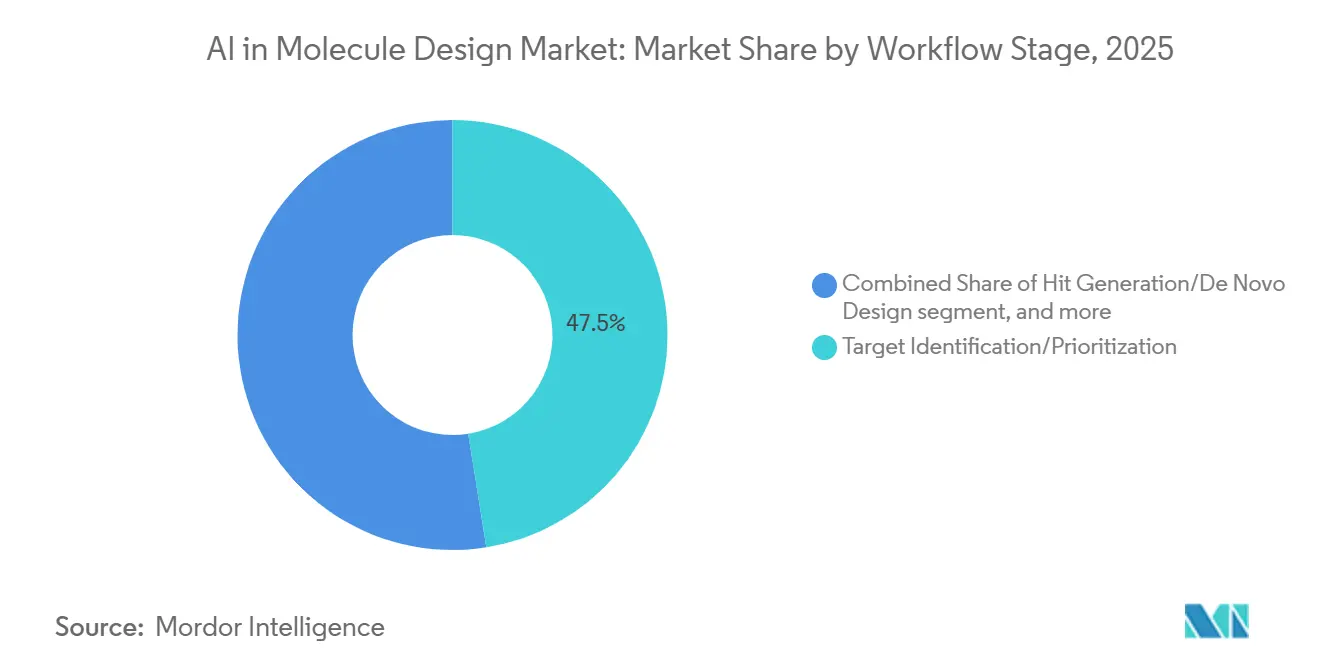

- By workflow stage, target identification accounted for 47.48% of deployments in 2025 and hit generation or de novo design is advancing at a 26.76% CAGR.

- By end user, pharmaceutical and biotechnology companies represented 65.42% in 2025 while CROs and CDMOs are set to grow at a 27.24% CAGR.

- By geography, North America held 44.54% in 2025 and Asia-Pacific is projected to expand at a 26.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Molecule Design Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharma R&D Productivity Pressure and Cost/Time Reduction Imperative | +6.8% | Global, concentrated in US and EU pharma hubs | Short term (≤ 2 years) |

| Foundation Models and Cloud-Scale Compute Enabling Generative Design at Scale | +5.4% | Global with infrastructure advantages in US and APAC | Medium term (2-4 years) |

| AlphaFold-Era Structure Data Unlocking Structure-Guided and Cofolding Design | +4.2% | Global, leveraging AlphaFold resources worldwide | Medium term (2-4 years) |

| Capital Flows and Big-Pharma Partnerships Validating AI Design Pipelines | +3.9% | North America and EU primarily; spillover to APAC via regional partnerships | Short term (≤ 2 years) |

| Closed-Loop, Lab Automation Integrated DMTA Cycles Shortening Iteration Time | +3.1% | North America and APAC core; early gains in EU clusters | Long term (≥ 4 years) |

| Regulatory Engagement De-Risking AI Use Across Discovery and Development | +2.1% | US and EU leadership with APAC following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pharma R&D Productivity Pressure and Cost/Time Reduction Imperative

Drug development timelines and success rates remain under pressure, reinforcing the need to compress discovery cycles and improve candidate quality before clinical investment escalates. Clinical success rates below 8% continue to constrain ROI, so discovery functions seek tools that boost target confidence and multi-parameter optimize leads earlier in the funnel. AI-driven design pipelines support faster hypothesis testing across potency, selectivity, and ADMET properties, which narrows attrition and reduces redundant synthesis of low-value analogs when paired with high-fidelity feedback data. The widespread availability of scalable foundation models and physics refinement workflows lowers unit costs for in silico screening and prioritization, leading to higher throughput and better allocation of wet-lab resources. As more precompetitive structural and sequence data enter public repositories, and as closed-loop labs collect higher quality proprietary measurements, model performance improves through continual fine-tuning that reflects real-world assay conditions.

Foundation Models and Cloud-Scale Compute Enabling Generative Design at Scale

AlphaFold 3 and related tools extend predictive capability across proteins, DNA, RNA, and ligands, which allows computational exploration of binding modes and conformations that historically depended on slower structural biology methods.[1]Chaim Gartenberg, “How We Built AlphaFold 3 to Predict the Structure and Interaction of All of Life’s Molecules,” The Keyword, blog.google Cloud-delivered microservices such as NVIDIA BioNeMo bring diffusion docking, protein folding, and molecular generation into standardized APIs, which encourages consistent, scalable deployment patterns across discovery portfolios. Companies report material speedups and broader target coverage as pre-trained model suites mature, and ongoing hardware optimization sustains throughput improvements without large on-premises capital outlays. IBM’s large-scale generative work illustrates the gains from training on billion-scale SMILES corpora, with improved novelty and diversity that expands explored chemical regions for virtual screening. Foundation models that learn latent chemical and structural rules generate candidates that extend beyond over-sampled scaffolds, which helps discovery teams locate viable first-in-class leads when combined with property filters and synthesis-aware scoring. Vendor ecosystems are coalescing around interoperable services that integrate protein prediction, docking, generation, and ADMET to enable end-to-end workflows with common data contracts and versioning.

AlphaFold-Era Structure Data Unlocking Structure-Guided and Cofolding Design

The scale and quality of predicted structures have shifted structure-based design from niche to mainstream, since researchers can explore interactions across targets without waiting for experimental structure determination. AlphaFold 3 added capacity for protein-ligand complexes, which supports virtual screening and rational design of binding-site interactions while guiding prioritization with predicted conformations. Benchmarking indicates strong performance for static interactions and highlights the need for hybrid workflows when binding induces larger conformational changes or when modeling ternary complexes, which points teams to physics-based refinement for affinity ranking and stability. Model developers are rapidly iterating with synthetic data from physics engines to improve complex prediction, which reduces error in flexible regions and membrane-associated targets as more training examples capture diverse biophysical scenarios. Continuous use of centralized servers for structure generation has removed bottlenecks for early discovery so that multiple target hypotheses can be progressed in parallel with consistent structural inputs. As organizations standardize on cofolding, induced fit, and ensemble modeling strategies, structure data now informs both hit generation and lead optimization stages across small molecules and biologics.

Closed-Loop, Lab Automation Integrated DMTA Cycles Shortening Iteration Time

Connecting design engines to robotic synthesis and rapid assay readouts turns the design-make-test-analyze cycle into a continuous loop, which cuts weeks or months from each iteration and expands the number of evaluable hypotheses per unit time. Autonomous and semi-autonomous systems have demonstrated faster optimization across potency and efficiency metrics in live projects, with high-throughput synthesis and analytics providing datasets that strengthen model retraining. In protein engineering, autonomous experimentation has delivered measurable gains in cost and speed, illustrating how lab-in-the-loop pipelines scale when model inference directs experimentation rather than relying on manual batching.[3]NVIDIA Corporation, “Expanding Computer-Aided Drug Discovery With New AI Models,” NVIDIA Blog, blogs.nvidia.com Digital twins and standardized data objects further reduce manual curation and enable near real-time hypothesis testing across synthesis and process parameters. Hardware vendors are addressing throughput caps with modular, scalable workcells that integrate with simulation for predictive maintenance and scheduling, which increases uptime for continuous cycles. The combined impact is a more productive and data-rich loop that feeds back into model performance and improves the overall efficiency profile of the AI in molecule design market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Quality, Bias, and Lack of Standards Limiting Model Generalization | -2.8% | Global, acute in regions with fragmented data infrastructure | Medium term (2-4 years) |

| High Implementation Costs and Talent Constraints for Scaling Programs | -2.3% | APAC and emerging EU markets face steeper talent deficits; US has stronger AI talent pools | Long term (≥ 4 years) |

| Synthesizability Gap Between AI Proposals and Executable Routes | -1.7% | Global, severity inversely correlated to medicinal chemistry infrastructure | Medium term (2-4 years) |

| Compute or GPU Supply and Energy Bottlenecks Constraining Training | -1.4% | National, where hyperscale access or local GPU supply is limited | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Quality, Bias, and Lack of Standards Limiting Model Generalization

Training data remain sparse relative to the vast chemical space, and errors or inconsistent protocols in public datasets introduce noise that can bias model learning and hurt external validity. Benchmark reviews show non-trivial label error rates across molecular property datasets, which can induce spurious correlations and reduce accuracy in prospective prediction settings. Heterogeneous assay conditions further complicate learning because models trained on aggregated sources may conflate measurements across cell-free, cellular, or in vivo contexts without adequate metadata to normalize differences. Demographic imbalance in clinical evidence raises generalizability risks for safety and exposure predictions, since underrepresented genetic backgrounds can experience adverse effects that are poorly captured by models trained on narrower populations. Activity cliffs and context-sensitive bioassay results add complexity, and the lack of standardized reporting rules for protocols and uncertainty makes it harder to compare or reuse datasets across programs. Organizations are addressing these gaps by generating proprietary experimental data at scale and by enriching metadata to improve model reliability, which supports better domain transfer within the AI in molecule design market.

Synthesizability Gap Between AI Proposals and Executable Routes

Generative models can output high-scoring molecules that are difficult to make, because many training sets lack explicit synthesis annotations and retrosynthetic constraints during generation. Studies that combine automated medicinal chemistry quality filters with docking and retrosynthesis show that only a small fraction of generated candidates pass all gates, underscoring the need to inject synthesis-aware objectives earlier in design. Incorporating retrosynthesis planners into tight optimization loops improves tractability but adds computational overhead that erodes the speed benefits of de novo generation at large scales. New frameworks that learn from retrosynthetic paths or fragment assembly are emerging to balance novelty with route feasibility, although extensive wet-lab validation remains limited compared to in silico metrics. Reward engineering and synthesis-guided fragment policies can reduce the gap by penalizing inaccessible motifs, while maintaining design diversity for SAR exploration. As retrosynthetic services and reagent-aware libraries integrate with generation stacks, design cycles are improving yield from in silico proposals to bench-tested candidates in the AI in molecule design market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates, Services Accelerate as Integration Deepens

Software held 61.56% of the AI in molecule design market in 2025, supported by cloud-based access to folding, docking, and generative models that allow teams to scale without major on-premises investments. Platform microservices such as BioNeMo expose models for docking, structure prediction, and molecule generation via standard APIs, which concentrates value in software workflows that can be orchestrated across multiple discovery programs. Major toolchains in physics-based refinement continue to update features for scale, including improvements in free energy calculations and categorical assay handling that align with discovery team workflows. The result is broader software penetration into the AI in molecule design market for routine steps such as hit expansion and early ADMET filtering, which are now accessible to cross-functional users through unified interfaces.

Services are the faster-growing component at a projected 26.14% CAGR, driven by end-to-end DMTA execution that links sequence or molecular design with in-house synthesis and characterization. RNA-focused providers illustrate this shift with integrated offerings spanning AI-assisted design, scalable manufacturing, and deep sequencing that validate expression and function within one cycle. Services-led models compress timeline and reduce coordination friction across vendors, while structured data capture supports continuous model retraining for the next iteration. As discovery organizations scale programs and standardize operating procedures, the service layer becomes a key execution partner that handles lab automation, assay throughput, and documentation to support quality and compliance needs for the AI in molecule design market.

By Application: Small-Molecule Dominance Gives Way to Biologics and Protein Design Surge

Small-molecule drug design accounted for 55.32% of applications in 2025, reflecting established pathways for virtual screening, physics-based refinement, and lead optimization that remain central to early discovery. Generative and physics engines are widely used in tandem to balance novelty with binding affinity prediction, which creates an efficient filter for prioritizing candidates before synthesis. The small-molecule stack is now more interoperable across targets and properties, with shared data formats enabling ensemble approaches that interleave docking, generation, and ADMET to drive early triage at scale in the AI in molecule design market. This tooling density keeps small molecules as a workhorse modality even as new classes attract investment and attention.

Biologics or protein design is the fastest-growing application at a projected 27.10% CAGR, supported by advances in structure prediction, inverse folding, and sequence optimization that reduce the need for exhaustive library screening. AI-first developers have reported clinical progress on antibody programs designed with sequence and structure-aware LLMs, providing external evidence that design-first workflows can generate candidates suitable for development. RNA and mRNA sequence design platforms are now integrating AI-driven optimization with scalable synthesis and analytics, which shortens the path from in silico proposals to validated expression constructs. As lab-in-the-loop validation becomes routine, biologics programs leverage design cycles that improve developability and potency in fewer iterations, reshaping application mix within the AI in molecule design market.

By Molecule Type: Proteins and Biologics Sprint Ahead as Foundation Models Mature

Small molecules represented 54.34% of the AI in molecule design market in 2025, supported by the availability of large virtual libraries and scalable screening strategies that run on standard cloud infrastructure. Structure-informed retrieval and screening frameworks have delivered orders-of-magnitude speedups, expanding the feasible search space per target and improving hit rates when coupled with property filters. This foundation maintains strong throughput for medicinal chemistry pipelines, which still benefit from standard ADMET models and clinical familiarity.

Proteins and biologics have the fastest projected growth at 27.32% CAGR, driven by better sequence-structure modeling, developability prediction, and autonomous experimentation that raises the yield of functional designs. RNA-centric modalities are also gaining traction through lab-in-the-loop platforms that optimize coding and non-coding features to improve expression and durability, which expands the practical design space for therapeutic applications. Clinical progress in gene editing and cell therapy supports continued investment in sequence-level design engines that integrate with validation workflows and quality analytics. As toolchains mature, the molecule-type mix tilts toward programs that are most sensitive to structure and sequence learning gains, accelerating share shifts within the AI in molecule design market.

By Technology: Generative Models Lead, Structure-Based Deep Learning Gains Momentum

Generative models accounted for 48.27% of technology deployment in 2025, reflecting their utility in proposing diverse, property-aware candidates for downstream filtering and optimization. Diffusion and transformer-based generators are displacing legacy methods for de novo design due to training stability and sample quality, while integration with ADMET and docking raises decision confidence for synthesis selections. Foundation model updates continue to expand target coverage and modality scope, enabling broader application across small molecules and proximity-based therapeutics in the AI in molecule design market.

Structure-based deep learning is the fastest-growing technology at a projected 27.06% CAGR, anchored by improvements in complex prediction and conformational modeling that support structure-guided design. Model builders are combining physics-generated synthetic data with learned representations to close accuracy gaps in flexible systems, which raises the utility of predicted structures for design and prioritization. Toolchains that integrate retrosynthesis and route feasibility into scoring functions further refine the candidate set, improving the handoff from in silico design to bench. This stack complements generative approaches and supports end-to-end workflows that connect targets, structures, generation, and synthesis awareness in the AI in molecule design market.

By Workflow Stage: Target Identification Dominates, Hit Generation Accelerates

Target identification or prioritization represented 47.48% of deployments in 2025, since selecting high-confidence targets is the most leveraged decision point for downstream discovery and development. Multimodal data integration and predictive modeling elevate target hypothesis strength and allow teams to align effort with the most promising biology, which reduces late-stage attrition. Structure and sequence resources now enable faster triage of target classes and binding site feasibility, which creates a clearer path for downstream hit generation in the AI in molecule design market.

Hit generation or de novo design is the fastest-growing step with a projected 26.76% CAGR, fueled by model ensembles that propose large batches of chemically diverse candidates conditioned on potency and developability properties. When integrated with closed-loop labs, this stage produces immediate feedback that sharpens subsequent generations and reduces time to qualified hits. Lead optimization then benefits from physics-based refinement and calibrated free energy predictions, which support smaller, more targeted syntheses for SAR expansion. End-to-end workflows increasingly bundle ADMET, retrosynthesis, and structure prediction microservices so discovery teams can operate continuous cycles within standardized data pipelines in the AI in molecule design market.

By End User: Pharma or Biotech Leads, CROs or CDMOs Surge as Outsourcing Accelerates

Pharmaceutical and biotechnology companies held 65.42% in 2025, reflecting the concentration of discovery budgets and the strategic need to replenish pipelines as modality mix evolves. Discovery teams within large organizations deploy standardized AI stacks across targets and modalities to align computational design with lab capacity, which improves throughput and data quality for iterative cycles in the AI in molecule design market.

CROs and CDMOs are the fastest-growing end users at a projected 27.24% CAGR, as sponsor companies shift work to partners capable of running AI-augmented chemistry and biology with integrated lab automation. Providers that bundle design engines with synthesis and analytics reduce sponsor overhead and accelerate cycles, while standardized documentation supports tech transfer and regulatory readiness. The effect is a more scalable services ecosystem that broadens access to advanced workflows within the AI in molecule design market.

Geography Analysis

North America accounted for 44.54% of the AI in molecule design market in 2025, supported by a critical mass of discovery budgets, computational talent, and lab infrastructure that integrates AI with automated experimentation. The region has active deployment of foundation model microservices and physics toolchains, enabling faster screening and prioritization across targets and modalities. Vendor ecosystems spanning GPU-accelerated cloud platforms and model hubs have increased access to high-performing tools, which supports large-scale experimentation across therapeutic areas in the AI in molecule design market.

Asia-Pacific is the fastest-growing region with a projected 26.57% CAGR through 2031, anchored by government-backed initiatives and academic-industry platforms that expand access to target analysis, generative design, and evaluation tools. China launched a full-process AI platform that offers free access for target analysis, molecule generation, and ADMET optimization, which lowers barriers for academic labs and startups. Tsinghua-linked programs reported million-fold speedups in virtual screening and opened large protein-ligand databases for the community, which expand the searchable space for discovery projects in the AI in molecule design market. Japan’s METI and NEDO supported work on large-scale foundation models for drug design, signaling public sector commitment to scale up AI-first discovery.

Europe benefits from coordinated public funding and a dense network of pharma, biotech, and academic centers that connect discovery modeling with translational infrastructure. National programs have introduced targeted funding to accelerate AI-enabled drug discovery, with strong infrastructure in countries that host major pharma and research institutions. Across the region, the AI in molecule design market expands as stakeholders connect foundation models, lab automation, and process analytics to support discovery and early development across multiple modalities.

Competitive Landscape

Competition in the AI in molecule design market is moderately fragmented across technology stacks, therapeutic modalities, and go-to-market models, with differentiation shifting toward data assets and lab-in-the-loop execution that improve design yield over time. Consolidation is reshaping capabilities through combinations of generative chemistry, phenomics, and target identification under one roof, which supports scaled discovery across portfolios. Data moats are central as companies invest in proprietary, high-quality datasets and automation that create feedback loops for improved model performance in the AI in molecule design market.

Ecosystem leaders are also standardizing model access through cloud microservices, which creates network effects as more users contribute to tuning and evaluation. RNA and protein engineering platforms are emerging as high-growth niches, reinforced by investor interest and lab-in-the-loop capabilities that connect design to synthesis and analytics in one environment. Companies are also emphasizing explainability and provenance to support sponsor requirements for internal governance and regulatory-ready documentation, which aligns technology differentiation with operational needs in discovery and development.

Select strategic moves illustrate the competitive arc of the AI in molecule design market as it scales. A high-profile biotech combination integrated large proprietary datasets and multi-modality discovery engines under one corporate structure to accelerate industrialized discovery. Foundation-model access hubs secured broad adoption across over one hundred companies, confirming the central role of standardized APIs and GPU cloud for molecular generation, docking, and folding at scale. Autonomous experimentation benchmarks in protein engineering demonstrated cost and speed gains from AI-directed lab workflows, validating the integration of model inference with automated laboratory systems in commercial settings.

AI In Molecule Design Industry Leaders

Schrödinger

Exscientia

Insilico Medicine

Recursion

XtalPi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Isomorphic Labs, the DeepMind spinout, is advancing AI-driven molecule design into a new phase by preparing its first human clinical trials of AI-designed drug candidates. Using its AI systems built on AlphaFold and generative models, the company designs and optimizes novel molecules for diseases such as cancer and immune disorders. After securing major pharma partnerships and funding, it is now transitioning from in-silico molecule generation to real-world validation, with human trials expected around 2026. This marks a key milestone where AI-designed molecules move from computational discovery to clinical testing in humans.

- March 2026: Roche launched an AI “factory” for drug development in collaboration with NVIDIA to scale AI-driven molecule design and drug discovery. The system uses large-scale GPU infrastructure to run generative AI models that help design new drug molecules, identify targets, and simulate biological behavior more efficiently. It integrates these capabilities across Roche’s R&D and manufacturing pipeline, enabling a more automated and data-driven approach to developing medicines.

- March 2026: Eli Lilly entered a USD 2.75 billion agreement with Insilico Medicine to advance AI-driven molecule design for drug discovery. The collaboration focused on using generative AI to create and optimize novel drug molecules, which Lilly develops into potential therapies, particularly in areas like oncology and metabolic diseases. This deal highlights growing pharma confidence in AI-designed molecules as viable preclinical drug candidates.

Global AI In Molecule Design Market Report Scope

As per the scope of the report, AI in molecule design refers to the use of machine‑learning and generative models to predict, create, and optimize molecular structures by learning from large chemical datasets, enabling faster exploration of chemical space and accelerating the design‑make‑test cycle. It supports tasks such as property prediction, de novo molecule generation, and automated optimization, helping scientists design novel drug candidates and materials more efficiently.

The AI in molecule design market is segmented into component, application, molecule type, technology, workflow stage, end user, and geography. By component, the market is segmented into software and services. By application, the market is segmented into small-molecule drug design, biologics/protein design, materials and specialty chemicals design, and agrochemicals design. By molecule type, the market is segmented into small molecules, peptides, proteins/biologics, RNA/oligonucleotides, and materials molecules/polymers. By technology, the market is segmented into generative models, structure-based deep learning, property prediction/ADMET ML, and synthesis planning and retrosynthesis AI. By workflow stage, the market is segmented into Target identification/prioritization, hit generation/de novo design, hit-to-lead, and lead optimization, and others. By end user, the market is segmented into pharmaceutical and biotechnology companies, CROs and CDMOs, chemicals and materials manufacturers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Small-Molecule Drug Design |

| Biologics/Protein Design |

| Materials and Specialty Chemicals Design |

| Agrochemicals Design |

| Small Molecules |

| Peptides |

| Proteins/Biologics |

| RNA/Oligonucleotides |

| Materials Molecules/Polymers |

| Generative Models |

| Structure-Based Deep Learning |

| Property Prediction/ADMET ML |

| Synthesis Planning and Retrosynthesis AI |

| Target Identification/Prioritization |

| Hit Generation/De Novo Design |

| Hit-To-Lead |

| Lead Optimization |

| Others |

| Pharmaceutical and Biotechnology Companies |

| CROs and CDMOs |

| Chemicals and Materials Manufacturers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Application | Small-Molecule Drug Design | |

| Biologics/Protein Design | ||

| Materials and Specialty Chemicals Design | ||

| Agrochemicals Design | ||

| By Molecule Type | Small Molecules | |

| Peptides | ||

| Proteins/Biologics | ||

| RNA/Oligonucleotides | ||

| Materials Molecules/Polymers | ||

| By Technology | Generative Models | |

| Structure-Based Deep Learning | ||

| Property Prediction/ADMET ML | ||

| Synthesis Planning and Retrosynthesis AI | ||

| By Workflow Stage | Target Identification/Prioritization | |

| Hit Generation/De Novo Design | ||

| Hit-To-Lead | ||

| Lead Optimization | ||

| Others | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| CROs and CDMOs | ||

| Chemicals and Materials Manufacturers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the AI in molecule design market?

The AI in molecule design market size was USD 1.69 billion in 2025 and is projected to reach USD 6.37 billion by 2031 at a 25.52% CAGR, signaling multi-year momentum across discovery workflows.

Which regions will drive the fastest expansion through 2031?

Asia-Pacific is the fastest-growing region with a projected 26.57% CAGR, supported by government-backed platforms and academic-industry programs that expand access to AI-enabled design tools.

Which applications and molecule types are set to grow the most?

Biologics or protein design is the fastest-growing application at a 27.10% CAGR, while proteins or biologics lead molecule-type growth at 27.32% with lab-in-the-loop and structure-aware models improving yield.

What technologies are most widely used today in AI-enabled design?

Generative models lead with 48.27% deployment, and structure-based deep learning is the fastest-growing with a 27.06% CAGR, aided by advances in complex prediction and cloud-delivered microservices.

Page last updated on: