AI In Nutraceutical Formulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

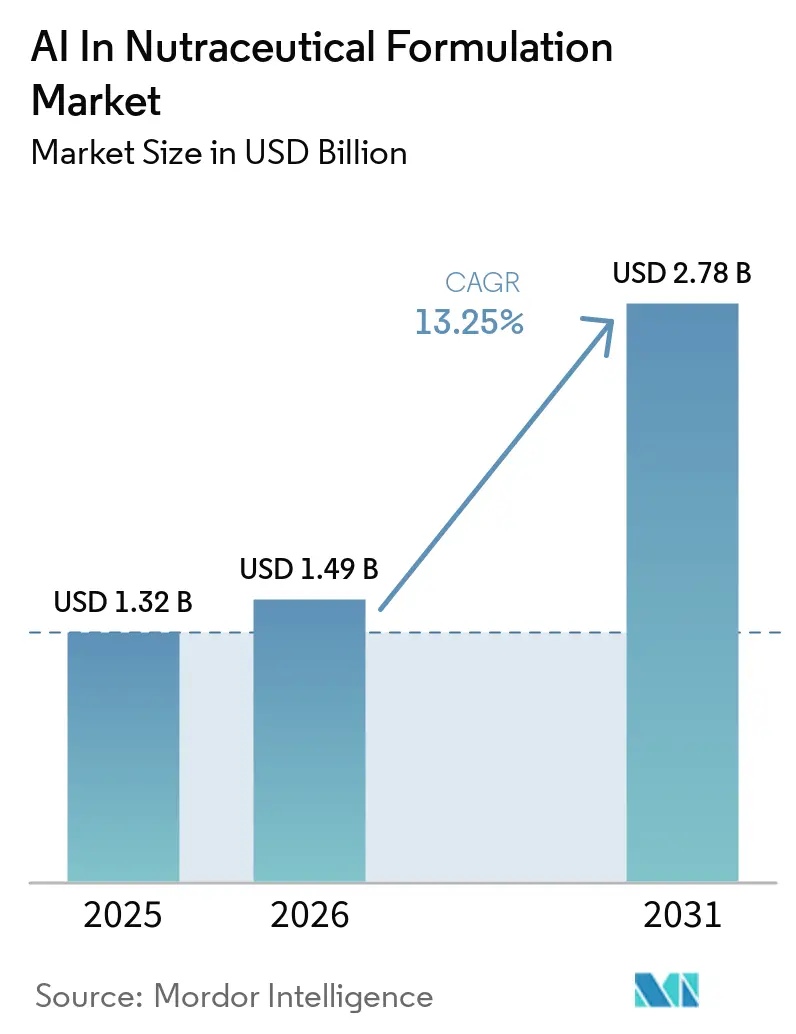

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 13.25% CAGR |

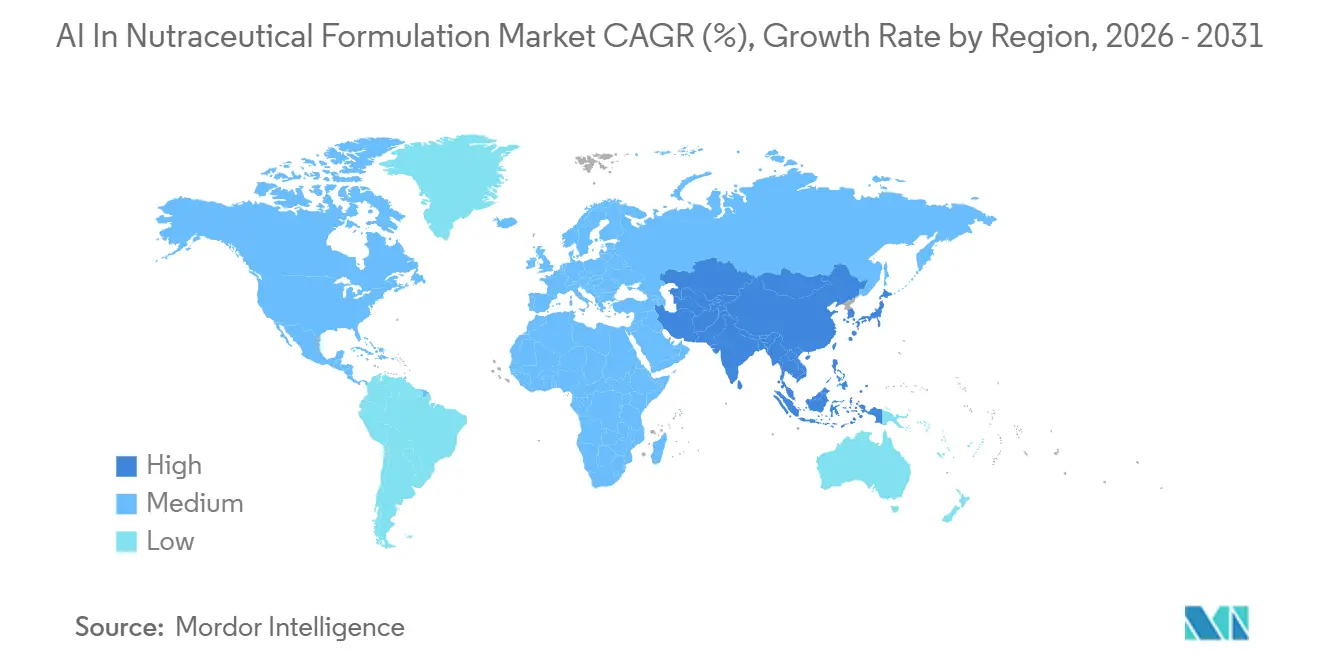

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Nutraceutical Formulation Market Analysis by Mordor Intelligence

The AI In Nutraceutical Formulation Market size is projected to expand from USD 1.32 billion in 2025 and USD 1.49 billion in 2026 to USD 2.78 billion by 2031, registering a CAGR of 13.25% between 2026 to 2031.

Supplement and functional food companies are transitioning from trial-and-error product development to data-driven formulation workflows, driving market growth. Machine learning models, predictive analytics, and generative AI platforms are reducing formulation cycles by 40% to 60%, enabling faster concept testing, claim documentation, and product commercialization. Retrieval-augmented generation systems, trained on extensive ingredient, clinical, and regulatory datasets, are making regulatory-ready formulation design accessible to smaller manufacturers, increasing competition. The AI-driven nutraceutical formulation market is further supported by rising demand for personalized nutrition, biomarker-led recommendation systems, and broader cloud deployment, which integrates data across wearables, laboratories, and formulation databases. However, growth depends on how effectively companies address health-data privacy, regulatory documentation, and fragmented ingredient master data across suppliers and regions.

Key Report Takeaways

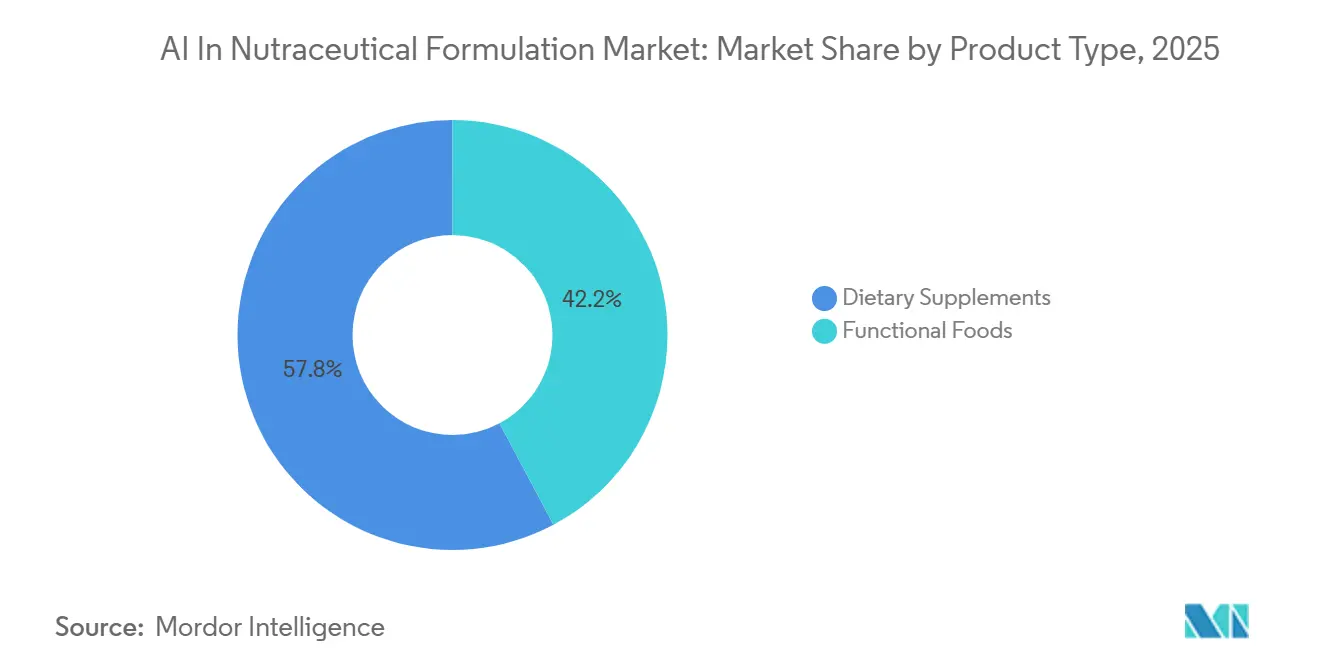

- By product type, dietary supplements held 57.78% of the market in 2025, while functional foods is projected to expand at a 14.24% CAGR from 2026 to 2031.

- By application, product formulation accounted for 31.55% of the market in 2025, while personalized nutrition is projected to record the highest CAGR of 14.76% through 2031.

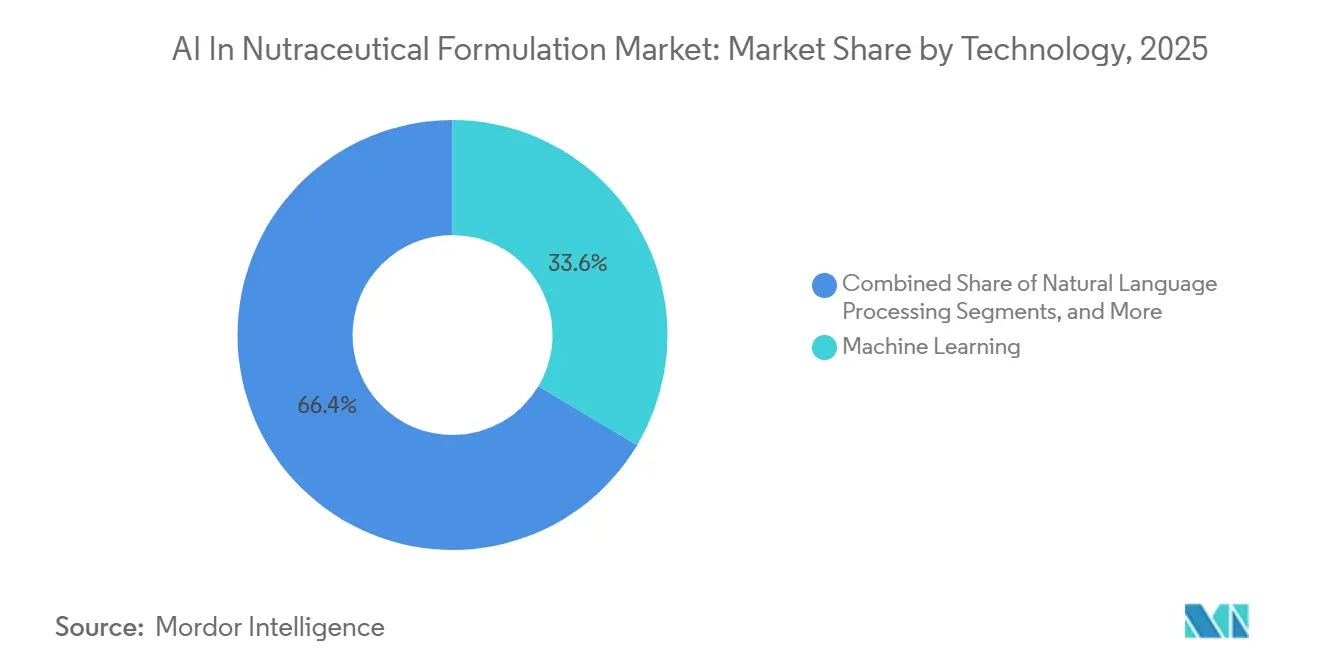

- By technology, machine learning held 33.56% of the market in 2025, while natural language processing is projected to grow at a 14.67% CAGR from 2026 to 2031.

- By deployment mode, cloud-based deployment holds 66.15% of the market in 2026 and is also the fastest-growing mode at a 13.78% CAGR from 2026 to 2031.

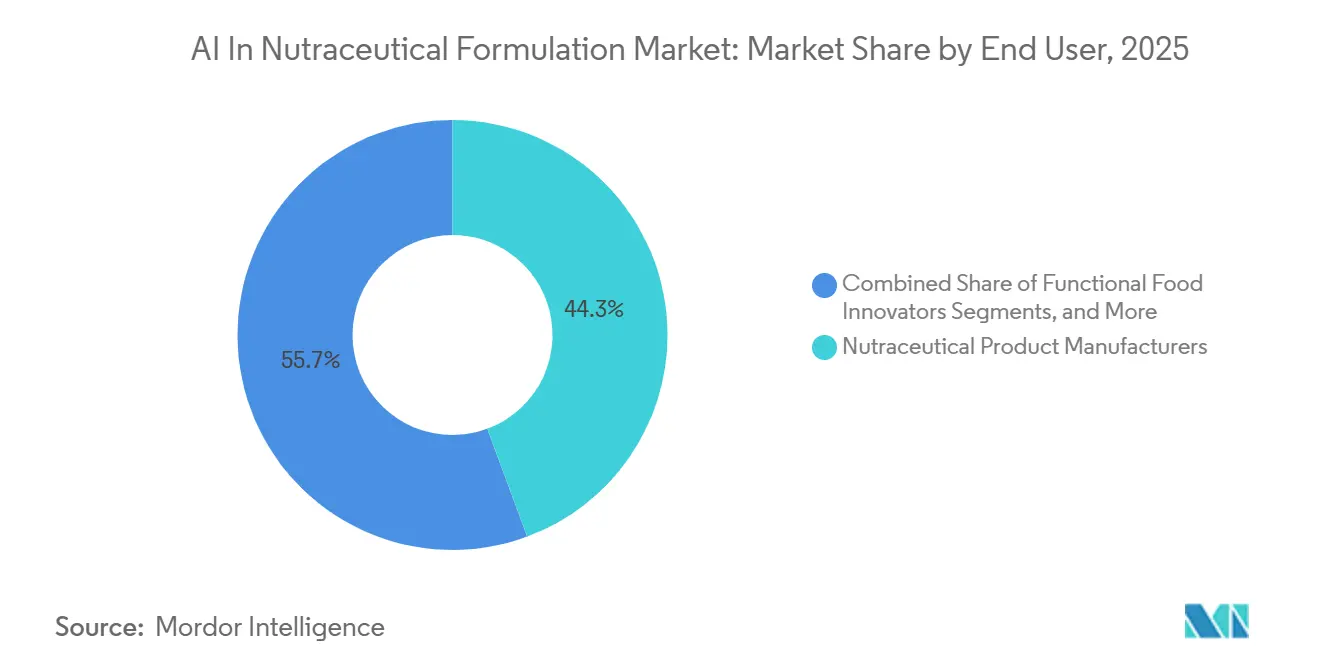

- By end user, nutraceutical product manufacturers captured 44.34% of the market in 2025, while functional food innovators are projected to expand at a 13.88% CAGR through 2031.

- By geography, North America commanded 38.77% of the market in 2025, while Asia-Pacific is projected to record the fastest regional CAGR of 14.45% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Nutraceutical Formulation Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Personalized nutrition and biomarker-led targeting | +3.0% | Global, with early intensity in North America, UK, and South Korea | Medium term (2-4 years) |

| Faster formulation cycles through AI screening | +2.5% | Global, with high adoption in North America and Western Europe | Short term (≤ 2 years) |

| Cloud deployment lowering adoption friction | +2.0% | Global, strongest in Asia-Pacific, with spillover to Middle East and Africa | Short term (≤ 2 years) |

| Aging and metabolic health demand expansion | +2.2% | Japan, Germany, South Korea, North America, China | Long term (≥ 4 years) |

| Digital twin and PBPK simulation for dose design | +1.5% | North America and EU core, emerging in Asia-Pacific | Medium term (2-4 years) |

| Claims-substantiation automation for faster launches | +1.3% | Global, with stronger regulatory influence in EU and Asia-Pacific markets under EFSA and FSSAI frameworks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Personalized Nutrition and Biomarker-Led Targeting Accelerates Product Science

AI is transforming the nutraceutical formulation market by shifting from generic dietary advice to supplements tailored to individual biological profiles. Multi-omics systems integrating genomics, transcriptomics, metabolomics, and microbiome data enable formulation teams to design products based on metabolic variations rather than population averages. Platforms building long-term biomarker histories enhance recommendation accuracy and create a competitive data advantage. Diagnostics and formulation are increasingly linked, with biological testing directly influencing product design and supplement recommendations. Privacy-by-design architecture is becoming critical as companies managing sensitive biological data with clear governance scale personalization effectively.

Faster Formulation Cycles Through AI Screening Compress Time-to-Market

AI platforms are accelerating nutraceutical development by simultaneously screening ingredients, scientific literature, pathway interactions, and regulatory compliance. This approach reduces traditional timelines from 18-24 months to 6-9 months, enabling brands to explore more variants at lower costs. AI also diminishes the advantage of exclusive novel ingredients by repurposing known ones for new health applications with better documentation. Formal support structures are growing, with AI tools mining extensive research archives for formulation insights. Speed is now a critical capability across product design, regulatory compliance, and commercialization.

Aging and Metabolic Health Demand Creates a Durable Structural Tailwind

The nutraceutical formulation market is driven by rising demand for products addressing aging, metabolic dysfunction, cognitive decline, and chronic health issues. The global prevalence of metabolic dysfunction-associated steatotic liver disease highlights the need for multi-target nutraceuticals to tackle complex conditions. Machine learning pipelines are enhancing confidence in selecting and combining bioactive components for such challenges. The market aligns with the demand for intricate design logic, precise dosing, and robust evidence chains. Companies leveraging AI formulation as a growth strategy face increasing competition in areas like metabolic health, muscle maintenance, and healthy aging.

Digital Twin and PBPK Simulation Reduce Costly Physical Prototyping

Digital twins and physiologically based pharmacokinetic modeling are optimizing dose design, delivery systems, and process parameters in the nutraceutical market. These technologies improve productivity, reduce process time, and minimize waste during pilot runs while enhancing confidence before scaling up. Platforms combining PBPK modeling, stability simulations, and regulatory checks test formulations across diverse virtual populations, broadening the scope of in silico designs before clinical trials. Digital simulations offer both scientific rigor and operational efficiency, positioning companies for stronger regulatory discussions with early safety and efficacy modeling.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy and health-data governance complexity | -1.8% | EU under GDPR and the EU AI Act, Asia-Pacific under varying national standards, North America under state-level data laws | Medium term (2-4 years) |

| High implementation and workflow-integration cost | -1.5% | Global, most acute for SMEs in South and Southeast Asia and Latin America | Short term (≤ 2 years) |

| Ingredient master-data fragmentation across suppliers | -0.9% | Global, with particular friction in Asia-Pacific and Middle East and Africa multi-tier supply chains | Long term (≥ 4 years) |

| Cross-country rules for AI-led claims and personalization | -0.8% | EU under EFSA, China under SAMR, India under FSSAI, US under FDA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Health-Data Governance Constraints Limit Biomarker Platform Scale

The biomarker depth that strengthens the AI in the nutraceutical formulation market also creates significant scaling challenges, as personalization depends on managing sensitive health data. The EU AI Act classifies certain health-related AI systems as high-risk, while GDPR enforces strict regulations on processing genetic and biometric data, increasing compliance burdens for multi-omics platforms.[1]Nutrigenomics Meets Multi-Omics, Integrating Genetic, Metabolic, and Microbiome Data for Personalized Nutrition Strategies,” Genes & Nutrition, genesandnutrition.biomedcentral.comThese challenges affect data transfer, model training, auditability, and how recommendations are communicated to users and regulators.

High Implementation and Workflow-Integration Costs Constrain Mid-Market Adoption

Small and mid-sized manufacturers face challenges in adopting AI for nutraceutical formulations due to the complexity of enterprise-grade deployment. Beyond software acquisition, companies must address data migration, system integration, specialized talent needs, and ongoing model updates as ingredient databases and regulations evolve. Many supplements lack strong scientific validation, resulting in incomplete datasets that hinder AI effectiveness. SaaS models are reducing entry barriers by offering pre-validated formulations and mapped supply chains, but integration with proprietary systems and internal processes remains a challenge. Without simplified interoperability and modular implementation, adoption may continue to favor well-capitalized players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dietary Supplements Anchor Volume, Functional Foods Drive Next-Phase Growth

In 2025, Dietary Supplements accounted for 57.78% of the AI-driven nutraceutical formulation market, making it the largest product category by revenue. This segment remains dominant due to high reformulation activity, claim support, and ingredient optimization across vitamins, minerals, botanicals, and specialty supplements.

Functional Foods are projected to grow at a 14.24% CAGR from 2026 to 2031, outpacing dietary supplements in growth despite a smaller base. AI enables supplement-grade design to be applied to consumer food formats like fortified beverages and plant-based dairy alternatives while addressing sensory, stability, and compliance challenges. This shift expands AI applications into complex food formulations, fostering collaboration between food science and nutraceutical R&D teams. Functional foods are increasingly used for rapid innovation in areas like metabolic health and cognitive function.

By Application: Personalized Nutrition AI Platforms Redefine Upstream Demand Signals

In 2025, Product Formulation held the largest application share at 31.55%, reflecting AI's primary role in ingredient selection, compatibility checks, and bioavailability improvement. This application offers measurable operational value and aligns with regulatory requirements for AI-generated evidence. The FDA's 2025 draft guidance emphasizes credibility and traceability, reinforcing Product Formulation's leadership in the market.

Personalized Nutrition is expected to grow at a 14.76% CAGR from 2026 to 2031, making it the fastest-growing application. Platforms now integrate biomarker data, wearable signals, and dietary inputs to provide dynamic recommendations. Research shows that AI-driven personalization improves adherence and physiological outcomes, shifting consumer data from post-production insights to upstream formulation decisions. This feedback loop is blurring the lines between formulation and personalized recommendations.

By Technology: Machine Learning Commands the Market, NLP Poised for Rapid Uptake

In 2025, Machine Learning led the market with a 33.56% share, driven by its use in ingredient interaction mapping, demand forecasting, and process optimization. Its compatibility with structured data and proven effectiveness in complex formulations have accelerated adoption. Machine learning remains the foundational predictive layer in the market.

Natural Language Processing is forecast to grow at a 14.67% CAGR from 2026 to 2031, emerging as the fastest-growing technology. NLP enables the conversion of product briefs into research summaries, formulation drafts, and compliance documentation, addressing bottlenecks in product development. It complements machine learning and regulatory databases, streamlining complex scientific processes and enhancing efficiency.

By Deployment Mode: Cloud Dominance Reflects Scalability and Regulatory Database Integration

In 2026, Cloud-Based deployment held 66.15% of the market and is projected to grow at a 13.78% CAGR from 2026 to 2031. Cloud systems support shared regulatory databases, ingredient libraries, and collaboration tools, making them ideal for global operations. Cloud-native environments integrate generative AI, validation modules, and digital twin tools, streamlining the transition from concept to scale-up while maintaining regulatory compliance.

By End User: Nutraceutical Manufacturers Drive Volume, Functional Food Innovators Accelerate

In 2025, Nutraceutical Product Manufacturers accounted for 44.34% of the market, driven by use cases like ingredient screening, dose optimization, and claims documentation. These manufacturers integrate AI into R&D and technical services, enhancing operational efficiency and fostering partnerships with AI-capable contract manufacturers.

Functional Food Innovators are projected to grow at a 13.88% CAGR from 2026 to 2031, making them the fastest-growing end-user segment. They leverage AI for sensory engineering, rapid variant development, and benefit validation, enabling quick responses to consumer trends in areas like metabolic health and cognitive support.

Geography Analysis

In 2025, North America accounted for 38.77% of the AI in nutraceutical formulation market, maintaining its leadership by revenue. This dominance is driven by significant R&D investments, a mature digital health ecosystem, and a consumer base favoring personalized nutrition. The FDA's draft guidance on AI for regulatory decision-making emphasizes credibility, traceability, and oversight, further shaping the region's market dynamics. These factors position North America as a hub for platform innovation, premium product launches, and biomarker-driven formulations.

Asia-Pacific is projected to grow at a CAGR of 14.45% from 2026 to 2031, making it the fastest-growing regional market. The region's growth is fueled by a shift toward precision nutrition, cloud-based product development, and rapid digital adoption across industries. Its large, diverse consumer base and preference for modular AI tools over heavy in-house systems create opportunities for personalization and quick concept testing.

Europe, the second-largest market, faces unique growth challenges due to strict regulations like EFSA's health claim framework, GDPR, and the EU AI Act. These regulations drive investments in auditability and governance, creating short-term hurdles but enhancing long-term credibility for compliant companies. South America, though in an early stage, shows potential as local players explore AI-driven nutraceutical designs leveraging regional biodiversity and faster workflows. Globally, the market's performance depends on regulatory readiness, digital infrastructure, and the ability to implement personalized nutrition effectively.

Competitive Landscape

The AI-driven nutraceutical formulation market is moderately fragmented, with leadership distributed among AI-focused bioactive discovery firms, formulation software providers, personalized supplement platforms, and established nutrition companies. Differentiation is driven by data access, algorithm quality, clinical validation, and distribution networks. Brightseed and Nuritas lead in AI-driven discovery, while platform players like Formulaite focus on workflow efficiency and simulation capabilities. Personalized nutrition specialists such as Bioniq and Viome leverage biomarker datasets, while larger firms like dsm-firmenich, Symrise, and Herbalife integrate AI into broader R&D and commercialization systems.

Vertical integration is a key trend, with companies combining formulation algorithms, biological datasets, regulatory insights, and distribution to accelerate product launches and improve customer retention. Biomarker-driven personalization platforms attract larger nutrition firms with established scale. Clinically focused enterprise platforms are also gaining traction, emphasizing recurring data and software revenues. Cloud-native strategies enable platform providers to serve multiple partners through subscription models and updated scientific libraries.

Proprietary biological and formulation data is a critical asset. Companies with extensive biomarker repositories or ingredient-response datasets gain a competitive edge in training models and improving personalization accuracy. Infrastructure providers that streamline product design, validation, and documentation also hold strong positions. Competition is expanding into areas like digital twins, PBPK simulation, and scientific co-pilot tools, broadening the market beyond ingredient discovery. While competition intensifies, specialization remains key as different customer groups prioritize distinct capabilities. Consolidation is expected as platform providers, biomarker data owners, and nutrition firms combine strengths to gain a competitive edge.

AI In Nutraceutical Formulation Industry Leaders

Ai Palette

NIQ BASES AI Product Developer

NutrifyGenie

Viome Life Sciences Inc.

Nuritas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Brightseed introduced its clinically validated enterprise AI platform for health sciences. Built on the Forager™ discovery engine, trained on over 11 million natural compounds across 23 health territories, the company transitioned to a Data-as-a-Service subscription model, serving over 40 partners in nutrition, pharmaceuticals, and personal care.

- April 2025: Nourish raised USD 70 million in Series B funding led by J.P. Morgan Private Capital, bringing total funding to USD 115 million. The investment supports the expansion of its AI-powered personalized nutrition platform, catering to hundreds of thousands of patients across all 50 US states.

Global AI In Nutraceutical Formulation Market Report Scope

As per the scope of the report, AI in nutraceutical formulation refers to the use of artificial intelligence and machine learning algorithms to design, optimize, and test dietary supplements and functional foods. It replaces traditional, time-consuming trial-and-error methods by predicting ingredient interactions, stability, bioavailability, and health benefits in silico before physical laboratory testing.

The AI in nutraceutical formulation market is segmented by product type, application, technology, deployment mode, and end-user. By product type, the market includes dietary supplements, vitamins and minerals, botanicals and herbals, probiotics, prebiotics, and synbiotics, sports nutrition, specialty condition-specific formulas, functional foods, fortified beverages, nutrition bars and snacks, functional dairy and dairy alternatives, and powdered nutrition mixes. By application, the market is segmented into ingredient selection and optimization, product formulation, personalized nutrition, quality control and safety assurance, and supply chain optimization. By technology, the market is categorized into machine learning, predictive analytics, natural language processing, computer vision, knowledge graphs, generative AI and large language models, and digital twins and mechanistic simulation. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By end-user, the market is segmented into nutraceutical product manufacturers, functional food innovators, personalized nutrition platforms, R&D labs and contract formulators, ingredient suppliers, and healthcare and wellness platforms. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Dietary Supplements | Vitamins and Minerals |

| Botanicals and Herbals | |

| Probiotics, Prebiotics, and Synbiotics | |

| Sports Nutrition | |

| Specialty Condition-Specific Formulas | |

| Functional Foods | Fortified Beverages |

| Nutrition Bars and Snacks | |

| Functional Dairy and Dairy Alternatives | |

| Powdered Nutrition Mixes |

| Ingredient Selection and Optimization |

| Product Formulation |

| Personalized Nutrition |

| Quality Control and Safety Assurance |

| Supply Chain Optimization |

| Machine Learning |

| Predictive Analytics |

| Natural Language Processing |

| Computer Vision |

| Knowledge Graphs |

| Generative AI and Large Language Models |

| Digital Twins and Mechanistic Simulation |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Nutraceutical Product Manufacturers |

| Functional Food Innovators |

| Personalized Nutrition Platforms |

| R&D Labs and Contract Formulators |

| Ingredient Suppliers |

| Healthcare and Wellness Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Dietary Supplements | Vitamins and Minerals |

| Botanicals and Herbals | ||

| Probiotics, Prebiotics, and Synbiotics | ||

| Sports Nutrition | ||

| Specialty Condition-Specific Formulas | ||

| Functional Foods | Fortified Beverages | |

| Nutrition Bars and Snacks | ||

| Functional Dairy and Dairy Alternatives | ||

| Powdered Nutrition Mixes | ||

| By Application | Ingredient Selection and Optimization | |

| Product Formulation | ||

| Personalized Nutrition | ||

| Quality Control and Safety Assurance | ||

| Supply Chain Optimization | ||

| By Technology | Machine Learning | |

| Predictive Analytics | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Knowledge Graphs | ||

| Generative AI and Large Language Models | ||

| Digital Twins and Mechanistic Simulation | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Nutraceutical Product Manufacturers | |

| Functional Food Innovators | ||

| Personalized Nutrition Platforms | ||

| R&D Labs and Contract Formulators | ||

| Ingredient Suppliers | ||

| Healthcare and Wellness Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in nutraceutical formulation?

Growth is being supported by the shift from trial-and-error product development to data-led formulation workflows, with the market moving from USD 1.49 billion in 2026 to USD 2.78 billion by 2031 at a 13.25% CAGR.

Which product segment currently leads revenue?

Dietary Supplements led with 57.78% share in 2025 because this category has the highest volume of reformulation, claims support, and ingredient optimization activity.

Which application area is growing the fastest?

Personalized Nutrition is the fastest-growing application, with a 14.76% CAGR from 2026 to 2031, supported by biomarker, wearable, and multi-omics integration.

Why is cloud deployment dominant in this space?

Cloud-Based deployment holds 66.15% of the market in 2026 because it supports scalability, shared regulatory databases, and easier integration with laboratory and wearable data streams.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at 14.45% CAGR from 2026 to 2031, making it the fastest-growing geography in the study period.

What is the main challenge slowing adoption?

Data privacy requirements, workflow integration costs, and fragmented ingredient master data remain the main barriers, especially for smaller manufacturers and multi-country platforms.

Page last updated on: