AI In Personalized Nutrition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

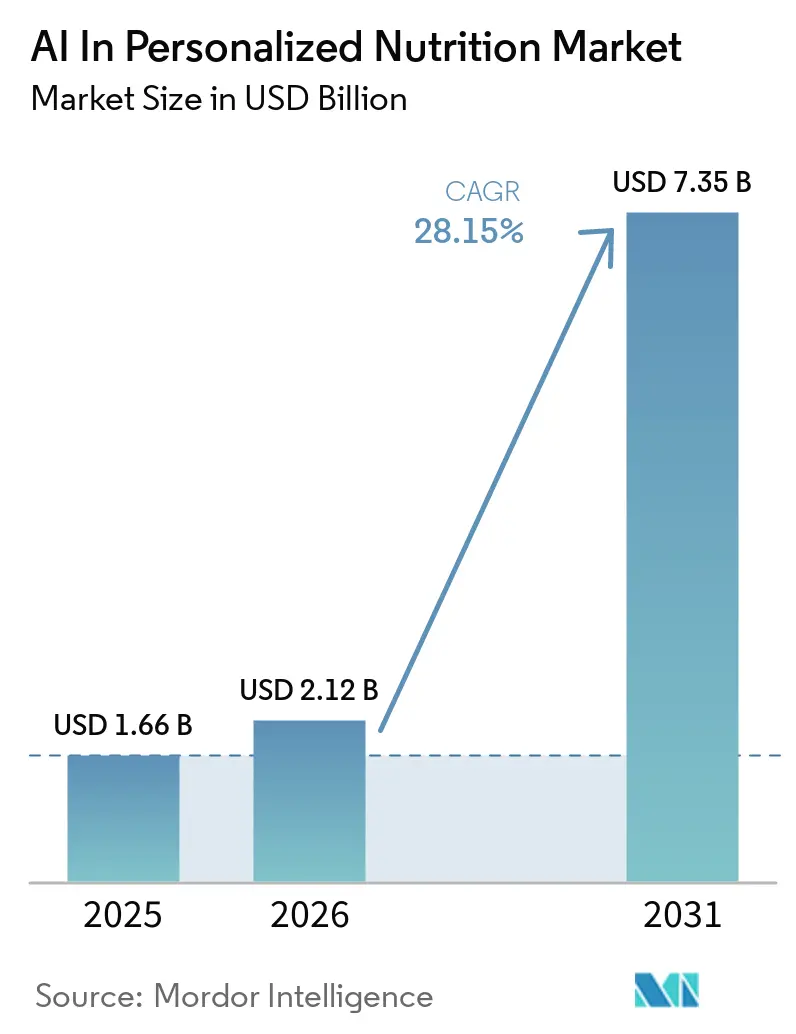

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 7.35 Billion |

| Growth Rate (2026 - 2031) | 28.15% CAGR |

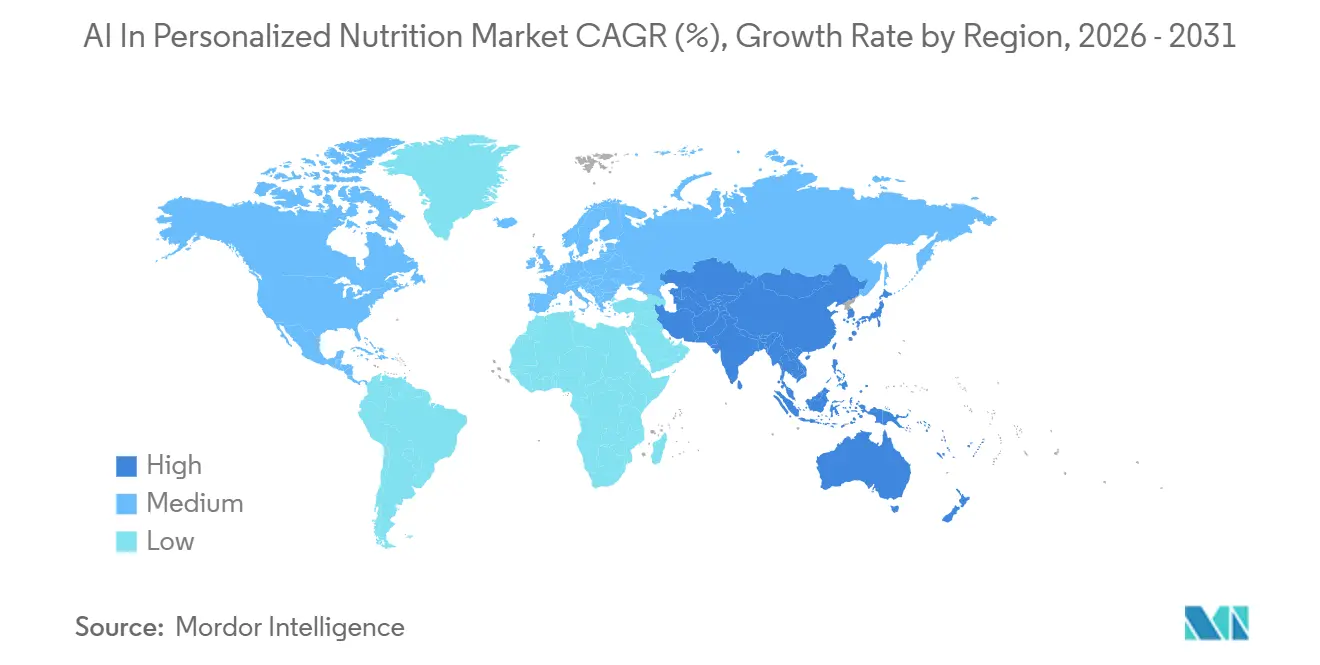

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Personalized Nutrition Market Analysis by Mordor Intelligence

The AI In Personalized Nutrition Market size is expected to increase from USD 1.66 billion in 2025 to USD 2.12 billion in 2026 and reach USD 7.35 billion by 2031, growing at a CAGR of 28.15% over 2026-2031.

Commercial momentum rests on the convergence of multimodal biological data streams and large-language-model reasoning engines that transform raw glucose curves, microbiome signatures, genomic variants, and wearable biometrics into self-updating dietary roadmaps. Venture funding has migrated from wellness point solutions toward clinically integrated platforms, while public-health agencies now promote food-as-medicine programs that reimburse precision meal guidance for diabetes and obesity.

Key Report Takeaways

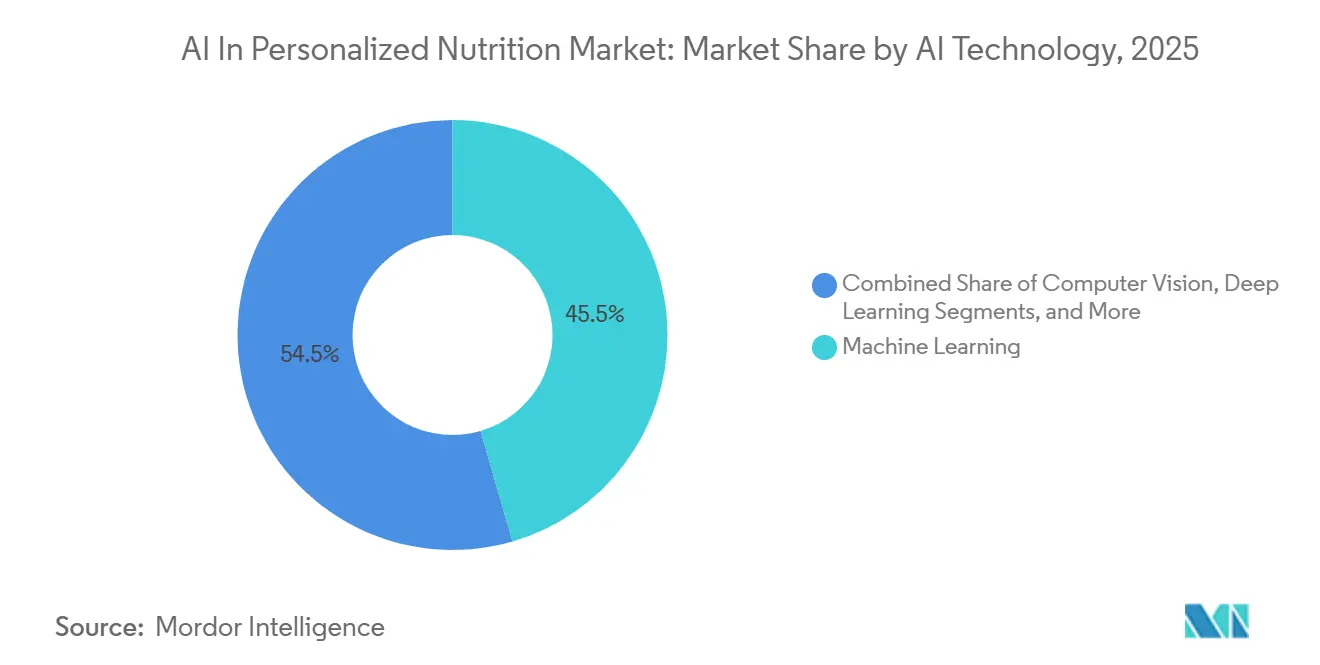

- By AI technology, machine learning led with 45.50% of AI in personalized nutrition market share in 2025, while computer vision is projected to grow at a 29.00% CAGR through 2031.

- By application, meal planning and recommendations accounted for 41.35% of the AI in the personalized nutrition market size in 2025, whereas personalized supplement recommendations are expected to grow at a 29.45% CAGR to 2031.

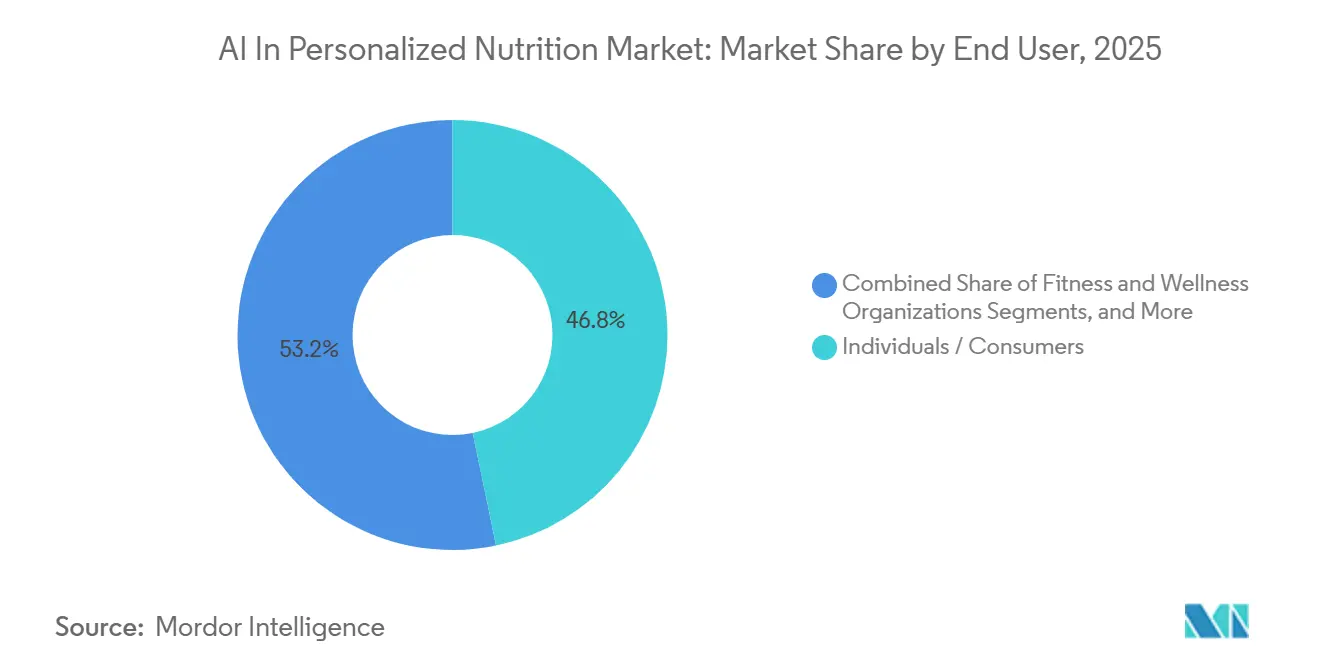

- By end user, individuals held 46.76% of 2025 revenue, whereas healthcare providers were expected to be the fastest-growing cohort at a 28.75% CAGR through 2031.

- By delivery model, mobile apps and cloud-based platforms controlled 61.2% of 2025 revenue, yet wearable-device-integrated platforms are expected to rise at a 28.98% CAGR over 2026-2031.

- By geography, North America controlled 41.50% of 2025 revenue, yet Asia-Pacific is expected to rise at a 29.25% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Personalized Nutrition Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising chronic-disease and metabolic-health burden | +6.5% | Global | Long term (≥ 4 years) |

| Expansion of wearables, CGMs, and at-home testing | +4.2% | North America & Europe, spill-over to APAC | Medium term (2-4 years) |

| Consumer shift toward preventive personalized wellness | +3.8% | North America, Europe, APAC core | Long term (≥ 4 years) |

| AI advances in multimodal nutrition data fusion | +3.5% | Global | Medium term (2-4 years) |

| GLP-1 nutrition support and lean-mass preservation | +3.1% | North America, early gains in UK & Australia | Short term (≤ 2 years) |

| Payor and employer food-as-medicine pilots | +2.3% | North America, emerging in Germany and the GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic-Disease and Metabolic-Health Burden

Non-communicable diseases account for 71% of global deaths and create an annual economic burden of USD 1.3 trillion. Population-level dietary guidelines often fail to address individual variations in post-meal glucose responses.[1]Guy Lutsker et al., “A Foundation Model for Continuous Glucose Monitoring Data,” Nature, nature.com However, AI models using data on glucose levels, sleep, activity, and gut microbiomes now provide personalized meal recommendations to stabilize blood sugar. A 2026 study demonstrated that the GluFormer foundation model, trained on 10 million glucose readings, predicted cardiovascular mortality more effectively than HbA1c, identifying 69% of events in the highest risk quartile. Integrated into consumer apps, these predictive tools elevate precision nutrition from lifestyle advice to reimbursable clinical services. Healthcare systems managing GLP-1 drug budgets are aligning dietary guidance with pharmacotherapy adherence, driving demand for AI-driven personalization in chronic disease management.

GLP-1 Nutrition Support and Lean-Mass Preservation Demand

By late 2025, one in eight U.S. adults was using GLP-1 therapy, doubling in 18 months. Medical guidelines recommend 80–120 g of daily protein intake for GLP-1 users to prevent lean-mass loss, but automation of this requirement remains limited.[2]Anand K. Gavai, “AI-Driven Personalized Nutrition for Metabolic Care,” HSOA Journal of Food Science and Nutrition, heraldopenaccess.us AI-powered meal planning tools can identify protein-rich options, adjust micronutrient goals, and suggest strength-training exercises based on wearable activity data. Employer insurance plans increasingly pair dietitian-supervised AI tools with GLP-1 prescriptions, as claims data shows a 23% reduction in diet-related expenses when precision nutrition complements drug therapy. Early data indicate that users combining GLP-1s with AI-driven dietitian services achieve 33% more weight loss and fewer side effects, presenting a strong ROI case for enterprises.

Expansion of Wearables, CGMs, and At-Home Biomarker Testing

Dexcom's Stelo over-the-counter CGM launched at USD 99 for 30 days, enabling non-diabetics to monitor glucose levels without prescriptions. In December 2024, Dexcom introduced a generative-AI feature for meal recognition and glycemic impact prediction, which was integrated across its product line by mid-2025.[3]Dexcom, “Dexcom Launches the First Generative AI Platform in Glucose Biosensing,” dexcom.com Oura Ring incorporated Dexcom's glucose data in May 2025, creating a unified biometric graph combining heart rate variability, sleep, activity, and glucose levels for nutrition-focused AI platforms. Research demonstrated that an SMS-based AI program using CGM data improved glycemic control by 18% in rural pre-diabetic adults, even in areas with limited smartphone access. These interconnected devices generate rich data, enhancing prediction accuracy and user engagement for AI-driven dietary platforms.

Payor and Employer Food-as-Medicine Pilots

In 2025, precision nutrition shifted from direct-to-consumer apps to managed-care contracts. A claims analysis across multiple employers found employees using precision nutrition digital therapy saved an average of USD 3,012 annually, reflecting a 23% reduction in diet-related medical costs. Blue Cross NC’s "Feed Your Health" initiative reported USD 227 monthly savings in Medicare Advantage costs and a 1.5-point HbA1c reduction within six months. In April 2026, January AI gained nationwide visibility by joining the CMS Medicare App Library, meeting federal privacy and interoperability standards. Early corporate programs demonstrate a data-flywheel effect, where food and biomarker data collected in employer pilots become proprietary assets for model training, strengthening the competitive edge of early platform leaders.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy and compliance complexity | -2.1% | Global, most acute in North America & EU | Short term (≤ 2 years) |

| Limited clinical validation and explainability | -1.6% | Global | Medium term (2-4 years) |

| Western-food dataset bias | -1.2% | APAC, MEA, South America | Long term (≥ 4 years) |

| Fragmented data rights across ecosystems | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Compliance Complexity for Genomic and Biometric Data

Effective April 2025, U.S. restrictions will prohibit the export of bulk genomic data involving anonymized sequences of over 100 individuals to specific countries of concern. Indiana’s HB 1521 and Montana’s SB 163 require explicit consent and deletion rights for genetic data, complicating DNA-based onboarding processes. The EU Artificial Intelligence Act categorizes nutrition advice based on sensitive biometric data as high-risk, necessitating mandatory compliance assessments. These overlapping regulations demand jurisdiction-specific data storage, increasing costs for multinational operations. Smaller vendors face challenges in building the necessary legal frameworks, giving larger, well-funded platforms a competitive edge.

Western-Food Dataset Bias Limiting Accuracy Across Cuisines

Commercial food-image libraries and nutrition databases are primarily designed around North American and Northern European diets. This bias results in misclassification of regional dishes like jollof rice and idli, and underrepresentation of spice blends that impact glycemic loads. Analysts in China report higher error rates in recommendation engines when analyzing menus from lower-tier cities due to culturally unique ingredients being excluded from training datasets. Additionally, local data protection laws complicate model retraining. A study on sustainability-focused menu planning highlighted strong compliance for Western recipes but significant gaps for Asian staples, emphasizing the need for improved cultural adaptability. Without diversified datasets, user trust in regions like APAC and MEA may decline, limiting growth in these high-potential markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By AI Technology: Machine Learning Anchors Revenue While Computer Vision Accelerates

In 2025, machine learning captured 45.50% of the AI-driven personalized nutrition market. Its success stems from the effectiveness of gradient-boosted trees and ensemble forests in predicting glycemic responses from limited lab and lifestyle data. Clinical deployments prioritize SHAP value explanations, which simplify feature weights into actionable nutrition goals for patients. By 2026, model compression advancements reduced inference latency to under 300 milliseconds on smartphones, enabling apps to deliver meal scores instantly. Platform strategies now focus on federated-learning updates, ensuring genomic data remains on-device while syncing only model gradients to the cloud. This approach addresses privacy concerns and enhances sample diversity.

Computer vision is projected to achieve a 29.00% CAGR through 2031, driven by global smartphone penetration exceeding 6.8 billion active devices. January AI’s extensive food ontology demonstrates the scalability of image recognition, maintaining high recall rates even for low-frequency ethnic dishes.

By Application: Meal Planning Leads While Supplement Recommendations Drive Growth

In 2025, meal planning and recommendation engines accounted for 41.35% of the revenue. This growth was supported by low biological-testing thresholds and viral sharing loops that transformed user-generated recipe libraries into effective marketing tools. Engagement rates exceeded 40% when push notifications aligned with CGM-flagged glucose spikes, sustaining user retention beyond the typical 90-day churn period. Collaborations with national grocers enhanced the appeal by offering shoppable meal plans with same-day ingredient delivery, creating a self-sustaining e-commerce model supporting freemium tiers.

Personalized supplement recommendations are expected to grow at a 29.45% CAGR through 2031, driven by declining costs of RNA, microbiome, and blood-spot assays, now below USD 150 per kit. Viome’s multi-omic SKU customizes probiotic, prebiotic, and vitamin packs based on individual inflammatory markers and provides bulk-capsule manufacturing as a private-label service for other apps.

By End User: Consumers Dominate While Healthcare Providers Accelerate

In 2025, individual consumers accounted for 46.76% of spending, driven by direct-to-consumer subscriptions and in-app upgrades. Surveys indicate over 60% of active supplement users trust AI-driven guidance, providing platforms with a strong base to promote advanced tests. Digital natives aged 25-44 are the most valuable demographic, spending USD 22 monthly on app premiums for enhanced macronutrient tracking.

Healthcare providers are projected to grow at a 28.75% CAGR through 2031, supported by the integration of algorithmic risk scores into reimbursable CPT codes. Registered dietitians use technology to auto-draft encounter notes, enabling clinicians to focus on motivational interviewing while ensuring billing compliance.

By Delivery & Deployment Model: Mobile Apps Lead as Wearable Integration Reshapes Value Chains

In 2025, mobile apps and cloud hubs dominated, accounting for 61.2% of revenue. Smartphones consolidate diverse data streams, including food logs, CGM feeds, sleep patterns, HRV, and lab panels, into unified decision dashboards. Japan’s Asken, with 13 million members and 10 billion logged meals, highlights the scalability of consumer engagement and model training for personalized insights. Cloud-based microservices offer meal-scoring APIs that third parties integrate into grocery and pharmacy apps, spreading R&D costs across broader GMV.

Wearable-integrated platforms are expected to grow at a 28.98% CAGR, driven by a post-pandemic shift in consumer perception, viewing biosensor subscriptions as essential health investments. The Oura-Dexcom partnership integrates continuous glucose, heart rate, and sleep data into a single vector, enabling recommendation engines to identify optimal insulin-sensitivity windows during peak carbohydrate tolerance.

Geography Analysis

In 2025, North America commanded a dominant 41.50% share of the AI-driven personalized nutrition market. This growth is attributed to the region's strong venture ecosystem, widespread adoption of over-the-counter continuous glucose monitors (CGMs), and a mature reimbursement framework treating food as medicine. January AI's inclusion in the CMS Medicare App Library in April 2026 allows millions of Medicare beneficiaries to access an approved app for glucose prediction and meal coaching, highlighting federal recognition of AI in healthcare. U.S. employers are scaling precision-nutrition initiatives, with a claims analysis from 48 self-insured firms showing an annual saving of USD 3,012 per member when digital nutrition therapies complement standard care. This has drawn board-level attention, accelerating procurement cycles.

Asia-Pacific is poised to be the fastest-growing region, with a projected 29.25% CAGR from 2026 to 2031, driven by domestic tech giants entering chronic disease management. In 2025, China's Meinian Health reported AI-related revenues of CNY 370 million (approximately USD 51 million), with plans to expand precision nutrition. Major players like Ant Group, Tencent, and ByteDance are integrating diet-scoring features into super-apps, leveraging social interactions to gather biometric data at scale. Japan's Asken maintains strong user engagement, while Singapore's Health Promotion Board is piloting CGM-subsidized meal vouchers, indicating that public policies can enhance private-sector efforts. South America and the GCC, though in early stages, offer potential for metabolic health interventions due to high obesity rates. However, fragmented data rights and limited lab networks may hinder short-term adoption.

Competitive Landscape

In 2026, the AI-driven personalized nutrition landscape remains splintered, with over 20 niche players carving out spaces based on biological data. At CES 2026, Abbott leveraged its 7 million FreeStyle Libre user base to introduce Libre Assist, integrating generative meal guidance into its CGM companion app. Similarly, Dexcom employs an embedded-software approach, transforming its hardware advantage into a safeguard against revenue risks as sensor commoditization approaches. On the software side, ZOE invested in Ziggie, an LLM-powered nutrition coach utilizing insights from its 300,000-sample gut-microbiome biobank. January AI repurposed its 54-million-item food ontology into enterprise APIs, signaling a shift toward backend support for health-system partnerships.

Three primary gaps present white-space opportunities: the need for culturally tailored recipe databases, B2B solutions to integrate nutrition logic into external applications, and structured guidance for GLP-1 users focused on maintaining lean mass. Brightseed’s Forager AI highlights the value of upstream ingredient discovery, identifying 530 previously unknown almond phytochemicals and positioning the company to license bioactive datasets to consumer platforms. Intellectual-property filings are increasing, with Viome securing patents for RNA-driven food and supplement recommendations, and ZOE expanding claims on gut-microbiome risk assessments. This indicates that legal protections, alongside data scale, are becoming critical competitive advantages. In capital markets, platforms with peer-reviewed data command higher contract values, emphasizing the importance of clinical validation over feature parity.

AI In Personalized Nutrition Industry Leaders

Abbott Laboratories

FoodMarble

InsideTracker

Persona Nutrition

January AI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: January AI became one of the first third-party apps accepted into the CMS Medicare App Library, signaling regulatory acceptance of AI-driven dietary guidance in U.S. federal healthcare.

- March 2026: ZOE launched ZOE 2.0, adding the Ziggie AI coach, photologging upgrades, and a processed-food risk scale while eliminating mandatory gut testing at entry level.

- January 2026: January AI released an enterprise Lifestyle Intelligence platform offering APIs for image-based food recognition and virtual glucose prediction, enabling health systems to embed nutrition logic into existing apps.

- January 2026: Abbott debuted Libre Assist, a generative-AI meal-guidance feature embedded in its Libre app, extending algorithmic nutrition to more than 7 million global CGM users at no added cost.

Global AI In Personalized Nutrition Market Report Scope

As per the scope of the report, AI in personalized nutrition is the application of artificial intelligence, specifically machine learning and data analytics, to analyze an individual's genetic, metabolic, behavioral, and lifestyle data to provide tailored, real-time dietary recommendations. It optimizes health by creating unique, data-driven eating plans, moving beyond traditional, one-size-fits-all guidelines.

The AI in personalized nutrition market is segmented by AI technology, application, end-user, delivery & deployment model, and geography. By AI technology, the market includes machine learning, deep learning, natural language processing, and computer vision. By application, the market is segmented into meal planning & recommendations, nutrient & micronutrient analysis, personalized supplement recommendations, allergen & food sensitivity identification, and health & metabolic monitoring. By end-user, the market is segmented into individuals/consumers, fitness & wellness organizations, healthcare providers, and employers & enterprises. By delivery & deployment model, the market is segmented into mobile apps & cloud-based platforms, on-premise/private-cloud enterprise deployments, wearable device-integrated platforms, and hybrid app + dietitian/coach models. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Meal Planning & Recommendations |

| Nutrient & Micronutrient Analysis |

| Personalized Supplement Recommendations |

| Allergen & Food Sensitivity Identification |

| Health & Metabolic Monitoring |

| Individuals / Consumers |

| Fitness & Wellness Organizations |

| Healthcare Providers |

| Employers & Enterprises |

| Mobile Apps & Cloud-Based Platforms |

| On-Premise / Private-Cloud Enterprise Deployments |

| Wearable Device-Integrated Platforms |

| Hybrid App + Dietitian / Coach Models |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By AI Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| By Application | Meal Planning & Recommendations | |

| Nutrient & Micronutrient Analysis | ||

| Personalized Supplement Recommendations | ||

| Allergen & Food Sensitivity Identification | ||

| Health & Metabolic Monitoring | ||

| By End User | Individuals / Consumers | |

| Fitness & Wellness Organizations | ||

| Healthcare Providers | ||

| Employers & Enterprises | ||

| By Delivery & Deployment Model | Mobile Apps & Cloud-Based Platforms | |

| On-Premise / Private-Cloud Enterprise Deployments | ||

| Wearable Device-Integrated Platforms | ||

| Hybrid App + Dietitian / Coach Models | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which application is growing fastest within personalized nutrition platforms?

Personalized supplement recommendations are forecast to expand at a 29.45% CAGR through 2031 as multi-omic testing costs continue to fall.

Why is Asia-Pacific expected to outpace other regions?

China's tech giants, rising chronic-disease prevalence, and policy support for digital health drive a 29.25% CAGR in Asia-Pacific, making it the fastest-growing region.

What role do GLP-1 medications play in market growth?

Widespread GLP-1 adoption creates demand for AI-guided protein-rich meal plans that safeguard lean mass, encouraging employers and payors to bundle nutrition platforms with drug therapy.

How are wearable devices influencing platform adoption?

Low-cost CGMs and multisensor wearables stream continuous metabolic data that improves algorithm accuracy and enriches user engagement, accelerating the shift toward wearable-integrated deployments.

What is the primary regulatory hurdle for vendors?

Data-privacy statutes governing genomic and biometric information, especially U.S. bulk-data export rules and the EU Artificial Intelligence Act, impose the strictest compliance requirements on vendors.

Page last updated on: